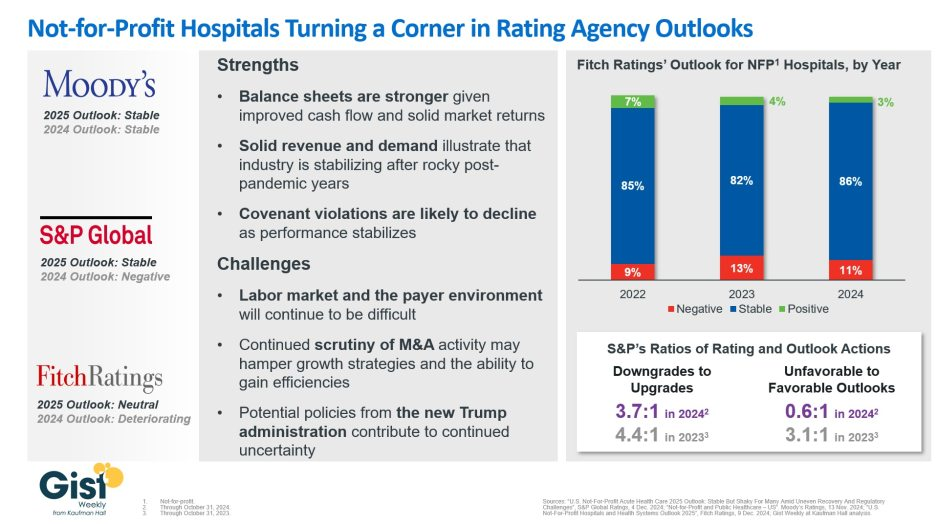

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

Expenses per provider remained considerably higher than revenue generated in the first quarter of 2024, although there are signs the gap could be closing, according to the Kaufman Hall “Physician Flash Report,” released May 2.

Kaufman Hall based their findings on a monthly report from Syntellis Performance Solutions, part of Strata. The report gathered data from more than 200,000 employed providers, including physicians and advanced practice providers.

Net patient revenue per provider full-time equivalent was $383,881 for the first quarter, up 4% from the same period last year. Total direct expenses per provider FTE hit $620,729 for the quarter. Expense growth has slowed over the last three years, with a 5% growth from 2022 to 2023 and just 3% growth from 2023 to 2024.

“Labor expenses are a growing proportion of total expenses, a trend that is unlikely to change significantly. Organizations should shift from optimizing downstream revenue to optimizing downstream margins,” the report authors advised, noting hospitals and physician organizations can evaluate provider specialties by outcomes or other metrics when they aren’t big revenue drivers.

Provider productivity was up 4% as measured by work relative value units. Physician wRVU per FTE was 5,979 for the first quarter, up 6% year over year. Physician compensation jumped 3% to $364,319, down from 6% growth between 2022 to 2023.

Labor expenses continue to rise while support staff decline across specialties. Labor was 84% of total expenses in the first quarter, and support staff per 10k provider wRVUs dropped 6% year over year to 3.14, even after an 8% drop from 2022 to 2023. Report authors recommended organizations find better ways to use APPs for higher physician productivity.

Here are specific data points from the first quarter report.

Median net patient revenue per provider FTE by specialty cohort were:

U.S. Hospital YTD Operating Margin Index November 2021-December 2023

The observations and questions from this chart are both interesting and required reading for hospital executives:

Why were hospitals profitable at the 4% plus level through the worst of the 2021 Covid period?

What exactly happened between December of 2021 and January of 2022 that resulted in a profitability decrease from a positive 4.2% to a negative 3.4%?

Despite the best efforts of hospital executives, overall operating margins were negative throughout calendar year 2022 and did not return to positive territory until March of 2023.

Hospital margins remained positive throughout 2023 and into 2024. However, overall margins have remained below those experienced in both 2021 and in the pre-Covid year of 2019.

The above questions and observations have proven interesting, and the ongoing numbers have proven quite useful in many quarters of healthcare. But recently I was talking with Erik Swanson, who is the leader of the Kaufman Hall Flash Report and our executive behind the data, numbers, and statistics. Erik and I were speculating about all of the above observations, but our key speculation was whether the 2023 operating margin results actually reflected a hospital financial turnaround or, in fact, were there “numbers behind the numbers” that told a different and much more nuanced story. So Erik and I asked different questions and took a much deeper dive into the Flash Report numbers. The results of that dive were quite telling:

Too many hospitals are still losing money. Despite the fact that the Operating Margin Index median for 2023 and into 2024 was over 2%, when you look harder at the Flash Report data, you find that 40% of American hospitals continue to lose money from operations into 2024.

There is a group of hospitals that have substantially recovered financially. Interestingly, the data shows over time that the high-performing hospitals in the country are doing better and better. They are effectively pulling away from the pack.

This leads to the key question: Why are high-performing hospitals doing better? It turns out that several key strategic and managerial moves are responsible for high-performing hospitals’ better and growing operating profitability:

Outpatient revenue. Hospitals with higher and accelerating outpatient revenue were, in general, more profitable.

Contract labor. Hospitals that have lowered their percentage of contract labor most quickly are now showing better operating profitability.

An important managerial fact.The Flash Report found that hospitals with aggressive reductions in contract labor were also correlated to rising wage rates for full-time employees. In other words, rising wage rates have appeared to attract and retain full-time staff which, in turn, has allowed those hospitals to reduce contract labor more quickly, all of which has led to higher profitability.

Average length of stay.No surprise here. A lower average length of stay is correlated to improved profitability. Those hospitals that have hyper-focused on patient throughput, which has led to appropriate and prompt patient discharge, have also proven this to be a positive financial strategy.

Lower financial performers have financially stagnated throughout the pandemic. The data shows that throughout the pandemic, hospitals with good financial results improved those results, but of more consequence, hospitals with poor financial performance saw that performance worsen. The Flash Report documents that the poorest financially performing hospitals currently show negative operating margins ranging from negative 4% to negative 19%. Continuation of this level of financial performance is not only unstainable but also makes crucial re-investment in community healthcare impossible.

The urban hospital/rural hospital myth. A popular and often quoted hospital comparison is that there is an observable financial divide between urban and rural hospitals. Erik Swanson and I found that recent data does not support this common perception. When you compare “all rurals” to “all urbans” on the basis of average operating margin, no statistically significant difference emerges. However, what does emerge—and is a very important statistical observation—is that the lowest performing 20% of rural hospitals are, in fact, generating much lower margins then their urban counterparts this year. It is at this lowest level of rural hospital performance where the real damage is being done.

Rural hospitals and obstetrics. The data does confirm one very important American healthcare issue: Obstetrics and delivery services are one of the leading money losers of all hospital service offerings. And the data further confirms that rural hospitals are closing obstetric departments with more frequency in order to protect the financial viability of the overall rural hospital enterprise. This is a health policy issue of major and growing consequence.

The point here is that data, numbers, and statistics matter both to setting long-term social health policy agendas and to the strategic management of complex provider organizations. But the other point is that the quality and depth of the analysis is an equally important part of the process. A first glance at the numbers may suggest one set of outcomes. However, a deeper, more careful and penetrating analysis may reveal critical quantitative conclusions that are much more telling and sophisticated and can accurately guide first-class organizational decision-making. Hopefully the analytics here are a good example of this very point.

Creating a great rating agency presentation is imperative to telling your story. I’ve probably seen a thousand presentations across the past three decades and I can say without a doubt that a great presentation will find its way into the rating committee. Show me a crisp, detailed, well-organized presentation, and I’ll show you a ratings analyst who walks away with high confidence that the management team can navigate the industry challenges ahead.

During the pandemic, Kaufman Hall recommended that hospitals move financial performance to the top of the presentation agenda. Better presentations chronicled the immediate, “line item by line item” steps management was taking to stop the financial bleeding and access liquidity. We still recommend this level of detail in your presentations, but as many hospitals relocate their bottom line, management teams are now returning to discussing longer-term strategy and financial performance in their presentations.

Beyond the facts and figures, many hospitals ask me what the rating analysts REALLY want to know. Over those one thousand presentations I’ve seen, the presentations that stood out the most addressed the three themes below:

What makes your organization essential? Hospitals maintain limited price elasticity as Medicare and Medicaid typically comprise at least half of patient service revenue, leaving only a small commercial slice to subsidize operations. The ability to negotiate meaningful rate increases with payers will largely rest on the ability to prove why the hospital is a “must-have” in the network. In other words, a health plan that can’t sell a product without a hospital in its network is the definition of essential. This conversation now also includes Medicare Advantage plans as penetration rates increase rapidly across the country. Essentiality may be demonstrated by distinct services, strong clinical outcomes and robust medical staff, multiple access points across a certain geography, or data that show the hospital is a low-cost alternative compared to other providers. Volume trends, revenue growth, and market share show that essentiality. A discussion on essentiality is particularly needed for independent providers who operate in crowded markets.

What makes your financial performance durable? Many hospitals are showing a return to better performance in recent quarters. Showing how your organization will sustain better financial results is important. Analysts will want to know what the new “run rate” is and why it is durable. What are the undergirding factors that make the better margins sustainable? Drivers may include negotiated rate increases from commercial payers and revenue cycle improvements. On the expense side, a well-chronicled plan to achieve operating efficiencies should receive material airtime in the presentation, particularly regarding labor. It is universally understood that high labor costs are a permanent, structural challenge for hospitals, so any effort to bend the labor cost curve will be well received. Management should also isolate non-recurring revenue or expenses that may drive results, such as FEMA funds or 340B settlements. To that end, many states have established new direct-to-provider payment programs which may be meaningful for hospitals. Expect questions on whether these funds are subject to annual approval by the state or CMS. The analysts will take a sharpened pencil to a growing reliance on these funds.

The durability of financial performance should be represented with highly detailed multi-year projections complete with computed margin, debt, and liquidity ratios. Know that analysts will create their own conservative projections if these are not provided, which effectively limits your voice in the rating committee.

We also recommend that hospitals include a catalogue of MTI and bank covenants in the presentation. Complying with covenants are part of the agreement that hospitals make with their lenders, and it is the organization’s responsibility to report how it’s performing against these covenants. General philosophy on headroom to covenants also provides insight to management’s operating philosophy. For example, is it the organization’s goal to have narrow, adequate, or ample headroom to the covenants and why? As the rating agencies will tell you, ratings are not solely based on covenant performance, but all rating factors influence your ability to comply with the covenants.

What makes your capital plan affordable? Every rating committee will ask what the hospital’s future capital needs are and how those capital needs will be supported by cash flow, also known as “capital capacity.” To answer that question, a hospital must understand what it can afford, based on financial projections. Funding sources may require debt, which requires a debt capacity analysis with goals on debt burden, coverage, and liquidity targets. Over the years, better presentations explain the organization’s capital model, outline the funding sources, and discuss management’s tolerance for leverage.

There is always a lot to cover when meeting with the rating agencies and a near endless array of metrics and indicators to provide. As I’ve written before, how you tell the story is as important as the story itself. If you can weave these three themes throughout the presentation, then you will have a greater shot at having your best voice heard in rating committee.

If you haven’t noticed (but I am sure you have) American business can be very unsettling from time to time, and occasionally the bigger the business, the more unsettling it gets. Exhibit A right now for this observation is, of course, the Boeing Company.

For years Boeing was an iconic, high reliability company; a worldwide leader in the growth of airplane transportation. As Bill Saporito wrote in the January 23 New York Times, Boeings’ airplanes were industry-changing, including the 707 jet in 1957, the 747 introduced in 1970, and perhaps the most successful commercial plane in aviation history, the 737.

But when things go bad, they can, indeed, go very bad. The newly designed 737 MAX crashed twice, once in 2018 and again in 2019, with a loss of life of 346 people. Now this year, a door plug fell off the Alaska Airlines Boeing 737 Max 9 at 16,000 feet and subsequent investigation revealed the possibility of missing bolts. All 737 MAX 9s were grounded while a special investigation was convened. Manufacturing airplanes is a special enterprise; lives are at stake. Airlines and the flying public take these Boeing problems very seriously.

What went wrong at Boeing?

Everybody has an opinion. One popular interpretation goes all the way back to Boeing’s merger in 1997 with McDonell Douglas. Recent articles suggest that prior to 1997 Boeing had a very dominant “engineering” culture. After the McDonell Douglas merger, the Boeing culture took a more “business” turn. That is the speculation anyway.

What strikes me here is the similarity between Boeing and the American hospital industry. Boeing “manufactures” planes and hospitals “manufacture” healthcare.

Neither industry can make mistakes; manufacturing errors in both cases change lives and cause real personal and societal pain. For both Boeing and hospitals, high reliability and error-free execution is the only acceptable business model.

Why is this analogy to Boeing apt and important?

Because American healthcare is likely the most intricate enterprise humanity has ever engineered. Therapeutic interventions are increasingly effective but demand pinpoint diagnoses and precision treatment. All of this is happening within profound technological complexity. The opportunity for regrettable manufacturing error—in fact the likelihood of such error—is so significant that no American hospital can possibly take for granted that high reliability processes and culture are properly in place and remain in place.

So what can hospitals do to keep from being Boeing?

In all candor, this question is over my paygrade, so for an experienced and nuanced answer, I turned to Allan Frankel, MD. Dr. Frankel is an anesthesiologist and former hospital executive who founded Safe and Reliable Healthcare after evaluating one too many disasters in healthcare delivery. He is currently an Executive Principal at Vizient Inc. Dr. Frankel offered the following high reliability tutorial:

High reliability manufacturing is directly dependent on the culture of the organization in question. Everyday excellence which leads to high reliability is dependent on the collective mindset and social norms of your workforce. Any high reliability workforce must trust its leadership and believe that the workforce values and leadership values are aligned. Further, a high reliability culture gives the workforce a sense of purpose and the opportunity to be their best professional selves on the job.

In the workplace, bi-directional communication is essential. Leaders and managers must round, see the actual work firsthand, learn what it is like to perform the work, and talk to individuals about the challenges of doing the work. Under best practices senior leaders should round 10% to 20% of their time. Line managers should round 80% to 90% of their time.

Workers, on the other hand, must have a sense of voice and agency. Voice means that workers are able to speak up about their concerns and ideas. Agency means that when workers do speak up, they see their ideas and concerns influence their work environment for the better.

Voice and agency require that workers feel safe in the high reliability process and that when identifying defects in the manufacturing process, they will be treated fairly. And importantly, that having the courage to speak up is an organizational attribute that is perceived as worthy. Such worthiness is described by discrete concepts including “psychological safety,” just culture,” and “respect.” Each of these concepts is definable and requires focused and ongoing training.

Concepts 3 and 4 require close attention and care and feeding. Functionally, this happens by robust leader rounding, robust managerial huddles, and timely feedback regarding manufacturing concerns and weaknesses. These activities need to be structural and must be built into a system of operations—such systems are often referred to as “standard work.” These changes plus the right frame of mind functionally drive improvement and change. Dr. Frankel noted “it’s not complicated, but as the Boeing example illustrates, the high reliability philosophy must be perpetually nourished.”

Once all the above is in place, there needs to be an effector arm. Process improvement skills are required to take ideas and concerns and test and implement them. Quality personnel must check on the changes as they are being made and audit operations. Dr. Frankel adds that this part of the high reliability journey is very often under-resourced in healthcare organizations, with the result that the overall process feels less effective so the activities stop occurring.

Training and skills are paramount. Skills come from training and reading. You should be thinking here about the “10,000 hours concept.” Worthy attitudes must be defined by your organization and then uniformly expected of all staff. Finally, behaviors can be structured, expectations set, and measures and metrics identified.

As you can see from the suggested activities, the foundations of high reliability are not rocket science. They require the right frame of mind, attention to detail, and clear accountability of all involved. No hospital should let that metaphorical 737 MAX 9 door plug fall off at 16,000 feet. It was, without question, a terrifying manufacturing moment.

For many providers, 2023 provided a return to profitability (albeit at modest levels) following the devastating operating and investment losses experienced in 2022.Kaufman Hall’s National Hospital Flash Report data illustrated generally improving operating margins throughout the year, leveling off at 2.0% in November on a year-to-date basis.

This level of performance is commendable given 2022 and early 2023 margins, although it is still well below the 3% to 4% range which we believe is needed for long-term sustainability in the not-for-profit healthcare world. We may well have reached a point of stability with respect to operating performance, but at a lower level.

The question for hospital and health system leaders is whether this level of operating stability provides sustainability?

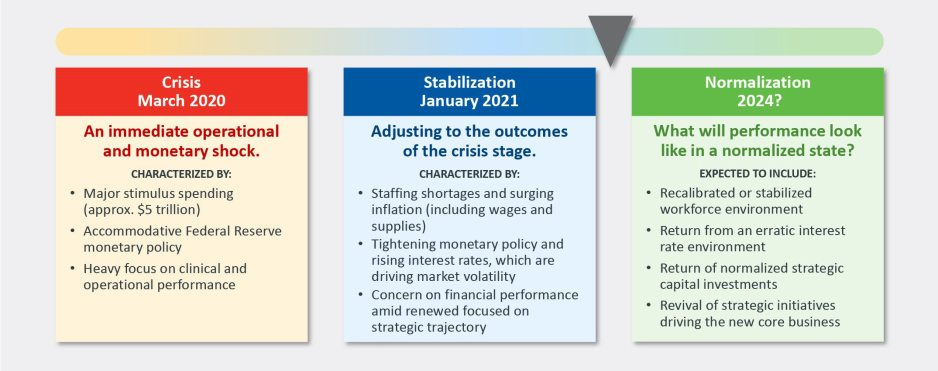

From stabilization to normalization

Since the pandemic began in 2020, the progress of recovery has been viewed over three phases: crisis, stabilization, and normalization. In last year’s outlook, we noted that we were in the midst of a potentially multi-year stabilization phase, which would continue to be marked with volatility—including ongoing labor market dislocations, inflationary pressures, and restrictive monetary policies. As we enter 2024, there are signs that we are now at the bridge between stabilization and normalization (Figure 1).

Figure 1: The Three Phases of Recovery from the Covid Pandemic

“The question for hospital and health system leaders is whether that level of stability provides sustainability?”

These signs include evidence that the first two indicators for normalization—a recalibrated or stabilized workforce environment and a return from an erratic interest rate environment—are coming into place. In our 2023 State of Healthcare Performance Improvement survey, respondents indicated that the spike in contract labor utilization that has been a dominant factor in operating expense increases was subsiding. Sixty percent of respondents said that utilization of contract labor was decreasing, and 36% said it was holding steady. Only 4% noted an increase in contract labor usage. Overall employee cost inflation seems to be subsiding as well: for all three labor categories in our survey (clinical, administrative, and support services), more organizations were able to hold salary increases to the 0% – 5% range in 2023 than in 2022.

There is good news on the interest rate front as well. After a series of rate increases in 2023, the Federal Reserve has held steady the last six months and has signaled rate cuts in 2024. Inflation has cooled markedly (albeit not yet at target levels), and employment rates have held steady. The Fed may have achieved a “soft landing” that satisfies its dual mandate of stable prices and maximum sustainable employment. Borrowing costs for not-for-profit hospital issuers have declined nearly 100 basis points in the last two months and we are expecting a return to more normal issuance levels in the first half of 2024.

There are other indications of normalization, including in the rating agencies’ outlooks for 2024. Regardless of the headline, all saw significant improvement in healthcare performance 2023.

The final answer to the question of whether the healthcare industry is entering the normalization phase likely will hinge on the last two indicators. Will we see a return of normalized strategic capital investments, and will we see a revival of strategic initiatives driving the core business (perhaps newly imagined)?

In effect, are health care systems simply surviving or are they thriving?

Looking forward, several factors could either bolster or undermine healthcare leaders’ confidence and willingness to resume a more normal level of investment in both capital needs and strategic growth. These include:

Politics and the 2024 elections. When North Carolina—a state that has traditionally leaned “red”—decided to opt into the Affordable Care Act’s (ACA’s) Medicaid expansion in 2023, it seemed that political debates over the ACA might be in the rearview mirror. But last November, former president Trump—currently the leading candidate for the Republican presidential nomination after strong wins in the Iowa caucuses and New Hampshire primary—indicated his intent to replace the ACA with something else. President Biden is now making protection and expansion of the ACA a key part of his 2024 campaign. What had appeared to be a settled issue may be a significant point of contention in the 2024 presidential election and beyond.

Although we do not anticipate any significant healthcare-related legislation in advance of the 2024 elections, healthcare leaders should be prepared for renewed attention to the costs of government-funded healthcare programs leading up to and following the elections. The national debt has increased rapidly over the past 20 years, tripling from $11 trillion in 2003 to $33 trillion in 2023. If the deficit and national debt become an important issue in the election, a move toward a balanced budget—akin to the Balanced Budget Act of 1997—post election could lead to further cuts to Medicare and Medicaid.

Temporary relief payments. Health systems continue to receive one-time cash infusions through the 340B settlement, Federal Emergency Management Agency (FEMA) payments and other governmental programs. Approximately 1,600 hospitals have or will be receiving a lump-sum payment to compensate them for a change in the Department of Health & Human Services’ (HHS’s) reimbursement rates for the 340B program from 2018 to 2022, which was ruled unlawful by the Supreme Court in a 2022 decision. The total amount to be distributed is approximately $9 billion and began hitting bank accounts in January 2024.

But what the right hand giveth, the left hand taketh away. Budget neutrality requirements will force HHS to recoup this offset—amounting to approximately $7.8 billion—which it will do by reducing payments for non-drug items and services to all Outpatient Prospective Payment System (OPPS) providers by 0.5% until the offset has been fully recouped, beginning in calendar year 2026. HHS estimates that this process will take approximately 16 years. Is this a harbinger of lower payments on other key governmental programs?

Many hospitals also continue to receive Covid-related payments from FEMA for expenses occurred during the pandemic. In addition, state supplemental payments—especially under Medicaid managed care and fee-for-service programs—are providing some relief. The Centers for Medicare & Medicaid Services has issued a proposed rule, however, that would limit states’ use of provider-based funding sources, such as provider taxes, and cap the rate of growth for state-directed payments.

As all of these payment programs dry up over the next few years, hospitals will need to replace the revenue and/or get leaner on the expense side in order to maintain today’s level of performance.

The hollowing of the commercial health insurance market. Our colleague, Joyjit Saha Choudhury, recently published a blog on the hollowing of the commercial health insurance market, driven by long-term concerns over the affordability of healthcare. While volumes have been recovering to pre-pandemic levels, this hollowing threatens the loss of the most profitable volumes and will pressure hospitals and health systems to create and deliver value, compete for inclusion in narrow networks, and develop more direct relationships with the employer community.

Related, the growing penetration of Medicare Advantage plans is reducing the number of traditional Medicare beneficiaries. Many CFOs report that these programs can be the most difficult with which to work given their high denial rates and required pre-authorization rates. A new rule requiring insurers to streamline prior authorizations for Medicare Advantage, Medicaid, and Affordable Care Act plans may help alleviate this issue; however, it will be incumbent upon management teams to stay ahead of them. Aging demographics are also reducing the percentage of commercially insured patients for many hospitals and health systems, further exacerbating the problem. This combination of fewer commercial patients (who often subsidize governmental patients) and more pressure on receiving the duly owed commercial revenue threatens to be an ongoing headache for management teams.

Ongoing impact of the Baby Boom generation. Despite the good news on inflation—and indications that the Fed may begin lowering interest rates in 2024—the economy is by no means out of the woods yet. The Baby Boom generation, which holds more than 50% of the wealth in the U.S. and is seemingly price agnostic, still has many years of spending ahead, in healthcare and general purchasing. This will likely continue to pressure inflation, especially in the healthcare sector, where demand will continue to grow. As the generation starts to shrink, the resulting wealth transfer will be the largest ever in our country’s history and have profound (and unforeseen) consequences on the overall economy and healthcare in general.

In sum, these other factors will continue to affect the sector (both positively and negatively) and require health system management teams to navigate an everchanging world. While many signs point toward short-term relief, the longer-term challenges persist. Improvements in the short term may, however, provide the opportunity to reposition organizations for the future.

How hospitals and health systems should respond

Healthcare leaders should view ongoing uncertainty in the political and economic climate as a tailwind as much as a headwind. This uncertainty, in other words, should be a motivation to put in place strategies that will buffer healthcare organizations from potential bumps in the road ahead. Setting balance sheet strategy should be a part of an organization’s planning process.

How an organization sets that strategy, measures its performance, and makes improvements will set apart top-performing organizations.

Although heightened debt issuance early in 2024 signals a return for many systems to a climate of investment, there is still limited energy around strategy and debt conversations in many boardrooms, especially in those organizations where financial improvement continues to lag. The last two years have illustrated that hospitals and health systems will not be able to cut their way to profitability. Lackluster performance cannot and will not improve without some level of strategic change, whether it is through market share gains, payer mix shift, or operational improvements. This strategic change requires investment and investment requires capital. Capital can be obtained in many forms—whether through growth in capital reserves, improved cash flow, or new debt issuance—but is essential for change. Reengaging in conversations about strategy and growth should be an imperative in 2024 and will require reexamining how that growth is funded.

Healthcare leaders should engage their partners as they continue or refocus on:

Changing the conversation from debt capacity to capital capacity. Management teams need to determine what they can afford to spend on capital if the new normal of cash flow will be constrained going forward. Capital capacity is and should be agnostic to the source of that capital, such as debt, cash flow from operations, or liquidity reserves. Healthcare leaders must focus on what they can spend, before deciding how to fund that spending. The conversation will need to balance investment for the future with maintaining key credit metrics in the short term.

Conducting a capitalization analysis. Separate but related to the previous entry, how much leverage should your organization have relative to its overall capitalization? Ostensibly, many organizations have been paying principal while curtailing borrowing needs, so capitalization may have improved. While that may be the case, many organizations have depleted reserves and/or experienced investment losses that have reduced capitalization. Understanding where the organization stands is an essential next step.

Evaluating surplus return. Consider surplus return as investment income net of interest expense. Organizations should evaluate their ability to reliably generate both operating cash flow and net surplus. How an organization’s balance sheet is positioned to generate returns and manage risk will be a critical success factor.

Focusing on the metrics that matter. These include operating cashflow margin, cash to debt, debt to revenue, and days cash on hand. As key metrics for rating analysts and investors continue to evolve, management teams need to make sure they are focused on the correct numbers. The discussion should be dually focused on ensuring adequate-to-ample headroom to basic financial covenants as well as a comparison to key medians and peers. Strong financial planning will address how these metrics can be improved over time through synergies, growth, and diversification strategies.

Although it has been a difficult few years, hospitals and health systems seem to have moved onto a more stable footing over the last twelve months. In order to build upon the upward trajectory, now is the time to harness strategy, planning, and investment to move organizations from stability to sustainability.

How should health systems spend their “community benefit” dollars?

That question was at the heart of a discussion we participated in recently at a member board meeting. To maintain their nonprofit status, all health systems are required to devote a portion of their earnings to activities that benefit the communities they serve, based on an assessment of local health needs.

The question our member’s board was grappling with, led by the system’s executive team, was how to ensure their “investment” in the community is as leveraged as possible, and generates the greatest “bang for the buck” in terms of better community health.

As the importance of addressing the social determinants of health grows, many systems are trying to target their resources toward activities that that enhance their ability to improve health status, and to reduce the barriers to better health faced by many. That requires a level of rigor and commitment to “community ROI” that goes beyond simply pointing to charity care statistics and the number of uninsured served.

What most impressed us in the discussion was the application of the same investment mindset to community benefit that the system brings to capital allocation decisions—with due attention to implementation plans, outcomes metrics, and accountability.

As the system’s COO framed it, “We don’t just want to be a ‘piggy bank’ for charitable causes, we want to make sure our investment in the community is really making a difference” in local residents’ health. At the same time, the board recognized that its role extends beyond simply contributing dollars to acting as a convener and facilitator of other community organizations working together toward a common set of goals. A worthy discussion for the board, for sure, and a priority we’re seeing leading systems begin to embrace in a serious way.

2022 and 2023 have been particularly difficult operating years for hospital providers. The financial challenges stand out but as we concluded in the August 7, 2023, blog, strategic planning and vision issues may be more compelling over the long term.

We previously identified two strategic issues that need to be reckoned with:

Strategic Relevance. Has everything changed organizationally post-Covid or does it just feel that way? If your strategy still seems dynamic and relevant, how do you capitalize on that? If your strategy feels entirely lost, how do you recapture organizational excitement and enthusiasm?

Vision. How important is organizational vision right now? You know the old saying, “a camel is a horse designed by a committee.” And many vision statements wind up looking more like that camel than like that desired horse. But be that as it may: Covid has been so disruptive to the organizational momentum of hospitals that finding a relevant and executable vision should be top of mind right now.

Given circumstances, one obvious conclusion is that any strategic exercise undertaken in the current moment needs to be well accomplished. Executive teams, clinicians, and Boards are simply too distracted or too tired to spend time on planning processes that are not well thought out and highly directed. This immediate observation next demands a discussion that outlines post-Covid strategic principles, definitions, and the creation of a vision that relates immediately to actionable strategy. It would be an understatement to note that for hospitals there is no “strategic time” to waste.

Start the post-Covid planning process with four very clear strategic definitions:

Vision: A time-bounded view of the future destination of your business.

Strategic Workstreams: The ways you devise to achieve the strategic vision.

Goals: Goals are the lag outcomes that you seek to achieve for your customers.

Metrics: Metrics measure the progress toward the goals.

Working from these definitions then allows you to move toward an organizationally appropriate vision and an actionable strategy that efficiently supports that vision as follows:

The vision should drive growth. Many hospital organizations have stopped growing organically. No growth is harmful financially, clinically, intellectually, and creatively.

The vision should differentiate the business from that of competitors. Everybody and everything competes with hospitals these days: other hospitals, pharmacy companies, insurers, private equity. It has no end.

The vision should endeavor to solve a basic customer problem or problems. The problem list is pretty apparent. The list of helpful solutions has been harder to come by.

The vision should be either incremental or transformational. In all candor, most hospitals’ post-Covid vision is going to be incremental. It takes considerable financial and capital capacity to move toward a transformational vision. That kind of capacity is available at only a small minority of hospitals nationwide.

Recognize that a transformational vision will require active management of culture and stakeholders. If you pivot to a transformational vision, you are likely to upset certain stakeholders and your existing culture may need to also adjust to the transformation.

Be prepared to modify or improve upon the vision, workstreams, and/or goals as you get ongoing feedback during the planning and execution process. Under any circumstances you need to be open to learning all along the way. For this to happen, your organization needs to be a listening organization and a learning organization. Not all hospitals and health systems are.

Does all this sound hard? It should sound hard because it is hard. Leading the hospital back to financial stability while finding a relevant post-Covid vison that proves to be competitive and, at the same time, energizes your team to find renewed purpose in your hospital’s work; that is unforgivably hard.

As Piet Hein, the Danish mathematician, profoundly said, “Problems worthy of attack prove their worth by fighting back.” And fighting back is the hospital job of the moment.

Note: “Culture eats strategy for breakfast” is a quote attributed to management consultant and writer Peter Drucker.