http://www.kff.org/health-reform/issue-brief/whats-the-near-term-outlook-for-the-affordable-care-act/?utm_campaign=KFF-2017-August-Health-Reform-Outlook-ACA&utm_medium=email&_hsenc=p2ANqtz-_EbLjzmzMtjCe5gWysdKFOYAKOhLUxytBE9QiRYkFON8iXqISeYScKKovbN72gQpEReUlNwoqtEivO7NiGu6poWGxL1A&utm_content=54950542&utm_source=hs_email&hsCtaTracking=b35f36e5-60c0-4e14-ba27-3e14c4025b79%7Cf0a0cb87-2715-4168-b499-2000076067bf

If Congress abandons efforts to repeal and replace the Affordable Care Act (ACA), President Trump has said he would “let Obamacare fail.” This Q&A examines what could happen if the Affordable Care Act, also called “Obamacare,” remains the law and what it might mean to let Obamacare fail.

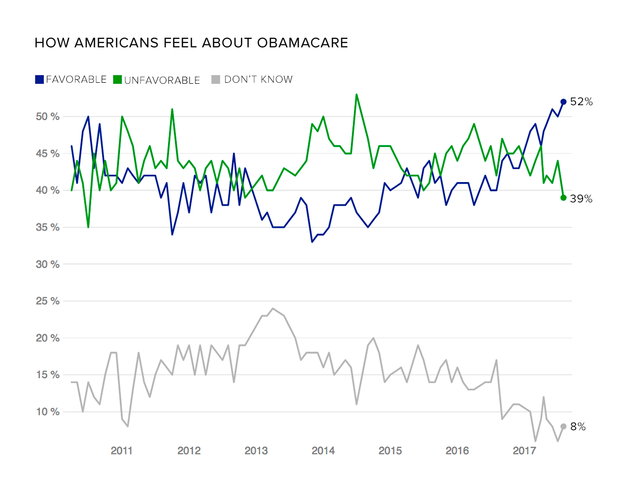

Is Obamacare failing?

The Affordable Care Act was a major piece of legislation that affects virtually all payers in the U.S. health system, including Medicaid, Medicare, employer-sponsored insurance, and coverage people buy on their own. One of the biggest changes under the health reform law was the expansion of the Medicaid program, which now covers nearly 75 million people, about 14 million of whom are signed up under the expansion. Most Americans, including most Republicans, believe the Medicaid program is working well.

When people talk about the idea of the ACA failing, they are usually referring to the exchange markets, also called Marketplaces. These markets, which first opened in 2014, are part of the broader individual insurance market where just 5-7% of the U.S. population gets their insurance. People who get insurance from other sources like their work or Medicaid are not directly affected by what happens in the individual insurance market.

The exchange markets have not been without problems: There have been some notable exits by insurance companies and premium increases going into 2017, and in the early years of the exchanges, insurers were losing money. The structure of the ACA’s premium subsidies – which rise along with premiums and cap what consumers have to pay for a benchmark plans a percentage of their income – prevents the market from deteriorating into a “death spiral.” However, premiums could become unaffordable in some parts of the country for people with incomes in excess of 400% of the poverty level, who are ineligible for premium assistance.

Insurer participation in this market has received a great deal of attention, as about 1 in 3 counties – primarily rural areas – have only one insurer on exchange. Rural counties have historically had limited competition even before the ACA, but data now available because of the Affordable Care Act brings the urban/rural divide into sharper focus. On average at the state level, competition in the individual market has been relatively stable – neither improving nor worsening.

Premiums in the reformed individual market started out relatively low and remained low in the first few years – about 12% lower than the Congressional Budget Office had projected as of 2016 –before increasing more rapidly in 2017. Most (83%) of the 12 million people buying their own coverage on the exchange receive subsidies and therefore are not as affected by the premium increases, but many of the approximately 9 million people buying off-exchange may have difficulty affording coverage, despite having higher incomes. As might be expected, after taking into account financial assistance and protections for people with pre-existing conditions, some people ended up paying more and others paying less than they did before the ACA. Our early polling in this market found that people in this market were nearly evenly split between paying more and paying less. About 3 millionpeople who remain uninsured are not eligible for assistance or employer coverage and many of them may be going without coverage due to costs.

Our recent analysis of first quarter 2017 insurer financial results finds that the market is not showing signs of collapse. Rather, insurers are on track to be profitable and the market appears to be stabilizing in the country overall. In other words, those premium increases going into 2017 may have been enough to make the market stable without discouraging too many healthy people from signing up. However, there are still markets – particularly rural ones – that are fragile.

How would administrative actions affect market stability?

Despite signs that the individual insurance market is generally stabilizing on its own, certain administrative actions could cause the market to destabilize again. Actions the Administration might take that would weaken the market include:

STOP ENFORCING OR WEAKEN THE INDIVIDUAL MANDATE

The individual mandate is the Obamacare requirement that most people either have insurance or pay a penalty. The purpose of it is to get young and healthy people into the market to bring down average costs. If there are not enough young and healthy people signing up, insurers have to raise premiums. If the administration signals it will either stop enforcement of the individual mandate or give broad exemptions, insurers will respond by raising premiums or exiting the market. The Congressional Budget Office (CBO) estimates that without the individual mandate, premiums in the individual insurance market could rise by 20%.

SCALE BACK OUTREACH AND CONSUMER ASSISTANCE

The individual market is often a transitional source of insurance when life circumstances change. People who are temporality unemployed, in school, or early retirees make up a substantial share of the individual market. Additionally, people in this market often experience income volatility and may cycle between Medicaid and subsidized exchange coverage. Those who are sick will be most likely to seek insurance coverage on their own when they go through a change in life circumstances, but outreach and consumer assistance programs – particularly those targeted at young and healthy individuals – can help balance out the risk pool and bring down average costs.

This coming open enrollment period (November 1 – December 15, 2017) is shorter than previous periods and may require more outreach to get people signed up before the deadline. This will also be the first enrollment period run from start to finish by the Trump administration and it is not yet clear how much outreach the administration will take on. Toward the end of the last open enrollment period, the Trump administration cut marketing and more recently has used outreach funds for messages critical of the health care law.

STOP MAKING COST-SHARING SUBSIDY PAYMENTS

Under the Affordable Care Act, insurers are required to offer low-deductible plans to low-income people (58% of marketplace enrollees benefit from these cost-sharing subsidies). For the lowest-income enrollees, these subsidies can bring down the deductible from a few thousand dollars to a couple hundred dollars (Figure 2 below). Providing these higher-value plans to low-income enrollees costs insurers more money (an estimated $10 billion dollars in 2018), so under the ACA the federal government reimburses insurers in the form of a cost-sharing subsidy payment. However, these payments are the subject of a lawsuit and the Administration has signaled they might stop making payments.

If these payments stop, we estimate that insurers would need to raise rates on silver-level plans – which are the only plans where consumers can access cost-sharing reductions – by 19 percent, with states that did not expand Medicaid (primarily red states) facing higher premium increases (Figure 3 below). Lower-income marketplace enrollees receiving premium subsidies would be protected from premium increases because subsidies would rise as well. However, higher-income enrollees not receiving premium subsidies would face higher premiums if insurers expect cost-sharing subsidy payments to end.

The combined effect of these policy changes (not enforcing the individual mandate and defunding cost-sharing subsidies) could cause some insurers to raise premiums on some plans by as much as 40 percentage points higher than they otherwise would. Because premium subsidies increase as premiums rise, administrative actions that cause premiums to rise can also cause taxpayer costs to increase. For example, we estimate that ending cost-sharing subsidy payments could increase net federal costs by about $2.3 billion per year.

Insurers have already submitted their preliminary premiums for the upcoming calendar year to state regulators. Since there has not been clarity on these issues, some insurers are already assuming that the Trump Administration or Congress may take an action that would destabilize the market. Some companies have either significantly raised premiums for next year, scaled back their footprints, or made plans to exit the exchange or individual market all together. Insurers are still negotiating rates for 2018, so if they do not get clarity soon, premiums could go up even more or more insurers could leave.

Again, these premium increases would only affect people who buy their own insurance (particularly middle-income or upper-middle-income people who buy their own insurance without a subsidy to offset the costs), and this group does not make up a large share of the American public. Nonetheless, more insurer exits or large premium increases on the exchange markets could be seen as Obamacare failing. It is worth noting, though, that a majority (64 percent) of the public – including 53 percent of Republicans – say that because President Trump and Republicans in Congress are now in control of the government, they are responsible for any problems with the ACA moving forward.

What happens if the market fails?

Following some announcements of 2018 exits by major insurers, there are some counties at risk of having no insurer on the exchange next year. This would be a first; thus far, all counties have had at least one insurer on the exchange. As negotiations between insurers and state regulators are still underway, there is still time for other insurers to come in and fill these gaps. Thus far, in most cases, a new or expanding insurer has already moved in to cover counties once thought to be “bare.” However, administrative actions that destabilize the market could encourage more insurers to exit.

If no exchange insurer ultimately moves in to some of these counties, people buying their own insurance will not be able to get subsidies and would have to pay full price for insurance. Paying for unsubsidized insurance would be particularly difficult for low-income and older adults living in high-cost areas like many rural parts of the country. Our subsidy calculator can show the difference in cost. For example, in Knox County Ohio, a low-income 60-year-old could get a silver plan for $83 per month but would have to pay $775 per month if he bought that plan without a subsidy, plus he would have a higher deductible because he would no longer benefit from cost sharing subsidies that are only available on the exchange. That same person would also qualify for a free ($0 premium) bronze plan if he buys on exchange, but off-exchange without a subsidy he would have to pay more than $600 per month for a similar plan. People shopping for coverage off-exchange in a county left without an exchange insurer – particularly lower income or older exchange shoppers – may not be able to afford any option and may drop their coverage.

If the market becomes destabilized, and particularly if the individual mandate is not enforced, insurers may decide to exit the off-exchange market as well. This would mean that people in these counties who would otherwise buy their own insurance may not have any option even if they could afford to pay full price.

What might be done to strengthen the Marketplaces?

Although the individual health insurance market is stabilizing on average, insurer financial performance varies and some companies in some states are still struggling. Additionally, some insurers have already decided to increase premiums significantly or exit the market in 2018 on the assumption that the Trump Administration or Congress will take actions that destabilize the market. Although there are many ideas on both the left and the right for how to improve these markets, there are not many options that have bipartisan support.

One possible policy response that could receive bipartisan support would be to reestablish a reinsuranceprogram. Reinsurance programs provide funds to insurers that enroll high-cost (sicker) individuals and can work to lower premiums. The Affordable Care Act included a reinsurance program but it was temporary and phased out in 2016. Republicans in Congress and the Administration have also signaled a willingness to establish reinsurance programs: Both the House and Senate repeal bills included stability funds for reinsurance and Health and Human Services Secretary Price has supported Alaska’s request for a waiver to support its reinsurance program. Though such a program could receive bipartisan support, it would require additional funds (for example, taxing insurers in other markets).

Additional state flexibility to address local challenges in implementing the health care law may also receive some bipartisan support. The challenge of attracting insurers to rural areas or certain states, for example, may warrant state-specific solutions – either as part of the ACA’s waiver program or by Congress giving states additional flexibility.