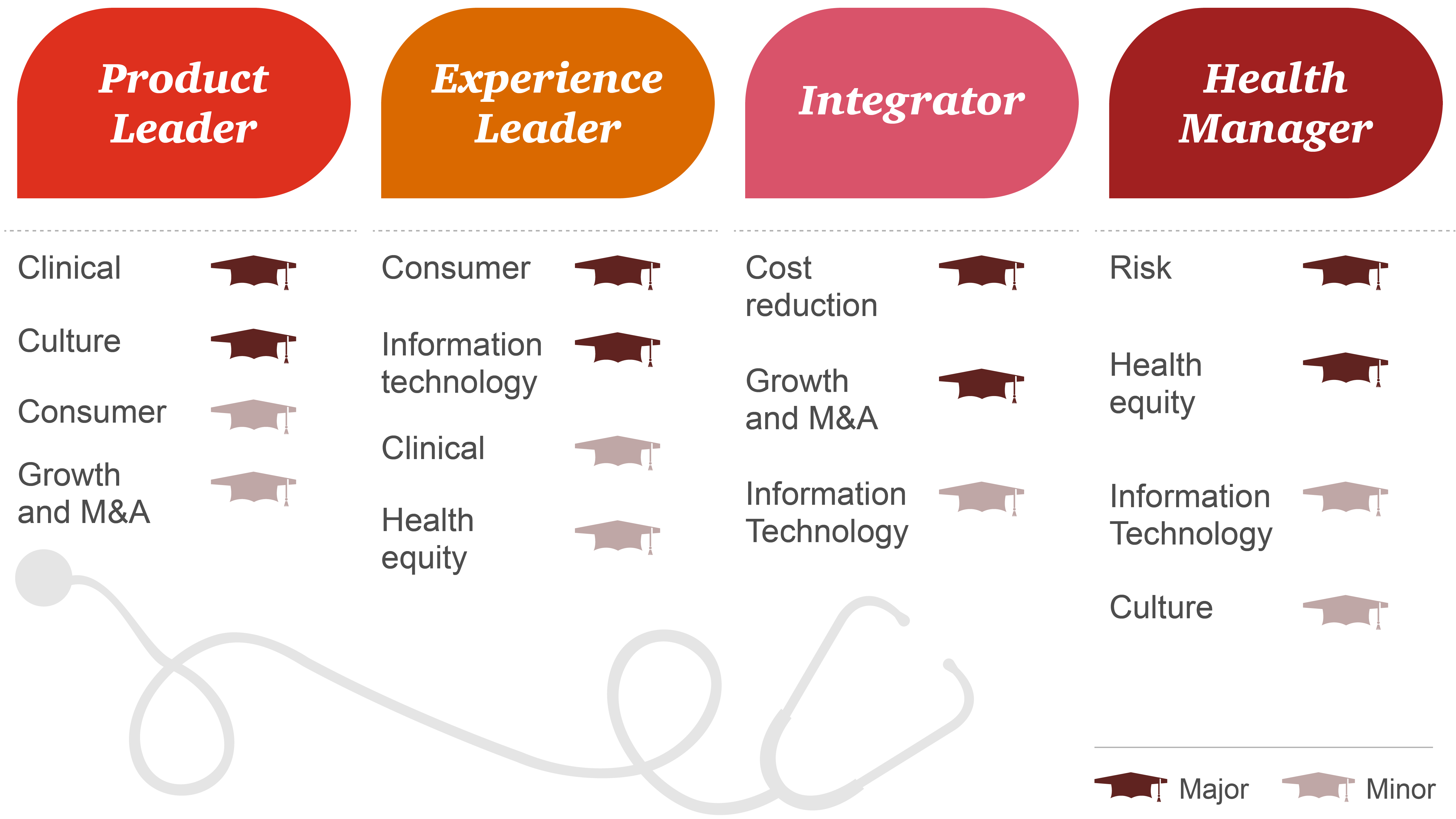

PwC’s Health Research Institute believes 2019 is the year the “New Health Economy” will finally become a reality.

The past year marked record interest in the healthcare industry, especially from outside forces like venture capitalists and business giants like Amazon, Berkshire Hathaway and JP Morgan Chase. PwC believes forces like these mean healthcare will no longer be an “outlier” industry that operates in its own world outside the greater U.S. economy.

In its 13th annual report, PwC’s HRI identified the following six healthcare trends to watch in 2019:

1. With an injection of $12.5 billion from investors over the past two years, PwC expects connected health devices and digital therapies to become integrated into care delivery and the regulatory process for drug and device approvals. PwC expects several new products to come to market in this category in 2019. What does this mean for providers? They will need to find a way to integrate this data into the EHR so it can be used to maximize the patient visit.

2. Artificial intelligence and automation will require healthcare organizations to invest in and train their workforce to succeed in a digital economy. Almost half (45 percent) of executives surveyed by PwC’s HRI said skill deficiencies among their workforce are holding their organization back, yet few employers are offering training in AI, robotics and automation or data analytics.

3. The 2017 Tax Cuts and Jobs Act will continue to create tax savings for healthcare organizations while creating new challenges. Providers are likely to feel the biggest challenges via changes to unrelated business taxable income, which could create new expenses. Academic medical centers may also feel minor negative pressure from the net investment excise tax on educational foundations.

4. The healthcare industry is ready for its own budget airline provider. It needs a disruptor that is low-cost, transparent, informed by technology and “laser-focused on the consumer” like Southwest Airlines, according to PwC. Organizations that answer this call are starting to emerge — like a profitable, Medicaid-focused, walk-in-only family medicine practice in Denver — but progress is slow and there isn’t one simple formula to follow. PwC advises healthcare organizations to look for patient segments that need a “budget airline” and determine how to meet those needs.

5. The pace of private equity investment is expected to accelerate as healthcare companies continue to divest noncore business units to investors next year. It also expects PE-healthcare partnerships to evolve, with some healthcare companies co-investing in their own spinoffs. PwC suggested healthcare organizations pursue PE partnerships not only for financing, but also for PE firms’ ability to provide strategic views of trends across their portfolio of investments.

6. Republican changes to the ACA will shift the law’s winners and losers. Providers are on the losing end of most of these changes, including softened insurance mandates, short-term health insurance plans, less federal support for ACA exchanges and reduced federal Medicaid spending, according to the report.

Download the report here.