An emergency helicopter flight, life-saving surgeries and a health insurer that said it wasn’t medically necessary.

When Pamela Talley came home from an Arizona cycling vacation with a surgically repaired broken left wrist and elbow, she knew – as a retired family physician – that she’d be facing a tough recovery.

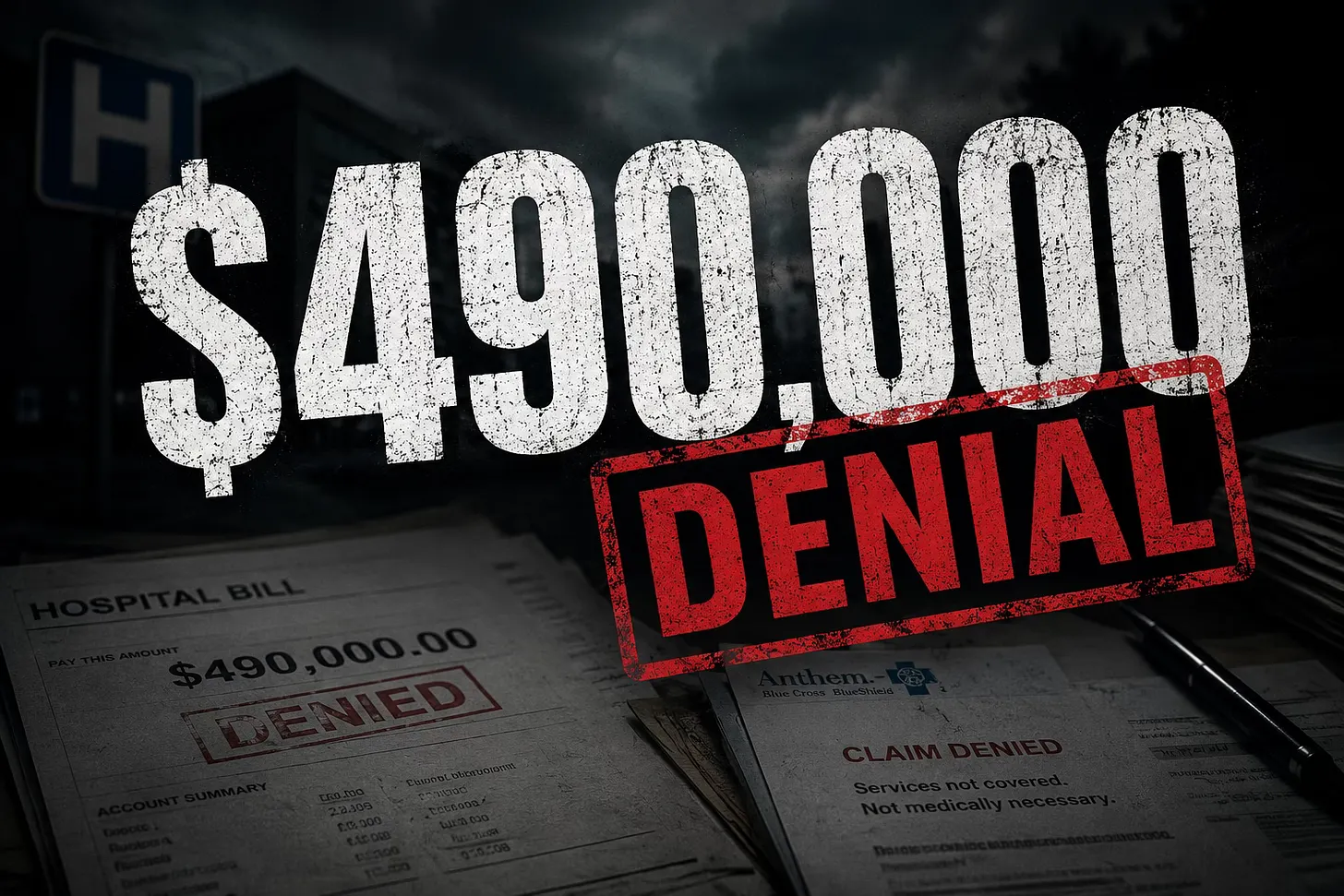

What the 62-year-old Colorado retiree wasn’t expecting was the letter she received not long after she got home last year from her health insurer, Anthem Blue Cross and Blue Shield. It informed Talley that her hospitalization in Tucson – where they’d helicoptered her after the nasty gravel spill which left part of her broken wrist protruding through her skin – was “medically unnecessary,” and the two emergency surgeries were not covered by her policy, either.

It said that she would be responsible for the medical costs that Anthem — which is part of the giant for-profit insurance conglomerate called Elevance Health — would not cover: $490,000.

“I’m still on narcotics,” Talley recalled of that moment. “I’m three days post-op. I’m in pain. I’m in a pretty vulnerable position. But my initial reaction – honestly, I think – as a physician was, ‘This is preposterous. I’m going to be able to resolve this with a telephone call.’”

Talley was not able to resolve this with a telephone call. Instead, the letter was just the beginning of an ordeal that lasted for 13 months and involved many two-hour phone calls, often waiting on hold, contradictory statements and explanations, and finally a plea for state regulators to help convince her insurer to pay.

The enormous dollar figure makes Talley’s battle somewhat unique, but receiving an insurance company denial letter is an experience that is painfully familiar to millions of Americans – and the problem is only getting worse. Exact numbers are hard to come by, but one 2023 study of patients covered in the Affordable Care Act (ACA) Marketplace found insurers initially denied 20% of claims.

Studies have also shown that it’s highly possible that patients who appeal these rejections can get them overturned, and yet very few – as few as 1%, it’s been reported – actually do fight back against rejections. Talley’s case arguably is a window into why, and why insurers count on this lack of appeals as they post record profits every year. Studies have shown that the cost of coverage denials falls hardest on lower-income Americans who lack the time and resources to fight back.

If a doctor like Talley with a lifetime of health care experience had to fight for more than a year for a fair resolution, what chance do the rest of us have?

Talley retired early from her second career in public health to move back to Colorado, where she had planted some roots and could better indulge her passion for the great outdoors. It was that hobby that took her with her two adult sons on the bicycle tour on scenic gravel trails in Arizona, near the border with Mexico.

On the second day of that excursion, Talley was moving quickly downhill on what the guides called a difficult “technical stretch,” and was clipped into her bicycle, when she fell – hard. As she lay on the gravel, she looked at her left arm, which she’d used to break the fall. Her wrist was clearly broken – a part of the bone was protruding through the skin – and it appeared her elbow was broken as well.

Between the pain and the remote site of the accident, Talley’s insurance coverage wasn’t on the top of her mind as the tour van trailing the cyclers picked her up and began the arduous task of getting her the urgent medical care she needed. It took two hours just to get to an emergency clinic near the border, where she was sedated, X-rayed, had the wrist placed in a splint – and where it was decided she’d need to get to a Level 1 trauma center. The nearest one was in Tucson, which was five hours away by car or 45 minutes by medical helicopter.

Knowing the risks of delaying an operation, she chose the helicopter.

“It was clear I needed surgery,” she recalled. But getting to Tucson was only the first step. “They see me, then I sit on a gurney in the hall in the emergency department for about eight hours,” she recalled. And then, because they had no beds upstairs, I was ultimately put into the labor and delivery ward overnight because that’s where they had a bed.”

Finally, she underwent two separate surgeries with hand and elbow specialists over a period that lasted nearly a day, as well as a procedure to alleviate nerve pressure. Talley would spend a couple nights in the hospital, first to get intravenous antibiotics and for observation, and also until she could arrange a flight back to Denver.

“So the day after I got back to Denver, I got a notice from Anthem that my $490,000 hospitalization bill was denied as medically unnecessary,” Talley said.

Too young for Medicare when she retired, Talley had signed up for Anthem’s high-deductible health insurance plan in the Affordable Care Act Marketplace. She said she knew she’d be liable for the first $10,000 or so in annual medical expenses, and she was OK with that. But she said she never expected that the giant insurer would find a plethora of grounds for not covering her emergency – that out-of-state care wasn’t eligible, or that her surgeons were out-of-network, or that some of her treatment was excessive.

Talley waited a couple days until she felt better to call Anthem, and then waited two hours to speak with someone who contradicted himself on the call, first stating that the denied care wasn’t medically necessary and then saying that actually the issue was that it occurred in Arizona and not in Colorado.

“Preposterous,” she said. “Come on, this was an emergency. It’s not like I went to get a hip replacement at the Mayo Clinic, which is what my plan is trying to prevent.” The Anthem representative promised her case would be reviewed, but nothing happened for a couple of months.

As bills for Talley’s complicated care trickled in, she was befuddled to see which services were covered and which were not. For example, Anthem was paying the anesthesiologist for her operation, but not the surgeons.

By now, Talley was calling Anthem about every three weeks, typically spending a couple of hours on hold each time. “I would get to a person, this conversation would start and they would hang up on me. And it got to the point where I felt like, oh, there’s a pop-up that says, ‘Hang up on this person. She’s persistent.’”

Talley filed a formal appeal within the six-month time period, and – again, with significant delay – finally received the guidelines for this policy upon which she argued that all of her care should have been covered. When Anthem denied her appeals, she looked into hiring a lawyer when she learned from a family member that the Colorado Department of Insurance had helped resolve a disputed claim for a much smaller amount. Talley convinced the state agency to help intervene in her matter.

Her last-gasp plea for government intervention worked, as regulators reminded Anthem of relevant state and federal statutes – such as the 2022 No Surprises Bill – intended to ensure claims such as Talley’s are covered. Still, the bills were resolved in pieces, not one fell swoop. By this spring, Talley was down from the initial $490,000 to one final $135 radiology bill, yet she continued to contest it.

“I’m stubborn,” she said with a laugh, and ultimately Anthem paid that bill as well. It took 13 months, but Talley ultimately only paid the $10,000 under her deductible.

But the big picture, unfortunately, is that there are too many other cases like Talley’s out there, and the number is likely to rise. For one thing, artificial intelligence, or AI, is increasingly used by Big Insurance to review claims, and often deny them, in the most coldly calculating fashion.

But also, the refusal late last year by the Republican-led Congress to extend subsidies that allowed millions of Americans to afford their monthly ACA premiums has forced many families to seek inferior alternatives – including high-deductible plans such as Talley’s. These policies typically have more loopholes that insurers can invoke to deny claims – exactly what happened to Talley.

However, as Talley herself pointed out, the tiny minority of patients who appeal these denials are often successful, especially when they are persistent, or make use of every available resource. For example, one KFF survey of 2022 data found that appeals of insurance companies’ prior authorization rejections successfully overturned them more than 82% of the time.

She also advised patients to study their insurers’ guidelines ahead of time. “I had never read my contract in detail,” Talley said. “What’s covered, what’s not covered. I’d never had the reason to do that, but now I know.”

Today, recovered from her Arizona accident, Talley is looking forward to her next outdoorsy travel adventure, in Europe. This time, she said she won’t clip into her bicycle – and she’s also getting trip insurance. She said: “I don’t want to not do things that have some risk, you know?”