In 63 days, Americans will know the composition of the 119th Congress and the new occupants of the White House and 11 Governor’s mansions. We’ll learn results of referenda in 10 states about abortion rights (AZ, CO, FL, MD, MO, MT, NE, NV, NY, SD) and see how insurance coverage for infertility (IVF therapy) fares as Californians vote on SB 729. But what we will not learn is the future of the U.S. health system at a critical time of uncertainty.

In 6 years, every baby boomer will be 65 years of age or older. In the next 20 years, the senior population will be 22% of the population–up from 18% today. That’s over 83 million who’ll hit the health system vis a vis Medicare while it is still digesting the tsunami of obesity, a scarcity of workers and unprecedented discontent:

The majority of voters is dissatisfied with the status quo. 69% think the system is fundamentally flawed and in need of major change vs. 7% who think otherwise. 60% believe it puts its profits above patient care vs. 13% who disagree.

Employers are fed up: Facing projected cost increases of 9% for employee coverage in 2025, they now reject industry claims of austerity when earnings reports and executive compensation indicate otherwise. They’re poised to push back harder than ever.

Congress is increasingly antagonistic: A bipartisan coalition in Congress is pushing populist reforms unwelcome by many industry insiders i.e. price transparency for hospitals, price controls for prescription drugs, limits on private equity ownership, constraint on hospital, insurer and physician consolidation, restrictions on tax exemptions of NFP hospitals, site neutral payment policies and many more.

Fanning these flames, media characterizations of targeted healthcare companies as price gouging villains led by highly-paid CEOs is mounting: last week, it was Acadia Health’s turn courtesy of the New York Times’ investigators.

Navigating uncertainty is tough for industries like healthcare where demand s growing, technologies are disrupting how and where services are provided and by whom, and pricing and affordability are hot button issues. And it’s too big to hide: at $5.049 trillion, it represents 17.6% of the U.S. GDP today increasing to 19.7% by 2032. Growing concern about national debt puts healthcare in the crosshairs of policymaker attention:

Per the Committee for a Responsible Federal Budget: “In the latest Congressional Budget Office (CBO) baseline, nominal spending is projected to grow from $6.8 trillion in Fiscal Year (FY) 2024 to $10.3 trillion in 2034. About 87% of this increase is due to three parts of the federal budget: Social Security, federal health care programs, and interest payments on the debt.”

In response, Boards in many healthcare organizations are hearing about the imperative for “transformational change” to embrace artificial intelligence, whole person health, digitization and more. They’re also learning about ways to cut their operating costs and squeeze out operating margins. Bold, long-term strategy is talked about, but most default to less risky, short-term strategies compatible with current operating plans and their leaders’ compensation packages. Thus, “transformational change” takes a back seat to survival or pragmatism for most.

For Boards of U.S. healthcare organizations, the imperative for transformational change is urgent: the future of the U.S. system is not a repeat of its past. But most Boards fail to analyze the future and construct future-state scenarios systematically. Lessons from other industries are instructive.

Transformational change in mission critical industries occurs over a span of 20-25 years. It starts with discontent with the status quo, then technologies and data that affirm plausible alternatives and private capital that fund scalable alternatives. It’s not overnight.

Transformational change is not paralyzed by regulatory hurdles. Transformers seek forgiveness, not permission while working to change the regulatory landscape. Advocacy is a critical function in transformer organizations.

Transformation is welcomed by consumers. Recognition of improved value by end-users—individual consumers—is what institutionalizes transformational success. Transformed industries define success in terms of the specific, transparent and understandable results of their work.

Per McKinsey, only one in 8 organizations is successful in fully implementing transformational change completely but the reward is significant: transformers outperform their competition three-to-one on measures of growth and effectiveness.

I am heading to Colorado Springs this weekend for the Governance Institute. There, I will offer Board leaders four basic questions.

Is the future of the U.S. health system a repeat of the past or something else?

How will its structure, roles and responsibilities change?

How will affordability, quality, innovation and value be defined and validated?

How will it be funded?

Answers to these require thoughtful discussion. They require independent judgement. They require insight from organizations outside healthcare whose experiences are instructive. They require fresh thinking.

Until and unless healthcare leaders recognize the imperative for transformational change, the system will calcify its victim-mindset and each sector will fend for itself with diminishing results. No sector—hospitals, insurers, drug companies, physicians—has all the answers and every sector faces enormous headwinds. Perhaps it’s time for a cross-sector coalition to step up with transformational change as the goal and the public’s well-being the moral compass.

PS: Last week, I caught up with Drs. Steve and Pat Gabbe in Columbus, Ohio. Having served alongside them at Vanderbilt and now as an observer of their work at Ohio State, I am reminded of the goodness and integrity of those in healthcare who devote their lives to meaningful, worthwhile work. Steve “burns with a clear blue flame” as a clinician, mentor and educator. Pat is the curator of a program, Moms2B, that seeks to alleviate Black-White disparities in infant mortality and maternal child health in Ohio. They’re great people who see purpose in their calling; they’re what make this industry worth fixing!

CVS has fared better because of its ability to scale and coordinate its other business model resources, Aetna and Signify, analyst says.

The disruption promised by the retailization of healthcare hasn’t materialized as planned.

Walmart and Walgreens recently announced the closing of retail clinics.

“The news is a significant setback for retail health players, some of whom are now realizing that delivering retail-driven primary care may not be economically viable and certainly isn’t causing the disruption in local healthcare markets that many predicted,” said Emarketer senior analyst for digital health Rajiv Leventhal.

Reimbursement for primary care is a major challenge, as are labor shortages and higher costs. Retailers that are not able to scale their clinics through synergies with other parts of their business models, as CVS has done, will find costs rising above their ability to make money.

Walmart is closing all 51 of its health centers across five states, saying the business model was unsustainable.

“Healthcare is very difficult and very challenging,” said Innocent Clement, cofounder and CEO of Ciba Health and a physician by training. “Walmart (was) very disappointing news. I expected a lot. It’s embedded in all of our communities.”

Retail clinics help make healthcare affordable and the convenience of pharmacies creates access for vulnerable populations, Clement said.

Retail based clinics and urgent care clinics play a role in controlling healthcare costs by diverting approximately 30% of cases from much higher-cost emergency rooms.

“Walmart Health’s decision to shut down its health centers and telehealth services is a sudden pivot from its recent plans to expand but not surprising given retailers’ overall struggles in the care delivery space,” Leventhal said.

“It’s not Walmart’s first failed attempt at operating medical clinics, but it will likely be its last crack at it considering how badly it went – going from signing off on a plan in 2018 to build 4,000 primary care clinics to shutting down in 2024 after opening just 51. The latest effort was littered with red flags throughout, from struggling with basic billing and payment functions to leadership changes and other operational obstacles.”

Walgreens suffered a $6 billion loss in its second quarter due to its struggles to make VillageMD profitable. It announced it was closing 60 VillageMD clinics and that number is expected to rise.

Walgreens invested $1 billion in VillageMD and then dumped in $5.2 billion more, Leventhal said. The plan was to keep expanding and co-locating VillageMD clinics with a Walgreens pharmacy. As of last year, Walgreens had 680 clinics with an estimated 200 co-located with a drugstore. Now 140 are already closed with 20 more to close, many of those are co-located with a Walgreens drugstore.

“They’re still leaning into VillageMD investments where they’re succeeding,” Leventhal said. However, “the investment just has not paid off at all. That led to a significant jaw dropping loss.”

Walgreens’ $1 billion cost-cutting strategy should put it in a better position going forward, Leventhal said.

“What many people don’t realize is that urgent care clinics are experiencing a level of extreme financial pressure that endangers their availability, range of services, and continued existence,” said longtime healthcare executive Web Golinkin, a former CEO of RediClinic and FastMed Urgent Care. He recently published a book about his experiences in “Here Be Dragons: One Man’s Quest to Make Healthcare More Accessible and Affordable.”

Reimbursements from third-party payers on services at clinics have been relatively flat over the past recent memory, Golinkin said. This includes both commercial and government payers, Medicare and Medicaid. At the same time, operating costs have increased dramatically.

“It’s difficult for providers to have leverage in a retail health setting. It’s harder than it looks,” Golinkin said. “The reason we were disruptive, we were open seven days a week for extended hours and co-located with a pharmacy.”

But supply and labor costs increased during the pandemic and have not reset, he said. There’s already a shortage of primary care physicians.

RediClinic began inside retail clinics such as Walmart and Walgreens before being sold to Rite Aid in 2014, Golinkin said. FastMed was sold off piecemeal to HCA Healthcare, HonorHealth in Arizona and others.

The bigger picture is the lack of access in this country to primary care, Golinkin said. CMS needs to shift dollars to primary care, he said, a statement backed by the American Medical Association, which has been banging the drum for greater physician reimbursement.

Healthcare has narrow margins to begin with, Golinkin said, but may be able to offset losses in one area with profits from another.

Retail clinics may be able to offset losses through pharmacy sales, with the clinics acting somewhat as a loss leader to getting customers in the store, Leventhal said.

But what’s really needed is the ability to scale and a business model that brings consumers from retail pharmacy sales and the clinic to drug purchases and other care needs, as CVS has done.

The struggles for Walmart and Walgreens are a cautionary tale for other retailers, Leventhal said.

“It’s difficult to operate a primary care startup,” he said.

There are nearly 14,000 urgent care clinics in the United States, Golinkin said, adding that most are under sole ownership and all are under the same financial pressure that caused Walmart to shut down.

“This is not just about Walmart. It’s an access issue,” Golinkin said. “What happened to Walmart is symptomatic.”

The answer may lie in partnerships between providers and retailers.

There are many examples of partnerships between retail medical providers and health systems. Prominent health systems such as Advocate Health Care, Providence, Kaiser Permanente and Cleveland Clinic either provide care in retail pharmacies or are clinically affiliated with one, according to Golinkin.

Walgreens has a partnership with Advocate Health Care.

It makes a lot of sense from a continuity of care perspective, Golinkin said. If someone goes into a clinic in a retail space and sees a clinician associated with a hospital or physician practice, and that doctor or PA or nurse says the consumer needs further care, that person goes to the provider.

Most clinics and urgent care centers are tied now to an EHR for a clinically integrated network.

“This approach will boost referrals for health systems while saving them the costs of maintaining their own outpatient practices,” he said. “That’s the model we’re really going to see going forward, more collaboration.”

WHY THIS MATTERS

CVS Health has created the scale to make its clinics successful, according to Leventhal.

Amazon is also lurking as a potential competitor through its expansion with primary care startup One Medical. Amazon bought One Medical for $3.9 billion last year.

CVS took a hit to its bottom line as well, but that was mostly due to high MA utilization through its insurer, Aetna.

CVS is in a much better position strategically, because it has an insurer, a pharmacy benefit manager and also Signify Health, said Leventhal.

CVS’s Aetna business makes it the most imposing retail health disruptor, he said. This combination of a payer and provider has substantial power in local markets and can influence patient decisions on where to get care.

The company’s acquisition of Oak Street Health and Signify Health gives it a full circle strategy. CVS is leaning into opening more Oak Street clinics within CVS drugstores, Leventhal said.

For example, over 650,000 Medicare beneficiaries (not all of them Aetna members) visit CVS stores in Oak Street geographies each week, CVS data said.

There are over 300,000 Signify Home visits annually in Oak Street geographies. Approximately one in six CVS customers end up scheduling a visit at an Oak Street clinic. CVS promotes this by setting up tables within their drugstores that have material on Oak Street.

Ten percent of Aetna seniors educated by Signify about Oak Street as a primary care option scheduled a Welcome Visit, the presentation said.

CVS was in a competitive battle to acquire Signify Health last year for $8 billion. Signify does risk assessments that are billed to the insurer, which connects them with services, specifically with Oak Street Health.

Even CVS would acknowledge delivering primary care through a retail entity is challenging due to low margins, Leventhal said.

In theory, clinics appeared to be the perfect one-stop shop model. In reality, they faced a bunch of challenges, especially during and after COVID-19, Golinkin said.

THE LARGER TREND

Pharmacies, particularly independents, are also dealing with the cost pressures of reimbursement.

Pharmacies are paid by pharmacy benefit managers a reimbursement fee for dispensing drugs, and over the course of the last 10 years those fees have materially declined, squeezing pharmacy margins, according to Seeking Alpha.

This squeeze is in part why Walgreens Boots Alliance’s cash flows have declined so precipitously and why rivals such as Rite Aid have been forced into bankruptcy, the report said.

The newest model for pharmacies is the cost-plus drug model. CVS, Walmart and Walgreens all have offerings and Walgreens is soon expected to roll out its own cost-plus drug model to create a more sustainable model for pharmacies to be reimbursed.

Walgreens CEO Tim Wentworth, who came aboard in October 2023, recently said that the company is ready to adopt a cost plus drug model, which is similar to the one used by Mark Cuban’s online pharmacy, Cost Plus Drugs.

Cost Plus Drugs, which launched in 2022, works directly with drug manufacturers to avoid PBM middlemen. It lowers prices on medications by basing costs on the manufacturing fee, plus a 15% markup, a $3 pharmacy handling fee and a $5 shipping fee. Cost Plus also transparently displays what it pays for its medicines.

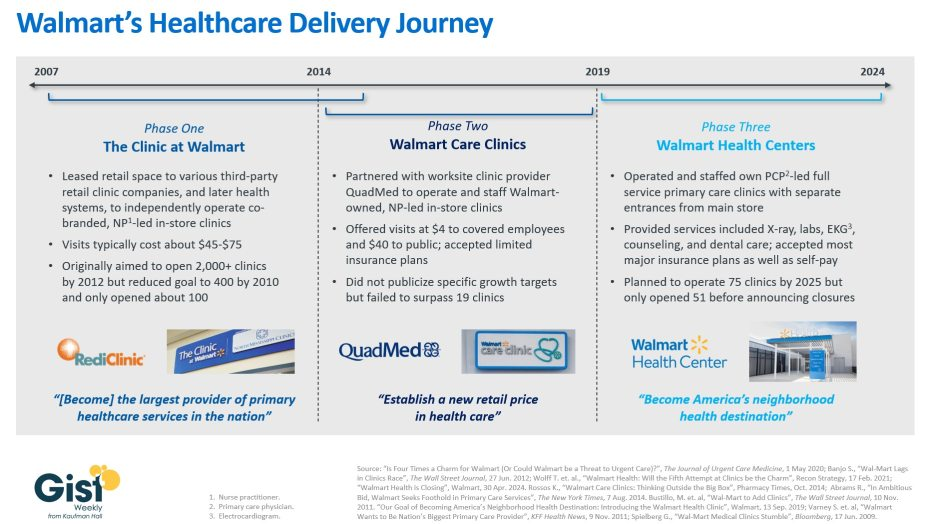

With Walmart’s announcement last week that it plans to shutter its Walmart Health business, this week’s graphic takes stock of the company’s healthcare delivery journey over nearly the past two decades.

In about 2007, Walmart launched “The Clinic at Walmart,” which leased retail space to various third-party retail clinic companies, and then later health systems, to provide basic primary care services inside Walmart stores, with the ambition of eventually becoming “the largest provider of primary healthcare services in the nation.”

However, low volumes and incompatible incentives between Walmart and its contractors led most of these clinics to close over time. In 2014 Walmart partnered with a single company, the worksite clinic provider QuadMed, to launch “Walmart Care Clinics.” These in-store clinics offered $4 visits for covered Walmart employees and $40 visits for the cash-paying public. Despite these low prices, this iteration of care clinic also suffered from low volumes, and Walmart scrapped the idea after opening only 19 of them.

The retail giant’s most recent effort at care delivery began in 2019 with its revamped “Walmart Health Centers,” which it announced alongside its goal to “become America’s neighborhood health destination.”

These health centers, which had separate entrances from the main store, featured physician-led, expanded primary care offerings including X-ray, labs, counseling, and dental services. As recently as April 2024, Walmart said it was planning to open almost two dozen more within the calendar year, until it announced it was shutting down its entire Walmart Health unit, which included virtual care offerings in addition to 51 health centers, citing an unfavorable operating environment.

Despite multiple rebranding efforts, consumers have thus far appeared unwilling to see affordability-focused Walmart as a healthcare provider.

Almost two decades of clinic experimentation have shown the company is willing to try things and admit failure, but it remains to be seen if this is just the end of Walmart’s latest phase or the end of the road for its healthcare delivery ambitions altogether.

Tuesday, the, FTC, and DOJ announced creation of a task force focused on tackling “unfair and illegal pricing” in healthcare. The same day, HHS joined FTC and DOJ regulators in launching an investigation with the DOJ and FTC probing private equity’ investments in healthcare expressing concern these deals may generate profits for corporate investors at the expense of patients’ health, workers’ safety and affordable care.

Thursday’s State of the Union address by President Biden (SOTU) and the Republican response by Alabama Senator Katey Britt put the spotlight on women’s reproductive health, drug prices and healthcare affordability.

Friday, the Senate passed a $468 billion spending bill (75-22) that had passed in the House Wednesday (339-85) averting a government shutdown. The bill postpones an $8 billion reduction in Medicaid disproportionate share hospital payments for a year, allocates $4.27 billion to federally qualified health centers through the end of the year and rolls back a significant portion of a Medicare physician pay cut that kicked in on Jan. 1. Next, Congress must pass appropriations for HHS and other agencies before the March 22 shutdown.

And all week, the cyberattack on Optum’s Change Healthcare discovered February 21 hovered as hospitals, clinics, pharmacies and others scrambled to manage gaps in transaction processing. Notably, the American Hospital Association and others have amplified criticism of UnitedHealth Group’s handling of the disruption, having, bought Change for $13 billion in October, 2022 after a lengthy Department of Justice anti-trust review. This week, UHG indicates partial service of CH support will be restored. Stay tuned.

Just another week for healthcare: Congressional infighting about healthcare spending. Regulator announcements of new rules to stimulate competition and protect consumers in the healthcare market. Lobbying by leading trade groups to protect funding and disable threats from rivals. And so on.

At the macro level, it’s understandable: healthcare is an attractive market, especially in its services sectors. Since the pandemic, prices for services (i.e. physicians, hospitals et al) have steadily increased and remain elevated despite the pressures of transparency mandates and insurer pushback. By contrast, prices for most products (drugs, disposables, technologies et al) have followed the broader market pricing trends where prices for some escalated fast and then dipped.

While some branded prescription medicines are exceptions, it is health services that have driven the majority of health cost inflation since the pandemic.

UnitedHealth Group’s financial success is illustrative:

it’s big, high profile and vertically integrated across all major services sectors. In its year end 2023 financial report (January 12, 2024) it reported revenues of $371.6 Billion (up 15% Year-Over-Year), earnings from operations up 14%, cash flows from operations of $29.1 Billion (1.3x Net Income), medical care ratio at 83.2% up from 82% last year, net earnings of $23.86/share and adjusted net earnings of $25.12/share and guidance its 2024 revenues of $400-403 billion. They buy products using their scale and scope leverage to pay less for services they don’t own less and products needed to support them. It’s a big business in a buyer’s market and that’s unsettling to many.

Big business is not new to healthcare:

it’s been dominant in every sector but of late more a focus of unflattering regulator and media attention. Coupled with growing public discontent about the system’s effectiveness and affordability, it seems it’s near a tipping point.

David Johnson, one of the most thoughtful analysts of the health industry, reminded his readers last week that the current state of affairs in U.S. healthcare is not new citing the January 1970 Fortune cover story “Our Ailing Medical System”

“American medicine, the pride of the nation for many years, stands now on the brink of chaos. To be sure, our medical practitioners have their great moments of drama and triumph. But much of U.S. medical care, particularly the everyday business of preventing and treating routine illnesses, is inferior in quality, wastefully dispensed, and inequitably financed…

Whether poor or not, most Americans are badly served by the obsolete, overstrained medical system that has grown up around them helter-skelter. … The time has come for radical change.”

Johnson added: “The healthcare industry, however, cannot fight gravity forever. Consumerism, technological advances and pro-market regulatory reforms are so powerful and coming so fast that status-quo healthcare cannot forestall their ascendance. Properly harnessed, these disruptive forces have the collective power necessary for U.S. healthcare to finally achieve the 1970 Fortune magazine goal of delivering “good care to every American with little increase in cost.”

He’s right.

I believe the U.S. health system as we know it has reached its tipping point. The big-name organizations in every sector see it and have nominal contingency plans in place; the smaller players are buying time until the shoe drops. But I am worried.

I am worried the system’s future is in the hands of hyper-partisanship by both parties seeking political advantage in election cycles over meaningful creation of a health system that functions for the greater good.

I am worried that the industry’s aversion toprice transparency, meaningful discussion about affordability and consistency in defining quality, safety and value will precipitate short-term gamesmanship for reputational advantage and nullify systemness and interoperability requisite to its transformation.

I am worried that understandably frustrated employers will drop employee health benefits to force the system to needed accountability.

I am worried that the growing armies of under-served and dissatisfied populations will revolt.

I am worried that its workforce is ill-prepared for a future that’s technology-enabled and consumer centric.

I am worried that the industry’s most prominent trade groups are concentrating more on “warfare” against their rivals and less about the long-term future of the system.

I am worried that transformational change is all talk.

It’s time to start an adult conversation about the future of the system. The starting point: acknowledging that it’s not about bad people; it’s about systemic flaws in its design and functioning. Fixing it requires balancing lag indicators about its use, costs and demand with assumptions about innovations that hold promise to shift its trajectory long-term. It requires employers to actively participate: in 2009-2010, Big Business mistakenly chose to sit out deliberations about the Affordable Care Act. And it requires independent, visionary facilitation free from bias and input beyond the DC talking heads that have dominated reform thought leadership for 6 decades.

Or, collectively, we can watch events like last week’s roll by and witness the emergence of a large public utility serving most and a smaller private option for those that afford it. Or something worse.

P.S. Today, thousands will make the pilgrimage to Orlando for HIMSS24 kicking off with a keynote by Robert Garrett, CEO of Hackensack Meridian Health tomorrow about ‘transformational change’ and closing Friday with a keynote by Nick Saban, legendary Alabama football coach on leadership. In between, the meeting’s 24 premier supporters and hundreds of exhibitors will push their latest solutions to prospects and customers keenly aware healthcare’s future is not a repeat of its past primarily due to technology. Information-driven healthcare is dependent on technologies that enable cost-effective, customized evidence-based care that’s readily accessible to individuals where and when they want it and with whom.

And many will be anticipating HCA Mission Health’s (Asheville NC) Plan of Action response due to CMS this Wednesday addressing deficiencies in 6 areas including CMS Deficiency 482.12 “which ensures that hospitals have a responsible governing body overseeing critical aspects of patient care and medical staff appointments.” Interest is high outside the region as the nation’s largest investor-owned system was put in “immediate jeopardy” of losing its Medicare participation status last year at Mission. FYI: HCA reported operating income of $7.7 billion (11.8% operating margin) on revenues of $65 billion in 2023.

Walgreens announced this week that it will be shutting down all of its Florida-based VillageMD primary care clinics. Fourteen clinics in the Sunshine State have already closed, with the remaining 38 expected to follow by March 15.

This move comes in the wake of a $1B cost-cutting initiative announced by Walgreens executives last fall, which included plans to shutter at least 60 VillageMD clinics across five markets in 2024.

Last month VillageMD exited the Indiana market, where it was operating a dozen clinics.

Despite downsizing its primary-care footprint, Walgreens says it remains committed to its expansion into the healthcare delivery sector, having invested $5.2B in VillageMD in 2021 and purchased Summit Health-CityMD for $9B through VillageMD in 2023.

The Gist:Having made significant investments in provider assets, Walgreens now faces the difficult task of creating an integrated and sustainable healthcare delivery model, which takes time.

Unlike long-established healthcare providers who feel more loyal to serving their local communities, nontraditional healthcare providers like Walgreens can more easily pick and choose markets based on profitability.

While this move is disruptive to VillageMD patients in Florida and the other markets it’s exiting, Walgreens seems to be answering to its investors, who have been dissatisfied with its recent earnings.

On Sunday, Miami, FL-based Cano Health, a Medicare Advantage (MA)-focused primary care clinic operator, filed for bankruptcy protection to reorganize and convert around $1B of secured debt into new debt.

The company, which went public in 2020 via a SPAC deal worth over $4B, has now been delisted from the New York Stock Exchange. After posting a $270M loss in Q2 of 2023, Cano began laying off employees, divesting assets, and seeking a buyer. As of Q3 2023, it managed the care of over 300K members, including nearly 200K in Medicare capitation arrangements, at its 126 medical centers.

The Gist:

Like Babylon Health before it, another “tech-enabled” member of the early-COVID healthcare SPAC wave is facing hard times. While the low interest rate-fueled trend of splashy public offerings was not limitedto healthcare, several prominent primary care innovators and “insurtechs” from this wave have struggled, adding further evidence to the adages that healthcare is both hard and difficult to disrupt.

Given that Cano sold its senior-focused clinics in Texas and Nevada to Humana’s CenterWell last fall, Cano may draw interest from other organizations looking to expand their MA footprints.

Earlier this month, leaders from more than 400 organizations descended on San Francisco for J.P. Morgan‘s 42nd annual healthcare conference to discuss some of the biggest issues in healthcare today. Here’s how Advisory Board experts are thinking about Modern Healthcare’s 10 biggest takeaways — and our top resources for each insight.

How we’re thinking about the top 10 takeaways from JPM’s annual healthcare conference

Following the conference, Modern Healthcare provided a breakdown of the top-of-mind issues attendees discussed.

Here’s how our experts are thinking about the top 10 takeaways from the conference — and the resources they recommend for each insight.

1. Ambulatory care provides a growth opportunity for some health systems

By Elizabeth Orr, Vidal Seegobin, and Paul Trigonoplos

At the conference, many health system leaders said they are evaluating growth opportunities for outpatient services.

However, results from our Strategic Planner’s Survey suggest only the biggest systems are investing in building new ambulatory facilities. That data, alongside the high cost of borrowing and the trifurcation of credit that Fitch is predicting, suggests that only a select group of health systems are currently poised to leverage ambulatory care as a growth opportunity.

Systems with limited capital will be well served by considering other ways to reach patients outside the hospital through virtual care, a better digital front door, and partnerships. The efficiency of outpatient operations and how they connect through the care continuum will affect the ROI on ambulatory investments. Buying or building ambulatory facilities does not guarantee dramatic revenue growth, and gaining ambulatory market share does not always yield improved margins.

While physician groups, together with management service organizations, are very good at optimizing care environments to generate margins (and thereby profit), most health systems use ambulatory surgery center development as a defensive market share tactic to keep patients within their system.

This approach leaves margins on the table and doesn’t solve the growth problem in the long term. Each of these ambulatory investments would do well to be evaluated on both their individual profitability and share of wallet.

On January 24 and 25, Advisory Board will convene experts from across the healthcare ecosystem to inventory the predominant growth strategies pursued by major players, explore considerations for specialty care and ambulatory network development, understand volume and site-of-care shifts, and more. Register here to join us for the Redefining Growth Virtual Summit.

Also, check out our resources to help you plan for shifts in patient utilization:

2. Rebounding patient volumes further strain capacity

By Jordan Peterson, Eliza Dailey, and Allyson Paiewonsky

Many health system leaders noted that both inpatient and outpatient volumes have surpassed pre-pandemic levels, placing further strain on workforces.

The rebound in patient volumes, coupled with an overstretched workforce, underscores the need to invest in technology to extend clinician reach, while at the same time doubling down on operational efficiency to help with things like patient access and scheduling.

For leaders looking to leverage technology and boost operational efficiency, we have a number of resources that can help:

3. Health systems aren’t specific on AI strategies

By Paul Trigonoplos and John League

According to Modern Healthcare, nearly all health systems discussed artificial intelligence (AI) at the conference, but few offered detailed implementation plans and expectations.

Over the past year, a big part of the work for Advisory Board’s digital health and health systems research teams has been to help members reframe the fear of missing out (FOMO) that many care delivery organizations have about AI.

We think AI can and will solve problems in healthcare. Every organization should at least be observing AI innovations. But we don’t believe that “the lack of detail on healthcare AI applications may signal that health systems aren’t ready to embrace the relatively untested and unregulated technology,” as Modern Healthcare reported.

The real challenge for many care delivery organizations is dealing with the pace of change — not readiness to embrace or accept it. They aren’t used to having to react to anything as fast-moving as AI’s recent evolution. If their focus for now is on low-hanging fruit, that’s completely understandable. It’s also much more important for these organizations to spend time now linking AI to their strategic goals and building out their governance structures than it is to be first in line with new applications.

Check out our top resources for health systems working to implement AI:

Digital health companies like Teladoc, R1 RCM, Veradigm, and Talkspace all spoke out about their use of generative AI.

This does not surprise us at all. In fact, we would be more surprised if digital health companies were not touting their AI capabilities. Generative AI’s flexibility and ease of use make it an accessible addition to nearly any technology solution.

However, that alone does not necessarily make the solution more valuable or useful. In fact, many organizations would do well to consider how they want to apply new AI solutions and compare those solutions to the ones that they would have used in October 2022 — before ChatGPT’s newest incarnation was unveiled. It may be that other forms of AI, predictive analytics, or robotic process automation are as effective at a better cost.

Again, we believe that AI can and will solve problems in healthcare. We just don’t think it will solve every problem in healthcare, or that every solution benefits from its inclusion.

During the conference, providers criticized insurers for the rate of denials, Modern Healthcare reports.

Denials — along with other utilization management techniques like prior authorization — continue to build tension between payers and providers, with payers emphasizing their importance for ensuring cost effective, appropriate care and providers overwhelmed by both the administrative burden and the impact of denials on their finances.

Many health plans have announced major moves to reduce prior authorizations and CMS recently announced plans to move forward with regulations to streamline the prior authorization process. However, these efforts haven’t significantly impacted providers yet.

In fact, most providers report no decrease in denials or overall administrative burden. A new report found that claims denials increased by 11.99% in the first three quarters of 2023, following similar double digit increases in 2021 and 2022.

Our team is actively researching the root cause of this discrepancy and reasons for the noted increase in denials. Stay tuned for more on improving denials performance — and the broader payer-provider relationship — in upcoming 2024 Advisory Board research.

For now, check out this case study to see how Baptist Health achieved a 0.65% denial write-off rate.

6. Insurers are prioritizing Star Ratings and risk adjustment changes

By Mallory Kirby

Various insurers and providers spoke about “the fallout from star ratings and risk adjustment changes.”

2023 presented organizations focused on MA with significant headwinds. While many insurers prioritized MA growth in recent years, leaders have increased their emphasis on quality and operational excellence to ensure financial sustainability.

With an eye on these headwinds, it makes sense that insurers are upping their game to manage Star Ratings and risk adjustment. While MA growth felt like the priority in years past, this focus on operational excellence to ensure financial sustainability has become a priority.

We’ve already seen litigation from health plans contesting the regulatory changes that impact the bottom line for many MA plans. But with more changes on the horizon — including the introduction of the Health Equity Index as a reward factor for Stars and phasing in of the new Risk Adjustment Data Validation model — plans must prioritize long-term sustainability.

Check out our latest MA research for strategies on MA coding accuracy and Star Ratings:

Pharmacy benefit manager (PBM) leaders discussed the ways they are preparing for potential congressional action, including “updating their pricing models and diversifying their revenue streams.”

Healthcare leaders should be prepared for Congress to move forward with PBM regulation in 2024. A final bill will likely include federal reporting requirements, spread pricing bans, and preferred pricing restrictions for PBMs with their own specialty pharmacy. In the short term, these regulations will likely apply to Medicare and Medicaid population benefits only, and not the commercial market.

Congress isn’t the only entity calling for change. Several states passed bills in the last year targeting PBM transparency and pricing structures. The Federal Trade Commission‘s ongoing investigation into select PBMs looks at some of the same practices Congress aims to regulate. PBM commercial clients are also applying pressure. In 2023, Blue Cross Blue Shield of California‘s (BSC) decided to outsource tasks historically performed by their PBM partner. A statement from BSC indicated the change was in part due to a desire for less complexity and more transparency.

Here’s what this means for PBMs:

Transparency is a must

The level of scrutiny on transparency will force the hand of PBMs. They will have to comply with federal and state policy change and likely give something to their commercial partners to stay competitive. We’re already seeing this unfold across some of the largest PBMs. Recently, CVS Caremarkand Express Scripts launched transparent reimbursement and pricing models for participating in-network pharmacies and plan sponsors.

While transparency requirements will be a headache for larger PBMs, they might be a real threat to smaller companies. Some small PBMs highlight transparency as their main value add. As the larger PBMs focus more on transparency, smaller PBMs who rely on transparent offerings to differentiate themselves in a crowded market may lose their main competitive edge.

PBMs will have to try new strategies to boost revenue

PBM practice of guiding prescriptions to their own specialty pharmacy or those providing more competitive pricing is a key strategy for revenue. Stricter regulations on spread pricing and patient steerage will prompt PBMs to look for additional revenue levers.

PBMs are already getting started — with Express Scripts reporting they will cut reimbursement for wholesale brand name drugs by about 10% in 2024. Other PBMs are trying to diversify their business opportunities. For example, CVS Caremark’s has offered a new TrueCost model to their clients for an additional fee. The model determines drug prices based on the net cost of drugs and clearly defined fee structures. We’re also watching growing interest in cross-benefitutilization management programs for specialty drugs. These offerings look across both medical and pharmacy benefits to ensure that the most cost-effective drug is prescribed for patients.

At the conference, retailers such as CVS, Walgreens, and Amazon doubled down on their healthcare services strategies.

Typically, disruptors do not get into care delivery because they think it will be easy. Disruptors get into care delivery because they look at what is currently available and it looks so hard — hard to access, hard to understand, and hard to pay for.

Many established players still view so-called disruptors as problematic, but we believe that most tech companies that move into healthcare are doing what they usually do — they look at incumbent approaches that make it hard for customers and stakeholders to access, understand, and pay for care, and see opportunities to use technology and innovative business models in an attempt to target these pain points.

CVS, Walgreens, and Amazon are pursuing strategies that are intended to make it more convenient for specific populations to get care. If those efforts aren’t clearly profitable, that does not mean that they will fail or that they won’t pressure legacy players to make changes to their own strategies. Other organizations don’t have to copy these disruptors (which is good because most can’t), but they must acknowledge why patient-consumers are attracted to these offerings.

For more information on how disruptors are impacting healthcare, check out these resources:

9. Financial pressures remain for many health systems

By Vidal Seegobin and Marisa Nives

Health systems are recovering from the worst financial year in recent history. While most large health systems presenting at the conference saw their finances improve in 2023, labor challenges and reimbursement pressures remain.

We would be remiss to say that hospitals aren’t working hard to improve their finances. In fact, operating margins in November 2023 broke 2%. But margins below 3% remain a challenge for long-term financial sustainability.

One of the more concerning trends is that margin growth is not tracking with a large rebound in volumes. There are number of culprits: elevated cost structures, increased patient complexity, and a reimbursement structure shifting towards government payers.

For many systems, this means they need to return to mastering the basics: Managing costs, workforce retention, and improving quality of care. While these efforts will help bridge the margin gap, the decoupling of volumes and margins means that growth for health systems can’t center on simply getting bigger to expand volumes.

Maximizing efficiency, improving access, and bending the cost curve will be the main pillars for growth and sustainability in 2024.

To learn more about what health system strategists are prioritizing in 2024, read our recent survey findings.

Also, check out our resources on external partnerships and cost-saving strategies:

During the conference, MA insurers reported seeing a spike in utilization driven by increased doctor’s visits and elective surgeries.

These increased medical expenses are putting more pressure on MA insurers’ margins, which are already facing headwinds due to CMS changes in MA risk-adjustment and Star Ratings calculations.

However, this increased utilization isn’t all bad news for insurers. Part of the increased utilization among seniors can be attributed to more preventive care, such as an uptick in RSV vaccinations.

In UnitedHealth Group‘s* Q4 earnings call, CFO John Rex noted that, “Interest in getting the shot, especially among the senior population, got some people into the doctor’s office when they hadn’t visited in a while,” which led to primary care physicians addressing other care needs. As seniors are referred to specialty care to address these needs, plans need to have strategies in place to better manage their specialist spend.

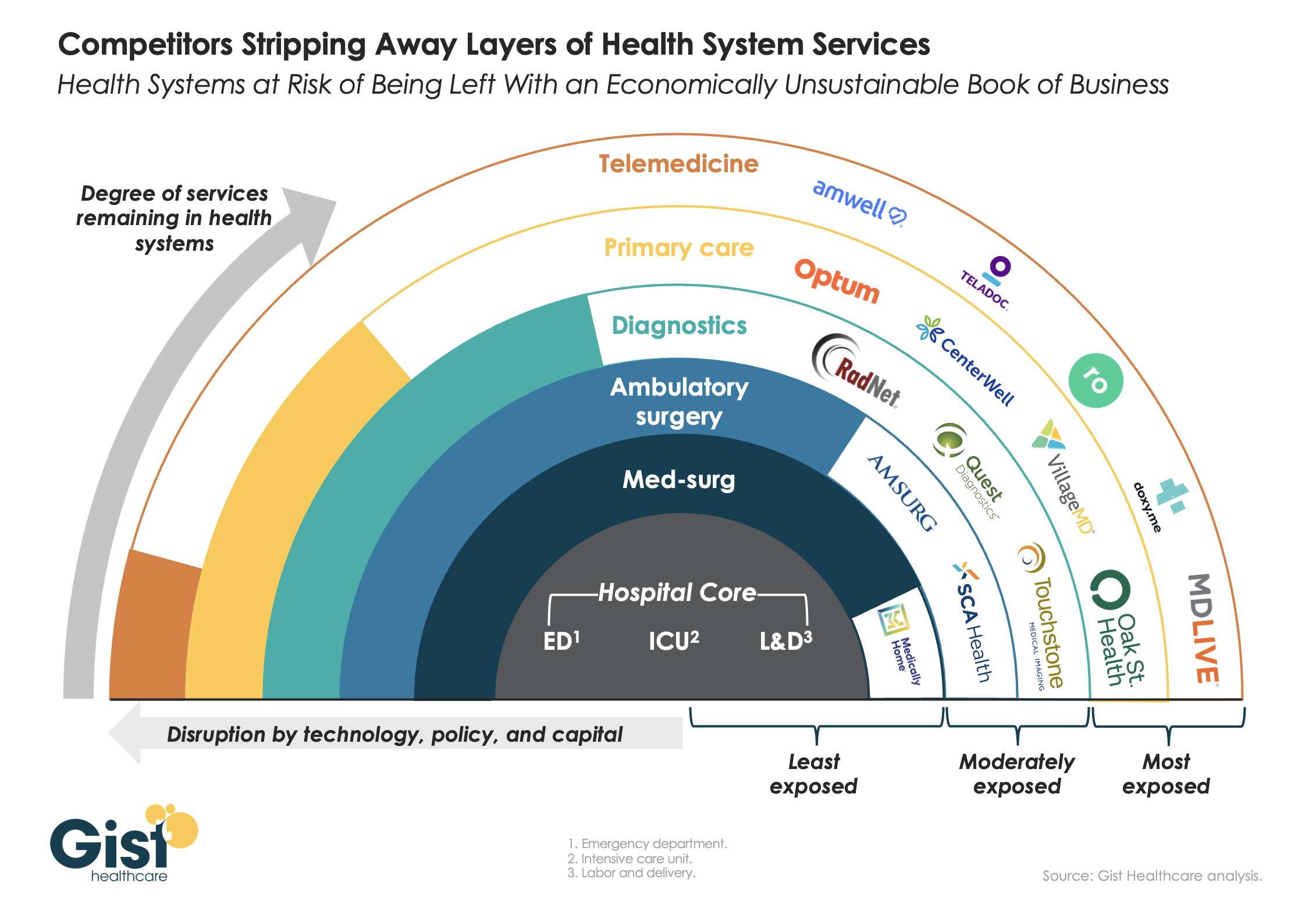

This week’s graphic features our assessment of the many emerging competitive challenges to traditional health systems.

Beyond inflation and high labor costs, health systems are struggling because competitors—ranging from vertically integrated payers to PE-backed physician groups—are effectively stripping away profitable services and moving them to lower-cost care sites. The tandem forces of technological advancement, policy changes, and capital investment have unlocked the ability of disruptors to enter market segments once considered safely within health system control.

While health systems’ most-exposed services, like telemedicine and primary care, were never key revenue sources (although they are key referral drivers), there are now more competitors than ever providing diagnostics and ambulatory surgery, which health systems have relied on to maintain their margins.

Moving forward, traditional systems run the risk of being “crammed down” into a smaller portfolio of (largely unprofitable) services: the emergency department, intensive care unit, and labor and delivery.

Health systems cannot support their operations by solely providing these core services, yet this is the future many will face if they don’temulate the strategies of disruptors by embracing the site-of-care shift, prioritizing high-margin procedures, rethinking care delivery within the hospital, and implementing lower-cost care models that enable them to compete on price.

On Sunday, venture capital (VC) firm General Catalyst unveiled the Health Assurance Transformation Corporation (HATCo), a new subsidiary company which aims to acquire a health system to serve as a blueprint for the VC firm’s vision of healthcare transformation.

Sharing this news on the first day of the HLTH 2023 conference in Las Vegas, General Catalyst declined to comment on which health systems are targets, or how much it is willing to spend, but CEO Hemant Taneja suggested that investment returns would be evaluated on a longer timeline than the typical 10-year venture capital horizon.

Dr. Marc Harrison, the former CEO of Intermountain Health who joined General Catalyst in 2022, has been tapped to lead HATCo. The new company will build on General Catalyst’s previously announced partnerships with health systems, including Intermountain, HCA Healthcare, and Universal Health Services, with the goal of connecting healthcare startups with health systems in order to test and scale their technologies.

The Gist:While private equity firms have backed health systems before, a VC firm expressing interest in health system ownership is a surprising development.

Even on a longer timeframe than most venture plays get, it’s difficult to imagine a health system ever delivering the outsized returns VC investors usually demand. It’s possible HATCo’s true value will come from scaling and selling the services of tech startups in General Catalyst’s portfolio after vetting them at their health system “proving ground”.

HATCo’s more ambitious aim to align payers and providers in a pivot to value-based care is a familiar one, but the new venture will find itself up against skepticism from insurers and other entrenched stakeholders, which has been difficult for even the most motivated health systems to overcome.

Artificial intelligence (AI) has long been heralded as an emerging force in medicine. Since the early 2000s, promises of a technological transformation in healthcare have echoed through the halls of hospitals and at medical meetings.

But despite 20-plus years of hype, AI’s impact on medical practice and America’s health remains negligible (with minor exceptions in areas like radiological imaging and predictive analytics).

As such, it’s understandable that physicians and healthcare administrators are skeptical about the benefits that generative AI tools like ChatGPT will provide.

They shouldn’t be. This next generation of AI is unlike any technology that has come before.

The launch of ChatGPT in late 2022 marked the dawn of a new era. This “large language model” developed by OpenAI first gained notoriety by helping users write better emails and term papers. Within months, a host of generative AI products sprang up from Google, Microsoft and Amazon and others. These tools are quickly becoming more than mere writing assistants.

In time, they will radically change healthcare, empower patients and redefine the doctor-patient relationship. To make sense of this bold vision for the future, this two-part article explores:

The massive differences between generative AI and prior artificial intelligences

How, for the first time in history, a technological innovation will democratize not just knowledge, but also clinical expertise, making medical prowess no longer the sole domain of healthcare professionals.

To understand why this time is different, it’s helpful to compare the limited power of the two earliest generations of AI against the near-limitless potential of the latest version.

Generation 1: Rules-Based Systems And The Dawn Of AI In Healthcare

The latter half of the 20th century ushered in the first generation of artificial intelligence, known as rule-based AI.

Programmed by computer engineers, this type of AI relies on a series of human-generated instructions (rules), enabling the technology to solve basic problems.

In many ways, the rule-based approach resembles a traditional medical-school pedagogy where medical students are taught hundreds of “algorithms” that help them translate a patient’s symptoms into a diagnosis.

These decision-making algorithms resemble a tree, beginning with a trunk (the patient’s chief complaint) and branching out from there. For example, if a patient complains of a severe cough, the doctor first assesses whether fever is present. If yes, the doctor moves to one set of questions and, if not, to a different set. Assuming the patient has been febrile (with fever), the next question is whether the patient’s sputum is normal or discolored. And once again, this leads to the next subdivision. Ultimately each end branch contains only a single diagnosis, which can range from bacterial, fungal or viral pneumonia to cancer, heart failure or a dozen other pulmonary diseases.

This first generation of AI could rapidly process data, sorting quickly through the entire branching tree. And in circumstances where the algorithm could accurately account for all possible outcomes, rule-based AI proved more efficient than doctors.

But patient problems are rarely so easy to analyze and categorize. Often, it’s difficult to separate one set of diseases from another at each branch point. As a result, this earliest form of AI wasn’t as accurate as doctors who combined medical science with their own intuition and experience. And because of its limitations, rule-based AI was rarely used in clinical practice.

Generation 2: Narrow AI And The Rise Of Specialized Systems

As the 21st century dawned, the second era of AI began. The introduction of neural networks, mimicking the human brain’s structure, paved the way for deep learning.

Narrow AI functioned very differently than its predecessors. Rather than researchers providing pre-defined rules, the second-gen system feasted on massive data sets, using them to discern patterns that the human mind, alone, could not.

In one example, researchers gave a narrow AI system thousands of mammograms, half showing malignant cancer and half benign. The model was able to quickly identify dozens of differences in the shape, density and shade of the radiological images, assigning impact factors to each that reflected the probability of malignancy. Importantly, this kind of AI wasn’t relying on heuristics (a few rules of thumb) the way humans do, but instead subtle variations between the malignant and normal exams that neither the radiologists nor software designers knew existed.

In contrast to rule-based AI, these narrow AI tools proved superior to the doctor’s intuition in terms of diagnostic accuracy. Still, narrow AI showed serious limitations. For one, each application is task specific. Meaning, a system trained to read mammograms can’t interpret brain scans or chest X-rays.

But the biggest limitation of narrow AI is that the system is only as good as the data it’s trained on. A glaring example of that weakness emerged when United Healthcare relied on narrow AI to identify its sickest patients and give them additional healthcare services.

In filtering through the data, researchers later discovered the AI had made a fatal assumption. Patients who received less medical care were categorized as healthier than patients who received more. In doing so, the AI failed to recognize that less treatment is not always the result of better health. This can also be the result of implicit human bias.

Indeed, when researchers went back and reviewed the outcomes, they found Black patients were being significantly undertreated and were, therefore, underrepresented in the group selected for additional medical services.

Media headlines proclaimed, “Healthcare algorithm has racial bias,” but it wasn’t the algorithm that had discriminated against Black patients. It was the result of physicians providing Black patients with insufficient and inequitable treatment. In other words, the problem was the humans, not narrow AI.

Generation 3: The Future Is Generative

Throughout history, humankind has produced a few innovations (printing press, internet, iPhone) that transformed society by democratizing knowledge—making information easier to access for everyone, not just the wealthy elite.

Now, generative AI is poised to go one step further, giving every individual access to not only knowledge but, more importantly, expertise as well.

Already, the latest AI tools allow users to create a stunning work of art in the style of Rembrandt without ever having taken a painting class. With large language models, people can record a hit song, even if they’ve never played a musical instrument. Individuals can write computer code, producing sophisticated websites and apps, despite never having enrolled in an IT course.

Future generations of generative AI will do the same in medicine, allowing people who never attended medical school to diagnose diseases and create a treatment plan as well as any clinician.

Already, one generative AI tool (Google’s Med-PaLM 2) passed the physician licensing exam with an expert level score. Another generative AI toolset responded to patient questions with advice that bested doctors in both accuracy and empathy. These tools can now write medical notes that are indistinguishable from the entries that physicians create and match residents’ ability to make complex diagnoses on difficult cases.

Granted, current versions require physician oversight and are nowhere close to replacing doctors. But at their present rate of exponential growth, these applications are expected to become at least 30 times more powerful in the next five years. As a result, they will soon empower patients in ways that were unimaginable even a year ago.

Unlike their predecessors, these models are pre-trained on datasets that encompass the near-totality of publicly available information—pulling from medical textbooks, journal articles, open-source platforms and the internet. In the not-distant future, these tools will be securely connected to electronic health records in hospitals, as well as to patient monitoring devices in the home. As generative AI feeds on this wealth of data, its clinical acumen will skyrocket.

Within the next five to 10 years, medical expertise will no longer be the sole domain of trained clinicians. Future generations of ChatGPT and its peers will put medical expertise in the hands of all Americans, radically altering the relationship between doctors and patients.

Whether physicians embrace this development or resist is uncertain. What is clear is the opportunity for improvement in American medicine. Today, an estimated 400,000 people die annually from misdiagnoses, 250,000 from medical errors, and 1.7 million from mostly preventable chronic diseases and their complications.

In the next article, I’ll offer a blueprint for Americans as they grapple to redefine the doctor-patient relationship in the context of generative AI. To reverse the healthcare failures of today, the future of medicine will have to belong to the empowered patient and the tech-savvy physician. The combination will prove vastly superior to either alone.