A few weeks ago The Commonwealth Fund, a philanthropic organization in New York City, which keeps tabs on health care trends, released an ominous study signaling that the bedrock of the U.S. health system is in trouble.

The study found that the employer insurance market, where millions of Americans have received good, affordable coverage since the end of World War II, could be in jeopardy. The continuing rise in the costs of medical care, and the insurance premiums to pay for it, may well cause employers to make cutbacks, leaving millions of workers uninsured or underinsured, often with no way to pay for their care and the prospect of debt for the rest of their lives.

Indeed the Fund revealed that 23% of adults in the U.S. are underinsured, meaning that though they were covered by health insurance, high deductibles and coinsurance made it difficult or impossible to pay for the care they needed.

“They have health plans that don’t provide affordable access to care,” said Sara Collins, senior adviser and vice president at the Fund. “They have out-of-pocket costs and deductibles that are high relative to their income.”

This predicament has forced many to assume medical debt or skip needed care. The Fund found that as many as one-third of people with chronic conditions like heart failure and diabetes reported they don’t take their medication or fill prescriptions because they cost too much.

Others did not go to a doctor when they were sick, skipping a recommended follow-up visit or test, and did not see a specialist when one was recommended. Nearly half of the respondents reported they did not get care for an ongoing condition because of the cost. Two out of five working-age adults who reported a delay or skipped care told researchers their health problem had gotten worse. Those findings belie the narrative, deployed when changes to the system are discussed, that America has the best health care in the world, and we dare not change it.

The seeds of today’s underinsurance predicament were planted in the 1990s when the system’s players decided remedies were needed to curb Americans’ appetite for medical interventions.

They devised managed care, with its HMOs, PPOs, insurance company approvals, and other restrictions that are with us today. But health care is far more expensive than it was in the ’90s, leaving patients to struggle to pay the higher prices, or, as the study shows, go without needed care.

Perhaps one of the study’s most striking findings is that a vast majority of underinsured workers had employer insurance plans, which over the decades had provided good coverage. Researchers concluded that recent cost containment measures were simply shifting more costs to workers through higher deductibles and coinsurance.

I checked in with Richard Master, the CEO of MCS Industries in Easton, Pennsylvania. We’ve talked over the years about the rising cost of health insurance for his 91 workers who make picture frames and wall decorations. This year, he was expecting a 5 to 6% increase in insurance rates.

A family plan now costs more than $39,000, he said, adding that “29% of people with employee plans are underinsured and have high out-of-pocket costs.”

To help reduce his own costs, he told me he has put in place a high-deductible plan and was setting up health saving accounts that allow him to give a sum of money to each worker to use for their medical expenses.

As health insurance premiums continue to rise, more employers will likely heap more of those rising costs onto workers, many of whom will inevitably have a tough time paying for them.

Every time there has been a hint in the air that maybe, just maybe, America might embrace a universal system like peer nations across the globe that offer health care to all their citizens, the special interests—doctors, hospitals, insurers, employers, and others that benefit financially from the current system have snuffed out any possibility that might happen, worried that such a system could affect their profits.

For as long as I can remember, the public has been told America has the best health care system in the world. Major holes in our system exposed by The Commonwealth Fund belie that assumption.

In late 2025, two events reset the U.S. health system’s future at least through 2026 and possibly beyond:

November 5, 2024: The Election: Its post-mortem by pollsters and pundits reflects a country divided and unsettled: 22 Red States, 7 Swing States and 21 Blue States. But a solid majority who thought the country was heading in the wrong direction and their financial insecurity driving voters to return the 45th President to the White House. With slim majorities in the House and Senate, and a short-leash before mid-term elections November 3, 2026, the Trump team has thrown out ‘convention’ in their setting policies and priorities for their second term. That includes healthcare.

December 4, 2024: The Murder of a Health Executive : The murder of Brian Thompson, United Healthcare CEO, sparked hostility toward health insurers and a widespread backlash against the corporatization of the U.S. health system. While UHG took the most direct hit for its aggressiveness in managing access and coverage disputes, social media and mainstream journalists exposed what pollsters affirmed—the majority of American’s distrust the health system, believing it puts its profits above their needs. And their polls indicate animosity is highest among young adults, in lower income households and among members of its own workforce.

These events provide the backdrop for what to expect this year and next. Four directional shifts seem to underly actions to date and announced plans:

From elitism to populism: Key personnel and policy changes will draw less from Ivy League credentials, DC connections and recycled federal health agency notables and more from private sector experience, known disruptors and unconventional thought leaders. Notably, the new Chairs of the 7 Congressional Committees that control healthcare regulation, funding and policy changes in the 119th Congress represent LA, AL, WV, ID, VA, MO & KY constituents—hardly Ivy League territory.

From workforce disparities to workforce modernization: The Departments of Health & Human Services, Labor, Commerce and Treasury will attempt to suspend/modify regulatory mandates and entities they deem derived from woke ideology. The Trump team will replace them with policies that enable workforce de-regulation and modernization in the private sector. Hiring quotas, non-compete contracts, DEI et al will get a fresh look in the context of technology-enabled workplaces and supply-demand constraints. The HR function in every organization will become ground zero for Trump Healthcare 2.0 system transformation.

From western medicine to whole person wellbeing: HHS Secretary Nominee Robert F. Kennedy Jr. (RFK) Jr.’s “Make America Healthy Again” pledges war on ultra-processed foods. CMS’ designee Mehmet Oz advocates for vitamins, supplements and managed care. FDA nominee Marty Makary, a Hopkins surgeon, is a RFKJ ally in the “Health Freedom” movement promoting suspicion about ‘mainstream medicine’ and raising doubts about vaccination efficacy for children and low-risk adults. NIH nominee Jay Bhattacharya, director of Stanford’s Center for Demography and Economics of Health and Aging, opposed Covid-19 lockdowns and is critical of vaccine policies. Collectively, this four-some will challenge conventional western (allopathic) medicine and add wide-range of non-traditional interventions that are a safe and cost-effective to the treatment arsenal for providers and consumers. The food supply will be a major focus: HHS will work closely with the USDA (nominee Brooke Rollins, currently CEO of the America First Policy Institute, to reduce the food chain’s dependence on ultra-processed foods in public health.

From DC dominated health policies to states: The 2022 Supreme Court’ Dobbs decision opened the door for states to play the lead role in setting policies for access to abortion for their female citizens. It follows federalism’s Constitutional preference that Washington DC’s powers over states be enumerated and limited. Thus, state provisions about healthcare services for its citizens will expand beyond their already formidable scope. Likely actions in some states will include revised terms and conditions that facilitate consolidation, allowance for physician owned hospitals and site-neutral payments, approval of “skinny” individual insurance policies that do not conform to the Affordable Care Act’s qualified health plan spec’s, expanded scope of practice for nurse practitioners, drug price controls and many others. At least for the immediate future, state legislatures will be the epicenters for major policy changes impacting healthcare organizations; federal changes outside appropriations activity are unlikely.

Transforming the U.S. health system is a bodacious ambition for the incoming Trump team. Early wins will be key—like expanding price transparency in every healthcare sector, softening restrictions on private equity investments, targeted cuts in Medicaid and Medicare funding and annulment of the Inflation Reduction Act. In tandem, it has promised to cut Federal government spending by $2 trillion and lower prices on everything including housing and healthcare—the two spending categories of highest concern to the working class. Healthcare will figure prominently in Team Trump’s agenda for 2025 and posturing for its 2026 mid-term campaign. And equally important, healthcare costs also figure prominently in quarterly earnings reports for companies that provide employee health benefits forecast to be 8% higher this year following a 7% spike the year prior. Last year’s 23% S&P growth is not expected to repeat this year raising shareholder anxiety and the economy’s long-term resilience and the large roles housing and healthcare play in its performance.

My take:

The 2024 election has been called a change election. That’s unwelcome news to most organizations in healthcare, especially the hospitals, physicians, post-acute providers and others who provide care to patients and operate at the bottom of the healthcare pyramid.

Equipping a healthcare organization to thoughtfully prepare for changes amidst growing uncertainty requires extraordinary time and attention by management teams and their Boards. There are no shortcuts. Before handicapping future state scenario possibilities, contingencies and resource requirements, a helpful starting point is this: On the four most pressing issues facing every U.S. healthcare company/organization today, Boards and Management should discuss…

Trust: On what basis can statements about our performance be verified? Is the data upon which our trust is based readily accessible? Does the organization’s workforce have more or less trust than outside stakeholders? What actions are necessary to strengthen/restore trust?

Purpose: Which stakeholder group is our organization’s highest priority? What values & behaviors define exceptional leadership in our organization? How are they reflected in their compensation?

Affordability: How do we measure and monitor the affordability of our services to the consumers and households we ultimately depend? How directly is our organization’s alignment of reducing cost reduction and pass-through savings to consumers? Is affordability a serious concern in our organization (or just a slogan)?

Scale: How large must we be to operate at the highest efficiency? How big must we become to achieve our long-term business goals?

This week, thousands of healthcare’s operators will be in San Francisco (JPM Healthcare Conference), Naples (TGI Leadership Conference) and in Las Vegas (Consumer Electronics Show) as healthcare begins a new year. No one knows for sure what’s ahead or who the winners and losers will be. What’s for sure is that healthcare will be in the spotlight and its future will not be a cut and paste of its past.

PS: The parallels between radical changes facing the health system and other industries is uncanny. College athletics is no exception. As you enjoy the College Football Final Four this weekend, consider its immediate past—since 2021, the impact of Name, Image and Likeness (NIL) monies on college athletics, and its immediate future–pending regulation that will codify permanent revenue sharing arrangements (to be implemented 2026-2030) between college athletes, their institutions and sponsors. What happened to the notion of student athlete and value of higher education? Has the notion of “not-for-profit” healthcare met a similar fate? Or is it all just business?

In late 2025, two events reset the U.S. health system’s future at least through 2026 and possibly beyond:

November 5, 2024: The Election: Its post-mortem by pollsters and pundits reflects a country divided and unsettled: 22 Red States, 7 Swing States and 21 Blue States. But a solid majority who thought the country was heading in the wrong direction and their financial insecurity driving voters to return the 45th President to the White House. With slim majorities in the House and Senate, and a short-leash before mid-term elections November 3, 2026, the Trump team has thrown out ‘convention’ in their setting policies and priorities for their second term. That includes healthcare.

December 4, 2024: The Murder of a Health Executive : The murder of Brian Thompson, United Healthcare CEO, sparked hostility toward health insurers and a widespread backlash against the corporatization of the U.S. health system. While UHG took the most direct hit for its aggressiveness in managing access and coverage disputes, social media and mainstream journalists exposed what pollsters affirmed—the majority of American’s distrust the health system, believing it puts its profits above their needs. And their polls indicate animosity is highest among young adults, in lower income households and among members of its own workforce.

These events provide the backdrop for what to expect this year and next. Four directional shifts seem to underly actions to date and announced plans:

From elitism to populism: Key personnel and policy changes will draw less from Ivy League credentials, DC connections and recycled federal health agency notables and more from private sector experience, known disruptors and unconventional thought leaders. Notably, the new Chairs of the 7 Congressional Committees that control healthcare regulation, funding and policy changes in the 119th Congress represent LA, AL, WV, ID, VA, MO & KY constituents—hardly Ivy League territory.

From workforce disparities to workforce modernization: The Departments of Health & Human Services, Labor, Commerce and Treasury will attempt to suspend/modify regulatory mandates and entities they deem derived from woke ideology. The Trump team will replace them with policies that enable workforce de-regulation and modernization in the private sector. Hiring quotas, non-compete contracts, DEI et al will get a fresh look in the context of technology-enabled workplaces and supply-demand constraints. The HR function in every organization will become ground zero for Trump Healthcare 2.0 system transformation.

From western medicine to whole person wellbeing: HHS Secretary Nominee Robert F. Kennedy Jr. (RFK) Jr.’s “Make America Healthy Again” pledges war on ultra-processed foods. CMS’ designee Mehmet Oz advocates for vitamins, supplements and managed care. FDA nominee Marty Makary, a Hopkins surgeon, is a RFKJ ally in the “Health Freedom” movement promoting suspicion about ‘mainstream medicine’ and raising doubts about vaccination efficacy for children and low-risk adults. NIH nominee Jay Bhattacharya, director of Stanford’s Center for Demography and Economics of Health and Aging, opposed Covid-19 lockdowns and is critical of vaccine policies. Collectively, this four-some will challenge conventional western (allopathic) medicine and add wide-range of non-traditional interventions that are a safe and cost-effective to the treatment arsenal for providers and consumers. The food supply will be a major focus: HHS will work closely with the USDA (nominee Brooke Rollins, currently CEO of the America First Policy Institute, to reduce the food chain’s dependence on ultra-processed foods in public health.

From DC dominated health policies to states: The 2022 Supreme Court’ Dobbs decision opened the door for states to play the lead role in setting policies for access to abortion for their female citizens. It follows federalism’s Constitutional preference that Washington DC’s powers over states be enumerated and limited. Thus, state provisions about healthcare services for its citizens will expand beyond their already formidable scope. Likely actions in some states will include revised terms and conditions that facilitate consolidation, allowance for physician owned hospitals and site-neutral payments, approval of “skinny” individual insurance policies that do not conform to the Affordable Care Act’s qualified health plan spec’s, expanded scope of practice for nurse practitioners, drug price controls and many others. At least for the immediate future, state legislatures will be the epicenters for major policy changes impacting healthcare organizations; federal changes outside appropriations activity are unlikely.

Transforming the U.S. health system is a bodacious ambition for the incoming Trump team. Early wins will be key—like expanding price transparency in every healthcare sector, softening restrictions on private equity investments, targeted cuts in Medicaid and Medicare funding and annulment of the Inflation Reduction Act. In tandem, it has promised to cut Federal government spending by $2 trillion and lower prices on everything including housing and healthcare—the two spending categories of highest concern to the working class. Healthcare will figure prominently in Team Trump’s agenda for 2025 and posturing for its 2026 mid-term campaign. And equally important, healthcare costs also figure prominently in quarterly earnings reports for companies that provide employee health benefits forecast to be 8% higher this year following a 7% spike the year prior. Last year’s 23% S&P growth is not expected to repeat this year raising shareholder anxiety and the economy’s long-term resilience and the large roles housing and healthcare play in its performance.

My take:

The 2024 election has been called a change election. That’s unwelcome news to most organizations in healthcare, especially the hospitals, physicians, post-acute providers and others who provide care to patients and operate at the bottom of the healthcare pyramid.

Equipping a healthcare organization to thoughtfully prepare for changes amidst growing uncertainty requires extraordinary time and attention by management teams and their Boards. There are no shortcuts. Before handicapping future state scenario possibilities, contingencies and resource requirements, a helpful starting point is this: On the four most pressing issues facing every U.S. healthcare company/organization today, Boards and Management should discuss…

Trust: On what basis can statements about our performance be verified? Is the data upon which our trust is based readily accessible? Does the organization’s workforce have more or less trust than outside stakeholders? What actions are necessary to strengthen/restore trust?

Purpose: Which stakeholder group is our organization’s highest priority? What values & behaviors define exceptional leadership in our organization? How are they reflected in their compensation?

Affordability: How do we measure and monitor the affordability of our services to the consumers and households we ultimately depend? How directly is our organization’s alignment of reducing cost reduction and pass-through savings to consumers? Is affordability a serious concern in our organization (or just a slogan)?

Scale: How large must we be to operate at the highest efficiency? How big must we become to achieve our long-term business goals?

This week, thousands of healthcare’s operators will be in San Francisco (JPM Healthcare Conference), Naples (TGI Leadership Conference) and in Las Vegas (Consumer Electronics Show) as healthcare begins a new year. No one knows for sure what’s ahead or who the winners and losers will be. What’s for sure is that healthcare will be in the spotlight and its future will not be a cut and paste of its past.

PS: The parallels between radical changes facing the health system and other industries is uncanny. College athletics is no exception. As you enjoy the College Football Final Four this weekend, consider its immediate past—since 2021, the impact of Name, Image and Likeness (NIL) monies on college athletics, and its immediate future–pending regulation that will codify permanent revenue sharing arrangements (to be implemented 2026-2030) between college athletes, their institutions and sponsors. What happened to the notion of student athlete and value of higher education? Has the notion of “not-for-profit” healthcare met a similar fate? Or is it all just business?

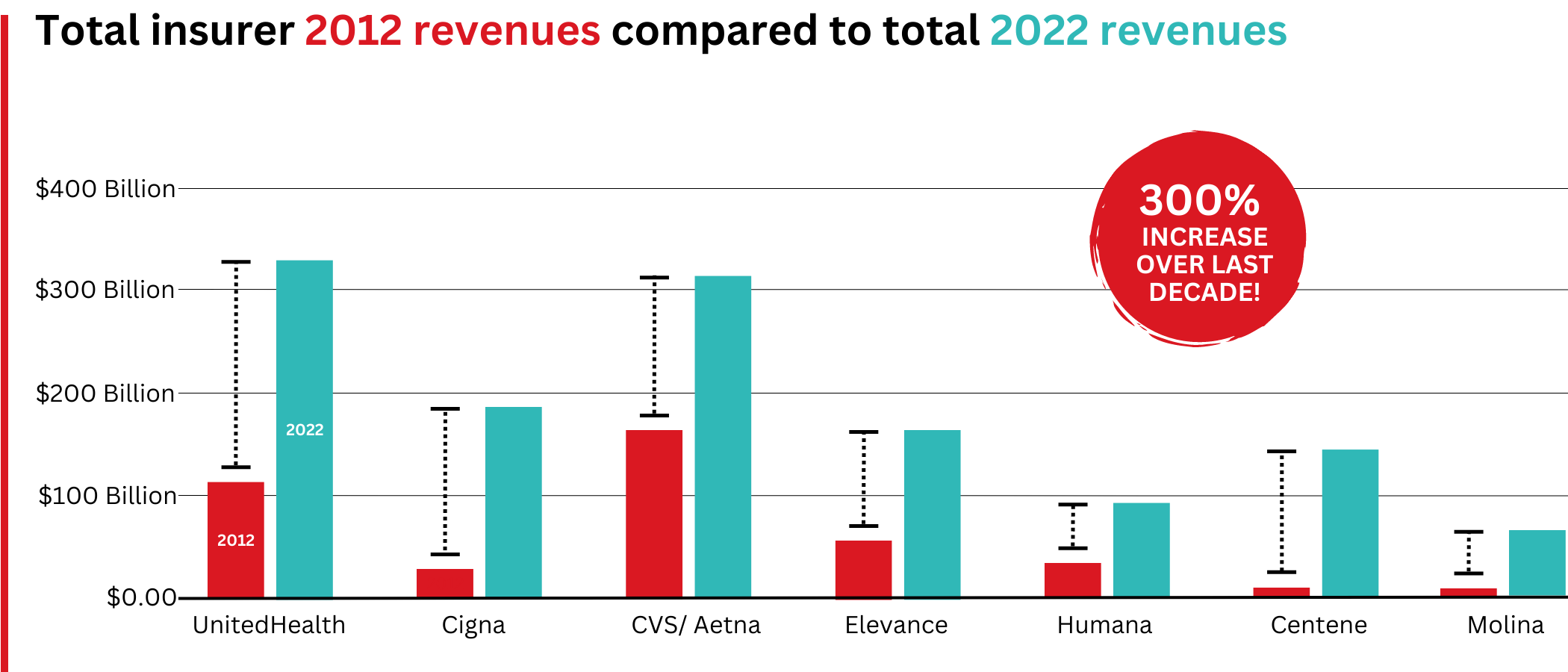

Big Insurance revenues and profits have increased by 300% and 287% respectively since 2012 due to explosive growth in the companies’ pharmacy benefit management (PBM) businesses and the Medicare replacement plans they call Medicare Advantage.

The for-profits now control more than 80% of the national PBM market and more than 70% of the Medicare Advantage market.

In 2022, Big Insurance revenues reached $1.25 trillion and profits soared to $69.3 billion.

That’s a 300% increase in revenue and a 287% increase in profits from 2012, when revenue was $412.9 billion and profits were $24 billion.

Big insurers’ revenues have grown dramatically over the past decade, the result of consolidation in the PBM business and taxpayer-supported Medicare and Medicaid programs.

Sucking billions out of the pharmacy supply chain – and taxpayers’ pockets

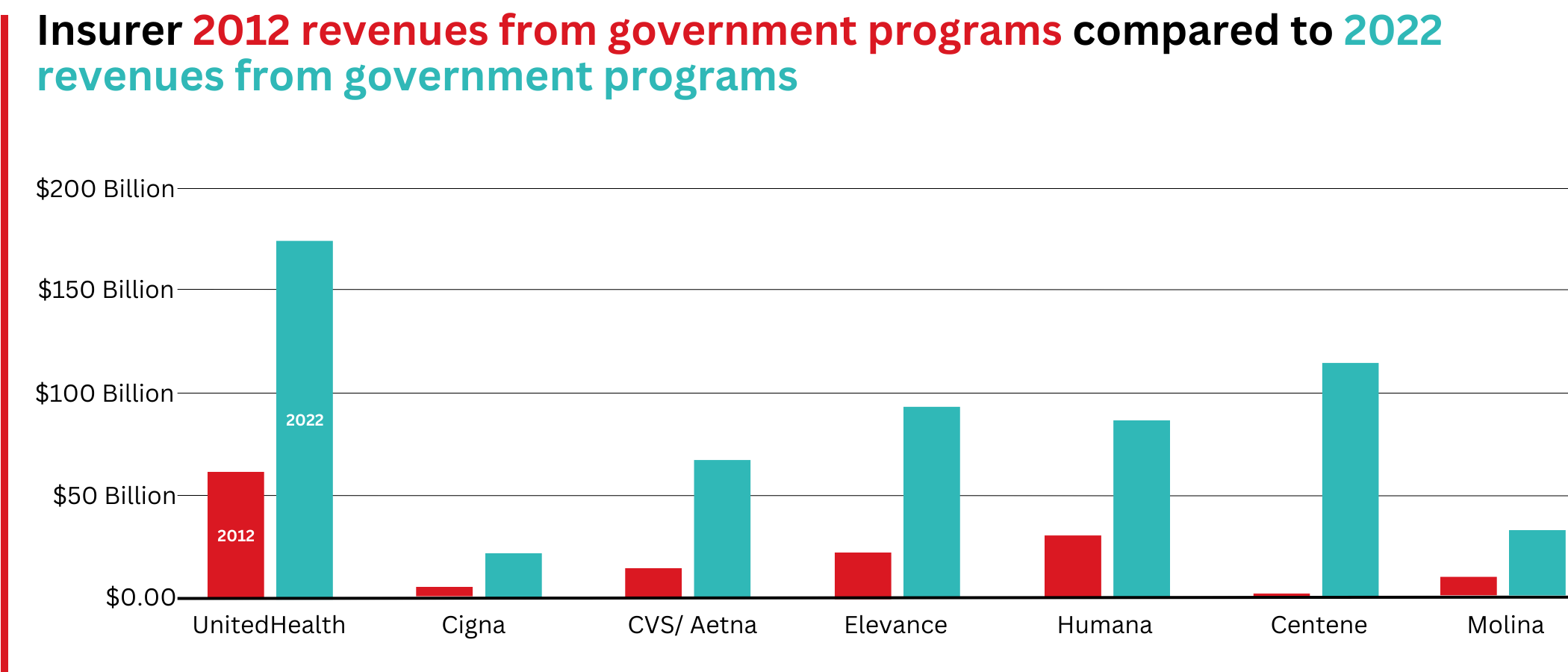

What has changed dramatically over the decade is that the big insurers are now getting far more of their revenues from the pharmaceutical supply chain and from taxpayers as they have moved aggressively into government programs. This is especially true of Humana, Centene, and Molina, which now get, respectively, 85%, 88%, and 94% of their health-plan revenues from government programs.

The two biggest drivers are their fast-growing pharmacy benefit managers (PBMs), the relatively new and little-known middleman between patients and pharmaceutical drug manufacturers, and the privately owned and operated Medicare replacement plans they market as Medicare Advantage.

With the exception of Humana, Centene, and Molina, most of the companies that constitute Big Insurance continue to make substantial amounts of money selling policies and services in what they refer to as their commercial businesses – to individuals, families, and employers – but the seven companies’ commercial revenue grew just 260%, or $176 billion, over 10 years (from $110.4 billion to $287.1 billion). While that’s significant, profitable growth in the commercial sector has become a major challenge for big insurers – so much so that Humana just last week announced it is exiting the employer-sponsored health-insurance marketplace entirely.

The percentage of U.S. employers providing some level of health benefits to their workers dropped from 69% to 51% between 1999 and 2022 – including a dramatic 8% decrease last year alone. Growth in this category is largely the result of insurers “stealing market share” from each other or from smaller competitors.

As a consequence of this segment’s relative stagnation, PBMs and government programs have become the new cash cows for Big Insurance.

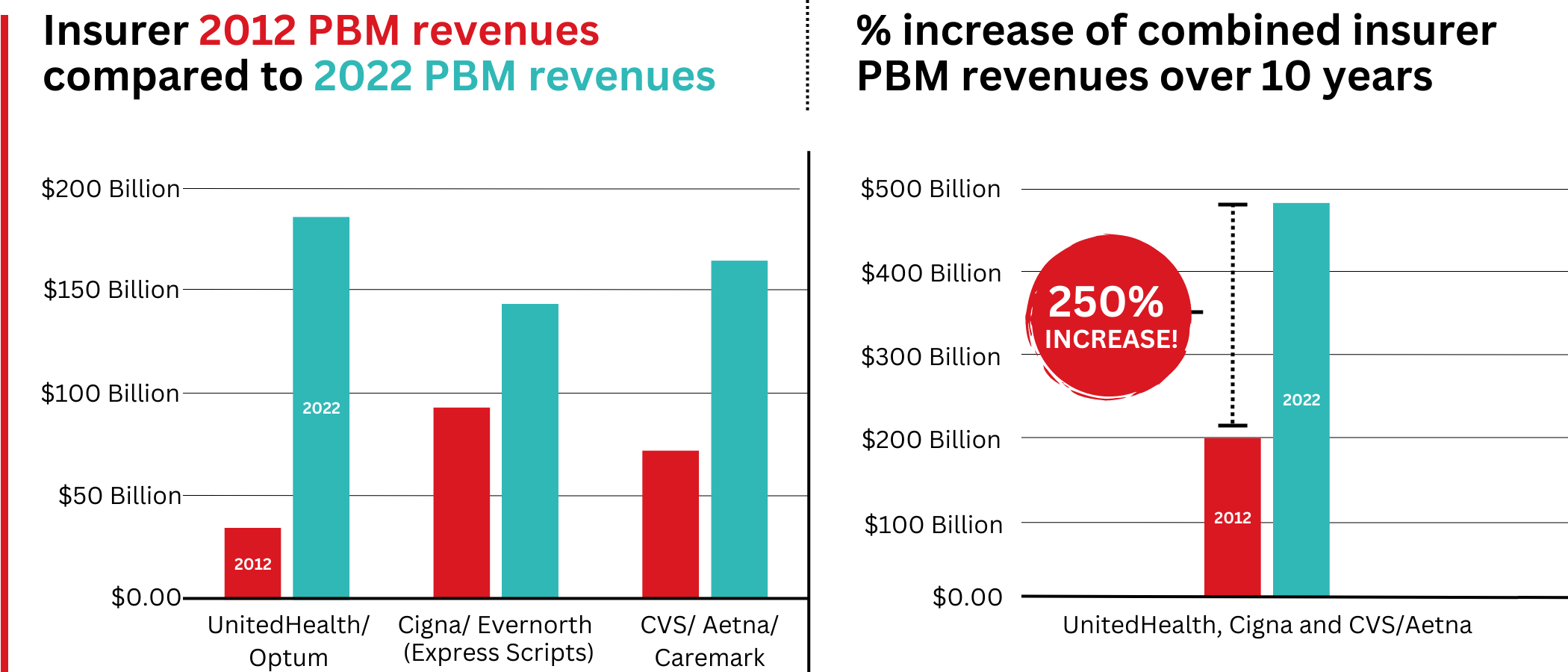

Spectacular PBM Growth

PBM HIGHLIGHTS

Cigna now gets far more revenue from its PBM than from its health plans. CVS gets more revenue from its PBM than from either Aetna’s health plans or its nearly 10,000 retail stores.

UnitedHealth has the biggest share of both the PBM and Medicare markets and, through numerous acquisitions of physician practices, is now the largest U.S. employer of doctors.

PBMs are middlemen companies that manage prescription drug benefits for health insurers, Medicare Part D drug plans, employers, and, in some cases, unions. As the Commonwealth Fund has noted:

PBMs have a significant behind-the-scenes impact in determining total drug costs for insurers, shaping patients’ access to medications, and determining how much pharmacies are paid.

The Commonwealth Fund went on to say that PBMs have faced growing scrutiny about their role in rising prescription drug costs and spending. A big reason for the scrutiny – by Congress, state lawmakers and now also by the FTC – is that the biggest PBMs are now owned by Big Insurance.

Through mergers and acquisitions in recent years, three of the seven for-profit insurers – Cigna, CVS/Aetna, and UnitedHealth – now control 80% of the U.S. pharmacy benefits market.

They determine which drugs will be listed in each of their formularies (lists of drugs they will “cover” based on secret deals they negotiate with pharmaceutical companies) and how much patients will have to pay out of their own pockets at the pharmacy counter – in many cases hundreds or thousands of dollars – before their coverage kicks in. The PBMs also “steer” health-plan enrollees to their preferred or owned pharmacies (and, increasingly, away from independent pharmacists), thereby capturing even more of what we spend on our prescription medications.

Cigna, CVS/Aetna, and UnitedHealth now control 80% of the U.S. PBM market. Correction: this graph was initially published with inaccurate numbers. The source for this information can be found here.

Ten years ago, PBMs contributed relatively little to the three companies’ revenues and profits. But since then, the rapid growth of PBMs has transformed all of the companies. The combined revenues from their PBM business units increased 250% between 2012 and 2022, from $196.7 billion to $492.4 billion.

Changes in PBM revenues between 2012 and 2022 for UnitedHealth Group, Cigna, and CVS/Aetna (Editor’s note: Cigna acquired PBM Express Scripts in 2018. To reflect revenue growth, Express Scripts’ pre-acquisition 2012 revenues are included in the Cigna total for that year.)

PBM Profit Generation

The PBM profit growth at the three companies over the past decade was even more dramatic than revenue growth. Collectively, their PBM profits increased 438%, from $6.3 billion in 2012 to $27.6 billion in 2022.

As a result of this fast growth, more than half (52%) of three companies’ profits in 2022 came from their PBM business units: Cigna’s Evernorth, CVS/Aetna’s Caremark, and UnitedHealth’s Optum. Cigna now gets far more revenue and profits from its PBM than from its health plans. And CVS gets more revenue from its PBM than from either Aetna’s health plans or its nearly 10,000 retail stores. (The companies’ business units that include their PBMs have also moved aggressively in recent years into health-care delivery through acquisitions of physician practices, clinics, dialysis centers, and other facilities. Notably, UnitedHealth Group is now the largest U.S. employer of physicians.)

Huge strides in privatizing both Medicare and Medicaid

GOVERNMENT PROGRAMS HIGHLIGHTS

More than 90% of health-plan revenues at three of the companies come from government programs as they continue to privatize both Medicare and Medicaid, through Medicare Advantage in particular.

Enrollment in government-funded programs increased by 261% in 10 years; by contrast commercial enrollment increased by just 10% over the past decade.

Commercial enrollment actually declinedat both UnitedHealth and Humana.

85% of Humana’s health-plan members are in government-funded programs; at Centene, it is 88%, and at Molina, it is 94%.

The big insurers now manage most states’ Medicaid programs – and make billions of dollars for shareholders doing so – but most of the insurers have found that selling their privately operated Medicare replacement plans is even more financially rewarding for their shareholders.

Revenue growth from government programs has been dramatic over the past 10 years. (Note the numbers do not include revenue from the Medicare Part D program, federal subsidy payments for many ACA marketplace plan enrollees, or Medicare supplement policies.)

This is especially apparent when you see that the Big Seven’s combined revenues from taxpayer-supported programs grew 500%, from $116.3 billion in 2012 to $577 billion in 2022.

These numbers should be of interest to the Biden administration and members of Congress, many of whom are calling for much greater scrutiny of the Medicare Advantage program. Numerous media and government reports have shown that the federal government is overpaying private insurers billions of dollars a year, largely because of loopholes in laws and regulations that enable them to get more taxpayer dollars by claiming their enrollees are sicker than they really are. The companies also make aggressive use of prior authorization, largely unknown in traditional Medicare, to avoid paying for doctor-ordered care and medications.

In addition to their focus on Medicare and Medicaid, the companies also profit from the generous subsidies the government pays insurers to reduce the premiums they charge individuals and families who do not qualify for either Medicare or Medicaid or who work for an employer that does not offer subsidized coverage. But many people enrolled in those types of plans – primarily through the health insurance “marketplaces” established by the Affordable Care Act – cannot afford the deductibles and other out-of-pocket requirements they must pay before their insurers will begin paying their medical claims.

Dramatic Enrollment Shifts

Changes in health-plan enrollment over the past decade show how dramatic this shift has been. Between 2012 and 2022, enrollment in the companies’ private commercial plans increased by 10%, from 85.1 million in 2012 to 93.8 million in 2022.

By comparison, growth in enrollment in taxpayer-supported government programs increased 261%, from 27 million in 2012 to 70.4 million in 2022.

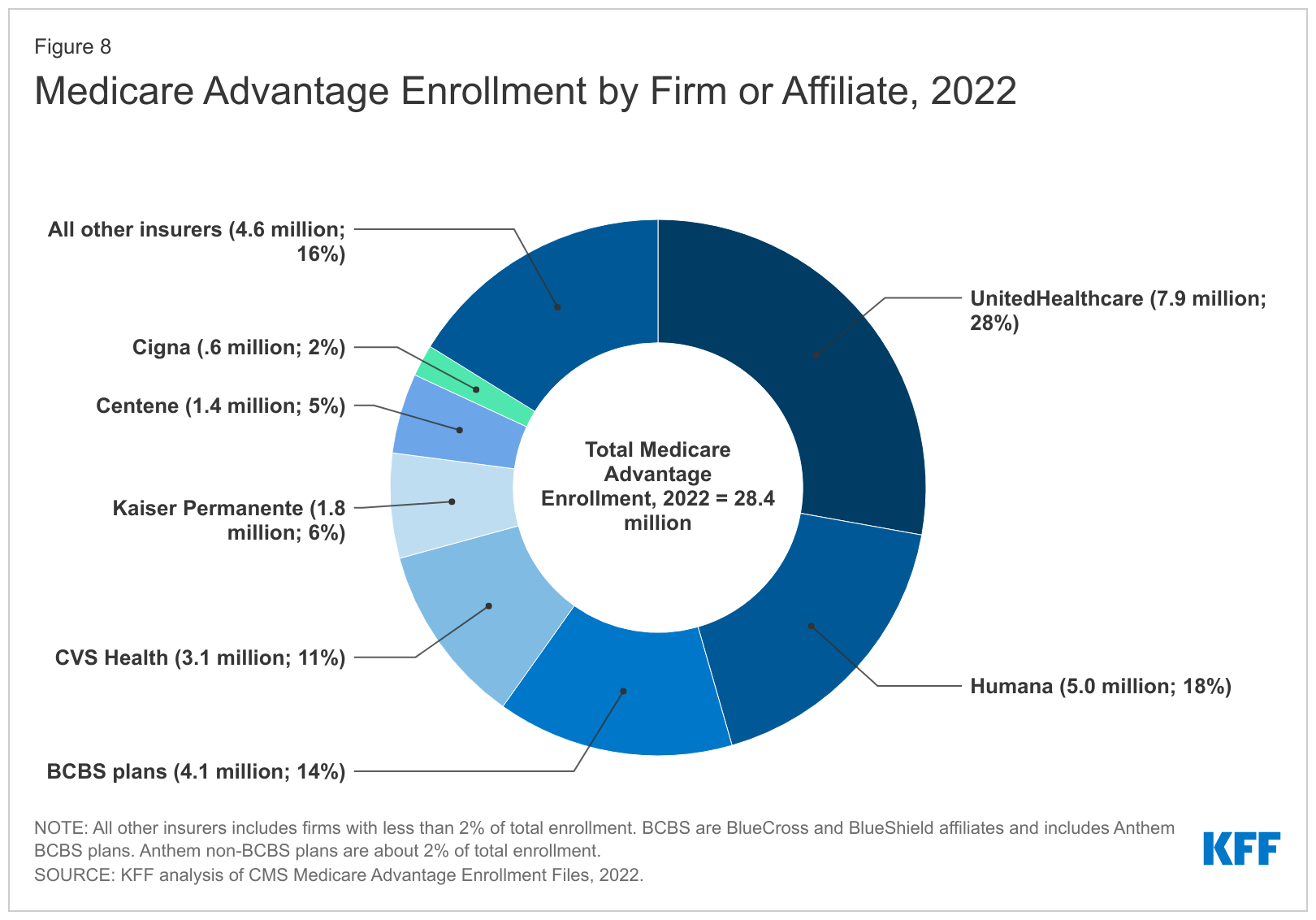

For-profit insurers dominate the Medicare Advantage market. Note that Anthem mentioned above is now known as Elevance. It owns 14 of the country’s Blue Cross Blue Shield plans.

Within that category, Medicare Advantage enrollment among the Big Seven increased 252%, from 7.8 million in 2012 to 19.7 million in 2022.

Nationwide, enrollment in Medicare Advantage plans increased to 28.4 million in 2022 (and to 30 million this year). That means that the Big Seven for-profit companies control more than 70% of the Medicare Advantage market.

UnitedHealth, Humana, Elevance, and CVS/Aetna have captured most of the Medicare Advantage market since the Affordable Care Act was passed in 2010.

The remaining growth in the government segment occurred in the Medicaid programs that a subset of the Big Seven (UnitedHealth, Elevance, Centene, and Molina in particular) manages for several states.

A few other facts and figures to keep in mind as Big Insurance thrives:

100 million of us – almost one of every three people in this country – now have medical debt.

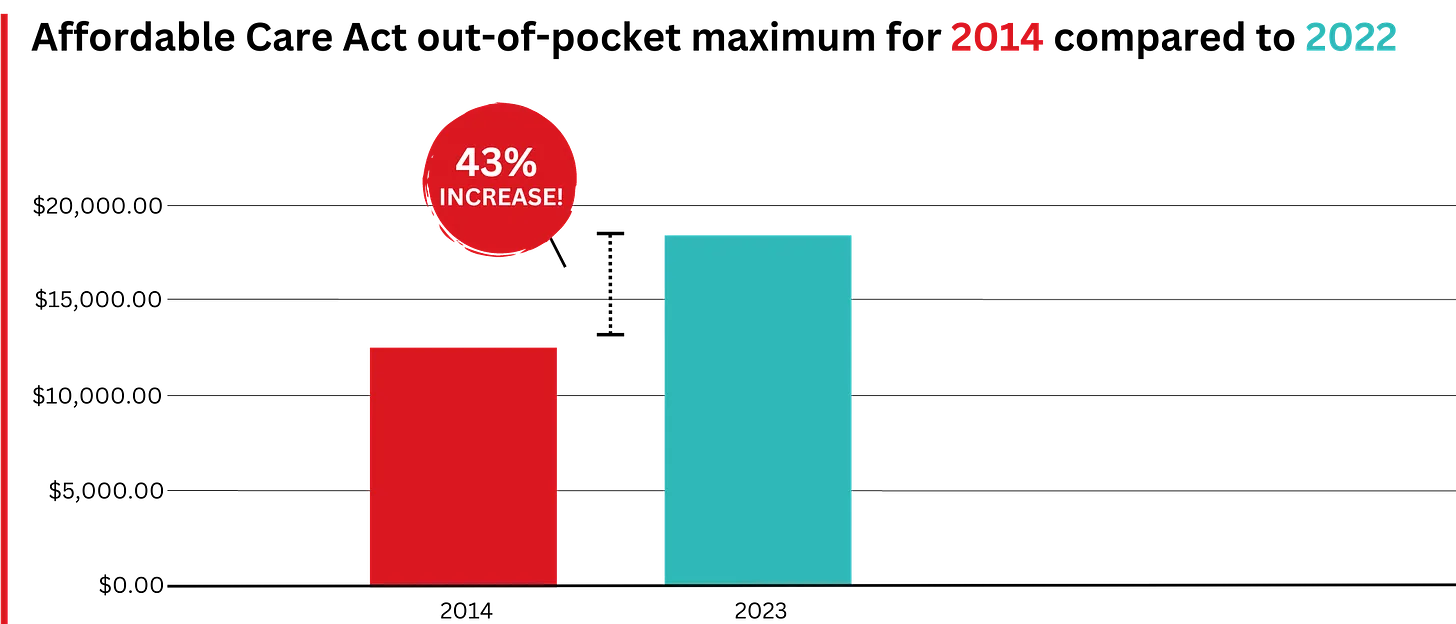

In 2023, U.S. families can be on the hook for up to $18,200 in out-of-pocket requirements before their coverage kicks in, up 43% since 2014 when it was $12,700.The Affordable Care Act allows the out-of-pocket maximum to increase annually – 43% since the maximum limit went into effect in 2014.

44% of people in the United States who purchased coverage through the individual market and (ACA) marketplaces were underinsured or functionally uninsured.

42% said they hadproblems paying medical bills or were paying off medical debt.

Half (49%) said they would be unable to pay an unexpected medical bill within 30 days, including 68% of adults with low income, 69% of Black adults, and 63% of Latino/Hispanic adults.

In 2021, about $650 million, or about one-third of all funds raised by GoFundMe, went to medical campaigns. That’s not surprising when you realize that in the United States, even people with insurance all too often feel they have no choice but to beg for money from strangers to get the care they or a loved one needs.

Even as we spend about $4.5 trillion on health care a year, Americans are now dying younger than people in other wealthy countries. Life expectancy in the United States actually decreased by 2.8 years between 2014 and 2021, erasing all gains since 1996, according to the Centers for Disease Control and Prevention.

BOTTOM LINE:

The companies that comprise Big Insurance are vastly different from what they were just 10 years ago, but policymakers, regulators, employers, and the media have so far shown scant interest in putting their business practices under the microscope.

Changes in federal law, including the Medicare Modernization Act of 2003, which created the lucrative Medicare Advantage market, and the Affordable Care Act of 2010, which gave insurers the green light to increase out-of-pocket requirements annually and restrict access to care in other ways, opened the Treasury and Medicare Trust Fund to Big Insurance. In addition, regulators have allowed almost all of their proposed acquisitions to go forward, which has created the behemoths they are today.

CVS/Health is now the 4th largest company on the Fortune 500 list of American companies. UnitedHealth Group is now No. 5 – and all the others are climbing toward the top 10.

The recent assassination of the CEO of UnitedHealthcare — the health insurance company with, reportedly, the highest rate of claims rejections(and thus dead, wounded, and furious customers and their relations) — gives us a perfect window to understand the stupidity and danger of the Musk/Trump/Ramaswamy strategy of “cutting government” to “make it more efficient, run it like a corporation.”

Consider health care, which in almost every other developed country in the world is legally part of the commons — the infrastructure of the nation, like our roads, public schools, parks, police, military, libraries, and fire departments — owned by the people collectively and run for the sole purpose of meeting a basic human need.

The entire idea of government — dating all the way back to Gilgamesh and before — is to fulfill that singular purpose of meeting citizens’ needs and keeping the nation strong and healthy. That’s a very different mandate from that of a corporation, which is solely directed (some argue by law) to generate profits.

The Veterans’ Administration healthcare system, for example, is essentially socialist rather than capitalist. The VA owns the land and buildings, pays the salaries of everybody from the surgeons to the janitors, and makes most all decisions about care. Its primary purpose — just like that of the healthcare systems of every other democracy in the world — is to keep and make veterans healthy. Its operation is nearly identical to that of Britain’s beloved socialist National Health Service.

UnitedHealthcare similarly owns its own land and buildings, and its officers and employees behave in a way that’s aligned with the company’s primary purpose, but that purpose is to make a profit. Sure, it writes checks for healthcare that’s then delivered to people, but that’s just the way UnitedHealthcare makes money; writing checks and, most importantly, refusing to write checks.

Think about it. If UnitedHealthcare’s main goal was to keep people healthy, they wouldn’t be rejecting 32 percent of claims presented to them. Like the VA, when people needed help they’d make sure they got it.

Instead, they make damn sure their executives get millions of dollars every year (and investors get billions) because making a massive profit ($23 billion last year, and nearly every penny arguably came from saying “no” to somebody’s healthcare needs) is their real business.

On the other hand, if the VA’s goal was to make or save money by “being run efficiently like a company,” they’d be refusing service to a lot more veterans (which it appears is on the horizon).

This is the essential difference between government and business, between meeting human needs (social) and reaching capitalism’s goal (profit).

It’s why its deeply idiotic to say, as Republicans have been doing since the Reagan Revolution, that “government should be run like a business.” That’s nearly as crackbrained a suggestion as saying that fire departments should make a profit (a doltish notion promoted by some Libertarians). Government should be run like a government, and companies should be run like companies.

Given how obvious this is with even a little bit of thought, where did this imbecilic idea that government should run like a business come from?

Turns out, it’s been driven for most of the past century by morbidly rich businessmen (almost entirely men) who don’t want to pay their taxes. As Jeff Tiedrich notes:

“The scariest sentence in the English language is: ‘I’m a billionaire, and I’m here to help.’”

Rightwing billionaires who don’t want to pay their fair share of the costs of society set up think tanks, policy centers, and built media operations to promote their idea that the commons are really there for them to plunder under the rubric of privatization and efficiency.

They’ve had considerable success. Slightly more than half of Medicare is now privatized, multiple Republican-controlled states are in the process of privatizing their public school systems, and the billionaire-funded Project 2025 and the incoming Trump administration have big plans for privatizing other essential government services.

The area where their success is most visible, though, is the American healthcare system. Because the desire of rightwing billionaires not to pay taxes have prevailed ever since Harry Truman first proposed single-payer healthcare like most of the rest of the world has, Americans spend significantly more on healthcare than other developed countries.

In 2022, citizens of the United States spent an estimated $12,742 per person on healthcare, the highest among wealthy nations. This is nearly twice the average of $6,850 per person for other wealthy OECD countries.

Over the next decade, it is estimated that America will spend between $55 and $60 trillion on healthcare if nothing changes and we continue to cut giant corporations in for a large slice of our healthcare money.

On the other hand, Senator Bernie Sanders’ single-payer Medicare For All plan would only cost $32 trillion over the next 10 years. And it would cover everybody in America, every man woman and child, in every medical aspect including vision, dental, psychological, and hearing.

If we keep our current system, the difference between it and the savings from a single-payer system will end up in the pockets, in large part, of massive insurance giants and their executives and investors. And as campaign contributions for bought off Republicans. This isn’t rocket science.

And you’d think that giving all those extra billions to companies like UnitedHealthcare would result in America having great health outcomes. But, no.

Despite insanely higher spending, the U.S. has a lower life expectancy at birth, higher rates of chronic diseases, higher rates of avoidable or treatable deaths, and higher maternal and infant mortality rates than any of our peer nations.

Compared to single-payer nations like Canada, the U.S. also has a higher incidence of chronic health conditions, Americans see doctors less often and have fewer hospital stays, and the U.S. has fewer hospital beds and physicians per person.

No other country in the world allows a predatory for-profit industry like this to exist as a primary way of providing healthcare. Every other advanced democracy considers healthcare a right of citizenship, rather than an opportunity for a handful of industry executives to hoard a fortune, buy Swiss chalets, and fly around on private jets.

This is one of the most widely shared graphics on social media over the past few days in posts having to do with Thompson’s murder…

Sure, there are lots of health insurance companies in other developed countries, but instead of offering basic healthcare (which is provided by the government) mostly wealthy people subscribe to them to pay for premium services like private hospital rooms, international air ambulance services, and cosmetic surgery.

Essentially, UnitedHealthcare’s CEO Brian Thompson made decisions that killed Americans for a living, in exchange for $10 million a year. He and his peers in the industry are probably paid as much as they are because there is an actual shortage of people with business training who are willing to oversee decisions that cause or allow others to die in exchange for millions in annual compensation.

That Americans are well aware of this obscenity explains the gleeful response to his murder that’s spread across social media, including the refusal of online sleuths to participate in finding his killer.

It shouldn’t need be said that vigilantism is no way to respond to toxic individuals and companies that cause Americans to die unnecessarily. Hopefully, Thompson’s murder will spark a conversation about the role of government and the commons — and the very real need to end the corrupt privatization of our healthcare system (including the Medicare Advantage scam) that has harmed so many of us and killed or injured so many of the people we love.

While speculation swirls around key cabinet appointments in the incoming Trump administration, much is being written about how things might change for industries and the companies that compose them. Healthcare is no exception.

Speculation about possible changes originates from media coverage, healthcare trade associations, law firms, consultancies, think tanks and academics. Their views are primarily based on Trump Healthcare 1.0 initiatives (2017-2021), presumed Trump 2.0 leverage in the U.S. Senate, House and conservative Supreme Court and a belief by the Trump-team leaders that their mandate is to lower costs for “everyday Americans” and tighten border security.

Thus, Trump Healthcare 2.0 policy changes will be extensive, leveraging legislation, executive orders, agency administrative actions, court decisions and appropriations processes to reset the U.S. health system.

Context:

The red shift that enabled the 45th President to regain the White House was fueled by discontent and fear: discontent with prices paid by ordinary consumers and fear that illegal immigration was an existential threat. Abortion was an important concern to women but inflation and prices for gas, groceries, housing and healthcare mattered more. Exit polls indicate voter concern about how Trump 2.0 economic policies (tariffs et al) might inflate consumer prices or add up to $7 trillion to the national debt was low. And the fate of the Affordable Care Act was a non-issue: assurance about protection for pre-existing condition coverage neutered attention to other elements of the ACA that will get attention in Trump Healthcare 2.0 (i.e. subsidies, short-term plans, et al).

The Four Pillars of Trump Healthcare 2.0 Policy Changes

The new administration is inclined toward a transactional view of the U.S. health system. It does not envision transformational change; instead, it sees opportunity for the system to perform significantly better. Its policies, leadership appointments and actions will be predicated on these four pillars:

Access to the U.S. healthcare system is a right to be earned. Fundamentally, Trump Healthcare 2.0 builds on its moral conviction that there should be NO FREE LUNCHES whether it’s illegal immigrants or patients who use the health system without doing their part. Trump Healthcare 2.0 will advance mechanisms to enable self-care, increase personal responsibility, promote cheaper/better alternatives to traditional insurance and health delivery and challenge lawmakers to limit financial support to free-loaders. The fundamental notions of public health and community benefit will be revisited and restrictions enacted.

The status quo is not working. Change is needed. Polls show the majority of Americans are dissatisfied with the health system. Affordability is their major concern: escalating, inexplicable costs are forcing their employers to share more responsibility. Trump Healthcare 2.0 will implement changes that lower spending and costs for consumers and employers. They’ll leverage coalitions of working-class voters and businesses to enact policies that expose waste, fraud and abuse in the system and direct the U.S. Department of Health & Human Services to streamline its structure and prioritize cost-effectiveness (the HHS Strategic Plan for 2022-2026 is up for review).

Private solutions solve public problems better than government. Trump Healthcare 2.0 posits that government is broken including the federal and state agencies that control healthcare oversight and funding. Reducing regulatory barriers to consolidation and innovation and lessening risks for private investors whose ventures align with Trump Healthcare 2.0 priorities will be foci. Fundamentally, Trump Healthcare 2.0 believes the private sector is better able to address problems than government bureaucrats: key Trump Healthcare 2.0 leadership positions will be filled by successful private sector operators instead of re-cycled DC luminaries desiring attention.

Price transparency fuels competition and value. Trump Healthcare 1.0 mandated hospital price transparency via its 2019 Executive Order: Trump Healthcare 2.0 will expand the scope and usefulness of price transparency mandates in hospital, ancillary and outpatient services, physician services, insurance and others. It will facilitate accelerated use of Artificial Intelligence in decision-making by consumers, providers and payers. It will expand timely access to data on prices, direct costs, overhead, executive compensation, outcomes, user experiences and other elements of care management provided by hospitals, physicians and other providers. And it will move quickly to implement site neutral payments in the 119th Trump Healthcare 2.0 holds that providers, insurers and drug companies are not inclined to transparency despite strong support from elected officials and voters. They’ll advance these policy changes anticipating pushback from industry insiders. Trump Healthcare 2.0 believes price transparency in healthcare will produce transformational changes that enable more competition and lower costs.

Looking ahead:

The Trump 2.0 team’s immediate task is to assemble its Cabinet: that’s taken prior administrations 38 days on average to complete. In tandem, temporary fixes for CMS’ pending Physician Pay Cut and telehealth expansion will pass as Congress’ lame duck session begins this week.

Looking to 2025, the Trump Healthcare 2.0 team will focus initially on issues in Congress where Bipartisan support appears strong i.e. regulation of PBMs, implementation of site neutral payment policies, expansion of drugs subject to Inflation Reduction Act’s pricing limits and perhaps others. It will plan its legislative agenda coordinating with key committees (i.e. Senate HELP, House Ways and Means et al) and outside groups that share its predisposition. And it will use its political clout to build popular support for healthcare reforms that respond directly to consumer (voter) concern about affordability.

Trump Healthcare 2.0 will bring heightened transparency to the health system and be premised on pillars that are popular with working class voters. It will not be a duplicate of Trump Healthcare 1.0: it will be much more.

As campaigns for November elections gear up for early voting and Congress considers bipartisan reforms to limit consolidation and enhance competition in U.S. healthcare, prospective voters are sending a cleat message to would-be office holders:

Healthcare Affordability must be addressed directly, transparently and now.

Polling by Gallup, Kaiser Family Foundation and Pew have consistently shown healthcare affordability among top concerns to voters alongside inflation, immigration and access to abortion. It is higher among Democratic-leaning voters but represents the majority in every socio-economic cohort–young and old, low and middle income and households with/without health insurance coverage., urban and rural and so on.

It’s understandable: household economic security is declining: per the Federal Reserve’s latest household finances report:

72% of US adults say they are doing well financially (down from 78% in 2021)

54% say they have emergency savings to cover 3 months expenses ($400)—down from high of 59% in 2015.

69% say their finances deteriorated in 2023. They’re paying more for groceries, fuel, insurance premiums and childcare.

Renters absorbed a 10% increase last year and mortgage interest spike has put home ownership beyond reach for 6 in 10 households

Thus, household financial security is the issue and healthcare expenses play a key role. Drug prices, hospital consolidation, price transparency and corporate greed will get frequent recognition in candidate rhetoric. “Reform” will be promised. And each sector in the industry will offer solutions that place the blame on others.

Granted, the U.S. health system lacks a uniform definition of healthcare affordability. It’s a flaw. In the Affordable Care Act, it was framed in the context of an individual’s eligibility for government-subsidized insurance coverage (8.39% adjusted gross income for households between 100% and 400% of the federal poverty level). But a broader application to the entire population was overlooked. Nonetheless, economists, regulators and consumers recognize the central role healthcare affordability plays in household financial security.

Handicapping the major players potential to win the hearts and minds of voters about healthcare affordability is tricky:

Each major sector has seen the ranks of its membership decrease and the influence (and visibility) of its bigger players increase. They’re easy targets for industry critics.

Each sector is seeing private equity and non-traditional players play bigger roles. The healthcare landscape is expanding beyond the traditional players.

Each sector is struggling to make their cases for incremental reforms while employers, legislators and consumers want more. Bipartisan support for anything is a rarity: an exception is antipathy toward healthcare consolidation and lack of price transparency.

All recognize that affordability is complicated. Unit cost and price increases for goods and services are the culprit: excess utilization is secondary.

Against this backdrop, here’s a scorecard on the current state of preparedness as each navigates affordability going into Campaign 2024:

Sector

Advantages

Disadvantages

Handicap Score1=Unprepared to5=Well Prepared

Hospitals

Community presence (employer, safety net) Economic impact Influence in Congress Scale: 30% of spending + direct employment of 52% of physicians Access to capital

Lack of costs & price transparency Unit costs inflation due to wage, supply chain & admin Shifting demand for core services. Low entry barriers for key services Regulator headwind (state, federal). Operating, governing culture Value proposition erosion with employers, pre-Medicare populations Consumer orientation

3

Physicians

Consumer trust Influence in Congress Shared savings (Medicare) Essentiality Specialization Access to technology

Care continuity Inadequacy of primary care Disorganization (fragmentation) Value of shared savings to general population (beyond Medicare) Culture: change-averse (education, licensing performance measurement, et al) Data: costs, outcomes

2

Drug Manufacturers

Increasing product demand Influence in Congress Public trust in drug efficacy Insurance structure that limits consumer price sensitivity to OOP Potential for AI -enabled discovery, market access Access to private capital Congress’ constraint on PBMs

Unit cost escalation Lack of price transparency Growing disaffection for FDA Long-term Basic Research Funding State Price Control Momentum Market access Restrictive Formulary Growth Transparency in Distributor-PBM business relationships Public perception of corporate greed

2

Health Insurers

Availability of claims, cost data Employer tax exemptions Growing government market Plan design: OOP, provider access Public association: coverage = financial security Access to private capital

Escalating premiums Declining group market Growing regulatory scrutiny (consolidation, data protection) Tension with health systems Value proposition erosion among government, employers, consumers

4

Retail Health

Non-incumbrance of restrictive regulatory framework Consumer acceptance Breadth of product opportunities Access to private capital Opportunity for care management (i.e. CVS- Epic) Operational orientation to consumers (convenience, pricing, et al) Potential with employers,

Lack of access, coordination with needed specialty care Threat of regulatory restraint on growth Risks associated with care management models

3

The biggest, investor-owned health insurers own the advantage today. As in other sectors, they’re growing faster than their smaller peers and enjoy advantages of scale and private capital access to fund their growth. A handful of big players in the other sectors stand-out, but their affordability solutions are, to date, not readily active.

In each sector above, there is consensus that a fundamental change in the structure, function and oversight of the U.S. health is eminent. In all, tribalism is an issue: publicly-owned, not for profits vs. investor-owned, independent vs. affiliated, big vs. small and so on.

Getting consensus to address affordability head on is hard, so not much is done by the sectors themselves. And none is approaching the solution in its necessary context—the financial security of a households facing unprecedented pressures to make ends meet. In all likelihood, the bigger, more prominent organizations in their ranks of these sectors will deliver affordability solutions well-above the lowest common denominators that are comfortable for most Thus, health care affordability will be associated with organizational brands and differentiated services, not the sectors from which their trace their origins. And it will be based on specified utilization, costs, outcome and spending guarantees to consumers and employers that are reasonable and transparent.

The Affordable Care Act turned 14 on March 23. It has done a lot of good for a lot of people, but big changes in the law are urgently needed to address some very big misses and consequences I don’t believe most proponents of the law intended or expected.

At the top of the list of needed reforms: restraining the power and influence of the rapidly growing corporations that are siphoning more and more money from federal and state governments – and our personal bank accounts – to enrich their executives and shareholders.

I was among many advocates who supported the ACA’s passage, despite the law’s ultimate shortcomings. It broadened access to health insurance, both through government subsidies to help people pay their premiums and by banning prevalent industry practices that had made it impossible for millions of American families to buy coverage at any price. It’s important to remember that before the ACA, insurers routinely refused to sell policies to a third or more applicants because of a long list of “preexisting conditions” – from acne and heart disease to simply being overweight – and frequently rescinded coverage when policyholders were diagnosed with cancer and other diseases.

While insurance company executives were publicly critical of the law, they quickly took advantage of loopholes (many of which their lobbyists created) that would allow them to reap windfall profits in the years ahead – and they have, as you’ll see below.

I wrote and spoke frequently as an industry whistleblower about what I thought Congress should know and do, perhaps most memorably in an interview with Bill Moyers. During my Congressional testimony in the months leading up to the final passage of the bill in 2010, I told lawmakers that if they passed it without a public option and acquiesced to industry demands, they might as well call it “The Health Insurance Industry Profit Protection and Enhancement Act.”

A health plan similar to Medicare that could have been a more affordable option for many of us almost happened, but at the last minute, the Senate was forced to strip the public option out of the bill at the insistence of Sen. Joe Lieberman (I-Connecticut), who died on March 27, 2024. The Senate did not have a single vote to spare as the final debate on the bill was approaching, and insurance industry lobbyists knew they could kill the public option if they could get just one of the bill’s supporters to oppose it. So they turned to Lieberman, a former Democrat who was Vice President Al Gore’s running mate in 2000 and who continued to caucus with Democrats. It worked. Lieberman wouldn’t even allow a vote on the bill if it created a public option. Among Lieberman’s constituents and campaign funders were insurance company executives who lived in or around Hartford, the insurance capital of the world. Lieberman would go on to be the founding chair of a political group called No Labels, which is trying to find someone to run as a third-party presidential candidate this year.

The work of Big Insurance and its army of lobbyists paid off as insurers had hoped. The demise of the public option was a driving force behind the record profits – and CEO pay – that we see in the industry today.

The good effects of the ACA:

Nearly 49 million U.S. residents (or 16%) were uninsured in 2010. The law has helped bring that down to 25.4 million, or 8.3% (although a large and growing number of Americans are now “functionally uninsured” because of unaffordable out-of-pocket requirements, which President Biden pledged to address in his recent State of the Union speech).

The ACA also made it illegal for insurers to refuse to sell coverage to people with preexisting conditions, which even included birth defects, or charge anyone more for their coverage based on their health status; it expanded Medicaid (in all but 10 states that still refuse to cover more low-income individuals and families); it allowed young people to stay on their families’ policies until they turn 26; and it required insurers to spend at least 80% of our premiums on the health care goods and services our doctors say we need (a well-intended provision of the law that insurers have figured out how to game).

The not-so-good effects of the ACA:

As taxpayers and health care consumers, we have paid a high price in many ways as health insurance companies have transformed themselves into massive money-making machines with tentacles reaching deep into health care delivery and taxpayers’ pockets.

To make policies affordable in the individual market, for example, the government agreed to subsidize premiums for the vast majority of people seeking coverage there, meaning billions of new dollars started flowing to private insurance companies. (It also allowed insurers to charge older Americans three times as much as they charge younger people for the same coverage.) Even more tax dollars have been sent to insurers as part of the Medicaid expansion. That’s because private insurers over the years have persuaded most states to turn their Medicaid programs over to them to administer.

We invite you to take a look at how the ascendency of health insurers over the past several years has made a few shareholders and executives much richer while the rest of us struggle despite – and in some cases because of – the Affordable Care Act.

BY THE NUMBERS

In 2010, we as a nation spent $2.6 trillion on health care. This year we will spend almost twice as much – an estimated $4.9 trillion, much of it out of our own pockets even with insurance.

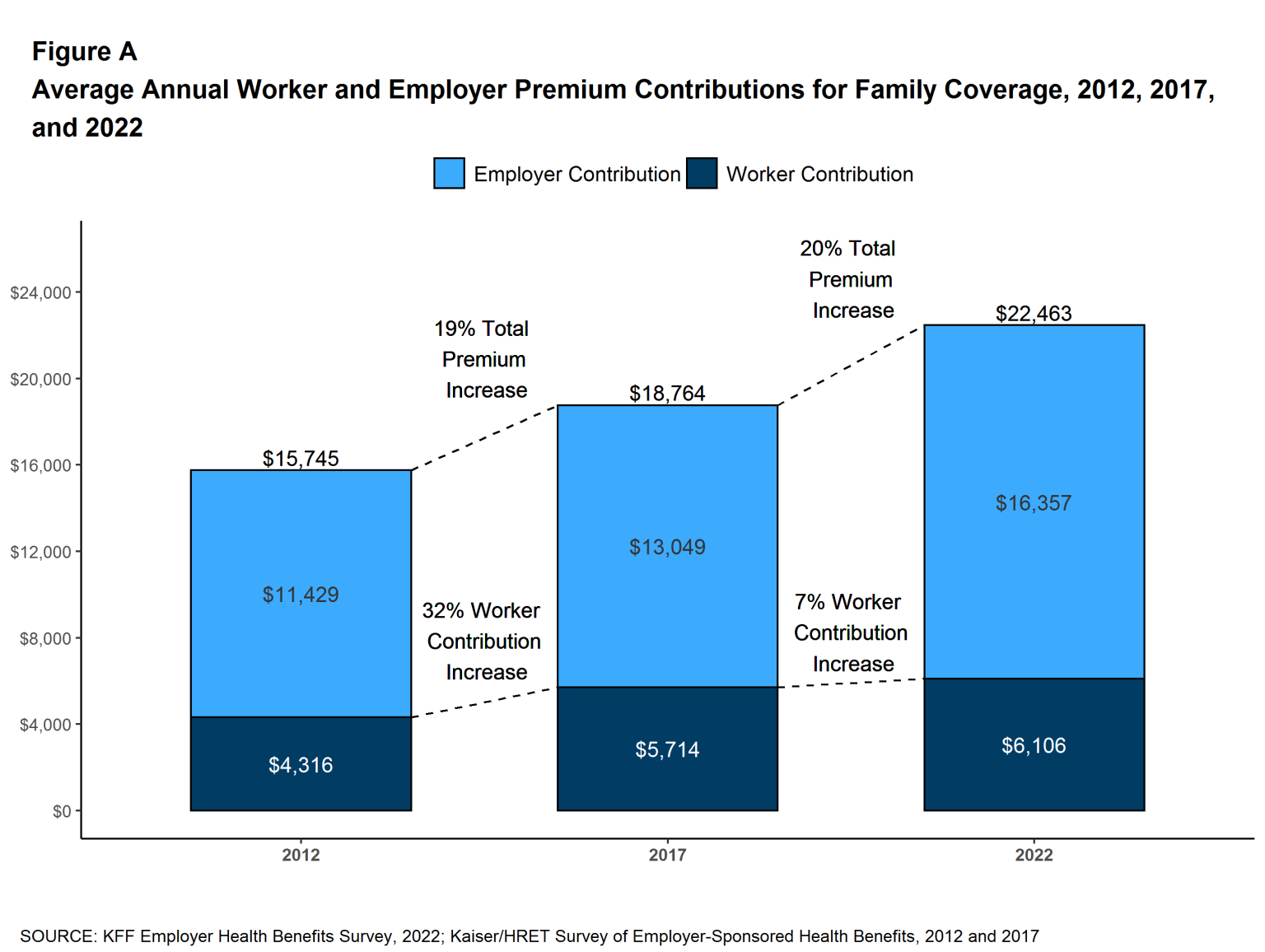

In 2010, the average cost of a family health insurance policy through an employer was $13,710. Last year, the average was nearly $24,000, a 75% increase.

The ACA, to its credit, set an annual maximum on how much those of us with insurance have to pay before our coverage kicks in, but, at the insurance industry’s insistence, it goes up every year. When that limit went into effect in 2014, it was $12,700 for a family. This year, it has increased by 48%, to $18,900. That means insurers can get away with paying fewer claims than they once did, and many families have to empty their bank accounts when a family member gets sick or injured. Most people don’t reach that limit, but even a few hundred dollars is more than many families have on hand to cover deductibles and other out-of-pocket requirements.

Now 100 million Americans – nearly one of every three of us – are mired in medical debt, even though almost 92% of us are presumably “covered.” The coverage just isn’t as adequate as it used to be or needs to be.

Meanwhile, insurance companies had a gangbuster 2023. The seven big for-profit U.S. health insurers’ revenues reached $1.39 trillion, and profits totaled a whopping $70.7 billion last year.

SWEEPING CHANGE, CONSOLIDATION–AND HUGE PROFITS FOR INVESTORS

Insurance company shareholders and executives have become much wealthier as the stock prices of the seven big for-profit corporations that control the health insurance market have skyrocketed.

NOTE: The Dow Jones Industrial Average is listed on this chart as a reference because it is a leading stock market index that tracks 30 of the largest publicly traded companies in the United States.

REVENUES collected by those seven companies have more than tripled (up 346%), increasing by more than $1 trillion in just the past ten years.

PROFITS (earnings from operations) have more than doubled (up 211%), increasing by more than $48 billion.

The CEOs of these companies are among the highest paid in the country. In 2022, the most recent year the companies have reported executive compensation, they collectively made $136.5 million.

U.S. HEALTH PLAN ENROLLMENT

Enrollment in the companies’ health plans is a mix of “commercial” policies they sell to individuals and families and that they manage for “plan sponsors” – primarily employers and unions – and government/enrollee-financed plans (Medicare, Medicaid, Tricare for military personnel and their dependents and the Federal Employee Health Benefits program).

Enrollment in their commercial plans grew by just 7.65% over the 10 years and declined significantly at UnitedHealth, CVS/Aetna and Humana. Centene and Molina picked up commercial enrollees through their participation in several ACA (Obamacare) markets in which most enrollees qualify for federal premium subsidies paid directly to insurers.

While not growing substantially, commercial plans remain very profitable because insurers charge considerably more in premiums now than a decade ago.

(1) The 2013 total for CVS/Aetna was reported by Aetna before its 2018 acquisition by CVS. (2) Humana announced last year it is exiting the commercial health insurance business. (3) Enrollment in the ACA’s marketplace plans account for all of Molina’s commercial business.

By contrast, enrollment in the government-financed Medicaid and Medicare Advantage programs has increased 197% and 167%, respectively, over the past 10 years.

(1) The 2013 total for CVS/Aetna was reported by Aetna before its 2018 acquisition by CVS.

Of the 65.9 million people eligible for Medicare at the beginning of 2024, 33 million, slightly more than half, enrolled in a private Medicare Advantage plan operated by either a nonprofit or for-profit health insurer, but, increasingly, three of the big for-profits grabbed most new enrollees. Of the 1.7 million new Medicare Advantage enrollees this year, 86% were captured by UnitedHealth, Humana and Aetna. Those three companies are the leaders in the Medicare Advantage business among the for-profit companies, and, according to the health care consulting firm Chartis, are taking over the program “at breakneck speed.”

(1) The 2013 total for CVS/Aetna was reported by Aetna before its 2018 acquisition by CVS. (2,3) Centene’s and Molina’s totals include Medicare Supplement; they do not break out enrollment in the two Medicare categories separately.

It is worth noting that although four companies saw growth in their Medicare Supplement enrollment over the decade, enrollment in Medicare Supplement policies has been declining in more recent years as insurers have attracted more seniors and disabled people into their Medicare Advantage plans.

OTHER FEDERAL PROGRAMS

In addition to the above categories, Humana and Centene have significant enrollment in Tricare, the government-financed program for the military. Humana reported 6 million military enrollees in 2023, up from 3.1 million in 2013. Centene reported 2.8 million in 2023. It did not report any military enrollment in 2013.

Elevance reported having 1.6 million enrollees in the Federal Employees Health Benefits Program in 2023, up from 1.5 million in 2013. That total is included in the commercial enrollment category above.

At Cigna, Express Scripts’ pharmacy operations now contribute more than 70% to the company’s total revenues. Caremark’s pharmacy operations contribute 33% to CVS/Aetna’s total revenues, and Optum Rx contributes 31% to UnitedHealth’s total revenues.

WHAT TO DO AND WHERE TO START

The official name of the ACA is the Patient Protection and Affordable Care Act. The law did indeed implement many important patient protections, and it made coverage more affordable for many Americans. But there is much more Congress and regulators must do to close the loopholes and dismantle the barriers erected by big insurers that enable them to pad their bottom lines and reward shareholders while making health care increasingly unaffordable and inaccessible for many of us.

Several bipartisan bills have been introduced in Congress to change how big insurers do business.

And as noted above, President Biden has asked Congress to broaden the recently enacted $2,000-a-year cap on prescription drugs to apply to people with private insurance, not just Medicare beneficiaries. That one policy change could save an untold number of lives and help keep millions of families out of medical debt. (A coalition of more than 70 organizations and businesses, which I lead, supports that, although we’re also calling on Congress to reduce the current overall annual out-of-pocket maximum to no more than $5,000.)

I encourage you to tell your members of Congress and the Biden administration that you support these reforms as well as improving, strengthening and expanding traditional Medicare. You can be certain the insurance industry and its allies are trying to keep any reforms that might shrink profit margins from becoming law.

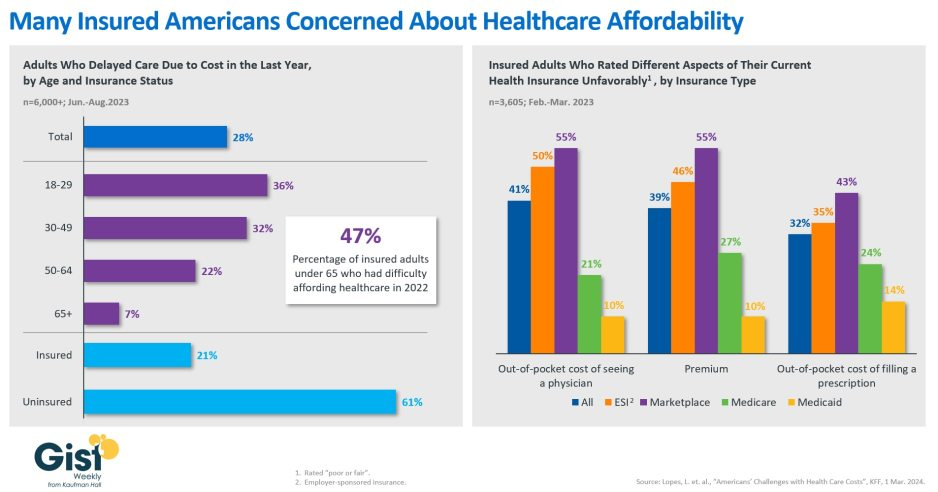

In this week’s graphic, we showcase recent KFF survey data on how healthcare costs impact the public, particularly those with health insurance.

Nearly half of US adults say it is difficult to afford healthcare, and in the last year, 28 percent have skipped or postponed care due to cost, with an even greater share of younger people delaying care due to cost concerns.

Although healthcare affordability has long been a problem for the uninsured, one in five adults with insurance skipped care in the past year because of cost. Insured Americans report low satisfaction with the affordability of their coverage.

In addition to high premiums, out-of-pocket costs to see a physician or fill a prescription are particular sources of concern. Adults with employer-sponsored or marketplace plans are far more likely to be dissatisfied with the affordability of their coverage, compared to those with government-sponsored plans.

With eight in ten American voters saying that it is “very important” for the 2024 presidential candidates to focus on the affordability of healthcare, we’ll no doubt see more attention focused on this issue as the presidential election race heats up.