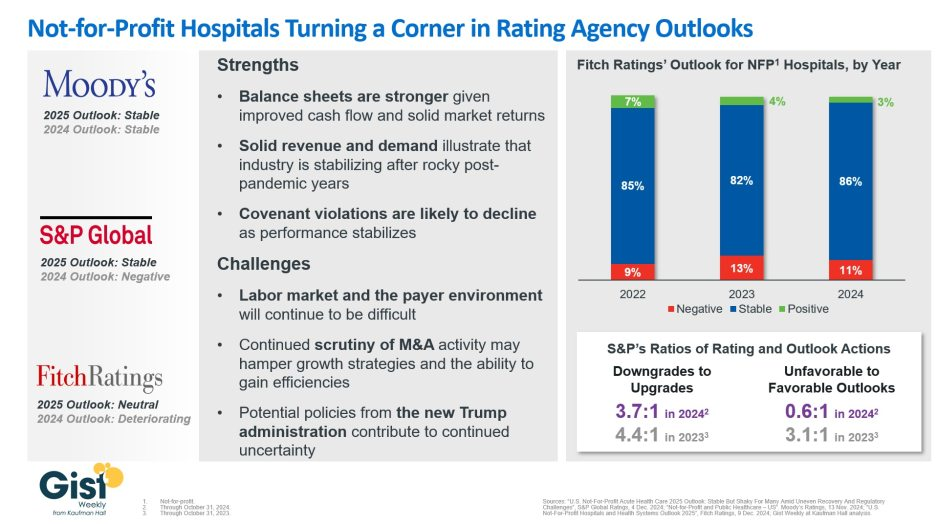

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

Here are 23 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence and pediatric trauma status, Fitch said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an”AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing positive in a stable service area with good population growth and demand for acute care services, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

Pittsburgh-based UPMC reported a $198 million operating loss (-0.7% margin) in 2023, down from a $162 million gain (0.6% margin) in 2022, according to financial documents published Feb. 28.

UPMC attributed the swing from operating income to loss to various factors, including increased labor and supply costs, increases in medical claims expense due to higher utilization and certain legal settlements.

Revenue for the health system increased 8.5% year over year to $27.7 billion and expenses rose 10% to $27.9 billion. Under expenses, labor costs increased 6.4% to $9.7 billion and supply costs were up 11% to $7.4 billion.

After accounting for nonoperating items, such as investment returns, UPMC ended 2023 with a $31 million net loss, compared to a $1 billion net loss the previous year.

As of Dec. 31, UPMC had more than $9.5 billion in cash and investments, $3.2 billion of which was held by its regulated health and captive insurance companies.

Here are 68 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings, Moody’s Investors Service and S&P Global in 2023.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating reflects the Altamonte Springs, Fla.-based system’s strong financial profile, characterized by still-adequate liquidity and moderate leverage, typically strong and highly predictable profitability, Fitch said.

Advocate Aurora Health has an “AA” rating and stable outlook with Fitch. The Downers Grove, Ill.- and Milwaukee-based system’s rating reflects a very strong financial profile in the context of an already sound market position and geographic reach that was enhanced after merging with Charlotte, N.C.-based Atrium Health, Fitch said.

AnMed Health has an “AA-” rating and stable outlook with Fitch. The Anderson, S.C.-based system has maintained strong performance through the COVID-19 pandemic and current labor market pressures, Fitch said.

AtlantiCare has an “AA-” rating and stable outlook with Fitch. The Atlantic City, N.J.-based system has a strong balance sheet with solid liquidity position and low debt burden, Fitch said.

Atrium Health has an “AA-” rating and stable outlook with S&P Global. The Charlotte, N.C.-based system’s rating reflects a robust financial profile, growing geographic diversity and expectations that management will continue to deploy capital with discipline.

Banner Health has an “AA-” and stable outlook with Fitch. The Phoenix-based system’s rating highlights the strength of its core hospital delivery system and growth of its insurance division, Fitch said.

BayCare Health System has an “AA” rating and stable outlook with Fitch. The Tampa, Fla.-based system’s rating reflects its excellent financial profile supported by its leading market position in a four-county area and the ability to sustain a solid operating outlook in the face of inflationary sector headwinds, Fitch said.

Bayhealth has an “AA” rating and stable outlook with Fitch. The rating reflects the strength of the Dover, Del.-based system’s market positions and the stability of its financial profile, Fitch said.

Beacon Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of the South Bend, Ind.-based system’s balance sheet, the rating agency said.

Berkshire Health has an “AA-” rating and stable outlook with Fitch. The Pittsfield, Mass.-based system has a strong financial profile, solid liquidity and modest leverage, according to Fitch.

Bryan Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Lincoln, Neb., system’s leading and growing market position as a regional referral center with strong expense flexibility and cash flow, Fitch said.

Cape Cod Healthcare has an “AA-” and stable outlook with Fitch. The Hyannis, Mass.-based system’s rating reflects a dominant market position in its service area and historically solid operating results, the rating agency said.

Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area, Fitch said.

CaroMont Health has an “AA-” rating and stable outlook with S&P Global. The Gastonia, N.C.-based system has a healthy financial profile and robust market share in a competitive region.

CentraCare has an “AA-” rating and stable outlook with Fitch. The St. Cloud, Minn.-based system has a leading market position, and its management’s focus on addressing workforce pressures, patient access and capacity constraints will improve operating margins over the medium term, Fitch said.

Children’s Health System of Texas has an “AA” and stable outlook with Fitch. The Dallas-based system’s rating reflects its solid operating performance in 2022, resulting from inpatient, outpatient and surgical volume growth, as well as one-time support from pandemic-era stimulus funding, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The Minneapolis-based system’s broad reach within the region continues to support long-term sustainability as a market leader and preferred provider for children’s health care, Fitch said.

Concord (N.H.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of Concord’s leverage and liquidity assessment and Fitch’s assessment that two recently acquired hospitals will be strategically and financially accretive.

Cone Health has an “AA” rating and stable outlook with Fitch. The rating reflects the expectation that the Greensboro, N.C.-based system will gradually return to stronger results in the medium term, the rating agency said.

Cottage Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Santa Barbara, Calif.-based system’s leading market position and broad reach in a service area that exhibits modest population growth but consistently high demand for acute care services, Fitch said.

Deaconess Health System has an “AA” rating and stable outlook with Fitch. The Evansville, Ind.-based system demonstrated operating cost flexibility through the pandemic and recent labor and inflationary pressure, Fitch said.

Duke University Health System has an “AA-” rating and stable outlook with Fitch. Fitch projects the Durham, N.C.-based system will benefit from the integration of the former Private Diagnostic Clinic and from North Carolina’s recently enacted Medicaid expansion and Healthcare Access and Stabilization Program.

El Camino Health has an “AA-” rating and stable outlook with Fitch. The Mountain View, Calif.-based system has a history of generating double-digit operating EBITDA margins, driven by a solid market position that features strong demographics and a very healthy payer mix, Fitch said.

Franciscan Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Mishawaka, Ind.-based system’s strong and stable balance sheet, favorable payer mix, and leading or near leading market share in its service areas, Fitch said.

Froedtert Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s maintenance of a strong, albeit compressed, operating performance and a robust liquidity position, Fitch said.

Geisinger has an “AA-” credit rating and stable outlook with S&P. The Danville, Pa.-based system enjoys strong integration and value-based care experience, the ratings agency said.

Hackensack Meridian Health has an “AA-” rating and stable outlook with Fitch. The Edison, N.J.-based system’s rating is supported by its strong presence in its large and demographically favorable market, Fitch said.

Harris Health System has an “AA” rating and stable outlook with Fitch. The Houston-based system has a “very strong” revenue defensibility, primarily based on the district’s significant taxing margin that provides support for operations and debt service, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by a leading market position in its immediate area and very strong financial profile, Fitch said.

Intermountain Health has an “Aa1” rating and stable outlook with Moody’s. The Salt Lake City-based system’s rating is reflected by its distinctly leading market position in Utah and strong absolute and relative cash levels, Moody’s said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The Mullica Hill, N.J.-based system’s rating reflects its leading market position in a stable service area and a large medical staff supported by a growing residency program, Fitch said.

IU Health has an “AA” rating and stable outlook with Fitch. The Indianapolis-based system has a long track record of strong operating margins and an overall credit profile that is supported by a strong balance sheet, the rating agency said.

Lucile Packard Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the Palo Alto, Calif.-based hospital’s role as a nationally known, leading children’s hospital, Fitch said. It also benefits from resilient clinical volumes and a solid market position, as well as its relationship with Stanford University and Stanford Health Care.

Kaiser Permanente has an “AA-” and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by a strong financial profile, which is maintained despite a challenging operating environment in fiscal year 2022.

Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The Rochester, Minn.-based system’s credit profile characterized by its excellent reputations for clinical services, research and education, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The Grand Blanc, Mich.-based system has a leading market position over a broad service area covering much of Michigan and a track-record of profitability despite sector-wide market challenges in recent years, Fitch said.

McLeod Regional Medical Center has an “AA-” rating and stable outlook with Fitch. The rating reflects the Florence, S.C.-based system’s very strong financial profile assessment, historically strong operating EBITDA margins and its solid market position, Fitch said.

MemorialCare has an “AA-” rating and stable outlook with Fitch. The rating reflects the Fountain Valley, Calif.-based system’s strong financial profile and excellent leverage metrics despite its weaker operating performance, Fitch said.

Memorial Sloan-Kettering Cancer Center has an “AA” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the New York City-based system’s national and international reputation as a premier cancer hospital will continue to support growth in its leading and increasing market share for its specialty services.

Midland (Texas) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Midland’s exceptional market position and limited competition for acute-care services and growing outpatient services, Fitch said.

Monument Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Rapid City, S.D.-based system’s dominant inpatient market share and excellent market position across its geographically broad service area, Fitch said.

Munson Healthcare has an “AA” rating and stable outlook with Fitch. The rating reflects the strength of the Traverse City, Mich.-based system’s market position and its leverage and liquidity profiles.

MyMichigan Health has an “AA-” rating and stable outlook with Fitch. The Midland-based system reflects the system’s market position as the largest provider of acute care services and its leading market position in a sizable geographic area covering 25 counties in mid and northern Michigan, the rating agency said.

North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The Tupelo-based system’s rating reflects its very strong cash position and strong market position, Fitch said.

NewYork-Presbyterian Hospital has an “AA” rating and stable outlook with Fitch. The rating reflects the New York City-based system’s market position as one of New York’s major academic healthcare systems with a reputation that extends beyond the region, Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The Winston-Salem, N.C.-based system has a highly competitive market share in three separate North Carolina markets, Fitch said, including a leading position in Winston-Salem (46.8 percent) and second only to Atrium Health in the Charlotte area.

NYC Health + Hospitals has an “AA-” rating with Fitch. The New York City system is the largest municipal health system in the country, serving more than 1 million New Yorkers annually in more than 70 patient locations across the city, including 11 hospitals, and employs more than 43,000 people.

OhioHealth has an “AA+” rating and stable outlook with Fitch. The Columbus-based system has an exceptionally strong credit profile, very favorable leverage metrics and reliably strong profitability, Fitch said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The system’s upgrade from “A+” reflects the continued strength of the health system’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market, Fitch said.

Phoenix Children’s Hospital has an “AA-” and stable outlook with Fitch. The rating reflects its position as a distinct leading provider of pediatric health services in a growing primary service area, Fitch said.

The Queen’s Health System has an “AA” rating and stable outlook with Fitch. The Honolulu-based system’s rating reflects its leading state-wide market position, historically strong operating performance and diverse revenue streams, the rating agency said.

Rush System for Health has an “AA-” and stable outlook with Fitch. The Chicago-based system has a strong financial profile despite ongoing labor issues and inflationary pressures, Fitch said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The Cape Girardeau, Mo.-based system enjoys robust operational performance and a strong local market share as well as manageable capital plans, Fitch said.

Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The system has a “very strong” financial profile and a leading market share position, Fitch said.

Sanford Health has an “AA-” rating and stable outlook with Fitch. The Sioux Falls, S.D.-based system rating reflects its leading inpatient market share positions in multiple markets and strong overall financial profile, the rating agency said.

Stanford Health Care has an “AA” rating and stable outlook with Fitch. The Palo Alto, Calif.-based system’s rating is supported by its extensive clinical reach in the greater San Francisco and Central Valley regions and nationwide/worldwide destination position for extremely high-acuity services, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system has a strong financial profile, multi-state presence and scale, with solid revenue diversity, Fitch said.

St. Clair Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Pittsburgh-based system’s strong financial profile assessment, solid market position and historically strong operating performance, the rating agency said.

St. Tammany Parish Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the Covington, La.-based system’s strong operating risk assessment and very strong financial profile supported by consistently robust operating cash flows, Fitch said.

Texas Medical Center has an “AA-” rating and stable outlook with Fitch. The rating reflects the Houston-based system’s profitable service enterprise, its long and collaborative relationship with strong university, nonprofit and medical industry partners, and sizable financial reserve levels, Fitch said.

TriHealth has an “AA-” rating and stable outlook with Fitch. The Cincinnati-based system’s rating reflects its broad reach, high-acuity services and stable market position in a highly fragmented and competitive market, Fitch said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s broad and growing reach for high-acuity services and the considerable benefits it receives from its high degree of integration with the University of Chicago, Fitch said.

UCHealth has an “AA” rating and stable outlook with Fitch. The Aurora, Colo.-based system’s margins are expected to remain robust, and the operating risk assessment remains strong, Fitch said.

University of Kansas Health System has an “AA-” rating and stable outlook with S&P Global. The Kansas City-based system has a solid market presence, good financial profile and solid management team, though some balance sheet figures remain relatively weak to peers, the rating agency said.

Virtua Health has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Marlton, N.J.-based system’s leading market position in a stable service area and the successful integration of the Lourdes Health System, Fitch said.

VHC Health has an”AA-” rating and stable outlook with Fitch. The Arlington-based system has demonstrated strong operating cost flexibility, growth in high acuity service lines and an expanding outpatient footprint, Fitch said.

WellSpan Health has an “Aa3” rating and stable outlook with Moody’s. The York, Pa.-based system has a distinctly leading market position across several contiguous counties in central Pennsylvania, and management’s financial stewardship and savings initiatives will continue to support sound operating cash flow margins when compared to peers, Moody’s said.

Willis-Knighton Health System has an “AA-” rating and stable outlook with Fitch. The Shreveport, La.-based system has a “dominant inpatient market position” and is well positioned to manage operating pressures, Fitch said.

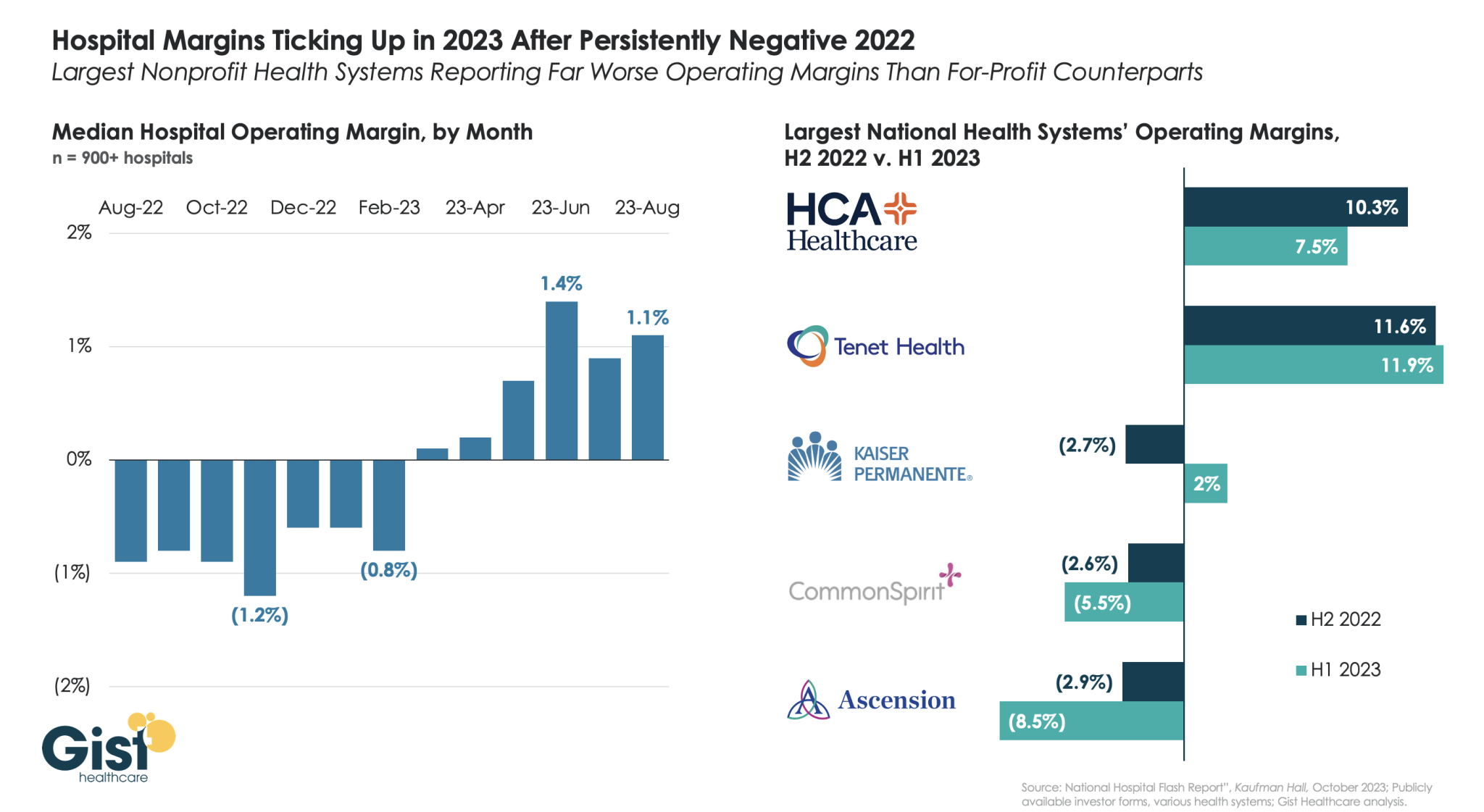

Using data from Kaufman Hall’s latest National Hospital Flash Report and publicly available investor reports for some of the nation’s largest health systems, the graphic below takes stock of the state of health system margins.

After the median hospital delivered negative operating margins for twelve-straight months, 2023 has made for a positive but slim year so far, with margins hovering around one percent. Amid this breakeven environment, fortunes have diverged between nonprofit and for-profit health systems.

The largest for-profit systems, HCA Healthcare and Tenet Healthcare, posted operating margins of around 10 percent between July 2022 and June 2023, while the three largest nonprofit systems, Kaiser Permanente, CommonSpirit Health, and Ascension, suffered net losses.

Although Kaiser Permanente’s margin bounced back in the first half of this year, CommonSpirit and Ascension’s margins continued to decline, more than doubling the operating losses of the prior six months.

One key to the recent success of the largest for-profit systems is their diversification away from inpatient care.

Case in point: almost half of Tenet’s profits in 2023 have come from its ambulatory division, driven by its United Surgical Partners International (USPI) ambulatory surgery center network, which has posted 40 percent margins over the past several quarters.

Kaiser Permanente built on 2023’s strong start with $2.08 billion of net income during the quarter ended June 30, bringing its midyear total to about $3.29 billion, the integrated system announced late Friday.

Operating income was also strong at $741 million (2.9% margin) and raised the organization’s six-month performance to $974 million (1.9% margin).

The numbers are both a sequential improvement and a stark turnaround from 2022. By the midpoint of that year, Kaiser Permanente was reporting a $1.3 billion net loss for the quarter and an $89 million operating gain (0.4% margin). Across 2022’s first half, the system had been down a total of $2.26 billion and added just $17 million from operations (0.0% margin).

The Oakland, California-based nonprofit is likely safe from repeating the nearly $4.5 billion net loss and $1.3 billion operating loss of full-year 2022.

Leadership, however, noted that the integrated system historically sees higher operating margins during the first half of the year “due in part to the annual enrollment cycle and seasonal care.”

“Our second-quarter financial results reflect operational improvements that, together with our ongoing expense reduction efforts, will help us face additional financial pressures in the second half of the year,” Kathy Lancaster, executive vice president and chief financial officer at Kaiser Permanente, said in a release. “The process of building our financial performance back to pre-pandemic levels requires that we continue to redesign our cost structure to support investments in our facilities, technology and people while staying competitive in a dynamic healthcare marketplace.”

Kaiser Permanente reported $25.17 billion in operating revenues for the second quarter, a 7.2% increase year over year. Operating expenses increased 4.5% year-over-year to $24.42 billion.

“Like all health systems, Kaiser Permanente is experiencing ongoing cost headwinds and volatility driven by inflation, labor shortages, and the lingering effects of the pandemic on access to care and service,” the system wrote in a release.

Kaiser Permanente’s membership has increased by more than 81,000 members since the start of the year and sits at almost 12.7 million as of June 30. The organization noted that it has kicked off an outreach campaign for Medicaid members “to ensure they have critical enrollment information as states go through the mandated process of eligibility redetermination.”

The largest impact on Kaiser Permanente’s bottom line came from investments. Owing to “favorable financial market conditions,” the organization recorded $1.34 billion in “other income and expense,” nearly a full reversal of the $1.39 billion loss on the same line item it’d logged during the same period last year.

The system’s capital spending reached $824 million for the quarter, which was up from $789 million during the second quarter of 2022 but a pullback from the first quarter of 2023’s $930 million.

“The post-pandemic financial pressures have led many in the industry to cut back on care and service,” CEO Greg Adams said in an accompanying statement. “At Kaiser Permanente, we remain focused on improving access and affordability for our patients, members and communities, which requires continued investment in care and coverage. … I want to thank all employees and physicians for turning the disruptions and challenges of the past three years into opportunities to make our healthcare system stronger and more equitable, with improved outcomes for all.”

Kaiser Permanente is the largest nonprofit health system in the country by revenue with more than $95 billion in annual revenues. As of June 30, it spanned 39 hospitals, 622 medical offices and 43 clinics in addition to its millions of covered health plan members.

Earlier in the year the system highlighted efforts to trim administrative and discretionary spending as well as a workforce push that improved clinical hiring by 15% year over year. It is in the midst of negotiating a new labor contract covering 85,000 unionized healthcare workers who are seeking workforce development investments and higher staffing levels across clinical settings.

The organization is also working toward its high-profile acquisition of fellow integrated nonprofit Geisinger Health, which Kaiser Permanente said would be the first step toward a cross-country value-based care organization called Risant Health.

Here are 45 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings, Moody’s Investors Service and S&P Global in 2023.

Note: This is not an exhaustive list. Health system names were compiled from credit rating reports.

1. AdventHealth has an “AA” rating and stable outlook with Fitch. The rating reflects the Altamonte Springs, Fla.-based system’s strong financial profile, characterized by still-adequate liquidity and moderate leverage, typically strong and highly predictable profitability, Fitch said.

2. AnMed Health has an “AA-” rating and stable outlook with Fitch. The Anderson, S.C.-based system has maintained strong performance through the COVID-19 pandemic and current labor market pressures, Fitch said.

3. Atrium Health has an “AA-” and stable outlook with S&P Global. The Charlotte, N.C.-based system’s rating reflects a robust financial profile, growing geographic diversity and expectations that management will continue to deploy capital with discipline.

4. Banner Health has an “AA-” and stable outlook with Fitch. The Phoenix-based system’s rating highlights the strength of its core hospital delivery system and growth of its insurance division, Fitch said.

5. BayCare Health System has an “AA” rating and stable outlook with Fitch. The Tampa, Fla.-based system’s rating reflects its excellent financial profile supported by its leading market position in a four-county area and the ability to sustain a solid operating outlook in the face of inflationary sector headwinds, Fitch said.

6. Beacon Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of the South Bend, Ind.-based system’s balance sheet, the rating agency said.

7. Berkshire Health has an “AA-” rating and stable outlook with Fitch. The Pittsfield, Mass.-based system has a strong financial profile, solid liquidity and modest leverage, according to Fitch.

8. Cape Cod Healthcare has an “AA-” and stable outlook with Fitch. The Hyannis, Mass.-based system’s rating reflects a dominant market position in its service area and historically solid operating results, the rating agency said.

9. Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area, Fitch said.

10.CaroMont Health has an “AA-” rating and stable outlook with S&P Global. The Gastonia, N.C.-based system has a healthy financial profile and robust market share in a competitive region.

11. CentraCare has an “AA-” rating and stable outlook with Fitch. The St. Cloud, Minn.-based system has a leading market position, and its management’s focus on addressing workforce pressures, patient access and capacity constraints will improve operating margins over the medium term, Fitch said.

12. Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The Minneapolis-based system’s broad reach within the region continues to support long-term sustainability as a market leader and preferred provider for children’s health care, Fitch said.

13. Concord (N.H.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of Concord’s leverage and liquidity assessment and Fitch’s assessment that two recently acquired hospitals will be strategically and financially accretive.

14. Cone Health has an “AA” rating and stable outlook with Fitch. The rating reflects the expectation that the Greensboro, N.C.-based system will gradually return to stronger results in the medium term, the rating agency said.

15. Cottage Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Santa Barbara, Calif.-based system’s leading market position and broad reach in a service area that exhibits modest population growth but consistently high demand for acute care services, Fitch said.

16. El Camino Health has an “AA-” rating and stable outlook with Fitch. The Mountain View, Calif.-based system has a history of generating double-digit operating EBITDA margins, driven by a solid market position that features strong demographics and a very healthy payer mix, Fitch said.

17. Froedtert Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s maintenance of a strong, albeit compressed, operating performance and a robust liquidity position, Fitch said.

18. Hackensack Meridian Health has an “AA-” rating and stable outlook with Fitch. The Edison, N.J.-based system’s rating is supported by its strong presence in its large and demographically favorable market, Fitch said.

19. Harris Health System has an “AA” rating and stable outlook with Fitch. The Houston-based system has a “very strong” revenue defensibility, primarily based on the district’s significant taxing margin that provides support for operations and debt service, Fitch said.

20. Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by a leading market position in its immediate area and very strong financial profile, Fitch said.

21. IU Health has an “AA” rating and stable outlook with Fitch. The Indianapolis-based system has a long track record of strong operating margins and an overall credit profile that is supported by a strong balance sheet, the rating agency said.

22. Inspira Health has an “AA-” rating and stable outlook with Fitch. The Mullica Hill, N.J.-based system’s rating reflects its leading market position in a stable service area and a large medical staff supported by a growing residency program, Fitch said.

23. Lucile Packard Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the Palo Alto, Calif.-based hospital’s role as a nationally known, leading children’s hospital, Fitch said. It also benefits from resilient clinical volumes and a solid market position, as well as its relationship with Stanford University and Stanford Health Care.

24. Kaiser Permanente has an “AA-” and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by a strong financial profile, which is maintained despite a challenging operating environment in fiscal year 2022.

25. Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The Rochester, Minn.-based system’s credit profile characterized by its excellent reputations for clinical services, research and education, Moody’s said.

26. McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The Grand Blanc, Mich.-based system has a leading market position over a broad service area covering much of Michigan and a track-record of profitability despite sector-wide market challenges in recent years, Fitch said.

27. MemorialCare has an “AA-” rating and stable outlook with Fitch. The rating reflects the Fountain Valley, Calif.-based system’s strong financial profile and excellent leverage metrics despite its weaker operating performance, Fitch said.

28. Memorial Sloan-Kettering Cancer Center has an “AA” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the New York City-based system’s national and international reputation as a premier cancer hospital will continue to support growth in its leading and increasing market share for its specialty services.

29. Midland (Texas) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Midland’s exceptional market position and limited competition for acute-care services and growing outpatient services, Fitch said.

30. Munson Healthcare has an “AA” rating and stable outlook with Fitch. The rating reflects the strength of the Traverse City, Mich.-based system’s market position and its leverage and liquidity profiles.

31. North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The Tupelo-based system’s rating reflects its very strong cash position and strong market position, Fitch said.

32. Novant Health has an “AA-” rating and stable outlook with Fitch. The Winston-Salem, N.C.-based system has a highly competitive market share in three separate North Carolina markets, Fitch said, including a leading position in Winston-Salem (46.8 percent) and second only to Atrium Health in the Charlotte area.

33. NYC Health + Hospitals has an “AA-” rating with Fitch. The New York City system is the largest municipal health system in the country, serving more than 1 million New Yorkers annually in more than 70 patient locations across the city, including 11 hospitals, and employs more than 43,000 people.

34. Orlando (Fla.) Health has an “AA-” and stable outlook with Fitch. The system’s upgrade from “A+” reflects the continued strength of the health system’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market, Fitch said.

35. The Queen’s Health System has an “AA” rating and stable outlook with Fitch. The Honolulu-based system’s rating reflects its leading state-wide market position, historically strong operating performance and diverse revenue streams, the rating agency said.

36. Rush System for Health has an “AA-” and stable outlook with Fitch. The Chicago-based system has a strong financial profile despite ongoing labor issues and inflationary pressures, Fitch said.

37. Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The Cape Girardeau, Mo.-based system enjoys robust operational performance and a strong local market share as well as manageable capital plans, Fitch said.

38. Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The system has a “very strong” financial profile and a leading market share position, Fitch said.

39. Stanford Health Care has an “AA” rating and stable outlook with Fitch. The Palo Alto, Calif.-based system’s rating is supported by its extensive clinical reach in the greater San Francisco and Central Valley regions and nationwide/worldwide destination position for extremely high-acuity services, Fitch said.

40. SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system has a strong financial profile, multi-state presence and scale, with solid revenue diversity, Fitch said.

41. St. Clair Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Pittsburgh-based system’s strong financial profile assessment, solid market position and historically strong operating performance, the rating agency said.

42. UCHealth has an “AA” rating and stable outlook with Fitch. The Aurora, Colo.-based system’s margins are expected to remain robust, and the operating risk assessment remains strong, Fitch said.

43. University of Kansas Health System has an “AA-” rating and stable outlook with S&P Global. The Kansas City-based system has a solid market presence, good financial profile and solid management team, though some balance sheet figures remain relatively weak to peers, the rating agency said.

44. WellSpan Health has an “Aa3” rating and stable outlook with Moody’s. The York, Pa.-based system has a distinctly leading market position across several contiguous counties in central Pennsylvania, and management’s financial stewardship and savings initiatives will continue to support sound operating cash flow margins when compared to peers, Moody’s said.

45. Willis-Knighton Health System has an “AA-” rating and stable outlook with Fitch. The Shreveport, La.-based system has a “dominant inpatient market position” and is well positioned to manage operating pressures, Fitch said.

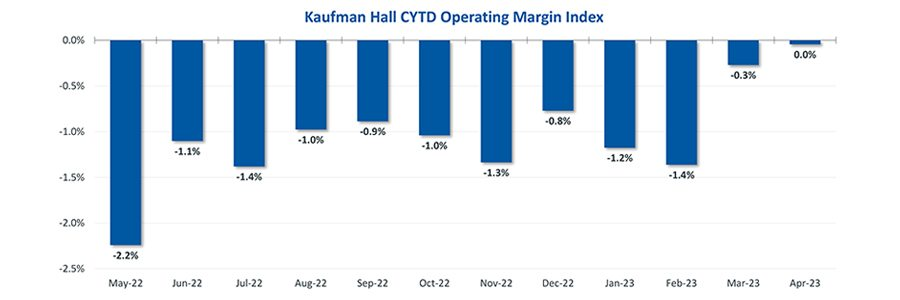

Hospital finances showed signs of stabilizing in May amid slightly improving operating margins, declining expenses and notable increases in outpatient visits.

The median Kaufman Hall Year-To-Date Operating Margin Index reflecting actual margins was 0.3% in May.

The National Hospital Flash Report uses both actual and budget data over the last three years, sampled from more than 900 hospitals on a recurring monthly basis from Syntellis Performance Solutions.

The sample of hospitals for this report is representative of all hospitals in the United States both geographically and by bed size. Additionally, hospitals of all types are represented, from large academic to small critical access. Advanced statistical techniques are used to standardize data, identify and handle outliers, and ensure statistical soundness prior to inclusion in the report.

While this report presents data in the aggregate, Syntellis Performance Solutions also has real-time data down to individual department, jobcode, paytype, and account levels, which can be customized into peer groups for unparalleled comparisons to drive operational decisions and performance improvement initiatives.

Key Takeaways

Hospitals broke even in April. The median operating margin for hospitals was 0% in April, leaving most hospitals with little to no financial wiggle room.

Volumes dropped while lengths of stay increased. Hospital volumes dropped across the board—including inpatient and outpatient. Emergency department volumes were the least affected.

Effects of Medicaid disenrollment could be materializing. Hospitals experienced increases in bad debt and charity care in April. Combined with anemic patient volumes, experts note this data could illustrate the effects of the start of widespread disenrollment from Medicaid following the end of the COVID-19 public health emergency.

Inflation continued to throttle hospital finances. Labor costs jumped in April and the costs of goods and services continued to be well above pre-pandemic levels. Though expenses generally fell in April, revenues declined at a faster rate.

National Non-Operating Results

Key Observations

At their May meeting, the Federal Open Market Committee (FOMC) raised the benchmark borrowing rate another 25 basis points, setting the range to 5.00-5.25% and marking the 10th consecutive hike in the cycle as well as a 16-year high

Fed officials acknowledged discussion of a potential pause in tightening while leaving wiggle room, saying “rates are going to come down” over a long period of time while also warning inflation “continues to run high” and the Fed will be taking a “data-dependent approach”

The consumer price index (CPI) rose 0.4% in April, a 4.9% increase year-over-year, an annual pace of inflation below 5% for the first time in two years

The labor market continued to show resilience in April as U.S. nonfarm payrolls grew by 253,000 and unemployment fell back to a 53-year low of 3.4%

Strong inflation, a robust labor market, continued banking sector woes, and a debt ceiling standoff further complicates credit conditions and may challenge the Fed to stabilize financial markets

Equities in April, as measured by the S&P 500, were up 1.5% in April and 8.6% YTD despite downbeat economic data, reoccurring banking sector fears, and mixed earnings

Despite a reasonably solid third quarter, Trinity Health is still operating at a loss in its 2023 fiscal year, according to a new filing.

The health system’s fiscal year began July 1, 2022, with the latest figures covering the first nine months. Its latest operating loss shrank to $263.1 million from the prior six months’ $298 million loss. Fiscal year 2023 operating revenue currently stands at $15.9 billion, up from the same period last year.

The nonprofit health system attributed its operating revenue growth to several acquisitions (MercyOne, North Ottawa Community Health System, Genesis Health System), which collectively added $1 billion of operating revenue. Net income for the last nine months was $856.3 million, compared to $43 million in the same period the prior year.

Though inpatient volumes are stabilizing to “a new normal,” management wrote in the latest filing, most of Trinity’s revenue comes from outpatient and other non-patient revenue. Operating expenses rose $1.1 billion compared to the same period in fiscal year 2022, mostly driven by the acquisitions.

Nonoperating income was $1.2 billion during the first nine months of fiscal year 2023, up from $264.6 million in the first six months. This hike was driven partly by a $629.3 million increase in investment returns.

The health system’s operating margin was 1.6%, per the latest filing, compared to 0.1% during the same period a year ago. Margins were affected by expenses outpacing revenue, primarily driven by premium labor rates and inflation impacting supplies as well as a $137 million reduction in CARES Act grant funding.

Trinity reports $10.2 billion in unrestricted cash and investments, including 180 days cash on hand compared to 211 days in fiscal year 2022, in its latest filing.

Trinity is focused on diversifying its business by shifting to ambulatory, home health, PACE, urgent care, specialty pharmacy and telehealth. The filing also noted the recent launch of a new care delivery model dubbed TogetherTeam, involving on-site and virtual nurses, that is expected to be implemented systemwide by the end of its 2024 fiscal year.

Salaries, wages and employee benefit costs rose 2.2%, offset by a reduction of $54.6 million in executive compensation and $39.7 million more pharmacy rebates than in the same period in fiscal year 2022. Same-facility contract labor costs decreased more than 40% to $193.9 million, reflecting “unprecedented” pandemic-related costs during the third quarter in 2022.

Trinity “continues to use strong cost controls over contract labor and other operational spending as colleague investment and utilization of its FirstChoice internal staffing agency promotes labor stabilization,” management wrote.

Trinity Health spans 88 acute care hospitals and hundreds of other care locations in 26 states and purports to have the second-largest Medicare PACE (Program of All-inclusive Care for the Elderly) program in the country. It provided services to 1.3 million people and reported a community benefit and charity of $1.4 billion in fiscal year 2022.

A decline in COVID-19 funding and sustained expenses issues helped lead St. Louis-based Ascension to a $1.8 billion operating loss in the nine months ending March 31.

The nine-month loss was on revenue of $21.3 billion. In the quarter ending March 31, the 140-hospital system reported an operating loss of $1.4 billion on $6.9 billion in revenue.

Such losses compared with $640 million and $671 million deficits in the nine-month and three-month periods, respectively, ending March 31, 2022.

Expenses for the nine-month period increased 3.7 percent on the previous year to total $22.3 billion.

“The reduction in COVID-19 funding negatively impacted revenue in the current year,” Ascension management said in the filing. “Additionally, challenges to expenses continue to persist resulting from the inflationary environment.”

The operating losses were offset by improved non-operating income in the first three months of 2023 but not over the nine-month period, which saw a net deficit of $1.9 billion.

Ascension, which operates 2,600 sites of care across 19 states and Washington, D.C., had 219 days of cash on hand as of March 31 compared with 259 at the same time last year.