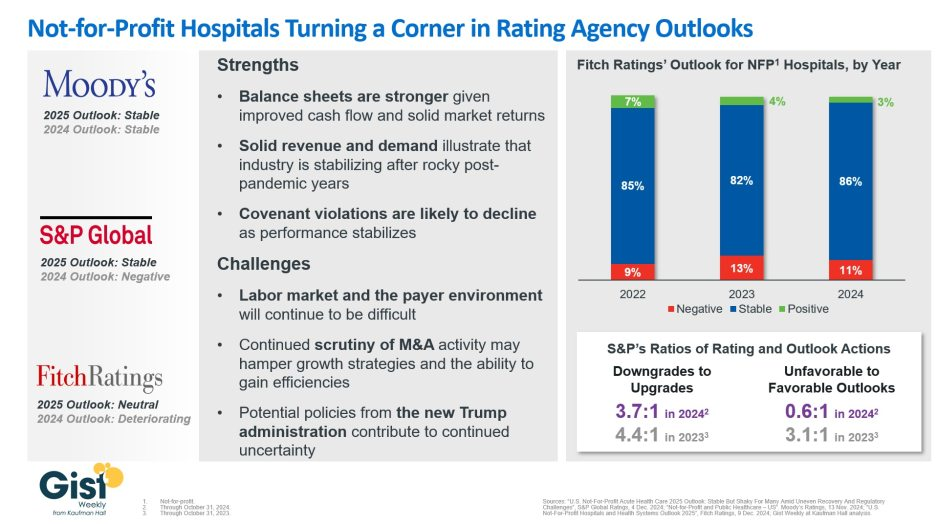

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

For many providers, 2023 provided a return to profitability (albeit at modest levels) following the devastating operating and investment losses experienced in 2022.Kaufman Hall’s National Hospital Flash Report data illustrated generally improving operating margins throughout the year, leveling off at 2.0% in November on a year-to-date basis.

This level of performance is commendable given 2022 and early 2023 margins, although it is still well below the 3% to 4% range which we believe is needed for long-term sustainability in the not-for-profit healthcare world. We may well have reached a point of stability with respect to operating performance, but at a lower level.

The question for hospital and health system leaders is whether this level of operating stability provides sustainability?

From stabilization to normalization

Since the pandemic began in 2020, the progress of recovery has been viewed over three phases: crisis, stabilization, and normalization. In last year’s outlook, we noted that we were in the midst of a potentially multi-year stabilization phase, which would continue to be marked with volatility—including ongoing labor market dislocations, inflationary pressures, and restrictive monetary policies. As we enter 2024, there are signs that we are now at the bridge between stabilization and normalization (Figure 1).

Figure 1: The Three Phases of Recovery from the Covid Pandemic

“The question for hospital and health system leaders is whether that level of stability provides sustainability?”

These signs include evidence that the first two indicators for normalization—a recalibrated or stabilized workforce environment and a return from an erratic interest rate environment—are coming into place. In our 2023 State of Healthcare Performance Improvement survey, respondents indicated that the spike in contract labor utilization that has been a dominant factor in operating expense increases was subsiding. Sixty percent of respondents said that utilization of contract labor was decreasing, and 36% said it was holding steady. Only 4% noted an increase in contract labor usage. Overall employee cost inflation seems to be subsiding as well: for all three labor categories in our survey (clinical, administrative, and support services), more organizations were able to hold salary increases to the 0% – 5% range in 2023 than in 2022.

There is good news on the interest rate front as well. After a series of rate increases in 2023, the Federal Reserve has held steady the last six months and has signaled rate cuts in 2024. Inflation has cooled markedly (albeit not yet at target levels), and employment rates have held steady. The Fed may have achieved a “soft landing” that satisfies its dual mandate of stable prices and maximum sustainable employment. Borrowing costs for not-for-profit hospital issuers have declined nearly 100 basis points in the last two months and we are expecting a return to more normal issuance levels in the first half of 2024.

There are other indications of normalization, including in the rating agencies’ outlooks for 2024. Regardless of the headline, all saw significant improvement in healthcare performance 2023.

The final answer to the question of whether the healthcare industry is entering the normalization phase likely will hinge on the last two indicators. Will we see a return of normalized strategic capital investments, and will we see a revival of strategic initiatives driving the core business (perhaps newly imagined)?

In effect, are health care systems simply surviving or are they thriving?

Looking forward, several factors could either bolster or undermine healthcare leaders’ confidence and willingness to resume a more normal level of investment in both capital needs and strategic growth. These include:

Politics and the 2024 elections. When North Carolina—a state that has traditionally leaned “red”—decided to opt into the Affordable Care Act’s (ACA’s) Medicaid expansion in 2023, it seemed that political debates over the ACA might be in the rearview mirror. But last November, former president Trump—currently the leading candidate for the Republican presidential nomination after strong wins in the Iowa caucuses and New Hampshire primary—indicated his intent to replace the ACA with something else. President Biden is now making protection and expansion of the ACA a key part of his 2024 campaign. What had appeared to be a settled issue may be a significant point of contention in the 2024 presidential election and beyond.

Although we do not anticipate any significant healthcare-related legislation in advance of the 2024 elections, healthcare leaders should be prepared for renewed attention to the costs of government-funded healthcare programs leading up to and following the elections. The national debt has increased rapidly over the past 20 years, tripling from $11 trillion in 2003 to $33 trillion in 2023. If the deficit and national debt become an important issue in the election, a move toward a balanced budget—akin to the Balanced Budget Act of 1997—post election could lead to further cuts to Medicare and Medicaid.

Temporary relief payments. Health systems continue to receive one-time cash infusions through the 340B settlement, Federal Emergency Management Agency (FEMA) payments and other governmental programs. Approximately 1,600 hospitals have or will be receiving a lump-sum payment to compensate them for a change in the Department of Health & Human Services’ (HHS’s) reimbursement rates for the 340B program from 2018 to 2022, which was ruled unlawful by the Supreme Court in a 2022 decision. The total amount to be distributed is approximately $9 billion and began hitting bank accounts in January 2024.

But what the right hand giveth, the left hand taketh away. Budget neutrality requirements will force HHS to recoup this offset—amounting to approximately $7.8 billion—which it will do by reducing payments for non-drug items and services to all Outpatient Prospective Payment System (OPPS) providers by 0.5% until the offset has been fully recouped, beginning in calendar year 2026. HHS estimates that this process will take approximately 16 years. Is this a harbinger of lower payments on other key governmental programs?

Many hospitals also continue to receive Covid-related payments from FEMA for expenses occurred during the pandemic. In addition, state supplemental payments—especially under Medicaid managed care and fee-for-service programs—are providing some relief. The Centers for Medicare & Medicaid Services has issued a proposed rule, however, that would limit states’ use of provider-based funding sources, such as provider taxes, and cap the rate of growth for state-directed payments.

As all of these payment programs dry up over the next few years, hospitals will need to replace the revenue and/or get leaner on the expense side in order to maintain today’s level of performance.

The hollowing of the commercial health insurance market. Our colleague, Joyjit Saha Choudhury, recently published a blog on the hollowing of the commercial health insurance market, driven by long-term concerns over the affordability of healthcare. While volumes have been recovering to pre-pandemic levels, this hollowing threatens the loss of the most profitable volumes and will pressure hospitals and health systems to create and deliver value, compete for inclusion in narrow networks, and develop more direct relationships with the employer community.

Related, the growing penetration of Medicare Advantage plans is reducing the number of traditional Medicare beneficiaries. Many CFOs report that these programs can be the most difficult with which to work given their high denial rates and required pre-authorization rates. A new rule requiring insurers to streamline prior authorizations for Medicare Advantage, Medicaid, and Affordable Care Act plans may help alleviate this issue; however, it will be incumbent upon management teams to stay ahead of them. Aging demographics are also reducing the percentage of commercially insured patients for many hospitals and health systems, further exacerbating the problem. This combination of fewer commercial patients (who often subsidize governmental patients) and more pressure on receiving the duly owed commercial revenue threatens to be an ongoing headache for management teams.

Ongoing impact of the Baby Boom generation. Despite the good news on inflation—and indications that the Fed may begin lowering interest rates in 2024—the economy is by no means out of the woods yet. The Baby Boom generation, which holds more than 50% of the wealth in the U.S. and is seemingly price agnostic, still has many years of spending ahead, in healthcare and general purchasing. This will likely continue to pressure inflation, especially in the healthcare sector, where demand will continue to grow. As the generation starts to shrink, the resulting wealth transfer will be the largest ever in our country’s history and have profound (and unforeseen) consequences on the overall economy and healthcare in general.

In sum, these other factors will continue to affect the sector (both positively and negatively) and require health system management teams to navigate an everchanging world. While many signs point toward short-term relief, the longer-term challenges persist. Improvements in the short term may, however, provide the opportunity to reposition organizations for the future.

How hospitals and health systems should respond

Healthcare leaders should view ongoing uncertainty in the political and economic climate as a tailwind as much as a headwind. This uncertainty, in other words, should be a motivation to put in place strategies that will buffer healthcare organizations from potential bumps in the road ahead. Setting balance sheet strategy should be a part of an organization’s planning process.

How an organization sets that strategy, measures its performance, and makes improvements will set apart top-performing organizations.

Although heightened debt issuance early in 2024 signals a return for many systems to a climate of investment, there is still limited energy around strategy and debt conversations in many boardrooms, especially in those organizations where financial improvement continues to lag. The last two years have illustrated that hospitals and health systems will not be able to cut their way to profitability. Lackluster performance cannot and will not improve without some level of strategic change, whether it is through market share gains, payer mix shift, or operational improvements. This strategic change requires investment and investment requires capital. Capital can be obtained in many forms—whether through growth in capital reserves, improved cash flow, or new debt issuance—but is essential for change. Reengaging in conversations about strategy and growth should be an imperative in 2024 and will require reexamining how that growth is funded.

Healthcare leaders should engage their partners as they continue or refocus on:

Changing the conversation from debt capacity to capital capacity. Management teams need to determine what they can afford to spend on capital if the new normal of cash flow will be constrained going forward. Capital capacity is and should be agnostic to the source of that capital, such as debt, cash flow from operations, or liquidity reserves. Healthcare leaders must focus on what they can spend, before deciding how to fund that spending. The conversation will need to balance investment for the future with maintaining key credit metrics in the short term.

Conducting a capitalization analysis. Separate but related to the previous entry, how much leverage should your organization have relative to its overall capitalization? Ostensibly, many organizations have been paying principal while curtailing borrowing needs, so capitalization may have improved. While that may be the case, many organizations have depleted reserves and/or experienced investment losses that have reduced capitalization. Understanding where the organization stands is an essential next step.

Evaluating surplus return. Consider surplus return as investment income net of interest expense. Organizations should evaluate their ability to reliably generate both operating cash flow and net surplus. How an organization’s balance sheet is positioned to generate returns and manage risk will be a critical success factor.

Focusing on the metrics that matter. These include operating cashflow margin, cash to debt, debt to revenue, and days cash on hand. As key metrics for rating analysts and investors continue to evolve, management teams need to make sure they are focused on the correct numbers. The discussion should be dually focused on ensuring adequate-to-ample headroom to basic financial covenants as well as a comparison to key medians and peers. Strong financial planning will address how these metrics can be improved over time through synergies, growth, and diversification strategies.

Although it has been a difficult few years, hospitals and health systems seem to have moved onto a more stable footing over the last twelve months. In order to build upon the upward trajectory, now is the time to harness strategy, planning, and investment to move organizations from stability to sustainability.

Here are 68 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings, Moody’s Investors Service and S&P Global in 2023.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating reflects the Altamonte Springs, Fla.-based system’s strong financial profile, characterized by still-adequate liquidity and moderate leverage, typically strong and highly predictable profitability, Fitch said.

Advocate Aurora Health has an “AA” rating and stable outlook with Fitch. The Downers Grove, Ill.- and Milwaukee-based system’s rating reflects a very strong financial profile in the context of an already sound market position and geographic reach that was enhanced after merging with Charlotte, N.C.-based Atrium Health, Fitch said.

AnMed Health has an “AA-” rating and stable outlook with Fitch. The Anderson, S.C.-based system has maintained strong performance through the COVID-19 pandemic and current labor market pressures, Fitch said.

AtlantiCare has an “AA-” rating and stable outlook with Fitch. The Atlantic City, N.J.-based system has a strong balance sheet with solid liquidity position and low debt burden, Fitch said.

Atrium Health has an “AA-” rating and stable outlook with S&P Global. The Charlotte, N.C.-based system’s rating reflects a robust financial profile, growing geographic diversity and expectations that management will continue to deploy capital with discipline.

Banner Health has an “AA-” and stable outlook with Fitch. The Phoenix-based system’s rating highlights the strength of its core hospital delivery system and growth of its insurance division, Fitch said.

BayCare Health System has an “AA” rating and stable outlook with Fitch. The Tampa, Fla.-based system’s rating reflects its excellent financial profile supported by its leading market position in a four-county area and the ability to sustain a solid operating outlook in the face of inflationary sector headwinds, Fitch said.

Bayhealth has an “AA” rating and stable outlook with Fitch. The rating reflects the strength of the Dover, Del.-based system’s market positions and the stability of its financial profile, Fitch said.

Beacon Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of the South Bend, Ind.-based system’s balance sheet, the rating agency said.

Berkshire Health has an “AA-” rating and stable outlook with Fitch. The Pittsfield, Mass.-based system has a strong financial profile, solid liquidity and modest leverage, according to Fitch.

Bryan Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Lincoln, Neb., system’s leading and growing market position as a regional referral center with strong expense flexibility and cash flow, Fitch said.

Cape Cod Healthcare has an “AA-” and stable outlook with Fitch. The Hyannis, Mass.-based system’s rating reflects a dominant market position in its service area and historically solid operating results, the rating agency said.

Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area, Fitch said.

CaroMont Health has an “AA-” rating and stable outlook with S&P Global. The Gastonia, N.C.-based system has a healthy financial profile and robust market share in a competitive region.

CentraCare has an “AA-” rating and stable outlook with Fitch. The St. Cloud, Minn.-based system has a leading market position, and its management’s focus on addressing workforce pressures, patient access and capacity constraints will improve operating margins over the medium term, Fitch said.

Children’s Health System of Texas has an “AA” and stable outlook with Fitch. The Dallas-based system’s rating reflects its solid operating performance in 2022, resulting from inpatient, outpatient and surgical volume growth, as well as one-time support from pandemic-era stimulus funding, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The Minneapolis-based system’s broad reach within the region continues to support long-term sustainability as a market leader and preferred provider for children’s health care, Fitch said.

Concord (N.H.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of Concord’s leverage and liquidity assessment and Fitch’s assessment that two recently acquired hospitals will be strategically and financially accretive.

Cone Health has an “AA” rating and stable outlook with Fitch. The rating reflects the expectation that the Greensboro, N.C.-based system will gradually return to stronger results in the medium term, the rating agency said.

Cottage Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Santa Barbara, Calif.-based system’s leading market position and broad reach in a service area that exhibits modest population growth but consistently high demand for acute care services, Fitch said.

Deaconess Health System has an “AA” rating and stable outlook with Fitch. The Evansville, Ind.-based system demonstrated operating cost flexibility through the pandemic and recent labor and inflationary pressure, Fitch said.

Duke University Health System has an “AA-” rating and stable outlook with Fitch. Fitch projects the Durham, N.C.-based system will benefit from the integration of the former Private Diagnostic Clinic and from North Carolina’s recently enacted Medicaid expansion and Healthcare Access and Stabilization Program.

El Camino Health has an “AA-” rating and stable outlook with Fitch. The Mountain View, Calif.-based system has a history of generating double-digit operating EBITDA margins, driven by a solid market position that features strong demographics and a very healthy payer mix, Fitch said.

Franciscan Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Mishawaka, Ind.-based system’s strong and stable balance sheet, favorable payer mix, and leading or near leading market share in its service areas, Fitch said.

Froedtert Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s maintenance of a strong, albeit compressed, operating performance and a robust liquidity position, Fitch said.

Geisinger has an “AA-” credit rating and stable outlook with S&P. The Danville, Pa.-based system enjoys strong integration and value-based care experience, the ratings agency said.

Hackensack Meridian Health has an “AA-” rating and stable outlook with Fitch. The Edison, N.J.-based system’s rating is supported by its strong presence in its large and demographically favorable market, Fitch said.

Harris Health System has an “AA” rating and stable outlook with Fitch. The Houston-based system has a “very strong” revenue defensibility, primarily based on the district’s significant taxing margin that provides support for operations and debt service, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by a leading market position in its immediate area and very strong financial profile, Fitch said.

Intermountain Health has an “Aa1” rating and stable outlook with Moody’s. The Salt Lake City-based system’s rating is reflected by its distinctly leading market position in Utah and strong absolute and relative cash levels, Moody’s said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The Mullica Hill, N.J.-based system’s rating reflects its leading market position in a stable service area and a large medical staff supported by a growing residency program, Fitch said.

IU Health has an “AA” rating and stable outlook with Fitch. The Indianapolis-based system has a long track record of strong operating margins and an overall credit profile that is supported by a strong balance sheet, the rating agency said.

Lucile Packard Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the Palo Alto, Calif.-based hospital’s role as a nationally known, leading children’s hospital, Fitch said. It also benefits from resilient clinical volumes and a solid market position, as well as its relationship with Stanford University and Stanford Health Care.

Kaiser Permanente has an “AA-” and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by a strong financial profile, which is maintained despite a challenging operating environment in fiscal year 2022.

Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The Rochester, Minn.-based system’s credit profile characterized by its excellent reputations for clinical services, research and education, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The Grand Blanc, Mich.-based system has a leading market position over a broad service area covering much of Michigan and a track-record of profitability despite sector-wide market challenges in recent years, Fitch said.

McLeod Regional Medical Center has an “AA-” rating and stable outlook with Fitch. The rating reflects the Florence, S.C.-based system’s very strong financial profile assessment, historically strong operating EBITDA margins and its solid market position, Fitch said.

MemorialCare has an “AA-” rating and stable outlook with Fitch. The rating reflects the Fountain Valley, Calif.-based system’s strong financial profile and excellent leverage metrics despite its weaker operating performance, Fitch said.

Memorial Sloan-Kettering Cancer Center has an “AA” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the New York City-based system’s national and international reputation as a premier cancer hospital will continue to support growth in its leading and increasing market share for its specialty services.

Midland (Texas) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Midland’s exceptional market position and limited competition for acute-care services and growing outpatient services, Fitch said.

Monument Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Rapid City, S.D.-based system’s dominant inpatient market share and excellent market position across its geographically broad service area, Fitch said.

Munson Healthcare has an “AA” rating and stable outlook with Fitch. The rating reflects the strength of the Traverse City, Mich.-based system’s market position and its leverage and liquidity profiles.

MyMichigan Health has an “AA-” rating and stable outlook with Fitch. The Midland-based system reflects the system’s market position as the largest provider of acute care services and its leading market position in a sizable geographic area covering 25 counties in mid and northern Michigan, the rating agency said.

North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The Tupelo-based system’s rating reflects its very strong cash position and strong market position, Fitch said.

NewYork-Presbyterian Hospital has an “AA” rating and stable outlook with Fitch. The rating reflects the New York City-based system’s market position as one of New York’s major academic healthcare systems with a reputation that extends beyond the region, Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The Winston-Salem, N.C.-based system has a highly competitive market share in three separate North Carolina markets, Fitch said, including a leading position in Winston-Salem (46.8 percent) and second only to Atrium Health in the Charlotte area.

NYC Health + Hospitals has an “AA-” rating with Fitch. The New York City system is the largest municipal health system in the country, serving more than 1 million New Yorkers annually in more than 70 patient locations across the city, including 11 hospitals, and employs more than 43,000 people.

OhioHealth has an “AA+” rating and stable outlook with Fitch. The Columbus-based system has an exceptionally strong credit profile, very favorable leverage metrics and reliably strong profitability, Fitch said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The system’s upgrade from “A+” reflects the continued strength of the health system’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market, Fitch said.

Phoenix Children’s Hospital has an “AA-” and stable outlook with Fitch. The rating reflects its position as a distinct leading provider of pediatric health services in a growing primary service area, Fitch said.

The Queen’s Health System has an “AA” rating and stable outlook with Fitch. The Honolulu-based system’s rating reflects its leading state-wide market position, historically strong operating performance and diverse revenue streams, the rating agency said.

Rush System for Health has an “AA-” and stable outlook with Fitch. The Chicago-based system has a strong financial profile despite ongoing labor issues and inflationary pressures, Fitch said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The Cape Girardeau, Mo.-based system enjoys robust operational performance and a strong local market share as well as manageable capital plans, Fitch said.

Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The system has a “very strong” financial profile and a leading market share position, Fitch said.

Sanford Health has an “AA-” rating and stable outlook with Fitch. The Sioux Falls, S.D.-based system rating reflects its leading inpatient market share positions in multiple markets and strong overall financial profile, the rating agency said.

Stanford Health Care has an “AA” rating and stable outlook with Fitch. The Palo Alto, Calif.-based system’s rating is supported by its extensive clinical reach in the greater San Francisco and Central Valley regions and nationwide/worldwide destination position for extremely high-acuity services, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system has a strong financial profile, multi-state presence and scale, with solid revenue diversity, Fitch said.

St. Clair Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Pittsburgh-based system’s strong financial profile assessment, solid market position and historically strong operating performance, the rating agency said.

St. Tammany Parish Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the Covington, La.-based system’s strong operating risk assessment and very strong financial profile supported by consistently robust operating cash flows, Fitch said.

Texas Medical Center has an “AA-” rating and stable outlook with Fitch. The rating reflects the Houston-based system’s profitable service enterprise, its long and collaborative relationship with strong university, nonprofit and medical industry partners, and sizable financial reserve levels, Fitch said.

TriHealth has an “AA-” rating and stable outlook with Fitch. The Cincinnati-based system’s rating reflects its broad reach, high-acuity services and stable market position in a highly fragmented and competitive market, Fitch said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s broad and growing reach for high-acuity services and the considerable benefits it receives from its high degree of integration with the University of Chicago, Fitch said.

UCHealth has an “AA” rating and stable outlook with Fitch. The Aurora, Colo.-based system’s margins are expected to remain robust, and the operating risk assessment remains strong, Fitch said.

University of Kansas Health System has an “AA-” rating and stable outlook with S&P Global. The Kansas City-based system has a solid market presence, good financial profile and solid management team, though some balance sheet figures remain relatively weak to peers, the rating agency said.

Virtua Health has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Marlton, N.J.-based system’s leading market position in a stable service area and the successful integration of the Lourdes Health System, Fitch said.

VHC Health has an”AA-” rating and stable outlook with Fitch. The Arlington-based system has demonstrated strong operating cost flexibility, growth in high acuity service lines and an expanding outpatient footprint, Fitch said.

WellSpan Health has an “Aa3” rating and stable outlook with Moody’s. The York, Pa.-based system has a distinctly leading market position across several contiguous counties in central Pennsylvania, and management’s financial stewardship and savings initiatives will continue to support sound operating cash flow margins when compared to peers, Moody’s said.

Willis-Knighton Health System has an “AA-” rating and stable outlook with Fitch. The Shreveport, La.-based system has a “dominant inpatient market position” and is well positioned to manage operating pressures, Fitch said.

Here is a summary of recent credit downgrades and outlook revisions for hospitals and health systems.

The downgrades and downward revisions reflect continued operating challenges many nonprofit systems are facing, with multiyear recovery processes expected.

Downgrades:

Yale New Haven (Conn.) Health: Operating weakness and elevated debt contributed to the downgrade of bonds held by Yale New Haven (Conn.) Health, Moody’s said May 5. The bond rating slipped from “Aa3” to “A1,” and the outlook was revised to stable from negative.

The system saw a second downgrade as its default rating and that on a series of bonds were revised one notch to “A+” from “AA-” amid continued operating woes, Fitch said June 28.

Not only have there been three straight years of such challenges, but the operating environment continues to cast a pall into the second quarter of the current fiscal year, Fitch said.

UC Health (Cincinnati): The system was downgraded on a series of bonds, Moody’s said May 10.

The move, which involved a lowering from a “Baa2” to “Baa3” grade, refers to such bonds with an overall value of $580 million.

In February, UC Health suffered a similar downgrade from “A” to “BBB+” on its overall rating and on some bonds because of what S&P Global termed “significantly escalating losses.”

UNC Southeastern (Lumberton, N.C.): The system, which is now part of the Chapel Hill, N.C.-based UNC Health network, saw its ratings on a series of bonds downgraded to “BB” amid operating losses and sustained weakness in its balance sheet, S&P Global said June 23.

While UNC Southeastern reported an operating loss of $74.8 million in fiscal 2022, such losses have continued into fiscal 2023 with a $15 million loss as of March 31, S&P Global said. The system had earlier been placed on CreditWatch but that was removed with this downgrade.

Butler (Pa.) Health: The system, now merged with Greensburg, Pa.-based Excela Health to form Independence Health System, saw its credit rating downgraded significantly, falling from “A” to “BBB.”

The move reflects continued operating challenges and low patient volumes, Fitch said June 26.

Such operating challenges, including low days of cash on hand, could result in potential default of debt covenants, Fitch warned.

Outlook revisions:

Redeemer Health (Meadowbrook, Pa.): The system had its outlook revised to negative amid “persistent operating losses,” Fitch Ratings said June 14. The health system, anchored by a 260-bed acute care hospital, reported a $37 million operating loss in the nine months ending March 31, Fitch said.

Thomas Jefferson University (Philadelphia): The June 9 downward revision of its outlook, which includes both the health system and the university’s academic sector, was due to sustained operating weakness, S&P Global said.

IU Health (Indianapolis): While it saw ratings affirmed at “AA,” the 16-hospital system had its outlook downgraded amid persistent inflationary pressures and large capital expense, Fitch said May 31.

UofL Health (Louisville, Ky.): Slumping operating income and low days of cash on hand (42.8 as of March 31) contributed to S&P Global revising its outlook for the six-hospital system to negative May 24.

The healthcare financings that came in the past couple of weeks generally did well. Maturities seemed to do better than put bonds, and it remains important to pay attention to couponing and how best to navigate a challenging yield curve. But these are episodic indicators rather than trends, given that the scale of issuance remains muted. Other capital markets—like real estate—are becoming more active and offer competitive funding and different credit considerations relative to debt market options. Credit management continues to be the main driver of low external capital formation, but those looking for outside funding should spend time up front considering the full array of channels and structures.

This Part of the Crisis

And now it’s official. After JPMorgan acquired First Republic Bank—with a whole lot of help from the Federal Deposit Insurance Corporation—CEO Jamie Dimon declared, “this part of the crisis is over.” Not sure regional bank shareholders would agree, but from Mr. Dimon’s perspective the biggest bank got bigger, which made it a good day.

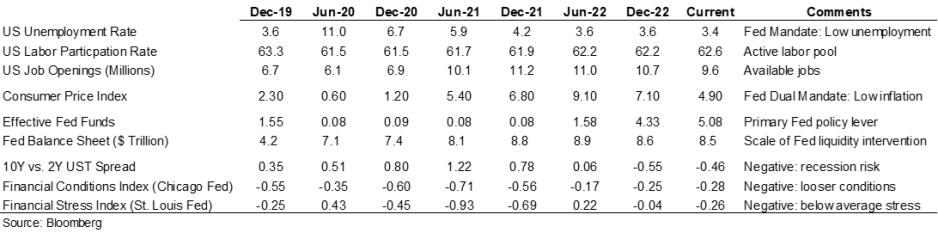

Last week the Federal Reserve raised rates another 25 basis points and the expectation (hope) seems to be that the Fed has reached the peak of its tightening cycle or will at least pause to see if constrictive forces like higher rates and regional bank balance sheet deflation slow activity enough to bring inflation back to the 2.0% Fed target. Assuming this is a pause point, it makes sense to check in on a few economic and market indicators.

Inflation is improving, although it remains well above the Fed’s 2.0% target range, and there are other indicators (like labor participation and unemployment) that have recovered some of the ground lost in 2020. But the weird part remains that this all seems quite civilized. To some, the Treasury curve spread continues to suggest a recession is looming, but in my neighborhood workers are still in short supply, restaurants are busy, and contractors are booked well into the future. Today’s ~3.36% 10-year Treasury rate is less than 100 basis points higher than the average since the start of the Fed interventionist era in 2008 and a whopping 257 basis points lower than the average since 1965. Think about how much capital has been raised in market environments much worse than now (including most of the modern-day healthcare inpatient infrastructure). Again, the main culprit in retarded capital formation is institutional credit management concerns rather than the funding environment.

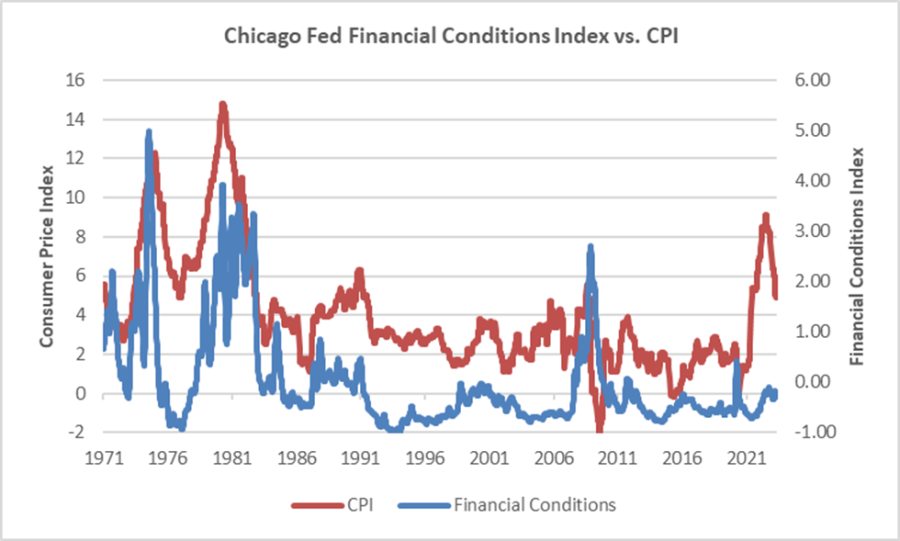

The major fallout from the Fed’s recent anti-inflation efforts seems concentrated with financial intermediaries rather than consumers (or workers), and the financial intermediary stress the Fed is relying on to help curb economic activity is grounded in their own balance sheet management decisions rather than deteriorating loan portfolios. We’ve looked at this before, but it bears repeating that in the “great inflation” of the 1970s, the Chicago Fed’s Financial Conditions Index reached its highest recorded points (higher means tighter than average conditions) and in this most recent inflationary cycle, that same index has remained consistently accommodative. Can you wring inflation out of a system while retaining relatively accommodative financial conditions? Which begs the question of whether any Fed pause is more about shifting priorities: downgrading the inflation fight in favor of moderating the financial intermediary threat? We might be living a remake of the 1970s version of stubborn inflation, which means that all the attendant issues—rolling volatility across operations, financing, and investing—might be sticking around as well.

Meanwhile, somewhere out in the Atlantic the debt ceiling storm is forming. Who knows whether it will make landfall as a storm or a hurricane, but it does remind us that the operative portion of the Jamie Dimon quote noted above is this part of the crisis is over. The next part of the long saga that is about us climbing out of a deep fiscal and monetary hole will roll in and new variations of the same central challenge will emerge for healthcare leaders.

A Healthcare Makeover

Ken Kaufman has been advancing the idea that healthcare needs a “makeover” to align with post-COVID realities. Look for a piece from him on this soon, but the thesis is that reverting to a 2019 world isn’t going to happen, which means that restructuring is the only option. The most recent National Hospital Flash Report suggests improving margins, but they remain well below historical norms and the labor part of the expense equation is structurally higher. Where we are is not sustainable and waiting for a reversion is a rapidly decaying option.

My contribution to Ken’s argument is to reemphasize that balance sheet is the essential (only) bridge between here and a restructured sector and the journey is going to require very careful planning about how to size, position, and deploy liquidity, leverage, and investments. Of course, the central focus will be on how to reposition operations. But if organic cash generation remains anemic, the gap will be filled by either weakening the balance sheet (drawing down reserves, adding leverage, or adopting more aggressive asset allocation) or by partnering with organizations that have the necessary resources.

Organizations reach the point of greatest enterprise risk when the scale of operating challenges outstrips the scale of balance sheet resources. Missteps are manageable when the imbalance is the product of rapid growth but not when it is the result of deflating resources. If the core imperative is to remake operations, the co-equal imperative is continuously repositioning the balance sheet to carry you from here to whatever defines success.

Credit rating downgrades for several hospitals and health systems were tied to cash flow issues in recent months.

The following seven hospital and health system credit rating downgrades occurred since February:

1. Jupiter (Fla.) Medical Center — lowered in June from “BBB+” to “BBB” (Fitch Ratings) “The ‘BBB’ rating reflects JMC’s increased leverage profile with the issuance of $150 million in additional debt to fund various campus expansion and improvement projects,” Fitch said. “While favorable population growth in the service area and demonstrated demand for services in an increasingly competitive market justify the overall strategic plan and project, the additional debt weakens JMC’s financial profile metrics and increases the overall risk profile.”

2. ProMedica (Toledo, Ohio) — lowered in May from “BBB-” to “BB+” (Fitch Ratings) “The long-term ‘BB+’ rating and the assigned outlook to negative on ProMedica Health System’s debt reflects the system’s significant financial challenges as result of continued pressure of the coronavirus pandemic and escalating expenses, with ProMedica reporting a $252 million operating loss that follows several years of weak performance,” Fitch said.

3. Providence (Renton, Wash.) — lowered in April from “Aa3” to to “A1” (Moody’s Investors Service); lowered from “AA-” to “A+” (Fitch Ratings) “The downgrade to ‘A1’ is driven by the disaffiliation with Hoag Hospital, and the expectation that weaker operating, balance sheet, and debt measures will continue for the time being,” Moody’s said.

4. San Gorgonio Memorial Healthcare District (Banning, Calif.) — lowered in May from “Ba1” to “Ba2” (Moody’s Investors Service) “The downgrade to Ba2 reflects the district’s tenuous cash position and weak finances that have contributed to difficulty in securing a bridge loan financing for liquidity needs pending the delayed receipt of approximately $8 million to $9 million in intergovernmental transfers beyond the end of the fiscal year,” Moody’s said.

5. Willis-Knighton Medical Center (Shreveport, La.) — lowered in March from “A1” to “A2” (Moody’s Investors Service) “The downgrade to A2 reflects expectations that Willis-Knighton will continue to face challenges in achieving budgeted operating cash flow margins due to heightened wage pressures and volume softness,” Moody’s said.

6. OU Health (Oklahoma City) — lowered in March from “Baa3” to “Ba2” (Moody’s Investors Service) “The magnitude of the downgrade to Ba2 reflects projected cashflow in fiscal 2022 that will be materially below prior expectations, from an escalation of labor costs, and reliance on a financing to avoid a further decline in already weak liquidity and potential covenant breach,” Moody’s said. “Also, the rating action reflects execution risk given a prolonged period of management turnover with several key positions unfilled or filled with interim leaders, a governance consideration under Moody’s ESG classification.”

7. Catholic Health System (Buffalo, N.Y.) — lowered in February from “Baa2” to “B1” (Moody’s Investors Service) “The downgrade to ‘B1’ anticipates minimal cashflow and a further significant decline in liquidity this year, following material losses in fiscal 2021 from a 40-day labor strike and the disproportionately severe impact of the pandemic, both social risks under Moody’s ESG classification,” the credit rating agency said.

Moody’s Investors Service has downgraded the ratings on Providence’s revenue bond debt to “A1” from “Aa3.”

“The downgrade to ‘A1’ is driven by the disaffiliation with Hoag Hospital, and the expectation that weaker operating, balance sheet, and debt measures will continue for the time being,” Moody’s said in an April 5 release.

Renton, Wash.-based Providence and Newport Beach, Calif.-based Hoag ended their affiliation Jan. 31. The two organizations cut ties at a time when Providence is facing several challenges, including operating pressures, variable utilization and reliance on temporary labor, Moody’s said.

The “A1” rating and stable outlook also reflect Providence’s strengths, including a large service area, a large revenue base of more than $25 billion and a leading market share in all of its markets.

Moody’s said it expects Providence to continue to grow its operating platform and generate additional revenue growth.

Here are 14 health systems with strong operational metrics and solid financial positions, according to reports from Fitch Ratings, Moody’s Investors Service and S&P Global Ratings.

1. Advocate Aurora Health has an “Aa3” rating and positive outlook with Moody’s. The health system, which has dual headquarters in Milwaukee and Downers Grove, Ill., has a leading market share in two regions and strong financial discipline, Moody’s said. The credit rating agency said it expects Advocate Aurora Health’s operating cash flow margins to return to pre-pandemic levels.

2. Pinehurst, N.C.-based FirstHealth of the Carolinas has an “AA” rating and stable outlook with Fitch. The health system has a strong financial profile and stable operating performance, despite disruption from the COVID-19 pandemic, Fitch said. The health system’s revenue in the first quarter of fiscal 2021 rebounded to levels close to historical trends, according to the credit rating agency.

3. Indianapolis-based Indiana University Health has an “Aa2” rating and stable outlook with Moody’s and an “AA” rating and positive outlook with Fitch. Cost controls and patient volume will help the system sustain strong margins and liquidity, Moody’s said.

4. Rapid City, S.D.-based Monument Health has an “AA-” rating and stable outlook with Fitch. The health system has solid operating margins that Fitch expects to remain stable over the near term. Monument Health’s operating margins will continue to support liquidity growth and capital spending levels, the credit rating agency said.

5. Chicago-based Northwestern Medicine has an “Aa2” rating and stable outlook with Moody’s, and an “AA+” rating and stable outlook with S&P. The system’s consolidated operating model will allow it to maintain a strong financial position while effectively executing strategies, Moody’s said. The credit rating agency expects Northwestern Medicine to expand its prominent market position in the broader Chicago region because of its strong brand and affiliation with Northwestern University’s Feinberg School of Medicine.

6. Renton, Wash.-based Providence has an “AA-” rating and stable outlook with Fitch and an “Aa3” rating and stable outlook with Moody’s. Fitch said Providence has a long-term strategic advantage over most of its peers because it has invested heavily in developing technology in recent years, and the system’s plan to transform healthcare delivery through the use of data and technology has been undeterred through the COVID-19 pandemic. Fitch said it expects Providence’s cash flow margins to be close to 7 percent in the coming years.

7. Livingston, N.J.-based RWJBarnabas Health has an “Aa3” rating and stable outlook with Moody’s. Moody’s said it expects RWJBarnabas, the largest integrated academic health system in New Jersey, to see near-term revenue growth and to execute on several strategic fronts while achieving targeted financial performance.

8. Broomfield, Colo.-based SCL Health has an “AA-” rating and stable outlook with Fitch and an “Aa3” rating and stable outlook with Moody’s. The health system has consistently improved its liquidity levels and has a long track record of exceptional operations, Fitch said. SCL Health is well positioned for change in the healthcare sector because it has built up cash reserves over time, according to the credit rating agency.

9. San Diego-based Scripps Health has an “Aa3” rating and stable outlook with Moody’s. The health system has ample liquidity coverage, an extensive footprint and strong brand and market share within San Diego County, Moody’s said. The credit rating agency said it expects Scripps to weather current operating challenges and to grow operating cash flow over the long term.

10. Norfolk, Va.-based Sentara Healthcare has an “Aa2” rating and stable outlook with Moody’s. The health system has strong margins, and Moody’s said it expects the system to maintain a strong financial position and balance sheet.

11. Arlington-based Texas Health Resources has an “Aa2” rating and stable outlook with Moody’s. The health system has a strong cash position, which will be boosted by favorable investment gains and bond proceeds, Moody’s said. Based on performance in the second quarter of this year, Moody’s expects Texas Health Resources’ patient volume and operating cash flow margins to recover to pre-COVID-19 levels.

12. Iowa City-based University of Iowa Hospitals & Clinics has an “Aa2” rating and stable outlook with Moody’s. The credit rating agency said it expects the system to maintain strong operating performance and cash flow. The system benefits as the only academic medical center in Iowa, according to Moody’s.

13. Des Moines, Iowa-based UnityPoint Health has an “AA-” rating and stable outlook with Fitch. The system has strong leverage metrics, and it benefited from strong market returns during the pandemic. The system’s days with cash on-hand increased to 285 days at the end of 2020, up from 231 days at the end of 2019, according to the credit rating agency.

14. Kansas City-based University of Kansas Health System has an “AA-” rating and stable outlook with Fitch. The health system has solid operating results and has sustained significant revenue growth, Fitch said. The system’s profitability dipped in fiscal year 2020 because of the COVID-19 pandemic, but its profitability rebounded in fiscal year 2021, according to the credit rating agency.

Here are 18 health systems with strong operational metrics and solid financial positions, according to reports from Fitch Ratings, Moody’s Investors Service and S&P Global Ratings.

1. Altamonte Springs, Fla.-based AdventHealth has an “Aa2” rating and stable outlook with Moody’s and an “AA” rating and a stable outlook with Fitch. The system has strong profitability, solid liquidity and presence in several high growth markets, Fitch said.

2. St. Louis-based BJC HealthCare has an “AA” rating and stable outlook with S&P and an “Aa2” rating and stable outlook with Moody’s. The health system has a leading market share and a highly regarded reputation, particularly for its flagship hospitals that are affiliated with Washington University School of Medicine in St. Louis, S&P said. The health system has consistently produced stable earnings and cash flow, even during the COVID-19 pandemic, according to the credit rating agency.

3. Dallas-based Children’s Health System of Texas has an “AA” rating and stable outlook with Fitch. The system has robust operating profitability, good expense management and strong EBITDA margins, according to Fitch.

4. Cleveland Clinic has an “Aa2” rating and stable outlook with Moody’s. The system’s international brand will allow it to grow revenue outside of the northeast Ohio market and offset the effects of the pandemic on patient volume, Moody’s said. The credit rating agency expects the system to maintain good cash flow margins.

5. Evansville, Ind.-based Deaconess Health System has an “AA” rating and stable outlook with Fitch. The health system has strong operating performance and an expanding footprint in a stable and economically diverse service area, Fitch said. Investments in core service lines should help support patient volume growth, according to the credit rating agency.

6. Durham, N.C.-based Duke Health has an “AA” rating and stable outlook with Fitch. The system has a strong clinical reputation and a solid balance sheet with substantial liquidity reserves, Fitch said.

7. Pinehurst, N.C.-based FirstHealth of the Carolinas has an “AA” rating and stable outlook with Fitch. The health system has a strong financial profile and stable operating performance, despite disruption from the COVID-19 pandemic, Fitch said. The health system’s revenue in the first quarter of fiscal 2021 rebounded to levels close to historical trends, according to the credit rating agency.

8. Milwaukee-based Froedtert Health has an “AA” rating and stable outlook with Fitch. The system has a solid market position and a robust liquidity position, Fitch said. The credit rating agency expects Froedtert to maintain robust operating cash flow levels.

9. Indianapolis-based Indiana University Health has an “Aa2” rating and stable outlook with Moody’s and an “AA” rating and positive outlook with Fitch. Cost controls and patient volume will help the system sustain strong margins and liquidity, Moody’s said.

10. IHC Health Services, the borrowing group of Salt Lake City-based Intermountain Healthcare, has an “Aa1” rating and stable outlook with Moody’s. Intermountain has a leading statewide market position, low debt levels and strong cash levels, Moody’s said. The credit rating agency expects Intermountain will sustain strong margins and cash levels.

11. Falls Church, Va.-based Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The system has a strong financial profile, and Moody’s expects Inova’s balance sheet to remain exceptionally strong.

12. Rochester, Minn.-based Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The health system has strong balance sheet measures, an excellent market position and strong patient demand at its three academic campuses in Minnesota, Arizona and Florida, Moody’s said. The credit rating agency expects strong patient demand and steps taken by management to allow Mayo to maintain adequate cash flow and strengthen balance sheet measures.

13. Traverse City, Mich.-based Munson Healthcare has an “AA” rating and stable outlook with Fitch. The system has strong leverage and liquidity, Fitch said. The credit rating agency expects Munson to maintain solid operating cash flow margins.

14. Tupelo-based North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The system has a leading market share in a large 20-county service area and strong adjusted leverage metrics, Fitch said.

15. Chicago-based Northwestern Memorial HealthCare has an “Aa2” rating and stable outlook with Moody’s and an “AA+” rating and stable outlook with S&P. The health system had strong pre-COVID margins and liquidity, Moody’s said. The credit rating agency expects the system to maintain strong operating cash flow margins.

16. Columbus-based OhioHealth has an “Aa2” rating and stable outlook with Moody’s and an “AA+” rating and stable outlook with S&P. The system has a leading market position and opportunities for service line expansion, Moody’s said. The credit rating agency expects the system’s strong liquidity to provide ample cushion for volatility in investment returns.

17. Stanford (Calif.) Health Care has an “AA” rating and stable outlook with Fitch. The system has broad reach and is a clinical destination for high acuity services, Fitch said. The credit rating agency expects the system to sustain strong EBITDA margins.

18. Iowa City-based University of Iowa Hospitals & Clinics has an “Aa2” rating and stable outlook with Moody’s. The credit rating agency expects the system to maintain strong operating performance and cash flow. The system benefits as the only academic medical center in Iowa, according to Moody’s.

Here are 10 hospitals and health systems with strong operational metrics and solid financial positions, according to reports from Fitch Ratings and Moody’s Investors Service.

1. Altamonte Springs, Fla.-based AdventHealth has an “Aa2” rating and stable outlook from Moody’s. The credit rating agency said the system benefits from strong operating cash flow margins, low operating leverage and a large scale with presence in multiple states.

2. Children’s Hospital of Philadelphia has an “Aa2” rating and stable outlook from Moody’s. The credit rating agency said the rating is reflective of Children’s Hospital of Philadelphia’s strong market position and brand equity as a top U.S. children’s hospital with advanced clinical research. The pediatric hospital network also has strong liquidity.

3. Cleveland Clinic has an “Aa2” rating and stable outlook from Moody’s. The credit rating agency said the health system benefits from its reputation as an international brand, which will allow it to grow revenue outside of the Ohio market. Moody’s said it maintains good cash flow margins and therefore very strong liquidity.

4. Cottage Health in Santa Barbara, Calif., has an “AA-” rating and stable outlook from Fitch. The credit rating agency said Cottage benefits from consistently strong profitability, a strong balance sheet and leading market position. Fitch also said the health system has broad reach in a service area that has high demand for acute care services.

5. Froedtert Health in Wauwatosa, Wis., has an “AA” rating and stable outlook from Fitch. The credit rating agency said the rating reflects the health system’s solid market position and robust liquidity position, as well as its strong utilization trends and operational metrics in recent years.

6. Indiana University Health in Indianapolis has an “AA” rating and positive outlook from Fitch. The credit rating agency said the health system has a long track record of strong operating margins and a “remarkably solid” balance sheet. The system also benefits as the largest healthcare system and academic medical center in Indiana, according to Fitch.

7. Vineland, N.J.-based Inspira Health has an “AA-” rating and stable outlook from Fitch. The credit rating agency said the rating is supported by Inspira’s stable financial profile, leading market position, large medical staff and expansive outpatient network. Fitch also said Inspira saw a strong operating performance through the construction and transition of its new campus, an IT implementation and through the peak of the pandemic.

8. Sanford Health in Sioux Falls, S.D., has an “AA-” rating and stable outlook from Fitch. The credit rating agency said the “AA-” rating reflects Sanford’s leading inpatient market share in multiple states and strong financial profile. Fitch also said Sanford’s growing health plan and plan for continued improvement and balance sheet growth are credit positives.

9. Spectrum Health in Grand Rapids, Mich., has an “Aa3” rating and stable outlook with Moody’s. The credit rating agency said the health system has a stable operating performance and strong balance sheet metrics. In particular, the system generated positive margins even without federal aid in fiscal year 2020. Moody’s said the health system will continue to benefit from a strong market share for patient care in western Michigan.

10. Texas Children’s Hospital in Houston has an “Aa2” rating and stable outlook from Moody’s. The credit rating agency said the children’s hospital network benefits from favorable leverage metrics and strong liquidity. Moody’s also said Texas Children’s has very strong patient demand and high acuity services as the academic medical center for Baylor College of Medicine’s pediatric department in Houston.