Healthcare leaders are grappling with a daunting healthcare challenge that persists quietly. Day-to-day, it doesn’t trigger loud alarms, emergency press conferences, or AI pilots, but addressing it will take immense collective effort.

As of 2022, there were 52 million Americans over the age of 65, a population that grows by 10,000 each day. By 2034, older Americans will outnumber younger ones. An estimated 50% of babies born in 2020 are expected to live beyond 100 years.

Behind these statistics lies a diverse population: 90-year-olds running marathons and 65-year-olds incapacitated by strokes. Biological age is distinct from numerical age, after all.

The intensifying demands of an aging population on the U.S. healthcare system represent a challenge of a lifetime, yet one often downplayed or overlooked in the day to day. This aligns with the history of geriatric medicine. The specialty focused on medical care for older adults and the promotion of healthy aging was not widely accepted in the U.S. even in the 1980s.

“About 25 years ago, if you were in most health systems and you talked about geriatric medicine, most clinicians would tell you there was no such thing,” said Michael Dowling, president and CEO of Northwell Health. “There was a denial about the fact that there was geriatric medicine. The idea was that people were older adults that were just getting older.”

Mr. Dowling is a co-author of “The Aging Revolution.” The book, released in June 2024, highlights the revolutionaries who rejected the status quo in elder care and pioneered new methods to improve aging adults’ quality and longevity of life.

Much of the geriatric medicine specialty originates in Northwell’s home base: New York City. There, Robert Butler, MD, earned his medical degree in 1953 and not long after began to notice gaps in his education when caring for older adults. Their health needs were more complex, interrelated, and varied, yet they were treated as no different from younger adults. Driven to know more, he joined the National Institute of Mental Health in Washington, D.C., to explore healthy aging, embarking on an irreversible journey.

Through the 1960s and early 1970s, Dr. Butler grew more impatient with the status quo healthcare treatment of older adults in America. He observed prevailing attitudes of paternalism, infantilism, avoidance or mere caretaking rather than meaningful treatment.

Dr. Butler made no effort to hide his frustration with the title of his 1975 book, “Why Survive? Being Old in America.” In it, he argued that healthcare professionals were not adequately trained to meet the needs of older patients. Their medical conditions were considered uninteresting by teaching institutions and stereotyped as cantankerous and bothersome. The book won the Pulitzer Prize for General Non-Fiction and resonated with other physicians, expanding the circle of healthcare professionals seeking specialization in the care of older patients.

In 1982, Dr. Butler established the Department of Geriatrics and Adult Development at Mount Sinai Medical Center in New York City, creating the first department of its kind in a U.S. medical school. He continued to promote the specialty and the pursuit of knowledge in geriatric medicine, a field in which he had no formal education because it did not exist during his training. Dr. Butler passed away in 2010 at the age of 83.

“He was a powerhouse. It was [Dr. Butler] who basically pushed the issue,” said Mr. Dowling. “It doesn’t mean it wasn’t discussed prior, but he actually took it upon himself to make a difference. That’s amazing.”

Mr. Dowling said the book, co-authored with Maria Torroella Carney, MD, chief of geriatric and palliative medicine for Northwell, and author Charles Kenney, aims to raise awareness about the relatively recent development of geriatric medicine. It highlights how a dedicated group of individuals transformed this field from a notable shortcoming into a reality not that long ago.

The book includes real patient stories and took two years to write, aiming to help readers understand healthcare for older adults vividly and not merely in theory. It covers the rise of palliative medicine in the 1990s, the return of home care and pioneers’ work to address the toughest geriatric syndromes, like falls and delirium.

The questions and shortcomings that Dr. Butler forcefully highlighted in the 1970s and 1980s remain relevant today.

Geriatricians provide comprehensive care for adults ages 65 through the end of their life. While this age group consumes more healthcare than any other,

there are fewer than 7,300 physicians that are board-certified geriatricians, which is fewer than 1% of all physicians.

This deficit places greater demands on entire systems, then, to better meet the needs of the aging population. Demand for services will increase, necessitating the evolution and expansion of skill sets, cultural competencies, access points and care settings.

This work makes the practice of geriatric medicine and the advancements made for older patients relevant to far more than the physicians earning certifications in the specialty. Health systems today face questions about what it means to be an age-friendly health system, which requires more than medical care. Age-friendly care is a specific model from the Institute for Healthcare Improvement and The John A. Hartford Foundation that rests on four M’s: What Matters Most, Medication, Mentation and Mobility.

Northwell is one of the largest systems to adopt the framework in all adult acute care settings, primary care ambulatory sites, and post-acute care locations. The effort requires staff training, evidence-based assessment tools and metrics, governance and partnerships with outside institutions. Nationwide, more than 4,000 sites of care have been recognized as age-friendly organizations.

Mr. Dowling’s focus on the topic is a steady one, with more initiatives to come. Aging presents a dual challenge: as people live longer, they place increasing demands on health systems and support infrastructures, compounded by declining birth rates.

“When the older population is growing by about 10,000 a day, and the population of children is declining, you have this massive imbalance, which is not just a healthcare issue. It’s a huge economic issue,” Mr. Dowling said. The book does not shy away from the challenge, including a chapter with seven experts addressing the question: How will we as a society deliver and pay for care needed by an aging population where every day 10,000 people turn 65?

“The Aging Revolution” celebrates the strides made in geriatric medicine and honors the pioneers who led the way, helping our elders avoid unnecessary suffering in the pursuit of longer, fulfilling lives. It also serves as a reminder that the aging of our society demands rigorous problem-solving today and in the years ahead, requiring a spirit of innovation equal to, if not greater than, that which drove its inception.

Understand the health care industry’s most urgent challenges—and greatest opportunities.

The health care industry is facing an increasingly tough business climate dominated by increasing costs and prices, tightening margins and capital, staffing upheaval, and state-level policymaking. These urgent, disruptive market forces mean that leaders must navigate an unusually high number of short-term crises.

But these near-term challenges also offer significant opportunities. The strategic choices health care leaders make now will have an outsized impact—positive or negative—on their organization’s long-term goals, as well as the equitability, sustainability, and affordability of the industry as a whole.

This briefing examines the biggest market forces to watch, the key strategic decisions that health care organizations must make to influence how the industry operates, and the emerging disruptions that will challenge the traditional structures of the entire industry.

Preview the insights below and download the full executive briefing (using the link above) now to learn the top 16 insights about the state of the health care industry today.

Preview the insights

Part 1 | Today’s market environment includes an overwhelming deluge of crises—and they all command strategic attention

Insight #1

The converging financial pressures of elevated input costs, a volatile macroeconomic climate, and the delayed impact of inflation on health care prices are exposing the entire industry to even greater scrutiny over affordability. Keep reading on pg. 6

Insight #2

The clinical workforce shortage is not temporary. It’s been building to a structural breaking point for years. Keep reading on pg. 8

Insight #3

Demand for health care services is growing more varied and complex—and pressuring the limited capacity of the health care industry when its bandwidth is most depleted. Keep reading on pg. 10

Insight #4

Insurance coverage shifted dramatically to publicly funded managed care. But Medicaid enrollment is poised to disperse unevenly after the public health emergency expires, while Medicare Advantage will grow (and consolidate). Keep reading on pg. 12

Part II | Competition for strategic assets continues at a rapid pace—influencing how and where patient care is delivered.

Insight #5

The current crisis conditions of hospital systems mask deeper vulnerabilities: rapidly eroding power to control procedural volumes and uncertainty around strategic acquisition and consolidation. Keep reading on pg. 15

Insight #6

Health care giants—especially national insurers, retailers, and big tech entrants—are building vertical ecosystems (and driving an asset-buying frenzy in the process). Keep reading on pg. 17

Insight #7

As employment options expand, physicians will determine which owners and partners benefit from their talent, clinical influence, and strategic capabilities—but only if these organizations can create an integrated physician enterprise. Keep reading on pg. 19

Insight #8

Broader, sustainable shifts to home-based care will require most care delivery organizations to focus on scaling select services. Keep reading on pg. 21

Insight #9

A flood of investment has expanded telehealth technology and changed what interactions with patients are possible. This has opened up new capabilities for coordinating care management or competing for consumer attention. Keep reading on pg. 23

Insight #10

Health care organizations are harnessing data and incentives to curate consumers choices—at both the service-specific and ecosystem-wide levels. Keep reading on pg. 25

Part III | Emerging structural disruptions require leaders to reckon with impacts to future business sustainability.

Insight #11

For value-based care to succeed outside of public programs, commercial plans and providers must coalesce around a sustainable risk-based payment approach that meets employers’ experience and cost needs. Keep reading on pg. 28

Insight #12

Industry pioneers are taking steps to integrate health equity into quality metrics. This could transform the health care business model, or it could relegate equity initiatives to just another target on a dashboard. Keep reading on pg. 30

Insight #13

Unprecedented behavioral health needs are hitting an already fragmented, marginalized care infrastructure. Leaders across all sectors will need to make difficult compromises to treat and pay for behavioral health like we do other complex, chronic conditions. Keep reading on pg. 32

Insight #14

As the population ages, the fragile patchwork of government payers, unpaid caregivers, and strained nursing homes is ill-equipped to provide sustainable, equitable senior care. This is putting pressure on Medicare Advantage plans to ultimately deliver results. Keep reading on pg. 34

Insight #15

The enormous pipeline of specialized high-cost therapies in development will see limited clinical use unless the entire industry prepares for paradigm shifts in evidence evaluation, utilization management, and financing. Keep reading on pg. 36

Insight #16

Self-funded employers, who are now liable for paying “reasonable” amounts, may contest the standard business practices of brokers and plans to avoid complex legal battles with poor optics. Keep reading on pg. 38

There are an estimated 19,000 full-time job vacancies across Massachusetts acute care hospitals, according to a survey published Oct. 31 by the Massachusetts Health & Hospital Association.

Hospitals are working to address backlogs and transfer patients to post-acute care settings while skyrocketing labor costs — including a projected $1 billion in travel labor costs this year — are compounding healthcare facilities’ financial woes, according to the report. These challenges are hampering hospital operations as well as leading to care delays and reduced access to care.

Fewer workers mean that fewer beds are available for patients, while the demand for care increases due to deferred care throughout the COVID-19 pandemic, the behavioral health crisis and reduced access to community-based services continue to challenge hospitals throughout the state. At any given time, more than 1,500 patients are in acute hospital beds awaiting placement to a specialized behavioral health bed or post-acute care, according to the MHA.

“Our healthcare system has never been more fragile, and its leaders have never been more concerned about what’s to come in months ahead,” Steve Walsh, president and CEO of the MHA, said in an Oct. 31 news release shared with Becker’s Hospital Review. “They are exhausting every option within their control to confront these challenges, but this is an unsustainable reality and providers are in dire need of support.”

In response to the survey, 37 hospitals — representing 70 percent of the state’s total hospital employment — reported 6,650 vacancies among 47 positions critical to hospital operations and clinical care. The positions range from direct care nurses to lab personnel and clinical support staff. Eighteen of the 47 positions have a vacancy rate greater than 20 percent.

At a 56 percent vacancy rate, licensed practical nurses is the most in-demand position, while home health aides (34 percent), mental health workers (32 percent), infection control nurses (26 percent) and CRNAs (24 percent) are also highly sought after.

Survey respondents identified 6,650 vacancies. The 47 positions included in the survey, which was conducted this summer, account for less than half of all hospital roles. The MHA said it extrapolated that across all positions and hospitals to arrive at an estimated 19,000 vacancies across the state.

Staffing shortages are driving labor costs to an unsustainable level for many hospitals already grappling with margins close to zero or in the red. Hospitals have relied on high-cost temporary staffing to fill critical positions during the pandemic, resulting in average hourly wage rates for travel nurses increasing 90 percent since 2019, according to the report. Massachusetts hospitals reported spending $445 million on temporary registered nurse staffing halfway through the fiscal year, with temporary RN staffing costs increasing 234 percent from fiscal year 2019 to March 2022.

If urgent steps are not taken to address healthcare’s staffing shortage, hospitals will continue to face capacity challenges and overpay for labor, which will lead to fiscal instability, according to Mr. Walsh.

The MHA urged providers, payers, public officials and government agencies to address the workforce crisis by investing in training and education, expanding the workforce pipeline, providing financial support to hospitals and advancing new models of care such as telehealth and at-home care.

Hospitals are experiencing significant increases in expenses for workforce, drugs and medical supplies

Introduction

For over two years since the outset of the COVID-19 pandemic, America’s hospitals and health systems have been on the front lines caring for patients, comforting families and protecting communities.

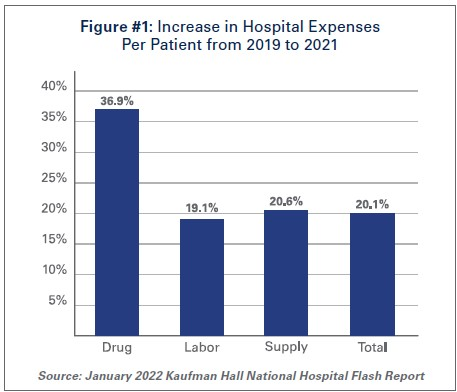

With over 80 million cases1, nearly 1 million deaths2, and over 4.6 million hospitalizations3, the pandemic has taken a significant toll on hospitals and health systems and placed enormous strain on the nation’s health care workforce. During this unprecedented public health crisis, hospitals and health systems have confronted many challenges, including historic volume and revenue losses, as well as skyrocketing expenses (See Figure #1).

Hospitals and health systems have been nimble in responding to surges in COVID-19 cases throughout the pandemic by expanding treatment capacity, hiring staff to meet demand, acquiring and maintaining adequate supplies and personal protective equipment (PPE) to protect patients and staff and ensuring that critical services and programs remain available to the patients and communities they serve. However, these and other factors have led to billions of dollars in losses over the last two years for hospitals, and over 33% of hospitals are operating on negative margins.

The most recent surges triggered by the delta and omicron variants have added even more pressure to hospitals. During these surges, hospitals saw the number of COVID-19 infected patients rise while other patient volumes fell, and patient acuity increased. This drove up expenses and added significant financial pressure for hospitals. Moreover, hospitals did not receive any government assistance through the COVID-19 Provider Relief Fund (PRF) to help mitigate rising expenses and lost revenues during the delta and omicron surges. This is despite the fact that more than half of COVID-19 hospitalizations have occurred since July 1, 2021, during these two most recent COVID-19 surges.

At the same time, patient acuity has increased, as measured by how long patients need to stay in the hospital. The increase in acuity is a result of the complexity of COVID-19 care, as well as treatment for patients who may have put off care during the pandemic. The average length of a patient stay increased 9.9% by the end of 2021 compared to pre-pandemic levels in 2019.4

As hospitals treat sicker patients requiring more intensive treatment, they also must ensure that sufficient staffing levels are available to care for these patients, and must acquire the necessary expensive drugs and medical supplies to provide high-quality care. As a result, overall hospital expenses have experienced considerable growth.

Data from Kaufman Hall, a consulting firm that tracks hospital financial metrics, shows that by the end of 2021, total hospital expenses were up 11% compared to pre-pandemic levels in 2019. Even after accounting for changes in volume that occurred during the pandemic, hospital expenses per patient increased significantly from pre-pandemic levels across every category. (See Figure #1)

The pandemic has strained hospitals’ and health systems’ finances. Many hospitals operate on razorthin margins, so even slight increases in expenses can have dramatic negative effects on operating margins, which can jeopardize their ability to care for patients. These expense increases have been more challenging to withstand in light of rising inflation and growth in input prices. In fact, despite modest growth in revenues compared to pre-pandemic levels, median hospital operating margins were down 3.8% by the end of 2021 compared to pre-pandemic levels, according to Kaufman Hall. Further exacerbating the problem for hospitals are Medicare sequestration cuts and payment increases that are well below increases in costs. For example, an analysis by PINC found that for fiscal year 2022, hospitals received a 2.4% increase in their Medicare inpatient payment rate, while hospital labor rates increased 6.5%.5

These levels of increased expenses and declines in operating margins are not sustainable. This report highlights key pressures currently facing hospitals and health systems, including:

Each of these issues separately presents significant challenges to the hospital field. Taken together, they represent conditions that would be potentially catastrophic for most organizations, institutions and industries. However, the fact that the nation’s hospitals and health systems continue to serve on the front lines of the ongoing pandemic is a testament to their resiliency and steadfast commitment to their mission to serve patients and communities around the country.

Hospitals and health systems are the cornerstones of their communities. Their patients depend on them for access to care 24 hours a day, seven days a week. Hospitals are often the largest employers in their community, and large purchasers of local services and goods. Additional support is needed to help ensure hospitals have the adequate resources to care for their communities.

I. Workforce and Contract Labor Expenses

The hospital workforce is central to the care process and often the largest expense for hospitals. It is no surprise then that even before the pandemic, labor costs — which include costs associated with recruiting and retaining employed staff, benefits and incentives — accounted for more than 50% of hospitals’ total expenses. Therefore, even a slight increase in these costs can have significant impacts on a hospital’s total expenses and operating margins.

As the pandemic has persisted for over two years, the toll on the health care workforce has been immense. A recent survey of health care workers found that approximately half of respondents felt “burned out” and nearly a quarter of respondents said they anticipated leaving the health care field.6

This has been mirrored by a significant and sustained decline in hospital employment, down approximately 100,000 employees from pre-pandemic levels.7 At the height of the omicron surge, approximately 1,400 hospitals or 30% of all U.S. hospitals reporting data to the government, indicated that they anticipated a critical staffing shortage within the week.8This high percentage of hospitals reporting a critical staffing shortage stayed relatively consistent throughout the delta and omicron surges.

The combination of employee burnout, fewer available staff, increased patient acuity and higher demand for care especially during the delta and omicron surges, has forced hospitals to turn to contract staffing firms to help address staffing shortages.

Though hospitals have long worked with contract staffing firms to bridge temporary gaps in staffing, the pandemic-driven-staffing-shortage has created an expanded reliance on contract staff, especially contract or travel registered nurses. Travel nurses are in particularly high demand because they serve a critical role in delivering care for both COVID-19 and non-COVID-19 patients and allow the hospital to meet the demand for care, especially during pandemic surges.

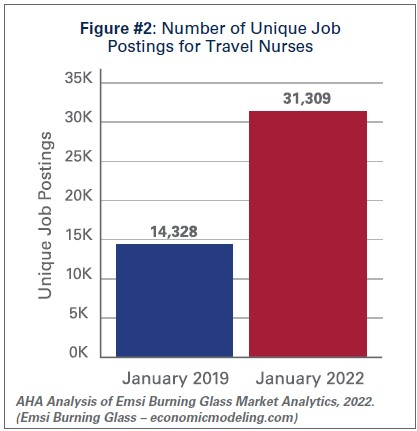

According to a survey by AMN Healthcare, one of the nation’s largest health care staffing agencies, 95% of health care facilities reported hiring nurse staff from contract labor firms during the pandemic.9Staffing firms have increased their recruitment of contract or travel nurses, illustrating the significant growth in their demand. According to data from EMSI/Burning Glass, there has been a nearly 120% increase in job postings for contract or travel nurses from pre-pandemic levels in January 2019 to January 2022. (See Figure #2)

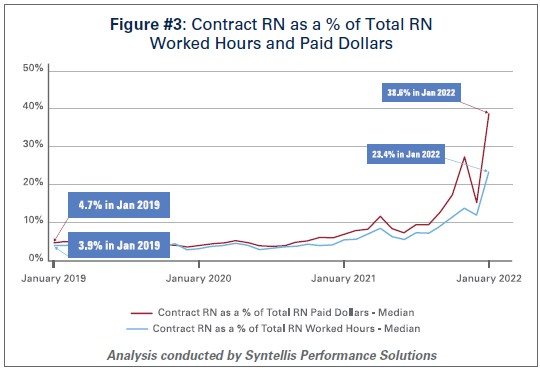

Similarly, the hours worked by contract or travel nurses as a percentage of total hours worked by nurses in hospitals has grown from 3.9% in January 2019 to 23.4% in January 2022, according to data from Syntellis Performance Solutions. (See Figure #3) In fact, a quarter of hospitals have experienced nearly a third of their total nurse hours accounted for by contract or travel nurses.

As the share of contract travel nurse hours has grown significantly compared to before the pandemic, so too have the costs of employing travel nurses compared to pre-pandemic levels. In 2019, hospitals spent a median of 4.7% of their total nurse labor expenses for contract travel nurses, which skyrocketed to a median of 38.6% in January 2022. (See Figure #3) A quarter of hospitals — those who have had to rely disproportionately on contract travel nurses — saw their costs for contract travel nurses account for over 50% of their total nurse labor expenses. In fact, while contract travel nurses accounted for 23.4% of total nurse hours in January 2022, they accounted for nearly 40% of the labor expenses for nurses. (See Figure #3) This difference has grown considerably compared to pre-pandemic levels in 2019, suggesting that the exorbitant prices charged by staffing companies are a primary driver of higher labor expenses for hospitals.

Data from Syntellis Performance Solutions show a 213% increase in hourly rates charged to hospitals by staffing companies for travel nurses in January 2022 compared to pre-pandemic levels in January 2019. This is because staffing agencies have exploited the situation by increasing the hourly rates billed to hospitals for contract travel nurses more than the hourly rates they pay to travel nurses. This is effectively the “margin” retained by the staffing agencies. During pre-pandemic levels in 2019, the average “margin” retained by staffing agencies for travel nurses was about 15%. As of January 2022, the average “margin” has grown to an astounding 62%. (See Figure #4)

These high “margins” have fueled massive growth in the revenues and profits of health care staffing companies. Several staffing firms have reported significant growth in their revenues to as high as $1.1 billion in just the fourth quarter of 202110, tripling their revenues and net income compared to 2020 levels.11

The data indicate that the growth in labor expenses for hospitals and health systems was in large part due to the exorbitant rates charged by contract staffing firms. By the end of 2021, hospital labor expenses per patient were 36.9% higher than pre-pandemic levels, and increased to 57% at the height of the omicron surge in January 2022.12 A study looking at hospitals in New Jersey found that the increased labor expenses for contract staff amounted to $670 million in 2021 alone, which was more than triple what their hospitals spent in 2020.13High reliance on contract or travel staff prevents hospitals and health systems from investing those costs into their existing employees, leading to low morale and high turnover, which further exacerbates the challenges hospitals and health systems have been facing.

II. Drug Expenses

Prescription drug spending in the U.S. has grown significantly since the pandemic. In 2021, drug spending (including spending in both retail and non-retail settings) increased 7.7%14, which was on top of an increase of 4.9%15 in 2020. While some of this growth can be attributed to increased utilization as patient acuity increased during the pandemic, a significant driver has been the continued increase in prices of existing drugs as well as the introduction of new products at very high prices. A study by GoodRx found that in January 2022 alone, drug companies increased the price of about 810 brand and generic drugs that they reviewed by an average of 5.1%.16 These price increases followed massive price hikes for certain drugs often used in the hospital such as Hydromorphone (107%), Mitomycin (99%), and Vasopressin (97%).17 For another example, the drug manufacturer of Humira, one of the most popular brand drugs used to treat rheumatoid arthritis, increased the price of the drug by 21% between 2019 and 2021.18 A study by the Kaiser Family Foundation found that in Medicare Part B and D markets, half of all drugs in each market experienced price increases above the rate of inflation between 2019 and 2020 – in fact, a third of these drugs experienced price increases of greater than 7.5%.19 At the same time, according to a report by the Institute for Clinical and Economic Review (ICER), eight drugs with unsupported U.S. drug price increases between 2019 and 2020 alone accounted for an additional $1.67 billion in drug spending, further illustrating that drug companies’ decisions to raise the prices of their drugs are simply an unsustainable practice.20

As hospitals have worked to treat sicker patients during the pandemic, they have been forced to contend with sky-high prices for drugs, many of which are critical and lifesaving for their patients. For example, in 2020, 16 of the top 25 drugs by spending in Medicare Part B (hospital outpatient settings) had price increases greater than inflation — two of the top three drugs, Keytruda and Prolia — experienced price increases of 3.3% and 4.1%, respectively.21

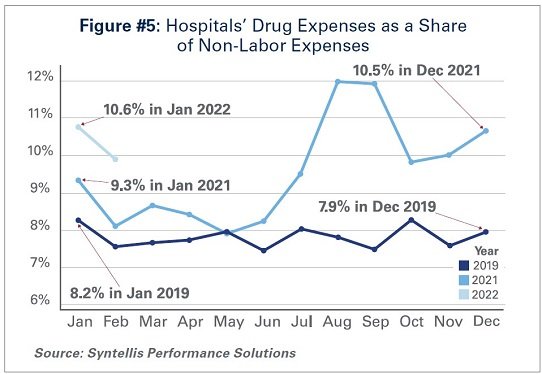

As a result of these price increases, hospital drug expenses have skyrocketed. By the end of 2021, total drug expenses were 28.2% higher than pre-pandemic levels.22 When taken as a share of all non-labor expenses, drug expenses have grown from approximately 8.2% in January 2019, to 9.3% in January 2021, and to 10.6% in January 2022. (See Figure #5) Even when considering changes in volume during the pandemic, drug expenses per patient compared to pre-pandemic levels in 2019 saw significant increases, with a 36.9% increase through 2021.

While continued drug price increases by drug companies have been a major driver of the growth in overall hospital drug expenses, there also are other important driving factors to consider:

Drug Treatments for COVID-19 Patients:Remdesivir, one of the primary drugs used to treat COVID-19 patients in the hospital, has become the top spend drug for most hospitals since the pandemic. This drug alone accounted for over $1 billion in sales in the fourth quarter of 2021.23 Priced at an average of $3,12024, Remdesivir’s cost was initially covered by the federal government. However, hospitals must now purchase the drug directly.

Limitation of 340B Contract Pharmacies: The 340B program allows eligible providers, including hospitals that treat many low-income patients or treat certain patient populations like children and cancer patients, to buy certain outpatient drugs at discounted prices and use those savings to provide more comprehensive services to the patients and communities they serve. Since July 2020, several of the largest drug manufacturers have denied 340B pricing to eligible hospitals through pharmacies with whom they contract, despite calls from the Department of Health and Human Services that such actions are illegal. Because of these actions, many 340B hospitals, especially rural hospitals who disproportionately rely on contract pharmacies to ensure access to drugs for their patients, have lost millions in 340B drug savings.25 In addition, these manufacturers have required claim-level data submissions as a condition of receiving 340B discounts, which has increased costs to deliver the data as well as staff time and expense to manage that process. The loss of 340B savings coupled with increased burden of providing detailed data to drug companies have contributed to increasing drug expenses.

Health Plans’/Pharmacy Benefit Managers’ (PBMs’) “White Bagging” Policies: Health plans and PBMs have engaged in a tactic that steers hospital patients to third-party specialty pharmacies to acquire medication necessary for clinician-administered treatments, known as “white-bagging.” This practice disallows the hospital from procuring and managing the handling of a drug — typically drugs that are infused or injected requiring a clinician to administer in a hospital or clinic setting — used in patient care. These policies not only create serious patient safety concerns, but create delays and risks in patient care; add to administration, storage and handling costs; and create important liability issues for hospitals.

Taken together, these factors increase both drug expenses and overall hospital expenses.

III. Medical Supply and PPE Expenses

The U.S., like most countries in the world, relies on global supply chains for goods and services. This is especially true for medical supplies used at hospitals and other health care settings. Everything from the masks and gloves worn by staff to medical devices used in patient care come from a large network of global suppliers. Prior to the global pandemic, hospitals had established relationships with distributors and other vendors in the global health care supply chain to deliver goods as necessitated by demand. After the pandemic hit, many factories, distributors and other vendors shut down their operations, leaving hospitals, which were on the front lines facing surging demand, to fend for themselves. In fact, supply chain disruptions across industries, including health care, increased by 67% in 2020 alone.26

As a result, hospitals turned to local suppliers and non-traditional suppliers, often paying significantly higher rates than they did prior to the pandemic. Between fall 2020 and early 2022 costs for energy, resins, cotton and most metals surged in excess of 30%; these all are critical elements in the manufacturing of medical supplies and devices used every day in hospitals.27 As COVID-19 cases surged, demand for hospital PPE, such as N95 masks, gloves, eye protection and surgical gowns, increased dramatically causing hospitals to invest in acquiring and maintaining reserves of these supplies. Further, downstream effects from other global events such as the war in Ukraine and the energy crisis in China, as well as domestic issues, such as labor shortages and rising fuel and transportation costs, have all contributed to drive up even higher overall medical supply expenses for hospitals in the U.S.28 For instance, according to the Health Industry Distributors Association, transportation times for medical supplies are 440% longer than pre-pandemic times resulting in massive delays.29

Compared to 2019 levels, supply expenses for hospitals were up 15.9%30 through the end of 2021. When focusing on hospital departments involved most directly in care for COVID-19 patients − primarily hospital intensive care units (ICUs) and respiratory care departments − the increase in expenses is significantly higher. Medical supply expenses in ICUs and respiratory care departments increased 31.5% and 22.3%, respectively. Further, accounting for changes in volume during surge and non-surge periods of the pandemic, medical supply expenses per patient in ICUs and respiratory care departments were 31.8% and 25.9% higher, respectively. (See Figure #6) These numbers help illustrate the magnitude of the impact that increases in supply costs have had on hospital finances during the pandemic.

IV. Impact of Rising Inflation

Higher economy-wide costs have serious implications for hospitals and health systems, increasing the pressures of higher labor, supply, and acquisition costs; and potentially lower consumer demand. Inflation is defined as the general increase in prices and the decrease in purchasing power. It is measured by the Consumer Price Index (CPI-U). In April 2021, the Bureau of Labor Statistics (BLS) reported that the CPI-U had the largest 12-month increase since September 2008. The CPI-U hit 40-year highs in February 2022.31 Overall, consumer prices rose by a historic 8.5% on an annualized basis in March 2022 alone.32

As inflation measured by consumer prices is at record highs, below are key considerations on the potential impact of higher general inflation on hospital prices:

Labor Costs and Retention: Labor costs represent a significant portion of hospital costs (typically more than 50% of hospital expenses are related to labor costs). As the cost-of-living increases, employees generally demand higher wages/total compensation packages to offset those costs. This is especially true in the health care sector, where labor demands are already high, and labor supply is low.

Supply Chain Costs: Medical supplies account for approximately 20% of hospital expenses, on average. As input/raw good costs increase due to general inflation, hospital supplies and medical device costs increase as well. Furthermore, shortages of raw materials, including those used to manufacture drugs, could stress supply chains (i.e., medical supply shortages), which may result in changes in care patterns and add further burden on staff to implement work arounds.

Capital Investment Costs: Capital investments also may be strained, especially as hospitals have already invested heavily in expanding capacity to treat patients during the pandemic (e.g., constructing spaces for testing and isolation of COVID-19 patients). One of the areas that has seen the largest increase in prices/shortages is building materials (e.g., lumber). Additionally, a historically large increase in inflation has resulted in increases in interest rates, which may hamper borrowing options and add to overall costs.

Consumer Demand: Higher inflation also may result in decreases in demand for health care services, specifically if inflation exceeds wage growth. Specifically, higher costs for necessities (food, transportation, etc.) could push down demand for health care services and, in turn, dampen hospital volumes and revenues in the long run.

Health care and hospital prices are not driving recent overall inflation increases. The BLS has cited increases in the indices for gasoline, shelter and food as the largest contributors to the seasonally adjusted all items increase. The CPI-U increased 0.8% in February on a seasonally adjusted basis, whereas the medical care index rose 0.2% in February. The index for prescription drugs rose 0.3%, but the hospital index for hospital services declined 0.1%.33

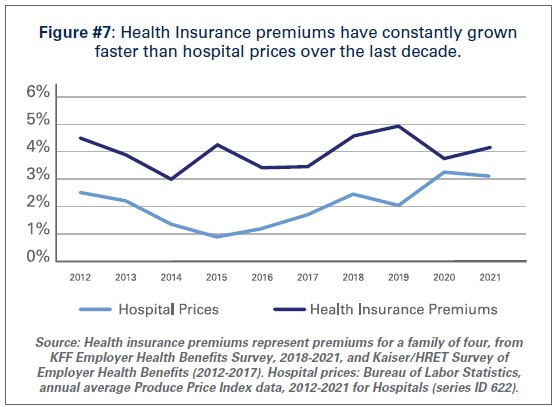

This is consistent with pre-pandemic trends. Despite persistent cost pressures, hospital prices have seen consistently modest growth in recent years. According to BLS data, hospital prices have grown an average 2.1% per year over the last decade, about half the average annual increase in health insurance premiums. (See Figure #7) More recently, hospital prices have grown much more slowly than the overall rate of inflation. In the 12 months ending in February 2022, hospital prices increased 2.1%. In fact, even when excluding the artificially low rates paid to hospitals by Medicare and Medicaid, average annual price growth has still been below 3% in recent years.34

Conclusion

While we hope that our nation is rounding the corner in the battle against COVID-19, it is clear that the pandemic is not over. During the week of April 11, there have been an average of over 33,000 cases per day35 and reports suggest that a new subvariant of the virus (Omicron BA.2) is now the dominant strain in the U.S.36As a result, the challenges hospitals and health systems are currently facing are bound to last much longer.

As COVID-19 infections and hospitalizations are decreasing in some parts of the U.S. and increasing in others, hospitals and health systems continue to care for COVID-19 and non-COVID-19 patients. With additional surges potentially on the horizon, the massive growth in expenses is unsustainable. Most of the nation’s hospitals were operating on razor thin margins prior to the pandemic; and now, many of these hospitals are in an even more precarious financial situation. Regardless of potential new surges of COVID-19, hospitals and health systems continue to face workforce retention and recruitment challenges, supply chain disruptions and exorbitant expenses as outlined in this report.

Hospitals appreciate the support and resources that Congress has provided throughout the pandemic; however, additional support is needed now to keep hospitals strong so they can continue to provide care to patients and communities.

While Omicron’s rapid spread is causing COVID hospitalizations to surge once again, the impact on consumer confidence may be different this time around. Drawing on the most recent data from analytics firm Strata Decision Technology, the graphic above shows how hospital volumes have fluctuated throughout the pandemic. Hospital volumes mostly returned to pre-COVID levels early last summer, until the Delta surge caused patients to begin avoiding care across all settings once again.

It remains to be seen if the forty percent of consumers who said they were less likely to seek non-emergency care during the Delta surge feel similarly about the Omicron spike. So far, consumer sentiment seems to be holding steady at last summer’s levels, though we’re still a few weeks away from Omicron’s expected peak.

As the pandemic enters its third year, it’s also likely that consumers who have been delaying care will simply be unwilling or unable to hold off any longer. But even if Omicron doesn’t dissuade consumers from seeking non-COVID care, health systems will be hard pressed to accommodate both COVID and non-COVID care amid worrisome staffing shortages.

Amid a nationwide staffing shortage, rising demand for nurses has led hospitals to increase salaries and other benefits to attract and retain workers, Melanie Evans reports for the Wall Street Journal.

Hospitals increase salaries, benefits to keep up with nursing demand

Hospitals across the country have been struggling amid staffing shortages, particularly of nurses, Evans reports. According to health care consultancy Premier, nurse turnover rates have increased to around 22% this year, up from the annual rate of about 18% in 2019.

“We are employing more nurses now than we ever have, and we also have more vacancies than we ever had,” said Greg Till, chief people officer at Providence Health & Services.

To retain their current nurses and attract new staff, many hospitals have increased their nurses’ salaries to remain competitive in the job market, Evans reports.

For example, HCA Healthcare, one of the largest hospital chains in the country, said it increased nurse pay this year to keep up with Covid-19 surges and compete with rivals also trying to fill vacant positions.

Similarly, Jefferson Health in May raised salaries for its nearly 10,000 nurses by 10% after the system discovered that rivals had increased their compensation. “The circumstances required it,” said Kate Fitzpatrick, Jefferson’s chief nurse executive.

In addition, Citizens Memorial Hospital in Bolivar, Mo., this month raised its nurses’ salaries by up to 5% after rivals in other nearby cities increased their workers’ wages. Sarah Hanak, Citizen Memorial’s CNO, said the hospital also increased the hourly wages of nurses working overnight shifts by around 15% to ensure sufficient staffing for those shifts.

“We were forced to,” Hanak said. “We absolutely have to stay competitive.”

Overall, the average annual salary for RNs, not including bonus pay, grew to $81,376, according to Premier—a 4% increase across the first nine months of the year. This is larger than the 3.3% increase in the average annual nurse salary for 2020 and the 2.6% increase in 2019, Evanswrites.

In addition to salary increases, some organizations, such as Providence, are also offering other benefits to attract and retain nurses, such as more time off, greater schedule flexibility, and new career development opportunities. Many hospitals are also hiring new graduates to work in specialized roles in ORs and other areas, allowing them to advance their careers more quickly than they would have before.

Overall, this rising demand for nurses has allowed those entering the workforce to negotiate higher salaries, more flexible working hours, and other benefits, Evans writes.

“I think you get to write your ticket,” said Tessa Johnson, president of the North Dakota Nurses Association.

Nurse compensation increases were inevitable—here’s why

It was inevitable that we would get to this point: baseline nurse compensation on a clear upward trajectory. Inevitable because this boils down to laws of supply and demand. Amid a clear nursing shortage, organizations are being forced to raise baseline compensation to compete for increasingly scarce qualified nurses. This is true in nearly every market, even for those considered to be ‘destination employers.’

If anything, what’s most surprising in the data from Premier is the moderated increase of around 4%. From a worker’s perspective, that’s not even covering cost of living increases due to inflation. However, amid this new data, it’s important to keep two things in mind:

Two considerations for health care leaders

New data only captures baseline compensation.Differentials—which organizations must standardize and expand across shifts, specialties, and even settings—plus overtime put baseline compensation much higher. Not to mention lucrative sign-on bonuses, that members tell us are increasingly table stakes in their markets. In general, we don’t recommend this type of incentive that does nothing for retention. You’re better off investing those resources in baseline compensation as well as beefing up your RN bonus plan to incentivize retention.

There is a new floor for wages (and it’s only going up from here).

Open questions (and important indicators) we are assessing

What happens to wages for entry-level clinical roles? As the shortage of RNs persists, organizations will need to make a shift to team-based models of care, and those are only possible with a stable workforce of entry-level personnel. Right now, that part of the health care workforce is anything but stable. When you consider their work and their wages in comparison to out-of-industry players that pay the same or better, that’s a clear area where investment is required.

Will the share of nurses working permanently with travel agencies return to pre-pandemic levels? That’s to say, what will those RNs who experienced the traveler lifestyle and pay value more moving forward: the flexibility and premium pay or stability of permanent employment? Even if this number stabilizes a couple percentage points above pre-pandemic levels, that will aggravate provider’s sense of shortage.

The healthcare industry is now at the peak of the long-awaited transition of the Baby Boom generation into Medicare. The “greying” of the Boomers will continue to bring a rapid influx of new Medicare beneficiaries, but this is just the beginning of a protracted period of growth for the program, with the number of Medicare-eligible Americans increasing by more than 50 percent over the next three decades.

Using data from the US Census Bureau, the graphic above shows how the generational makeup of the Medicare population will change across time. The next decade will bring the fastest growth, as the latter half of the Baby Boom generation turns 65. Over that time, the Medicare-eligible population will increase by almost a third. Gen X will begin to age into Medicare in 2029. (Go ahead, take a minute. It hurts.) While fewer in number, Gen X beneficiaries, combined with the longer lifespan of Baby Boomers, will bring no respite from Medicare growth, with enrollment still increasing 11 percent between 2030 and 2040.

As the country looks at a prolonged period of Medicare cost growth, we’ll be counting on a ballooning workforce of Millennials and Gen Z youngsters—each part of generations even larger than the Baby Boom—to continue to fund the Medicare trust across the next 25 years, when the first Millennials will receive their Medicare cards. (See how it feels?)

The US now has more job openings than any time in history—and the mismatch in workforce supply and demand in the broader economy is even more acute in the healthcare sector. While the industry saw significant job losses in April 2020, employment in many healthcare subsectors quickly rebounded to slightly below pre-pandemic levels, according to data from the Bureau of Labor Statistics.

While ambulatory and hospital employment has mostly recovered, employment in nursing and residential care facilities has continued to decline.

Healthcare’s sluggish return to pre-pandemic employment levels is not for lack of demand. The number of job listings has grown nearly 30 percent since the second quarter of 2020, to nearly 4.5M openings, while new hires have flatlined, resulting in over half of healthcare job listings remaining unfilled as of Q2 2021.

In a recent McKinsey & Company survey of over 100 large US hospitals, health system executives ranked workforce shortages among nurses and clinical staff as their greatest barrier to increasing capacity.

Amid the current COVID surge, many systems are offering sizeable bonuses to attract new employees. These strategies will be critical across the next year, as systems look to reduce spending on costly travel nurses, manage COVID surges while continuing to offer elective care, and forestall further burnout.

But longer term, rethinking job functions, integrating new technology and finding ways to educate and upskill critical clinical talent will be key to winning the war for talent.

The signs of progress are encouraging, but the metrics are still down slightly when compared to last month.

Slowly, the financial health of the nation’s healthcare institutions are improving. Hospitals and health systems continued to see performance improvements in April compared to the devastating losses experienced in the early months of the COVID-19 pandemic.

Hospital margins, volumes, and revenues were up across most performance metrics, both year-to-date and year-over-year, but were down compared to March, according to the latest issue of Kaufman Hall’s National Hospital Flash Report. There was no explicit reason given for the dip, but any number of factors small and large could play into the results. It’s possible that clearer trend lines will develop over time.

WHAT’S THE IMPACT?

While any signs of progress are encouraging, the April results draw a clear contrast to the severity of record-low performance seen during the first two months of the pandemic in 2020, rather than strong overall performance so far this year.

Operating margin, for example, rose 101.9% (or 8.6 percentage points) compared to January-April 2020, not including federal Coronavirus Aid, Relief, and Economic Security Act funding. With the funding, operating margin was up 90.6% year-to-date, or 6.9 percentage points.

Operating margin was up 113.1% (39.3%) without CARES and 109.5% (21.4%) with CARES, compared to the first full month of the pandemic in April 2020, when nationwide shutdowns and broad restrictions on outpatient procedures caused operating margins to plummet 282% year-over-year.

April 2021 hospital margins, however, remained relatively thin. The median Kaufman Hall hospital operating margin index was 2.4% for the month, not including CARES. Even with the funding, it was 3.3%.

When it came to volumes, hospitals saw them increase across most metrics compared to 2020 levels, but decrease slightly compared to March. Adjusted discharges were up 5.9% year-to-date and jumped 66.4% year-over-year, while adjusted patient days rose 10% year-to-date and 64.8% year-over-year. Both metrics fell 1% month-over-month.

Emergency department visits were mixed, falling 7% compared to the first four months of 2020, but rising 57.2% year-over-year and 5.3% month-over-month. Operating room minutes were down 3.6% from March, but increased 26.1% year-to-date, and shot up 189.2% compared to April 2020, when COVID-19 abruptly halted most outpatient procedures.

Revenues followed a similar pattern, with gross operating revenue (not including CARES) up 16.7% year-to-date and 71.8% year-over-year, but down 2.5% compared to the prior month. Inpatient revenue rose 10.6% year-to-date and 37.1% year-over-year, but was down 1.9% month-over-month. Outpatient revenue rose 20.3% year-to-date, jumped 114.8% compared to April 2020, but fell 2% from March.

Total expenses continued to increase both year-to-date and year-over-year, but saw moderate decreases month-over-month. Total expense was up 6.6% year to date and 13.1% year over year. Total labor expense increased 6.1% year-to-date and 9.4% year-over-year, and total nonlabor expense rose 7% year-to-date and 16.3% year-over-year.

Compared to March, though, all three metrics were down about 3%. Expense results were mixed when adjusted for the month’s volumes. Total expense per adjusted discharge, for example, increased 2% compared to January-April 2020, but fell 32.3% from April 2020 and 2% from March.

THE LARGER TREND

Despite the ongoing pandemic, the 2021 financial outlook for the global healthcare sector is mostly positive, as strong demand for products and services – including those related to COVID-19 – will more than offset lingering pressures from the public health emergency, Moody’s Investors Service found in December.

The demand will remain strong, largely due to aging populations, the improvement in access and the introduction of new and innovative products. There is one caveat: steadily rising healthcare expenditures, which will cause payers to continue to restrict utilization and lower prices.

In October, Moody’s found that owning a public hospital during the COVID-19 pandemic carriedoperational risk, which will compound the fiscal and credit difficulties facing many large urban counties across the U.S.

Whether recovery from the coronavirus this year is relatively rapid or relatively slow, America’s hospitals will face another year of struggle to regain their financial health.