The nonprofit health system narrowed its operating loss while continuing to grapple with financial and policy pressures as it progresses towards profitability.

KEY TAKEAWAYS

Providence cut its operating loss in the second quarter to $21 million, improving from a $123 million loss a year ago.

Revenue rose 3% year-over-year to $7.91 billion, driven by higher patient volumes and better commercial rates.

The health system faces ongoing “polycrisis” challenges, including rising supply costs, staffing mandates, insurer denials, and looming Medicaid cuts, which have already prompted layoffs, hiring pauses, and leadership restructuring.

Providence made promising strides toward financial sustainability in the second quarter as higher patient volumes helped trim an operating loss that has weighed heavily on its balance sheet.

Yet the Renton, Washington-based health system warned that a compounding set of external pressures, which it labeled a “polycrisis,” still poses formidable challenges to its mission and future.

For the three months ended June 30, the nonprofit reported an operating loss of $21 million, equating to an operating margin of –0.3%, representing a marked improvement from the $123 million loss (–1.6%) posted over the same period in 2024. Compared with the previous quarter, the gain was even starker as Providence trimmed its deficit by $223 million. Through the first six months of the year, the health system had an operating loss of $265 million (-1.7%).

Revenue growth was fueled by higher patient volumes and improved commercial rates, Providence highlighted. Operating revenue rose 3% year-over-year to $7.91 billion as inpatient admissions (up 3%), outpatient visits (up 3%), case mix–adjusted admissions (up 3%), physician visits (up 8%), and outpatient surgeries (up 5%) all contributed.

On the expense side, Providence managed a 2% rise in operating costs to $7.93 billion, thanks largely to productivity gains, including a 43% reduction in agency contract labor. However, supply costs swelled by 9% and pharmacy expenses jumped by 12% year-over-year.

Providence, along with the healthcare industry at large, faces what CEO Erik Wexler called a “polycrisis” due to a mix of inflation, tariff-driven supply pressures, new state laws on staffing and charity care, insurer reimbursement delays and denials, and looming federal Medicaid cuts, especially from the One Big Beautiful Bill Act, which the health system said “threatens to intensify health care pressures.”

Those factors are significantly influencing hospitals’ and health systems’ decision-making. Providence has made staffing adjustments that include cutting 128 jobs in Oregon earlier this month, a restructuring in June that eliminated 600 full-time equivalent positions, apause on nonclinical hiring in April, and leadership reorganization since Wexler took over as CEO in January.

Accounts receivable is another area that has been indicative of headwinds, with Providence noting that while it improved in the second quarter, it “remains elevated compared to historical trends.”

Even with the roadblocks in its path, Providence is working towards profitability after being in the red for several years running.

“I’m incredibly proud of the progress we’ve made and grateful to our caregivers and teams across Providence St. Joseph Health for their continued dedication,” Wexler said in the news release. “The strain remains, especially with emerging challenges like H.R.1, but we will continue to respond to the times and answer the call while transforming for the future.”

Companies grappling with liquidity concerns are looking to cut costs and streamline operations, according to a new survey.

Dive Brief:

Over three-quarters of healthcare chief financial officers expect to see profitability increases in 2024, according to a recent survey from advisory firm BDO USA. However, to become profitable, many organizations say they will have to reduce investments in underperforming service lines, or pursue mergers and acquisitions.

More than 40% of respondents said theywill decrease investments in primary care and behavioral health services in 2024, citing disruptions from retail players. They will shift funds to home care, ambulatory services and telehealth that provide higher returns, according to the report.

Nearly three-quarters of healthcare CFOs plan to pursue some type of M&A deal in the year ahead, despite possible regulatory threats.

Dive Insight:

Though inflationary pressures have eased since the height of the COVID-19 pandemic, healthcare CFOs remain cognizant of managing costs amid liquidity concerns, according to the report.

The firmpolled 100 healthcare CFOs serving hospitals, medical groups, outpatient services, academic centers and home health providers with revenues from $250 million to $3 billion or more in October 2023.

Just over a third of organizations surveyed carried more than 60 days of cash on hand. In comparison, a recent analysis from KFF found that financially strong health systems carried at least 150 days of cash on hand in 2022.

Liquidity is a concern for CFOs given high rates of bond and loan covenant violations over the past year. More than half of organizations violated such agreements in 2023, while 41% are concerned they will in 2024, according to the report.

To remain solvent, 44% of CFOs expect to have more strategic conversations about their economic resiliency in 2024, exploring external partnerships, options for service line adjustments and investments in workforce and technology optimization.

Most organizations are interested in exploring sales, according to the report. Financially struggling organizations are among the most likely to consider deals. Nearly one in three organizations that violated their bond or loan covenants in 2023 are planning a carve-out or divestiture this year. Organizations with less than 30 days of cash on hand are also likely to consider carve-outs.

Organizations will also turn to automation to cut costs. Ninety-eight percent of organizations surveyed had pilotedgenerative AI tools in a bid to alleviate resource and cost constraints, according to the consultancy.

“Healthcare leaders believe AI will be essential to helping clinicians operate at the top of their licenses, focusing their time on patient care and interaction over administrative or repetitive tasks,” authors wrote. Nearly one in three CFOs plan to leverage automation and AI in the next 12 months.

However, CFOs are keeping an eye on the risks. As more data flows through their organizations, they are increasingly concerned about cybersecurity. More than half of executives surveyed said data breaches are a bigger risk in 2024 compared to 2023.

Earlier this month, leaders from more than 400 organizations descended on San Francisco for J.P. Morgan‘s 42nd annual healthcare conference to discuss some of the biggest issues in healthcare today. Here’s how Advisory Board experts are thinking about Modern Healthcare’s 10 biggest takeaways — and our top resources for each insight.

How we’re thinking about the top 10 takeaways from JPM’s annual healthcare conference

Following the conference, Modern Healthcare provided a breakdown of the top-of-mind issues attendees discussed.

Here’s how our experts are thinking about the top 10 takeaways from the conference — and the resources they recommend for each insight.

1. Ambulatory care provides a growth opportunity for some health systems

By Elizabeth Orr, Vidal Seegobin, and Paul Trigonoplos

At the conference, many health system leaders said they are evaluating growth opportunities for outpatient services.

However, results from our Strategic Planner’s Survey suggest only the biggest systems are investing in building new ambulatory facilities. That data, alongside the high cost of borrowing and the trifurcation of credit that Fitch is predicting, suggests that only a select group of health systems are currently poised to leverage ambulatory care as a growth opportunity.

Systems with limited capital will be well served by considering other ways to reach patients outside the hospital through virtual care, a better digital front door, and partnerships. The efficiency of outpatient operations and how they connect through the care continuum will affect the ROI on ambulatory investments. Buying or building ambulatory facilities does not guarantee dramatic revenue growth, and gaining ambulatory market share does not always yield improved margins.

While physician groups, together with management service organizations, are very good at optimizing care environments to generate margins (and thereby profit), most health systems use ambulatory surgery center development as a defensive market share tactic to keep patients within their system.

This approach leaves margins on the table and doesn’t solve the growth problem in the long term. Each of these ambulatory investments would do well to be evaluated on both their individual profitability and share of wallet.

On January 24 and 25, Advisory Board will convene experts from across the healthcare ecosystem to inventory the predominant growth strategies pursued by major players, explore considerations for specialty care and ambulatory network development, understand volume and site-of-care shifts, and more. Register here to join us for the Redefining Growth Virtual Summit.

Also, check out our resources to help you plan for shifts in patient utilization:

2. Rebounding patient volumes further strain capacity

By Jordan Peterson, Eliza Dailey, and Allyson Paiewonsky

Many health system leaders noted that both inpatient and outpatient volumes have surpassed pre-pandemic levels, placing further strain on workforces.

The rebound in patient volumes, coupled with an overstretched workforce, underscores the need to invest in technology to extend clinician reach, while at the same time doubling down on operational efficiency to help with things like patient access and scheduling.

For leaders looking to leverage technology and boost operational efficiency, we have a number of resources that can help:

3. Health systems aren’t specific on AI strategies

By Paul Trigonoplos and John League

According to Modern Healthcare, nearly all health systems discussed artificial intelligence (AI) at the conference, but few offered detailed implementation plans and expectations.

Over the past year, a big part of the work for Advisory Board’s digital health and health systems research teams has been to help members reframe the fear of missing out (FOMO) that many care delivery organizations have about AI.

We think AI can and will solve problems in healthcare. Every organization should at least be observing AI innovations. But we don’t believe that “the lack of detail on healthcare AI applications may signal that health systems aren’t ready to embrace the relatively untested and unregulated technology,” as Modern Healthcare reported.

The real challenge for many care delivery organizations is dealing with the pace of change — not readiness to embrace or accept it. They aren’t used to having to react to anything as fast-moving as AI’s recent evolution. If their focus for now is on low-hanging fruit, that’s completely understandable. It’s also much more important for these organizations to spend time now linking AI to their strategic goals and building out their governance structures than it is to be first in line with new applications.

Check out our top resources for health systems working to implement AI:

Digital health companies like Teladoc, R1 RCM, Veradigm, and Talkspace all spoke out about their use of generative AI.

This does not surprise us at all. In fact, we would be more surprised if digital health companies were not touting their AI capabilities. Generative AI’s flexibility and ease of use make it an accessible addition to nearly any technology solution.

However, that alone does not necessarily make the solution more valuable or useful. In fact, many organizations would do well to consider how they want to apply new AI solutions and compare those solutions to the ones that they would have used in October 2022 — before ChatGPT’s newest incarnation was unveiled. It may be that other forms of AI, predictive analytics, or robotic process automation are as effective at a better cost.

Again, we believe that AI can and will solve problems in healthcare. We just don’t think it will solve every problem in healthcare, or that every solution benefits from its inclusion.

During the conference, providers criticized insurers for the rate of denials, Modern Healthcare reports.

Denials — along with other utilization management techniques like prior authorization — continue to build tension between payers and providers, with payers emphasizing their importance for ensuring cost effective, appropriate care and providers overwhelmed by both the administrative burden and the impact of denials on their finances.

Many health plans have announced major moves to reduce prior authorizations and CMS recently announced plans to move forward with regulations to streamline the prior authorization process. However, these efforts haven’t significantly impacted providers yet.

In fact, most providers report no decrease in denials or overall administrative burden. A new report found that claims denials increased by 11.99% in the first three quarters of 2023, following similar double digit increases in 2021 and 2022.

Our team is actively researching the root cause of this discrepancy and reasons for the noted increase in denials. Stay tuned for more on improving denials performance — and the broader payer-provider relationship — in upcoming 2024 Advisory Board research.

For now, check out this case study to see how Baptist Health achieved a 0.65% denial write-off rate.

6. Insurers are prioritizing Star Ratings and risk adjustment changes

By Mallory Kirby

Various insurers and providers spoke about “the fallout from star ratings and risk adjustment changes.”

2023 presented organizations focused on MA with significant headwinds. While many insurers prioritized MA growth in recent years, leaders have increased their emphasis on quality and operational excellence to ensure financial sustainability.

With an eye on these headwinds, it makes sense that insurers are upping their game to manage Star Ratings and risk adjustment. While MA growth felt like the priority in years past, this focus on operational excellence to ensure financial sustainability has become a priority.

We’ve already seen litigation from health plans contesting the regulatory changes that impact the bottom line for many MA plans. But with more changes on the horizon — including the introduction of the Health Equity Index as a reward factor for Stars and phasing in of the new Risk Adjustment Data Validation model — plans must prioritize long-term sustainability.

Check out our latest MA research for strategies on MA coding accuracy and Star Ratings:

Pharmacy benefit manager (PBM) leaders discussed the ways they are preparing for potential congressional action, including “updating their pricing models and diversifying their revenue streams.”

Healthcare leaders should be prepared for Congress to move forward with PBM regulation in 2024. A final bill will likely include federal reporting requirements, spread pricing bans, and preferred pricing restrictions for PBMs with their own specialty pharmacy. In the short term, these regulations will likely apply to Medicare and Medicaid population benefits only, and not the commercial market.

Congress isn’t the only entity calling for change. Several states passed bills in the last year targeting PBM transparency and pricing structures. The Federal Trade Commission‘s ongoing investigation into select PBMs looks at some of the same practices Congress aims to regulate. PBM commercial clients are also applying pressure. In 2023, Blue Cross Blue Shield of California‘s (BSC) decided to outsource tasks historically performed by their PBM partner. A statement from BSC indicated the change was in part due to a desire for less complexity and more transparency.

Here’s what this means for PBMs:

Transparency is a must

The level of scrutiny on transparency will force the hand of PBMs. They will have to comply with federal and state policy change and likely give something to their commercial partners to stay competitive. We’re already seeing this unfold across some of the largest PBMs. Recently, CVS Caremarkand Express Scripts launched transparent reimbursement and pricing models for participating in-network pharmacies and plan sponsors.

While transparency requirements will be a headache for larger PBMs, they might be a real threat to smaller companies. Some small PBMs highlight transparency as their main value add. As the larger PBMs focus more on transparency, smaller PBMs who rely on transparent offerings to differentiate themselves in a crowded market may lose their main competitive edge.

PBMs will have to try new strategies to boost revenue

PBM practice of guiding prescriptions to their own specialty pharmacy or those providing more competitive pricing is a key strategy for revenue. Stricter regulations on spread pricing and patient steerage will prompt PBMs to look for additional revenue levers.

PBMs are already getting started — with Express Scripts reporting they will cut reimbursement for wholesale brand name drugs by about 10% in 2024. Other PBMs are trying to diversify their business opportunities. For example, CVS Caremark’s has offered a new TrueCost model to their clients for an additional fee. The model determines drug prices based on the net cost of drugs and clearly defined fee structures. We’re also watching growing interest in cross-benefitutilization management programs for specialty drugs. These offerings look across both medical and pharmacy benefits to ensure that the most cost-effective drug is prescribed for patients.

At the conference, retailers such as CVS, Walgreens, and Amazon doubled down on their healthcare services strategies.

Typically, disruptors do not get into care delivery because they think it will be easy. Disruptors get into care delivery because they look at what is currently available and it looks so hard — hard to access, hard to understand, and hard to pay for.

Many established players still view so-called disruptors as problematic, but we believe that most tech companies that move into healthcare are doing what they usually do — they look at incumbent approaches that make it hard for customers and stakeholders to access, understand, and pay for care, and see opportunities to use technology and innovative business models in an attempt to target these pain points.

CVS, Walgreens, and Amazon are pursuing strategies that are intended to make it more convenient for specific populations to get care. If those efforts aren’t clearly profitable, that does not mean that they will fail or that they won’t pressure legacy players to make changes to their own strategies. Other organizations don’t have to copy these disruptors (which is good because most can’t), but they must acknowledge why patient-consumers are attracted to these offerings.

For more information on how disruptors are impacting healthcare, check out these resources:

9. Financial pressures remain for many health systems

By Vidal Seegobin and Marisa Nives

Health systems are recovering from the worst financial year in recent history. While most large health systems presenting at the conference saw their finances improve in 2023, labor challenges and reimbursement pressures remain.

We would be remiss to say that hospitals aren’t working hard to improve their finances. In fact, operating margins in November 2023 broke 2%. But margins below 3% remain a challenge for long-term financial sustainability.

One of the more concerning trends is that margin growth is not tracking with a large rebound in volumes. There are number of culprits: elevated cost structures, increased patient complexity, and a reimbursement structure shifting towards government payers.

For many systems, this means they need to return to mastering the basics: Managing costs, workforce retention, and improving quality of care. While these efforts will help bridge the margin gap, the decoupling of volumes and margins means that growth for health systems can’t center on simply getting bigger to expand volumes.

Maximizing efficiency, improving access, and bending the cost curve will be the main pillars for growth and sustainability in 2024.

To learn more about what health system strategists are prioritizing in 2024, read our recent survey findings.

Also, check out our resources on external partnerships and cost-saving strategies:

During the conference, MA insurers reported seeing a spike in utilization driven by increased doctor’s visits and elective surgeries.

These increased medical expenses are putting more pressure on MA insurers’ margins, which are already facing headwinds due to CMS changes in MA risk-adjustment and Star Ratings calculations.

However, this increased utilization isn’t all bad news for insurers. Part of the increased utilization among seniors can be attributed to more preventive care, such as an uptick in RSV vaccinations.

In UnitedHealth Group‘s* Q4 earnings call, CFO John Rex noted that, “Interest in getting the shot, especially among the senior population, got some people into the doctor’s office when they hadn’t visited in a while,” which led to primary care physicians addressing other care needs. As seniors are referred to specialty care to address these needs, plans need to have strategies in place to better manage their specialist spend.

West Reading, Pa.-based Tower Health has turned down a $706 million offer from StoneBridge Healthcare, a hospital turnaround firm, making this the fourth purchase offer rejected by the system since 2021.

StoneBridge received an email from Andrew Turnbull, a managing director at Houlihan Lokey, an investment bank that works with Tower Health, saying that there had been a board meeting and the firm’s offer had been rejected, Joshua Nemzoff, CEO of StoneBridge Healthcare, told Becker’s.

“I’m not sure what they’re thinking. We have requested multiple board meetings, but we’ve never had a chance to meet with the board. We’ve just gotten emails back saying they’re rejecting the offer,” Mr. Nemzoff said.

WoodBridge, a nonprofit sister organization to StoneBridge, initially shared a nonbinding agreement in principle with Tower Health, which included the intent to purchase the system’s assets.

“We’ve given them a number of other offers. I think the last one was more than a year ago. They’ve lost $400 million in operations in the last two years, and they’re $1.8 billion in revenue and $1.5 billion in debt, and 30 days of cash,” Mr. Nemzoff told Becker’s.

Tower Health initially turned down a $675 million offer from StoneBridge in November 2022. In partnership with Allentown, Pa.-based Lehigh Valley Health Network, the firm also made two conditional offers to acquire the system’s assets for $600 million in 2021, which were also rejected.

“Given their cash position and given their extraordinary amount of debt, I think our plan is just to frankly to wait for them to go bankrupt and show up in court for the auction. I think that’s going to happen next year,” Mr. Nemzoff said.

StoneBridge was formed in 2020. The firm currently does not own or operate any hospitals. Like StoneBridge, WoodBridge has also not completed any hospital deals, Mr. Nemzoff told Becker’s.

Three Philadelphia-based hospitals are reportedly up for sale, according to an email notice from Los Angeles-based investment bank Xnergy, The Philadelphia Inquirer reported Dec. 19.

The names of three hospitals are not confirmed. And the notice, which was obtained by the publication, did not name an owner of the hospitals. However, it did describe the hospitals’ owner as one that has acute care facilities with an average of 136 beds.

Three Philadelphia-area hospitals fit the bed parameters in the notice: Bristol-based Lower Bucks Hospital, Philadelphia-based Roxborough Memorial Hospital, and Norristown-based Suburban Community Hospital. All three are owned by Ontario, Calif.-based Prime Healthcare Services, The Philadelphia Inquirer reported.

Roxborough and Lower Bucks were acquired by Prime in 2012, with Suburban acquired by Prime’s nonprofit affiliate Prime Healthcare Foundation in 2016. The hospitals have also seen significant annual operating loss over the last five years with a 43% combined inpatient volume drop, from 3,795 discharges in 2018 to 2,250 discharges in 2022, the publication shared.

Members of the Pennsylvania Association of Staff Nurses & Allied Professionals at both Suburban and Lower Bucks are also set to launch five-day strikes Dec. 22 due to ongoing labor contract negotiations for things like increased wages and important benefits, a union spokesperson told Becker’s.

“Prime Healthcare’s mission is to always do what’s best for our communities and patients, however, we do not comment on strategic merger and acquisition initiatives,” Elizabeth Nikels, vice president of communications and public relations for Prime Healthcare, said in an email response to Becker’s regarding the sale.

Hospitals and health systems are seeing some signs of stabilization in 2023 following an extremely difficult year in 2022. Workforce-related challenges persist, however, keeping costs high and contributing to issues with patient access to care. The percentage of respondents who report that they have run at less than full capacity at some time over the past year because of staffing shortages, for example, remains at 66%, unchanged from last year’s State of Healthcare Performance Improvement report. A solid majority of respondents (63%) are struggling to meet demand within their physician enterprise, with patient concerns or complaints about access to physician clinics increasing at approximately one-third (32%) of respondent organizations.

Most organizations are pursuing multiple strategies to recruit and retain staff. They recognize, however, that this is an issue that will take years to resolve—especially with respect to nursing staff—as an older generation of talent moves toward retirement and current educational pipelines fail to generate an adequate flow of new talent. One bright spot is utilization of contract labor, which is decreasing at almost two-thirds (60%) of respondent organizations.

Many of the organizations we interviewed have recovered from a year of negative or breakeven operating margins. But most foresee a slow climb back to the 3% to 4% operating margins that help ensure long-term sustainability, with adequate resources to make needed investments for the future. Difficulties with financial performance are reflected in the relatively high percentage of respondents (24%) who report that their organization has faced challenges with respect to debt covenants over the past year, and the even higher percentage (34%) who foresee challenges over the coming year. Interviews confirmed that some of these challenges were “near misses,” not an actual breach of covenants, but hitting key metrics such as days cash on hand and debt service coverage ratios remains a concern.

As in last year’s survey, an increased rate of claims denials has had the most significant impact on revenue cycle over the past year. Interviewees confirm that this is an issue across health plans, but it seems particularly acute in markets with a higher penetration of Medicare Advantage plans. A significant percentage of respondents also report a lower percentage of commercially insured patients (52%), an increase in bad debt and uncompensated care (50%), and a higher percentage of Medicaid patients (47%).

Supply chain issues are concentrated largely in distribution delays and raw product and sourcing availability. These issues are sometimes connected when difficulties sourcing raw materials result in distribution delays. The most common measures organizations are taking to mitigate these issues are defining approved vendor product substitutes (82%) and increasing inventory levels (57%). Also, as care delivery continues to migrate to outpatient settings, organizations are working to standardize supplies across their non-acute settings and align acute and non-acute ordering to the extent possible to secure volume discounts.

Survey Highlights

98% of respondents are pursuing one or more recruitment and retention strategies

90%have raised starting salaries or the minimum wage

73%report an increased rate of claims denials

71% are encountering distribution delays in their supply chain

70%are boarding patients in the emergency department or post-anesthesia care unit because of a lack of staffing or bed capacity

66% report that staffing shortages have required their organization to run at less than full capacity at some time over the past year

63% are struggling to meet demand for patient access to their physician enterprise

60% see decreasing utilization of contract labor at their organization

44%report that inpatient volumes remain below pre-pandemic levels

32% say that patients concerns or complaints about access to their physician enterprise are increasing

24%have encountered debt covenant challenges during the past 12 months

None of our respondents believe that their organization has fully optimized its use of the automation technologies in which it has already invested

So far, 2023 is shaping up to be a slightly better year for hospital performance, but it comes on the heels of unprecedented financial difficulties for the sector.

In the graphic above, we evaluated nearly 30 years of historical data from Kaufman Hall and the American Hospital Association to provide a broader perspective on hospital operating margins over time. 2020 and 2022 have been the only years in which a majority of hospitals—53 percent—posted a negative operating margin.

During the most comparable periods of recent economic hardship, the “dot-com bubble burst” of the late 1990s and the 2009 Great Recession, the share of hospitals with negative operating margins amounted to only 42 and 32 percent, respectively.

With this context, hospitals’ current financial distress is more severe than anything we’ve seen in the past three decades.

Healthcare is clearly no longer recession-proof: a four percent operating margin—the level needed for health systems to not only sustain operations but also invest in growth—feels even more elusive as labor costs remain high, surgical care continues to shift to outpatient settings, the second half of the Baby-Boom generation ages into Medicare, and deep-pocketed competitors compete for profitable services.

Fitch Ratings Senior Director Kevin Holloran dubbed 2022 the worst operating year ever and most nonprofit health systems reported large losses. However, the losses are shrinking and some systems have even reported gains during 2023 so far.

Cleveland Clinic reported $335.5 million net income for the first quarter of the year, compared with a $282.5 million loss over the same period in 2022. The health system reported revenue of $3.5 billion for the quarter. Cleveland Clinic has 321 days cash on hand, which puts it in a strong position for the future.

Boston-based Mass General Brighamreported $361 million gain for the second quarter ending March 31, which is up from a $867 million loss in the same period last year. The health system reported quarterly revenue jumped 11 percent year over year to $4.5 billion. The system’s quarterly loss on operations was down significantly this year, hitting $8 million, compared to $183 million last year.

Renton, Wash.-based Providence reported first quarter revenues were up 5.1 percent in 2023 to $7.1 billion, and operating loss is also moving in the right direction. The system reported $345 million operating loss in the first quarter of 2023, down from $510 million last year.

All three systems cited ongoing labor shortages and labor costs as a challenge, but are working on initiatives to reduce expenses. Cleveland Clinic and Mass General Brigham reported operating margin improvement to nearly positive numbers.

Kaiser Permanente, based in Oakland, Calif., also reported operating income at $233 million for the first quarter of the year, an increase from $72 million operating loss over the same period last year. The system is focused on advancing value-based care for the remainder of the year and its health plan grew more than 120,000 members year over year.

Even more regional systems are stemming their losses. SSM Health, based in St. Louis, went from a $57.4 million loss for the first quarter of 2022 to $16.5 million quarterly loss this year. Revenue increased 13.3 percent to $2.5 billion for the quarter, with increased labor expenses and inflation on supply costs continuing to weigh on the system.

UCHealth in Aurora, Colo., also reported a first quarter income of $61.8 million and revenue of more than $5 billion.

Not every system is seeing losses decline. Chicago-based CommonSpirit Health, which reported larger operating losses in the first quarter year over year, hitting $658 million and $1.1 billion for the nine-month’s end March 31. The system was able to reduce contract labor costs, but still finds hiring a challenge and spent time last year recovering from a cybersecurity incident.

Hospitals face a long road to financial recovery from the pandemic as inflation persists and labor shortages become the norm, but movement in the right direction is welcome.

Last month, Eric Jordahl, Managing Director of Kaufman Hall’s Treasury and Capital Markets practice, blogged about the dangers of nonprofit healthcare providers’ extremely conservative risk management in today’s uncertain economy.

Healthcare public debt issuance in the first quarter of 2023 was down almost 70 percent compared to the first quarter of 2022. While not the only funding channel for not-for-profit healthcare organizations,

the level of public debt issuance is a bellwether for the ambition of the sector’s capital formation strategies.

While health systems have plenty of reasons to be cautious about credit management right now, it’s important not to underrate the dangers of being too risk averse. As Jordahl puts it: “Retrenchment might be the right risk management choice in times of crisis, but once that crisis moderates that same strategy can quickly become a risk driver.”

The Gist: Given current market conditions, there are a host of good reasons why caution reigns among nonprofit health systems, but this current holding pattern for capital spending endangers their future competitiveness and potentially even their survival.

Nonprofit systems aren’t just at risk of losing a competitive edge to vertically integrated payers, whom the pandemic market treated far more kindly in financial terms, but also to for-profit national systems, like HCA and Tenet, who have been flywheeling strong quarterly results into revamped growth and expansion plans.

Health systems should be wary of becoming stuck on defense while the competition is running up the score.

The healthcare financings that came in the past couple of weeks generally did well. Maturities seemed to do better than put bonds, and it remains important to pay attention to couponing and how best to navigate a challenging yield curve. But these are episodic indicators rather than trends, given that the scale of issuance remains muted. Other capital markets—like real estate—are becoming more active and offer competitive funding and different credit considerations relative to debt market options. Credit management continues to be the main driver of low external capital formation, but those looking for outside funding should spend time up front considering the full array of channels and structures.

This Part of the Crisis

And now it’s official. After JPMorgan acquired First Republic Bank—with a whole lot of help from the Federal Deposit Insurance Corporation—CEO Jamie Dimon declared, “this part of the crisis is over.” Not sure regional bank shareholders would agree, but from Mr. Dimon’s perspective the biggest bank got bigger, which made it a good day.

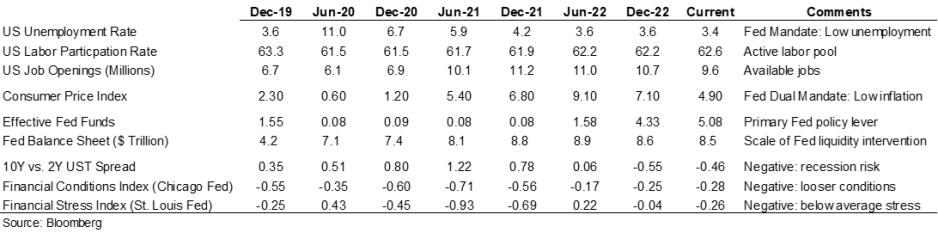

Last week the Federal Reserve raised rates another 25 basis points and the expectation (hope) seems to be that the Fed has reached the peak of its tightening cycle or will at least pause to see if constrictive forces like higher rates and regional bank balance sheet deflation slow activity enough to bring inflation back to the 2.0% Fed target. Assuming this is a pause point, it makes sense to check in on a few economic and market indicators.

Inflation is improving, although it remains well above the Fed’s 2.0% target range, and there are other indicators (like labor participation and unemployment) that have recovered some of the ground lost in 2020. But the weird part remains that this all seems quite civilized. To some, the Treasury curve spread continues to suggest a recession is looming, but in my neighborhood workers are still in short supply, restaurants are busy, and contractors are booked well into the future. Today’s ~3.36% 10-year Treasury rate is less than 100 basis points higher than the average since the start of the Fed interventionist era in 2008 and a whopping 257 basis points lower than the average since 1965. Think about how much capital has been raised in market environments much worse than now (including most of the modern-day healthcare inpatient infrastructure). Again, the main culprit in retarded capital formation is institutional credit management concerns rather than the funding environment.

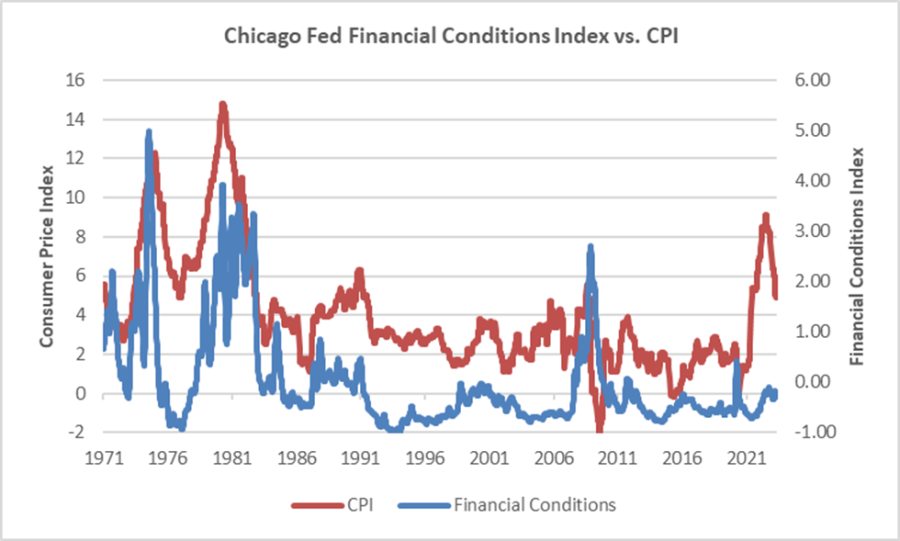

The major fallout from the Fed’s recent anti-inflation efforts seems concentrated with financial intermediaries rather than consumers (or workers), and the financial intermediary stress the Fed is relying on to help curb economic activity is grounded in their own balance sheet management decisions rather than deteriorating loan portfolios. We’ve looked at this before, but it bears repeating that in the “great inflation” of the 1970s, the Chicago Fed’s Financial Conditions Index reached its highest recorded points (higher means tighter than average conditions) and in this most recent inflationary cycle, that same index has remained consistently accommodative. Can you wring inflation out of a system while retaining relatively accommodative financial conditions? Which begs the question of whether any Fed pause is more about shifting priorities: downgrading the inflation fight in favor of moderating the financial intermediary threat? We might be living a remake of the 1970s version of stubborn inflation, which means that all the attendant issues—rolling volatility across operations, financing, and investing—might be sticking around as well.

Meanwhile, somewhere out in the Atlantic the debt ceiling storm is forming. Who knows whether it will make landfall as a storm or a hurricane, but it does remind us that the operative portion of the Jamie Dimon quote noted above is this part of the crisis is over. The next part of the long saga that is about us climbing out of a deep fiscal and monetary hole will roll in and new variations of the same central challenge will emerge for healthcare leaders.

A Healthcare Makeover

Ken Kaufman has been advancing the idea that healthcare needs a “makeover” to align with post-COVID realities. Look for a piece from him on this soon, but the thesis is that reverting to a 2019 world isn’t going to happen, which means that restructuring is the only option. The most recent National Hospital Flash Report suggests improving margins, but they remain well below historical norms and the labor part of the expense equation is structurally higher. Where we are is not sustainable and waiting for a reversion is a rapidly decaying option.

My contribution to Ken’s argument is to reemphasize that balance sheet is the essential (only) bridge between here and a restructured sector and the journey is going to require very careful planning about how to size, position, and deploy liquidity, leverage, and investments. Of course, the central focus will be on how to reposition operations. But if organic cash generation remains anemic, the gap will be filled by either weakening the balance sheet (drawing down reserves, adding leverage, or adopting more aggressive asset allocation) or by partnering with organizations that have the necessary resources.

Organizations reach the point of greatest enterprise risk when the scale of operating challenges outstrips the scale of balance sheet resources. Missteps are manageable when the imbalance is the product of rapid growth but not when it is the result of deflating resources. If the core imperative is to remake operations, the co-equal imperative is continuously repositioning the balance sheet to carry you from here to whatever defines success.