Since filing for bankruptcy Monday, Steward Health Care revealed it’s carrying more than $1 billion in debt and said its entire hospital portfolio is for sale.

Eleven minutes later, Steward employees had an email waiting from their CEO, Ralph de la Torre. The CEO told his staff that industrywide economic headwinds and delays in Steward’s planned asset sales had forced the physician-owned health network to initiate restructuring proceedings.

“It is incumbent on all of us to ensure that this process has no impact on the quality care our patients, their families, and our communities can continue to receive at our hospitals,” de la Torre wrote in an email viewed by Healthcare Dive. “To the vast majority of you, operations will either not be different or improve.”

“To be clear, this is a restructuring under chapter 11; it is not a closure and it is not a liquidation,” he wrote.

The email was the first time employees had heard directly from Steward leadership about the company’s financial distress — though rumorsanduncertainty about the operatorhad been festering for weeks, according to Marlishia Aho, regional communications director for the union 1199SEIU United Healthcare Workers East.

Leading up to Monday’s filing, state and federal lawmakers were increasingly worried about how a bankruptcy at the largest physician-led hospital operator in the country would impact access to care.

Regulators in Massachusetts — where Steward operates eight hospitals — held closed-door strategy sessions to map out contingency in case of a bankruptcy, and workers staged rallies to protest possible hospital closures.

Steward provides care for more than 2 million patients each year across 31 hospitals and 400 facility locations, according to bankruptcy filings. The company also employs nearly 30,000 employees across its eight-state portfolio, including 4,500 primary and specialty care physicians.

Steward’s first-day bankruptcy motions shed light on the operator’s future — and outlines its strategy for paying down its massive debt by selling assets. Here are the biggest takeaways.

Steward’s sprawling debt

Steward has earned a reputation for being cagey about its finances — to the dismayof Massachusetts Gov. Maura Healey, who accused the company of operating in a “black box” in a letter to its CEO earlier this year.

The operator has refused to file routine finances with Massachusetts regulators for years, citing a need to protect confidential business data. Even as the company shutteredhospitals this winter, regulators said Steward still dragged its feet on providing financial data, frustrating policymakers’ efforts to build out contingency plans.

“One of the good things about bankruptcy is that Steward and its CEO … will no longer be able to lie,” said Healey during a press conference Monday morning. “Transparency is really important here, and that’s why you know we’re looking forward to seeing what is in the various documents … We need clarity about debts and liabilities.”

In a slew of first-day motions, Steward now revealed it owes around $1.2 billion in total loan debts and about $6.6 billion in long-term lease payments.

Steward owes north of $600 million to 30 of its largest lenders, which include UnitedHealth-owned Change Healthcare, Philips North America LLC, Medline Industries, AYA Healthcare and Cerner.

The healthcare operator owes $289.8 million in unpaid compensation obligations, including $68 million to its own workers in unpaid employee salaries, $105.6 million in payments for physician services and $47.7 million owed to staffing agencies.

It also has approximately $979.4 million outstanding in trade obligations, of which approximately 70% are over 120 days past due.

Though Steward had a consortium of six private lenders financing its asset-based loans this year, now only one lender is listed in bankruptcy filings as funding its debtor-in-possession financing: its landlord, Medical Properties Trust.

The change in vendors is notable, according to Laura Coordes, professor of law at the Sandra Day O’Connor College of Law at Arizona State University.

“Something went on to get these other lenders to drop out,” she said.

The landlord may be opting to fund Steward during bankruptcy proceedings in hopes of getting its own money back more expediently, according to Coordes.

Steward is MPT’s largest tenant and the healthcare network will owe MPT at least $6.9 billion in debt and lease obligations by 2041, according to the filings.

During Tuesday morning’s first day hearing a representative for Steward told Judge Chris Lopez that all of Steward’s 31 hospitals are for sale. But to receive the $225 million from MPT, Steward has to hit aggressive sales milestones. It must host an auction for all non-Florida hospitals by June 28 and all Florida properties by July 30.

Since February, MPT executives have said there is strong interest from buyers in taking over Steward leases. However, Steward has yet to sell a hospital.

Experts have told Healthcare Dive they’re skeptical other operators would take on Steward’s leases at MPT’s current rental rates.

“Given the unaffordability of the leases and given that it hasn’t worked in the past, I do think that really material rent concessions are going to be needed to get this done,” said Rob Simone, sector head of real estate investment trusts at analyst firm Hedgeye.

Steward also signed a letter of intent to sell its physician group, Stewardship Health, to UnitedHealth. Although the deal was first announced in March, regulators have not yet begun reviewing the deal, according to David Seltz, executive director of the Massachusetts Health Policy Commission. Seltz said missing paperwork is delaying the review.

The Stewardship deal is not tied to further funding. A representative from UnitedHealth declined to comment on the pending deal and whether the bankruptcy proceeding would impact the sale.

Future of Steward

Employees have received conflicting messages about the future of Steward hospitals.

On one hand, both de la Torre and Massachusetts officials said Monday that Steward hospitals would remain open this week. However, Healey also emphasized that she wants Steward out of the state.

“Ultimately, [bankruptcy] is a step toward our goal of getting Steward out of Massachusetts,” Healey said during a press conference Monday.

Some Steward facilities may wind down during the bankruptcy proceedings, said Massachusetts Attorney General Andrea Campbell. Her office will oversee that process closely, and Steward will be required to provide licensing and notice obligations.

A healthcare worker at Steward’s Nashoba Valley Hospital told Healthcare Dive Monday she’s particularly concerned about the fate of her facility, which she says serves 14 communities but is small compared to some other hospitals in Steward’s portfolio. She doesn’t want regulators to forget about Nashoba.

“What I’m hoping for is that our state representatives and our local representatives really push to keep the hospital open,” she said. “But my concern is we get overlooked.”

State officials said they would continue monitoring Steward facilities to ensure quality care and push for the appointment of a patient care ombudsman to represent the interests of patients and employees during bankruptcy proceedings. Officials have already launched a website to offer resources about the bankruptcy process.

Still, employees are unsure of the path forward.

The Nashoba Valley Hospital employee told Healthcare Dive they’re conflicted about whether to stay at the hospital they’ve worked at for years or try to find a new position while they can.

“I’ve used the hospital since I moved out here. I’ve been living out in this area for like 25 years … I’ve brought my mother to this hospital,” the worker said. “It’s my hospital. It’s not just where I work. It’s what I use, and it’s vitally important to the community.”

Health systems are increasingly focused on their regional structures, reorganizing leadership to provide oversight most effectively. On Oct. 23, those changes hit the corner office.

Providence is phasing out the CEO role at two of its California hospitals, the Renton, Wash.-based system confirmed to Becker’s. One year ago, Providence’s Northern and Southern California regions came together to create a sole South Division. Now, a single chief executive — Garry Olney, DNP, RN — will oversee operations in the Northern California service area, replacing the CEOs of Napa-based Queen of the Valley Medical Center and Santa Rosa (Calif.) Memorial Hospital.

“This was part of a systemwide restructuring to streamline executive roles so we could preserve more resources for front-line caregivers and become nimbler and more responsive to the times,” the system said in a statement.

Providence isn’t alone in its desire to streamline leadership. Corewell Health East — part of Corewell Health, which has dual headquarters in Grand Rapids and Southfield, Mich. — made seven executive changes within the region, the system confirmed to Becker’s on Oct. 23. The senior vice president of medical group operations was let go, along with two hospital presidents. The region’s COO of acute and post-acute care, Nancy Susick, RN, will take over one hospital in addition to her current duties; the second hospital will be overseen in a dual capacity by Derk Pronger, who already helms another hospital in the region.

The word “streamline” was also used by Chicago-based CommonSpirit, which recently shared plans to lighten its regional load.

“We are also making further changes to streamline the organization, including the consolidation of our operating divisions into five regions from eight, clearly define our market-based focus and strategies and continue to refine our operating model,” CFO Dan Morissette said on an Oct. 12 investor call.

Regional revamps don’t always lead to cuts or “consolidation.” In some cases, they lead to the creation of new roles. Atlanta-based Emory Healthcare recently split its 10 hospitals into two divisions — one for regional hospitals, one for university hospitals — and tapped a president to helm each. Plus, Tampa (Fla.) General Hospital named eight new executives in a C-suite overhaul following the adoption of three Bravera Health hospitals into TGH North.

If the healthcare leaders plan to confront looming challenges, they need to be comfortable with “innovating and disrupting [themselves],” John Couris, president and CEO of Tampa General, told Becker’s.

“The way I would describe this is the last five years was all about foundational work,” Mr. Couris said. “The next five years and beyond is all about transformational work. So we’re shifting from the foundational activity to the transformational activity, and we need an organizational structure and a leadership team that reflects that journey. That’s why we made the changes.”

This is Part 2 of a series by Cain Brothers about the first-ever collaboration conference between health systems and private equity (PE) investment firms. Part 1 of this series addressed the conference’s who, what and where. This commentary will focus on the why. We will explore the underlying forces uniting health systems with private equity during this period of unprecedented industry disruption.

Why Health Systems and PE Need Each Other

On June 13 and 14, 2023, Cain Brothers hosted the first-ever collaboration conference between health systems and private equity (PE) investment firms. Timing, market dynamics and opportunity aligned. The conference was an over-the-moon success. Along with its sponsors, Cain Brothers will seek to expand the conference and align initiatives through the coming years.

Why Now? Healthcare is Stuck and Needs Solutions

As a society, the U.S. is spending ever-higher amounts of money while its population is getting sicker. A maldistribution of facilities and practitioners creates inequitable access to healthcare services in lower-income communities with the highest levels of chronic disease.

New competitors and business models along with unfavorable macro forces, including high inflation, aging demographics and deteriorating payer mixes, are fundamentally challenging health systems’ status quo business practices.

Governments, particularly the federal government, have become healthcare’s largest payers, funding over 40% of healthcare’s projected $4.7 trillion expenditure in 2023. Individual patients often get lost in the massive payment shuffle between payers and providers.

Meanwhile, governments’ pockets are emptying. As a percentage of GDP, U.S. government debt obligations have grown from 55% in 2001 to 124% currently. With rising interest rates and the commensurate increase in debt service costs, as well as an aging population, there is little to suggest that new funding sources will emerge to fund expansive healthcare expenditures. Scarcity reigns where resources for healthcare providers were once plentiful.

As a consequence, the healthcare industry is entering a period of more fundamental economic limitations. Delaying transformation and expecting society to fund ongoing excess expenditure is not a sustainable long-term strategy. Current economic realities are forcing a dramatic reallocation of resources within the healthcare industry.

The healthcare industry will need to do more with less. Pleading poverty will fall on deaf ears. There will be winners and losers. The nation’s acute care footprint will shrink. For these reasons, health systems are experiencing unprecedented levels of financial distress. Indeed, parts of the system appear on the verge of collapse, particularly in medically underserved rural and urban communities.

More of the same approaches will yield more of the same dismal results. Waking up to this existential challenge, enlightened health systems have become more open to new business models and collaborative partnerships.

Necessity Stimulates Innovation

Two disruptive and value-based business models are on the verge of achieving critical mass. They are risk-bearing “payvider” companies (e.g. Kaiser, Oak Street Health and others) and consumer-friendly, digital-savvy delivery platforms (e.g. OneMedical and innumerable point-solution companies).

Value-based care providers and their investors have the scars and bruises to show for challenging entrenched business practices reliant on fee-for-service (FFS) business models and administrative services only (ASO) contracting. Incumbents have protected their privileged market position well through market leverage and outsized political influence.

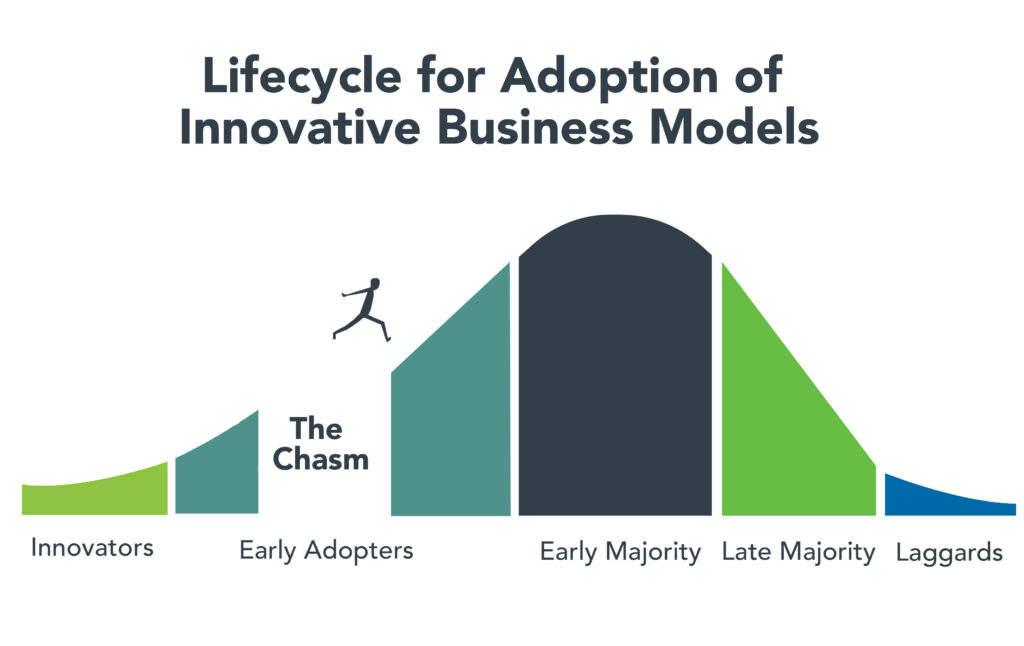

Despite market resistance, “payvider” and digital platform companies are emerging from the proverbial “innovators’ chasm.” More early adopters, including those health systems attending the Nashville conference, are embracing value-creating business models. The chart below illustrates the well-trodden path innovation takes to achieve market penetration.

Ironically, during this period of industry disruption, health systems understand they need to deliver greater value to customers to maintain market relevance. It will require great execution and overcoming legacy practices to develop business platforms that incorporate the following value-creating capabilities:

Decentralized care delivery (to make care more accessible and lower cost).

Root-cause treatment of chronic conditions.

Integrated physical and mental healthcare services.

Consistent, high-quality consumer experience.

Coordinated service delivery.

Standardized protocols that improve care quality and outcomes.

A truly patient/customer-centric operating orientation.

It’s not what to do, it’s how to get it done that creates the vexing conundrum. Solutions require collaboration. Platform business models replete with strategic partnerships are emerging. Paraphrasing an African proverb, it’s going to take a village to fix healthcare. That’s why the moment for health systems and PE firms to collaborate is now.

PE to the Rescue?

Private equity has become the dominant investment channel for business growth across industries and nations. According to a recent McKinsey report, PE has more than $11.7 trillion in assets under management globally. This is a massive number that has grown steadily. PE changes markets. It turbocharges productivity. It is a relentless force for value creation.

By investing in a wide spectrum of asset classes, private equity has become a vital source of investment returns for pensions, endowments, sovereign wealth funds and insurance companies. Healthcare, given its size and inefficiencies, is a target-rich environment for PE investment and returns. This explains the PE’s growing interest in working with health systems to develop mutually beneficial, value-creating healthcare enterprises.

Despite reports to the contrary, PE firms must invest for the long term. Unlike the stock market, where investors can buy and sell a stock within a matter of seconds, PE firms do not have that luxury. To generate a return, they must acquire and grow businesses over a period of years to create suitable exit strategies.

Money talks. By definition, all buyers of new companies value their purchase more than the capital required for the acquisition. In making purchase decisions, buyers evaluate businesses’ past performance. They also assess how the new business will perform under their stewardship. PE or PE-backed acquirers also consider which future buyers will be most likely acquire the company after a five-plus year development period.

PE’s investment approach can align well with health systems looking to create sustainable long-term businesses tied to their brands and market positioning. PE firms buy and build companies that attract customers, employees and capital over the long term, far beyond their typical five- to seven-year ownership period. Health systems that partner with PE firms to develop companies are the logical acquirers of those companies if they succeed in the marketplace. In this way, a rising valuation creates value for both health systems and their PE partners.

It is important to note that not all PE are created the same. Like health systems, PE firms differ in size, market orientation, investment theses, experience and partner expectations. Given this inherent diversity, it takes time, effort and a shared commitment to value creation for health systems and PE firms to determine whether to become strategic partners. Not all of these partnerships will succeed, but some will succeed spectacularly.

For health system-PE partnerships to work, the principals must align on strategic objectives, governance, performance targets and reporting guidelines. Trust, honest communication and clear expectations are the key ingredients that enable these partnerships to overcome short-term hurdles on the road to long-term success.

Conclusion: Time to Slay Healthcare’s Dragons

Market corrections are hard. As a nation, the U.S. has invested too heavily in hospital-centric, disease-centric, volume-centric healthcare delivery. The result is a fragmented, high-cost system that fails both consumers and caregivers. The marketplace is working to reallocate resources away from failing business practices and into value-creating enterprises that deliver better care outcomes at lower costs with much less friction.

Progressive health systems and PE firms share the goal of creating better healthcare for more Americans. Cain Brothers is committed to advancing collaboration between health systems and PE-backed companies. In addition to the Nashville conference, the firm has combined its historically separate corporate and non-profit coverage groups to foster idea exchange, expand sector understanding and deliver higher value to clients.

The ability to connect and collaborate effectively with private equity to advance business models will differentiate winning health systems. In a consolidating industry, this differentiation is a prerequisite for sustaining competitiveness. It’s adapt or die time. Health systems that proactively embrace transformation will control their future destiny. Those that fail to do so will lose market relevance.

The future of healthcare is not a zero-sum equation. Markets evolve by creating more complex win-win arrangements that create value for customers. No industry requires restructuring more than healthcare. As a nation and an industry, we have the capacity to fix America’s broken healthcare system. The real question is whether we have the collective will, creativity and resourcefulness to power the transformation. We believe the answer to that question is yes.

Paraphrasing Rev. Theodore Parker, the economic arc of the marketplace is long but it bends toward value. Together, health systems and PE firms can power value-creation and transformation more effectively than either sector can do independently. Each needs the other to succeed. Slaying healthcare’s dragons will not be easy but it is doable. It’s going to take a village to fix healthcare.

A number of hospitals and health systems are trimming their workforces or jobs due to financial and operational challenges.

Below are workforce reduction efforts or job eliminations that were announced within the past year and/or take effect later in 2023.

September

Indianapolis-based IU Health confirmed it is laying off 84 employees from its Blackford Hospital Hartford City, Ind. The staff will be laid off from the facility effective Nov. 3, and the system said it intends to offer alternative positions to those affected.

Chicago-based CommonSpirit Healthimplemented workforce reductions in the fourth quarter of the fiscal year ending June 30, resulting in about 2,000 job cuts. The health system announced the cuts, which affected about 2,000 full-time equivalents in ancillary, support and overhead functions, in its most recent financial statement.

Toledo, Ohio-based ProMedica is laying off about 20 administrative workers.The layoffs, affecting about one-tenth of a percent of ProMedica employees, comes after the health system laid off 262 employees in January.

Los Angeles-based Prospect Medical Holdings-owned Waterbury (Conn.) Hospital notified 26 staff they will lose their jobs at the facility. Seventeen of the 26 are in clinical positions including patient assistants and surgical technicians while the remainder are nonclinical, Prospect said.

Sebastian (Fla.) River Medical Center, part of Dallas-based Steward Health Care, is reducing its workforce. The hospital implemented the limited workforce reduction, which also included the elimination of some open positions and the transfer of some nonclinical staff to other positions within Steward, a spokesperson said in a statement shared with Becker’s on Sept. 5.

Tri-City Medical Center in Oceanside, Calif., will lay off 96 employees on Sept. 30, according to a WARN notice filed in the state. All affected employees served in women’s and newborn services, a hospital representative confirmed to Becker’s.

August

The University of Michigan Health is restructuring its executive team to oversee operations at the University of Michigan Health-West in Wyoming, Mich., and Lansing, Mich.-based Sparrow Health, which it acquired in April. Four Sparrow executives have been laid off in the restructuring.

Mechanicsburg, Pa.-based Vibra Healthcare is laying off 76 employees at its specialty hospital in DeSoto, Texas, according to WARN filings from July 27. Layoffs take effect Sept. 29 at the critical access facility.

Burlington, Mass.-based Tufts Medicine is eliminating hundreds of jobs as it outsources its outreach laboratory business and some operating assets to Labcorp, according to Worker Adjustment and Retraining Notification documents filed Aug. 11. However, the health system said it will work with Labcorp to have the majority of affected employees transition to a similar position with Labcorp.

The University of Arkansas for Medical Sciences is laying off 51 workers in support services, administration and service lines. Some previously open positions will also be left vacant, the Little Rock-based institution told the Becker’s in a prepared statement. Some job duties will be reassigned.

Springfield, Ill.-based Memorial Healthannounced layoffs of hundreds of employees, including 20 percent of leadership positions. A statement shared with Becker’s indicates the reduction represents 5 percent of Memorial’s total salary and benefits.

Boone Health, a county-owned system based in Columbia, Mo., will cut 62 jobs, most of which are unfilled. Fifteen of the 62 positions are held by existing employees.

The in-home care arm of Syracuse, N.Y.-based St. Joseph’s Health, part of Livonia, Mich.-based Trinity Health, is closing in October, pending the discharge of all patients. The closure includes the termination of 71 employees. Mark McPherson, president and CEO of Trinity Health At Home, said 63 full and part-time positions are being eliminated, while the remaining eight were contingent positions.

July

Chapel Hill, N.C.-based UNC Health will lay off 246 employees. The reduction will occur after the organization ends services at a behavioral health facility in Raleigh on Sept. 30, according to a WARN notice filed July 21 with the North Carolina Department of Commerce.

Philadelphia-based Jefferson Health is reducing its workforce by about 400 positions. The reduction represents approximately 1 percent of the workforce.

Tupelo-based North Mississippi Health Services is moving forward with layoffs and job reassignments as part of its “redesign” plan to improve the organization’s financial picture, according to a message sent to NMHS employees and affiliated providers July 19. NMHS did not provide the number of affected positions or types of positions affected.

Allina Healthbegan layoffs affecting about 350 team members throughout the Minneapolis-based organization. The health system said the layoffs began July 17 and that most of the affected jobs are leadership and non-direct caregiving roles.

Middletown, N.Y.-based Garnet Health laid off 49 employees, including 25 leaders. The reductions represent 1.13 percent of the organization’s total workforce.

June

Coral Gables-based Baptist Health South Florida is offering its executives at the director level and above a “one-time opportunity” to apply for voluntary separation, according to a June 29 Miami Herald report. Decisions on buyout applications will be made during the summer.

MultiCare Health System, a 12-hospital organization based in Tacoma, Wash., will lay off 229 employees, or about 1 percent of its 23,000 staff members, including about two dozen leaders, as part of cost-cutting efforts, the health system said June 29. The layoffs primarily affect support departments, such as marketing, IT and finance.

Greensburg, Pa.-based Independence Health Systemlaid off 53 employees and has cut 226 positions — including resignations, retirements and elimination of vacant positions — since January, The Butler Eagle reported June 28. The 226 reductions began at the executive level, with 13 manager positions terminated in March.

Billings (Mont.) Clinic will lay off workers as part of a restructuring plan to address financial and operational headwinds in today’s healthcare environment, the organization confirmed. The layoffs are expected to affect approximately 27 or fewer positions.

Melbourne, Fla.-based Health First is eliminating some positions and leaving open ones vacant, Florida Today reported June 21. Seventeen jobs will be cut and 36 will be left unfilled, according to Paula Just, the health system’s chief experience officer.

Pittsburgh-based Highmark Healthlaid off 118 employees on June 21, including two from Allegheny Health Network, a spokesperson for the health system told Becker’s. The layoffs follow the health system’s cutbacks in March and April, according to the Pittsburgh Business Times. Highmark laid off 141 workers earlier this year.

Vibra Hospital of Western Massachusetts, a long-term-acute care hospital in Springfield, will lay off 87 employees by Aug. 15 ahead of the facility’s planned closure. About 30 patients will be relocated to Baystate Health’s Valley Springs Behavioral Health Hospital in Holyoke, Mass., which will open in August.

Cortez, Colo.-based Southwest Memorial Hospitallaid off nine people to help ensure the hospital is staffed appropriately, and create financial stability for the future, a spokesperson confirmed to Becker’s. The spokesperson, Chuck Krupa, said the layoffs occurred June 14 and included administrative workers. No bedside care positions were affected.

Henry Mayo Newhall Hospital in Valencia, Calif., is making “a little over 100” layoffs amid financial challenges, spokesperson Patrick Moody confirmed to Becker’s. Mr. Moody said the layoffs affect workers “in a wide range of hospital departments.” This includes some management-level employees. The hospital, which has about 1,800 employees total, is not providing specific numbers for specific job titles or departments.

Dartmouth Health is laying off 75 workers and eliminating 100 job vacancies. The layoffs came after the Lebanon, N.H.-based health system implemented a performance improvement plan in November.

Seattle Children’s is eliminating 135 leader roles, citing financial challenges. The management restructuring and reduction affects 1.5 percent of employees across the organization.

White Rock (Texas) Medical Centerlaid off 30 workers across 28 departments. The layoffs include clinical and administrative roles.

Jackson, Miss.-based St. Dominic Health Services is laying off 157 workers and ending behavioral health services. The reduction represents 5.5 percent of the hospital’s workforce.

Danville, Pa.-based Geisinger laid off 47 employees from its IT department. The reduction is part of a restructuring plan to offset high labor and supply costs.

Cascade Behavioral Health Hospital in Tukwila, Wash., is winding down operations and laying off 288 employees. The 137-bed psychiatric facility is slated to close by July 31.

Cambridge (Mass.) Health Alliance is laying off 69 employees, reducing the hours of 15 others and eliminating 170 open positions, according to The Boston Globe. The reductions are primarily in management, administrative and support areas, a health system spokesperson told Becker’s.

May

Wenatchee, Wash.-based Confluence Health has eliminated its chief operating officer amid restructuring efforts and financial pressures, the health system confirmed to Becker’s May 16.

Conemaugh Memorial Medical Center, a Duke LifePoint hospital in Johnstown, Pa., has laid off less than 1 percent of its workforce, the hospital confirmed to Becker’s May 15.

Community Health Network, a nonprofit health system based in Indianapolis, plans to cut an unspecified number of jobs as it restructures its workforce and makes organizational changes. The health system confirmed the job cuts in a statement shared with Becker’s on May 11. It did not say how many jobs would be cut or which positions would be affected.

New Orleans-based Ochsner Health eliminated 770 positions, or about 2 percent of its workforce, on May 11. This is the largest layoff to date for the health system.

Cedars-Sinai Medical Center eliminated the positions of 131 employees and cut about two dozen other jobs at related Cedars-Sinai facilities, a spokesperson confirmed via a statement shared with Becker’s May 7. The Los Angeles-based organization said reductions represent less than 1 percent of the workforce and apply to management and non-management roles primarily in non-patient care jobs.

Rochester (N.Y.) Regional Health is eliminating about 60 positions. A statement from RRH said the changes affect less than one-half percent of the system population, mostly in nonclinical and management positions.

Memorial Health Systemlaid off fewer than 90 people, or less than 2 percent of its workforce.The Gulfport, Miss.-based health system said May 2 that most of the affected positions are nonclinical or management roles, and the majority do not involve direct patient care.

Monument Healthlaid off at least 80 employees, or about 2 percent of its workforce. The Rapid City, S.D.-based system said positions are primarily corporate service roles and will not affect patient services. Unfilled corporate service positions were also eliminated.

April

Habersham Medical Center in Demorest, Ga., laid off four executives. The layoffs are part of cost-cutting measures before the hospital joins Gainesville-based Northeast Georgia Health System in July, nowhaberbasham.com reported April 27.

Scripps Health is eliminating 70 administrative roles, according to WARN documents filed by the San Diego-based health system in March. The layoffs take effect May 8 and affect corporate positions in San Diego and La Jolla, Calif.

Trinity Health Mid-Atlantic, part of Livonia, Mich.-based Trinity Health, eliminated fewer than 40 positions, a spokesperson confirmed to Becker’s April 24. The layoffs represent 0.5 percent of the health system’s approximately 7,000-person workforce.

PeaceHealth eliminated 251 caregiver roles across multiple locations. The Vancouver, Wash.-based health system said affected roles include 121 from Shared Services, which supports its 16,000 caregivers in Washington, Oregon and Alaska.

Toledo, Ohio-based ProMedica plans to lay off 26 skilled nursing support staff. The layoffs, effective in June, affect 20 employees who work remotely across the U.S, and six who work at the ProMedica Summit Center in Toledo, according to a Worker Adjustment and Retraining Notification filed April 18. Most affected positions support sales, marketing and administrative functions for the skilled nursing facilities, Promecia told Becker’s.

Northern Inyo Healthcare District, which operates a 25-bed critical access hospital in Bishop, Calif., anticipates eliminating about 15 positions, or less than 4 percent of its 460-member workforce, by April 21, a spokesperson confirmed to Becker’s. The layoffs include nonclinical roles within support and administration, according to a news release. No further details were provided about specific positions affected.

West Reading, Pa.-based Tower Health is eliminating 100 full-time equivalent positions. The move will affect 45 individuals, according to an April 13 news release the health system shared with Becker’s. The other 55 positions are either recently vacated or involve individuals who plan to retire in the coming weeks and months.

Grand Forks, N.D.-based Altru Health is trimming its executive team as its new hospital project moves forward. The health system is trimming its executive team from nine to six and incentivizing 34 other employees to take early retirement.

Tacoma, Wash.-based Virginia Mason Franciscan Health laid off nearly 400 employees, most of whom are in non-patient-facing roles. The job cuts affected less than 2 percent of the health system’s 19,000-plus workforce.

Katherine Shaw Bethea Hospital in Dixon, Ill., will lay off 20 employees, citing financial headwinds affecting health organizations across the U.S. It will also leave other positions unfilled to reduce expenses amid rising labor and supply costs and reductions in payments by insurance plans. Affected employees largely work in administrative support areas and not direct patient care.

Danbury, Conn.-based Nuvance Health will close a 100-bed rehabilitation facility in Rhinebeck, N.Y., resulting in 102 layoffs. The layoffs are effective April 12, according to the Daily Freeman.

March

Charleston, S.C.-based MUSC Health University Medical Center laid off an unspecified number of employees from its Midlands hospitals in the Columbia, S.C. area. Division President Terry Gunn also resigned after the facilities missed budget expectations by $40 million in the first six months of the fiscal year, The Post and Courier reported March 30.

Winston-Salem, N.C.-based Novant Health laid off about 50 workers, including C-level executives, the health system confirmed to Becker’s March 29. The layoffs affected Jesse Cureton, the health system’s executive vice president and chief consumer officer since 2013; Angela Yochem, its executive vice president and chief transformation and digital officer since 2020; and Paula Dean Kranz, vice president of innovation enablement and executive director of the Novant Health Innovation Labs.

Penn Medicine Lancaster (Pa.) General Health eliminated fewer than 65 jobs, or less than 1 percent of its workforce of about 9,700, the health system confirmed to Becker’s March 30. The layoffs include support, administrative and executive roles, and COVID-19-related support staff, spokesperson John Lines said, according to lancasteronline.com. Mr. Lines did not provide a specific number of affected workers.

McLaren St. Luke’s Hospital in Maumee, Ohio, will lay off 743 workers, including 239 registered nurses, when it permanently closes this spring. Other affected roles include physical therapists, radiology technicians, respiratory therapists, pharmacists and pharmacy support staff, and nursing assistants. The hospital’s COO is also affected, and a spokesperson for McLaren Health Care told Becker’s other senior leadership roles are also affected.

Bellevue, Wash.-based Overlake Medical Center and Clinics laid off administrative staff, the health system confirmed to the Puget Sound Business Journal. The layoffs, which occurred earlier this year, included 30 workers across Overlake’s human resources, information technology and finance departments, a spokesperson said, according to the publication. This represents about 6 percent of the organization’s administrative workforce. Overlake’s website says it employs more than 3,000 people total.

Columbia-based University of Missouri Health Care is eliminating five hospital leadership positions across the organization, spokesperson Eric Maze confirmed to Becker’s March 20. Mr. Maze did not specify which roles are being eliminated saying that the organization won’t address individual personnel actions. According to MU Health Care, the move is a result of restructuring “to better support patients and the future healthcare needs of Missourians.”

Greensboro, N.C.-based Cone Health eliminated 68 senior-level jobs. The job eliminations occurred Feb. 21, Cone Health COO Mandy Eaton told The Alamance News. Of the 68 positions eliminated, 21 were filled. Affected employees were offered severance packages.

The newly merged Greensburg, Pa.-based organization made up of Excela Health and Butler Health System eliminated 13 filled managerial jobs. The affected employees and positions are from across both sides of the new organization, Tom Chakurda, spokesperson for the Excela-Butler enterprise, confirmed to Becker’s. The positions were in various support functions unrelated to direct patient care.

Crozer Health, a four-hospital system based in Upland, Pa., is laying off roughly 215 employees amid financial challenges. The system announced the layoffs March 15 as part of its “operational restructuring plan” that “focuses on removing duplication in administrative oversight and discontinuing underutilized services.” Affected employees represent about 4 percent of the organization’s workforce.

Philadelphia-based Penn Medicine is eliminating administrative positions. The change is part of a reorganization plan to save the health system $40 million annually, the Philadelphia Business Journal reported March 13. Kevin Mahoney, CEO of the University of Pennsylvania Health System, told Penn Medicine’s 49,000 employees last week that changes include the elimination of a “small number of administrative positions which no longer align with our key objectives,” according to the publication. The memo did not indicate the exact number of positions that were eliminated.

Sovah Health, part of Brentwood, Tenn.-based Lifepoint Health, eliminated the COO positions at its Danville and Martinsville, Va., campuses. The responsibilities of both COO roles will now be spread across members of the existing administrative team.

Valley Health, a six-hospital health system based in Winchester, Va., eliminated 31 administrative positions. The job cuts are part of the consolidation of the organization’s leadership team and administrative roles.

Marshfield (Wis.) Clinic Health System said it would lay off 346 employees, representing less than 3 percent of its employee base.

Roseville, Calif.-based Adventist Health plans to go from seven networks of care to five systemwide to reduce costs and strengthen operations. The reorganization will result in job cuts, including reducing administration by more than $100 million.

Arcata, Calif.-based Mad River Community Hospital is cutting 27 jobs as it suspends home health services.

Hutchinson (Kan.) Regional Medical Center laid off 85 employees, a move tied to challenges in today’s healthcare environment.

January

Oklahoma City-based OU Health eliminated about 100 positions as part of an organizational redesign to complete the integration from its 2021 merger.

Memorial Sloan Kettering Cancer Center announced it would lay off to reduce costs amid widespread hospital financial challenges. The layoffs are spread across 14 sites in New York City, and equate to about 1.8 percent of Memorial Sloan’s 22,500 workforce.

St. Louis-based Ascension completed layoffs in Texas, the health system confirmed in January. A statement shared with Becker’s says the layoffs primarily affected nonclinical support roles. The health system declined to specify to Becker’s the number of employees or positions affected.

Chillicothe, Ohio-based Adena Health System announced it would eliminate 69 positions — 1.6 percent of its workforce — and send 340 revenue cycle department employees to Ensemble Health Partners’ payroll in a move aimed to help the health system’s financial stability.

Ascension St. Vincent’s Riverside in Jacksonville, Fla., will end maternity care at the hospital, affecting 68 jobs, according to a Workforce Adjustment and Retraining Notification filed with the state Jan. 17. The move will affect 62 registered nurses as well as six other positions.

Visalia, Calif.-based Kaweah Health said it aimed to eliminate 94 positions as part of a new strategy to reduce labor costs. The job cuts come in addition to previously announced workforce reductions; the health system already eliminated 90 unfilled positions and lowered its workforce by 106 employees.

Oklahoma City-based Integris Health said it would eliminate 200 jobs to curb expenses. The eliminations include 140 caregiver roles and 60 vacant jobs.

Toledo, Ohio-based ProMedica announced plans to lay off 262 employees, a move tied to its exit from a skilled-nursing facility joint venture late last year. The layoffs will take effect between March 10 and April 1.

Employees at Las Vegas-based Desert Springs Hospital Medical Center were notified of layoffs coming to the facility, which will transition to a freestanding emergency department. There are 970 employees affected. Desert Springs is part of the Valley Health System, a system owned and operated by King of Prussia, Pa.-based Universal Health Services.

Philadelphia-based Jefferson Health plans to go from five divisions to three in an effort to flatten management and become more efficient. The reorganization will result in an unspecified number of job cuts, primarily among executives.

December

Pikeville (Ky.) Medical Center said it would lay off 112 employees as it outsources its environmental services department. The 112 layoffs were effective Jan. 1, 2023.

Southern Illinois Healthcare, a four-hospital system based in Carbondale, announced it would eliminate or restructure 76 jobs in management and leadership. The 76 positions fall under senior leadership, management and corporate services. Included in that figure are 33 vacant positions, which will not be filled. No positions in patient care are affected.

Citing a need to further reduce overhead expenses and support additional investments in patient care and wages, Traverse City, Mich.-based Munson Health said it would eliminate 31 positions and leave another 20 jobs unfilled. All affected positions are in corporate services or management. The layoffs represent less than 1 percent of the health system’s workforce of nearly 8,000.

November

West Reading, Pa.-based Tower Health on Nov. 16 laid off 52 corporate employees as the health system shrinks from six hospitals to four. The layoffs, which are expected to save $15 million a year, account for 13 percent of Tower Health’s corporate management staff.

St. Vincent Charity Medical Center in Cleveland closed its inpatient and emergency room care Nov. 11, four days before originally planned — and laid off 978 workers in doing so. After the transition, the Sisters of Charity Health System will offer outpatient behavioral health, urgent care and primary care.

October

Sioux Falls, S.D.-based Sanford Health announced layoffs affecting an undisclosed number of staff in October, a decision its CEO said was made “to streamline leadership structure and simplify operations” in certain areas. The layoffs primarily affect nonclinical areas.

A number of healthcare organizations have recently closed medical departments or ended services at facilities to shore up finances, focus on more in-demand services or address staffing shortages.

Here are 45 closures or services ending, announced, advanced or finalized that Becker’s has reported since Feb. 2:

1. Vicksburg, Miss.-based Merit Health River Regionclosed its behavioral health unit on June 30.

2. Wilkes-Barre (Pa.) General Hospital moved up the date it planned to end childbirth services by about three weeks, with the care ending abruptly July 11.

3. Good Samaritan Hospital, operated by Nashville, Tenn.-based HCA Healthcare, plans to close the inpatient psychiatric facility at its Mission Oaks Hospital in Los Gatos, Calif., on Aug. 20.

4. Philadelphia-based Penn Medicine shut down one of its urgent care centers, Penn Urgent Care South Philadelphia, on June 30, as more patients are turning to telehealth for care.

5. Hartford City, Ind.-based IU Health Blackford Hospital announced it will close its emergency department and no longer offer inpatient services due to a reduction in patient volume.

6. The Illinois Health Facilities and Services Review Board on June 27 unanimously approved a request from HSHS St. Mary’s Hospital to shutter four of its units. The Decatur, Ill.-based hospital will wrap up its advanced inpatient rehabilitation, obstetrics and newborn nursery, pediatrics and inpatient behavioral health services.

7. Albany, N.Y.-based St. Peter’s Health Partners submitted a plan to the state Department of Health to shut down the maternity unit at Samaritan Hospital. If approved, the Troy, N.Y., hospital will close the unit in about four to six months.

8. Jackson, Miss.-based St. Dominic Health Services is ending its behavioral health services unit, citing financial difficulties. The unit stopped taking admissions after June 6.

9. Fort Wayne, Ind.-based Lutheran Hospital is closing its heart transplant and inpatient burn units due to low patient volumes. The inpatient burn unit stopped accepting new patients June 2.

10. Worcester, Mass.-based UMass Memorial Health plans to close the maternity ward at its HealthAlliance-Clinton Hospital Sept. 22 due to staff shortages and a declining number of births in the area.

11. Vancouver, Wash.-based PeaceHealth closed its pediatric cardiology clinic, sleep clinic, optometry clinic and optical shop July 21. It also ended its comprehensive outpatient palliative care May 26 and reduced staff to one nurse and one social worker for in-home care.

12. Milwaukee-based Froedtert closed the behavioral health unit at Froedtert Menomonee Falls (Wis.) May 12.

13. Welch (W.Va.) Community Hospitalannounced plans to close its long-term care unit. The closure of the 59-bed unit is part of the hospital’s transition to the West Virginia University Health System.

14. Peoria, Ill.-based OSF HealthCare is closing its labor and delivery services at OSF Heart of Mary Medical Center in Urbana, Ill. Starting in September, labor and delivery patients will be redirected to OSF Sacred Heart Medical Center in Danville, Ill. or OSF St. Joseph Medical Center in Bloomington, Ill.

15. Northern Maine Medical Center in Fort Kent closed its obstetrics unit May 26. The move comes as birth rates decline in the area along with staffing trouble.

16. Philadelphia-based Jefferson Health ended acute care, general surgery and emergency services at Einstein Medical Center Elkins Park (Pa.) and convert the facility solely into a physical rehabilitation provider.

17. CoxHealth closed the labor and delivery unit at Cox (Mo.) Monett Hospital, citing difficulties recruiting obstetricians and family practice physicians.

18. Warsaw, N.Y.-based Wyoming County Community Health Systemended its birthing services June 1 amid financial challenges and declining births in the area.

19. Alta Vista Regional Hospital in Las Vegas, N.M., ended intensive care unit services June 3. The hospital said the change would allow it to focus on its highly utilized medical-surgical unit.

20. Springfield, Ore.-based McKenzie-Willamette Medical Center closed its maternity health practice July 7. The for-profit McKenzie-Willamette hospital said the 11-employee midwifery program was “unsustainable.”

21. Renton, Wash.-based Providence ended labor and delivery at Petaluma (Calif.) Valley Hospital May 1 until further notice.

22. Gardner, Mass.-based Heywood Hospitalclosed its pulmonary unit in mid-April due to financial reasons.

23. Yale New Haven (Conn.) Hospital “ceased use” of its emergency use annex April 11 amid discussions to extend its certificate of occupancy.

24. Chelsea (Mich.) Hospitalclosed its inpatient behavioral health unit and moved 12 of its beds to Trinity Health Ann Arbor.

25. Danbury, Conn.-based Nuvance Health closedThompson House, a 100-bed rehabilitation facility in Rhinebeck, N.Y., and laid off its 102 employees, effective April 12.

26. Holly Springs, Miss.-based Alliance HealthCare System began transitioning to rural emergency hospital status March 31, meaning it will end all inpatient care services.

27. MercyOne North Iowaclosed its hospice facility in Mason City April 17 amid industry pressures of inflation and high labor costs.

28. Brewer, Maine-based Northern Light Health is no longer providing cataract, glaucoma and oculoplastic surgeries at Eastern Maine Medical Center in Bangor.

29. Plymouth, Ind.-based St. Joseph Health Systemclosed its New Beginnings Birthplace center because it has been unable to attract an obstetrician. It also closed its OB-GYN office March 31.

30. Springfield, Mass.-based Baystate Health and medical services provider Shields Healthclosed their urgent care clinic locations in Feeding Hills, Longmeadow and Westfield, Mass., on March 31.

31. Palomar Medical Center Poway (Calif.), part of Escondido, Calif.-based Palomar Health, closed its labor and delivery unit, at least temporarily, in June.

32. A combination of a loss of pediatricians, changing demographics and some of the strictest abortion laws in the country forced Sandpoint, Idaho-based Bonner General Hospital to end obstetrics services.

33. Cabell Huntington (W.Va.) Hospital, part of Mountain Health Network, closed its CHH Surgery Center April 28 and is phasing out its home health services to better align its resources and reduce costs amid financial headwinds.

34. The only hospital in Manitowoc, Wis., a city of nearly 35,000 — Froedtert Holy Family Memorial Hospital — stopped all obstetrics care June 1.

35. Citing a lack of provider coverage, Ocean Springs, Miss.-based Singing River Health Systemsaid it would end obstetric services, which include labor and delivery, at Singing River Gulfport (Miss.), at least temporarily. The move became effective April 1.

36. Astria Toppenish (Wash.) Hospital is one of many rural hospitals closing labor and delivery care due to costs, creating maternity deserts in areas that need care most, The New York Times reported.

37. Cleveland-based University Hospitalsended labor and delivery services at UH Lake West in Willoughby, Ohio, April 15. The hospital said services would be consolidated at TriPoint in Concord Township, which is about 15 miles away.

38. Jefferson, Mo.-based Capital Region Medical Center closed two clinics in Holts Summit and St. Elizabeth, Mo., April 15.

39. In February, Trinity Health Muskegon (Mich.)announced plans to temporarily close a 30-bed surgical floor due to staffing shortages.

40. St. Mark’s Medical Center in La Grange, Texas, cut nearly half its staff and various services as it looks to survive amid significant financial challenges. Service cuts include inpatient and surgical services, post-acute skilled rehab care, its orthopedic clinic, speech therapy and ambulatory care.

41. OhioHealth’s Shelby Hospitalstopped providing maternity services Feb. 28. Maternity services are provided 13 miles away at OhioHealth Mansfield Hospital.

42. Arcata, Calif.-based Mad River Community Hospitalcut 27 jobs as it suspends its home health services program. The program will be suspended upon the completion of services to the hospital’s existing patients, which was expected to be in April.

43. Oroville (Calif.) Hospitalclosed Golden Valley Home Health, the hospital’s home health business.

44. Ascension Providence Hospital-Southfield (Mich.)ended midwifery services in February.

45. Rumford (Maine) Hospitalclosed its maternity program March 31 after 97 years in service.

A couple of months ago, I got a call from a CEO of a regional health system—a long-time client and one of the smartest and most committed executives I know. This health system lost tens of millions of dollars in fiscal year 2022 and the CEO told me that he had come to the conclusion that he could not solve a problem of this magnitude with the usual and traditional solutions. Pushing the pre-Covid managerial buttons was just not getting the job done.

This organization is fiercely independent. It has been very successful in almost every respect for many years. It has had an effective and stable board and management team over the past 30 to 40 years.

But when the CEO looked at the current situation—economic, social, financial, operational, clinical—he saw that everything has changed and he knew that his healthcare organization needed to change as well. The system would not be able to return to profitability just by doing the same things it would have done five years or 10 years ago. Instead of looking at a small number of factors and making incremental improvements, he wanted to look across the total enterprise all at once. And to look at all aspects of the enterprise with an eye toward organizational renovation.

I said, “So, you want a makeover.”

The CEO is right. In an environment unlike anything any of us have experienced, and in an industry of complex interdependencies, the only way to get back to financial equilibrium is to take a comprehensive, holistic view of our organizations and environments, and to be open to an outcome in which we do things very differently.

In other words, a makeover.

Consider just a few areas that the hospital makeover could and should address:

There’s the REVENUE SIDE: Getting paid for what you are doing and the severity of the patient you are treating—which requires a focus on clinical documentation improvement and core revenue cycle delivery—and looking for any material revenue diversification opportunities.

There is the relationship with payers: Involving a mix of growth, disruption, and optimization strategies to increase payments, grow share of wallet, or develop new revenue streams.

There’s the EXPENSE SIDE: Optimizing workforce performance, focusing on care management and patient throughput, rethinking the shared services infrastructure, and realizing opportunities for savings in administrative services, purchased services, and the supply chain. While these have been historic areas of focus, organizations must move from an episodic to a constant, ongoing approach.

There’s the BALANCE SHEET: Establishing a parallel balance sheet strategy that will create the bridge across the operational makeover by reconfiguring invested assets and capital structure, repositioning the real estate portfolio, and optimizing liquidity management and treasury operations.

There is NETWORK REDESIGN: Ensuring that the services offered across the network are delivered efficiently and that each market and asset is optimized; reducing redundancy, increasing quality, and improving financial performance.

There is a whole concept around PORTFOLIO OPTIMIZATION: Developing a deep understanding of how the various components of your business perform, and how to optimize, scale back, or partner to drive further value and operational performance.

Incrementalism is a long-held business approach in healthcare, and for good reason. Any prominent change has the potential to affect the health of communities and those changes must be considered carefully to ensure that any outcome of those changes is a positive one. Any ill-considered action could have unintended consequences for any of a hospital’s many constituencies.

But today, incrementalism is both unrealistic and insufficient.

Just for starters, healthcare executive teams must recognize that back-office expenses are having a significant and negative impact on the ability of hospitals to make a sufficient operating margin. And also, healthcare executive teams must further realize that the old concept of “all things to all people” is literally bringing parts of the hospital industry toward bankruptcy.

As I described in a previous blog post, healthcare comprises some of the most wicked problems in our society—problems that are complex, that have no clear solution, and for which a solution intended to fix one aspect of a problem may well make other aspects worse.

The very nature of wicked problems argues for the kind of comprehensive approach that the CEO of this organization is taking—not tackling one issue at a time in linear fashion but making a sophisticated assessment of multiple solutions and studying their potential interdependencies, interactions, and intertwined effects.

My colleague Eric Jordahl has noted that “reverting to a 2019 world is not going to happen, which means that restructuring is the only option. . . . Where we are is not sustainable and waiting for a reversion is a rapidly decaying option.”

The very nature of the socioeconomic environment makes doing nothing or taking an incremental approach untenable. It is clearly beyond time for the hospital industry makeover.

Physician staffing firm Envision Healthcare filed for Chapter 11 bankruptcy this week, but will “continue operating its business as usual” so that the company can “provide patients with the high-quality care they require.”

Envision Healthcare files for Chapter 11 bankruptcy

On Monday, Envision Healthcare filed for Chapter 11 bankruptcy in the U.S. Bankruptcy Court for the Southern District of Texas. Following the filing, all of the company’s debt — except for a revolving credit facility for working capital — will be cancelled, totaling around $5.6 billion.

In a news release, Envision said several events have placed significant pressure on its finances since it was acquired by private equity (PE) firm KKR for $10 billion in 2018.

“The lingering impacts from COVID-19 on volume and labor costs, the delays resulting from tactics and recalcitrance by Envision’s largest insurance payors, and the ongoing regulatory uncertainty caused by the flawed implementation of the No Surprises Act have proven too much,” said Paul Keglevic, Envision’s chief restructuring officer.

Throughout the pandemic, healthcare staffing firms struggled to find enough workers to meet patient demand, especially in the highly competitive contract labor market, Modern Healthcare reports.

While Envision said it filed for bankruptcy because it is not generating enough revenue to cover its expenses and debt, it currently has $665 million of cash in the bank. According to the filing, the company expects those funds to help it exit bankruptcy faster.

“The decision to file these chapter 11 cases now, while the debtors have ample cash on hand, will ensure that the company can continue to provide patients with the high-quality care they require,” Keglevic said in the filings.

The company has entered a Restructuring Support Agreement (RSA), with plans to operate normally during the restructuring. Pending court approval, Envision said it will tap into cash collateral from ongoing operations to cover costs, “including supplier obligations and employee wages, salaries, and benefits during the restructuring process.”

“This will enable the company to continue operating its business as usual throughout the process and provide support to critical partners, including clinicians, hospitals, vendors and suppliers,” the company said.

Under the RSA, the company will divide its primary businesses, AMSURG and Envision Physician Services, which will be owned by their respective lenders.

Does Envision’s bankruptcy spell trouble for other PE investments?

Envision isn’t like other medical group PE investments

As we discussed in a previous expert insight, PE investments in physician practices aren’t a monolith. Many different types of medical groups receive investments, and PE firms have a range of healthcare sector experience and business practices.

Envision is an example of an outlier in all of these areas. First, their physician services are all hospital-based, with a heavy emphasis on emergency medicine — this contrasts with the predominant wave of physician practice investment in ambulatory practices. KKR only has one other physician practice investment, and their healthcare portfolio is rather limited.

Most importantly, Envision’s business model was reliant on exploiting questionable business practices and loopholes, which were heavily impacted by the No Surprises Act.

So, this bankruptcy isn’t an indictment of PE investment in physician groups. It just shows that healthcare organizations are not immune to being caught on their bad business practices — though PE, which is already struggling in the court of public opinion, won’t be helped by Envision’s demise.

What Envision’s bankruptcy means

Envision’s bankruptcy shines a light on trends we’ve been watching with hospital-based medicine that make financial solvency challenging: the strain of uninsured patients on revenue, workforce shortages driving up labor costs, and COVID-related volume impacts, to name a few.

What’s different with the average health system compared to Envision? While clearly rife with inefficiencies, health systems have mechanisms to self-correct.

Envision’s business model was not an innovation on care design or delivery.

It was a model taking advantage of pricing distortions and patients who are not in a position to shop for emergency care. That model inherently has limited running room.

On the physician practice front, Envision’s bankruptcy highlights the challenging business environment PE firms choose to enter when they invest in physician practices. Medical groups are a low-margin business, and the running room on cost savings has a low ceiling.

While many of the highest profile PE investments in physician groups come from firms with a long track record in the physician space, it remains to be seen whether the return on their investments will be high enough to satisfy investors.

The spotlight on large, heavily resourced healthcare organizations is not going away anytime soon. In fact, as consolidation continues, new investors enter the forefront, and organizations diversify the type of assets they acquire, that spotlight is only getting brighter.

Last week, California’s legislature passed a bill establishing the Distressed Hospital Loan Program, which will dole out $150M in interest-free emergency loans to struggling nonprofit hospitals in the state which meet specific eligibility criteria, including operating in an underserved area and serving a large share of Medicaid beneficiaries. A combination of state agencies will establish a specific methodology for selection, but hospitals that are part of a health system with more than two separately licensed hospital facilities will be ineligible.

Hospitals receiving loans must provide a plan for how they will use the loans to achieve financial sustainability, and must pay back the money within six years.

The Gist: With twenty percent of the state’s hospitals at risk of shuttering, California lawmakers are hoping to provide the most vulnerable hospitals an alternative to either closure or consolidation, an example other states may follow. But unlike the Paycheck Protection Program loans that shored up businesses through the pandemic’s initial disruption, the outlook for small, struggling, independent hospitals isn’t expected to improve in coming years, even if the economy recovers.

Whether these loans provide lifelines or merely serve as Band-Aids on an untenable situation will depend on whether recipient hospitals can use them to restructure their operating models to absorb increased labor costs amid stagnating volumes and commercial reimbursement.

If these loans aren’t used for transformation, they will only delay the inevitable: more closures, and more mergers to find shelter in scale.