Liberal advocacy groups are ramping up efforts to protect the Medicaid program from potential cuts by Republican lawmakers and the new Trump administration.

The Democratic group Protect Our Care launched Tuesday an eight-figure “Hands off Medicaid” ad campaign targeting key Republicans in the House and Senate, warning of health care being “ripped away” from vulnerable Americans.

The lawmakers include GOP Sens. Bill Cassidy (La.), Chuck Grassley (Iowa), Lisa Murkowski (Alaska) and Susan Collins (Maine), as well as Reps. David Schweikert (Ariz.), Mike Lawler (N.Y.) and David Valadao (Calif.).

The campaign will also include digital advertising across platforms targeting the Medicaid population in areas around nursing homes and rural hospitals, ads on streaming platforms as well as billboards and bus stop wraps.

Medicaid covers 1 in 5 Americans, and the group wants to highlight that includes “kids, moms, seniors, people of color, rural Americans, and people with disabilities.”

“The American people didn’t vote in November to have their grandparents kicked out of nursing homes or health care ripped away from kids with disabilities or expectant moms in order to give Elon Musk another tax cut,” Protect Our Care chair Leslie Dach said in a statement.

House Republicans have expressed openness to making some drastic changes in the Medicaid program to pay for extending President Trump’s signature tax cuts, including instituting work requirements and capping how much federal money is spent per person. The ideas have been conservative mainstays since they were included as part of the 2017 Obamacare repeal effort.

Separately, advocacy group Families USA led a letter with more than 425 national, state and local organizations calling on Trump to protect Medicaid.

The groups noted that if the Trump administration wants to trim health costs, “there are many well-vetted, commonsense and bipartisan proposals” that don’t involve slashing Medicaid.

“In 2017, millions upon millions of Americans rose up against proposed cuts and caps and made clear how much they valued Medicaid as a critical health and economic lifeline for themselves, their families, and their communities. The American people are watching once again, and we urge you to take this opportunity to choose a different path,” they wrote.

As Donald Trump begins his second term, America’s healthcare system is in crisis: medical costs are skyrocketing, life expectancy has stagnated, and burnout runs rampant among healthcare workers.

These problems are likely to become worse now that Trump has handed the federal budget over to Elon Musk. The world’s richest man now co-heads the Department of Government Efficiency (DOGE), a non-government entity tasked with slashing $500 billion in “wasteful” spending.

The harsh reality is that Musk’s mission can’t succeed without gutting healthcare access and coverage for millions of Americans.

Deleting dollars from American healthcare

Since Trump’s first term, the country’s economic outlook has worsened significantly. In 2016, the national debt was $19 trillion, with $430 billion allocated to annual interest payments. By 2024, the debt had nearly doubled to $36 trillion, requiring $882 billion in debt service—12% of federal spending that is legally untouchable.

Add to that another 50% of government expenditures that Trump has deemed politically off-limits: Social Security ($1.35 trillion), Medicare ($848 billion) and Defense ($1.13 trillion). That leaves just $2.6 trillion—less than 40% of the $6.75 trillion federal budget—available for cuts.

In a recent op-ed, Musk and DOGE co-chair Vivek Ramaswamy proposed eliminating expired or misused funds for programs like Public Broadcasting and Planned Parenthood, but these examples account for less than $3 billion total—not even 1% of their target.

This shortfall will require Musk to cut billions in government healthcare spending. But where will he find it?

With Medicare off limits to DOGE, the options for major reductions are extremely limited. Big-ticket healthcare items like the $300 billion in tax-deductibility for employer-sponsored health insurance and $120 billion in expired health programs for veterans will prove politically untouchable. One will raise taxes for 160 million working families and the latter will leave veterans without essential medical care.

This means DOGE will have to attack Medicaid and the ACA health exchanges. Here’s how 20 million people will likely lose coverage as a result.

1. Reduced ACA exchange funding

Since its enactment in 2010, the Affordable Care Act (ACA) has provided premium subsidies to Americans earning 100% to 400% of the federal poverty level. For lower-income families, the ACA also offers Cost Sharing Reductions, which help offset deductibles and co-payments that fund 30% of total medical costs per enrollee. Without CSRs, a family of four earning $40,000 could face deductibles as high as $5,000 before their insurance benefits apply.

If Congress allows CSR payments to expire in 2026, federal spending would decrease by approximately $35 billion annually. If that happens, the Congressional Budget Office expects 7 million individuals to drop out of the exchanges. Worse, without affordable coverage alternatives, 4 million families would lose their health insurance altogether.

2. Slashing Medicaid coverage and tightening eligibility

Medicaid currently provides healthcare for over 90 million low-income Americans, including children, seniors and individuals with disabilities. To meet DOGE’s $500 billion goal, several cost-cutting strategies appear likely:

Reversing Medicaid expansion: The ACA expanded Medicaid eligibility to those earning up to 138% of the federal poverty level, reducing the uninsured rate from 16% to 8%. Undoing this expansion would strip coverage from millions in the 40 states that adopted the program.

Imposing work requirements: Proponents argue this could encourage employment, but most Medicaid recipients already work for employers that don’t provide insurance. In reality, work requirements primarily create bureaucratic barriers that disqualify millions of eligible individuals, reducing program costs at the expense of coverage.

Switching to block grants: Unlike the current Medicaid system, which adjusts funding based on need, less-expensive block grants would provide states with fixed allocations. This will, however, force them to cut services and reduce enrollment.

Medicaid currently costs $800 billion annually, with the federal government covering 70%. Reducing enrollment by 10% (9 million people) could save over $50 billion annually, while a 20% reduction (18 million people) could save $100 billion.

Either outcome would devastate families by eliminating access to vital services including prenatal care, vaccinations, chronic disease management and nursing home care. As states are forced to absorb the financial burden, they’ll likely cut education budgets and reduce infrastructure investments.

The first 100 days

The numbers don’t lie: Musk and DOGE could slash Medicaid funding and ACA subsidies to achieve much of their $500 billion target. But the human cost of this approach would be staggering.

Fortunately, there are alternative solutions that would reduce spending without sacrificing quality. Shifting provider payments in ways that reward better outcomes rather than higher volumes, capping drug prices at levels comparable to peer nations, and leveraging generative AI to improve chronic disease management could all drive down costs while preserving access to care.

These strategies address the root causes of high medical spending, including chronic diseases that, if better managed, could prevent 30-50% of heart attacks, strokes, cancers, and kidney failures according to CDC estimates.

Yet, in their pursuit of immediate budgetary cuts, Musk and DOGE have omitted these kinds of reform options. As a result, the health of millions of Americans is at major risk.

The new year dawned on a health insurance industry beset by challenges.

Only 7% of health plan executives view 2024 positively after being hammered by the coronavirus pandemic, regulatory turbulence and rising cost pressures, according to a Deloitte survey.

Costs are spiking, and health insurers remain uncertain how the lingering effects of COVID-19 will impact care utilization. Medicaid redeterminations are rewriting the coverage landscape state by state, while Medicare Advantage — the darling of payers’ business sheets — experiences significant regulatory upheaval.

Meanwhile, 2024 is a presidential election year. That’s adding more political uncertainty into the picture as Washington hammers payers over claims denials and the business practices of pharmacy benefit units.

Here’s what experts see coming down the pike for health insurers this year.

The uninsured rate will go up

The number of Americans without insurance coverage is almost certainly going to rise this year as states overhaul their Medicaid rolls, experts say.

During the pandemic, continuous enrollment protections led a record number of people to enroll in Medicaid. But earlier this year, states resumed checking eligibility for the safety-net program. Around 14.4 million Americans have been removed from Medicaid due to the redeterminations process, many for administrative reasons like incorrect paperwork despite remaining eligible.

“We are going to see an increase in the uninsured rate for children and probably adults as well as a consequence,” said Joan Alker, executive director of the Georgetown University Center for Children and Families.

The question is how big of an increase, experts said. Redeterminations began in April, but lagging information and state differences in data reporting has made it difficult to determine where individuals are turning for coverage, and in what numbers.

Early signs suggest some people losing Medicaid have found plans in the Affordable Care Act exchanges, though it’s probably “a very small percentage,” Alker said. More than 20 million people have signed up for ACA coverage since open enrollment began in November — an all-time high, according to data released by the Biden administration in early January.

Experts say the growth is due in part to redeterminations, along with the effects of more generous federal subsidies. Those subsidies are slated to expire in 2025, meaning ACA enrollment should stay elevated until then.

But it’s unlikely everyone who loses Medicaid will find a home on the marketplaces. The cost of family coverage without an employer remains out of reach for many Americans. It’s also too early to determine how many people terminated from Medicaid have shifted into employer coverage — that data should also emerge as 2024 continues, said Matt Fiedler, a senior fellow with the Brookings Schaeffer Initiative on Health Policy.

Federal regulators have also taken a number of actions to try and curb improper procedural Medicaid losses, like cracking down on states with high levels of child disenrollments. Yet, procedural terminations are unlikely to improve significantly this year, experts said.

“We do see a very hopeful trend” in some states, like Washington and Oregon, embracing longer periods of continuous eligibility, Alker noted.

The government has ramped up ACA marketplace outreach, which — along with macro forces like a strong labor market — are positive signs that individuals no longer eligible for Medicaid may find alternative coverage, whether in the ACA exchanges or through employment.

But “it’s likely we’ll see an increase in the uninsured rate. I think the question is how much,” Fiedler said.

Increasing vigilance around costs

Healthcare costs are projected to grow much faster in 2024 than the historical average, fueled by inflation, supply chain disruption and labor pressures increasing provider wages. Those costs are burdening employers already stressed by worker mental health and deferred preventive screenings that could worsen health conditions down the line.

As a result, employers are investing heavily in mental health and substance use disorder services. Seven out of ten employers say mental healthcare access is a priority in 2024, and employers say they’ll turn to virtual care providers to address the need, according to a Business Group on Health survey.

As a result, employers are increasingly demanding integrated platforms combining different benefits, continuing a pivot away from the point solutions they were deluged with during the pandemic. Payers are racing to meet that need.

This year, UnitedHealthcare plans to integrate more than 20 standalone products into a “supported benefits platform,” said Dan Kueter, CEO of the payer’s employer and individual business, during an investor day in November.

Cigna, which focuses on employer-sponsored plans, plans to add more services to its behavioral health navigator to help employers personalize the platform for their employees this year, said CEO David Cordani during a November earnings call.

For their part, health insurers are likely to raise premiums and combat hospital reimbursement hikes in 2024 to control costs, according to credit rating agency Fitch Ratings.

However, that outlook is complicated by uncertainty around how much elevated care utilization seen in 2023 will continue. Some payers, like UnitedHealth and Humana, are forecasting high utilization, while others like CVS have said they expect it to drop.

More payers might pursue mergers and acquisitions or build out internal musculoskeletal management programs to control costs, said Prateesh Maheshwari, a managing director at venture capital firm Maverick Ventures. Hip and knee surgeries were an oft-cited driver of utilization last year.

Still, publicly traded health insurance companies could see their margins moderately decrease in 2024, Fitch said.

GLP-1 coverage will increase — slowly

Surging demand for GLP-1s means insurance coverage for the drugs is expected to increase next year, putting more stress on the nation’s pressured healthcare payment system. GLP-1s, or glucagon-like peptide-1 drugs, have historically been used to treat diabetes but have shown efficacy in weight loss.

The drugs are exceedingly expensive, butthat hasn’t stopped peoplefrom trying to get theirhands on GLP-1s — off-label or not. TD Cowen predicts GLP-1 sales could reach $102 billion by 2030, with $41 billion of that for obesity.

More private payers are considering covering the drugs next year, though the doors to coverage aren’t being thrown wide open. According to a November survey by the International Foundation of Employee Benefit Plans, while 76% of employers provide GLP-1 drug coverage for diabetes, just 27% provide coverage for weight loss.

Yet, 13% are considering adding coverage for weight loss.

As insurance coverage increases, payers will ensure only eligible patients are accessing the drugs through checks like step therapy, said Nathan Ray, head of healthcare M&A at consultancy West Monroe. As a result, access could remain restricted.

Payers will also tie coverage for GLP-1s to additional behavioral management programs. That trend has proved a gold rush for chronic condition management companies and telehealth providers, which have rushed to stand up new business lines for weight loss that include GLP-1s.

“Things like this, that include the opportunity for medication along with the accompaniment of behavioral change, is where I think the market will go in 2024,” said Heather Dlugolenski, Cigna’s U.S. commercial strategy officer.

Proponents of weight loss medication are also eyeing a potential overturn of the ban on Medicare coverage of weight loss drugs next year. A growing number of lawmakers (and drugmakers standing to profit from Medicare coverage) have come out in support of a bill introduced in 2023 to allow Medicare to cover anti-obesity drugs.

The bill is unlikely to be prioritized given Washington has a lot on its plate during the election year, but passage isn’t out of the realm of possibility, experts said.

Medicare Advantage will continue to grow under Washington’s watchful eye

In MA, the government contracts with private insurers to manage the care of Medicare seniors. MA has become increasingly popular, swelling to cover 31 million people last year — a boon for insurers offering the coverage, which can be twice as profitable for private payers than other types of plans.

As such, MA plans have been advertising heavily, trumpeting their supplemental benefits like gym memberships or subsidized groceries. Seniors find those benefits attractive, Brookings’ Fiedler said, and may not understand that MA plans may not cover as much medical care as traditional Medicare.

”My best bet would be MA enrollment in the near term continues to grow,” Fiedler said. “I don’t think we’re at the ceiling yet.”

Despite elevated costs in 2023 from seniors using more medical care, insurers generally didn’t cut back on plan benefits this year as they continue to compete for members.

Yet, the program hasn’t been without its complications. Payers cried foul last year over tweaks to MA rates, star ratings and reimbursement audits, with Humana and Elevance suing to stop the changes.

MA “should remain a key long-term growth driver for managed care, but we see a more challenging setup in 2024 as weaker funding, risk coding changes, and lower Star ratings combine to pressure margins,” J.P. Morgan analysts wrote in an outlook report published late last year.

Insurers were also plagued in 2023 by congressional hearings and lawsuits over their claims reviews processes, sparking criticism that seniors may not be receiving the care they’re due.

Scrutiny from Washington around such practices is likely to continue.

“We are seeing both in the Senate and House a lot of interest in peeling back the layers of the onion of how big health plans are operating their Medicare Advantage programs. That’s going to continue to be an issue,” said Reed Stephens, a healthcare chair at law firm Winston & Strawn who focuses on risk.

Though it’s unlikely that legislation will be passed reforming MA, Reed said. Overall, regulatory and political turbulence should subside somewhat this year.

The rate and marketing changes were “short of the last train out of the station,” said Brookings’ Fiedler. “The administration is unlikely to want a big fight with MA plans in an election year.”

The Mark Cuban effect: Payers with PBMs will launch more ‘transparent’ options

Major pharmacy benefit managers will introduce more options billed as transparent and cost-effective to retain clients after some turned to upstart competitors last year.

PBM clients are clamoring for outcomes-based pricing, with structures tying PBM compensation to measures like adherence, according to a J.P. Morgan survey from late 2023. Clients also want transparency, whether more data sharing or full administration models.

The changes aren’t revolutionary, but they hint at ongoing distrust of major PBMs from benefits teams, J.P. Morgan said.

UnitedHealth’s Optum Rx, Cigna’s Express Scripts and CVS Caremark — which together control 80% of prescriptions in the U.S. — have all recently launched new programs, partnerships or models they say are more affordable and transparent to meet the demand.

The industry is likely to see more moves along those lines in 2024, experts say — especially as Congress considers legislation to reform PBMs. The Lower Costs, More Transparency Act passed the House in December. The bill is seen as unlikely to clear the Senate, but specific measures, like forced PBM transparency, could make it into larger legislative packages.

The passing of measures around transparency could satisfy politicians’ need for a win when it comes to drug pricing without creating meaningful reform in the sector, according to Jefferies analyst Brian Tanquilut.

Yet, momentum to do something about high drug costs will certainly carry into this year. Presidential candidates on both sides of the aisle are expected to wield the issue on the campaign trail.

“The companies in those markets are going to have to stay nimble and keep on their toes,” said Winston & Strawn’s Stephens.

M&A, especially vertical integration, carries on

Companies like UnitedHealth, CVS and Humana will continue building out networks of physical care sites in 2024. New M&A guidelines from the Department of Justice and Federal Trade Commission could raise the bar for merger approvals, but the value proposition for insurers to acquire healthcare providers is too high for them to be dissuaded, experts said.

Payers will continue to pursue as many deals “as they can find willing, available targets,” said West Monroe’s Ray.

By directing members to owned locations for medical needs, health insurers can essentially pay themselves for providing a service, keeping more revenue in-house. As a result, payers — especially those with a large presence in MA, which incentivizes organizations to better manage cost — will stay on the hunt for acquisition targets.

While healthcare M&A was relatively slow in 2023, 68% of senior leaders in the sector expect deal volume to rise in 2024, according to a survey by investment bank Jefferies.

Optum — which employs or is affiliated with around one-tenth of all doctors in the U.S. — is already eyeing M&A. The health services arm of UnitedHealth is currently pursuing an acquisition of a physician-owned clinic chain in Oregon, even as it comes off a number of big provider buys in 2023, including the multi-billion-dollar acquisitions of home health providers Amedisys and LHC Group.

Cigna has also said it plans to look for smaller strategic acquisitions to grow its business, after a potential merger with rival Humana crumbled late last year.

Albert Einstein determined that time is relative. And when it comes to healthcare, five years can be both a long and a short amount of time.

In August 2018, I launched the Fixing Healthcare podcast. At the time, the medium felt like the perfect auditory companion to the books and articles I’d been writing. By bringing on world-renowned guests and engaging in difficult but meaningful discussions, I hoped the show would have a positive impact on American medicine. After five years and 100 episodes, now is an opportune time to look back and examine how healthcare has improved and in what ways American medicine has become more problematic.

Here’s a look at the good, the bad and the ugly since episode one of Fixing Healthcare:

The Good

Drug breakthroughs and government actions headline medicine’s biggest wins over the past five years.

At first, health experts expressed doubts that Pfizer, Moderna and others could create a safe and effective Covid-19 vaccine with messenger RNA (mRNA) technology. After all, no one had succeeded in more than two decades of trying.

Thanks in part to Operation Warp Speed, the government-funded springboard for research, our nation produced multiple vaccines within less than a year. Previously, the quickest vaccine took four years to develop (mumps). All others required a minimum of five years.

The vaccines were pivotal in ending the coronavirus pandemic, and their success has opened the door to other life-saving drugs, including those that might prevent or fight cancer. And, of course, our world is now better prepared for when the next viral pandemic strikes.

Weight-Loss Drugs

Originally designed to help patients manage Type 2 diabetes, drugs like Ozempic have been helping people reverse obesity—a condition closely correlated with diabetes, heart disease and cancer.

For decades, America’s $150 billion a year diet industry has failed to curb the nation’s continued weight gain. So too have calls for increased exercise and proper nutrition, including restrictions on sugary sodas and fast foods.

In contrast, these GLP-1 medications are highly effective. They help overweight and obese people lose 15 to 25 pounds on average with side effects that are manageable for nearly all users.

The biggest stumbling block to their widespread use is the drug’s exorbitant price (upwards of $16,000 for a year’s supply).

Drug-Pricing Laws

With the Inflation Reduction Act of 2022, Congress took meaningful action to lower drug prices, a move the CBO estimates would reduce the federal deficit by $237 billion over 10 years.

It’s a good start. Americans today pay twice as much for the same medications as people in Europe largely because of Congressional legislation passed in 2003.

That law, the Medicare Prescription Drug Price Negotiation Act, made it illegal for Health and Human Services (HHS) to negotiate drug prices with manufacturers—even for the individuals publicly insured through Medicare and Medicaid.

Now, under provisions of the new Inflation Reduction Act, the government will be able to negotiate the prices of 10 widely prescribed medications based on how much Medicare’s Part D program spends. The lineup is expected to include prescription treatments for arthritis, cancer, asthma and cardiovascular disease. Unfortunately, the program won’t take effect until 2026. And as of now, several legal challenges from both drug manufacturers and the U.S. Chamber of Commerce are pending.

The Bad

Spiking costs, ongoing racial inequalities and millions of Americans without health insurance make up three disappointing healthcare failures of the past five years.

Cost And Quality

The U.S. spends nearly twice as much on healthcare per citizen as other countries, yet our nation lags 10 of the wealthiest countries in medical performance and clinical outcomes. As a result, Americans die younger and experience more complications from chronic diseases than people in peer nations.

As prices climb ever-higher, at least half of Americans can’t afford to pay their out-of-pocket medical bills, which remain the leading cause of U.S. bankruptcy. And with rising insurance premiums alongside growing out-of-pocket expenses, more people are delaying their medical care and rationing their medications, including life-essential drugs like insulin. This creates a vicious cycle that will likely prolong today’s healthcare problems well into the future.

Health Disparities

Inequalities in American medicine persist along racial lines—despite action-oriented words from health officials that date back decades.

Today, patients in minority populations receive unequal and inequitable medical treatment when compared to white patients. That’s true even when adjusting for differences in geography, insurance status and socioeconomics.

Racism in medical care has been well-documented throughout history. But the early days of the Covid-19 pandemic provided several recent and deadly examples. From testing to treatment, Black and Latino patients received both poorer quality and less medical care, doubling and even tripling their chances of dying from the disease.

The problems can be observed across the medical spectrum. Studies show Black women are still less likely to be offered breast reconstruction after mastectomy than white women. Research also finds that Black patients are 40% less likely to receive pain medication after surgery. Although technology could have helped to mitigate health disparities, our nation’s unwillingness to acknowledge the severity of the problem has made the problem worse.

Uninsurance

Although there are now more than 90 million Americans enrolled in Medicaid, there are still 30 million people without any health insurance. This disturbing reality comes a full decade after the passage of the Affordable Care Act.

On Capitol Hill, there is no plan in place to reduce the number of uninsured.

Moreover, many states are looking to significantly rollback their Medicaid enrollment in the post-Covid era. Kaiser Family Foundation estimates that between 8 million and 24 million people will lose Medicaid coverage during the unwinding of the continuous enrollment provisions implemented during the pandemic. Without coverage, people have a harder time obtaining the preventive services they need and, as a result, they suffer more chronic diseases and die younger.

The Ugly

An overall decrease in longevity, along with higher maternal mortality and a worsening mental-health crisis, comprise the greatest failures of U.S. healthcare over the past five years.

Life Expectancy

Despite radical advances in medical science over the past five years, American life expectancy is back to where it was at the turn of the 20th century, according to CDC data.

Alongside environmental and social factors are a number of medical causes for the nation’s dip in longevity. Research demonstrated that many of the 1 million-plus Covid-19 deaths were preventable. So, too, was the nation’s rise in opioid deaths and teen suicides.

Regardless of exact causation, Americans are living two years less on average than when we started the Fixing Healthcare podcast five years ago.

Maternal Mortality

Compared to peer nations, the United States is the only country with a growing rate of mothers dying from childbirth. The U.S. experiences 17.4 maternal deaths per 100,000 live births. In contrast, Norway is at 1.8 and the Netherlands at 3.0.

The risk of dying during delivery or in the post-partum period is dramatically higher for Black women in the United States. Even when controlling for economic factors, Black mothers still suffer twice as many deaths from childbirth as white women.

And with growing restrictions on a woman’s right to choose, the maternal mortality rate will likely continue to rise in the United States going forward.

Mental Health

Finally, the mental health of our country is in decline with rates of anxiety, depression and suicide on the rise.

These problems were bad prior to Covid-19, but years of isolation and social distancing only aggravated the problem. Suicide is now a leading cause of death for teenagers. Now, more than 1 in every 1,000 youths take their own lives each year. The newest data show that suicides across the U.S. have reached an all-time high and now exceed homicides.

Even with the expanded use of telemedicine, mental health in our nation is likely to become worse as Americans struggle to access and afford the services they require.

The Future

In looking at the three lists, I’m reminded of a baseball slugger who can occasionally hit awe-inspiring home runs but strikes out most of the time. The crowd may love the big hitter and celebrate the long ball, but in both baseball and healthcare, failing at the basics consistently results in more losses than wins.

Over the past five years, American medicine has produced a losing record. New drugs and surgical breakthroughs have made headlines, but the deeper, more systemic failures of American healthcare have rarely penetrated the news cycle.

If our nation wants to make the next five years better and healthier than the last five, elected officials and healthcare leaders will need to make major improvements. The steps required to do so will be the focus of my next article.

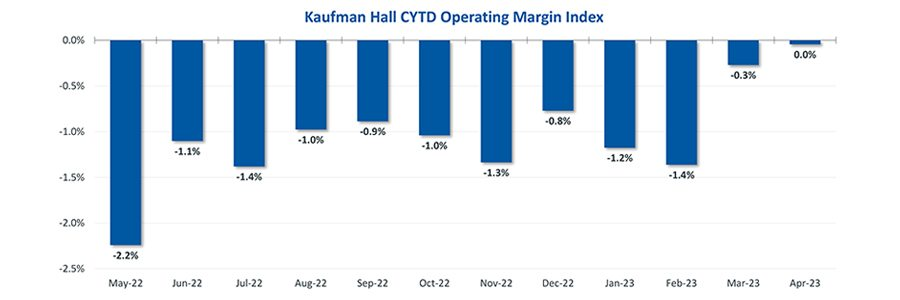

Hospital finances showed signs of stabilizing in May amid slightly improving operating margins, declining expenses and notable increases in outpatient visits.

The median Kaufman Hall Year-To-Date Operating Margin Index reflecting actual margins was 0.3% in May.

The National Hospital Flash Report uses both actual and budget data over the last three years, sampled from more than 900 hospitals on a recurring monthly basis from Syntellis Performance Solutions.

The sample of hospitals for this report is representative of all hospitals in the United States both geographically and by bed size. Additionally, hospitals of all types are represented, from large academic to small critical access. Advanced statistical techniques are used to standardize data, identify and handle outliers, and ensure statistical soundness prior to inclusion in the report.

While this report presents data in the aggregate, Syntellis Performance Solutions also has real-time data down to individual department, jobcode, paytype, and account levels, which can be customized into peer groups for unparalleled comparisons to drive operational decisions and performance improvement initiatives.

Key Takeaways

Hospitals broke even in April. The median operating margin for hospitals was 0% in April, leaving most hospitals with little to no financial wiggle room.

Volumes dropped while lengths of stay increased. Hospital volumes dropped across the board—including inpatient and outpatient. Emergency department volumes were the least affected.

Effects of Medicaid disenrollment could be materializing. Hospitals experienced increases in bad debt and charity care in April. Combined with anemic patient volumes, experts note this data could illustrate the effects of the start of widespread disenrollment from Medicaid following the end of the COVID-19 public health emergency.

Inflation continued to throttle hospital finances. Labor costs jumped in April and the costs of goods and services continued to be well above pre-pandemic levels. Though expenses generally fell in April, revenues declined at a faster rate.

National Non-Operating Results

Key Observations

At their May meeting, the Federal Open Market Committee (FOMC) raised the benchmark borrowing rate another 25 basis points, setting the range to 5.00-5.25% and marking the 10th consecutive hike in the cycle as well as a 16-year high

Fed officials acknowledged discussion of a potential pause in tightening while leaving wiggle room, saying “rates are going to come down” over a long period of time while also warning inflation “continues to run high” and the Fed will be taking a “data-dependent approach”

The consumer price index (CPI) rose 0.4% in April, a 4.9% increase year-over-year, an annual pace of inflation below 5% for the first time in two years

The labor market continued to show resilience in April as U.S. nonfarm payrolls grew by 253,000 and unemployment fell back to a 53-year low of 3.4%

Strong inflation, a robust labor market, continued banking sector woes, and a debt ceiling standoff further complicates credit conditions and may challenge the Fed to stabilize financial markets

Equities in April, as measured by the S&P 500, were up 1.5% in April and 8.6% YTD despite downbeat economic data, reoccurring banking sector fears, and mixed earnings

On April 1st, Medicaid’s pandemic-era continuous enrollment policy began to sunset, kicking off a 14-month window for states to reassess their Medicaid rolls. In this week’s graphic, we highlight new Congressional Budget Office projections showing the impact of Medicaid redeterminations on insurance coverage rates over the next decade for the under-65 population.

The Medicaid and Children’s Health Insurance Program (CHIP) coverage rate is expected to drop from 31 percent of all Americans under 65 in 2023, to 27 percent in 2024.

Meanwhile, after reaching an all-time low in 2023,the under-65 uninsured rate is projected to surpass nine percent in 2024 and climb to over 10 percent by 2033.

While over 15M Americans are expected to lose Medicaid coverage during redeterminations, a majority of those disenrolled will gain health insurance either through an employer-sponsored or non-group plan.

But over 6M people, nearly 40 percent of those losing Medicaid coverage, are projected to become uninsured, erasing nearly half the progress the country has made since 2019 at lowering the uninsured rate.

Last week, Marlee Stark and I published an op-ed in the Arkansas Democrat Gazette on why the Arkansas Department of Human Services (DHS) should press pause on its Medicaid unwinding process. Earlier this month, DHS released its first report laying out how many people lost coverage in April, as the state resumed its redetermination process.

As we write,

According to DHS’ recent report, over 50,000 people were disenrolled for procedural reasons, like failure to return paperwork or requested information, or because the state didn’t have their correct address on file. Only 15 percent of those who were disenrolled were confirmed truly ineligible or said they no longer needed their coverage, likely because they acquired another source of coverage during the pandemic.

In our piece, we argue that DHS should take a look at why so many people are losing coverage even though they may still be eligible—and outline some of the consequences the state may face if it chooses not to do so.

A surge in the uninsured population from Medicaid redetermination could swamp some health systems that struggled to stay afloat during the pandemic. But experts say it could also translate into a financial boost for networks, if enough individuals find new sources of coverage.

Why it matters:

Even the temporary loss of coverage as states unwind their COVID-era Medicaid enrollment requirements means more people will go without checkups and other primary care, increasing the likelihood they’ll wait until they’re sick to seek help.

A key question is how many of the disenrolled will find new arrangements through workplace insurance or subsidized Affordable Care Act plans, both of which pay providers at higher rates than Medicaid.

Driving the news:

More than 170,000 people lost their Medicaid coverage in four states in April, and it’s not clear from state data how many of those people found new arrangements, reapplied successfully for Medicaid or remain uninsured.

An estimated 17 million children and adults could lose Medicaid coverage this year, after pandemic-era protections are rolled back, per a recent KFF survey.

Trinity Health, an 88-hospital health system operating in 26 states, estimates that Medicaid redetermination could result in a loss of $70 million to $90 million if disenrolled people don’t find other arrangements and the system has to provide them with charity care.

“It’s painful to watch; it’s not good for people and for our communities and those who are most vulnerable,” Dan Roth, chief clinical officer at Trinity Health, told Axios.

Emergency departments could fill up quickly if enough people who delay care wait for a health crisis to get help, said Ben Finder, director of policy research and analysis at the American Hospital Association.

He said other patients could cut pills in half or otherwise make medications last longer, “which can create cascading problems for folks.”

What we’re watching:

Redeterminations could change the payer mix in a revenue-positive way if patients go from Medicaid to employer-sponsored or ACA plans.

One Urban Institute report estimates that as many as 10.5 million patients could shift from Medicaid to employer-sponsored coverage or a marketplace plan.

This could boost payments to hospitals significantly, per Duane Wright, a Bloomberg Intelligence analyst, since commercial payment rates for hospital services are on average 223% higher than Medicare payments.

Zoom in:

Providers might be the first ones to inform patients who don’t know that their coverage has been terminated when they come in seeking care.

Health systems can create special teams to proactively reach out to Medicaid patients before they even come to the hospital, said Karen Shields, chief client engagement officer at Gainwell and former deputy director at the Centers for Medicare and Medicaid Services.

“There is a moral and financial imperative for us to be good at this,” Shields told Axios.

The bottom line:

Most health systems have bounced back from a shaky 2022. But redeterminations, combined with inflation, supply chain problems and staffing shortages, could prove too much, especially during the colder months when respiratory viruses proliferate.

“Everyone is holding their breath watching for how this unfolds in each state,” Finder told Axios.

April 1st marked the start date of a one-year window for state Medicaid offices to reassess their beneficiary rolls, as Medicaid’s continuous enrollment policy sunsets. Since the early days of the pandemic, the federal government has boosted state Medicaid funding by 6.2 percent, in exchange for a requirement that current Medicaid beneficiaries maintain eligibility, regardless of changes to their income or other qualifiers. This policy helped grow national Medicaid enrollment to a record 90M, but a projected 15M may now lose coverage through the redetermination process.

The Gist: After the US uninsured rate recently hit a record low, millions of Americans will now lose insurance coverage, at least temporarily.Of those no longer eligible for Medicaid, an estimated 2.7M will qualify for subsidized exchange plans, while around 400K in non-expansion states will have incomes too high for Medicaid and too low for exchange subsidies. The impact will vary in each state, both in terms of how quickly and how many Medicaid beneficiaries are disenrolled.

But in over half of states,at least one-fifth of those who will lose Medicaid coverage are projected to remain uninsured—a significant step backward in the effort to ensure universal coverage.

Communication from Medicaid offices and exchange plan navigators will be key to preventing as many people as possible from becoming uninsured.

Researchers estimate 15 million people will lose their Medicaid starting April 1 when states begin removing people from the low-income health insurance program for the first time in three years.

In March 2020, Congress banned states from removing people from Medicaid during the pandemic in exchange for more federal funding for state Medicaid programs. Medicaid enrollment is usually tied to people’s incomes, and individuals normally have to regularly prove they still qualify in what’s known as a redetermination. (In the 39 states and Washington, D.C., that have expanded Medicaid, a family of four has to make less than $40,000 to qualify. In non-expansion states, the cutoff is even lower.)

With redeterminations paused, Medicaid enrollment nationwide has grown from 71 million in February 2020 to an estimated 95 million in March 2023.Research shows Medicaid coverage is associated with better access to care, more financial security, better health and lower mortality. During the pandemic, beneficiaries have been able to enjoy these benefits without worrying about confirming their eligibility.

In December, Congress voted to let states restart the process of clearing their rolls on April 1, what’s sometimes referred to as “unwinding.”Lawmakers are giving states 14 months to redetermine millions of people’s eligibility — an unprecedented task made even more difficult by serious staffing and experience shortages in many Medicaid offices.

“It’s going to be a big lift,” said Sayeh Nikpay, a health policy researcher at the University of Minnesota and Tradeoffs Senior Research Advisor. “States have never had to do this many redeterminations this quickly before, and there’s a lot of uncertainty about what will happen.”

We asked Nikpay to pick out a few relevant studies to help us understand what is happening and how states and employers could keep more people insured. Here are three she identified as particularly helpful.

Two types of people will lose coverage

The Office of the Assistant Secretary for Planning and Evaluation, which provides research for the U.S. Department of Health and Human Services, released a report in August 2022 that estimated 15 million people will lose Medicaid coverage as a result of the unwinding. (The estimate is similar to another analysis by the independent Urban Institute.)

ASPE breaks those 15 million people into two groups. In the first group are people who make too much money to qualify for Medicaid. ASPE estimates there are about 8 million people in that category, and they should be able to get insurance through work or the Obamacare exchanges.

In the second group are roughly 7 million people ASPE estimates are still eligible but will lose coverage because of what’s called “administrative churn.”This can happen if the Medicaid office can’t get in touch with someone to confirm their eligibility because they’ve moved or changed their phone number or if they’re unable to make an in-person appointment because of work or child care responsibilities. (The Urban Institute projects about 4 million people will be in this group.)

These two groups represent a key tension to the unwinding process: States want to shed people who make too much money, but officials also know eligible people often lose coverage during redeterminations, and that danger is heightened given the scale and speed of this process.

Making the switch from Medicaid to private insurance

This next paper looks at the first group: the roughly 8 million people expected to move from Medicaid to private coverage, and specifically the roughly 4 million who are expected to get coverage through the Obamacare exchanges. Adrianna McIntyre, an assistant professor of health policy at Harvard, wrote in JAMA Health Forum in October 2022 about the most effective ways to move people from Medicaid onto private Obamacare plans.

There’s limited data on this, but based on the few studies available, McIntyre found that only 3 to 5 percent of people who leave Medicaid end up getting an Obamacare plan. Many policymakers are relying on the Obamacare exchanges to provide a life preserver to millions of people losing Medicaid coverage, but the research cited by McIntyre shows getting people into these plans is not guaranteed and will take focused effort by states.

McIntyre’s review cites several randomized controlled trials where states tested different ways of increasing enrollment in Obamacare plans. These studies found simple reminders from the state – like physical letters, emails and phone calls help – boost sign-ups anywhere from 7 to 16 percent.

But what really seems to make a difference is reminders plus connecting people to someone who can get them signed up while they are on the phone. In one of those trials published in 2022, people in California who got a reminder email and a call connecting them to enrollment assistance were almost 50% more likely to sign up for a plan. Such extra effort is obviously costly, and it may not be a priority or financially feasible for some states.

McIntyre’s review did not include any research on what employers can do to help their workers transition from Medicaid to work-based coverage, but based on the studies McIntyre cited, Nikpay said she thinks it’s a good idea for employers to make sure people know Medicaid could be going away and provide as much help as possible in getting new coverage.

Making it easier to stay on Medicaid can have other benefits

The final study looks at the second group of people expected to lose Medicaid coverage: the 7 million people who may lose coverage due to administrative churn even though they are still eligible.

Some states have tried to limit that churn, and researchers at the RAND Corporation evaluated New York’s effort. Starting in 2014, New York allowed people to stay on Medicaid without any redeterminations for 12 months once enrolled.

In addition to keeping more people on Medicaid for longer, researchers found that after this policy was in place, hospital admissions and monthly costs per beneficiary went down. The researchers can’t say whether the continuous enrollment policy directly caused these improved outcomes, but the findings suggest that avoiding administrative churn can help people stay covered without ballooning costs.

“It seems reasonable to me,” Nikpay said of the findings, “that making it easier to stay on Medicaid, even outside of a global pandemic, could benefit people’s health given what we know about how Medicaid affects people.”