New Medicaid funding rules proposed by Congress this week would halt efforts at the state level to better fund rural hospitals and deliver services to the most vulnerable populations in those areas. You can be certain that the administrators and staff of those hospitals, as well as leaders of the communities they serve, are watching closely to see if the cuts are enacted.

Lawmakers at the federal level are trying to make deeper cuts to Medicaid spending in an effort to lower the amount of deficit spending that would be created by President Trump’s spending plan. Trump has dubbed the plan his “big beautiful bill.”

Feds Would Strip Rural Hospitals of Lifeline Funds

Republican members of the Senate Finance Committee this week released their version of the bill that would drain funding for rural hospitals, which rely heavily on Medicaid funds to treat patients. It’s estimated that 25 to 40 percent of services provided by such hospitals are funded by Medicaid.

The federal government and states share the up-front medical costs for Medicaid patients. The federal government then reimburses states up to 50 percent of their Medicaid spending every year.

Many states fund their portion of the cost by taxing entities that provide those services to Medicaid patients.

The latest proposal in Congress would not only restrict how many patients could receive benefits, but it would also stop states from implementing those provider tax programs to help fund Medicaid services provided to residents.

At the federal level, the thinking is that if states keep taxing providers to fund Medicaid services, then the federal government will have to keep reimbursing states a portion of those costs.

The downside to that is many experts, along with several Republicans in Congress, namely Sens. Susan Collins of Maine, Lisa Murkowski of Alaska and Josh Hawley of Missouri, have predicted it will decimate rural hospitals.

West Virginia Republican Sen. Jim Justice went a step further, saying that the plan to limit states’ use of provider taxes will “really hurt a lot of folks.” Despite that statement, Justice said he is OK with the freeze.

State Lawmakers Sound the Alarm

There are 39 states with at least three or more provider taxes used to help fund Medicaid services. Alaska is the only state with no such tax.

Some states, such as Ohio, have set up a new rural hospital fund using provider taxes to help rural hospitals deliver Medicaid services to patients.

Ohio Governor Mike DeWine and the Republican-led state legislature set up a pilot program called the Rural Ohio Hospital Tax Pilot Program. The measure would allow counties to levy a tax on their local hospitals that would then be used to fund Medicaid services.

DeWine said the pilot program would help ease the financial stress rural hospitals face in Ohio. The plan contained in Ohio House Bill 96 has the blessing of the Ohio Hospital Association.

A group of Republican state lawmakers recently sent a letter to their federal counterparts pleading with them to remove the bill language because it would “torpedo” plans to keep rural hospitals functioning.

The American Hospital Association, a 130-year-old trade group of more than 5,000 hospitals and health care providers, this month released the impact on rural hospitals if this plan went into effect.

More than $50 billion would be lost by 2034, and more than 1.8 million rural Americans would lose health benefits.

Kentucky residents would be impacted the most, with 143,000 losing benefits, followed by 135,000 Californians. More than 86,000 Ohioans would lose Medicaid coverage under the plan by 2034, making it the third most impacted state.

To blunt the effects of the cuts, Collins reportedly is proposing the establishment of a $100 billion relief fund that could provide financial support to affected providers, rural hospitals in particular. Whether that or a similar but smaller fund will wind up in the final draft of the legislation apparently will be decided this weekend. Meanwhile, the Senate parliamentarian has ruled against many of the provisions of the Senate version of the bill, including the Finance Committee’s provider tax framework, which puts the whole thing in flux.

Senate leaders say they plan a long series of votes on amendments of the bill on Sunday. The “vote-arama” likely will go on throughout Sunday night and into Monday. If the Senate does pass its version of the bill, it will have to go back to the House. Lawmakers are under a self-imposed deadline to get the legislation to Trump by the July 4 holiday.

Medicaid serves as a vital source of health insurance coverage for Americans living in rural areas, including children, parents, seniors, individuals with disabilities, and pregnant women. Congressional lawmakers are currently considering more than $800 billion in cuts to the Medicaid program, which would reduce Medicaid funding and terminate coverage for vulnerable Americans.

The proposed changes would also result in a significant reduction in Medicaid reimbursement that could result in rural hospital closures.

The National Rural Health Association recently partnered with experts from Manatt Health to shed light on the potential impacts of those cuts on rural residents and the hospitals that care for them over the next decade.

NRHA held a press conference on June 24 that can be accessed with passcode MBTZf4$H. NRHA chief policy officer Carrie Cochran-McClain discussed the findings with Manatt Health partner and former deputy administrator at CMS Cindy Mann and the real world implications of the details of this report with three NRHA member hospital and health system leaders

Report findings provide insight into the impact on rural America at a critical moment in the Congressional debate over the future of the reconciliation package.

The report shows the significant impact from coverage losses that rural communities will face given:

Medicaid plays an outsized role in rural America, covering a larger share of children and adults in rural communities than in urban ones.

Nearly half of all children and one in five adults in small towns and rural areas rely on Medicaid or CHIP for their health insurance.

Medicaid covers nearly one-quarter of women of childbearing age and finances half of all births in these communities.

According to Manatt’s estimates, rural hospitals will lose 21 cents out of every dollar they receive in Medicaid funding due to the One Big Beautiful Bill Act. Total cuts in Medicaid reimbursement for rural hospitals—including both federal and state funds—over the ten-year period outlined in the bill would reach almost $70 billion for hospitals in rural areas.

Reductions in Medicaid funding of this magnitude would likely accelerate rural hospital closures and reduce access to care for rural residents, exacerbating economic hardship in communities where hospitals are major employers.

As a key insurer in rural communities, Medicaid provides a financial lifeline for rural health care providers — including hospitals, rural health clinics, community health centers, and nursing homes—that are already facing significant financial distress. These cuts may lead to more hospitals and other rural facility closures, and for those rural hospitals that remain open, lead to the elimination or curtailment of critical services, such as obstetrics.

“Medicaid is a substantial source of federal funds in rural communities across the country. The proposed changes to Medicaid will result in significant coverage losses, reduce access to care for rural patients, and threaten the viability of rural facilities,” said Alan Morgan, CEO of the National Rural Health Association.

“It’s very clear that Medicaid cuts will result in rural hospital closures resulting in loss of access to care for those living in rural America.”

A media briefing will be held on Tuesday, June 24, from noon to 1:00 PMEST to provide more information about the analysis. This event will feature representatives from NRHA, Manatt Health, and rural hospital leaders across the country. Questions may be submitted in advance, as well as during the press conference. To register for and join the media briefing, click on the Zoom link here.

NRHA is a non-profit membership organization that provides leadership on rural health issues with tens of thousands of members nationwide. Our membership includes nearly every component of rural America’s health care, including rural community hospitals, critical access hospitals, doctors, nurses, and patients. We work to improve rural America’s health needs through government advocacy, communications, education, and research. Learn more about the association at RuralHealth.US.

About Manatt Health

Manatt Health is a leading professional services firm specializing in health policy, health care transformation, and Medicaid redesign. Their modeling draws upon publicly available state data including Medicaid financial management report data from the Centers for Medicare and Medicaid Services, enrollment and expenditure data from the Medicaid Budget and Expenditure System, and data from the Medicaid and CHIP Payment and Access Commission. The Manatt Health Model is tailored specifically to rural health and has been reviewed in consultation with states and other key stakeholders.

Hospitals across the country are starting to reckon with the effects President Trump’s tariffs are having on medical supplies like syringes and PPE, and in some cases freezing spending and making other contingencies.

Why it matters:

A global trade war could bring a return to pandemic disruptions if imported goods that health systems purchase in high volumes from China can’t be replenished. And there’s still the prospect of Trump’s tariffs on pharmaceuticals.

Ultimately, experts warn, supply disruptions and price hikes could drive up the price of patient care.

“Tariffs have the potential to add a layer of complication to [hospitals’] ability to get all of those medical goods, the drugs and the devices that they need to deliver care,” said Akin Demehin, the American Hospital Association’s vice president of quality and patient safety policy.

State of play:

So far, there have been no widespread shortages or price spikes.

What most concerns the providers is a reliance on medical gear from China. Enteral syringes used to deliver drugs or nutrition through feeding tubes have no alternative sources and are subject to a 245% tariff, according to group purchasing organization Premier.

“With the consumables — the gowns, the gloves, masks … hospitals go through an enormous volume of those every year. Certainly there is some risk there,” said Kyle MacKinnon, senior director of operational excellence at Premier.

The pandemic spawned more domestic manufacturing of medical gear — and an anticipated reduction in dependence on overseas suppliers. But many of the startups have since disappeared, the New York Times reported, leaving the health system once again vulnerable to supply shocks amid threats like measles outbreaks and avian flu.

Between the lines:

The situation could be further complicated by tariffs on pharmaceuticals that could weigh particularly hard on imported generics.

Cancer and cardiovascular medications, as well as immunosuppressives and antibiotics, are of great concern to hospitals, per a letter the American Hospital Association sent earlier this year to Trump. MD Anderson Cancer Center in Houston instituted a hiring freeze due to uncertainty, in part, from the tariffs’ impact on drug prices.

Medical devices are also facing a high level of exposure with roughly 70% of U.S. marketed medical devices manufactured exclusively outside the U.S., Premier wrote.

The American Hospital Association on Wednesday pointed to data that found 82% of health care experts expect tariff-related expenses to raise hospital costs by at least 15% over the next six months.

94% of health care administrators expected to put off equipment upgrades, in response.

Reality check:

Many hospitals may still be insulated from the worst effects because of long-term purchasing contracts.

Universal Health Services CFO Steve Filton said during an earnings call that three-quarters of the company’s supply chain had fixed contracted prices, Fierce Healthcare reported.

The company had begun to see “fees or stipends” on invoices with vendors with fixed contracted prices but had been ignoring them. “At the moment, it feels like there’s not a great deal of pressure,” he said.

But a dramatic reduction in goods from a major trading partner will eventually hit multiple players needing to replenish inventories, experts predict.

What to watch:

Hospitals are among trade groups lobbying for tariff exemptions for critical medical supplies, including drugs. One question is whether pharmaceutical manufacturers can limit their exposure by “reshoring” more intellectual property in order to pay more U.S. taxes, Leerink Partners wrote in an investor note on Wednesday.

As supplies that have been stockpiled by hospitals begin to run low or as contracted prices expire, the true costs will begin to be felt.

“We especially worry about the potential impacts to vulnerable and to rural health care providers who already are operating on thin margins, and for whom changes in the cost of those kinds of goods could have a disproportionate impact,” Demehin said.

Some of America’s largest hospital systems saw their financials soar in the first half of 2024. And yet, more than 700 facilities across the country still are at risk of closing.

Why it matters:

It’s a familiar tale of the rich getting richer, as big, mostly for-profit health systems see improved margins while smaller facilities in outlying areas are barely hanging on.

That could worsen access for some of the most vulnerable Americans — and hasten consolidation in an industry that’s been a magnet for M&A.

The big picture:

Health systems with big footprints, including large academic medical centers, have weathered the pandemic and economic headwinds and are seeing margins as good or better than before COVID-19.

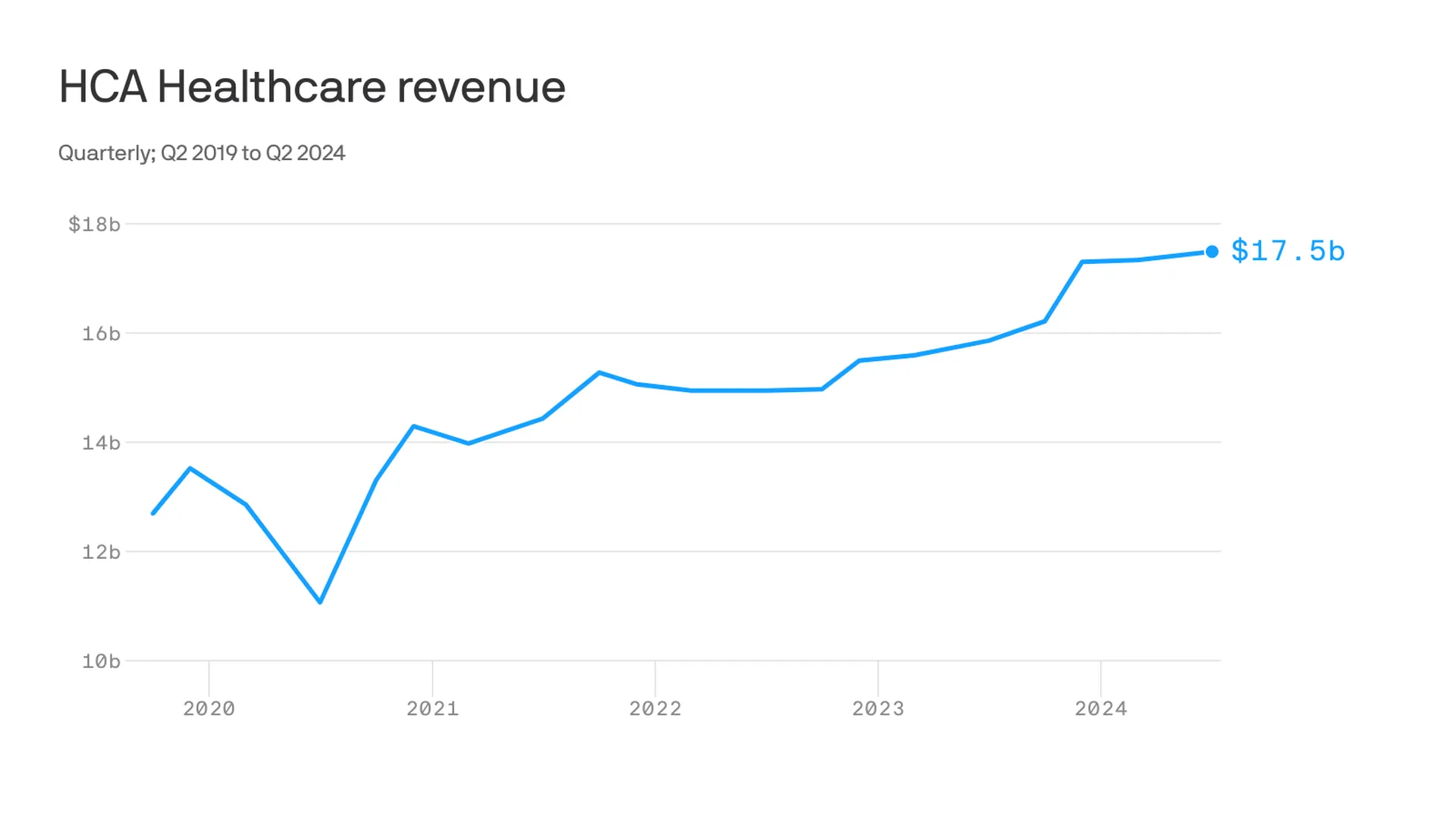

Nashville-based industry behemoth HCA Healthcare posted 23% year-over-year profit growth for the quarter, revising its forecast for the rest of the year, projecting it’ll reach as much as $6 billion. It posted a 10% year-over-year increase in revenue.

King of Prussia, Pennsylvania-based Universal Health Services similarly reported a strong quarter, posting nearly 69% growth on its bottom line over the same period last year while Dallas-based Tenet Healthcare reported a 111% jump in its net income over the same quarter last year.

Yes, but:

Smaller nonprofit hospitals, especially in rural areas, that made it through the crisis with the help of government aid are paring services like maternity wards and struggling to stay open.

“There are a lot of hospitals that survived, but their balance sheets are so weakened, their margin for error is basically zero at this point,” said Mike Eaton, senior vice president of strategy at population health company Navvis.

Hospitals that once could manage their expenses and the needs of communities are “going to really struggle to invest in what comes next,” he said.

Between the lines:

The biggest health systems have benefited from less volatility, seeing stabilizing drug prices and more predictable supply chains and labor costs, per a new report from Strata Decision Technology.

“It’s at least something you can manage to,” Steve Wasson, Strata’s chief data and intelligence officer, told Axios.

Revenues already were up thanks to renegotiated contracts health systems struck with payers last year, Wasson said.

There also have been changes on the federal side that boosted Medicare admissions and put some hospitals in line to be reimbursed for billions in underpayments from the 340B drug discount program.

Zoom in:

It’s all translated to operating margins that are up 17% year-to-date compared with the same time period in 2023, according to the latest Kaufman Hall National Hospital Flash Report.

Volumes as measured by hospital discharges per day are up 4% year-to-date.

Expenses per day are also up 6% year to date, including labor (4%), supplies (8%) and drugs (8%), but are far less volatile and thus easier to plan for, said Erik Swanson, senior vice president at Kaufman Hall.

But there’s a growing gulf between the top third of U.S. hospitals, which are seeing outsize growth, and the rest, Swanson said.

Threat level: A new report from the Center for Healthcare Quality and Payment Reform estimated 703 hospitals — or more than one-third of rural hospitals — are at risk of closure, based on Centers for Medicare and Medicaid Services financial information from July. Losses on privately insured patients are the biggest culprit.

“We’re looking at 50% of rural operating in the red. The situation is very challenging,” Michael Topchik, partner at Chartis Center for Rural Health, told Axios.

These smaller hospitals may still be there, but there will continue to be a steady erosion of the kinds of services they offer, such as obstetrics, cancer care and general surgery, he said.

What’s next:

Private equity investment in rural health care is already booming and with it, prospects for service and staffing cuts.

The South generally has the highest concentration of private equity-owned rural hospitals, often with lower patient satisfaction and fewer full-time staff compared with non-acquired hospitals, according to the Private Equity Stakeholder Project.

Congress is ramping up oversight of private equity investments in the sector, though most lawmakers are loath to take steps to actually halt deals.

For several decades, the economics, demographics, and technology of healthcare have been fueling a trend toward closure of inpatient hospitals.

In the past ten years, from 2014 through 2023, 229 hospitals closed without being converted into other facilities, while only 118 new hospitals opened, according to data provided by MedPAC in its March 2020 and March 2024 reports to Congress.

Rural closures have generated significant concern—justifiably so due to the risk of reduced access to care. Of the 229 hospitals that closed in the past decade, 68 were rural, with an additional 48 closing and converting into other types of care facilities, according to the Sheps Center for Health Services Research at the University of North Carolina. Although the number of rural closures is high, the numbers also show that the issue is by no means confined to rural areas.

The circumstances leading to hospital closures are as serious as they are familiar: rising operating expenses, labor shortages, shifts from inpatient to outpatient care, high-cost technology, flattening reimbursement, an aging population, and population migration.

At the same time these forces are driving some hospitals toward financial distress, they can also create clinical and even safety concerns—including inpatient volume that is reduced to the point where quality may be compromised and an inability to maintain aging physical plants.

These forces are inexorable. Attempting to maintain the status quo is simply not a viable strategy. Unfortunately, a desire to protect the status quo is often what health systems encounter when attempting to close a hospital. This impulse toward protectionism is understandable. Community groups are concerned about losing access to care. Labor groups are worried about losing jobs. Political leaders are concerned about both, and about the continued economic strength of their localities.

In too many cases, these understandable concerns have the unintended consequence of keeping open a hospital that no longer effectively serves its community. In other cases, they make the process of necessary change unnecessarily painful and protracted.

The challenge for healthcare executives and community leaders alike is to figure out a new path forward—one that creates a clinically, operationally, and economically viable approach to providing needed access to high quality care but offers an alternative to complete hospital closure or to a facility continuing to exist in a state of distress.

Recently, we came across a man named Scott Keller, who has spent the past 28 years shaping and implementing what looks to me like a creative and workable path forward for many communities facing hospital closures.

The intellectual underpinning of Scott’s approach is to combine community health, economic development, and neighborhood planning. Through that lens, Scott and his team at Dynamis look to transform hospitals that are no longer viable into community hubs that he calls “Healthy Villages®.”

These hubs address a range of community needs that include some traditional healthcare services, but also social and other community services. They bring these services together—under one roof and extending into the neighborhood—into a careful system that creates an opportunity to develop new care models built on the foundation of value-based, population-based care, prioritizing health, prevention, and elimination of disparities and barriers to care. The aim is to treat the whole person in a walkable, thriving community.

At a macro level, Scott’s approach involves consolidating treatment services into a fraction of the square footage of the existing facility and leasing the remaining space to partners focused on social determinants of health, much like a successful multifaceted retail environment creates an excellent consumer experience.

From there, the hub integrates with other neighborhood partners such as senior housing providers, financial institutions for social-impact financing, and education providers to support workforce training.

Scott explained to us that the approach can be applied in settings from challenged urban neighborhoods to rural towns, at scales from neighborhoods to full towns, and in concert with initiatives such as a health system’s service-line planning. In addition, some of these hubs have unique sources of funding that support the community, funding not typically available to a traditional hospital.

Perhaps the most attractive quality of Scott’s approach is to shift the conversation about a distressed hospital from the binary close-or-don’t close to a thoughtful consideration of what it means to deliver healthcare in a setting that has difficulty supporting a particular hospital.

In doing so, Scott helps us focus on the true issue at hand. America’s economic, demographic, and technological forces are aligned in certain markets to challenge the adequacy of the traditional hospital. The question is not whether this group of hospitals will change, but how they will change.

In too many instances and too many locations, that hospital change becomes an enemy to be fought against, resulting in a transformation that is protractedly painful and that often ends poorly for all concerned. Scott’s approach is a welcome example of how organizations and communities, rather than clinging to the status quo, can apply creative thinking, broad participation, and systematic planning to shape a future that may turn out to be not an enemy, but a real and lasting improvement.

It’s no secret I feel strongly that “Medicare Advantage for All” is not a healthy end goal for universal health care coverage in our country. But I also recognize there are many folks, across the political spectrum, who see the program as one that has some merit. And it’s not going away anytime soon. To say the insurance industry has clout in Washington is an understatement.

As politicians in both parties increase their scrutiny of Medicare Advantage, and the Biden administration reviews proposed reforms to the program, I think it’s important to highlight common-sense, achievable changes with broad appeal that would address the many problems with MA and begin leveling the playing field with the traditional Medicare program.

1. Align prior authorization MA standards with traditional Medicare

Since my mother entered into an MA plan more than a decade ago, I’ve watched how health insurers have applied practices from traditional employer-based plans to MA beneficiaries. For many years, insurers have made doctors submit a proposed course of treatment for a patient to the insurance company for payment pre-approval — widely known as “prior authorization.”

While most prior authorization requests are approved, and most of those denied are approved if they are appealed, prior authorization accomplishes two things that increase insurers’ margins.

The practice adds a hurdle between diagnosis and treatment and increases the likelihood that a patient or doctor won’t follow through, which decreases the odds that the insurer will ultimately have to pay a claim. In addition, prior authorization increases the length of time insurers can hold on to premium dollars, which they invest to drive higher earnings. (A considerable percentage of insurers’ profits come from the investments they make using the premiums you pay.)

Last year, the Kaiser Family Foundation found the level of prior authorization requests in MA plans increased significantly in recent years, which is partially the result of the share of services subject to prior authorization increasing dramatically. While most requests were ultimately approved (as they were with employer-based insurance plans), the process delayed care and kept dollars in insurers’ coffers longer.

The outrage generated by older Americans in MA plans waiting for prior authorization approvals has moved the Biden administration to action.

Beginning in 2024, MA plans may be no more restrictive with prior authorization requirements than traditional Medicare.

That’s a significant change and one for which Health and Human Services Secretary Xavier Becerra should be lauded.

But as large provider groups like the American Hospital Association have pointed out, the federal government must remain vigilant in its enforcement of this rule. As I wrote about recently with the implementation of the No Surprises Act, well-intentioned legislation and implementation rules put in place by regulators can have little real-world impact if insurers are not held accountable. It’s important to note, though, that federal regulatory agencies must be adequately staffed and resourced to be able to police the industry and address insurers’ relentless efforts to find loopholes in federal policy to maximize profits. Congress needs to provide the Department of Health and Human Services with additional funding for enforcement activities, for HHS to require transparency and reporting by insurers on their practices, and for stakeholders, especially providers and patients, to have an avenue to raise concerns with insurers’ practices as they become apparent.

2. Protect seniors from marketing scams

If it’s fall, it’s football season. And that means it’s time for former NFL quarterback Joe Namath’s annual call to action on the airwaves for MA enrollment.

As Congresswoman Jan Schakowsky and I wrote about more than a year ago, these innocent-appearing advertisements are misleading at their best and fraudulent at their worst. Thankfully, this is another area the Biden administration has also been watching over the past year.

CMS now prohibits the use of ads that do not mention a specific plan name or that use the Medicare name and logos in a misleading way, the marketing of benefits in a service area where they are not available, and the use of superlatives (e.g., “best” or “most”) in marketing when not substantiated by data from the current or prior year.

As part of its efforts to enforce the new marketing restrictions, the Center for Medicare and Medicaid Services for the first time evaluated more than 3,000 MA ads before they ran in advance of 2024 open enrollment. It rejected more than 1,000 for being misleading, confusing, or otherwise non-compliant with the new requirements. These types of reviews will, I hope, continue.

CMS has proposed a fixed payment to brokers of MA plans that, if implemented, would significantly improve the problem of steering seniors to the highest-paying plan — with the highest compensation for the insurance broker. I think we can all agree brokers should be required to direct their clients to the best product, not the one that pays the broker the most. (That has been established practice for financial advisors for many years.) CMS should see this rule through, and send MA brokers profiteering off seniors packing.

A bonus regulation in this space to consider: banning MA plan brokers from selling the contact information of MA beneficiaries. Ever wonder why grandma and grandpa get so many spam calls targeting their health conditions? This practice has a lot to do with it. And there’s bipartisan support in Congress for banning sales of beneficiary contact information.

In addition, just as drug companies have to mention the potential side effects of their medications, MA plans should also be required to be forthcoming about their restrictions, including prior authorization requirements, limited networks, and potentially high out-of-pocket costs, in their ads and marketing materials.

3. Be real about supplemental benefits

Tell me if this one sounds familiar. The federal government introduced flexibility to MA plans to offer seniors benefits beyond what they can receive in traditional Medicare funded primarily through taxpayer dollars.

Those “supplemental” benefits were intended to keep seniors active and healthy. Instead, insurers have manipulated the program to offer benefits seniors are less likely to use, so more of the dollars CMS doles out to pay for those benefits stay with payers.

Many seniors in MA plans will see options to enroll in wellness plans, access gym memberships, acquire food vouchers, pick out new sneakers, and even help pay for pet care, believe it or not — all included under their MA plan. Those benefits are paid for by a pot of “rebate” dollars that CMS passes through to plans, with the presumed goal of improving health outcomes through innovative uses.

There is a growing sense, though, that insurers have figured out how to game this system. While some of these offerings seem appealing and are certainly a focus of marketing by insurers, how heavily are they being used? How heavily do insurers communicate to seniors that they have these benefits, once seniors have signed up for them? Are insurers offering things people are actually using? Or are insurers strategically offering benefits that are rarely used?

Those answers are important because MA plans do not have to pay unused rebate dollars back to the federal government.

CMS in 2024 is requiring insurers to submit detailed data for the first time on how seniors are using these benefits. The agency should lean into this effort and ensure plan compliance with the reporting. And as this year rolls on, CMS should be prepared to make the case to Congress that we expect the data to show that plans are pocketing many of these dollars, and they are not significantly improving health outcomes of older Americans.

4. Addressing coding intensity

If you’re a regular reader, you probably know one of my core views on traditional Medicare vs. Medicare Advantage plans. Traditional Medicare has straightforward, transparent payment, while Medicare Advantage presents more avenues for insurers to arbitrarily raise what they charge the government. A good example of this is in higher coding per patient found in MA plans relative to Traditional Medicare.

An older patient goes in to see their doctor. They are diagnosed, and prescribed a course of treatment. Under Traditional Medicare, that service performed by the doctor is coded and reimbursed. The payment is generally the same no matter what conditions or health history that patient brought into the exam room. Straightforward.

MA plans, however, pay more when more codes are added to a diagnosis.

Plans have advertised this to doctors, incentivizing the providers to add every possible code to a submission for reimbursement. So, if that same patient described above has diabetes, but they’re being treated for an unrelated flu diagnosis, the doctor is incentivized by MA to add a code for diabetes treatment. MA plans, in turn, get paid more by the government based on their enrollee’s health status, as determined based on the diagnoses associated with that individual.

Extrapolate that out across tens of millions of seniors with MA plans, and it’s clear MA plans are significantly overcharging the federal government because of over-coding.

One solution I find appealing: similar to fee-for-service, create a new baseline for payments in MA plans to remove the incentive to add more codes to submissions. Proposals I’ve seen would pay providers more than traditional Medicare but without creating the plan-driven incentive for doctors to over-code.

5. Focusing in on Medicare Advantage network cuts in rural areas

Rural America is older and unhealthier than the national average. This should be the area where MA plans should experience the highest utilization.

Instead, we’re seeing that the aggressive practices insurers use to maximize profits force many rural hospitals to cancel their contracts with MA plans. As we wrote about at length in December, MA is becoming a ghost benefit for seniors living in rural communities. The reimbursement rates these plans pay hospitals in rural communities are significantly lower than traditional Medicare. That has further stressed the low margins rural hospitals face.

As Congressional focus on MA grows, I predict more bipartisan recommendations to come forth that address the growing gap between MA plan payments and what hospitals need to be paid in rural areas.

If MA is not accepted by providers in older, rural America, then truly, what purpose does it serve?

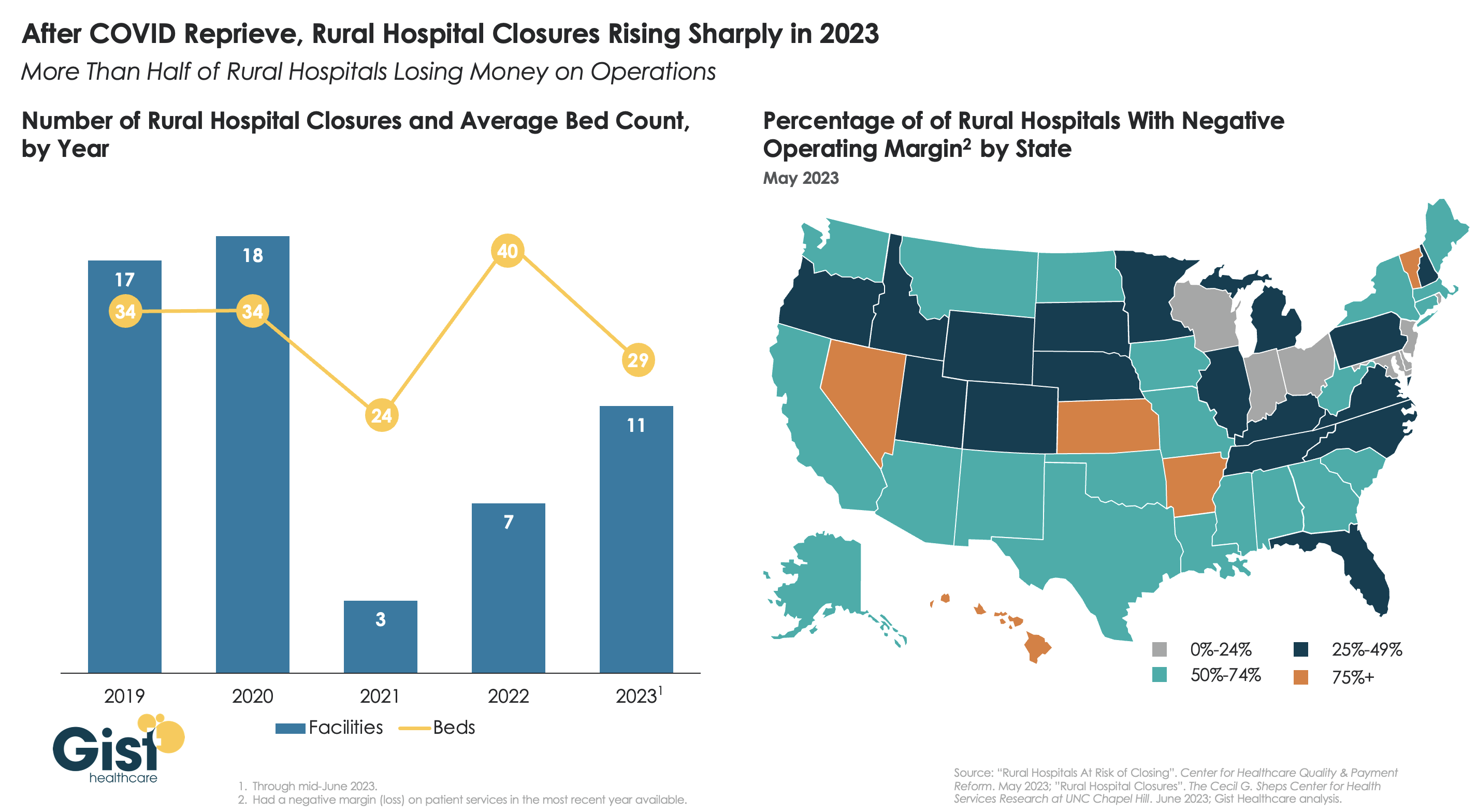

After a brief reprieve thanks to COVID relief funds, rural hospital closures are once again on the rise, with 11 facilities already closing in the first half of this year.

More rural facilities have already closed in 2023 than the previous two years combined, and this year is on pace to be the second-highest number of rural hospital beds lost since 2005.

And the majority of rural hospitals that haven’t closed are experiencing negative operating margins, with almost one in three at immediate or high risk of closure due to declining volumes, shifting payer mix, and increased labor and supply costs.

Leaders at rural hospitals now face difficult decisions including drastically cutting services, merging with a larger system, or closing their doors altogether. The Centers for Medicare and Medicaid Services (CMS) launched the Rural Emergency Hospital Program recently, designed to financially support small rural hospitals that convert to providing emergency services only, but so far program uptake has been limited.

While efforts to prop up hospitals will help to sustain access to care in the near term, rural communities ultimately need a new model for care, with reimagined facilities, supported by enhanced virtual connections to specialists and higher-acuity services.

Last week, California’s legislature passed a bill establishing the Distressed Hospital Loan Program, which will dole out $150M in interest-free emergency loans to struggling nonprofit hospitals in the state which meet specific eligibility criteria, including operating in an underserved area and serving a large share of Medicaid beneficiaries. A combination of state agencies will establish a specific methodology for selection, but hospitals that are part of a health system with more than two separately licensed hospital facilities will be ineligible.

Hospitals receiving loans must provide a plan for how they will use the loans to achieve financial sustainability, and must pay back the money within six years.

The Gist: With twenty percent of the state’s hospitals at risk of shuttering, California lawmakers are hoping to provide the most vulnerable hospitals an alternative to either closure or consolidation, an example other states may follow. But unlike the Paycheck Protection Program loans that shored up businesses through the pandemic’s initial disruption, the outlook for small, struggling, independent hospitals isn’t expected to improve in coming years, even if the economy recovers.

Whether these loans provide lifelines or merely serve as Band-Aids on an untenable situation will depend on whether recipient hospitals can use them to restructure their operating models to absorb increased labor costs amid stagnating volumes and commercial reimbursement.

If these loans aren’t used for transformation, they will only delay the inevitable: more closures, and more mergers to find shelter in scale.

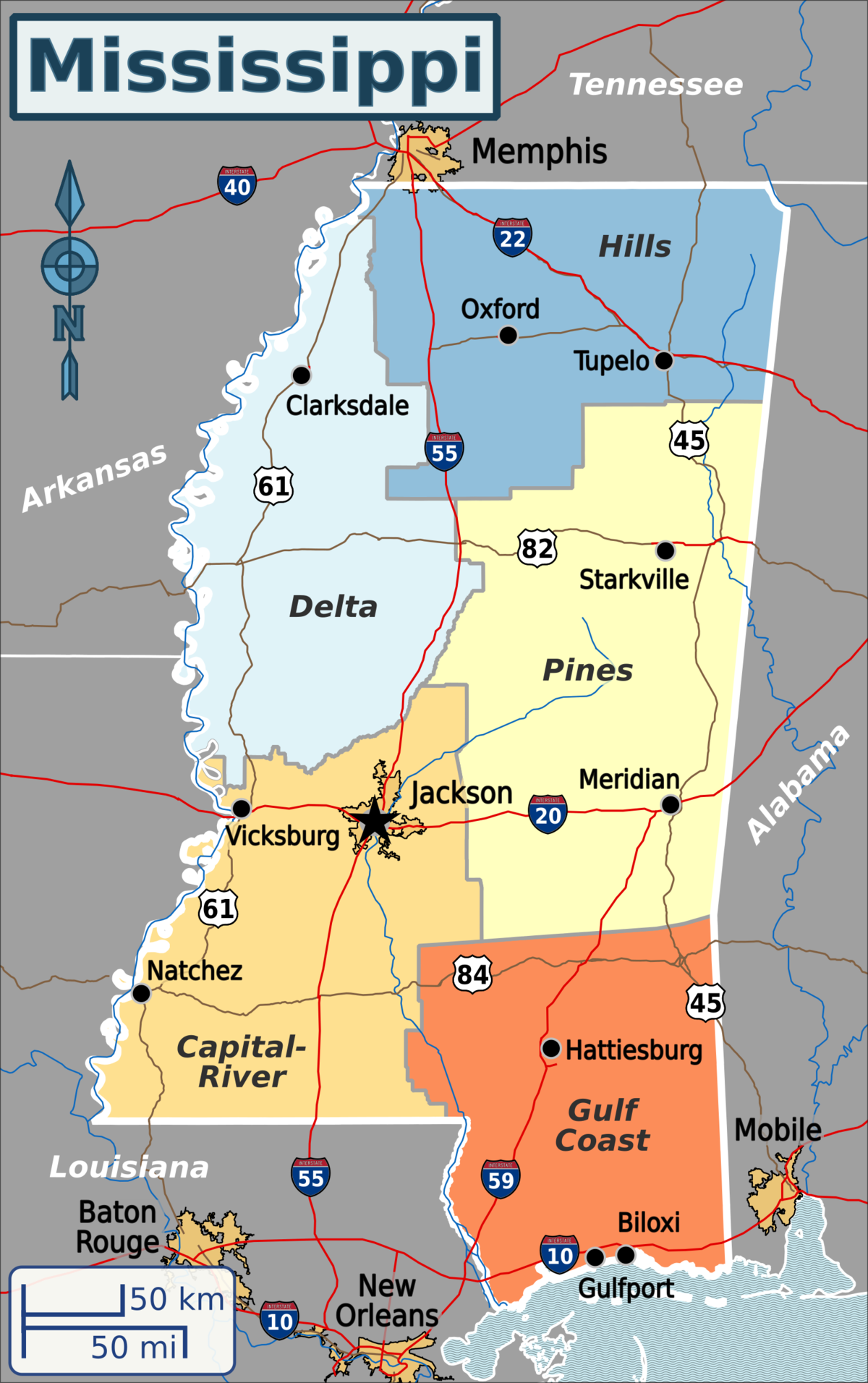

Published this week in the New York Times, this article describes the decaying state of Greenwood Leflore Hospital, a 117 year-old facility in the Mississippi Delta that may be within months of closure. While rural hospitals across the country are struggling, Mississippi’s firm opposition to Medicaid expansion has exacerbated the problem in that state, by depriving providers of an additional $1.4B per year in federal funds. Instead, only a few of the state’s 100-plus hospitals actually turn an annual profit, and uncompensated care costs are almost 10 percent of the average hospital’s operating costs.

Despite a dozen or more hospitals at imminent risk of closure, Mississippi officials would rather use the state’s $3.9B budget surplus to lower or eliminate the state income tax.

The Gist:Expanding Medicaid doesn’t just reduce rates of uncompensated care provided by hospitals, it changes the volume and type of care they provide.

Further, Medicaid expansion has been found to result in significant reductions in all-cause mortality.

Ensuring that low-income residents in Mississippi and other non-expansion states have access to Medicaid would allow providers to administer more preventive care and manage chronic diseases more effectively, before costly exacerbations require hospitalization.