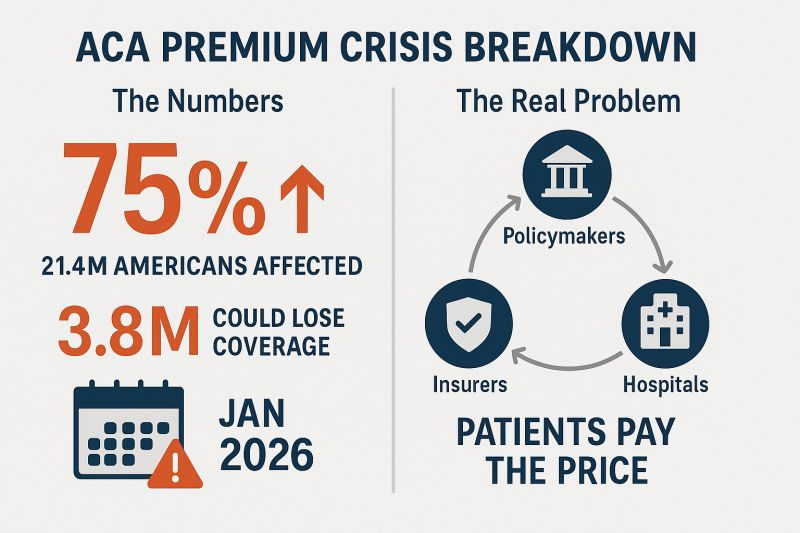

People who buy health insurance through the Affordable Care Act (ACA) are set to see a median premium increase of 18 percent, more than double last year’s 7 percent median proposed increase, according to an analysis of preliminary filings by KFF.

The proposed rates are preliminary and could change before being finalized in late summer. The analysis includes proposed rate changes from 312 insurers in all 50 states and DC.

It’s the largest rate change insurers have requested since 2018, the last time that policy uncertainty contributed to sharp premium increases. On average, ACA marketplace insurers are raising premiums by about 20 percent in 2026, KFF found.

Insurers said they wanted higher premiums to cover rising health care costs, like hospitalizations and physician care, as well as prescription drug costs. Tariffs on imported goods could play a role in rising medical costs, but insurers said there was a lot of uncertainty around implementation, and not many insurers were citing tariffs as a reason for higher rates.

But they are adding in higher increases due to changes being made by the Trump administration and Republicans in Congress. For instance, the majority of insurers said they are taking into account the potential expiration of enhanced premium tax credits.

Those subsidies, put in place during the COVID-19 pandemic, are set to expire at the end of the year, and there are few signs that Republicans are interested in tackling the issue at all.

If Congress takes no action, premiums for subsidized enrollees are projected to increase by over 75 percent starting in January 2026, according to KFF.

But some states are pushing back.

Arkansas Gov. Sarah Huckabee Sanders (R) on Wednesday called on the state’s insurance commissioner to disapprove the proposed increases from Centene and Blue Cross Blue Shield. The companies filed increases of up to 54 percent and 25.5 percent, respectively, she said.

“Arkansas’ Insurance Commissioner is required to disapprove of proposed rate increases if they are excessive or discriminatory, and these are both,” Huckabee Sanders said in a statement.

“I’m calling on my Commissioner to follow the law, reject these insane rate increases, and protect Arkansans.”

Medicaid cuts have received the lion’s share of attention from critics of Republicans’ sweeping tax cuts legislation, but the GOP’s decision not to extend enhanced ObamaCare subsidies could have a much more immediate impact ahead of next year’s midterms.

Extra subsidies put in place during the coronavirus pandemic are set to expire at the end of the year, and there are few signs Republicans are interested in tackling the issue at all.

To date, only Sens. Lisa Murkowski (R-Alaska) and Thom Tillis (R-N.C.) have spoken publicly about wanting to extend them.

The absence of an extension in the “big, beautiful bill” was especially notable given the sweeping changes the legislation makes to the health care system, and it gives Democrats an easy message: If Republicans in Congress let the subsidies expire at the end of the year, premiums will spike, and millions of people across the country could lose health insurance.

In a statement released last month as the House was debating its version of the bill, House and Senate Democratic health leaders pointed out what they said was GOP hypocrisy.

“Their bill extends hundreds of tax policies that expire at the end of the year. The omission of this policy will cause millions of Americans to lose their health insurance and will raise premiums on 24 million Americans,” wrote Senate Finance Committee ranking member Ron Wyden (D-Ore.), House Ways and Means Committee ranking member Richard Neal (D-Mass.) and House Energy and Commerce Committee ranking member Frank Pallone (D-N.J.).

“The Republican failure to stop this premium spike is a policy choice, and it needs to be recognized as such.”

More than 24 million Americans are enrolled in the insurance marketplace this year, and about 90 percent — more than 22 million people — are receiving enhanced subsidies.

“All of those folks will experience quite large out-of-pocket premium increases,” said Ellen Montz, who helped run the federal ObamaCare exchanges under the Biden administration and is now a managing director with Manatt Health.

“When premiums become less affordable, you have this kind of self-fulfilling prophecy where the youngest and the healthiest people drop out of the marketplace, and then premiums become even less affordable in the next year,” Montz said.

The subsidies have been an extremely important driver of ObamaCare enrollment. Experts say if they were to expire, those gains would be erased.

According to the Congressional Budget Office (CBO), 4.2 million people are projected to lose insurance by 2034 if the subsidies aren’t renewed.

Combined with changes to Medicaid in the new tax cut law, at least 17 million Americans could be uninsured in the next decade.

The enhanced subsidies increase financial help to make health insurance plans more affordable. Eligible applicants can use the credit to lower insurance premium costs upfront or claim the tax break when filing their return.

Premiums are expected to increase by more than 75 percent on average, with people in some states seeing their payments more than double, according to health research group KFF.

Devon Trolley, executive director of Pennie, the Affordable Care Act (ACA) exchange in Pennsylvania, said she expects at least a 30 percent drop in enrollment if the subsidies expire.

The state starts ramping up its open enrollment infrastructure in mid-August, she said, so time is running short for Congress to act.

“The only vehicle left for funding the tax credits, if they were to extend them, would be the government funding bill with a deadline of September 30, which we really see as the last possible chance for Congress to do anything,” Trolley said.

Trolley said three-quarters of enrollees in the state’s exchange have never purchased coverage without the enhanced tax credits in place.

“They don’t know sort of a prior life of when the coverage was 82 percent more expensive. And we are very concerned this is going to come as a huge sticker shock to people, and that is going to significantly erode enrollment,” Trolley said.

The enhanced subsidies were first put into effect during the height of the coronavirus pandemic as part of former President Biden’s 2021 economic recovery law and then extended as part of the Inflation Reduction Act.

The CBO said permanently extending the subsidies would cost $358 billion over the next 10 years.

Republicans have balked at the cost. They argue the credits hide the true cost of the health law and subsidize Americans who don’t need the help. They also argue the subsidies have been a driver of fraudulent enrollment by unscrupulous brokers seeking high commissions.

Sen. Bill Cassidy (R-La.), chair of the Senate Health, Education, Labor and Pensions Committee, last year said Congress should reject extending the subsidies.

The Republican Study Committee’s 2025 fiscal budget said the subsidies “only perpetuate a never-ending cycle of rising premiums and federal bailouts — with taxpayers forced to foot the bill.”

But since 2020, enrollment in the Affordable Care Act marketplace has grown faster in the states won by President Trump in 2024, primarily rural Southern red states that haven’t expanded Medicaid. Explaining to millions of Americans why their health insurance premiums are suddenly too expensive for them to afford could be politically unpopular for Republicans.

According to a recent KFF survey, 45 percent of Americans who buy their own health insurance through the ACA exchanges identify as Republican or lean Republican. Three in 10 said they identify as “Make America Great Again” supporters.

“So much of that growth has just been a handful of Southern red states … Texas, Florida, Georgia, the Carolinas,” said Cynthia Cox, vice president at KFF and director of the firm’s ACA program. “That’s where I think we’re going to see a lot more people being uninsured.”

New Medicaid funding rules proposed by Congress this week would halt efforts at the state level to better fund rural hospitals and deliver services to the most vulnerable populations in those areas. You can be certain that the administrators and staff of those hospitals, as well as leaders of the communities they serve, are watching closely to see if the cuts are enacted.

Lawmakers at the federal level are trying to make deeper cuts to Medicaid spending in an effort to lower the amount of deficit spending that would be created by President Trump’s spending plan. Trump has dubbed the plan his “big beautiful bill.”

Feds Would Strip Rural Hospitals of Lifeline Funds

Republican members of the Senate Finance Committee this week released their version of the bill that would drain funding for rural hospitals, which rely heavily on Medicaid funds to treat patients. It’s estimated that 25 to 40 percent of services provided by such hospitals are funded by Medicaid.

The federal government and states share the up-front medical costs for Medicaid patients. The federal government then reimburses states up to 50 percent of their Medicaid spending every year.

Many states fund their portion of the cost by taxing entities that provide those services to Medicaid patients.

The latest proposal in Congress would not only restrict how many patients could receive benefits, but it would also stop states from implementing those provider tax programs to help fund Medicaid services provided to residents.

At the federal level, the thinking is that if states keep taxing providers to fund Medicaid services, then the federal government will have to keep reimbursing states a portion of those costs.

The downside to that is many experts, along with several Republicans in Congress, namely Sens. Susan Collins of Maine, Lisa Murkowski of Alaska and Josh Hawley of Missouri, have predicted it will decimate rural hospitals.

West Virginia Republican Sen. Jim Justice went a step further, saying that the plan to limit states’ use of provider taxes will “really hurt a lot of folks.” Despite that statement, Justice said he is OK with the freeze.

State Lawmakers Sound the Alarm

There are 39 states with at least three or more provider taxes used to help fund Medicaid services. Alaska is the only state with no such tax.

Some states, such as Ohio, have set up a new rural hospital fund using provider taxes to help rural hospitals deliver Medicaid services to patients.

Ohio Governor Mike DeWine and the Republican-led state legislature set up a pilot program called the Rural Ohio Hospital Tax Pilot Program. The measure would allow counties to levy a tax on their local hospitals that would then be used to fund Medicaid services.

DeWine said the pilot program would help ease the financial stress rural hospitals face in Ohio. The plan contained in Ohio House Bill 96 has the blessing of the Ohio Hospital Association.

A group of Republican state lawmakers recently sent a letter to their federal counterparts pleading with them to remove the bill language because it would “torpedo” plans to keep rural hospitals functioning.

The American Hospital Association, a 130-year-old trade group of more than 5,000 hospitals and health care providers, this month released the impact on rural hospitals if this plan went into effect.

More than $50 billion would be lost by 2034, and more than 1.8 million rural Americans would lose health benefits.

Kentucky residents would be impacted the most, with 143,000 losing benefits, followed by 135,000 Californians. More than 86,000 Ohioans would lose Medicaid coverage under the plan by 2034, making it the third most impacted state.

To blunt the effects of the cuts, Collins reportedly is proposing the establishment of a $100 billion relief fund that could provide financial support to affected providers, rural hospitals in particular. Whether that or a similar but smaller fund will wind up in the final draft of the legislation apparently will be decided this weekend. Meanwhile, the Senate parliamentarian has ruled against many of the provisions of the Senate version of the bill, including the Finance Committee’s provider tax framework, which puts the whole thing in flux.

Senate leaders say they plan a long series of votes on amendments of the bill on Sunday. The “vote-arama” likely will go on throughout Sunday night and into Monday. If the Senate does pass its version of the bill, it will have to go back to the House. Lawmakers are under a self-imposed deadline to get the legislation to Trump by the July 4 holiday.

Manatee Memorial Hospital in Bradenton, Fla., is revising its charity care policies due to funding shortfalls, a move the investor-owned hospital called a “difficult, yet responsible, fiscally prudent decision,” according to a June 3 report by the Sarasota Herald-Tribune.

Part of King of Prussia, Pa.-based Universal Health Services, Manatee Memorial Hospital is a 300-bed facility staffed by over 800 physicians, residents, and allied health professionals.

In May, the hospital informed stakeholders it would no longer accept patients enrolled in Manatee County’s healthcare plan or unfunded referrals from the We Care Manatee nonprofit for uninsured, low-income county residents, effective June 1, the Sarasota Herald-Tribune reported.

Emergency room access will be maintained in compliance with the federal Emergency Medical Treatment and Labor Act.

“Our projected deficit from unfunded care, beyond charity care, amounts to several millions of dollars,” Manatee Memorial wrote in a May letter to stakeholders, as reported by the Sarasota Herald-Tribune. “The significant cost of unreimbursed care is unsustainable. We continue to be a supportive community partner and will maintain open discussions with Manatee County regarding solutions, however, we need to make this difficult, yet responsible, fiscally prudent decision.”

In April, Manatee Memorial Hospital CEO Tom McDougal indicated the hospital’s funding for indigent care services was unsustainable. He noted that the hospital’s costs for charity, indigent and uninsured care rose by 47% over two years, reaching $21.2 million in 2023, with an additional $2.9 million in uncollectable care. Last year, the hospital received $2.7 million in indigent funding from Manatee County.

“Ladies and gentlemen, I simply can’t afford to keep doing this without being compensated for it,” Mr. McDougal said at the April 16 public county commission meeting. “It takes away care from other patients.”

McDougal made his remarks at a commission meeting focused on undocumented immigration, acknowledging that specific figures linking undocumented immigrants to the rise in charity care costs were not available. Six percent of patients in the hospital emergency room self-disclosed their status as undocumented immigrants, which Mr. McDougal believes is an undercount.

The latest changes follow Mr. McDougal’s “very uncomfortable decision,” as he put it, in February to stop oncology services and some surgeries for Manatee County health plan enrollees, as the hospital’s costs under the program reached $9 million in 2023, compared to the $2.7 million reimbursement from the county.

This discussion was recorded on November 16, 2023. This transcript has been edited for clarity.

Robert D. Glatter, MD: Welcome. I’m Dr Robert Glatter, medical advisor for Medscape Emergency Medicine. Joining me today is Dr Brian Miller, a hospitalist with Johns Hopkins University School of Medicine and a health policy expert, to discuss the current and renewed interest in physician-owned hospitals.

Welcome, Dr Miller. It’s a pleasure to have you join me today.

Brian J. Miller, MD, MBA, MPH: Thank you for having me.

History and Controversies Surrounding Physician-Owned Hospitals

Miller: Thank you. I should note that my views are my own and don’t represent those of Hopkins or the American Enterprise Institute, where I’m a nonresident fellow nor the Medicare Payment Advisory Commission, of which I’m a Commissioner.

The story about physician-owned hospitals is an interesting one. Hospitals turned into health systems in the 1980s and 1990s, and physicians started to shift purely from an independent model into a more organized group practice or employed model. Physicians realized that they wanted an alternative operating arrangement. You want a choice of how you practice and what your employment is. And as community hospitals started to buy physicians and also establish their own physician groups de novo, physicians opened physician-owned hospitals.

Physician-owned hospitals fell into a couple of buckets. One is what we call community hospitals, or what the antitrust lawyers would call general acute care hospitals: those offering emergency room (ER) services, labor and delivery, primary care, general surgery — the whole regular gamut, except that some of the owners were physicians.

The other half of the marketplace ended up being specialty hospitals: those built around a specific medical specialty and series of procedures and chronic care. For example, cardiac hospitals often do CABG, TAVR, maybe abdominal aortic aneurysm (triple A) repairs, and they have cardiology clinics, cath labs, a cardiac intensive care unit (ICU), ER, etc. There were also orthopedic surgical specialty hospitals, which were sort of like an ambulatory surgery center (ASC) plus several beds. Then there were general surgical specialty hospitals. At one point, there were some women’s health–focused specialty hospitals.

The hospital industry, of course, as you can understand, didn’t exactly like this. They had a series of concerns about what we would historically call cherry-picking or lemon-dropping of patients. They were worried that physician-owned facilities didn’t want to serve public payer patients, and there was a whole series of reports and investigations.

Around the time the Affordable Care Act passed, the hospital industry had many concerns about physician-owned specialty hospitals, and there was a moratorium as part of the 2003 Medicare Modernization Act. As part of the bargaining over the hospital industry support for the Affordable Care Act, they traded their support for, among other things, their number one priority, which is a statutory prohibition on new or expanded physician-owned hospitals from participating in Medicare. That included both physician-owned community hospitals and physician-owned specialty hospitals.

Glatter: I guess the main interest is that, when physicians have an ownership or a stake in the hospital, this is what the Stark laws obviously were aimed at. That was part of the impetus to prevent physicians from referring patients where they had an ownership stake. Certainly, hospitals can be owned by attorneys and nonprofit organizations, and certainly, ASCs can be owned by physicians. There is an ongoing issue in terms of physicians not being able to have an ownership stake. In terms of equity ownership, we know that certain other models allow this, but basically, it sounds like this is an issue with Medicare. That seems to be the crux of it, correct?

Miller: Yes. I would also add that it’s interesting when we look at other professions. When we look at lawyers, nonlawyers are actually not allowed to own an equity stake in a law practice. In many other professions, you either have corporate ownership or professional ownership, or the alternative is you have only professional ownership.I would say the hospital industry is one of the few areas where professional ownership not only is not allowed, but also is statutorily prohibited functionally through the Medicare program.

Unveiling the Dynamics of Hospital Ownership

Glatter: A recent study done by two PhDs looked at 2019 data on 20 of the most expensive diagnosis-related groups (DRGs). It examined the cost savings, and we’re talking over $1 billion in expenditures when you look at the data from general acute care hospitals vs physician-owned hospitals. This is what appears to me to be a key driver of the push to loosen restrictions on physician-owned hospitals. Isn’t that correct?

Miller: I would say that’s one of many components. There’s more history to this issue. I remember sitting at a think tank talking to someone several years ago about hospital consolidation as an issue. We went through the usual levers that us policy wonks go through. We talked about antitrust enforcement, certificate of need, rising hospital costs from consolidation, lower quality (or at least no quality gains, as shown by a New England Journal of Medicine study), and decrements in patient experience that result from the diseconomies of scale. They sort of pooh-poohed many of the policy ideas. They basically said that there was no hope for hospital consolidation as an issue.

Well, what about physician ownership? I started with my research team to comb through the literature and found a variety of studies — some of which were sort of entertaining, because they’d do things like study physician-owned specialty hospitals, nonprofit-owned specialty hospitals, and for-profit specialty hospitals and compare them with nonprofit or for-profit community hospitals, and then say physician-owned hospitals that were specialty were bad.

They mixed ownership and service markets right there in so many ways, I’m not sure where to start. My team did a systematic review of around 30 years of research, looking at the evidence base in this space. We found a couple of things.

We found that physician-owned community hospitals did not have a cost or quality difference, meaning that there was no definitive evidence that the physician-owned community hospitals were cheaper based on historical evidence, which was very old. That means there’s not specific harm from them. When you permit market entry for community hospitals, that promotes competition, which results in lower prices and higher quality.

Then we also looked at the specialty hospital markets — surgical specialty hospitals, orthopedic surgical specialty hospitals, and cardiac hospitals. We noted for cardiac hospitals, there wasn’t clear evidence about cost savings, but there was definitive evidence of higher quality, from things like 30-day mortality for significant procedures like treatment of acute MI, triple A repair, stuff like that.

For orthopedic surgical specialty hospitals, we noted lower costs and higher quality, which again fits with operationally what we would know. If you have a facility that’s doing 20 total hips a day, you’re creating a focused factory. Just like if you think about it for interventional cardiology, your boards have a minimum number of procedures that you have to do to stay certified because we know about the volume-quality relationship.

Then we looked at general surgical specialty hospitals. There wasn’t enough evidence to make a conclusive thought about costs, and there was a clear trend toward higher quality. I would say this recent study is important, but there is a whole bunch of other literature out there, too.

Exploring the Scope of Emergency Care in Physician-Owned Hospitals

One thing I want to bring up — and this is an important issue — is that the risk for patients has been talked about by the American Hospital Association and the Federation of American Hospitals, in terms of limited or no emergency services at such physician-owned hospitals and having to call 911 when patients need emergent care or stabilization. That’s been the rebuttal, along with an Office of Inspector General (OIG) report from 2008. Almost, I guess, three quarters of the patients that needed emergent care got this at publicly funded hospitals.

Miller: I’m familiar with the argument about emergency care. If you actually go and look at it, it differs by specialty market. Physician-owned community hospitals have ERs because that’s how they get their business. If you are running a hospital medicine floor, a general surgical specialty floor, you have a labor delivery unit, a primary care clinic, and a cardiology clinic. You have all the things that all the other hospitals have. The physician-owned community hospitals almost uniformly have an ER.

When you look at the physician-owned specialty hospitals, it’s a little more granular. If you look at the cardiac hospitals, they have ERs. They also have cardiac ICUs, operating rooms, etc. The area where the hospital industry had concerns — which I think is valid to point out — is that physician-owned orthopedic surgical specialty hospitals don’t have ERs. But this makes sense because of what that hospital functionally is: a factory for whatever the scope of procedures is, be it joint replacements or shoulder arthroscopy. The orthopedic surgical specialty hospital is like an ASC plus several hospital beds. Many of those did not have ERs because clinically it didn’t make sense.

What’s interesting, though, is that the hospital industry also operates specialty hospitals. If you go into many of the large systems, they have cardiac specialty hospitals and cancer specialty hospitals. I would say that some of them have ERs, as they appropriately should, and some of those specialty hospitals do not. They might have a community hospital down the street that’s part of that health system that has an ER, but some of the specialty hospitals don’t necessarily have a dedicated ER.

I agree, that’s a valid concern. I would say, though, the question is, what are the scope of services in that hospital? Is an ER required? Community hospitals should have ERs. It makes sense also for a cardiac hospital to have one. If you’re running a total joint replacement factory, it might not make clinical sense.

Glatter: The patients who are treated at that hospital, if they do have emergent conditions, need to have board-certified emergency physicians treating them, in my view because I’m an ER physician. Having surgeons that are not emergency physicians staff a department at a specialty orthopedic hospital or, say, a cancer hospital is not acceptable from my standpoint. That’s my opinion and recommendation, coming from emergency medicine.

Miller: I would say that anesthesiologists are actually highly qualified in critical care. The question is about clinical decompensation; if you’re doing a procedure, you have an anesthesiologist right there who is capable of critical care. The function of the ER is to either serve as a window into the hospital for patient volume or to serve as a referral for emergent complaints.

Glatter: An anesthesiologist — I’ll take issue with that — does not have the training of an emergency physician in terms of scope of practice.

Miller: My anesthesiology colleagues would probably disagree for managing an emergency during an operating room case.

Glatter: Fair enough, but I think in the general sense. The other issue is that, in terms of emergent responses to patients that decompensate, when you have to transfer a patient, that violates Medicare requirements. How is that even a valid issue or argument if you’re going to have to transfer a patient from your specialty hospital? That happens. Again, I know that you’re saying these hospitals are completely independent and can function, stabilize patients, and treat emergencies, but that’s not the reality across the country, in my opinion.

Miller: I don’t think that’s the case for the physician-owned specialty cardiac hospitals, for starters. Many of those have ICUs in addition to operating rooms as a matter of routine in addition to ERs. I don’t think that’s the case for physician-owned community hospitals, which have ERs, ICUs, medicine floors, and surgical floors. Physician-owned community hospitals are around half the market. Of that remaining market, a significant percentage are cardiac hospitals. If you’re taking an issue with orthopedic surgical specialty hospitals, that’s a clinical operational question that can and should be answered.

I’d also posit that the nonprofit and for-profit hospital industries also operate specialty hospitals. Any of these questions, we shouldn’t just be asking about physician-owned facilities; we should be asking about them across ownership types, because we’re talking about scope of service and quality and safety. The ownership in that case doesn’t matter. The broader question is, are orthopedic surgical specialty hospitals owned by physicians, tax-exempt hospitals, or tax-paying hospitals? Is that a valid clinical business model? Is it safe? Does it meet Medicare conditions of participation? I would say that’s what that question is, because other ownership models do operate those facilities.

Glatter: You make some valid points, and I do agree on some of them. I think that, ultimately, these models of care, and certainly cost and quality, are issues. Again, it goes back to being able, in my opinion, to provide emergent care, which seems to me a very important issue.

Miller: I agree that providing emergent care is an issue. It’s an issue in any site of care. The hospital industry posits that all hospital outpatient departments (HOPDs) have emergent care. I can tell you, having worked in HOPDs (I’ve trained in them during residency), the response if something emergent happens is to either call 911 or wheel the patient down to the ER in a wheelchair or stretcher. I think that these hospital claims about emergency care coverage —these are important questions, but we should be asking them across all clinical settings and say what is the appropriate scope of care provided? What is the appropriate level of acuity and ability to provide emergent or critical care? That’s an important question regardless of ownership model across the entire industry.

Deeper Dive Into Data on Physician-Owned Hospitals

Glatter: We need to really focus on that. I’ll agree with you on that.

There was a March 2023 report from Dobson | DaVanzo. It showed that physician-owned hospitals had lower Medicaid, dual-eligible, and uncompensated care and charity care discharges than full-service acute care hospitals. Physician-owned hospitals had less than half the proportion of Medicaid discharges compared with non–physician-owned hospitals. They were also less likely to care for dual-eligible patients overall compared with non–physician-owned hospitals.

In addition, when COVID hit, the physician-owned hospitals overall — and again, there may be exceptions — were not equipped to handle these patient surges in the acute setting of a public health emergency. There was a hospital in Texas that did pivot that I’m aware of — Renaissance Hospital, which ramped up a long-term care facility to become a COVID hospital — but I think that’s the exception. I think this report raises some valid concerns; I’ll let you rebut that.

Miller: A couple of things. One, I am not aware that there’s any clear market evidence or a systematic study that shows that physician-owned hospitals had trouble responding to COVID. I don’t think that assertion has been proven. The study was funded by the hospital industry. First of all, it was not a peer-reviewed study; it was funded by an industry that paid a consulting firm. It doesn’t mean that we still shouldn’t read it, but that brings bias into question. The joke in Washington is, pick your favorite statistician or economist, and they can say what you want and have a battle of economists and statisticians.

For example, in that study, they didn’t include the entire ownership universe of physician-owned hospitals. If we go to the peer-reviewed literature, there’s a great 2015 BMJ paper showing that the Medicaid payer mix is actually the same between physician-owned hospitals vs not. The mix of patients by ethnicity — for example, think about African American patients — was the same. I would be more inclined to believe the peer-reviewed literature in BMJ as opposed to an industry-funded study that was not peer-reviewed and not independent and has methodological questions.

Glatter: Those data are 8 years old, so I’d like to see more recent data. It would be interesting, just as a follow-up to that, to see where the needle has moved — if it has, for that matter — in terms of Medicaid patients that you’re referring to.

Miller: I tend to be skeptical of all industry research, regardless of who published it, because they have an economic incentive. If they’re selecting certain age groups or excluding certain hospitals, that makes you wonder about the validity of the study. Your job as an industry-funded researcher is that, essentially, you’re being paid to look for an answer. It’s not necessarily an honest evaluation of the data.

Glatter: I want to bring up another point about the Hospital Readmissions Reduction Program (HRRP) and the data on how physician-owned hospitals compared with acute care hospitals that are non–physician-owned and have you comment on that. The Dobson | DaVanzo study called into question that physician-owned hospitals treat fewer patients who are dual-eligible, which we know.

Miller: I don’t think we do know that.

Glatter: There are data that point to that, again, looking at the studies.

Miller: I’m saying that’s a single study funded by industry as opposed to an independent, academic, peer-reviewed literature paper. That would be like saying, during the debate of the Inflation Reduction Act (IRA), that you should read the pharmaceutical industries research but take any of it at pure face value as factual. Yes, we should read it. Yes, we should evaluate it on its own merits. I think, again, appropriately, you need to be concerned when people have an economic incentive.

The question about the HRRP I’m going to take a little broader, because I think that program is unfair to the industry overall. There are many factors that drive hospital readmission. Whether Mrs Smith went home and ate potato chips and then took her Lasix, that’s very much outside of the hospital industry’s control, and there’s some evidence that the HRRP increases mortality in some patient populations.

In terms of a quality metric, it’s unfair to the industry. I think we took an operating process, internal metric for the hospital industry, turned it into a quality metric, and attached it to a financial bonus, which is an inappropriate policy decision.

Rethinking Ownership Models and Empowering Clinicians

Glatter: I agree with you on that. One thing I do want to bring up is that whether the physician-owned hospitals are subject to many of the quality measures that full-service, acute care hospitals are. That really is, I think, a broader context.

Miller: Fifty-five percent of physician-owned hospitals are full-service community hospitals, so I would say at least half the market is 100% subject to that.

Glatter: If only 50% are, that’s already an issue.

Miller: Cardiac specialty hospitals — which, as I said, nonprofit and for-profit hospital chains also operate — are also subject to the appropriate quality measures, readmissions, etc. Just because we don’t necessarily have the best quality measurement in the system in the country, it doesn’t mean that we shouldn’t allow care specialization. As I’d point out, if we’re concerned about specialty hospitals, the concern shouldn’t just be about physician-owned specialty hospitals; it should be about specialty hospitals by and large. Many health systems run cardiac specialty hospitals, cancer specialty hospitals, and orthopedic specialty hospitals. If we’re going to have a discussion about concerns there, it should be about the entire industry of specialty hospitals.

I think specialty hospitals serve an important role in society, allowing for specialization and exploiting in a positive way the volume-quality relationship. Whether those are owned by a for-profit publicly traded company, a tax-exempt facility, or physicians, I think that is an important way to have innovation and care delivery because frankly, we haven’t had much innovation in care delivery. Much of what we do in terms of how we practice clinically hasn’t really changed in the 50 years since my late father graduated from medical school. We still have rounds, we’re still taking notes, we’re still operating in the same way. Many processes are manual. We don’t have the mass production and mass customization of care that we need.

When you have a focused factory, it allows you to design care in a way that drives up quality, not just for the average patient but also the patients at the tail ends, because you have time to focus on that specific service line and that specific patient population.

Physician-owned community hospitals offer an important opportunity for a different employment model. I remember going to the dermatologist and the dermatologist was depressed, shuffling around the room, sad, and I asked him why. He said he didn’t really like his employer, and I said, “Why don’t you pick another one?” He’s like, “There are only two large health systems I can work for. They all have the same clinical practice environment and functionally the same value.”

Physicians are increasingly burned out. They face monopsony power in who purchases their labor. They have little control. They don’t want to go through five committees, seven administrators, and attend 25 meetings just to change a single small process in clinical operations. If you’re an owner operator, you have a much better ability to do it.

Frankly, when many facilities do well now, when they do well clinically and do well financially, who benefits? The hospital administration and the hospital executives. The doctors aren’t benefiting. The nurses aren’t benefiting. The CNA is not benefiting. The secretary is not benefiting. The custodian is not benefiting. Shouldn’t the workers have a right to own and operate the business and do well when the business does well serving the community? That puts me in the weird space of agreeing with both conservatives and progressives.

Glatter: I agree with you. I think an ownership stake is always attractive. It helps with retention of employed persons. There’s no question that, when they have a stake, when they have skin in the game, they feel more empowered. I will not argue with you about that.

Miller: We don’t have business models where workers have that option in healthcare. Like the National Academy of Medicine said, one of the key drivers of burnout is the externalization of the locus of control over clinical practice, and the current business operating models guarantee an externalization of the locus of control over clinical practice.

If you actually look at the recent American Medical Association (AMA) meeting, there was a resolution to ban the corporate practice of medicine. They wanted to go more toward the legal professions model where only physicians can own and operate care delivery.

Miller: It’s not just doctors. I think nurses want a better lifestyle. The nurses are treated as interchangeable lines on a spreadsheet. The nurses are an integral part of our clinical team. Why don’t we work together as a clinical unit to build a better delivery system? What better way to do that than to have clinicians in charge of it, right?

My favorite bakery that’s about 30 minutes away is owned by a baker. It is not owned by a large tax-exempt corporation. It’s owned by an owner operator who takes pride in their work. I think that is something that the profession would do well to return to. When I was a resident, one of my colleagues was already planning their retirement. That’s how depressed they were.

I went into medicine to actually care for patients. I think that we can make the world a better place for our patients. What that means is not only treating them with drugs and devices, but also creating a delivery system where they don’t have to wander from lobby to lobby in a 200,000 square-foot facility, wait in line for hours on end, get bills 6 months later, and fill out endless paper forms over and over again.

All of these basic processes in healthcare delivery that are broken could have and should have been fixed — and have been fixed in almost every other industry. I had to replace one of my car tires because I had a flat tire. The local tire shop has an app, and it sends me SMS text messages telling me when my appointment is and when my car is ready. We have solved all of these problems in many other businesses.

We have not solved them in healthcare delivery because, one, we have massive monopolies that are raising prices, have lower quality, and deliver a crappy patient experience, and we have also subjugated the clinical worker into a corporate automaton. We are functionally drones. We don’t have the agency and the authority to improve clinical operations anymore. It’s really depressing, and we should have that option again.

I trust my doctor. I trust the nurses that I work with, and I would like them to help make clinical decisions in a financially responsible and a sensible operational manner. We need to empower our workforce in order to do that so we can recapture the value of what it means to be a clinician again.

The current model of corporate employment: massive scale, more administrators, more processes, more emails, more meetings, more PowerPoint decks, more federal subsidies. The hospital industry has choices. It can improve clinical operations. It can show up in Washington and lobby for increased subsidies. It can invest in the market and not pay taxes for the tax-exempt facilities. Obviously, it makes the logical choices as an economic actor to show up, lobby for increased subsidies, and then also invest in the stock market.

Improving clinical operations is hard. It hasn’t happened. The Bureau of Labor Statistics shows that the private community hospital industry has had flat labor productivity growth, on average, for the past 25 years, and for some years it even declined. This is totally atypical across the economy.

We have failed our clinicians, and most importantly, we have failed our patients. I’ve been sick. My relatives have been sick, waiting hours, not able to get appointments, and redoing forms. It’s a total disaster. It’s time and reasonable to try an alternative ownership and operating model. There are obviously problems. The problems can and should be addressed, but it doesn’t mean that we should have a statutory prohibition on professionals owning and operating their own business.

Glatter: There was a report that $500 million was saved by limiting or banning or putting a moratorium on physician-owned hospitals by the Congressional Budget Office.

The CBO is not transparent about what its assumptions are or its analysis and methods. As a researcher, we have to publish our information. It has to go through peer review. I want to know what goes into that $500 million figure — what the assumptions are and what the model is. It’s hard to comment without knowing how they came up with it.

Glatter: The points you make are very valid. Physicians and nurses want a better lifestyle.

Miller: It’s not even a better lifestyle. It’s about having a say in how clinical operations work and helping make them better. We want the delivery system to work better. This is an opportunity for us to do so.

Glatter: That translates into technology: obviously, generative artificial intelligence (AI) coming into the forefront, as we know, and changing care delivery models as you’re referring to, which is going to happen. It’s going to be a slow process. I think that the evolution is happening and will happen, as you accurately described.

Miller: The other thing that’s different now vs 20 years ago is that managed care is here, there, and everywhere, as Dr Seuss would say. You have utilization review and prior authorization, which I’ve experienced as a patient and a physician, and boy, is it not a fun process. There’s a large amount of friction that needs to be improved. If we’re worried about induced demand or inappropriate utilization, we have managed care right there to help police bad behavior.

Reforming Healthcare Systems and Restoring Patient-Centric Focus

Glatter: If you were to come up with, say, three bullet points of how we can work our way out of this current morass of where our healthcare systems exist, where do you see the solutions or how can we make and effect change?

Miller: I’d say there are a couple of things. One is, let business models compete fairly on an equal playing field. Let the physician-owned hospital compete with the tax-exempt hospital and the nonprofit hospital. Put them on an equal playing field. We have things like 340B, which favors tax-exempt hospitals. For-profit or tax-paying hospitals are not able to participate in that. That doesn’t make any sense just from a public policy perspective. Tax-paying hospitals and physician-owned hospitals pay taxes on investments, but tax-exempt hospitals don’t. I think, in public policy, we need to equalize the playing field between business models. Let the best business model win.

The other thing we need to do is to encourage the adoption of technology. The physician will eventually be an arbiter of tech-driven or AI-driven tools. In fact, at some point, the standard of care might be to use those tools. Not using those tools would be seen as negligence. If you think about placing a jugular or central venous catheter, to not use ultrasound would be considered insane. Thirty years ago, to use ultrasound would be considered novel. I think technology and AI will get us to that point of helping make care more efficient and more customized.

Those are the two biggest interventions, I would say. Third, every time we have a conversation in public policy, we need to remember what it is to be a patient. The decision should be driven not around any one industry’s profitability, but what it is to be a patient and how we can make that experience less burdensome, less expensive, or in plain English, suck less.

Glatter: Safety net hospitals and critical access hospitals are part of this discussion that, yes, we want everything to, in an ideal world, function more efficiently and effectively, with less cost and less red tape. The safety net of our nation is struggling.

Miller: I 100% agree. The Cook County hospitals of the world are deserving of our support and, frankly, our gratitude. Facilities like that have huge burdens of patients with Medicaid. We also still have millions of uninsured patients. The neighborhoods that they serve are also poorer. I think facilities like that are deserving of public support.

I also think we need to clearly define what those hospitals are. One of the challenges I’ve realized as I waded into this space is that market definitions of what a service market is for a hospital, its specialty type or what a safety net hospital is need to be more clearly defined because those facilities 100% are deserving of our support. We just need to be clear about what they are.

Regarding critical access hospitals, when you practice in a rural area, you have to think differently about care delivery. I’d say many of the rural systems are highly creative in how they structure clinical operations. Before the public health emergency, during the COVID pandemic, when we had a massive change in telehealth, rural hospitals were using — within the very narrow confines — as much telehealth as they could and should.

Rural hospitals also make greater use of nurse practitioners (NPs) and physician assistants (PAs). For many of the specialty services, I remember, your first call was an NP or a PA because the physician was downstairs doing procedures. They’d come up and assess the patient before the procedure, but most of your consult questions were answered by the NP or PA. I’m not saying that’s the model we should use nationwide, but that rural systems are highly innovative and creative; they’re deserving of our time, attention, and support, and frankly, we can learn from them.

Glatter: I want to thank you for your time and your expertise in this area. We’ll see how the congressional hearings affect the industry as a whole, how the needle moves, and whether the ban or moratorium on physician-owned hospitals continues to exist going forward.

Miller: I appreciate you having me. The hospital industry is one of the most important industries for health care. This is a time of inflection, right? We need to go back to the value of what it means to be a clinician and serve patients. Hospitals need to reorient themselves around that core concern. How do we help support clinicians — doctors, nurses, pharmacists, whomever it is — in serving patients? Hospitals have become too corporate, so I think that this is an expected pushback.

Glatter: Again, I want to thank you for your time. This was a very important discussion. Thank you for your expertise.

Robert D. Glatter, MD, is an assistant professor of emergency medicine at Zucker School of Medicine at Hofstra/Northwell in Hempstead, New York. He is a medical advisor for Medscape and hosts the Hot Topics in EM series.

Brian J. Miller, MD, MBA, MPH, is a hospitalist and an assistant professor of medicine at the Johns Hopkins University School of Medicine. He is also a nonresident fellow at the American Enterprise Institute. From 2014 – 2017, Dr Miller worked at four federal regulatory agencies: Federal Trade Commission (FTC), Federal Communications Commission (FCC), Centers for Medicare & Medicaid Services (CMS), and the Food & Drug Administration (FDA).

New York Gov. Kathy Hochul has vowed to protect New Yorkers from medical debt, limit hospitals’ ability to sue patients and expand financial assistance programs as part of her 2024 State of the State.

Ms. Hochul aims to introduce legislation that would curb hospitals’ ability to sue patients earning less than 400% of the federal poverty level ($120,000 for a family of four).

The legislation would also expand hospital financial assistance programs for low-income New Yorkers, limit the size of monthly payments and interest charged for medical debt, among other protections to improve access to financial assistance and mitigate the effects of medical debt.

“More than 700,000 New Yorkers have medical debt in collections. Individuals with medical debt are less likely to seek necessary medical care and report being forced to cut back on critical social determinants of health, including food, heat, and rent,” Ms. Hochul’s office said in a Jan. 2 news release. “As a result, substantial debt levels threaten not only the financial stability of many individuals and families, but also undermine the state’s commitment to improving health equity and health outcomes.”

The governor also aims to eliminate insulin cost-sharing through proposed legislation and provide financial relief to New Yorkers and improve adherence to these medications. With 1.58 million New Yorkers diagnosed with diabetes, Ms. Hochul’s office estimates this initiative will save about $14 million in 2025 alone.

“Too many New Yorkers today must overextend their finances to afford critical healthcare, like insulin, and to pay everyday expenses, like rent,” New York State Department of Financial Services Superintendent Adrienne Harris said. “When an individual is forced to choose between the two, deprioritizing their health impacts their lives, their families, and ultimately increases costs across the healthcare system. The alternative is no better. Without enough cash to cover all expenses, New Yorkers have turned to buy now, pay later products, racking up debt with companies that have operated without guardrails in this state for too long.”

Last week, Kaiser Family Foundation (KFF) released its Annual Employer Health Benefits Survey which included a surprise:

The average annual single premium and the average annual family premium each increased by 7% over the last year.

In 2022 as post-pandemic recovery was the focus for employers, the average single premium grew by 2% and the average family premium increased by 1%. Health costs and insurance premiums were not top of mind concerns to employers struggling to keep employees paid and door open. But 7% is an eye-opener.

The rest of the findings in the 2023 KFF Report are unremarkable: they reflect employer willingness to maintain benefits at/near pre-pandemic levels and slight inclination toward expanded benefits beyond mental health:

“The average annual premium for employer-sponsored health insurance in 2023 is $8,435 for single coverage and $23,968 for family coverage. Comparatively, there was an increase of 5.2% in workers’ wages and inflation of 5.8%2. The average single and family premiums increased faster this year than last year (2% vs. 7% and 1% vs. 7% respectively).

Over the last five years, the average premium for family coverage has increased by 22% compared to an 27% increase in workers’ wages and 21% inflation.

For single coverage, the average premium for covered workers is higher at small firms than at large firms ($8,722 vs. $8,321). The average premiums for family coverage are comparable for covered workers in small and large firms ($23,621 vs. $24,104) …

Most covered workers contribute to the cost of the premium for their coverage. On average, covered workers contribute 17% of the premium for single coverage and 29% of the premium for family coverage, similar to the percentages contributed in 2022…

90% of workers with single coverage have a general annual deductible that must be met before most services are paid for by the plan, similar to the percentage last year (88%).

The average deductible amount in 2023 for workers with single coverage and a general annual deductible is $1,735, similar to last year…

In 2023, among workers with single coverage, 47% of workers at small firms and 25% of workers at large firms have a general annual deductible of $2,000 or more. Over the last five years, the percentage of covered workers with a general annual deductible of $2,000 or more for single coverage has grown from 26% to 31%.

While nearly all large firms (firms with 200 or more workers) offer health benefits to at least some workers, small firms (3-199 workers) are significantly less likely to do so. In 2023, 53% of all firms offered some health benefits, similar to the percentage last year (51%).”

My take:

These findings show that employers are not prone to drastic changes in health benefits for their employees despite recognition it is expensive and unaffordable to small companies and for many of their own employees. But many large self-insured employers (except those in government, education and healthcare) are poised to make significant changes next year. They recognize themselves as the primary source of profits enjoyed by insurers, hospitals, physicians, drug companies and others.

They’re developing multi-year at risk direct contracts, value-based purchasing arrangements, primary care gatekeeping, narrow networks, restricted formularies, alternative care models and more to that leverage their clout. They’re going on offense.

The KFF Benefits Survey is a snapshot of where employer benefits are today, but it’s likely not the same next year. It appears employers are ready to engage the health industry head on.

PS Last week, the feud between Senate Health, Education, Labor and Pensions (HELP) Committee Chair Bernie Sanders and Not-for-Profit Health Systems heated up. On Oct. 10, he released a Majority Staff Report that said NFP hospitals do not deserve their tax exemptions as they spend “paltry amounts” on charity care. “Hospitals have gladly accepted the tax benefits that come with nonprofit status but have failed to provide the required community benefits. Non-profit hospitals spent only an estimated $16 billion on charity care in 2020, or about 57% of the value of their tax breaks in the same year.”

The same day, the American Hospital Association (AHA) released its analysis of hospital Schedule H filings concluding that tax-exempt hospitals provided $130 billion in community benefits in 2020 and called the HELP report “just plain wrong”.

In response to the AHA report, Sanders noted that AHA had not included CEO Compensation for NFPs in its analysis though featured prominently in his Majority Staff Report: “In 2021, the most recent year for which data is available for all of the 16 hospital chains, those companies’ CEOs averaged more than $8 million in compensation and collectively made over $140 million…

The disparities between the paltry amounts these hospitals are spending on charity care and their massive revenues and excessive executive compensation demonstrates that they are failing to live up to their end of the non-profit bargain.”

This tit for tat between the Committee Chairman and AHA is notable for 2 reasons: it draws attention to the Schedule H information goldmine about how not-for-profit hospitals operate since they’re now required to attach their S-10 Medicare cost report worksheets. Quantifying charity care in Exhibit 3B (for which there’s no expectation of payment) and the myriad of claimed community benefits including bad debt in Schedule 3C will likely intensify scrutiny of NFPs even more. Second, it draws attention to Executive Pay in hospitals: in this regard the Majority Staff Report commentary on CEO pay is misleading: by combining Column B (wages, bonuses) with Columns C (Deferred compensation) and D (non-taxable benefits), the total is significantly higher than one-year’s actual take-home pay for the CEOs. But it makes headlines!

If not-for-profit systems wish to lead transformational change in U.S. healthcare, not-for-profit system boards and their trade associations must be prepared to address the storm clouds gathering above. The skirmish between the Senate HELP Chair and AHA mirrors an increasingly skeptical public who, with Congress, believe the system is being gamed.

A bipartisan quartet of influential senators is tapping tax regulators within the U.S. Treasury for detailed information on nonprofit hospitals’ reported charity care and community investments, the latest in legislators’ increasing scrutiny of tax-exempt hospitals’ business practices.

In a pair of letters (PDF) sent Monday, Sens. Elizabeth Warren, D-Massachusetts, Raphael Warnock, D-Georgia, Bill Cassidy, M.D., R-Louisiana, and Chuck Grassley, R-Iowa, wrote they “are alarmed by reports that despite their tax-exempt status, certain nonprofit hospitals may be taking advantage of this overly broad definition of ‘community benefit’ and engaging in practices that are not in the best interest of the patient.”

They also outlined studies from academic and policy groups highlighting that the tax-exempt status of the nation’s nonprofit hospitals collectively was worth about $28 billion in 2020 and how this tally paled in comparison to the charity care most of those hospitals had provided during that same period.

Such studies have been quickly contested by the hospital lobby, which highlights that charity care is just one component of the broader activities that constitute a nonprofit hospital’s community benefit spending.

However, that ambiguity was squarely in the crosshairs of the legislators who said the long-standing community benefit standard “is arguably insufficient in its current form to guarantee protection and services to the communities hosting these hospitals.”

They cited a 2020 report from the Government Accountability Office that found oversight of nonprofit hospitals’ tax exemptions was “challenging” due to the vague definition of community benefit.

Though the IRS implemented several of the office’s recommendations from the report, “more is required to ensure nonprofit hospitals’ community benefit information is standardized, consistent and easily identifiable.” Included here could be additional updates to Form 990’s Schedule H, where nonprofits detail their community benefits and related activities.

To get a better handle on the agencies’ current oversight, the legislators requested from the IRS and the Treasury’s Tax Exempt & Government Entities Division a laundry list of information related to nonprofits’ tax filings from the last several years, including “a list of the most commonly reported community benefit activities that qualified a nonprofit hospital for tax exemptions in FY2021 and FY2022.”

They also sought lists of the nonprofit hospitals that were flagged, penalized or had their tax-exempt status revoked for violating community benefit standard requirements.

In another letter to the Treasury’s inspector general for tax administration, they asked the auditor to update their upcoming reviews to evaluate existing standards for financial assistance policy and other “practices that reduce unnecessary medical debt from patients who qualify for free or discounted care.”

The lawmakers also asked the inspector general to explore how often nonprofit hospitals bill patients with “gross charges” and to make sure the IRS is doing enough to ensure hospitals are making “’reasonable efforts’ to determine whether individuals are eligible for financial assistance before initiating extraordinary collection actions.”

Both letters from the senators gave the tax regulators 60 days to provide the requested information.

This brief examines past-due medical debt among nonelderly adults and their families using nationally representative survey data collected in June 2022. The analysis assesses the share of adults ages 18 to 64 with past-due medical bills owed to hospitals and other health care providers as well as the actions taken by hospitals to collect payment or make bills easier to settle.

It focuses on the experiences of adults with family incomes below and above 250 percent of the federal poverty level (FPL), approximating the income cutoff used by many hospitals to determine eligibility for free and discounted care.

WHY THIS MATTERS

In their efforts to protect patients from medical debt, policymakers have increasingly focused on the role of hospital billing and collection practices, with particular scrutiny directed toward nonprofit hospitals’ provision of charity care. Understanding the experiences of people with past-due bills owed to hospitals and other providers can shed light on the potential for new consumer protections to alleviate debt burdens.

WHAT WE FOUND

More than one in seven nonelderly adults (15.4 percent) live in families with past-due medical debt. Nearly two-thirds of these adults have incomes below 250 percent of FPL.

Nearly three in four adults with past-due medical debt (72.9 percent) reported owing at least some of that debt to hospitals, including 27.9 percent owing hospitals only and 45.1 percent owing both hospitals and other providers. Adults with past-due hospital bills generally have much higher total amounts of debt than those with past-due bills only owed to non-hospital providers.

Most adults (60.9 percent) with past-due hospital bills reported that a collection agency contacted them about the debt, but much smaller shares reported that the hospital filed a lawsuit against them (5.2 percent), garnished their wages (3.9 percent), or seized funds from a bank account (1.9 percent).

Though about one-third (35.7 percent) of adults with past-due hospital bills reported working out a payment plan, only about one-fifth (21.7 percent) received discounted care.

Adults with incomes below 250 percent of FPL were as likely as those with higher incomes to experience hospital debt collection actions and to have received discounted care.

The concentration of past-due medical debt among families with low incomes and the large share who owe a portion of that debt to hospitals suggests that expanded access to hospital charity care and stronger consumer protections could complement health insurance coverage expansions and other efforts to mitigate the impact of unaffordable medical bills.

HOW WE DID IT

This analysis draws on data from the June 2022 round of the Urban Institute’s Health Reform Monitoring Survey (HRMS), a nationally representative, internet-based survey of adults ages 18 to 64 that provides timely information on health insurance coverage, health care access and affordability, and other health topics. Approximately 9,500 adults participated in the June 2022 HRMS.

Researchers estimate 15 million people will lose their Medicaid starting April 1 when states begin removing people from the low-income health insurance program for the first time in three years.

In March 2020, Congress banned states from removing people from Medicaid during the pandemic in exchange for more federal funding for state Medicaid programs. Medicaid enrollment is usually tied to people’s incomes, and individuals normally have to regularly prove they still qualify in what’s known as a redetermination. (In the 39 states and Washington, D.C., that have expanded Medicaid, a family of four has to make less than $40,000 to qualify. In non-expansion states, the cutoff is even lower.)

With redeterminations paused, Medicaid enrollment nationwide has grown from 71 million in February 2020 to an estimated 95 million in March 2023.Research shows Medicaid coverage is associated with better access to care, more financial security, better health and lower mortality. During the pandemic, beneficiaries have been able to enjoy these benefits without worrying about confirming their eligibility.

In December, Congress voted to let states restart the process of clearing their rolls on April 1, what’s sometimes referred to as “unwinding.”Lawmakers are giving states 14 months to redetermine millions of people’s eligibility — an unprecedented task made even more difficult by serious staffing and experience shortages in many Medicaid offices.

“It’s going to be a big lift,” said Sayeh Nikpay, a health policy researcher at the University of Minnesota and Tradeoffs Senior Research Advisor. “States have never had to do this many redeterminations this quickly before, and there’s a lot of uncertainty about what will happen.”

We asked Nikpay to pick out a few relevant studies to help us understand what is happening and how states and employers could keep more people insured. Here are three she identified as particularly helpful.

Two types of people will lose coverage

The Office of the Assistant Secretary for Planning and Evaluation, which provides research for the U.S. Department of Health and Human Services, released a report in August 2022 that estimated 15 million people will lose Medicaid coverage as a result of the unwinding. (The estimate is similar to another analysis by the independent Urban Institute.)

ASPE breaks those 15 million people into two groups. In the first group are people who make too much money to qualify for Medicaid. ASPE estimates there are about 8 million people in that category, and they should be able to get insurance through work or the Obamacare exchanges.

In the second group are roughly 7 million people ASPE estimates are still eligible but will lose coverage because of what’s called “administrative churn.”This can happen if the Medicaid office can’t get in touch with someone to confirm their eligibility because they’ve moved or changed their phone number or if they’re unable to make an in-person appointment because of work or child care responsibilities. (The Urban Institute projects about 4 million people will be in this group.)

These two groups represent a key tension to the unwinding process: States want to shed people who make too much money, but officials also know eligible people often lose coverage during redeterminations, and that danger is heightened given the scale and speed of this process.

Making the switch from Medicaid to private insurance

This next paper looks at the first group: the roughly 8 million people expected to move from Medicaid to private coverage, and specifically the roughly 4 million who are expected to get coverage through the Obamacare exchanges. Adrianna McIntyre, an assistant professor of health policy at Harvard, wrote in JAMA Health Forum in October 2022 about the most effective ways to move people from Medicaid onto private Obamacare plans.

There’s limited data on this, but based on the few studies available, McIntyre found that only 3 to 5 percent of people who leave Medicaid end up getting an Obamacare plan. Many policymakers are relying on the Obamacare exchanges to provide a life preserver to millions of people losing Medicaid coverage, but the research cited by McIntyre shows getting people into these plans is not guaranteed and will take focused effort by states.

McIntyre’s review cites several randomized controlled trials where states tested different ways of increasing enrollment in Obamacare plans. These studies found simple reminders from the state – like physical letters, emails and phone calls help – boost sign-ups anywhere from 7 to 16 percent.

But what really seems to make a difference is reminders plus connecting people to someone who can get them signed up while they are on the phone. In one of those trials published in 2022, people in California who got a reminder email and a call connecting them to enrollment assistance were almost 50% more likely to sign up for a plan. Such extra effort is obviously costly, and it may not be a priority or financially feasible for some states.

McIntyre’s review did not include any research on what employers can do to help their workers transition from Medicaid to work-based coverage, but based on the studies McIntyre cited, Nikpay said she thinks it’s a good idea for employers to make sure people know Medicaid could be going away and provide as much help as possible in getting new coverage.

Making it easier to stay on Medicaid can have other benefits

The final study looks at the second group of people expected to lose Medicaid coverage: the 7 million people who may lose coverage due to administrative churn even though they are still eligible.

Some states have tried to limit that churn, and researchers at the RAND Corporation evaluated New York’s effort. Starting in 2014, New York allowed people to stay on Medicaid without any redeterminations for 12 months once enrolled.

In addition to keeping more people on Medicaid for longer, researchers found that after this policy was in place, hospital admissions and monthly costs per beneficiary went down. The researchers can’t say whether the continuous enrollment policy directly caused these improved outcomes, but the findings suggest that avoiding administrative churn can help people stay covered without ballooning costs.

“It seems reasonable to me,” Nikpay said of the findings, “that making it easier to stay on Medicaid, even outside of a global pandemic, could benefit people’s health given what we know about how Medicaid affects people.”