On January 17, 2025, a list of potential cost reductions to the federal budget was released by Republicans on the House Budget Committee. The list is long and covers the federal budget waterfront, but it spends considerable time focusing on reductions to healthcare spending. This laundry list of cost reductions is important because the highest priority of the Trump administration is a further reduction in federal taxes. A reduction in taxes would, of course, reduce federal revenue; if federal expenses are not proportionately reduced then the federal deficit will increase. When the deficit increases then the federal debt must increase and at that point the overall impact on the American economy becomes concerning and possibly damaging. There has already been much public speculation as to how the Federal Reserve might react to such a scenario.

It is not possible right now to highlight and describe all of the House budget proposals, but one proposal absolutely stands out: The suggestion to eliminate the tax-exempt status for interest payments on all municipal bonds, or potentially in a more targeted manner, for private activity bonds, including those issued by not-for-profit hospitals. Siebert Williams Shank, an investment banking firm, described the elimination of tax exemption for municipal bonds as “the most alarming of the proposed reforms impacting non-profit and municipal issuers.”[1] This is certainly true for hospitals, since over the past 60 years the growth and capability of America’s hospitals has been substantially constructed on the foundation of flexible and relatively inexpensive tax-exempt debt. Given all of this, it is not too early to begin speculating on the impact of the elimination of tax-exempt debt on hospital finances and strategy.

We should also point out that a separate topic is under discussion, related to the potential loss of not-for-profit status for hospitals and health systems. Such a maneuver could potentially expose hospitals to income taxes, property taxes, and higher funding costs. For now, that is beyond the scope of this blog but may be something we write about in future posts.

Below is a series of important questions related to the elimination of tax-exempt financing and some speculations on the overall impact:

What immediately happens if 501(c)(3) hospitals lose the ability to issue tax-exempt bonds? Let’s treat fixed rate debt first. Assume for now that only newly issued debt would be affected and that all currently outstanding tax-exempt fixed rate debt would remain tax-exempt. We could see an effort to apply any changes retroactively to existing bonds, but we view that as unlikely. Therefore, our current expectation is that outstanding fixed-rate debt would not see a change in interest expense.

However, it is possible that outstanding floating rate debt would immediately begin to trade based on the taxable equivalent. Historically the tax-exempt floating rate index trades at about 65% of the taxable index. The difference between the tax-exempt and taxable floating rate indices in the current market is 175 basis points. For every $100 million of debt, this would increase interest expense by $1.75m annually.

How would new hospital debt be issued? New debt would be issued in the municipal market on a taxable basis or in the corporate taxable market. The taxable municipal market would need to adapt and expand to accommodate a significant level of new issuance. The concern in the corporate taxable market is greater. Currently, the corporate market requires issuance of significant dollar size and generally the issuer brings significant name recognition to the market. Many hospitals may have difficulty meeting the issuance size of the corporate debt market and/or the necessary market recognition. As such, smaller and less frequent issuers would expect to pay a penalty of 25-50 basis points for issuing in the corporate market.

If tax-exempt debt goes away will certain hospitals be advantaged and others disadvantaged? Larger hospitals with national or regional name recognition that issue bonds with sufficiently large transaction size and frequency will likely borrow at better terms and lower rates. Smaller- to medium-sized hospitals may find borrowing much more difficult, and borrowing may come with more problematic terms and/or amortization schedules and likely higher interest rates.

Will borrowing costs go up? The cost of funds for new borrowings would increase for all hospital borrowers. For a typical A-rated hospital, annual interest expense would increase by approximately 30%. For example, in the current market, on $100 million of new debt, average annual interest expense would increase by $815,000 annually.

Will debt capacity go down? All other things being equal, interest rates will go up and hospital debt capacity will go down. Also, if the taxable market shortens amortization schedules, then that will decrease overall debt capacity as well.

What would the impact of the elimination of tax-exempt debt be on synthetic fixed rate structures? Hospitals have long employed derivative structures to hedge interest rate risk on outstanding variable rate bonds and loans. The loss of tax-exemption for outstanding variable rate bonds and loans would precipitate an adjustment to taxable rates, but corresponding swap cash flows are not designed to adjust. Interest rate risk is hedged, but tax reform risk is not. The net effect to borrowers would be an increase in cost similar to the cost contemplated above for variable rate bonds.

What are the rating implications of the elimination of the tax-exempt market? Rating implications will be varied. Hospitals with strong financial performance and liquidity are likely to absorb the increased interest expense of a taxable borrowing with little to no rating impact. In fact, over the past decade, many larger health systems in the AA rating categories have successfully issued debt in the taxable market without rating implications despite a higher borrowing rate. Even amid the pandemic chaos of 2021, numerous AA and A rated systems issued sizable, taxable debt offerings to bolster liquidity as proceeds were for general corporate purposes and not restricted by a third-party, such as a bond trustee.

Lower-rated hospitals with modest performance and below-average liquidity will be at greater risk for a downgrade. These hospitals may not be able to absorb the increased interest expense and maintain their ratings. While interest expense is typically a small percentage of a hospital’s total expenses, it is a use of cash flow.

We do not anticipate the rating agencies will take wholesale downgrade action on the rated portfolio as there would likely be a phase-in period before the elimination occurs. Rather, we expect the rating agencies will take a measured approach with a case-by-case evaluation of each rated organization through the normal course of surveillance, as they did during the pandemic and liquidity crisis in 2008. A dialogue on capital budgets and funding sources, typically held at the end of a rating meeting, would be moved to the top of the agenda, as it will have a direct impact on long-term viability.

How would the loss of the tax-exempt market impact the pace of consolidation in the hospital industry? If a hospital cannot afford the taxable market, then large capital projects would need to be funded through cash and operations. This inevitably will limit organizational liquidity, which will lead to downward rating pressure. Some hospitals, in such a situation, will be unable to both fund capital and adequately serve their local community and, therefore, will need to find a partner who can. We anticipate that the loss of the tax-exempt bond market will lead to further consolidation in the industry.

Let’s indulge in one last bit of speculation. What is the probability that Congress will pass legislation that eliminates tax-exempt financing? Sources in Washington tell us that it is premature to wager on any of the items put forth by the Budget Committee. And it should be noted that over the years the elimination of tax-exempt financing has been proposed on several occasions and never advanced in Congress. However, one well-informed source noted that as the tax and related legislation moves forward, there is likely to be significant horse-trading (especially in the House) to secure the necessary votes to pass the entire package. What happens during that horse-trading process is anybody’s guess. So the best advice to our hospital readership right now is to not take anything for granted. But be absolutely assured that the maintenance of tax-exempt financing is an essential strategic component for the successful future of America’s hospitals.

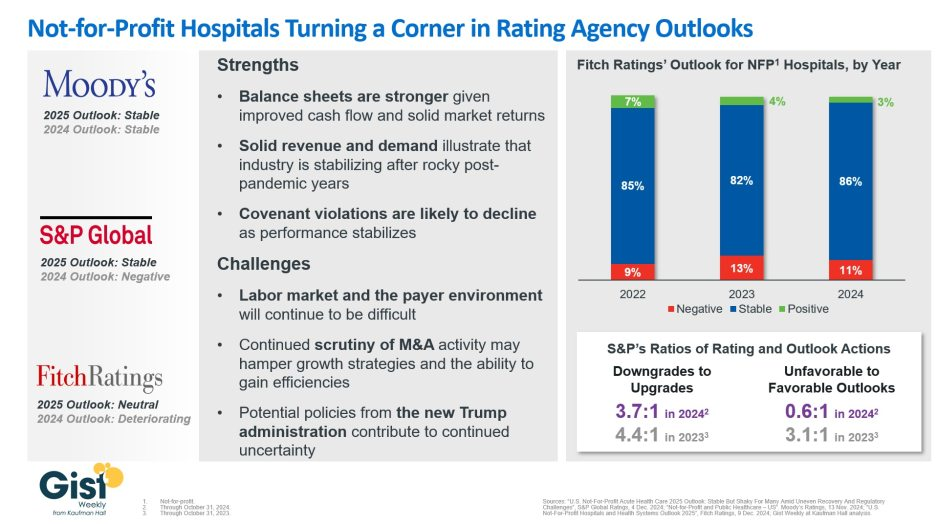

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

Here are 67 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating is based on the Altamonte Springs, Fla.-based system’s competitive market position—especially in its core Florida markets—and its financial profile, Fitch said.

Advocate Health members Advocate Aurora Health and Atrium Health have “Aa3” ratings and positive outlooks with Moody’s. The ratings are supported by the Charlotte, N.C.-based system’s significant scale, strong market share across several major metro areas, and good financial performance and liquidity, Moody’s said.

AnMed Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Anderson, S.C.-based system’s strong and stable operating performance and leading market position in a sound service area, Fitch said.

Ann & Robert H. Lurie Children’s Hospital of Chicago has an “AA” rating and stable outlook with Fitch. The rating is supported by the system’s strong balance sheet with low leverage ratios derived from modest debt, Fitch said.

Atlantic Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Morristown, N.J.-based system’s fundamental strengths, including strong operating performance with high single digit operating cash flow margins and favorable liquidity of over 300 days cash on hand, Moody’s said.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

BayCare Health System has an “AA” rating and stable outlook with Fitch. The Clearwater, Fla.-based system on June 30 moved to a new corporate legal structure, replacing a joint operating agreement between multiple hospitals that were responsible for the creation of BayCare in 1997. Fitch views the dissolution of the JOA and the move to the new structure as a credit positive.

Beacon Health System has an “AA-” rating and stable outlook with Fitch. Fitch said the rating reflects the strength of the South Bend, Ind.-based system’s balance sheet.

Bon Secours Mercy Health has an “AA-” rating and stable outlook with Fitch. The Cincinnati-based system has a favorable and stable payor mix, leading or secondary market share position in nine of its 11 U.S. markets with improving market share positions in eight, and adequate cash flows to support the system’s strategic plans, Fitch said.

BJC Health System has an “Aa2” rating and stable outlook with Moody’s. The St. Louis-based system reflects its reputation as a leading academic medical center with a long-standing affiliation with Washington University School of Medicine, Moody’s said.

Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area and Fitch’s expectation that the system will sustain its strong capital-related ratios in the context of the system’s midrange revenue defensibility and strong operating risk profile assessments.

Carilion Clinic has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Roanoke, Va.-based system’s scale, regional significance as a tertiary referral system with broad geographic capture, and a highly integrated physician base with a well-defined culture, Moody’s said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals, and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence, and pediatric trauma status, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The rating reflects the Minneapolis-based system’s strong balance sheet, robust liquidity position, and dominant pediatric market position, Fitch said.

Cincinnati Children’s Hospital Medical Center has an “Aa2” rating and stable outlook with Moody’s. The rating is supported by its national and international reputation in clinical services and research, Moody’s said.

Cleveland Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the system’s strength as an international brand in highly complex clinical care and research and centralized governance model, the ratings agency said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth, Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

Corewell Health has an “Aa3” rating and stable outlook with Fitch. The rating reflects the Grand Rapids and Southfield, Mich.-based system’s significant scale as a provider and payer in Michigan, Moody’s said. The organization also has good and stable financial performance and liquidity.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

Froedtert ThedaCare Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s solid market position, track record of strong utilization and operations, and strong financial profile, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by its strong operating risk assessment, leading market position in its immediate service area, and strong financial profile, Fitch said.

Holland (Mich.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects Holland Hospital’s stable and strong liquidity and capital-related metrics despite sector-wide operating pressures, Fitch said.

Indiana University Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Indianapolis-based health system’s sustained track record of strong operating margins, ratings agency said.

Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The Falls Church, Va.-based system’s rating is anchored by its role as one of the largest health systems in Virginia with a leading market position in a rapidly growing region with unusually high commercial business, Moody’s said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Mullica Hill, N.J.-based system will return to strong operating cash flows following the operating challenges of 2022 and 2023, as well as the successful integration of Inspira Medical Center of Mannington (formerly Salem Medical Center).

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Kaiser Permanente has an “AA-” rating and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by its strong financial profile, bolstered by a large and diversified revenue base, Fitch said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Rochester, Minn.-based system’s preeminent reputation for clinical care and research, including new discoveries and cutting-edge treatment, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

McLeod Health has an “AA-” rating and stable outlook with Fitch. The Florence, S.C.-based system maintains a leading and growing market position in its primary service area and is expanding the Carolina’s Forest campus in an area that is expected to experience rapid growth over the coming years, Fitch said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Memorial Healthcare System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects that the Hollywood, Fla.-based system will continue to benefit from good strategic positioning of its large, diversified geographic footprint.

Memorial Hermann Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Houston-based system’s leading and expanding market position and strong demand in a growing region, Moody’s said.

Methodist Health System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects the Dallas-based system’s consistently strong operating performance, excellent liquidity, and very good market position.

Monument Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Rapid City, S.D.-based system has a dominant inpatient market position as the leading acute care provider in its geographically broad primary service area

Nationwide Children’s Hospital has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Columbus, Ohio-based system’s strong market position in pediatric services, growing statewide and national reputation, and continued expansion strategies.

Nicklaus Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Miami-based system’s position as the “premier pediatric hospital in South Florida with a leading and growing market share,” Fitch said.

North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The rating reflects the Tupelo-based system’s strong cash position and strong market position with a leading market share in its primary services area, Fitch said.

Northwestern Memorial HealthCare has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Chicago-based system’s growing market position, single operating model and financial discipline, Moody’s said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research, and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Parkland Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Dallas-based system will remain the leading provider of public (safety net) services in the vast Dallas County service area, supported by its tax levy.

Phoenix Children’s has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong cash flow generation that has significantly improved its balance sheet in recent years, Fitch said.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rady Children’s Hospital has an “Aa3” rating and stable outlook with Moody’s. The San Diego-based system’s rating reflects its well-established strengths, including an “extremely high” market share in all of San Diego County, Moody’s said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing position in a stable service area with good population growth and demand for acute care services, Fitch said.

Sarasota (Fla.) Memorial Health Care System has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s leading market position in a growing service area, robust historical operating cash flow levels and strong liquidity position, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

St. Elizabeth Medical Center has an “AA” rating and stable outlook with Fitch. The rating reflects the Edgewood, Ky.-based system’s strong liquidity, leading market position, and strong financial management, Fitch said.

St. Tammany Parish Hospital has an “AA-” rating and stable outlook with Fitch. The Covington, La.-based system has a strong operating risk assessment and very strong financial profile supported by consistently robust operating cash flows, Fitch said.

Stanford Health Care has an “Aa3” rating and positive outlook with Moody’s. The rating reflects the Palo Alto, Calif.-based system’s clinical prominence, patient demand, and its location in an affluent and well-insured market, Moody’s said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong financial profile in the context of its broad and growing reach for high-acuity services, Fitch said.

University Health has an “AA+” rating and stable outlook with Fitch. The San Antonio-based system’s outlook is based on the Bexar County Hospital District’s significant tax margin, good cost management, and strong leverage position relative to its liquidity and outstanding debt.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

University of Kansas Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects Kansas City-based system’s flagship hospital’s important presence as the only academic medical center in Kansas and a major provider of many high end and unique services to a large geographic area, Fitch said.

UW Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Madison, Wis.-based system’s strong clinical reputation, high acuity services, and important role as the academic medical center affiliated with the state’s flagship public university, Moody’s said.

VCU Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Richmond, Va.-based system’s status as one of Virginia’s leading academic medical centers and essential role as its largest safety net provider, supporting excellent patient demand at high acuity levels, Moody’s said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

Here are 48 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating is based on the Altamonte Springs, Fla.-based system’s competitive market position—especially in its core Florida markets—and its financial profile, Fitch said.

Advocate Health members Advocate Aurora Health and Atrium Health have “Aa3” ratings and positive outlooks with Moody’s. The ratings are supported by the Charlotte, N.C.-based system’s significant scale, strong market share across several major metro areas, and good financial performance and liquidity, Moody’s said.

Ann & Robert H. Lurie Children’s Hospital of Chicago has an “AA” rating and stable outlook with Fitch. The rating is supported by the system’s strong balance sheet with low leverage ratios derived from modest debt, Fitch said.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

Beacon Health System has an “AA-” rating and stable outlook with Fitch. Fitch said the rating reflects the strength of the South Bend, Ind.-based system’s balance sheet.

Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area and Fitch’s expectation that the system will sustain its strong capital-related ratios in the context of the system’s midrange revenue defensibility and strong operating risk profile assessments.

Carilion Clinic has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Roanoke, Va.-based system’s scale, regional significance as a tertiary referral system with broad geographic capture, and a highly integrated physician base with a well-defined culture, Moody’s said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals, and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence, and pediatric trauma status, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The rating reflects the Minneapolis-based system’s strong balance sheet, robust liquidity position, and dominant pediatric market position, Fitch said.

Cincinnati Children’s Hospital Medical Center has an “Aa2” rating and stable outlook with Moody’s. The rating is supported by its national and international reputation in clinical services and research, Moody’s said.

Cleveland Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the system’s strength as an international brand in highly complex clinical care and research and centralized governance model, the ratings agency said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth, Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

Froedtert ThedaCare Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s solid market position, track record of strong utilization and operations, and strong financial profile, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by its strong operating risk assessment, leading market position in its immediate service area, and strong financial profile, Fitch said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Mullica Hill, N.J.-based system will return to strong operating cash flows following the operating challenges of 2022 and 2023, as well as the successful integration of Inspira Medical Center of Mannington (formerly Salem Medical Center).

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Rochester, Minn.-based system’s preeminent reputation for clinical care and research, including new discoveries and cutting-edge treatment, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Memorial Healthcare System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects that the Hollywood, Fla.-based system will continue to benefit from good strategic positioning of its large, diversified geographic footprint.

Memorial Hermann Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Houston-based system’s leading and expanding market position and strong demand in a growing region, Moody’s said.

Methodist Health System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects the Dallas-based system’s consistently strong operating performance, excellent liquidity, and very good market position.

Nationwide Children’s Hospital has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Columbus, Ohio-based system’s strong market position in pediatric services, growing statewide and national reputation, and continued expansion strategies.

Nicklaus Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Miami-based system’s position as the “premier pediatric hospital in South Florida with a leading and growing market share,” Fitch said.

North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The rating reflects the Tupelo-based system’s strong cash position and strong market position with a leading market share in its primary services area, Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research, and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Parkland Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Dallas-based system will remain the leading provider of public (safety net) services in the vast Dallas County service area, supported by its tax levy.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing position in a stable service area with good population growth and demand for acute care services, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

St. Elizabeth Medical Center has an “AA” rating and stable outlook with Fitch. The rating reflects the Edgewood, Ky.-based system’s strong liquidity, leading market position, and strong financial management, Fitch said.

Stanford Health Care has an “Aa3” rating and positive outlook with Moody’s. The rating reflects the Palo Alto, Calif.-based system’s clinical prominence, patient demand, and its location in an affluent and well-insured market, Moody’s said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong financial profile in the context of its broad and growing reach for high-acuity services, Fitch said.

University Health has an “AA+” rating and stable outlook with Fitch. The San Antonio-based system’s outlook is based on the Bexar County Hospital District’s significant tax margin, good cost management, and strong leverage position relative to its liquidity and outstanding debt.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

VCU Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Richmond, Va.-based system’s status as one of Virginia’s leading academic medical centers and essential role as its largest safety net provider, supporting excellent patient demand at high acuity levels, Moody’s said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

Days cash on hand is one of the most important metrics in hospital credit analysis. The ratio calculates an organization’s unrestricted cash and investments relative to daily operating expenses.

Here’s a computation commonly used to calculate days cash on hand:

Math aside, let’s unpack what days cash on hand really tells us. Days cash on hand gives an indication of a hospital’s flexibility and financial health. Essentially, it tells us how long a hospital could continue to operate if cash flow were to stop. From a ratings perspective, the higher the days cash, the better, to create a cushion or rainy-day fund for unexpected events.

While the sheer abatement of cash flow feels like a doomsday scenario, we don’t have to look far back to see examples. The shutdown in the early days of Covid and the recent Change Healthcare cyberattack are examples of events that can materially impact cash flow. While these may be considered extreme, there are plenty of more common events that can disrupt cash flow, including a delay in supplemental funding, an IT installation, a change in Medicare fiscal intermediary, an escalation in construction costs, or the bankruptcy of a payer.

Size and diversified business enterprises can impact days cash on hand. For example, small hospitals with outsized cash positions relative to operations often report a dizzying level of days cash on hand. Health systems with wholly owned health plans often show lower days cash when compared to like-sized peers without health plans. Analysts will also review a hospital’s cash-to-debt ratio, which is an indication of leverage and compares absolute unrestricted cash to long-term obligations. Cash-to-debt creates a more comparable ratio across the portfolio.

In the years leading up to the pandemic, the days cash on hand median increased steadily as the industry went through a period of stable financial performance and steady equity market returns. Hospitals took advantage of an attractive debt market to fund large capital projects or reimburse for prior capital spending. The median crested over 200 days. As discussed during our March 20, 2024, rating agency webinar, days cash median for 2023 is expected to decline or remain flat at best, not because of an increase in capital spending or deficit operations, but because daily expenses (mainly driven by labor) will grow faster than absolute cash. Expenses will outrun the bear, so to speak.

Days cash on hand will remain a pillar liquidity ratio for the industry, but equally important is the concept of liquidity. Days cash on hand doesn’t tell the whole story regarding liquidity. A hospital may compute that it has, say, 200 days cash on hand, but that calculation is based on total unrestricted cash and investments, which usually includes long-term investment pools. A sizable portion of that 200 days may not be accessible on a daily basis.

Recall that during the 2008 liquidity crisis, many hospitals had large portions of their unrestricted investment pools tied up in illiquid investments. When you needed it the most, you couldn’t get it. 2008 was a watershed moment that starkly showed the difference between wealth and liquidity and the growing importance of the latter. Days cash on hand didn’t necessarily mean “on hand.” Many hospitals scrambled for liquidity, which came in the form of expensive bank lines because liquidating equity investments in a down market would come at a huge cost.

Nearly overnight, daily liquidity became a fundamental part of credit analysis.

While the events were different, Covid and Change Healthcare followed the same fact pattern: crisis occurred, cash flow abated, and hospitals scrambled for liquidity, drawing on lines of credit to fund operating needs. Within a quick minute healthcare went “back to the future,” and undoubtedly, there will be another liquidity crisis ahead.

Rating reports now include information on investment allocation and diversification within those investments, and report new ratios such as monthly liquidity to total cash and investments. A hospital with below average days cash on hand or cash-to-debt may receive more attention in the rating report regarding immediately accessible funds.

Irrespective of a high or low cash position or rating category, providing rating analysts with a schedule highlighting where management would turn to when liquidity is needed would be well received. For example, do you draw on lines of credit, hit depository accounts, pause capital, extend payables, or liquidate investments, and in what order? Some health systems are taking this a step further with an in-depth sophisticated analysis to quantify their operating risks and size their liquidity needs accordingly, which we call Strategic Resource Allocation. This analysis would boost an analyst’s confidence in management’s preparedness for the next crisis with the segmenting of true cash “on hand.” It would also help ensure that, when the next crisis arrives, management will know where to turn to maintain liquidity and meet daily cash needs.

Here are 30 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence and pediatric trauma status, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The rating reflects the Minneapolis-based system’s strong balance sheet, robust liquidity position and dominant pediatric market position, Fitch said.

Cincinnati Children’s Hospital Medical Center has an “Aa2” rating and stable outlook with Moody’s. The rating is supported by its national and international reputation in clinical services and research, Moody’s said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by its strong operating risk assessment, leading market position in its immediate service area and strong financial profile,” Fitch said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Mullica Hill, N.J.-based system will return to strong operating cash flows following the operating challenges of 2022 and 2023, as well as the successful integration of Inspira Medical Center of Mannington (formerly Salem Medical Center).

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Nicklaus Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Miami-based system’s position as the “premier pediatric hospital in South Florida with a leading and growing market share,” Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an”AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing positive in a stable service area with good population growth and demand for acute care services, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

St. Elizabeth Medical Center has an “AA” rating and stable outlook with Fitch. The rating reflects the Edgewood, Ky.-based system’s strong liquidity, leading market position and strong financial management, Fitch said.

Stanford Health Care has an “Aa3” rating and positive outlook with Moody’s. The rating reflects the Palo Alto, Calif.-based system’s clinical prominence, patient demand and its location in an affluent and well insured market, Moody’s said.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

On Monday, Fitch Ratings, the New York City-based credit rating agency, released a report predicting that the US not-for-profit hospital sector will see average operating margins reset in the one-to-two percent range, rather than returning to historical levels of above three percent.

Following disruptions from the pandemic that saw utilization drop and operating costs rise, hospitals have seen a slower-than-expected recovery.

But, according to Fitch, these rebased margins are unlikely to lead to widespread credit downgrades as most hospitals still carry robust balance sheets and have curtailed capital spending in response.

The Gist:As labor costs stabilize and volumes return, the median hospital has been able to maintain a positive operating margin for the past ten months.

But nonprofit hospitals are in a transitory period, one with both continued challenges—including labor costs that rebased at a higher rate and ongoing capital restraints—and opportunities—including the increase in outpatient demand, which has driven hospital outpatient revenue up over 40 percent from 2020 levels.

While the future margin outlook for individual hospitals will depend on factors that vary greatly across markets, organizations that thrive in this new era will be the ones willing to pivot, take risks, and invest heavily in outpatient services.

Creating a great rating agency presentation is imperative to telling your story. I’ve probably seen a thousand presentations across the past three decades and I can say without a doubt that a great presentation will find its way into the rating committee. Show me a crisp, detailed, well-organized presentation, and I’ll show you a ratings analyst who walks away with high confidence that the management team can navigate the industry challenges ahead.

During the pandemic, Kaufman Hall recommended that hospitals move financial performance to the top of the presentation agenda. Better presentations chronicled the immediate, “line item by line item” steps management was taking to stop the financial bleeding and access liquidity. We still recommend this level of detail in your presentations, but as many hospitals relocate their bottom line, management teams are now returning to discussing longer-term strategy and financial performance in their presentations.

Beyond the facts and figures, many hospitals ask me what the rating analysts REALLY want to know. Over those one thousand presentations I’ve seen, the presentations that stood out the most addressed the three themes below:

What makes your organization essential? Hospitals maintain limited price elasticity as Medicare and Medicaid typically comprise at least half of patient service revenue, leaving only a small commercial slice to subsidize operations. The ability to negotiate meaningful rate increases with payers will largely rest on the ability to prove why the hospital is a “must-have” in the network. In other words, a health plan that can’t sell a product without a hospital in its network is the definition of essential. This conversation now also includes Medicare Advantage plans as penetration rates increase rapidly across the country. Essentiality may be demonstrated by distinct services, strong clinical outcomes and robust medical staff, multiple access points across a certain geography, or data that show the hospital is a low-cost alternative compared to other providers. Volume trends, revenue growth, and market share show that essentiality. A discussion on essentiality is particularly needed for independent providers who operate in crowded markets.

What makes your financial performance durable? Many hospitals are showing a return to better performance in recent quarters. Showing how your organization will sustain better financial results is important. Analysts will want to know what the new “run rate” is and why it is durable. What are the undergirding factors that make the better margins sustainable? Drivers may include negotiated rate increases from commercial payers and revenue cycle improvements. On the expense side, a well-chronicled plan to achieve operating efficiencies should receive material airtime in the presentation, particularly regarding labor. It is universally understood that high labor costs are a permanent, structural challenge for hospitals, so any effort to bend the labor cost curve will be well received. Management should also isolate non-recurring revenue or expenses that may drive results, such as FEMA funds or 340B settlements. To that end, many states have established new direct-to-provider payment programs which may be meaningful for hospitals. Expect questions on whether these funds are subject to annual approval by the state or CMS. The analysts will take a sharpened pencil to a growing reliance on these funds.

The durability of financial performance should be represented with highly detailed multi-year projections complete with computed margin, debt, and liquidity ratios. Know that analysts will create their own conservative projections if these are not provided, which effectively limits your voice in the rating committee.

We also recommend that hospitals include a catalogue of MTI and bank covenants in the presentation. Complying with covenants are part of the agreement that hospitals make with their lenders, and it is the organization’s responsibility to report how it’s performing against these covenants. General philosophy on headroom to covenants also provides insight to management’s operating philosophy. For example, is it the organization’s goal to have narrow, adequate, or ample headroom to the covenants and why? As the rating agencies will tell you, ratings are not solely based on covenant performance, but all rating factors influence your ability to comply with the covenants.

What makes your capital plan affordable? Every rating committee will ask what the hospital’s future capital needs are and how those capital needs will be supported by cash flow, also known as “capital capacity.” To answer that question, a hospital must understand what it can afford, based on financial projections. Funding sources may require debt, which requires a debt capacity analysis with goals on debt burden, coverage, and liquidity targets. Over the years, better presentations explain the organization’s capital model, outline the funding sources, and discuss management’s tolerance for leverage.

There is always a lot to cover when meeting with the rating agencies and a near endless array of metrics and indicators to provide. As I’ve written before, how you tell the story is as important as the story itself. If you can weave these three themes throughout the presentation, then you will have a greater shot at having your best voice heard in rating committee.

Asexpected, 2023 saw a material increase in downgrades over 2022 while the number of upgrades declined from the prior year. Volume showed favorable growth for many hospitals during 2023 although some indicators remained below pre-pandemic levels. Other hospitals reported a payer mix shift toward more Medicare as the population continued to age and Medicare Advantage plans gained momentum at the expense of commercial revenues. Continued labor challenges drove expense growth, even with many organizations reporting a reduction in temporary labor, as permanent hires pressured salary and benefit expenses. Some of the downgrades reflected pronounced operating challenges that led to covenant violations while others were due to a material increase in leverage viewed to be too high for the rating category.

Figure1: Downgrades at Moody’s, S&P, and Fitch

Here are five key takeaways:

The ratio of downgrades to upgrades reached a high level for all three rating agencies: Moody’s, 3.2-to-1; S&P: 3.8-to-1; and Fitch: 3.5-to-1. In 2022, the ratio crested just above 2.0-to-1 at the highest among the three firms.

Downgrades covered a wide swath of hospitals, ranging from single-site general acute care facilities to academic medical centers as well as large regional and multistate systems. Many of the hospital downgrades were concentrated in New York, Pennsylvania, Ohio, and Washington. All rating categories saw downgrades, although the majority were clustered in the Baa/BBB and lower categories.

Multi-notch downgrades were mainly relegated to ratings that were already deep into speculative grade. Multi-notch upgrades were due to mergers or acquisitions where the debt was guaranteed by or added to the legal borrowing group of the higher rated system.

Upgrades reflected fundamental improvement in financial performance and debt service coverage along with strengthening balance sheet indicators. Like the downgraded organizations, upgraded hospitals and health systems ranged from single-site hospitals to expansive, super-regional systems. Some of the upgrades reflected mergers into higher-rated systems.

The wide span between downgrades to upgrades in 2023 would suggest that the credit gap between highly rated hospitals (say, the “A” or “Aa/AA” category) compared to “Baa/BBB” and speculative grade is widening. That said, given that rating affirmations remain the predominant rating activity annually, the rating agencies reported only a subtle shift in the overall distribution of ratings since the beginning of the pandemic in their panel discussion at Kaufman Hall’s October 2023 Healthcare Leadership Conference.

One person’s prediction for 2024?

It’s a safe bet that downgrades will outpace upgrades given the persistent challenges, although the ratio may narrow if the improvement in current performanceholds. That said, the rating agencies are maintaining mixed views for 2024. S&P and Fitch are sticking with negative and deteriorating outlooks, respectively, while Moody’s has revised its outlook to stable, anticipating that the rough times of 2022 are behind us.

All three rating agencies predict that we are not out of the woods yet when it comes to covenant challenges, especially in the lower rating categories or for those organizations that report a second year of covenant violations.