Recently published in Stat, this article outlines how the launch of telehealth platforms by pharmaceutical companies, most notably Eli Lilly’s LillyDirect, portends a gamechanger for DTC prescription marketing.

Spurred by the escalating demand for Eli Lilly’s Zepbound and Mounjaro GLP-1 drugs, LillyDirect connects consumers with a third-party telehealth provider for prescriptions, an online pharmacy for fulfillment, and in-house payment support through streamlined coupon applications and prior authorization troubleshooting. In exchange, Eli Lilly gets access to reams of patient data, in addition to boosted sales. Pharma companies insist that the platforms have proper firewalls in place, as no money directly changes hands between them and their affiliated telehealth providers.

The Gist:With so manyothercompanies hopping on the GLP-1 virtual prescription bandwagon, it’s no wonder why pharma companies are opting to enter the market directly. What LillyDirect offers is not fundamentally different than platforms like Ro or Teladoc: using telehealth to blur the lines between prescription and over-the-counter medications by empowering consumers to seek out the care they want.

However, Eli Lilly’s control of the drug supply, ability to offer coupons, relationships with pharmacy benefit managers, and inherent brand association with the drugs give it a leg up on the competition.

By replacing “talk to your doctor about” with “visit our website for”, these consumer-focused platforms perpetuate the ongoing fragmentation of care and risk tapping into the potentially harmful side of consumerization in healthcare.

Costco is now offering members online health checkups for as low as $29.

The retailer is offering the new service in partnership with Sesame, a direct-to-consumer health care marketplace that connects medical providers nationwide with consumers.

Sesame, in a release, said Costco members beginning Monday can book health care visits directly through their memberships in all 50 states.

The New York-based company said its platform doesn’t accept health insurance because it primarily caters to uninsured Americans and those with high-deductible plans who prefer to pay cash for their health care. It said its model helps keep prices of services low for its users.

The services listed on Costco Pharmacy’s homepage, include virtual primary care visits for $29, health checkups (a standard lab panel and a virtual follow-up consultation with a provider) for just $72 and online mental health visits for $79.

“Quality, great value, and low price are what the Costco brand is known for,” David Goldhill, Sesame’s co-founder and CEO, said in a statement. “When it comes to health care, Sesame also delivers high quality and great value – and a low price that will be appreciated by Costco Members when it comes to their own care.”

Amazon, in August, announced that its virtual clinic was now also available nationwide. Amazon Clinic launched last November offering 24/7 access to third-party health-care providers directly on Amazon’s website and mobile app.

Amazon customers, through the clinic, can access telehealth treatment for dozens of common conditions, such as pink eye, urinary tract infections and hair loss, the retailer said.

Other retailers, including CVS to Walgreens to Walmart, have made similar moves.

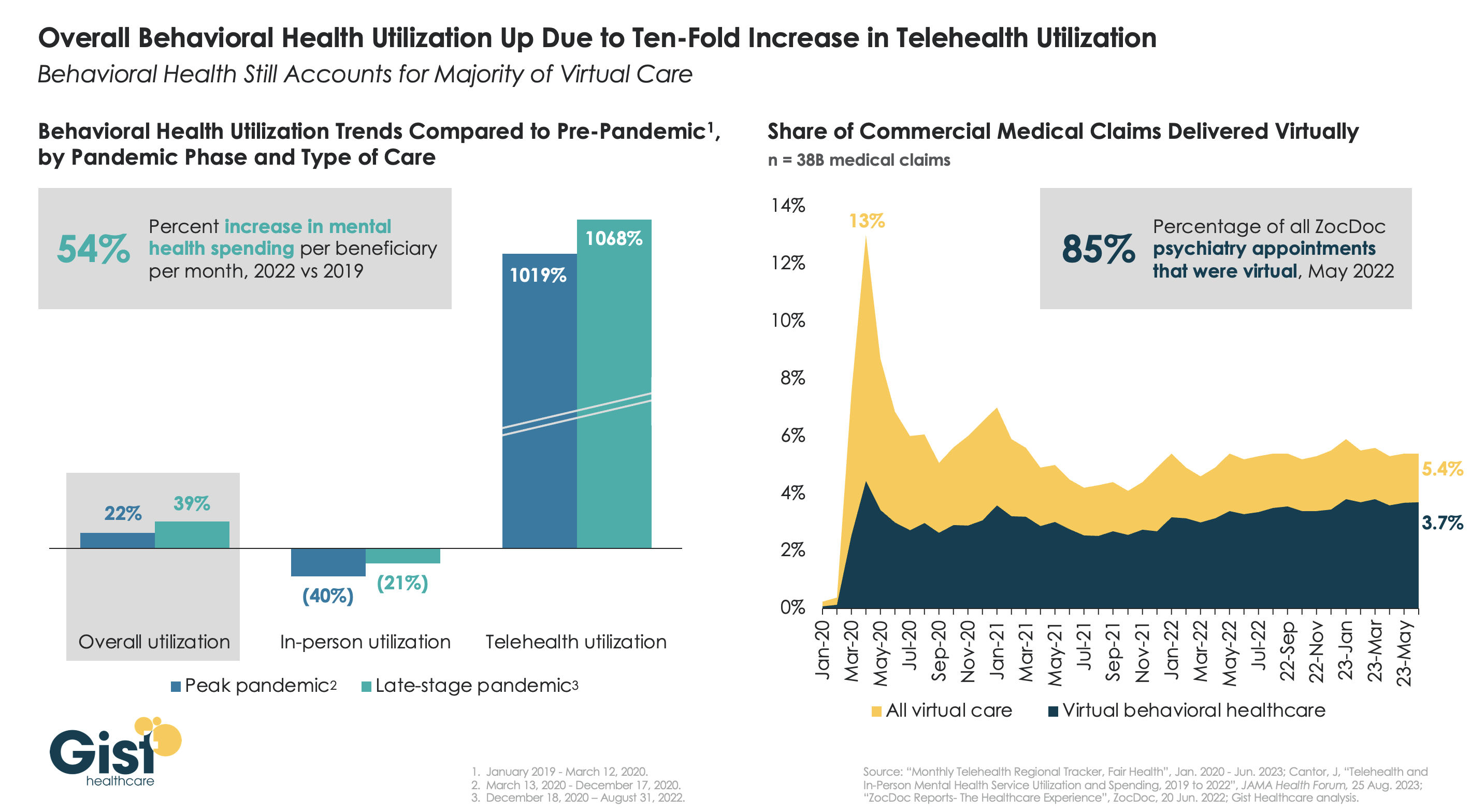

The pandemic worsened the existing mental health crisis in the United States, greatly increasing demand for care. In this week’s graphic, we highlight new data from JAMA Health Forum on mental healthcare trends from 2019 to 2022.

Overall behavioral health utilization increased in 2022 compared to pre-pandemic and peak-pandemic levels, fueled by a ten-fold increase in telehealth usage.

In-person behavioral health utilization decreased early in the pandemic and declines continued in 2022, compared to pre-pandemic levels. Behavioral health still accounts for more than two-thirds of all telehealth visits, a trend that has remained largely unchanged since 2021.

While many consumers and mental health providers continue to embrace telehealth as a means to expand access and increase affordability, a recent Morning Consult survey found that most Americans actually favor in-person visits for quality and efficiency—that is, if they can access it.

Additionally, the future of some types of virtual behavioral healthcare remains murky as the Drug Enforcement Agency (DEA) has yet to establish rules for prescribing controlled substances via telehealth beyond November 2024.

Five years ago, I started the Fixing Healthcare podcast with the aim of spotlighting the boldest possible solutions—ones that could completely transform our nation’s broken medical system.

But since then, rather than improving, U.S. healthcare has fallen further behind its global peers, notching far more failures than wins.

In that time, the rate of chronic disease has climbed while life expectancy has fallen, dramatically. Nearly half of American adults now struggle to afford healthcare. In addition, a growing mental-health crisis grips our country. Maternal mortality is on the rise. And healthcare disparities are expanding along racial and socioeconomic lines.

Reflecting on why few if any of these recommendations have been implemented, I don’t believe the problem has been a lack of desire to change or the quality of ideas. Rather, the biggest obstacle has been the immense size and scope of the changes proposed.

To overcome the inertia, our nation will need to narrow its ambitions and begin with a few incremental steps that address key failures. Here are three actionable and inexpensive steps that elected officials and healthcare leaders can quickly take to improve our nation’s health:

1. Shore Up Primary Care

Compared to the United States, the world’s most-effective and highest-performing healthcare systems deliver better quality of care at significantly lower costs.

One important difference between us and them: primary care.

In most high-income nations, primary care makes up roughly half of the physician workforce. In the United States, it accounts for less than 30% (with a projected shortage of 48,000 primary care physicians over the next decade).

Primary care—better than any other specialty—simultaneously increases life expectancy while lowering overall medical expenses by (a) screening for and preventing diseases and (b) helping patients with chronic illness avoid the deadliest and most-expensive complications (heart attack, stroke, cancer).

But considering that it takes at least three years after medical school to train a primary care physician, to make a dent in the shortage over the next five years the U.S. government must act immediately:

The first action is to expand resident education for primary care. Congress, which authorizes the funding, would allocate $200 million annually to create 1,000 additional primary-care residency positions each year. The cost would be less than 0.2% of federal spending on healthcare.

The second action requires no additional spending. Instead, the Centers for Medicare & Medicaid Services, which covers the cost of care for roughly half of all American adults, would shift dollars to narrow the $108,000 pay gap between primary care doctors and specialists. This will help attract the best medical students to the specialty.

Together, these actions will bolster primary care and improve the health of millions.

2. Use Technology To Expand Access, Lower Costs

A decade after the passage of the Affordable Care Act, 30 million Americans are without health insurance while tens of millions more are underinsured, limiting access to necessary medical care.

Furthermore, healthcare is expected to become even less affordable for most Americans. Without urgent action, national medical expenditures are projected to rise from $4.3 trillion to $7.2 trillion over the next eight years, and the Medicare trust fund will become insolvent.

With costs soaring, payers (businesses and government) will resist any proposal that expands coverage and, most likely, will look to restrict health benefits as premiums rise.

Almost every industry that has had to overcome similar financial headwinds did so with technology. Healthcare can take a page from this playbook by expanding the use of telemedicine and generative AI.

At the peak of the Covid-19 pandemic, telehealth visits accounted for 69% of all physician appointments as the government waived restrictions on usage. And, contrary to widespread fears at the time, patients and doctors rated the quality, convenience and safety of these virtual visits as excellent. However, with the end of Covid-19, many states are now restricting telemedicine, particularly when clinicians practice in a different state than the patient.

To expand telemedicine use—both for physical and mental health issues—state legislators and regulators will need to loosen restrictions on virtual care. This will increase access for patients and diminish the cost of medical care.

It doesn’t make sense that doctors can provide treatment to people who drive across state lines, but they can’t offer the same care virtually when the individual is at home.

Similarly, physicians who faced a shortage of hospital beds during the pandemic began to treat patients in their homes. As with telemedicine, the excellent quality and convenience of care drew praise from clinicians and patients alike.

Building on that success, doctors could combine wearable devices and generative AI tools like ChatGPT to monitor patients 24/7. Doing so would allow physicians to relocate care—safely and more affordably—from hospitals to people’s homes.

Translating this technology-driven opportunity into standard medical practice will require federal agencies like the FDA, NIH and CDC to encourage pilot projects and facilitate innovative, inexpensive applications of generative AI, rather than restricting their use.

3. Reduce Disparities In Medical Care

American healthcare is a system of haves and have-nots, where your income and race heavily determine the quality of care you receive.

Black patients, in particular, experience poorer outcomes from chronic disease and greater difficulty accessing state-of-the-art treatments. In childbirth, black mothers in the U.S. die at twice the rate of white women, even when data are corrected for insurance and financial status.

Generative AI applications like ChatGPT can help, provided that hospitals and clinicians embrace it for the purpose of providing more inclusive, equitable care.

Previous AI tools were narrow and designed by researchers to mirror how doctors practiced. As a result, when clinicians provided inferior care to Black patients, AI outputs proved equally biased. Now that we understand the problem of implicit human bias, future generations of ChatGPT can help overcome it.

The first step will be for hospitals leaders to connect electronic health record systems to generative AI apps. Then, they will need to prompt the technology to notify clinicians when they provide insufficient care to patients from different racial or socioeconomic backgrounds. Bringing implicit bias to consciousness would save the lives of more Black women and children during delivery and could go a long way toward reversing our nation’s embarrassing maternal mortality rate (along with improving the country’s health overall).

The Next Five Years

Two things are inevitable over the next five years. Both will challenge the practice of medicine like never before and each has the potential to transform American healthcare.

First, generative AI will provide patients with more options and greater control. Faced with the difficulty of finding an available doctor, patients will turn to chatbots for their physical and psychological problems.

Already, AI has been shown to be more accurate in diagnosing medical problems and even more empathetic than clinicians in responding to patient messages. The latest versions of generative AI are not ready to fulfill the most complex clinical roles, but they will be in five years when they are 30-times more powerful and capable.

Second, the retail giants (Amazon, CVS, Walmart) will play an ever-bigger role in care delivery. Each of these retailers has acquired primary care, pharmacy, IT and insurance capability and all appear focused on Medicare Advantage, the capitated option for people over the age of 65. Five years from now, they will be ready to provide the businesses that pay for the medical coverage of over 150 million Americans the same type of prepaid, value-based healthcare that currently isn’t available in nearly all parts of the country.

American healthcare can stop the current slide over the next five years if change begins now. I urge medical leaders and elected officials to lead the process by joining forces and implementing these highly effective, inexpensive approaches to rebuilding primary care, lowering medical costs, improving access and making healthcare more equitable.

This annual look at high-impact trends affecting healthcare in the coming year is based on evaluation of current industry research data. Healthcare Finance Trendsfor2023 (Trends) explores eight themes identified by CommerceHealthcare® ranging across four areas:

Financial. Providers enter the year contending with multiple financial stress points. They will also seek growth in technology-enabled remote care.

Patient financial experience. The need to drive not only improvement but also personalization of the financial experience is paramount. A central role will be played by patient financing programs which will see growing demand in 2023.

Trust. Building trust with all constituencies is explored as a linchpin for long-term provider success. The latest findings on cybersecurity show that this contributor to trust will continue to consume leadership attention.

Digital transformation. Pursuit of digital-first operations is accelerating, with the finance area an important focus. Emerging payment modes are finding a home in healthcare’s digital finance landscape.

This report’s consistent message is that these trends intersect in ways that compound both the challenges and the upside potential of strategies that address them.

1. Multiple Financial Stress Points Will Constrain Options

Healthcare’s financial predicament for the next 12–18 months is being described in strong terms. Citing $450 billion of EBITDA that could be in jeopardy, more than half of the industry’s project profit pool by 2027, one analyst suggests “a gathering storm.” Another perceives “broad and serious threats” as “elevated expenses” erode margins and exact “a profound financial toll.” Fitch Ratings issued a “deteriorating” outlook for nonprofit health systems.

These financial headwinds are upending healthcare’s traditional status as “recession-proof.” It is helpful to probe the multiple forces in play, the urgent workforce management challenge, and the varied solution set.

Multiple stress factors at work

Observing that margins will be down 37% in 2022 relative to pre-pandemic, a recent stark assessment concluded, “U.S. hospitals are likely to face billions of dollars in losses — which would result in the most difficult year for hospitals and health systems since the beginning of the pandemic.”

A confluence of factors is exacerbating the stress for 2023:

Rising acuity levels. Over two-thirds of surveyed C-suite executives said patient health has worsened from pandemic-induced delayed care. The upshot, stated by 27% of CFOs, is rising expenses due to higher acuity. Inpatient days are projected to increase at an 8% rate over the coming decade.

Reimbursement gaps and inflation. Commercial and government reimbursement rates are not keeping pace with rising costs. Surging inflation is widening this gap. Hospitals are also reporting substantial insurer payment delays and denials.

Investment declines. Stock and bond market declines have removed a cushion for operating weakness. Market uncertainty will complicate 2023 portfolio management.

Persistent workforce concerns remain center stage

Burnout and shortages have disrupted the clinical workforce. Nearly 60% of physician, advanced practice provider and nurse survey respondents said their teams are not adequately staffed, and 40% lack resources to operate at full potential. Many providers face extreme to moderate shortages of allied health professionals.

The problem extends beyond the clinical. A survey saw 48% of respondents experiencing severe labor deficiencies in revenue cycle management (RCM) and billing, and one in four finance leaders must fill over 20 positions to be fully staffed.

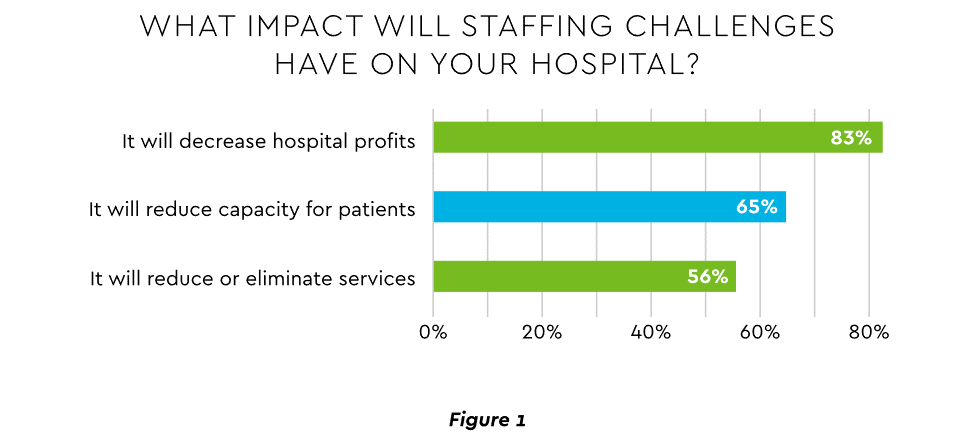

An executive outlook highlighted demonstrable impact on financial performance and growth from these workforce problems, citing reductions in profitability, capacity and service (Figure 1).1

Expenses. Hospital employee expense is expected to increase $57 billion from 2021 to 2022, with contract labor ballooning another $29 billion. Average weekly earnings are up 21.1% since early 2022. Half of medical practices budgeted higher staff cost-of-living increases in 2022. Shortages plague post-acute facilities as well. Their reduced capability to accept discharged patients is lengthening many hospitals’ patient stays.

Capacity constraint. Two-thirds of healthcare leaders identify “ability to meet demand” as their top workforce concern, suggesting a “looming capacity gap between future demand and labor supply.”

Range of measures being deployed

Health systems, hospitals and practices will vigorously pursue at least four direct actions to overcome the financial and staffing hurdles:

Cost cutting. Expense control will be paramount and “hospitals will be forced to take aggressive cost-cutting measures.” McKinsey estimates total industry administrative savings of $1 trillion through multiple aggressive changes.

Service line rationalization. Providers are rethinking how they deliver services to optimize efficiency. One path is utilizing “lower level” healthcare professionals in ways that free RNs and LPAs for more complex work suited to their top skills. Integrating remote care into the mix is another core element of the strategy.

Recruitment and retention programs. Attracting and retaining talent is crucial. Compensation is one avenue. Over two-thirds of organizations are offering signing bonuses for allied health professionals. Some are instituting value-based payments for physicians, offering salary floors to protect from drops in patient volume. CFOs and CNOs are joining forces to invest in nurse retention strategies.

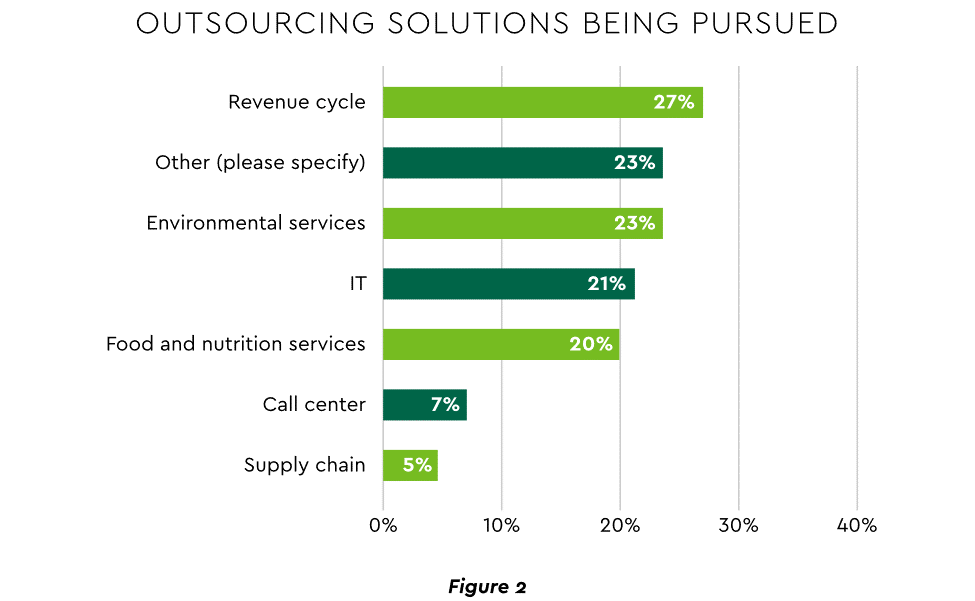

Staffing management. An increasingly popular tool to reduce labor cost and optimize staff resources is outsourcing. Figure 2 shows that RCM is leading the way among those using the solution.

2. Growth Strategies Favor Outpatient, Virtual, Acute Home Care

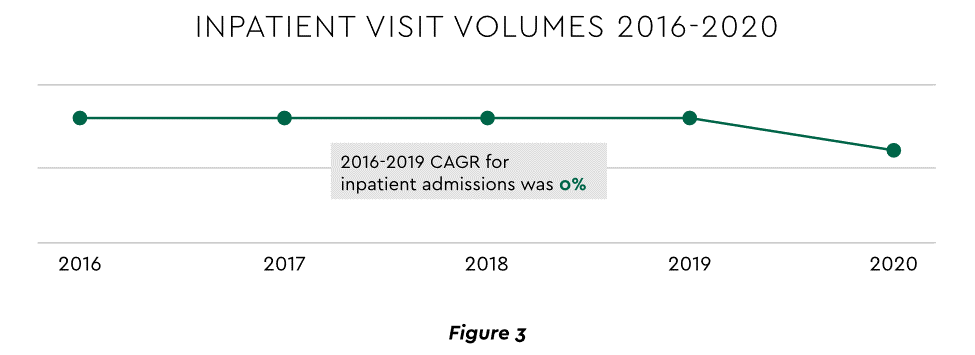

Pursuing top line growth in tandem with reining in expenses is essential. Inpatient volume growth has been tepid for several years ─ essentially flat in the 2016–20 period (Figure 3).

Leaders have been pivoting to outpatient and virtual care to diversify revenue streams. Two high-potential 2023 growth tracks in this sector merit deeper assessment.

Telehealth

Considerable evidence attests to strong commitment to telehealth and remote care. Sixty-three percent of physicians worldwide expect most consultations to be performed remotely within 10 years. Approximately 40% of health centers are using remote patient monitoring today. Consumers are also positive: 94% definitely or probably will use telehealth again, 57% prefer it for regular mental health visits and 61% use it for convenient care.

Telehealth is still in early stages of maturity. Only 4% of surveyed top executives consider their organization proficient at implementing remote care. Healthcare is also recognizing that a full telehealth ecosystem must be constructed. A physician leader explained that the industry’s early telehealth incarnations failed to build “virtual-only environments or really drive e-consults as a way of doing things.” A vital ecosystem demands alterations to current contracts, coding, collections, patient financing, staff training and other business practices.

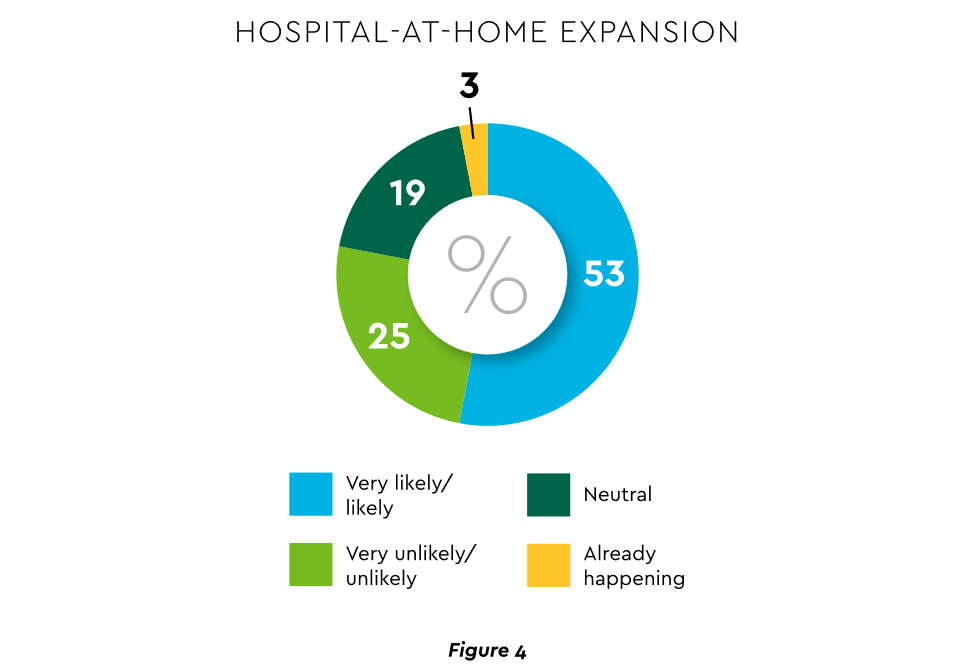

Hospital-at-Home (HaH)

Health systems see particularly promising growth in the provision of acute care in patients’ home settings, including post-surgical and cancer treatment. The federal government has already allowed waivers to 114 systems and 256 hospitals to obtain inpatient-level reimbursement for acute care at home. However, these waivers were prompted by the pandemic and are slated to end in early 2023. The renewal uncertainty has stymied some activity and represents an overhang on the opportunity. However, enthusiasm appears strong, and 33% of hospitals in a recent poll said they would be prone to continue HaH even without renewal.

The forecasts are encouraging. Over half of hospitals believe it likely they will utilize HaH for at least half of their chronically ill patients over the next several years (Figure 4).

Harvesting the HaH potential will require implementation of current and emerging enabling technologies in remote monitoring, high-speed networks and artificial intelligence that generates algorithmic guidance for caregivers and patients alike.

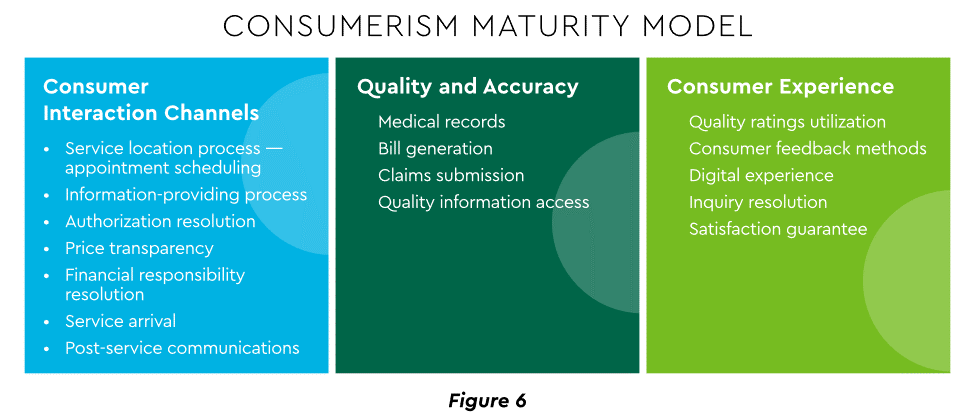

3. Strong Drive to Improve and Personalize the Patient Financial Experience

Today’s healthcare market dynamics place a premium on positive patient experiences. The goal is to deliver “an empathetic relationship between customers and brands built on what the customer wants and how they want to be treated.” It is a complex undertaking, with numerous touchpoints as captured in HFMA’s Consumerism Maturity Model (Figure 6).

An array of studies underscores the value proposition for intense provider focus on patient financial experience:

Sixty-one percent of consumers said that ease of making payments is very or somewhat important in decisions to continue seeing a doctor. Over half of patients also said text message reminders make them very or somewhat more likely to pay a bill faster than usual.

Thirty-five percent of respondents “have changed or would change healthcare providers to get a better digital patient administrative experience.”

A quality financial experience encompasses “simplified explanations, consolidated bills that match one’s health plan benefits, clear language displaying patient liability and payment options.”35

Significantly improving the financial experience requires a unified strategy, not just a collection of individual initiatives. Three threads to such a strategy will be prominent in 2023.

Using a Digital Front Door

Organizations have been moving swiftly to channel many patient financial transactions through an integrated Digital Front Door (DFD). This approach offers patients a singular online point of access and intelligent navigation to needed services. Growth is accelerating. A DFD is their patients’ first contact point for 55% of responding organizations, according to one technology survey. A leading forecaster sees 65% of patients engaging services via digital front doors by 2023.

Expanding price transparency

Mandates for full price transparency and “no surprises” billing are in effect, but estimates of compliance are mixed. An analysis of 2,000 hospitals determined that only 16% met the requirement to post an online “machine readable” file displaying clear charges for 300 “shoppable services.” Another assessment showed a more substantial 76% of hospitals had posted files, and 55% were deemed “complete.” One provision of interest to practices is the “good faith estimate” of expected charges required to be given to uninsured and self-pay individuals when they schedule visits. CommerceHealthcare® has worked with clients to enhance the patient financial experience by complementing their website pricing data with clear information on patient financing options and enrollment access. Bill pay information can also be added for one-stop guidance.

Personalizing the experience

Beyond choice and convenience, the deeper objective is truly personalized experiences throughout the care journey. The words of leading analysts best define the drive to personalize:

“Tomorrow’s healthcare experience will be built by patients tailoring their own experience.”

“By 2024, 30% of chronic care patients will truly own and openly leverage their personal health information to advocate for, secure, and realize better personalized care.”

Opportunities abound to personalize the patient financial experience. Automating manual processes establishes a foundation. Patient financing with no- or low-interest credit lines and flexible terms can produce monthly payment schedules tailored to each patient’s needs. Refunds can be made through multiple payment modes to meet varying patient preferences.

4. Evidence Underscores Growing Demand for Patient Financing

Emphasizing patient financing as part of the overall experience is powerful. Patients continue to struggle paying for care. Recent granular data details three related forces at work.

Meeting care costs difficult for many patients

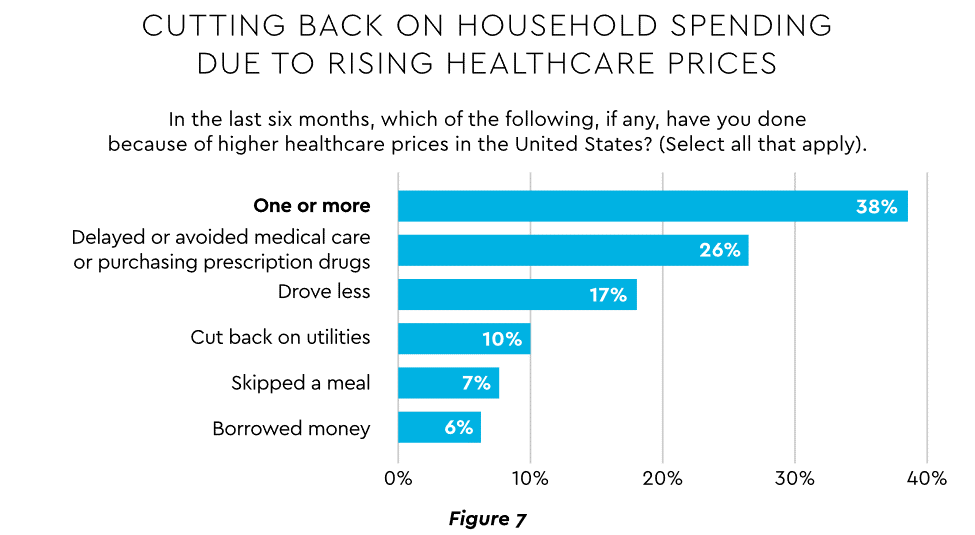

Commonwealth Fund found that 42% of individuals had problems paying medical bills or were paying off medical debt during the past year, while 49% were unable to pay an unexpected $1,000 medical bill.42 Health costs trigger reduction in a range of personal expenditures, led by deferring or avoiding care and drugs (Figure 7).

Twenty-eight percent of Americans now describe themselves as less prepared than last year to pay for routine or unanticipated care.

Patient obligation for care costs still rising

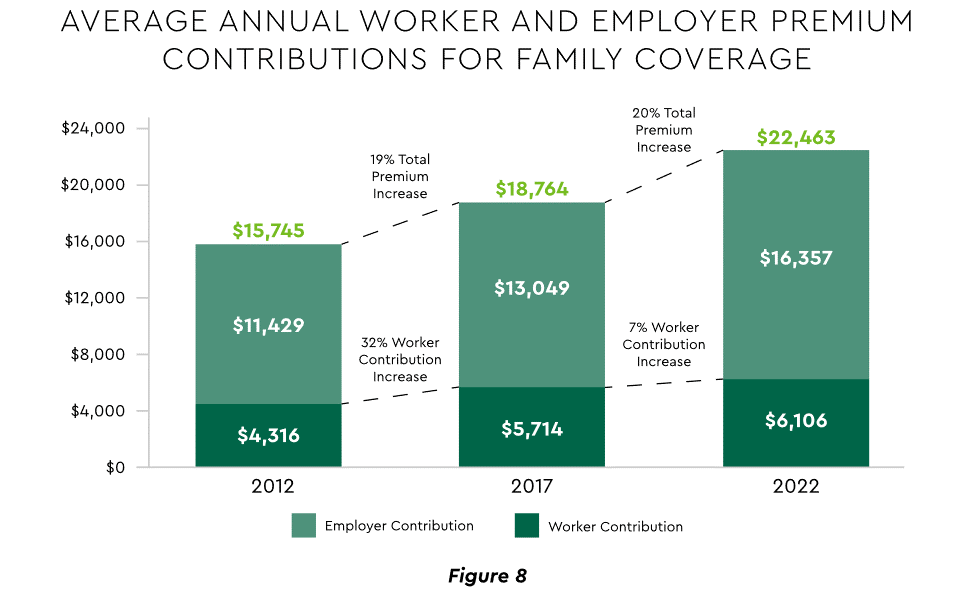

Patient obligation continues its upward march. Insurance premiums have climbed steadily for both the insured and their employers, and employees now pay over $6,000 annually on average for family coverage (Figure 8).45

High deductible health plans (HDHP) also place substantial burden on the patient. Through 2021, 28% of workers were enrolled in an HDHP with an average family deductible of $4,705. Employer satisfaction with these plans is high, auguring further expansion.

Providers feeling the financial effects

Patient payment difficulties are clearly impacting provider financials. A recent in-depth analysis uncovered substantial self-pay issues:

Self-pay accounts represented 60% of 2021 patient bad debt, up from 11% in 2018.

Nearly 18% of patient balances were over $7,500 and 17% over $14,000. Collections were noticeably lower at these balances.

Multiple chronic conditions add to the problem. A recent extensive analysis concluded: “Among individuals with medical debt in collections, the estimated amount increased with the number of chronic conditions ($784 for individuals with no conditions to $1,252 for individuals with 7–13).”

For their part, providers will be encouraged to broaden patient financing programs. Patients are certainly interested. When asked, 62% of consumers indicated they would use financing options or creative payment plans if available for large bill amounts. Many health systems, hospitals and practices will turn to outside help to satisfy the demand. A recent analysis recommended that health systems “consider keeping shorter-term payment plans in-house and extended term plans through external partnerships.”

Organizations will also need to step up their communications. A survey revealed that 64% of patients were unaware that their doctors and hospitals offered payment plans or financial help.

5. Building Trust Becoming a Critical Success Factor

Trust has emerged as a paramount issue today for most organizations as they encounter an “imperative to build trust and transparency among different stakeholder groups — employees, customers, suppliers, regulators and the communities in which they operate.” Healthcare is no exception, and the trust issue is growing in both complexity and urgency.

Healthcare’s trust gap

Trust in healthcare took a hit from the COVID-19 experience. A spring 2022 HFMA survey recorded 44% of finance leaders saying they perceived decreased patient trust. Between April 2020 and December 2021, the percentage of Americans who trusted information from doctors “a great deal” declined by 23%, from hospitals 21%, and from nurses 16%. The patient financial experience also faces “drivers of mistrust,” according to surveyed leaders who cited general payment confusion (58%), surprise billing (39%), high prices of commodity items (28%) and lack of price transparency (26%). Building trust reaps dividends. People who trust their providers are five times more likely to stay with them than those who are neutral or distrustful.

Strategies for building trust

Industry experts promote several approaches to galvanize trust among all constituencies:

Commitment. Embedding trust deeply in the organization requires full support from senior leadership.

Data transparency and governance. IDC predicts that “by end of 2023, 20% of expenses on care integration solutions will be centered around ‘trust’ to protect data, workflows and transactions.”

Reliance on fewer business partners. Many health systems, hospitals and practices are reducing their number of vendors in order to focus on a set of trusted long-term partners. For example, almost two-thirds of surveyed providers said they were seeking to streamline the number of software solutions over the next year.

The bank partner advantage

A provider’s banking relationship can yield valuable collaboration in the trust-building endeavor. Banks enjoy solid trust among consumers. As an example, 53.4% of consumers rated banks as most trusted to provide payment “super apps” and financial digital front doors ─ exceeding the next closest source by 10 points.

6. Cybersecurity in 2023: No Rest for the Weary

Cybersecurity is part of the trust calculus and has become an evergreen topic in healthcare. Compromised data and ransomware attacks are ongoing and leaders must continually refine their understanding in at least three areas: the overall security landscape, particular financially related considerations and contemporary security defenses.

The current landscape

The latest statistics quantify the cyber assault on healthcare:

Incidence. 89% of organizations suffered at least one attack in the past 12 months with the average number at 43.

Cost. A provider’s most serious attack costs an average of $4.4 million. IBM calculated healthcare’s average total cost of a breach at $10.1 million, up 42% since 2020.

Attack Characteristics. Healthcare data types most commonly compromised are personal (58%), medical (46%), and credentials (29%). Organizations have an exposure to an average of over 26,000 network-connected devices. A disturbing finding is that those healthcare institutions that paid ransom got back only 65% of their data in 2021.

Specific financial considerations

Finance leaders will also need awareness of the following:

Cyberattacks could affect credit ratings and are often a component of Environmental, Social and Governance assessments.

Financial outsourcing requires monitoring. A recent news story chronicled an accounts receivable firm’s breach that exposed individual information, account balances and payments.

Cyber insurance premiums are likely to increase substantially.

Responses/tools

Beyond a host of management and monitoring tools being deployed, a strategic philosophy is rapidly gaining ground. The “zero trust” model sounds counter to the trust-building mindset described earlier, but it has become essential. It “denies access to applications and data by default,” and 58% of hospitals and health systems have a zero trust initiative in place. Another 37% intend to implement one within 12–18 months.

Cybersecurity investment will challenge CFOs in 2023, especially in areas such as talent. Cybersecurity worker availability is estimated to satisfy only 68% of open positions. Banking partners will also be expected to play an important role. Over the years, major banks have become “leaders in enhancing cyber strategy and investing in cyber defenses, processes and talent.”

7. Digital Transformation of Finance In Focus

Digital transformation is fundamental to healthcare’s business and care delivery model changes. IBM’s website succinctly captures the goal, “Digital transformation means adopting digital-first customer, business partner, and employee experiences.” A leading forecaster believes 70% of healthcare organizations will rely on digital-first strategies by 2027.

Transformation efforts need to accelerate. One study showed that “digital, technology and analytics strategies exist for nearly all organizations, yet only 30% have begun to execute on those plans.”

One functional segment ramping up digital transformation is finance. According to a recent survey, 94% of CFOs and senior leaders stated that such efforts will be at the forefront of financial operations and strategy for 2023–2024, and 79% described it as an “absolute need” for “commercial stabilization and long-term survival of their healthcare organization.”

Advanced technology is gaining traction. Many see optimization in combining robotic process automation (RPA), artificial intelligence and machine learning to create “intelligent automation.” Together, these technologies create algorithms to automate decisions that guide “robotic” software to perform financial actions and thereby reduce manual labor.

Getting to digital-first in finance and across the enterprise has several critical success factors. These include sustained commitment, a platform-centric mindset and effective governance.

Commitment

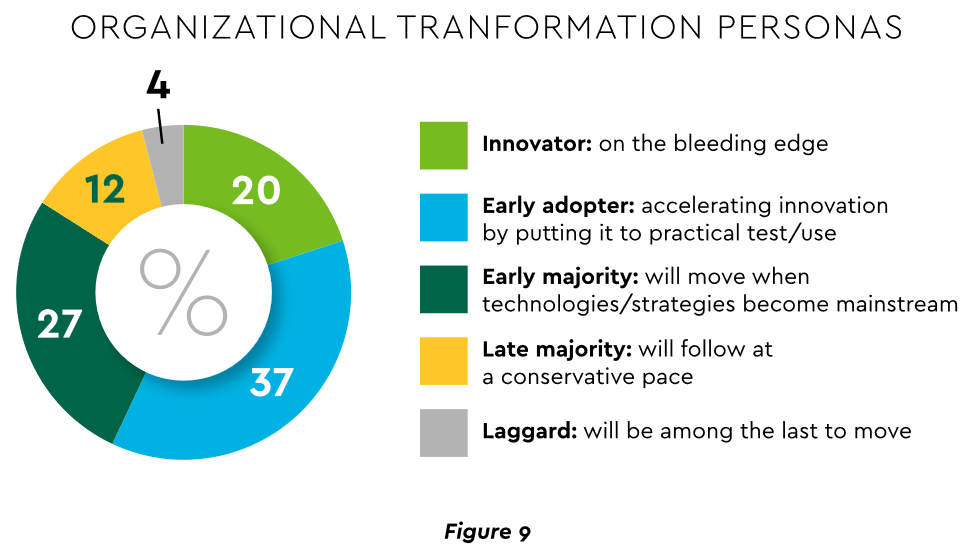

Some assert that few healthcare executives have “created digital strategies that look far enough into the future.” Speed of change is also important. Health systems, hospitals and practices exhibit varying risk appetites and change rates. When asked to self-identify “transformation personas,” a little over half regarded themselves as being on the innovative “early mover” end of the spectrum, while the remainder will adapt as technologies prove themselves (Figure 9). Slower organizations will likely need to increase the pace.

Implementing enterprise platforms rather than proliferating “point solutions” is obligatory. Organizations must be “prepared to compete in the platform economy as platform-based business models have changed the way we live, work and receive care.”

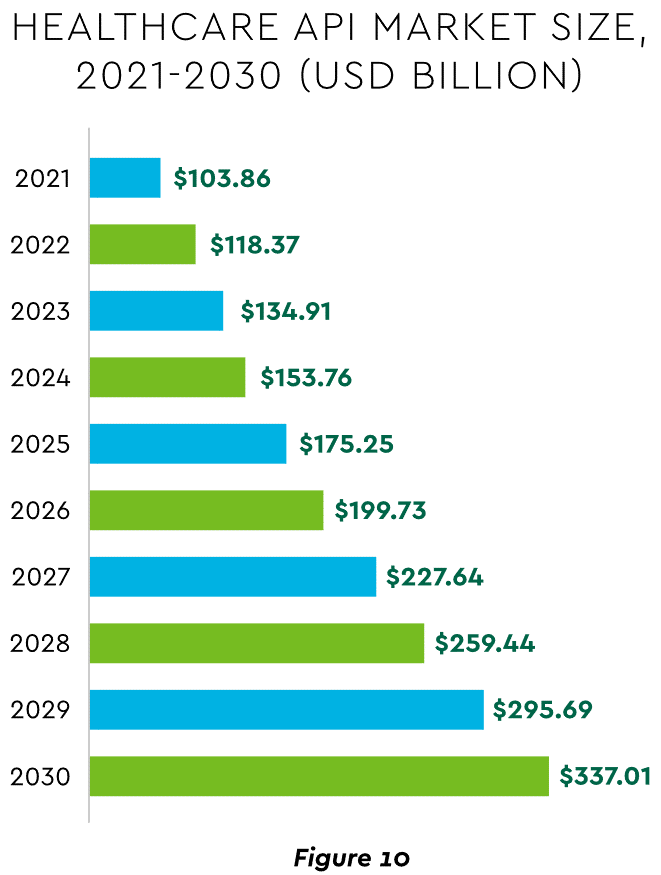

There are still too many tools and applications. A survey of top decision-makers at health systems found that 60% use over 50 software solutions just in operations (24% have over 150). System integration is one answer. Use of application programming interfaces (API) helps this effort substantially. API-first is fast becoming the norm among solution providers, with global API investment expected to nearly triple by 2030 (Figure 10)

Effective governance is vital to constructing a platform-based transformative model and to ensuring wide user adoption. Healthcare has seen the rise of new senior roles such as Chief Digital Officer and Chief Transformation Officer, positions focusing on initiatives like ownership of technology success at the department level and devising user incentives.

8. Digital Payments on the Horizon for Healthcare

A variety of emerging digital payment modes will further the transformation of finance. These payments are expected to grow almost 23% annually in healthcare. ACH payments have been on a strong upward trajectory in healthcare for several years, especially for business transactions. In 2021, ACH tallied a yearly increase of 18% in volume and 5% in dollars.

Notable technologies and payment rails to watch for expected crossover from consumer markets to healthcare include:

Mobile payments. The market for mobile payment technologies has been growing at a 16% compound annual clip and should reach $90 billion in 2023, powered by wide smartphone use, 5G networks and convenience. This category encompasses technologies such as e-wallets, forecasted to grow 23% annually worldwide through 2030.

Real-time payments (RTP). These digital transactions are settled nearly instantaneously through platforms such as The Clearing House. One forecast sees 30.4% compound RTP growth in the U.S. from 2022 to 2030.

Buy Now Pay Later (BNPL). This growing mode offers consumers short-term financing to stretch payments over several installments. A recent survey established that 23% of American adult respondents have used a BNPL service. BNPL is just entering healthcare and is currently regarded as an option for certain elective or cosmetic procedures or for specific individual credit scenarios.

Earned Wage Access (EWA). Using an RTP approach, employers are beginning to offer on-demand pay which enables “instant access to earned wages right after the work is performed, at the end of the shift, or upon completion of a project.” It is not a loan or advance pay. A 2021 poll conducted by Harris found that 83% of U.S. workers feel they should be able to access earned wages at the end of each day. Millennials were particularly interested: 80% would like daily automatic pay streaming to their bank accounts, and 78% said free EWA would boost loyalty to their employer. Given its pressing workforce concerns, healthcare is likely to find EWA a tool to promote retention.

Seeking the right use cases for these payment technologies offers many potential provider benefits.

Conclusion

The connected forces discussed and quantified here create major challenges to address in 2023. The strategic agenda calls for balancing tight cost control with investment in growth opportunities, significantly enhancing patient financial experience by meeting growing patient financial need, shoring up trusted relationships and cybersecurity, and accelerating the digital transformation of finance.

In January 2023, the Rockefeller Institute published a three-part blog series on trends to watch in healthcare in 2023. The series covered broad issues related to the healthcare workforce, economy, and health policy, and highlighted internal industry changes and trends in service delivery, quality, and equity.

Here, we provide a recap and mid-year update on those trends.

The Public Health Emergency:

In January, we anticipated the COVID-19 federal public health emergency (PHE) would end at some point during the year and its ending would impact the industry by rolling back flexibilities and programs that were temporarily put in place to combat the pandemic. The end of the PHE, while not a “trend” per se, held significant potential to alter the trajectory of trends in healthcare coverage, access, and care delivery that were occurring during the pandemic.

Mid-year Update: As predicted, the PHE was not renewed and ended on May 11, 2023. The most notable impact of the non-renewal of the PHE was the end of continuous Medicaid public health insurance coverage. The Kaiser Family Foundation’s Medicaid Enrollment Tracker shows that, as of July 5, 2023, 1,652,000 Medicaid enrollees were disenrolled by the District of Columbia and 28 states reporting data. For context, this means that 39% of people with a completed renewal were disenrolled in reporting states, though disenrollment rates varied significantly across those states from 16 percent in Virginia to 75 percent in South Carolina. The eligibility redetermination process that can lead to a potential disenrollment is being conducted differently in each state with some states moving quickly to make redeterminations and others doing the process more deliberately over the course of the year with a clear intent to avoid shedding people from the Medicaid program because of an inability to submit administrative paperwork.

The process for eligibility renewals will continue to play out over the course of the next year since states have until mid-2024 to update all Medicaid enrollees’ eligibility status. Also notable are some changes made under the purview of the PHE that persist despite the emergency’s conclusion. For example, access to COVID-19 vaccinations and certain COVID-19 treatments generally have not been affected. Some telehealth flexibilities that were allowed under the PHE are also staying in effect, at least until the end of 2024.

Healthcare Workforce Shortages:

Prior to the pandemic, larger demographic trends in society were already impacting the supply of the healthcare workforce. The number of people aging and needing healthcare services was growing while the number of people available to provide care was not keeping pace thus creating a long-term healthcare workforce shortage.

Mid-year Update:The workforce shortage continues. As outlined in a May 23rd Becker’s Hospital Review article, several sources point to a continued shortage. They include a report that says the US could see a deficit of 200,000 to 450,000 registered nurses by 2025. Within the next five years, another report also projects a shortage of more than 3.2 million lower-wage healthcare workers, such as medical assistants, home health aides, and nursing assistants. As a result, some healthcare providers are becoming more creative in their efforts to counteract the workforce shortage: creating alumni networks from which to recruit or providing other benefits to their workforce, such as housing or educational assistance. Policymakers can help counteract the negative impacts of the workforce shortage through a variety of strategies. With the shortage expected to continue, it will be important to enact additional policies that bolster the workforce.

Price Inflation:

As we noted, price inflation was significant in 2022 but was not unique to the health sector.Inflation was particularly exacerbated by the re-opening of the economy after the pandemic, the continued war in Ukraine, and supply chain challenges.

Mid-year Update: Prices for many consumer goods and services increased faster than usual, with overall inflation reaching a four-decade high in mid-2022. The Bureau of Labor Statistics (BLS) reported inflation rates have slowed, with overall prices growing by 6 percent in February 2023 compared to the previous year. Interestingly, prices for medical care increased only 2.3 percent. Similarly, BLS reported that the average price of health care in the United States increased by 0.7 percent in the 12 months ending May 2023, following a previous increase of 1.1 percent. The slower price growth in healthcare compared to other sectors of the economy is highly unusual,[i] and while inflation is not easily influenced by state-level policymakers’ actions alone, the trend is still worth monitoring to better understand the impacts on healthcare access and quality. As of early July, the latest predictions from PwC are that healthcare costs will rise 7% in 2024.

Declining Margins at Hospitals:

Previous analysis by the consulting firm Kaufman Hall predicted that more than half of all hospitals would have negative margins at the end of 2022. As we noted, this was due to such factors as higher-than-normal expenses for staff, supplies, and pharmaceuticals and lower revenues.

Mid-year Update: The latest report from Kaufman Hall offers data that shows a reversal in this trend for the first part of 2023. May was the third consecutive month in which hospital margins were positive after operating in the red for most of 2022. The return to normal is largely driven by revenues that are more in line with pre-pandemic levels. With revenues returning to more normal levels, expenses will be particularly important to watch for the remainder of 2023. If hospital expenses continue to outweigh revenues, policymakers may need to evaluate the financial health of providers and the potential impact that may have on access to services for patients.

Private Equity in Healthcare:

We predicted that private equity (PE) would continue to grow in healthcare, pointing to a PwC consulting report that indicated that PE companies still had plenty of “dry powder,” or money, to invest in 2023.

Mid-year Update:There has been a slowdown in private equity deals over the last year. But it is notable that there were still 200 private equity deals in healthcare in the first quarter of 2023, according to PitchBook’s healthcare services report released in May 2023. While lower than the year before, this is still considered active when compared to pre-pandemic PE dealmaking. Because of the waning of the pandemic and stability returning to the healthcare sector, it is more likely that PE deals stabilize in 2023. And some industry predictions indicate that dealmaking will bounce back further in the second half of 2023. As noted in our previous blog, it will be important to monitor the proliferation of PE in healthcare and determine its impact on healthcare markets, care delivery, innovation, and quality.

Consolidations:

Like many other industries, consolidations of all sorts have been happening in healthcare. The consolidations are both vertical—combining two or more stages of production normally operated by separate companies into one company, such as when hospitals or insurers employ physicians and/or acquire physician practices or other entities like pharmacies—and horizontal—combining organizations that provide the same or similar services, such as hospitals acquiring hospitals.

Mid-year Update: Consolidations of all sorts of healthcare entities continued in 2023 with some of the biggest potential consolidations yet. Those include the proposed merger of two major bi-coastal health system providers: Geisinger, based in Pennsylvania, and Kaiser, based in California. Although the deal must still go through regulatory approval, if completed, the two systems will create a nonprofit that will look to add five or six more systems nationally over the next five years. Other notable consolidations include the finalization of tech-giant Amazon’s purchase of One Medical, a primary care network. And Optum, one of the largest conglomerates that is a subsidiary of United Health Group, increased its net revenue growth by 25% to $54.1 billion in the first quarter of 2023, primarily due to more patients visiting OptumHealth clinics and growth in OptumRx pharmacy scripts processed. Optum’s growth is likely to continue in 2023 as they expect to add another 10,000 physicians. Case in point, in February of this year, Optum paid an undisclosed sum for Crystal Run Healthcare, a network of nearly 400 providers in New York. A goal of consolidation has been better coordination of patient care for improved outcomes and value. Results have been mixed and it is therefore an important trend for policymakers and researchers to monitor and to ensure the impacts are positive.

Alternate Payment Models:

Alternate payment models (APMs) in healthcare have been expanding especially since enactment of the Patient Protection and Affordable Care Act in 2010. They are primarily being developed by the Center for Medicare and Medicaid Innovation (CMMI) which has driven payment policy (including APMs) in the two big government healthcare programs: Medicaid and Medicare. There have been several iterations of APMs—over 50 models—but the one common theme is that all of them generally seek to reward better care.

Mid-year Update: Since the start of 2023, the most notable expansion of the trend toward more alternate payment models was CMMI’s introduction of a new primary care-focused APM called Making Care Primary. In addition to this model, it is expected that the Centers for Medicaid and Medicare Services (CMS), which oversees the operation of these two large public health insurance programs, will introduce more new payment models in 2023, including one that allows states to manage the total cost of care in a given region. This may take various forms, including something akin to Maryland’s global budget, which is used statewide. Since the total cost of care model has yet to be officially revealed, this trend and the emergence of any new developments is worth watching in the second half of 2023. Policymakers can learn from these various payment models and use them to inform the plans implemented in their own state or region in order to improve healthcare.

Attention to Health Equity:

A notable aspect of the pandemic was the disparate impact it had on people of color and other marginalized groups. In response, policymakers and providers began paying more attention to the underlying cause of these disparities. In 2021, President Joe Biden signed an executive order to focus federal resources and attention on reducing health disparities.

Mid-year Update: Increased attention to health equity in healthcare has continued. Ernst and Young, an international consulting group, released its first-ever report on the state of health equity in the United States, which involved a survey of over 500 providers to begin tracking their methods for, and progress in, addressing health disparities. More recently, in June 2023, The Joint Commission on the Accreditation of Healthcare Organizations (JCAHO) announced that it will be adding a certification program for healthcare organizations specifically targeted towards improving health equity. While attention to equity has grown, what will be interesting to watch in the second half of 2023 is the degree to which such efforts are having an impact on actually reducing disparities. Understanding the impacts of various interventions can help policymakers expand efforts that are effective.

Digital TeleHealth Delivery Expansion:

The use of digital health expanded dramatically from 2020 to 2022 as social distancing practices were adopted and telehealth options became more widely available. As noted in our blog series, digital health “includes mobile health (mHealth), health information technology (IT), wearable devices, telehealth and telemedicine, and personalized medicine.” It also includes, “mobile medical apps and software that support the clinical decisions doctors make every day to do artificial intelligence and machine learning.”

Mid-year Update: At the end of 2022 and the start of 2023, the ability to infuse capital to drive the expansion of digital health seemed tenuous, in part due to the collapse of Silicon Valley Bank (SVB). As noted by the publication Pitchbook and CB Insights, venture capital funding in the digital health space totaled $7.5 billion in 2022, a 57 percent year-over-year drop. Although the fast pace of investment in digital health may have slowed since its explosion during the pandemic, the expansion of digital health continues. Our January blog suggested that areas such as behavioral health, care at home, and maternal health were areas to watch. In 2023, digital access is expanding in other areas, such as in-home urgent primary care to allow for the treatment of complex injuries and illnesses with the goal of reducing emergency department visits. And other important digital health deals are still occurring: health tech startup Florence picked up Zipnosis from Bright Health to expand its virtual care capabilities. And with the launch of consumer-facing tech products, such as Chat GPT and Apple Vision Pro in the first half of 2023, additional opportunities for applying such technologies in healthcare may fuel further expansion of digital health. Policies that are developed in the future may want to support the growth of such innovation, while also being mindful to monitor the potential impacts on care.

Expansion of Non-Traditional Providers:

In January, we noted an emergence of companies in healthcare whose genesis was something other than healthcare. The blog pointed to examples of how companies such as Walgreens, CVS, and Amazon were expanding their offerings in healthcare.

Mid-year Update:Non-traditional entities continue to expand in the healthcare space. Notable examples include the recent acquisitions and expansions made by CVS. One of these expansions is being done through its affiliation with the insurance company, Aetna. Through Aetna, CVS has entered the insurance exchange market in four more states in 2023, in addition to the 12 states in which it already operates. CVS also closed a deal in the first half of 2023 to acquire Oak Street Health for over $10 billion. And, in March 2023, CVS announced it had officially acquired Signify Health, a digital telehealth company that enables more care to occur in-home. As noted earlier, Amazon officially completed its deal to acquire OneMedical and United Health Group is working on expanding its use of value-based care through a partnership with Walmart. Monitoring the impact of these emerging companies in healthcare will be important for policymakers that have historically only focused on more traditional providers, such as hospitals. These non-traditional entrants, in many cases, are large organizations with substantial resources and their impact may be just as significant if not greater than traditional providers.

Conclusion

These trends merit close attention in the second half of 2023. As healthcare takes on new shapes, the implications for those in the sector and all who depend on it will be huge. In addition, there are important implications for state and federal policymakers who will need to consider how these trends impact access, affordability, and quality of health care, so they can determine whether and how government might help to accelerate beneficial innovations, invest in promising trends, prevent or reverse harmful trends, and monitor the impacts on consumers.

On Tuesday, the US Preventative Services Task Force (USPSTF), which is appointed by an arm of the Department of Health and Human Services, finalized guidance that all adults ages 19 to 64 should be routinely screened for anxiety, even in the absence of symptoms. Last fall, USPSTF proposed a draft version of this guidance, and also finalized its recommendation that children and adolescents ages 8-18 be screened for anxiety. The task force found that anxiety screening for seniors, as well as suicide-risk screening for all adults, lacked conclusive evidence of effectiveness.

The Gist: Policymakers and providers are right to respond to the nationwide increase in anxiety and depression brought on by the pandemic, and regular screenings will help quantify the scope of a problem we face.

However, given the pervasive undersupply of behavioral health practitioners, widespread screenings will only lead to better care if access to treatment can be scaled.

Solutions that take advantage of telemedicine’s success in behavioral health, combined with the tools—and time—to manage mild anxiety in the primary care setting, are critical to provide support for a coming wave of newly identified patients.

Understand the health care industry’s most urgent challenges—and greatest opportunities.

The health care industry is facing an increasingly tough business climate dominated by increasing costs and prices, tightening margins and capital, staffing upheaval, and state-level policymaking. These urgent, disruptive market forces mean that leaders must navigate an unusually high number of short-term crises.

But these near-term challenges also offer significant opportunities. The strategic choices health care leaders make now will have an outsized impact—positive or negative—on their organization’s long-term goals, as well as the equitability, sustainability, and affordability of the industry as a whole.

This briefing examines the biggest market forces to watch, the key strategic decisions that health care organizations must make to influence how the industry operates, and the emerging disruptions that will challenge the traditional structures of the entire industry.

Preview the insights below and download the full executive briefing (using the link above) now to learn the top 16 insights about the state of the health care industry today.

Preview the insights

Part 1 | Today’s market environment includes an overwhelming deluge of crises—and they all command strategic attention

Insight #1

The converging financial pressures of elevated input costs, a volatile macroeconomic climate, and the delayed impact of inflation on health care prices are exposing the entire industry to even greater scrutiny over affordability. Keep reading on pg. 6

Insight #2

The clinical workforce shortage is not temporary. It’s been building to a structural breaking point for years. Keep reading on pg. 8

Insight #3

Demand for health care services is growing more varied and complex—and pressuring the limited capacity of the health care industry when its bandwidth is most depleted. Keep reading on pg. 10

Insight #4

Insurance coverage shifted dramatically to publicly funded managed care. But Medicaid enrollment is poised to disperse unevenly after the public health emergency expires, while Medicare Advantage will grow (and consolidate). Keep reading on pg. 12

Part II | Competition for strategic assets continues at a rapid pace—influencing how and where patient care is delivered.

Insight #5

The current crisis conditions of hospital systems mask deeper vulnerabilities: rapidly eroding power to control procedural volumes and uncertainty around strategic acquisition and consolidation. Keep reading on pg. 15

Insight #6

Health care giants—especially national insurers, retailers, and big tech entrants—are building vertical ecosystems (and driving an asset-buying frenzy in the process). Keep reading on pg. 17

Insight #7

As employment options expand, physicians will determine which owners and partners benefit from their talent, clinical influence, and strategic capabilities—but only if these organizations can create an integrated physician enterprise. Keep reading on pg. 19

Insight #8

Broader, sustainable shifts to home-based care will require most care delivery organizations to focus on scaling select services. Keep reading on pg. 21

Insight #9

A flood of investment has expanded telehealth technology and changed what interactions with patients are possible. This has opened up new capabilities for coordinating care management or competing for consumer attention. Keep reading on pg. 23

Insight #10

Health care organizations are harnessing data and incentives to curate consumers choices—at both the service-specific and ecosystem-wide levels. Keep reading on pg. 25

Part III | Emerging structural disruptions require leaders to reckon with impacts to future business sustainability.

Insight #11

For value-based care to succeed outside of public programs, commercial plans and providers must coalesce around a sustainable risk-based payment approach that meets employers’ experience and cost needs. Keep reading on pg. 28

Insight #12

Industry pioneers are taking steps to integrate health equity into quality metrics. This could transform the health care business model, or it could relegate equity initiatives to just another target on a dashboard. Keep reading on pg. 30

Insight #13

Unprecedented behavioral health needs are hitting an already fragmented, marginalized care infrastructure. Leaders across all sectors will need to make difficult compromises to treat and pay for behavioral health like we do other complex, chronic conditions. Keep reading on pg. 32

Insight #14

As the population ages, the fragile patchwork of government payers, unpaid caregivers, and strained nursing homes is ill-equipped to provide sustainable, equitable senior care. This is putting pressure on Medicare Advantage plans to ultimately deliver results. Keep reading on pg. 34

Insight #15

The enormous pipeline of specialized high-cost therapies in development will see limited clinical use unless the entire industry prepares for paradigm shifts in evidence evaluation, utilization management, and financing. Keep reading on pg. 36

Insight #16

Self-funded employers, who are now liable for paying “reasonable” amounts, may contest the standard business practices of brokers and plans to avoid complex legal battles with poor optics. Keep reading on pg. 38

While healthcare wasn’t a top priority for lawmakers hammering out the Omnibus bill aimed at keeping the government open through next September, the graphic above outlines the bill’s three greatest areas of impact for providers.

The package reduces the planned 4.5 percent 2023 physician fee schedule cut to two percent, while also extending value-based care bonuses in alternative payment models (albeit at 3.5 percent, instead of five percent). It also delays the $38B Medicare spending cut required by the PAYGO sequester, pushing that cut out two years.

On the telehealth front, the bill extends Medicare’s pandemic-era virtual care flexibilities through 2024, including the “hospital at home” waiver. It also sets April 1, 2023 as the start date of a one-year window for states to reassess Medicaid enrollment,decoupling the start of eligibility redeterminations from the end of the federal COVID public health emergency. Medicaid enrollment grew by 25 percent over the course of the pandemic, but around two-thirds of new enrollees may lose eligibility after redeterminations.

Overall, the legislation is a mixed bag for providers.The uninsured population is expected to grow, at least in the short term. Physician groups had hopes for a complete reprieve from Medicare pay cuts, and the fact that they didn’t get it may signalgrowing Congressional hesitancy to intervene with the Medicare physician fee schedule in the future. But the telehealth extensions may encourage other wider adoption of reimbursement by private insurers, bolstering providers’ long-term virtual care investments.

Radio Advisory’s Rachel Woods sat down with Optum EVP Dr. Jim Bonnette to discuss the sustainability of modern-day hospitals and why scaling down might be the best strategy for a stable future.

Rachel Woods:When I talk about hospitals of the future, I think it’s very easy for folks to think about something that feels very futuristic, the Jetsons, Star Trek, pick your example here. But you have a very different take when it comes to the hospital, the future, and it’s one that’s perhaps a lot more streamlined than even the hospitals that we have today. Why is that your take?

Jim Bonnette: My concern about hospital future is that when people think about the technology side of it, they forget that there’s no technology that I can name that has lowered health care costs that’s been implemented in a hospital. Everything I can think of has increased costs and I don’t think that’s sustainable for the future.

And so looking at how hospitals have to function, I think the things that hospitals do that should no longer be in the hospital need to move out and they need to move out now. I think that there are a large number of procedures that could safely and easily be done in a lower cost setting, in an ASC for example, that is still done in hospitals because we still pay for them that way. I’m not sure that’s going to continue.

Woods: And to be honest, we’ve talked about that shift, I think about the outpatient shift. We’ve been talking about that for several years but you just said the change needs to happen now. Why is the impetus for this change very different today than maybe it was two, three, four, five years ago? Why is this change going to be frankly forced upon hospitals in the very near future, if not already?

Bonnette: Part of the explanation is regarding the issues that have been pushed regarding price transparency. So if employers can see the difference between the charges for an ASC and an HOPD department, which are often quite dramatic, they’re going to be looking to say to their brokers, “Well, what’s the network that involves ASCs and not hospitals?” And that data hasn’t been so easily available in the past, and I think economic times are different now.

We’re not in a hyper growth phase, we’re not where the economy’s performing super at the moment and if interest rates keep going up, things are going to slow down more. So I think employers are going to become more sensitized to prices that they haven’t been in the past. Regardless of the requirements under the Consolidated Appropriations Act, which require employers to know the costs, which they didn’t have to know before. They’re just going to more sensitive to price.

Woods: I completely agree with you by the way, that employers are a key catalyst here and we’ve certainly seen a few very active employers and some that are very passive and I too am interested to see what role they play or do they all take much more of an active role.

And I think some people would be surprised that it’s not necessarily consumers themselves that are the big catalyst for change on where they’re going to get care, how they want to receive care. It’s the employers that are going to be making those decisions as purchasers themselves.

Bonnette: I agree and they’re the ultimate payers. For most commercial insurance employers are the ultimate payers, not the insurance companies. And it’s a cost of care share for patients, but the majority of the money comes from the employers. So it’s basically cutting into their profits.

Woods: We are on the same page, but I’m going to be honest, I’m not sure that all of our listeners are right. We’re talking about why these changes could happen soon, but when I have conversations with folks, they still think about a future of a more consolidated hospital, a more outpatient focused practice is something that is coming but is still far enough in the future that there’s some time to prepare for.

I guess my question is what do you say to that pushback? And are there any inflection points that you’re watching for that would really need to hit for this kind of change to hit all hospitals, to be something that we see across the industry?

Bonnette: So when I look at hospitals in general, I don’t see them as much different than they were 20 years ago. We have talked about this movement for a long time, but hospitals are dragging their feet and realistically it’s because they still get paid the same way until we start thinking about how we pay differently or refuse to pay for certain kinds of things in a hospital setting, the inertia is such that they’re going to keep doing it.

Again, I think the push from employers and most likely the brokers are going to force this change sooner rather than later, but that’s still probably between three and five years because there’s so much inertia in health care.

On the other hand, we are hitting sort of an unsustainable phase of cost. The other thing that people don’t talk about very much that I think is important is there’s only so many dollars that are going to health care.

And if you look at the last 10 years, the growth in pharmaceutical spend has to eat into the dollars available for everybody else. So a pharmaceutical spend is growing much faster than anything else, the dollars are going to come out of somebody’s hide and then next logical target is the hospital.

Woods: And we talked last week about how slim hospital margins are, how many of them are actually negative. And what we didn’t mention that is top of mind for me after we just come out of this election is that there’s actually not a lot of appetite for the government to step in and shore up hospitals.

There’s a lot of feeling that they’ve done their due diligence, they stepped in when they needed to at the beginning of the Covid crisis and they shouldn’t need to again. That kind of savior is probably not their outside of very specific circumstances.

Bonnette: I agree. I think it’s highly unlikely that the government is going to step in to rescue hospitals. And part of that comes from the perception about pricing, which I’m sure Congress gets lots of complaints about the prices from hospitals.

And in addition, you’ll notice that the for-profit hospitals don’t have negative margins. They may not be quite as good as they were before, but they’re not negative, which tells me there’s an operational inefficiency in the not for-profit hospitals that doesn’t exist in the for-profits.

Woods: This is where I wanted to go next. So let’s say that a hospital, a health system decides the new path forward is to become smaller, to become cheaper, to become more streamlined, and to decide what specifically needs to happen in the hospital versus elsewhere in our organization.

Maybe I know where you’re going next, but do you have an example of an organization who has had this success already that we can learn from?

Bonnette: Not in the not-for-profit section, no. In the for-profits, yes, because they have already started moving into ambulatory surgery centers. So Tenet has a huge practice of ambulatory surgery centers. It generates high margins.

So, I used to run ambulatory surgery centers in a for-profit system. And so think about ASCs get paid half as much as a hospital for a procedure, and my margin on that business in those ASCs was 40% to 50%. Whereas in the hospital the margin was about 7% and so even though the total dollars were less, my margin was higher because it’s so much more efficient. And the for-profits already recognize this.

Woods: And I’m guessing you’re going to tell me you want to see not-for-profit hospitals make these moves too? Or is there a different move that they should be making?

Bonnette: No, I think they have to. I think there are things beyond just ASCs though, for example, medical patients who can be treated at home should not be in the hospital. Most not-for-profits lose money on every medical admission.

Now, when I worked for a for-profit, I didn’t lose money on every Medicare patient that was a medical patient. We had a 7% margin so it’s doable. Again, it’s efficiency of care delivery and it’s attention to detail, which sometimes in a not-for-profit friends, that just doesn’t happen.