Abstract

Issue:

The tax and spending law known as H.R. 1 includes provisions to revise what is counted as a Medicaid payment error and to recoup more federal funds. The new rules, which go into effect in 2029, target payments with inadequate documentation.

Goals: To review the scope of improper Medicaid payments and the potential impact of H.R. 1 policies on states, providers, and patients.

Methods: Analysis of research, government data, proposals, final rules, and laws.

Key Findings and Conclusion:

Although the provisions aim to reduce erroneous Medicaid payments, error rates could rise due to new Medicaid work requirements and other H.R. 1 provisions that make eligibility determination processes more complex for states. More than 20 states already have improper payment rates that exceed the threshold, meaning they could face significant financial penalties when the provisions go into effect. Policymakers could help reduce payment errors and the financial risk to states by encouraging the Centers for Medicare and Medicaid Services (CMS) and the U.S. Department of Health and Human Services to share best practices with states, use state audit data to improve oversight, and streamline Medicaid regulatory requirements. Additionally, CMS and states already have processes in place — including corrective action plans — to address erroneous payments.

Introduction

The tax and spending law, H.R. 1 (originally titled the “One Big Beautiful Bill”), enacted in July 2025, includes more than $900 billion in cuts to Medicaid, the public health insurance program financed jointly by the federal government and states. Some analysts have projected that, along with the law’s other changes to Medicaid, these cuts — the largest in the program’s 60-year history — will cause more than 7 million Americans to lose their Medicaid health coverage.1 The cuts will also shift costs to states, weaken the fiscal stability of health care providers, and diminish patients’ access to care.2

Supporters of H.R. 1 have asserted that it contains measures to address fraud, waste, and abuse. One of these provisions requires the U.S. Department of Health and Human Services (HHS) to recoup federal dollars for erroneous Medicaid payments — such as payments made for medical services when billing paperwork was missing or Medicaid eligibility paperwork was incomplete — once those payments exceed a certain level. The most recent data from the Centers for Medicare and Medicaid Services (CMS) released in January 2026 indicate that the nationwide error rate is 6.12 percent, slightly more than twice the 3 percent rate allowed under H.R. 1.3 According to that report, 77.17 percent of erroneous payments are due to incomplete documentation (namely missing paperwork), which is not generally indicative of fraud or abuse.4

The Congressional Budget Office (CBO) estimates that the policy change will reduce federal Medicaid spending by $7.55 billion and cause 100,000 individuals to lose their coverage as states tighten their processes to avoid penalties.5 To reduce error rates to comply with the new requirement and avoid financial penalties, states could further restrict eligibility determination processes to add greater certainty to ensuring all documentation has been submitted or require prior authorization before a provider can provide care.

Cumulatively, the implementation of H.R. 1’s broader Medicaid changes — such as implementation of work requirements, more frequent coverage renewals for certain enrollees, and changes to provider taxes — could make reducing improper payments more difficult.6 These changes will increase the administrative burden for states and patients while decreasing the funding available for Medicaid programs. With more administrative requirements and fewer dollars with which to implement programs, the chance of error increases.

This brief defines erroneous Medicaid payments and explores whether improper payment rates are an accurate measure of fraud. We describe how H.R. 1 expands the definition of an erroneous payment while limiting the federal government’s ability to waive penalties on states with improper payment rates that exceed a certain threshold even if they are making good faith efforts to address the errors. We also present data showing the disproportionate impact on some states and offer alternative strategies for policymakers to better support states in reducing improper Medicaid payments.

Defining Improper and Erroneous Medicaid Payments

Improper Medicaid payments, as defined in statute, can be overpayments, underpayments, and payments where there is not enough information to determine whether the payment was correct — such as when medical billing codes are inaccurate, provider paperwork is missing, or applicants submit incomplete documentation. Improper payments also include payments made for individuals who were enrolled in Medicaid despite being ineligible, as well as payments for services that do not comply with Medicaid program requirements such as duplicative payments.

The federal government determines what’s “improper” by reviewing Medicaid fee-for-service claims, managed care payments, and eligibility decisions. “Improper payments” is a broad category, while “erroneous payments” — payments that are incorrect under program rules — represent a more specific subset within it.7 Sometimes the terms are used interchangeably.

How CMS Defines Improper Payments

Improper payments can result from a variety of circumstances, including:

- Items or services with no documentation.

- Items or services with insufficient documentation.

- Items or services with documentation that does not substantiate the payment.

- Items or services where the payment was to the right recipient for the right amount, but the payment process did not comply with applicable statutory or regulatory payment requirements.

- With respect to Medicaid and CHIP, there is no record of the required verification of an individual’s eligibility factors, such as income.

Data: Centers for Medicare and Medicaid Services, “Fiscal Year 2025 Improper Payments Fact Sheet,” Jan. 15, 2026.

Improper Medicaid Payments as a Measure of Fraud

According to CMS, the improper payment rate is not a “fraud rate” but rather a measurement of payments made that did not meet statutory, regulatory, or administrative requirements.8

More than 75 percent of improper payments — just over 77 percent in 2025, as mentioned above — are due to insufficient documentation, and most involve a state, contractor, or provider missing an administrative step.9 With additional documentation, these payments may be correct.

Calculating Improper Medicaid Payments

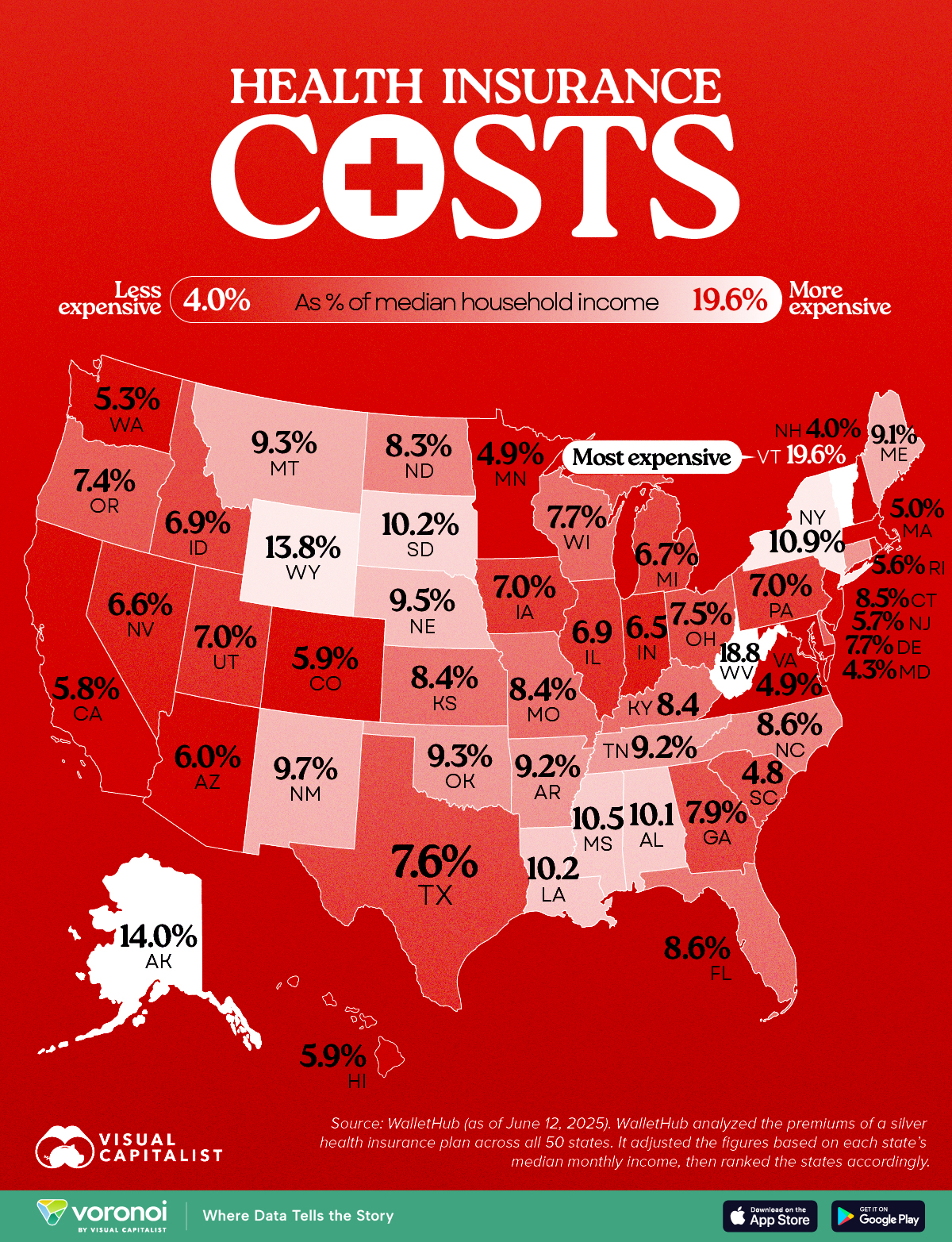

Each year, CMS conducts a payment error rate measurement (PERM) audit in 17 states — one-third of all states — so every state is reviewed once every three years. Each state’s improper payment rate is calculated by dividing the total value of overpayments and underpayments in a representative sample from three categories (Medicaid eligibility, fee-for-service, and managed care) by the state’s total Medicaid expenditures.10 CMS also publishes a national Medicaid improper payment rate, which was 6.12 percent in the most recent data.11 In 2025, these improper payments totaled $37.9 billion, including $10.8 billion (28.6%) from fee-for-service Medicaid, $27.0 billion (71.4%) from eligibility, and $0 from managed care Medicaid.12

Since 1983, federal law has set an allowable improper payment rate of 3 percent. When a state exceeds this threshold, the HHS secretary is required to recover the federal share of the excess erroneous payments as a penalty. However, the secretary has long had discretion to waive these repayments if a state was making a good faith effort not to exceed the allowable error rate, and the secretary has generally waived penalties.13

Medicaid Improper Payment Rate for Fiscal Year 2025

- Medicaid improper payment rate: 6.12%; $37.39 billion

- Medicaid appropriate federal payment rate: 93.88%; $573.6 billion

- Percentage of improper payments resulting from insufficient documentation: 77.17%

Notes: Each year approximately 17 states are reviewed. The national improper payment rate is a combination of the more recent three cycles in 2023, 2024, and 2025. In contrast to the 3 percent allowable error rate for Medicaid, Medicare is allowed a 10 percent error rate.

Data: Centers for Medicare and Medicaid Services, 2025 Medicaid and CHIP Supplemental Improper Payment Data (CMS, Jan. 2026).

What Is the Current Process for States to Address Error Rates?

States are required to develop a Medicaid corrective action plan (CAP) and submit it to CMS within 90 days of receiving their PERM error rate to address the errors identified in the PERM review.14 The CAP serves as the formal vehicle through which the state explains why errors occurred and identifies root causes across fee-for-service, managed care, and eligibility categories. In the CAP, which is intended to serve as a performance management tool, a state also commits to specific corrective actions designed to reduce future improper payments.

Once CMS approves the state’s PERM CAP, the state is required to implement the corrective actions in accordance with the approved schedule, usually over the course of multiple years. CMS collaborates with states by providing guidance, technical assistance, templates, and other supports.15 All states are required to keep CMS updated regarding the status of the CAP implementation, but states with PERM error rates above 3 percent are required to do so every other month according to federal regulations.16

A state is deemed to be making a good faith effort if it is meaningfully implementing its CAP in alignment with the underlying regulation even if the state has not yet fully eliminated improper payments. As mentioned, historically the HHS secretary has been allowed to waive penalties if the state was making a good faith effort; however H.R. 1 eliminates the option to do so.

Key Findings

H.R. 1 expands what’s considered an erroneous payment and restricts HHS’ authority to waive penalties.

The law alters erroneous payments, which are included in CMS’ PERM audits, in two primary ways: it expands the definition of an erroneous payment, and it adds restrictions to HHS’ ability to waive the penalty for erroneous payments.

Widening the scope of erroneous Medicaid payments. H.R. 1 expands the definition of erroneous payments to include payments made on behalf of individuals who the state does not know for sure are eligible for Medicaid because insufficient information is available to prove their eligibility (such as someone whose documentation was not saved correctly at enrollment or renewal). Expanding the definition in this way risks overstating improper activity by the states by equating administrative uncertainty with fraud.

Restricting HHS’ authority to waive penalties. The law also limits which erroneous payments can be waived: HHS can waive up to the total amount paid in overpayments on behalf of eligible individuals, or payments where there is not enough information available to prove eligibility. HHS can no longer waive penalties for payments made on behalf of individuals who were ineligible for Medicaid, or for services provided to patients with insufficient information to confirm their eligibility. Guidance from CMS will clarify how this will be implemented. Ultimately, this change takes away HHS’ flexibility to waive financial penalties when states are making good faith efforts to address their errors.

H.R. 1 also expands the type of audits that can be used to determine Medicaid erroneous payment rates. Whereas historically these audits have been conducted by CMS, the law gives the secretary authority to conduct audits directly or to use state audits, such as the Medicaid Eligibility Quality Control program.17

These erroneous payment provisions take effect in fiscal year 2030, which begins on October 1, 2029. In November 2025, CMS indicated that it plans to issue further guidance to states on how to implement this section of the law.18 That guidance has not yet been released and could come in the form of preliminary guidance or a proposed regulation. H.R. 1 does not require CMS to use a specific regulatory pathway for implementation.

H.R. 1’s erroneous payment provisions will have a disproportionate impact on some states.

The following table illustrates the state rates during the most recent audits, including which states had rates over the 3 percent threshold, making them subject to penalties under the new law starting in 2029. As mentioned, the most recent national Medicaid PERM rate is 6.12 percent.19

H.R. 1 already puts extensive strain on state budgets, shifting costs for Medicaid, the Supplemental Nutrition Assistance Program (SNAP), and other programs from the federal government to states. The erroneous payment provision contributes to this by adding yet another potential reduction in federal funding and further jeopardizing states’ fiscal stability. In response, states may adopt stricter approaches to eligibility determinations, such as requiring complete documentation or prior authorization before payments are made. These changes could delay treatment for patients, add additional medical debt or uncompensated care if care is not covered, add additional administrative burden for patients and providers, and put states out of compliance with federal application processing times.

Although the provision is intended to reduce erroneous payments, error rates are likely to rise as states implement other H.R. 1 provisions that make processes more complex — such as adding Medicaid work requirements and doubling the frequency of eligibility redeterminations for individuals eligible for Medicaid under the Affordable Care Act Medicaid expansion. These changes increase the risk of errors, and states may not have sufficient time to fully adjust before the new erroneous payment rules go into effect in 2029.

Recommendations for Reducing Fraud, Waste, and Abuse

Given the potential negative impact of the H.R. 1 provisions on states, policymakers have an opportunity to identify other options that could be more effective at reducing erroneous Medicaid payments. The Medicaid and CHIP Payment and Access Commission (MACPAC), Government Accountability Office (GAO), and National Association of Medicaid Directors (NAMD) have each offered recommendations to reduce unnecessary spending in Medicaid.20

About Medicaid Program Integrity

When designed and implemented well, program integrity initiatives help to ensure that:

- eligibility decisions are made correctly

- prospective and enrolled providers meet federal and state participation requirements

- services provided to enrollees are medically necessary and appropriate, and

- provider payments are made in the correct amount and for appropriate services.

Data: Statement of Tim Hill, Commissioner, Medicaid and CHIP Payment and Access Commission, “Examining How Improper Payments Cost Taxpayers Billions and Weaken Medicare and Medicaid,” Committee on Energy and Commerce, Subcommittee on Oversight and Investigations, U.S. House of Representatives, Apr. 16, 2024.

Of these, NAMD’s recommendations are particularly helpful to consider as state Medicaid agencies share the federal government’s commitment to safeguarding Medicaid funds. Program integrity efforts depend on effective collaboration between state Medicaid agencies and CMS. NAMD recently outlined five core areas of recommendations to improve program integrity in Medicaid:

- Strengthen the federal and state partnership through training, technical assistance, and structured collaboration. Expanding access to the Medicaid Integrity Institute and strengthening peer-to-peer learning opportunities are two options. Other strategies include enhancing the role of the Fraud, Waste, and Abuse Advisory Group and convening key program integrity partners, including Medicaid agencies, program integrity units, and others.

- Provide targeted support for high-risk service areas that present elevated program integrity risks. Suggestions include developing national risk indicators for high-risk services and providers, and offering more targeted guidance on monitoring strategies, including more frequent provider reverification and clearer documentation expectations.

- Improve data sharing and national visibility. Enhancing use of CMS’ nationwide dataset, the Transformed Medicaid Statistical Information System (T-MSIS), could allow program integrity efforts to be driven by actionable nationwide data — rather than a single state’s data. Agencies could then identify cross-state billing patterns, detect emerging fraud schemes, and flag providers operating across multiple jurisdictions.

- Enhance information sharing on providers and enforcement actions across programs. This would involve shifting from passive data collection to actionable intelligence across multiple programs, such as Medicaid, Medicare, and Veterans Affairs.

- Expand access to tools, technology, and analytic capacity to support program integrity efforts. Predictive modeling, data analytics, interoperable systems, cross-program datasets, and artificial intelligence tools — with appropriate safeguards — could help states develop a more complete picture and effectively identify suspicious patterns.

Additional details regarding these recommendations are available from NAMD.21

Of note, these strategies — as well as those set forth by MACPAC22 and GAO23 — are collaborative, not punitive. They focus on ensuring states have the resources they need to effectively prevent and address erroneous payments. They acknowledge that as fraud schemes grow increasingly complex and span multiple programs and jurisdictions, stronger coordination, expanded data sharing, and more closely aligned federal and state/territorial strategies are needed to effectively identify and address emerging risks. Both states and CMS can play key roles in helping this happen effectively.

In contrast, H.R. 1’s erroneous payment provisions — combined with the law’s broad Medicaid cuts — create considerable financial risk for states without pairing that with the supports necessary for states to effectively address erroneous payments. As a result, states may need to limit coverage or erect barriers to services for beneficiaries, who are the least likely actors to commit fraud against Medicaid.24

HOW WE CONDUCTED THIS STUDY

This study was conducted by analyzing the underlying statute of the One Big Beautiful Bill (H.R. 1) that was signed into law on July 4, 2025; reviewing CMS data on Medicaid program integrity, including the most recent data from FY2025 that was released in 2026; analyzing relevant regulations that govern requirements related to improper payments and Medicaid corrective action plans; reviewing the preliminary and interim guidance released by the Centers for Medicare and Medicaid Services (CMS) to date to implement H.R. 1; reviewing previous guidance from CMS regarding erroneous payments; reviewing recommendations from advisory bodies such as the Medicaid and CHIP Payment and Access Commission (MACPAC) and the Government Accountability Office (GAO); considering recommendations from entities such as the National Association of Medicaid Directors; and conducting a literature review.

Listen to the article7 min

Listen to the article7 min