The nonprofit health system narrowed its operating loss while continuing to grapple with financial and policy pressures as it progresses towards profitability.

KEY TAKEAWAYS

Providence cut its operating loss in the second quarter to $21 million, improving from a $123 million loss a year ago.

Revenue rose 3% year-over-year to $7.91 billion, driven by higher patient volumes and better commercial rates.

The health system faces ongoing “polycrisis” challenges, including rising supply costs, staffing mandates, insurer denials, and looming Medicaid cuts, which have already prompted layoffs, hiring pauses, and leadership restructuring.

Providence made promising strides toward financial sustainability in the second quarter as higher patient volumes helped trim an operating loss that has weighed heavily on its balance sheet.

Yet the Renton, Washington-based health system warned that a compounding set of external pressures, which it labeled a “polycrisis,” still poses formidable challenges to its mission and future.

For the three months ended June 30, the nonprofit reported an operating loss of $21 million, equating to an operating margin of –0.3%, representing a marked improvement from the $123 million loss (–1.6%) posted over the same period in 2024. Compared with the previous quarter, the gain was even starker as Providence trimmed its deficit by $223 million. Through the first six months of the year, the health system had an operating loss of $265 million (-1.7%).

Revenue growth was fueled by higher patient volumes and improved commercial rates, Providence highlighted. Operating revenue rose 3% year-over-year to $7.91 billion as inpatient admissions (up 3%), outpatient visits (up 3%), case mix–adjusted admissions (up 3%), physician visits (up 8%), and outpatient surgeries (up 5%) all contributed.

On the expense side, Providence managed a 2% rise in operating costs to $7.93 billion, thanks largely to productivity gains, including a 43% reduction in agency contract labor. However, supply costs swelled by 9% and pharmacy expenses jumped by 12% year-over-year.

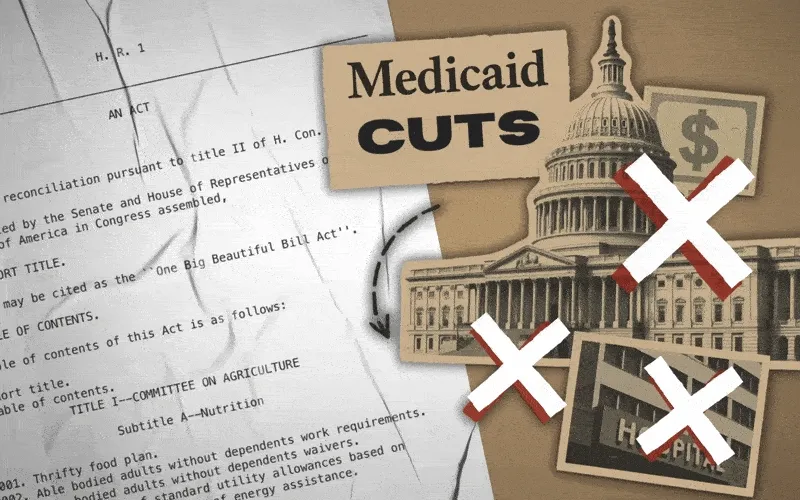

Providence, along with the healthcare industry at large, faces what CEO Erik Wexler called a “polycrisis” due to a mix of inflation, tariff-driven supply pressures, new state laws on staffing and charity care, insurer reimbursement delays and denials, and looming federal Medicaid cuts, especially from the One Big Beautiful Bill Act, which the health system said “threatens to intensify health care pressures.”

Those factors are significantly influencing hospitals’ and health systems’ decision-making. Providence has made staffing adjustments that include cutting 128 jobs in Oregon earlier this month, a restructuring in June that eliminated 600 full-time equivalent positions, apause on nonclinical hiring in April, and leadership reorganization since Wexler took over as CEO in January.

Accounts receivable is another area that has been indicative of headwinds, with Providence noting that while it improved in the second quarter, it “remains elevated compared to historical trends.”

Even with the roadblocks in its path, Providence is working towards profitability after being in the red for several years running.

“I’m incredibly proud of the progress we’ve made and grateful to our caregivers and teams across Providence St. Joseph Health for their continued dedication,” Wexler said in the news release. “The strain remains, especially with emerging challenges like H.R.1, but we will continue to respond to the times and answer the call while transforming for the future.”

New Medicaid funding rules proposed by Congress this week would halt efforts at the state level to better fund rural hospitals and deliver services to the most vulnerable populations in those areas. You can be certain that the administrators and staff of those hospitals, as well as leaders of the communities they serve, are watching closely to see if the cuts are enacted.

Lawmakers at the federal level are trying to make deeper cuts to Medicaid spending in an effort to lower the amount of deficit spending that would be created by President Trump’s spending plan. Trump has dubbed the plan his “big beautiful bill.”

Feds Would Strip Rural Hospitals of Lifeline Funds

Republican members of the Senate Finance Committee this week released their version of the bill that would drain funding for rural hospitals, which rely heavily on Medicaid funds to treat patients. It’s estimated that 25 to 40 percent of services provided by such hospitals are funded by Medicaid.

The federal government and states share the up-front medical costs for Medicaid patients. The federal government then reimburses states up to 50 percent of their Medicaid spending every year.

Many states fund their portion of the cost by taxing entities that provide those services to Medicaid patients.

The latest proposal in Congress would not only restrict how many patients could receive benefits, but it would also stop states from implementing those provider tax programs to help fund Medicaid services provided to residents.

At the federal level, the thinking is that if states keep taxing providers to fund Medicaid services, then the federal government will have to keep reimbursing states a portion of those costs.

The downside to that is many experts, along with several Republicans in Congress, namely Sens. Susan Collins of Maine, Lisa Murkowski of Alaska and Josh Hawley of Missouri, have predicted it will decimate rural hospitals.

West Virginia Republican Sen. Jim Justice went a step further, saying that the plan to limit states’ use of provider taxes will “really hurt a lot of folks.” Despite that statement, Justice said he is OK with the freeze.

State Lawmakers Sound the Alarm

There are 39 states with at least three or more provider taxes used to help fund Medicaid services. Alaska is the only state with no such tax.

Some states, such as Ohio, have set up a new rural hospital fund using provider taxes to help rural hospitals deliver Medicaid services to patients.

Ohio Governor Mike DeWine and the Republican-led state legislature set up a pilot program called the Rural Ohio Hospital Tax Pilot Program. The measure would allow counties to levy a tax on their local hospitals that would then be used to fund Medicaid services.

DeWine said the pilot program would help ease the financial stress rural hospitals face in Ohio. The plan contained in Ohio House Bill 96 has the blessing of the Ohio Hospital Association.

A group of Republican state lawmakers recently sent a letter to their federal counterparts pleading with them to remove the bill language because it would “torpedo” plans to keep rural hospitals functioning.

The American Hospital Association, a 130-year-old trade group of more than 5,000 hospitals and health care providers, this month released the impact on rural hospitals if this plan went into effect.

More than $50 billion would be lost by 2034, and more than 1.8 million rural Americans would lose health benefits.

Kentucky residents would be impacted the most, with 143,000 losing benefits, followed by 135,000 Californians. More than 86,000 Ohioans would lose Medicaid coverage under the plan by 2034, making it the third most impacted state.

To blunt the effects of the cuts, Collins reportedly is proposing the establishment of a $100 billion relief fund that could provide financial support to affected providers, rural hospitals in particular. Whether that or a similar but smaller fund will wind up in the final draft of the legislation apparently will be decided this weekend. Meanwhile, the Senate parliamentarian has ruled against many of the provisions of the Senate version of the bill, including the Finance Committee’s provider tax framework, which puts the whole thing in flux.

Senate leaders say they plan a long series of votes on amendments of the bill on Sunday. The “vote-arama” likely will go on throughout Sunday night and into Monday. If the Senate does pass its version of the bill, it will have to go back to the House. Lawmakers are under a self-imposed deadline to get the legislation to Trump by the July 4 holiday.

A bipartisan Senate report on private equity ownership of two health systems shows PE investment puts a priority of profit over patient health and hospital finances.

A yearlong investigation found that patient care deteriorated at both systems, while private equity owners received millions, according to the Senate Budget Committee’s bipartisan staff report, “Profits Over Patients: The Harmful Effects of Private Equity on the U.S. Health Care System.”

The investigation was led by Senate Budget Committee Chairman Sheldon Whitehouse, D-R.I., and Ranking Member Charles E. Grassley, R-Iowa.

WHY THIS MATTERS

The report centered on the hospital Ottumwa Regional Health Center in Iowa and its operating company, Lifepoint Health in Tennessee.

Private equity company Apollo Global Management owns Lifepoint Health.

The investigation expanded to include other entities, including PE firmLeonard Green & Partners and hospital operator Prospect Medical Holdings, in which Leonard Green & Partners held a majority stake. Leonard Green & Partners (LGP) is a private equity firm in Los Angeles that owns hospitals under Prospect Medical Holdings (PMH).

“LGP and PMH’s primary focus was on financial goals rather than quality of care at their hospitals, leading to multiple health and safety violations as well as understaffing and the closure of several hospitals,” the report said.

The investigation originated from questions over the role, if any, private equity played in a series of patient sexual assaults by a nurse practitioner at the Iowa hospital. In 2022, a nurse practitioner fatally overdosed on drugs acquired at the hospital. Police discovered the nurse had sexually assaulted nine incapacitated female patients over a two-year period, the report said.

Prospect Medical Holdings owns and operates hospitals in urban and suburban areas, primarily on the East and West Coasts, including Connecticut, Rhode Island, Pennsylvania and California.

It is a previously public traded company that went private in 2010 when LGP acquired a 61% majority stake. During the course of LGP’s majority ownership, Prospect Medical Holdings acquired 16 hospitals over a span of four years. PMH has operated a total of 21 unique hospitals, the report said.

Apollo has a 97% ownership stake in Lifepoint Health, a company that owns and operates acute care hospitals in predominantly rural areas. This includes Ottumwa Regional Health Center. Apollo owns around 220 hospitals nationwide, making it the single largest private equity owner of hospitals in the United States, the report said.

Ottumwa has been under PE ownership since 2010, when it was acquired by the PE-owned hospital operator RegionalCare, which was later acquired by Apollo.

KEY FINDINGS

The report’s key findings show that LGP controlled the Prospect Medical Holding board of directors, which incentivized management to satisfy financial goals regardless of patient outcomes.

“According to documents obtained by the committee, discussion amongst PMH and LGP leadership during board meetings centered around profits, costs, acquisitions, managing labor expenses and increasing patient volume – with little or no discussion of patient outcomes or quality of care.”

Current PMH leadership has overseen the closure of eight hospitals, with three-fourths coming during or directly after LGP’s majority ownership, including four in Texas and two in Pennsylvania.

Several hospitals suffered from labor cuts, decreased patient capacity, unsafe building maintenance and financial distress, the report said.

Despite this, LGP took home $424 million of the $645 million that PMH paid out in dividends and preferred stock redemption, in addition to over $13 million in fees, leaving PMH in severe financial distress.

In order to pay investors dividend distributions, PMH was forced to take on hundreds of millions of dollars in debt, running out of cash and defaulting on its loans, the report said.

ORHC’s PE owned companies, including Lifepoint Health, have failed to fulfill at least seven promises, including legally binding ones made to Ottumwa, including those related to growth, physician recruitment, routine capital expenditures, charity care, patient satisfaction and continuation of services.

Patient volumes have decreased, likely due to long wait times in the ER, outgoing transfers, insufficient staffing and a lack of specialists, the report said. This has also resulted from having a poor reputation in the community.

Because of financial harm, OTHC is dependent on Lifepoint Health to pay its expenses.

However, Lifepoint pays Apollo $9.2 million annually in management fees, as well as a 1% transaction fee each time Lifepoint completes an acquisition, which included a $55 million fee in relation to the acquisition of Lifepoint Health in 2018.

THE LARGER TREND

PE and other private funds had less than $1 trillion in managed assets in 2004, but now manage more than $13 trillion globally. PE firms create affiliated funds with money raised from investors, such as pension funds, foundations and insurance companies. The intention is generating returns for their investors within a short period of time.

PE has grown in healthcare. In the 2010s investors spent more than $1 trillion. By 2021 PE investment had reached an all-time high of 515 deals valued at $151 billion.

ON THE RECORD

“Recent peer reviewed studies have generally found negative consequences for general acute care hospitals during the first three years of PE ownership as compared to non-PE owned hospitals, including lower quality of care, increased transfers to other hospitals, decreased staffing and higher prices,” the report said.

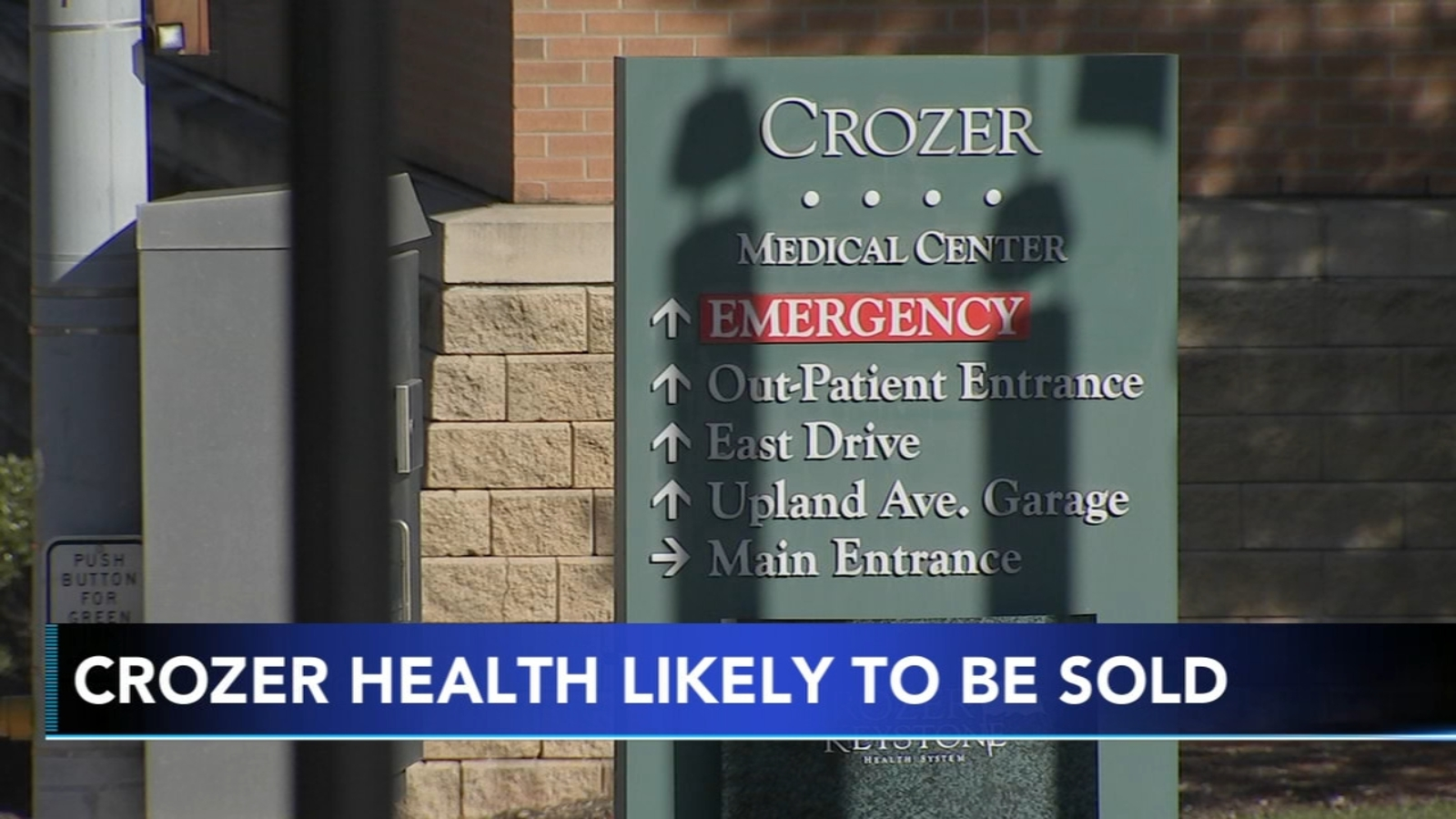

Pennsylvania state Sen. Tim Kearney has raised concerns about the lack of transparency and details around the planned sale of Upland, Pa.-based Crozer Health and has called on the state attorney general to step in and conduct a thorough analysis of the deal, the Daily Times reported Aug. 22.

Earlier this month, Los Angeles-based Prospect Medical Holdings and CHA Partners signed a letter of intent for CHA to acquire Crozer. The proposed deal would involve transitioning Crozer’s four hospitals back to nonprofit status.

“Prospect’s proposed sale of Crozer to CHA Partners LLC exemplifies the need for state oversight of hospital sales, as both entities appear to have histories of burning public partners despite demanding hefty subsidies,” Mr. Kearney said in a statement shared with Becker’s.

Unlike many other states, Pennsylvania’s Attorney General lacks statutory authority to deeply evaluate these deals, according to Mr. Kearney.

“While the AG’s legal settlement with Prospect gives them some oversight of this deal, the legislature needs to provide the AG with greater authority to protect hospitals and the communities that depend on them,” he said. “If the choice is CHA or closure, then we need some assurances that they will be a responsible organization and not just a profiteering speculator.”

Prospect, a for-profit company, plans to sell nine of its 16 hospitals in Pennsylvania, Rhode Island and Connecticut and is also being investigated by the Justice Department for alleged violations of the False Claims Act. A spokesperson for Prospect told Becker’s the system will continue to cooperate with the investigation, but feels that the allegations have no merit.

CHA did not respond to Becker’s request for comment.

Here are 67 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating is based on the Altamonte Springs, Fla.-based system’s competitive market position—especially in its core Florida markets—and its financial profile, Fitch said.

Advocate Health members Advocate Aurora Health and Atrium Health have “Aa3” ratings and positive outlooks with Moody’s. The ratings are supported by the Charlotte, N.C.-based system’s significant scale, strong market share across several major metro areas, and good financial performance and liquidity, Moody’s said.

AnMed Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Anderson, S.C.-based system’s strong and stable operating performance and leading market position in a sound service area, Fitch said.

Ann & Robert H. Lurie Children’s Hospital of Chicago has an “AA” rating and stable outlook with Fitch. The rating is supported by the system’s strong balance sheet with low leverage ratios derived from modest debt, Fitch said.

Atlantic Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Morristown, N.J.-based system’s fundamental strengths, including strong operating performance with high single digit operating cash flow margins and favorable liquidity of over 300 days cash on hand, Moody’s said.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

BayCare Health System has an “AA” rating and stable outlook with Fitch. The Clearwater, Fla.-based system on June 30 moved to a new corporate legal structure, replacing a joint operating agreement between multiple hospitals that were responsible for the creation of BayCare in 1997. Fitch views the dissolution of the JOA and the move to the new structure as a credit positive.

Beacon Health System has an “AA-” rating and stable outlook with Fitch. Fitch said the rating reflects the strength of the South Bend, Ind.-based system’s balance sheet.

Bon Secours Mercy Health has an “AA-” rating and stable outlook with Fitch. The Cincinnati-based system has a favorable and stable payor mix, leading or secondary market share position in nine of its 11 U.S. markets with improving market share positions in eight, and adequate cash flows to support the system’s strategic plans, Fitch said.

BJC Health System has an “Aa2” rating and stable outlook with Moody’s. The St. Louis-based system reflects its reputation as a leading academic medical center with a long-standing affiliation with Washington University School of Medicine, Moody’s said.

Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area and Fitch’s expectation that the system will sustain its strong capital-related ratios in the context of the system’s midrange revenue defensibility and strong operating risk profile assessments.

Carilion Clinic has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Roanoke, Va.-based system’s scale, regional significance as a tertiary referral system with broad geographic capture, and a highly integrated physician base with a well-defined culture, Moody’s said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals, and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence, and pediatric trauma status, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The rating reflects the Minneapolis-based system’s strong balance sheet, robust liquidity position, and dominant pediatric market position, Fitch said.

Cincinnati Children’s Hospital Medical Center has an “Aa2” rating and stable outlook with Moody’s. The rating is supported by its national and international reputation in clinical services and research, Moody’s said.

Cleveland Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the system’s strength as an international brand in highly complex clinical care and research and centralized governance model, the ratings agency said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth, Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

Corewell Health has an “Aa3” rating and stable outlook with Fitch. The rating reflects the Grand Rapids and Southfield, Mich.-based system’s significant scale as a provider and payer in Michigan, Moody’s said. The organization also has good and stable financial performance and liquidity.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

Froedtert ThedaCare Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s solid market position, track record of strong utilization and operations, and strong financial profile, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by its strong operating risk assessment, leading market position in its immediate service area, and strong financial profile, Fitch said.

Holland (Mich.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects Holland Hospital’s stable and strong liquidity and capital-related metrics despite sector-wide operating pressures, Fitch said.

Indiana University Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Indianapolis-based health system’s sustained track record of strong operating margins, ratings agency said.

Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The Falls Church, Va.-based system’s rating is anchored by its role as one of the largest health systems in Virginia with a leading market position in a rapidly growing region with unusually high commercial business, Moody’s said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Mullica Hill, N.J.-based system will return to strong operating cash flows following the operating challenges of 2022 and 2023, as well as the successful integration of Inspira Medical Center of Mannington (formerly Salem Medical Center).

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Kaiser Permanente has an “AA-” rating and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by its strong financial profile, bolstered by a large and diversified revenue base, Fitch said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Rochester, Minn.-based system’s preeminent reputation for clinical care and research, including new discoveries and cutting-edge treatment, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

McLeod Health has an “AA-” rating and stable outlook with Fitch. The Florence, S.C.-based system maintains a leading and growing market position in its primary service area and is expanding the Carolina’s Forest campus in an area that is expected to experience rapid growth over the coming years, Fitch said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Memorial Healthcare System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects that the Hollywood, Fla.-based system will continue to benefit from good strategic positioning of its large, diversified geographic footprint.

Memorial Hermann Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Houston-based system’s leading and expanding market position and strong demand in a growing region, Moody’s said.

Methodist Health System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects the Dallas-based system’s consistently strong operating performance, excellent liquidity, and very good market position.

Monument Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Rapid City, S.D.-based system has a dominant inpatient market position as the leading acute care provider in its geographically broad primary service area

Nationwide Children’s Hospital has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Columbus, Ohio-based system’s strong market position in pediatric services, growing statewide and national reputation, and continued expansion strategies.

Nicklaus Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Miami-based system’s position as the “premier pediatric hospital in South Florida with a leading and growing market share,” Fitch said.

North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The rating reflects the Tupelo-based system’s strong cash position and strong market position with a leading market share in its primary services area, Fitch said.

Northwestern Memorial HealthCare has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Chicago-based system’s growing market position, single operating model and financial discipline, Moody’s said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research, and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Parkland Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Dallas-based system will remain the leading provider of public (safety net) services in the vast Dallas County service area, supported by its tax levy.

Phoenix Children’s has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong cash flow generation that has significantly improved its balance sheet in recent years, Fitch said.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rady Children’s Hospital has an “Aa3” rating and stable outlook with Moody’s. The San Diego-based system’s rating reflects its well-established strengths, including an “extremely high” market share in all of San Diego County, Moody’s said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing position in a stable service area with good population growth and demand for acute care services, Fitch said.

Sarasota (Fla.) Memorial Health Care System has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s leading market position in a growing service area, robust historical operating cash flow levels and strong liquidity position, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

St. Elizabeth Medical Center has an “AA” rating and stable outlook with Fitch. The rating reflects the Edgewood, Ky.-based system’s strong liquidity, leading market position, and strong financial management, Fitch said.

St. Tammany Parish Hospital has an “AA-” rating and stable outlook with Fitch. The Covington, La.-based system has a strong operating risk assessment and very strong financial profile supported by consistently robust operating cash flows, Fitch said.

Stanford Health Care has an “Aa3” rating and positive outlook with Moody’s. The rating reflects the Palo Alto, Calif.-based system’s clinical prominence, patient demand, and its location in an affluent and well-insured market, Moody’s said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong financial profile in the context of its broad and growing reach for high-acuity services, Fitch said.

University Health has an “AA+” rating and stable outlook with Fitch. The San Antonio-based system’s outlook is based on the Bexar County Hospital District’s significant tax margin, good cost management, and strong leverage position relative to its liquidity and outstanding debt.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

University of Kansas Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects Kansas City-based system’s flagship hospital’s important presence as the only academic medical center in Kansas and a major provider of many high end and unique services to a large geographic area, Fitch said.

UW Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Madison, Wis.-based system’s strong clinical reputation, high acuity services, and important role as the academic medical center affiliated with the state’s flagship public university, Moody’s said.

VCU Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Richmond, Va.-based system’s status as one of Virginia’s leading academic medical centers and essential role as its largest safety net provider, supporting excellent patient demand at high acuity levels, Moody’s said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

Here are 48 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating is based on the Altamonte Springs, Fla.-based system’s competitive market position—especially in its core Florida markets—and its financial profile, Fitch said.

Advocate Health members Advocate Aurora Health and Atrium Health have “Aa3” ratings and positive outlooks with Moody’s. The ratings are supported by the Charlotte, N.C.-based system’s significant scale, strong market share across several major metro areas, and good financial performance and liquidity, Moody’s said.

Ann & Robert H. Lurie Children’s Hospital of Chicago has an “AA” rating and stable outlook with Fitch. The rating is supported by the system’s strong balance sheet with low leverage ratios derived from modest debt, Fitch said.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

Beacon Health System has an “AA-” rating and stable outlook with Fitch. Fitch said the rating reflects the strength of the South Bend, Ind.-based system’s balance sheet.

Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area and Fitch’s expectation that the system will sustain its strong capital-related ratios in the context of the system’s midrange revenue defensibility and strong operating risk profile assessments.

Carilion Clinic has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Roanoke, Va.-based system’s scale, regional significance as a tertiary referral system with broad geographic capture, and a highly integrated physician base with a well-defined culture, Moody’s said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals, and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence, and pediatric trauma status, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The rating reflects the Minneapolis-based system’s strong balance sheet, robust liquidity position, and dominant pediatric market position, Fitch said.

Cincinnati Children’s Hospital Medical Center has an “Aa2” rating and stable outlook with Moody’s. The rating is supported by its national and international reputation in clinical services and research, Moody’s said.

Cleveland Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the system’s strength as an international brand in highly complex clinical care and research and centralized governance model, the ratings agency said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth, Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

Froedtert ThedaCare Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s solid market position, track record of strong utilization and operations, and strong financial profile, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by its strong operating risk assessment, leading market position in its immediate service area, and strong financial profile, Fitch said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Mullica Hill, N.J.-based system will return to strong operating cash flows following the operating challenges of 2022 and 2023, as well as the successful integration of Inspira Medical Center of Mannington (formerly Salem Medical Center).

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Rochester, Minn.-based system’s preeminent reputation for clinical care and research, including new discoveries and cutting-edge treatment, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Memorial Healthcare System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects that the Hollywood, Fla.-based system will continue to benefit from good strategic positioning of its large, diversified geographic footprint.

Memorial Hermann Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Houston-based system’s leading and expanding market position and strong demand in a growing region, Moody’s said.

Methodist Health System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects the Dallas-based system’s consistently strong operating performance, excellent liquidity, and very good market position.

Nationwide Children’s Hospital has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Columbus, Ohio-based system’s strong market position in pediatric services, growing statewide and national reputation, and continued expansion strategies.

Nicklaus Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Miami-based system’s position as the “premier pediatric hospital in South Florida with a leading and growing market share,” Fitch said.

North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The rating reflects the Tupelo-based system’s strong cash position and strong market position with a leading market share in its primary services area, Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research, and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Parkland Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Dallas-based system will remain the leading provider of public (safety net) services in the vast Dallas County service area, supported by its tax levy.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing position in a stable service area with good population growth and demand for acute care services, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

St. Elizabeth Medical Center has an “AA” rating and stable outlook with Fitch. The rating reflects the Edgewood, Ky.-based system’s strong liquidity, leading market position, and strong financial management, Fitch said.

Stanford Health Care has an “Aa3” rating and positive outlook with Moody’s. The rating reflects the Palo Alto, Calif.-based system’s clinical prominence, patient demand, and its location in an affluent and well-insured market, Moody’s said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong financial profile in the context of its broad and growing reach for high-acuity services, Fitch said.

University Health has an “AA+” rating and stable outlook with Fitch. The San Antonio-based system’s outlook is based on the Bexar County Hospital District’s significant tax margin, good cost management, and strong leverage position relative to its liquidity and outstanding debt.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

VCU Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Richmond, Va.-based system’s status as one of Virginia’s leading academic medical centers and essential role as its largest safety net provider, supporting excellent patient demand at high acuity levels, Moody’s said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

Portland-based Oregon Health & Science University told staff June 6 that it plans to lay off at least 500 employees, citing financial issues.

“Our expenses, including supplies and labor costs, continue to outpace increases in revenue,” top leaders told staff in a message shared with Becker’s. “Despite our efforts to increase our revenue, our financial position requires difficult choices about internal structures, workforce and programs to ensure that we achieve our state-mandated missions and thrive over the long term.”

Willamette Week was first to report the news, which follows Oregon Health & Science University and Portland-based Legacy Health signing a binding, definitive agreement to come together as one health system under OHSU Health. OHSU Health would comprise 12 hospitals and, more than 32,000 employees and will be one of the largest providers of services to Medicaid members in Oregon.

An Oregon Health & Science University spokesperson told Becker’s more information about the layoffs will be provided in the coming weeks.

In the June 6 message, leaders told staff that “while we work to address short-term financial challenges, we must also plan for an impactful and successful future. We understand that last week’s announcement regarding the Legacy Health definitive agreement, while exciting and potentially transformational, raises questions about how we can afford the required investment in light of our financial situation.”

They added that a capital investment in Legacy “represents a strategic expansion designed to enhance our capacity,” and will be funded by borrowing with 30-year bonds.

“These capital dollars cannot be used to close gaps in our fiscal year 2025 OHSU budget or to pay our members. The OHSU Strategic Alignment and budgetary work would be necessary with or without the Legacy Health integration,” leaders said.

OHSU has planned a town hall next week to further discuss the combination with Legacy.

Leaders said discussions between managers and members about workforce reductions will begin after the annual review and contract renewal process, with additional reductions occurring over the next few months.

Other senior executives also cashed out as the company faced a $1.6 billion threat that wreaked havoc throughout the health care system.

On February 21, the same day that a ransomware attack began to wreak havoc throughout UnitedHealth Group and the U.S. health care system, five of UnitedHealth’s C-suite executives, including CEO Andrew Witty and the company’s chief legal officer, sold $17.7 million worth of their stock in the company. Witty alone accounted for $5.6 million of those sales.

The company’s stock has not recovered since the ransomware attack and has underperformed the S&P 500 index of major stocks by 8% during that time. In the two weeks following the ransomware attack, the company’s stock slid by 10.4%, wiping out more than $46 billion in market cap and greatly reducing the value of shares held by non-insiders. The slide continued for several weeks. On the day Witty and the other executives sold their shares, the stock price closed at $521.97. By April 12, it had fallen to $439.20.

“He (Witty) sold the shares on the same day that he learned of the ransomware attack,” said Richard Painter, a professor at the University of Minnesota School of Law who is also the vice chair of Citizens for Responsibility and Ethics in Washington. “That’s not good. For the SEC to prove a civil case of insider trading they just have to prove that it’s more probable than not that executives acted on inside information. CEOs have got to be a heck of a lot more careful.

You’re the CEO of a company, you should not be buying or selling the stock right in the middle of a material event like a ransomware attack. You’re asking for trouble. You’re going to end up with an SEC investigation. If that goes badly you could end up with a DOJ investigation.”

How much UnitedHealth’s C-suite executives sold in company stock on February 21, 2024:

Brian Thompson, the CEO of UHG’s insurance arm, sold $1.5 million on the same day. John Rex, then the CFO and now the CFO and president, sold $4.4 million, as did Dirk McMahon, now the former president. Chief Legal Officer Rupert Bondy, who would likely have to have signed off on the sales, sold $750,000.

HEALTH CARE un-covered is the first media outlet to report these disclosures.

The ransomware attack was caused at least in part by negligence on UnitedHealth’s part, Witty admitted at the Finance Committee hearing. He acknowledged that the company had failed to use multi-factor authentication — requiring more than just a password to access information — to secure its data. The cyberattack exposed the personal health information of as much as a third of Americans’ health information.

“This incident and the harm that it caused was, like so many other security breaches, completely preventable and the direct result of corporate negligence,”

Sen. Ron Wyden (D-Ore.) wrote to federal regulators on May 30. “UHG has publicly confirmed that the hackers gained their initial foothold by logging into a remote access server that was not protected with multi-factor authentication (MFA). MFA is an industry-standard cyber defense that protects against hackers who have guessed or stolen a valid username and password for a system.”

UnitedHealth exploited the crisis created by its own negligence to further entrench its position as the largest employer of doctors in the country,acquiring medical practices that were unable to pay their bills due at least in part to the chaos created by the ransomware attack. The American Medical Association is considering legal action against the company for the attack, with a proposal for its House of Delegates conference beginning June 8 stating that “Optum is the largest employer of physicians and has acquired practices when the ransomware disruption made those practices unable to survive without acquisition… Even the practices that survive will have ongoing damages including but not limited to denials related to giving therapy when it was impossible to obtain prior authorization, from using lines of credit and having to pay interest, from having billing departments and others work overtime to submit claims, to losing key employees from inability to make payroll.”

Other well-timed insider stock transactions

In April, Bloomberg reported that in the lead up to the disclosure of an FTC investigation into UnitedHealth’s monopolistic practices, other UnitedHealth insiders, including Chairman Stephen Hemsley, had sold $102 million worth of their shares.

News of that investigation and the stock sales led Sen. Elizabeth Warren (D-Mass.) and other lawmakers to call for an SEC investigation into the trading.

The disclosures revealed here, however, are potentially more incriminating: the executives sold the stock the same day the company became aware of the devastating ransomware attack. When Witty was supposed to be all hands on deck strategizing how to protect health care providers and millions of patients, he spent at least part of his day taking action to preserve his net worth.

EDITOR’S NOTE:

This is not the first time UnitedHealth executives have engaged in questionable or illegal stock transactions. In 2007, former CEO William McGuire agreed to a record $468 million settlement with the SEC after it was learned that for more than a decade he had engaged in a scheme to inflate the value of his holdings in the company and, consequently, his net worth.

An SEC investigation that year found that over a 12-year period, “McGuire repeatedly caused the company to grant undisclosed, in-the-money stock options to himself and other UnitedHealth officers and employees without recording in the company’s books and disclosing to shareholders material amounts of compensation expenses as required by applicable accounting rules.” In other words, he was back-dating his stock options.

As the SEC explained:

[F]rom at least 1994 through 2005, McGuire looked back over a window of time and picked grant dates for UnitedHealth options that coincided with dates of historically low quarterly closing prices for the company’s common stock, resulting in grants of in-the-money options.

According to the complaint, McGuire signed and approved backdated documents falsely indicating that the options had actually been granted on these earlier dates when UnitedHealth’s stock price was at or near these low points.

These inaccurate documents caused the company to understate compensation expenses for stock options, and were routinely provided to the company’s external auditors in connection with their audits and reviews of UnitedHealth’s financial statements.

Here are 37 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating is based on the Altamonte Springs, Fla.-based system’s competitive market position — especially in its core Florida markets — and its financial profile, Fitch said.

Advocate Health members Advocate Aurora Health and Atrium Health have “Aa3” ratings and positive outlooks with Moody’s. The ratings are supported by the Charlotte, N.C-based system’s significant scale, strong market share across several major metro areas and good financial performance and liquidity, Moody’s said.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

Carilion Clinic has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Roanoke, Va.-based system’s scale, regional significance as a tertiary referral system with broad geographic capture, and a highly integrated physician base with a well-defined culture, Moody’s said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence and pediatric trauma status, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The rating reflects the Minneapolis-based system’s strong balance sheet, robust liquidity position and dominant pediatric market position, Fitch said.

Cincinnati Children’s Hospital Medical Center has an “Aa2” rating and stable outlook with Moody’s. The rating is supported by its national and international reputation in clinical services and research, Moody’s said.

Cleveland Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the system’s strength as an international brand in highly complex clinical care and research and centralized governance model, the ratings agency said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by its strong operating risk assessment, leading market position in its immediate service area and strong financial profile,” Fitch said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Mullica Hill, N.J.-based system will return to strong operating cash flows following the operating challenges of 2022 and 2023, as well as the successful integration of Inspira Medical Center of Mannington (formerly Salem Medical Center).

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Memorial Hermann Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Houston-based system’s leading and expanding market position and strong demand in a growing region, Moody’s said.

Nationwide Children’s Hospital has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Columbus, Ohio-based system’s strong market position in pediatric services, growing statewide and national reputation and continued expansion strategies.

Nicklaus Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Miami-based system’s position as the “premier pediatric hospital in South Florida with a leading and growing market share,” Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an”AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing positive in a stable service area with good population growth and demand for acute care services, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

St. Elizabeth Medical Center has an “AA” rating and stable outlook with Fitch. The rating reflects the Edgewood, Ky.-based system’s strong liquidity, leading market position and strong financial management, Fitch said.

Stanford Health Care has an “Aa3” rating and positive outlook with Moody’s. The rating reflects the Palo Alto, Calif.-based system’s clinical prominence, patient demand and its location in an affluent and well insured market, Moody’s said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong financial profile in the context of its broad and growing reach for high-acuity services, Fitch said.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

Steward Health Care’s Chapter 11 bankruptcy filing onMay 6, 2024, brought back bad memories of another large health system bankruptcy.

On July 21, 1998, Pittsburgh-based Allegheny Health and Education Research Foundation (AHERF) filed Chapter 11. AHERF grew very rapidly, acquiring hospitals, physicians, and medical schools in its vigorous pursuit of scale across Pennsylvania. Utilizing debt capacity and spending cash, AHERF quickly ran out of both, defaulted on its obligations, and then filed for bankruptcy. It was one of the largest bankruptcy filings in municipal finance and the largest in the rated not-for-profit hospital universe.

Steward Health Care is a for-profit, physician-owned hospital company, but its long-standing roots were in faith-based not-for-profit healthcare. Prior to the acquisition by Cerberus Capital Management in 2010, Caritas Christi Health Care System was comprised of six hospitals in eastern Massachusetts. Caritas was a well-regarded health system, providing a community alternative to the academic medical centers in downtown Boston. Over the next 14 years, Steward grew rapidly to 31 hospitals in eight states, most recently bolstered through an expansive sale-leaseback structure with a REIT. Per the bankruptcy filings, the company reported $9 billion in secured debt and leases on $6 billion of revenue.

Chapter 11 bankruptcy filings in corporate America are a means to efficiently sell assets or a path to re-emergence as a new streamlined company. A quick glance at Steward’s organizational structure shows a dizzying checkerboard of companies and LLCs that will require a massive untangling. Further, its capital structure includes both secured debt for operations and a separate and distinct lease structure for its facilities, and in bankruptcy, that signals significant complexity. Bankruptcy filings in not-for-profit healthcare are less common, although it is surprising that the industry did not see an increase after the pandemic. Not-for-profit hospitals that are in distress seem to hang on long enough to find a buyer, gain increased state funding, attain accommodations on obligations, or find some other escape route to avoid a payment default or filing.

Details regarding Steward’s undoing will unfold in the coming weeks as it moves through an auction process. But there are some early takeaways the not-for-profit industry can learn from this:

Remain essential in your local market. Hospitals must prove their value to their constituents, including managed care payers, especially in competitive urban markets, as Steward may have learned in eastern Massachusetts and Miami. Prior strategies of making a margin as an out-of-network provider are no longer viable as patients must shoulder more of the financial burden. Simply put, your organization should be asking one question: does a managed care plan need our existing network to sell a product in our market? If the answer is no, you need to develop strategies that make your hospital essential.

Embrace financial planning for long-term viability. Without it, a hospital or health system will be unable to afford the capital spending it needs to maintain attractive, patient-friendly, state-of-the art facilities or absorb long-term debt to fund the capital. Annual financial planning is more than just a trendline going forward. The scenarios and inputs must be well-founded, well-grounded in detail, and based on conservative assumptions. Increasing attention has to be paid to disrupters, innovators, specialized/segmented offerings, and expansion plans of existing and new competitors. Investors expect this from not-for-profit borrowers. Higher-performing hospitals and health systems of all sizes do this well.

Build capital capacity through improved cash flow. It is undoubtedly clear that Steward, like AHERF, was unable to afford the capital and debt they thought they could, either through flawed financial planning of its future state or, more concerning, the complete absence of it. Or they believed that rapid growth would solve all problems, not detailed financial planning, the use of benchmarks, or a sharp focus on operations. Increasing that capacity through sustained financial performance will allow an organization to de-leverage and build capital capacity.

When the case studies are written about Steward, a fact pattern will be revealed that includes the inability or unwillingness to attain synergies as a system, underspending on facility capital needs given a severe liquidity crunch, labor challenges, and a rapid payer mix shift.

Underlying all of this will undoubtedly be a failure of governance and leadership as we saw with AHERF. It will also likely indicate that one of the most precious assets healthcare providers may have is the management bandwidth to ensure strategic plans are appropriately made, tested, monitored, and executed.

While Steward and AHERF may be held up as extreme cases, not-for-profit hospital governance must continue to focus on checks-and-balances of management resources. Likewise, management must utilize benchmarks, data, and strong financial planning, given the challenges the industry faces.