The nonprofit health system narrowed its operating loss while continuing to grapple with financial and policy pressures as it progresses towards profitability.

KEY TAKEAWAYS

Providence cut its operating loss in the second quarter to $21 million, improving from a $123 million loss a year ago.

Revenue rose 3% year-over-year to $7.91 billion, driven by higher patient volumes and better commercial rates.

The health system faces ongoing “polycrisis” challenges, including rising supply costs, staffing mandates, insurer denials, and looming Medicaid cuts, which have already prompted layoffs, hiring pauses, and leadership restructuring.

Providence made promising strides toward financial sustainability in the second quarter as higher patient volumes helped trim an operating loss that has weighed heavily on its balance sheet.

Yet the Renton, Washington-based health system warned that a compounding set of external pressures, which it labeled a “polycrisis,” still poses formidable challenges to its mission and future.

For the three months ended June 30, the nonprofit reported an operating loss of $21 million, equating to an operating margin of –0.3%, representing a marked improvement from the $123 million loss (–1.6%) posted over the same period in 2024. Compared with the previous quarter, the gain was even starker as Providence trimmed its deficit by $223 million. Through the first six months of the year, the health system had an operating loss of $265 million (-1.7%).

Revenue growth was fueled by higher patient volumes and improved commercial rates, Providence highlighted. Operating revenue rose 3% year-over-year to $7.91 billion as inpatient admissions (up 3%), outpatient visits (up 3%), case mix–adjusted admissions (up 3%), physician visits (up 8%), and outpatient surgeries (up 5%) all contributed.

On the expense side, Providence managed a 2% rise in operating costs to $7.93 billion, thanks largely to productivity gains, including a 43% reduction in agency contract labor. However, supply costs swelled by 9% and pharmacy expenses jumped by 12% year-over-year.

Providence, along with the healthcare industry at large, faces what CEO Erik Wexler called a “polycrisis” due to a mix of inflation, tariff-driven supply pressures, new state laws on staffing and charity care, insurer reimbursement delays and denials, and looming federal Medicaid cuts, especially from the One Big Beautiful Bill Act, which the health system said “threatens to intensify health care pressures.”

Those factors are significantly influencing hospitals’ and health systems’ decision-making. Providence has made staffing adjustments that include cutting 128 jobs in Oregon earlier this month, a restructuring in June that eliminated 600 full-time equivalent positions, apause on nonclinical hiring in April, and leadership reorganization since Wexler took over as CEO in January.

Accounts receivable is another area that has been indicative of headwinds, with Providence noting that while it improved in the second quarter, it “remains elevated compared to historical trends.”

Even with the roadblocks in its path, Providence is working towards profitability after being in the red for several years running.

“I’m incredibly proud of the progress we’ve made and grateful to our caregivers and teams across Providence St. Joseph Health for their continued dedication,” Wexler said in the news release. “The strain remains, especially with emerging challenges like H.R.1, but we will continue to respond to the times and answer the call while transforming for the future.”

For the past six years, Kaufman Hall has been publishing its monthly National Hospital Flash Report, which is designed to provide a pulse on the health of the healthcare industry and to highlight meaningful and pertinent trends for hospital and health system leaders. The data that powers the report is taken from over 1,300 hospitals, which are reflective of all geographic locations, hospital sizes and types. To ensure the content is digestible and understandable, Kaufman Hall aggregates the data into larger cohorts and measures a select set of key metrics that are most important for understanding the health of the industry. Industry groups and system leaders use these reports both for peer review purposes but also to paint an overall story for their boards and communities.

Through a detailed review of the Flash Report data, each month Kaufman Hall develops findings that healthcare leaders may find instructive as they determine how to adjust to changing market conditions. In 2024 it was reasonably obvious that there was a widening divide between the highest performing hospitals and the lowest performers.While a significant cadre of hospitals and health systems have recovered to pre-Covid financial success, 37% of American hospitals continue to lose money.

We are often asked what the successful hospitals are doing—and importantly—what the data tell us about those that are less successful. Using 2024 data, we have drawn two important conclusions around the role of leading management teams and what separates their organizations from others.

These teams have:

A sophisticated and balanced approach to the management of departmental performance: and

An understanding of the management of shared service costs.

A sophisticated and balanced approach to the management of departmental performance

It turns out that current data demonstrate that the management of departmental performance is critical to overall hospital financial performance but in a more nuanced manner than expected.

Our analysis was conducted as follows:

First, we looked at data across hospitals nationwide to understand the difference in departmental performance between top and bottom performing hospitals.

Second, we ranked each department in a hospital from 0 to 100, with 100 representing the best performance based on expense per unit of service.

Third, we then grouped all hospitals based on their bottom-line operating margin into three cohorts: those hospitals that fell into the bottom quartile of financial performance, those between the bottom and top quartile, and those in the top quartile.

Finally, we created a histogram of the average composition of departmental performance across each of the three margin cohorts.

The findings demonstrate that organizations with top financial performance have departmental results that look like a normal curve around the median. Said more simply, in top-performing hospitals the number of lower-performing departments is roughly equal to the number of higher-performing departments, with most departments operating near the national departmental medians. In contrast, hospitals with the lowest financial performance show a much greater number of departments operating with high cost per units of service and a few departments that operate extremely efficiently.

It appears that poorer performing hospitals focus on the management of the largest clinical and nursing areas. These are the departments that tend to be the “easiest” to manage because they are the “easiest” to benchmark. But the data show that these same hospitals tend to have poor performance over the remainder of the departments, which leads to poor financial results for the total hospital.

Hospitals with top quartile financial performance tend to manage all departments as close to the benchmark median as possible. Such a result means spending more managerial time on the harder to manage departments, especially those departments that are more “unique” and where overall performance is harder to characterize and benchmark.

The observations that can be drawn here are important and as follows:

First, oversight and management of individual departments is critical to the financial success of the entire hospital or system.

Second, the overall organizational structure of departmental administration is critical as well. The more complicated your departmental structure and the more individual departments you maintain and administer, the more difficult it will be to manage a majority of departments to “median” results.

The data suggest a perhaps unexpected operational conclusion. The achievement of median national departmental benchmarks is leading to overall positive hospital financial operating margins. This outcome offers significant budgeting advice and over the course of a fiscal year should prove to be a remarkably useful administrative lesson.

Understanding the management of shared service costs

Given the growing costs of shared services and related overhead, Kaufman Hall wanted a closer look at how well hospital organizations were scaling shared service costs related to the organization’s size. Unexpectedly, shared service costs were not highly correlated to the size of the hospital or hospital system. This suggests that the management of shared service costs on a per unit basis is difficult and that this aspect of expense management requires diligent focus to enact and sustain cost change. Our data often indicates a wide variation of cost performance among shared services of similar types within different large organizations. This suggests that standardization of such services is not well developed and that there may be a certain level of wishful thinking that increases in organizational size will automatically correlate to lower per unit costs.

The data did indicate, however, that larger organizations can achieve higher performance over smaller organizations relative to shared service expenses. This is an indication that size can be leveraged for superior performance but that such results are not automatic. The takeaway here is that the total spend for shared service functions is very substantial and growing. In that regard, it is most important to proactively address expenses in these areas, build appropriate management plans, and understand how to focus on the right buttons and levers. To the extent that organizations are assuming that growth (both organic and inorganic) will create economies of scale with the overall shared service apparatus, the data demonstrate that such an outcome is possible but only with strong planning and execution.

Operating hospitals in 2025 is flat-out hard and likely to get harder over the year. Hospital executives right now should use every managerial advantage available. A close look at the National Hospital Flash Report data identifies important relationships that provide for a more nuanced and sophisticated operation of both individual departments and the bundle of shared services. The data clearly demonstrate that better results in both these areas will lead to improved financial performance within the hospital overall. The data also indicate key managerial strategies that will lead to such improvement.

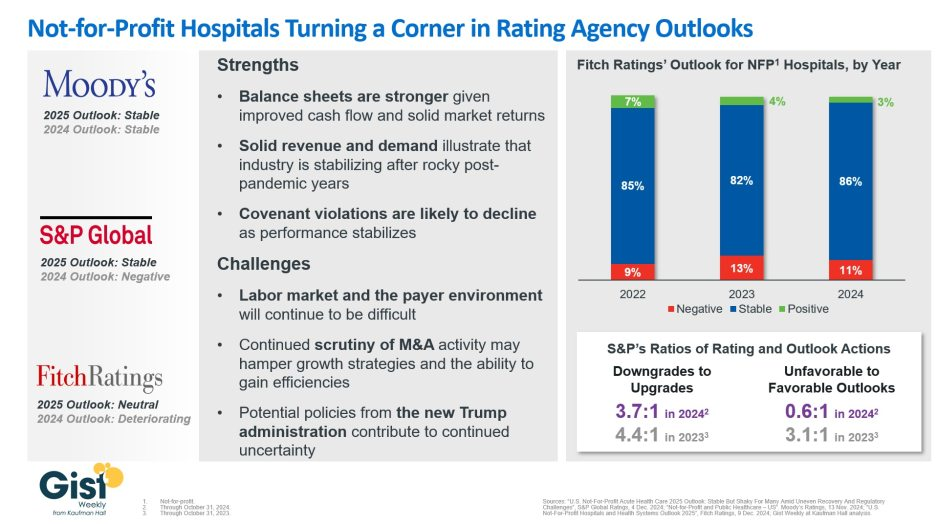

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

Some of America’s largest hospital systems saw their financials soar in the first half of 2024. And yet, more than 700 facilities across the country still are at risk of closing.

Why it matters:

It’s a familiar tale of the rich getting richer, as big, mostly for-profit health systems see improved margins while smaller facilities in outlying areas are barely hanging on.

That could worsen access for some of the most vulnerable Americans — and hasten consolidation in an industry that’s been a magnet for M&A.

The big picture:

Health systems with big footprints, including large academic medical centers, have weathered the pandemic and economic headwinds and are seeing margins as good or better than before COVID-19.

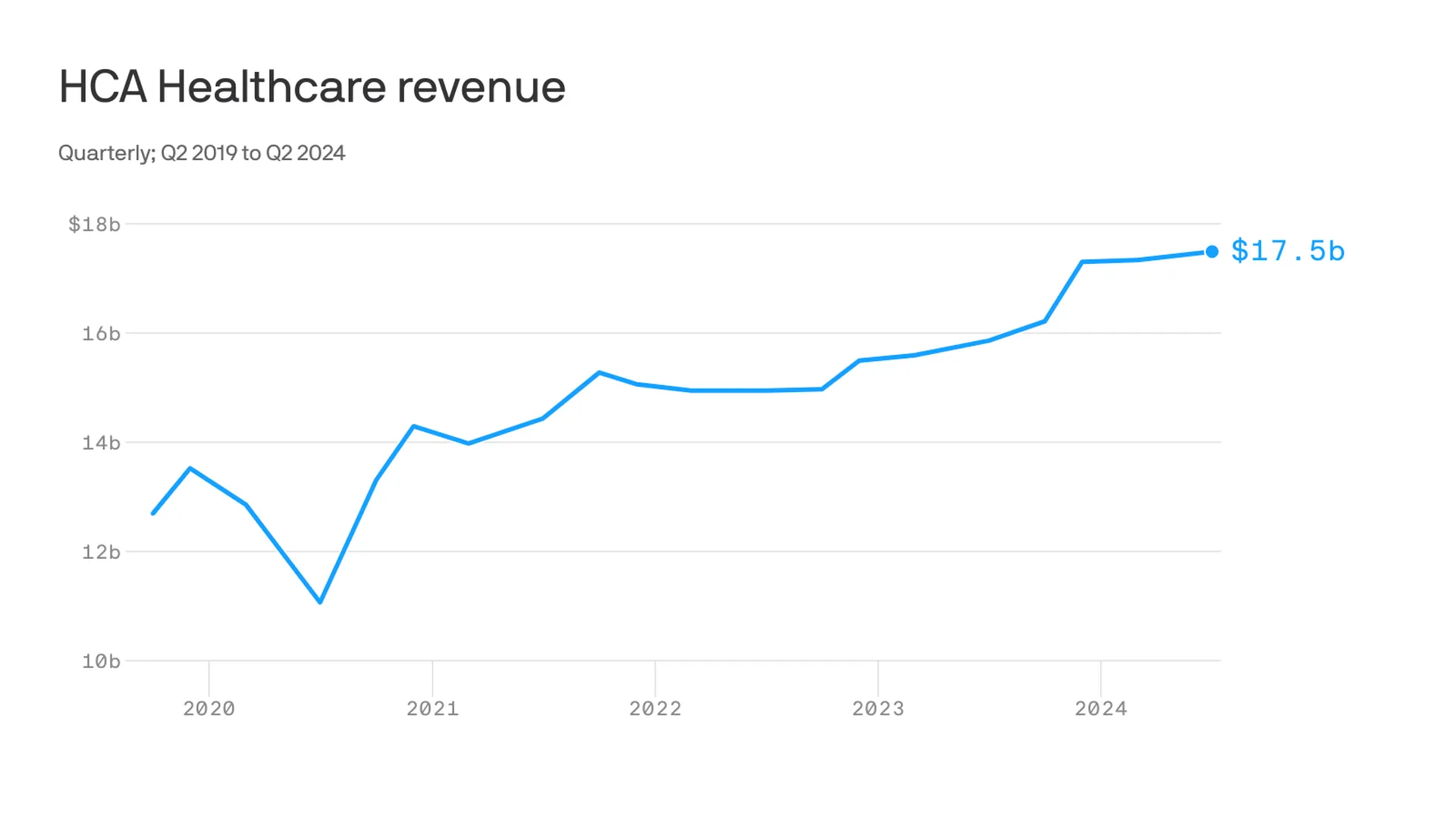

Nashville-based industry behemoth HCA Healthcare posted 23% year-over-year profit growth for the quarter, revising its forecast for the rest of the year, projecting it’ll reach as much as $6 billion. It posted a 10% year-over-year increase in revenue.

King of Prussia, Pennsylvania-based Universal Health Services similarly reported a strong quarter, posting nearly 69% growth on its bottom line over the same period last year while Dallas-based Tenet Healthcare reported a 111% jump in its net income over the same quarter last year.

Yes, but:

Smaller nonprofit hospitals, especially in rural areas, that made it through the crisis with the help of government aid are paring services like maternity wards and struggling to stay open.

“There are a lot of hospitals that survived, but their balance sheets are so weakened, their margin for error is basically zero at this point,” said Mike Eaton, senior vice president of strategy at population health company Navvis.

Hospitals that once could manage their expenses and the needs of communities are “going to really struggle to invest in what comes next,” he said.

Between the lines:

The biggest health systems have benefited from less volatility, seeing stabilizing drug prices and more predictable supply chains and labor costs, per a new report from Strata Decision Technology.

“It’s at least something you can manage to,” Steve Wasson, Strata’s chief data and intelligence officer, told Axios.

Revenues already were up thanks to renegotiated contracts health systems struck with payers last year, Wasson said.

There also have been changes on the federal side that boosted Medicare admissions and put some hospitals in line to be reimbursed for billions in underpayments from the 340B drug discount program.

Zoom in:

It’s all translated to operating margins that are up 17% year-to-date compared with the same time period in 2023, according to the latest Kaufman Hall National Hospital Flash Report.

Volumes as measured by hospital discharges per day are up 4% year-to-date.

Expenses per day are also up 6% year to date, including labor (4%), supplies (8%) and drugs (8%), but are far less volatile and thus easier to plan for, said Erik Swanson, senior vice president at Kaufman Hall.

But there’s a growing gulf between the top third of U.S. hospitals, which are seeing outsize growth, and the rest, Swanson said.

Threat level: A new report from the Center for Healthcare Quality and Payment Reform estimated 703 hospitals — or more than one-third of rural hospitals — are at risk of closure, based on Centers for Medicare and Medicaid Services financial information from July. Losses on privately insured patients are the biggest culprit.

“We’re looking at 50% of rural operating in the red. The situation is very challenging,” Michael Topchik, partner at Chartis Center for Rural Health, told Axios.

These smaller hospitals may still be there, but there will continue to be a steady erosion of the kinds of services they offer, such as obstetrics, cancer care and general surgery, he said.

What’s next:

Private equity investment in rural health care is already booming and with it, prospects for service and staffing cuts.

The South generally has the highest concentration of private equity-owned rural hospitals, often with lower patient satisfaction and fewer full-time staff compared with non-acquired hospitals, according to the Private Equity Stakeholder Project.

Congress is ramping up oversight of private equity investments in the sector, though most lawmakers are loath to take steps to actually halt deals.

Congress returns from its July 4 break today and its focus will be on the President: will he resign or tough it out through the election in 120 days. But not everyone is paying attention to this DC drama.

In fact, most are disgusted with the performance of the political system and looking for something better. Per Gallup, trust and confidence in the U.S. Congress is at an all-time low.

The same is true of the healthcare system:

69% think it’s fundamentally flawed and in need of systemic change vs. 7% who think otherwise (Keckley Poll). And 60% think it puts its profits above all else, laying the blame at all its major players—hospitals, insurers, physician, drug companies and their army of advisors and suppliers.

These feelings are strongly shared by its workforce, especially the caregivers and support personnel who service patient in hospital, clinic and long-term care facilities. Their ranks are growing, but their morale is sinking.

Career satisfaction among clinical professionals (nurses, physicians, dentists, counselors) is at all time low and burnout is at an all-time high.

Last Friday, the Bureau of Labor issued its June 2024 Jobs report. To no one’s surprise, job growth was steady (+206,000 for the month) –slightly ahead of its 3-month average (177,000) despite a stubborn inflation rate that’s hovered around 3.3% for 15 months. Healthcare providers accounted for 49,000 of those jobs–the biggest non-government industry employer.

But buried in the detail is a troubling finding: for hospital employment (NAICS 6221.3): productivity was up 5.9%, unit labor costs for the month were down 1.1% and hourly wages grew 4.8%–higher than other healthcare sectors.

For the 4.7 million rank and file directly employed in U.S. hospitals, these productivity gains are interpreted as harder work for less pay. Their wages have not kept pace with their performance improvements while executive pay seems unbridled.

Next weekend, the American Hospital Association will host its annual Leadership Summit in San Diego: 8 themes are its focus:

Building a More Flexible and Sustainable Workforce is among them. That’s appropriate and it’s urgent.

An optimistic view is that emergent technologies and AI will de-lever hospitals from their unmanageable labor cost spiral. Chief Human Resource Officers doubt it. Energizing and incentivizing technology-enabled self-care, expanding scope of practice opportunities for mid-level professionals and moving services out of hospitals are acknowledged keys, but guilds that protect licensing and professional training push back.

By contrast, the application of artificial intelligence to routine administrative tasks is more promising: reducing indirect costs (overhead) that accounts for a third of total spending is the biggest near-term opportunity and a welcome focus to payers and consumers.

Thus, most organizations advance workforce changes cautiously. That’s the first problem.

The second problem is this:

lack of a national healthcare workforce modernization strategy to secure, prepare and equip the health system to effectively perform. Section V of the Affordable Care Act (March 2010) authorized a national workforce commission to modernize the caregiver workforce. Due to funding, it was never implemented. It’s needed today more than ever. The roles of incentives, technologies, AI, data and clinical performance measurement were not considered in the workforce’ ACA charter: Today, they’re vital.

Transformational changes in how the healthcare workforce is composed, evaluated and funded needs fresh thinking and boldness. It must include input from new players and disavow sacred cows. It includes each organization’s stewardship and a national spotlight on modernization.

It’s easier to talk about healthcare’s workforce issues but It’s harder to fix them. That’s why incrementalism is the rule and transformational change just noise.

PS: In doing research for this report, I found wide variance in definitions and counts for the workforce. It may be as high as 24 million, and that does not include millions of unpaid caregivers. All the more reason to urgently address its modernization.

A number of hospitals and health systems are reducing their workforces or jobs due to financial and operational challenges.

Below are workforce reduction efforts or job eliminations announced this year.

June

West Monroe, La.-based Glenwood Regional Medical Center, part of Dallas-based Steward Health Care, laid off 23 employees. Affected roles included leadership, a spokesperson for the hospital said in a statement shared with Becker’s.

Cleveland-based University Hospitals is reducing its leadership structure by more than 10% as part of more than 300 layoffs. COO Paul Hinchey, MD, told Becker’s C-suite level leaders and vice presidents were included in the cuts.

Portland-based Oregon Health & Science Universitytold staff June 6 that it plans to lay off at least 500 employees, citing financial issues. The news follows the institution and Portland-based Legacy Health signing a binding, definitive agreement to come together as one health system under OHSU Health.

May

The All of Us Research Program, a collaboration of the University of Arizona in Tucson and Phoenix-based Banner Health, plans to lay off 45 workers due to reduced federal research funding, according to an Arizona WARN notice filed May 28. The program, launched in 2018, is part of HHS’ National Institutes of Health.

Burlington, Mass.-based Tufts Medicine will lay off 174 employees due to industry challenges, the health system confirmed in a May 21 statement shared with Becker’s. The layoffs, which have varying effective dates, will primarily affect administrative and non-direct patient care roles. Some leadership roles were affected, a spokesperson told Becker’s.

Doral, Fla.-based Sanitas Medical Centerlaid off 56 employees between May 17 and May 20. Some of the affected roles included nine care coordinators, one care educator, and two case managers, according to a May 20 WARN notice accessed by Becker’s.

Select Specialty Hospital in Longview, Texas, will close on or about June 30, affecting 94 employees, Becker’s has confirmed. The hospital, operated by Mechanicsburg, Pa.-based Select Medical, is a 32-bed, critical illness recovery facility.

White Rock Medical Center in Dallaslaid off nearly 35% of its staff. The hospital temporarily stopped taking patients transported by emergency medical services due to the layoffs, The Dallas Morning News reported. It has since resumed accepting those patients.

Oakland-based Kaiser Foundation Hospitals is laying off 76 workers in California. The layoffs primarily affect employees in IT and marketing, according to regulatory documents filed with the state May 1.

April

Pittsburgh-based UPMC will lay off approximately 1,000 employees. The layoffs, which represent more than 1% of the health system’s 100,000 workforce will primarily affect nonclinical, administrative and non-member-facing employees.

Union Springs, Ala.-based Bullock County Hospitallaid off 95 employees beginning April 9, according to regulatory documents filed with the state. The layoffs occurred as Bullock seeks to become a rural emergency hospital and is ending psychiatric services as part of the shift, AL.com reported April 25.

Jackson Health Systemreduced compensation programs for senior leaders; laid off fewer than 25 people, including one hospital CEO; and froze many vacant positions, especially in support and nonclinical areas, a spokesperson for the Miami-based organization confirmed to Becker’s. President and CEO Carlos Migoya shared these efforts in a message to staff, citing financial challenges.

Coos Bay, Ore.-based Bay Area Hospital plans to conduct layoffs as it outsources its revenue cycle management operations, a spokesperson for the hospital confirmed to Becker’s. The transition will affect 27 positions.

Manchester, N.H.-based Catholic Medical Centerplans to cut 142 positions, including 54 layoffs. An April 18 letter to employees from CMC president and CEO Alex Walker, obtained by Becker’s, said cuts would occur through the 54 staff eliminations, open position cuts, reduced hours, planned departures, and resource redeployment in satellite locations for CMC.

Marshfield (Wis.) Clinic Health System will lay off furloughed staff, effective in early May. The health system furloughed about 3% of its workforce in January, affecting positions mostly in non-patient-seeing departments, including leadership roles.

Norwalk, Ohio-based Fisher-Titus Medical Centerlaid off some workers in nonclinical roles and reduced hours for others. Seven employees, about 0.5% of the health system’s workforce, were laid off April 1. Work hours were reduced for another 10 positions, a hospital spokesperson told Becker’s.

March

Robbinsdale, Minn.-based North Memorial Health is laying off 103 employees in clinical and nonclinical roles, citing financial challenges. The layoffs affect several services across the two-hospital system.

AHMC’s San Gabriel (Calif.) Valley Medical Center is laying off 62 workers, according to regulatory documents filed with the state March 13. The layoffs take effect May 13.

Miami-based North Shore Medical Center, part of Steward Health Care, started conducting layoffs as part of cuts to some of its programs amid the Dallas-based health system’s continued financial struggles. Around 152 workers represented by 1199SEIU were laid off, a union spokesperson confirmed. However that number could be higher as their members do not represent every employee at NSMC, the spokesperson said.

Oakland, Calif.-based Kaiser Foundation Hospitals is laying off more than 70 employees. The layoffs primarily affect those in IT roles.

February

Lion Star, the group that operates Nacogdoches (Texas) Memorial Hospital, is closing four of its clinics on March 22, which will result in fewer than 50 layoffs, a Lion Star spokesperson confirmed to Becker’s. No additional layoffs are planned.

Little Rock-based Arkansas Heart Hospital has laid off fewer than 50 employees since the beginning of 2024, citing low reimbursement rates. The layoffs affected lower-paying positions, Bruce Murphy, MD, CEO of the hospital, said, according to Arkansas Business.

Cincinnati-based Mercy Health will lay off some call center positions. The system attributed the move to its partnership with a third party to operate its enterprise contact center for primary care scheduling.

Ridgecrest (Calif.) Regional Hospital announced more layoffs to avoid closure. It is laying off 31 more employees, including seven licensed vocational nurses and four registered nurses, two months after it announced plans to lay off nearly 30 others and suspend its labor and delivery unit, Bakersfield.com reported Feb. 15.

Medford, Ore.-based Asante health system laid off about 3% of its workforce. The layoffs primarily affected administrative and support roles and were necessary to offset “financial headwinds” over the past several years, according to a report from NBC affiliate KOBI-TV, which is based on an internal memo sent to staff Feb. 9.

Oakdale, Calif.-based Oak Valley Hospital District is scaling back services and laying off workers to improve its finances. The hospital said in a Feb. 2 statement shared with Becker’s that it will close its five-bed intensive care unit, discontinue its family support network department and lay off 28 employees, including those in senior management and supervisor positions.

Chicago-based Rush University System for Healthlaid off an undisclosed number of workers in administrative and leadership positions, citing “financial headwinds affecting healthcare providers nationwide.” No additional information was provided about the layoffs, including the number of affected employees.

University of Chicago Medical Center laid off about 180 employees, or less than 2% of its roughly 13,000-person workforce. The majority of affected positions are not direct patient facing, the organization said in a statement shared with Becker’s.

Fountain Valley, Calif.-based MemorialCarelaid off 72 workers due to restructuring efforts at its Long Beach (Calif.) Medical Center and Long Beach, Calif.-based Miller Children’s and Women’s Hospital. The layoffs include 13 positions at Long Beach Medical Center’s outpatient retail pharmacy, which is closing Feb. 2, a spokesperson for MemorialCare said in a statement shared with Becker’s.

January

George Washington University Hospital in Washington, D.C., part of King of Prussia, Pa.-based Universal Health Services, is laying off “less than 3%” of its employees. The move is attributed to restructuring efforts.

Amarillo-based Northwest Texas Healthcare System, also part of Universal Health Services, announced plans to lay off a “limited number of positions.” The move is attributed to restructuring efforts.

Lehigh Valley Health Network is cutting its chiropractic services and laying off 10 chiropractors. The layoffs are effective April 12 and due to restructuring. The Allentown, Pa.-based health system has 10 chiropractic locations, according to its website.

Central Maine Healthcare is laying off 45 employees as part of management reorganization. The Lewiston-based system, which also ended urgent care services at its Maine Urgent Care on Sabattus Street in Lewiston on Jan. 12, has 3,100 employees total.

University of Vermont Health Network, based in Burlington, is cutting 130 open positions. The move is part of the health system’s efforts to reduce expenses by $20 million.

Med-Trans, a medical transport provider based in Lewisville, Texas,closed its UF Health ShandsCair base serving Gainesville, Fla.-based UF Health Shands Hospital on Jan. 10 due to decreased transportation demands. The move also resulted in layoffs, a spokesperson for UF Health, the hospital’s parent company, told Becker’s in a statement.

RWJBarnabas Health, based in West Orange, N.J., is laying off 79 employees, according to documents filed with the state on Jan. 8. The layoffs are effective March 31 and April 5. A spokesperson for the health system told Becker’s that 74 of the positions were “time-limited information technology training job functions.” The other layoffs were due to closure of an urgent care center.

Citing financial challenges, Cleveland-based University Hospitals is reducing its leadership structure by more than 10% as part of more than 300 layoffs.

Rising costs of supplies, labor and purchase services, and reduced Medicare reimbursement rates, have affected UH and various other systems, according to COO Paul Hinchey, MD.

“All of that’s creating significant downward pressure on our revenue,” Dr. Hinchey told Becker’s.

The news from UH follows a national trend of hospitals facing significant headwinds. Kaufman Hall found in early June that 40% of hospitals in the U.S. are still losing money.

At UH, revenue has increased nearly 9% year over year due to various changes, such as increased access for patients and implementing a new EHR system, according to UH.

“[However], in spite of our efforts and being successful in growth, that downward pressure on revenue and the increasing prices is pinching our margin,” said Dr. Hinchey.

Dr. Hinchey said the health system has been optimizing operations since the end of the pandemic.

“We took a look at our cost structure and recognized we needed to get our cost structure down,” he said. “We’ve done a couple initiatives that we put under the auspices of a Medicare break-even initiative to try to drive down our cost structure.”

Some actions already taken have included increasing efficiency, consolidating service lines and closing hospitals in Bedford and Richmond Heights, according to UH.

Most recently, the health system identified an opportunity to make cuts to leadership. Dr. Hinchey said C-suite level leaders and vice presidents were included in the cuts.

“These decisions are never easy,” Cliff Megerian, MD, CEO and Jane and Henry Meyer Chief Executive Officer Distinguished Chair, said in a news release. “The important thing is that we make these strategic moves now so we can continue to serve our community and fulfill our mission for decades to come. We are thankful for our hometown team that delivers lifesaving care to our neighbors, friends and relatives each and every day.”

Dr. Hinchey said UH began notifying employees of the layoffs on June 17. Affected workers will receive a severance package aligned with their roles and tenure.

Portland-based Oregon Health & Science University told staff June 6 that it plans to lay off at least 500 employees, citing financial issues.

“Our expenses, including supplies and labor costs, continue to outpace increases in revenue,” top leaders told staff in a message shared with Becker’s. “Despite our efforts to increase our revenue, our financial position requires difficult choices about internal structures, workforce and programs to ensure that we achieve our state-mandated missions and thrive over the long term.”

Willamette Week was first to report the news, which follows Oregon Health & Science University and Portland-based Legacy Health signing a binding, definitive agreement to come together as one health system under OHSU Health. OHSU Health would comprise 12 hospitals and, more than 32,000 employees and will be one of the largest providers of services to Medicaid members in Oregon.

An Oregon Health & Science University spokesperson told Becker’s more information about the layoffs will be provided in the coming weeks.

In the June 6 message, leaders told staff that “while we work to address short-term financial challenges, we must also plan for an impactful and successful future. We understand that last week’s announcement regarding the Legacy Health definitive agreement, while exciting and potentially transformational, raises questions about how we can afford the required investment in light of our financial situation.”

They added that a capital investment in Legacy “represents a strategic expansion designed to enhance our capacity,” and will be funded by borrowing with 30-year bonds.

“These capital dollars cannot be used to close gaps in our fiscal year 2025 OHSU budget or to pay our members. The OHSU Strategic Alignment and budgetary work would be necessary with or without the Legacy Health integration,” leaders said.

OHSU has planned a town hall next week to further discuss the combination with Legacy.

Leaders said discussions between managers and members about workforce reductions will begin after the annual review and contract renewal process, with additional reductions occurring over the next few months.

Hundreds of nurses at University Hospitals are facing a decrease in pay as the Cleveland-based health system pivots from its COVID-19 pandemic model, cleveland.com reported.

A spokesperson told Becker’s the pay adjustment is effective June 16 and applies to 350 Enterprise Staffing Services nurses.

“UH’s Enterprise Staffing Services is an in-house staffing agency formed in response to the once-in-a-lifetime global health pandemic that stretched our resources and workforce to the extreme,” a UH statement shared with Becker’s said. “During the pandemic, hospitals across the country (including UH) increased their use of agency nurses to fill gaps in staffing with government funding assistance, with agency costing up to twice as much or more than our hospital-based full-time nurses.

“Nurses are the heartbeat of our health system and we will never be able to thank them enough for their commitment and dedication to our patients during the pandemic. Unfortunately, the pandemic care model is not sustainable in today’s environment.”

The statement said those affected by the pay adjustment, representing 1% of the health system’s workforce, will still be paid about twice the national average.

Pay for staffing services nurses on night shift will decrease from $75 to $65 an hour, a 13% cut, UH said, according to cleveland.com, which obtained a health system memo related to the change. Pay for staffing services nurses on day shift will decrease 8%, from $60 to $55 an hour.

Pay for a new staffing services job without benefits will be $75 per hour for night shift, and $65 per hour for day shift, UH said in the memo, which also encouraged staffing services nurses to apply for other health system roles, according to cleveland.com.

“As we continue to exit from our pandemic model, external nursing staffing agencies and internal hospital nurse staffing agencies nationwide are adjusting pay accordingly,”

UH’s statement said. “We have provided cutting-edge, compassionate care to our neighbors in Northeast Ohio since 1866. We’re taking the appropriate steps to ensure we can continue fulfilling our mission for future generations.”