Hospitals and health systems across the country are telling some Medicare and Medicaid patients that they can’t schedule telehealth appointments due to the federal government’s shutdown, now heading into its second week. That’s because Medicare reimbursement for telehealth expired on September 30, leaving health systems with the choice of pausing such visits or keeping them going in hopes of retroactive reimbursement after the shutdown ends.

Reimbursement for the Hospital at Home program, which allows patients to receive care without being admitted to a hospital, also lapsed with the shutdown. That led to providers scrambling to discharge patients under the program or admit them to a hospital. Mayo Clinic, for example, had to move around 30 patients from their homes in Arizona, Florida and Wisconsin to its facilities.

At issue in the government shutdown is healthcare, specifically tax credits for middle- and lower-income Americans that enable them to afford health insurance on the federal exchanges set up by the Affordable Care Act. Democrats want to extend those tax credits, which are set to expire at the end of the year, while Republicans want to reopen the government first and then negotiate about the tax credits in a final budget.

The impasse has prevented the Senate from overcoming a filibuster, despite a Republican majority. Around 24 million Americans get their health insurance through the ACA, and the loss of tax credits will cause their premiums to rise an average of 75%–and as high as 90% in rural areas–and likely cause at least 4 million people to lose coverage entirely.

The government’s closure has reverberated through its operations in healthcare. The Department of Health and Human Services has furloughed some 41% of its staff, making it harder to run oversight operations. CDC’s lack of staff will hinder surveillance of public health threats. And FDA won’t accept any new drug applications until funding is restored.

When the government might reopen remains unclear. Most shutdowns are relatively brief, but the longest one, which lasted 35 days, came during Donald Trump’s first term. Senate majority leader John Thune, R-S.D., and Speaker of the House Mike Johnson, R-La., have both said they won’t negotiate with Democrats, and the House won’t meet again until October 14.Bettors on Polymarket currently expect it to last until at least October 15. Pressure on Congress will increase after that date because there won’t be funds available to pay active military members.

The healthcare industry is still licking its wounds from $1 trillion in federal funding cuts included in the One Big Beautiful Bill Act (OBBBA) signed into law July 4.

Adding insult to injury, the Center for Medicare and Medicaid services issued a 913-page proposed rule last Tuesday that includes unwelcome changes especially troublesome for hospitals i.e. adoption of site neutral payments, expansion of hospital price transparency requirements, reduction of inpatient-only services, acceleration of hospital 340B discount repayment obligations and more.

The combination of the two is bad news for healthcare overall and hospitals especially: the timing is precarious:

Economic uncertainty: Economists believe a recession is less likely but uncertainty about tariffs, fear about rising inflation, labor market volatility a housing market slowdown and speculation about interest rates have capital markets anxious. Healthcare is capital intense: the impact of the two in tandem with economic uncertainty is unsettling.

Consumer spending fragility: Consumer spending is holding steady for the time being but housing equity values are dropping, rents are increasing, student loan obligations suspended during Covid are now re-activated, prices for hospital and physicians are increasing faster than other necessities and inflation ticked up slightly last month. Consumer out-of-pocket spending for healthcare products and services is directly impacted by purchases in every category.

Heightened payer pressures: Insurers and employers are expecting double-digit increases for premiums and health benefits next year blaming their higher costs on hospitals and drugs, OBBBA-induced insurance coverage lapses and systemic lack of cost-accountability. For insurers, already reeling from 2023-2024 financial reversals, forecasts are dire. Payers will heighten pressure on healthcare providers—especially hospitals and specialists—as a result.

Why healthcare appears to have borne the brunt of the funding cuts in the OBBBA is speculative:

Might a case have been made for cuts in other departments? Might healthcare programs other than Medicaid have been ripe for “waste, fraud and abuse” driven cuts? Might technology-driven administrative costs reductions across the expanse of federal and state government been more effective than DOGE- blunt experimentation?

Healthcare is 18% of the GDP and 28% of total federal spending: that leaves room for cuts in other industries.

Why hospitals, along with nursing homes and public health programs, are likely to bear the lion’s share of OBBBA’ cut fallout and CMS’ proposed rule disruptions is equally vexing. Might the high-profile successes of some not-for-profit hospital operators have drawn attention? Might Congress have been attentive to IRS Form 990 filings for NFP operators and quarterly earnings of investor-owned systems and assume hospital finances are OK? Might advocacy efforts to maintain the status quo with facility fees, 340B drug discounts, executive compensation et al been overshadowed by concerns about consolidation-induced cost increases and disregard for affordability? Hospital emergency rooms in rural and urban communities, nursing homes, public health programs and many physicians will be adversely impacted by the OBBBA cuts: the impact will vary by state. What’s not clear is how much.

My take:

Having read both the OBBBA and CMS proposed rules and observed reactions from industry, two things are clear to me:

The antipathy toward the healthcare industry among the public and in Congress played a key role in passage of the OBBBA and regulatory changes likely to follow.

Polls show three-fourths of likely voters want to see transformational change to healthcare and two-thirds think the industry is more concerned with its profit over their care: these views lend to hostile regulatory changes. The public and the majority of elected officials think the industry prioritizes protection of the status quo over obligations to serve communities and the greater good.

The result: winners and losers in each sector, lack of continuity and interoperability, runaway costs and poor outcomes.

No sector in healthcare stands as the surrogate for the health and wellbeing of the population. There are well-intended players in each sector who seek the moral high ground for healthcare, but their boards and leaders put short-term sustainability above long-term systemness and purpose. That void needs to be filled.

The timing of these changes is predictably political.

Most of the lower-cost initiatives in both the OBBBA changes and CMS proposals carry obligations to commence in 2026—in time for the November 2026 mid-term campaigns. Most of the results, including costs and savings, will not be known before 2028 or after. They’re geared toward voters inclined to think healthcare is systemically fraudulent, wasteful and self-serving.

And they’re just the start: officials across the Departments of Health and Human Services, Justice, Commerce, Labor and Veterans Affairs will add to the lists.

This week, the House Energy and Commerce and Ways and Means Committees begins work on the reconciliation bill they hope to complete by Memorial Day. Healthcare cuts are expected to figure prominently in the committee’s work.

And in San Diego, America’s Physician Groups (APG) will host its spring meeting “Kickstarting Accountable Care: Innovations for an Urgent Future” featuring Presidential historian Dorris Kearns Goodwin and new CMS Innovation Center Director Abe Sutton. Its focus will be the immediate future of value-based programs in Trump Healthcare 2.0, especially accountable care organizations (ACOs) and alternative payment models (APMs).

Central to both efforts is the administration’s mandate to reduce federal spending which it deems achievable, in part, by replacing fee for services with value-based payments to providers from the government’s Medicare and Medicaid programs.

The CMS Center for Medicare and Medicaid Innovation (CMMI) is the government’s primary vehicle to test and implement alternative payment programs that reduce federal spending and improve the quality and effectiveness of services simultaneously.

Pledges to replace fee-for-service payments with value-based incentives are not new to Medicare. Twenty-five years ago, they were called “pay for performance” programs and, in 2010, included in the Affordable Care as alternative payment models overseen by CMMI.

But the effectiveness of APMs has been modest at best: of 50+ models attempted, only 6 proved effective in reducing Medicare spending while spending $5.4 billion on the programs. Few were adopted in Medicaid and only a handful by commercial payers and large self-insured employers. Critics argue the APMs were poorly structured, more costly to implement than potential shared savings payments and sometimes more focused on equity and DEI aims than actual savings.

The question is how the Mehmet Oz-Abe Sutten version of CMMI will approach its version of value-based care, given modest APM results historically and the administration’s focus on cost-cutting.

Context is key:

Recent efforts by the Trump Healthcare 2.0 team and its leadership appointments in CMS and CMMI point to a value-agenda will change significantly. Alternative payment models will be fewer and participation by provider groups will be mandated for several. Measures of quality and savings will be fewer, more easily measured and and standardized across more episodes of care. Financial risks and shared savings will be higher and regulatory compliance will be simplified in tandem with restructuring in HHS, CMS and CMMI to improve responsiveness and consistency across federal agencies and programs.

Sutton’s experience as the point for CMMI is significant. Like Adam Boehler, Brad Smith and other top Trump Healthcare 2.0 leaders, he brings prior experience in federal health agencies and operating insight from private equity-backed ventures (Honest Health, Privia, Evergreen Nephrology funded through Nashville-based Rubicon Founders). Sutton’s deals have focused on physician-driven risk-bearing arrangements with Medicare with funding from private investors.

The Trump Healthcare 2.0 team share a view that the healthcare system is unnecessarily expensive and wasteful, overly-regulated and under-performing. They see big hospitals and drug companies as complicit—more concerned about self-protection than consumer engagement and affordability.

They see flawed incentives as a root cause, and believe previous efforts by CMS and CMMI veered inappropriately toward DEI and equity rather than reducing health costs.

And they think physicians organized into risk bearing structures with shared incentives, point of care technologies and dependable data will reduce unnecessary utilization (spending) and improve care for patients (including access and affordability).

There’s will be a more aggressive approach to spending reduction and value-creation with Medicare as the focus: stronger alternative payment models and expansion of Medicare Advantage will book-end their collective efforts as Trump Healthcare 2.0 seeks cost-reduction in Medicare.

What’s ahead?

Trump Healthcare 2.0 value-based care is a take-no prisoners strategy in which private insurers in Medicare Advantage have a seat at their table alongside hospitals that sponsor ACOs and distribute the majority of shared savings to the practicing physicians. But the agenda will be set, and re-set by the administration and link-minded physician organizations like America’s Physician Groups and others that welcome financial risk-sharing with Medicare and beyond.

The results of the Trump Healthcare 2.0 value agenda will be unknown to voters in the November 2026 mid-term but apparent by the Presidential campaign in 2028. In the interim, surrogate measures for performance—like physician participation and projected savings–will be used to show progress and the administration will claim success. It will also spark criticism especially from providers who believe access to needed specialty care will be restricted, public and rural health advocates whose funding is threatened, teaching and clinical research organizations who facing DOGE cuts and regulatory uncertainty, patient’s right advocacy groups fearing lack of attention and private payers lacking scalable experience in Medicare Advantage and risk-based relationships with physicians.

Last week, the American Medical Association named Dr. John Whyte its next President replacing widely-respected 12-year CEO/EVP Jim Madara. When he assumes this office in July, he’ll inherit an association that has historically steered clear of major policy issues but the administration’s value-based care agenda will quickly require his attention.

Physicians including AMA members are restless:

At last fall’s House of Delegates (HOD), members passed a resolution calling for constraints on not-for-profit hospital’ tax exemptions due to misleading community benefits reporting and more consistency in charity care reporting by all hospitals.

The majority of practicing physicians are burned-out due to loss of clinical autonomy and income pressures—especially the 75% who are employees of hospitals and private-equity backed groups. And last week, the American College of Physicians went on record favoring “collective action” to remedy physician grievances. All impact the execution of the administration’s value-based agenda.

Arguably, the most important key to success for the Trump Healthcare 2.0 is its value agenda and physician support—especially the primary care physicians on whom the consumer engagement and appropriate utilization is based. It’s a tall order.

The Trump Healthcare 2.0 value agenda is focused on near-term spending reductions in Medicare. Savings in federal spending for Medicaid will come thru reconciliation efforts in Congress that will likely include work-requirements for enrollees, elimination of subsidies for low-income adults and drug formulary restrictions among others. And, at least for the time being, attention to those with private insurance will be on the back burner, though the administration favors insurance reforms adding flexible options for individuals and small groups.

The Trump Healthcare 2.0 value-agenda is disruptive, aggressive and opportunistic for physician organizations and their partners who embrace performance risk as a permanent replacement for fee for service healthcare. It’s a threat to those that don’t.

Democrat lawmakers are urging Republicans debating cuts to Medicaid to focus instead on fraud, waste and abuse in another federal healthcare program: Medicare Advantage.

Curbing upcoding in the privatized Medicare plans, wherein insurers exaggerate the health needs of their members to inflate government reimbursement, is a better avenue for saving federal dollars than restricting benefits or cutting eligibility in Medicaid, the 36 Democrats wrote in a letter to GOP leadership on Wednesday.

The letter was addressed to Senate Majority Leader John Thune, R-S.D, and House Speaker Mike Johnson, R-La., and comes as Republicans debate different policies to reach savings targets.

Dive Insight:

Republicans in Congress are aiming to extend tax cuts from President Donald Trump’s first term. Their budget directs the House Energy and Commerce Committee to cut $880 billion in spending — a goal that’s impossible to reach without touching Medicaid, which (along with its sister program for children) provides safety-net insurance to some 80 million Americans.

Now, Democrats in both chambers are urging Republicans to redirect their attention from Medicaid to MA, privatized plans for Medicare seniors that can provide additional benefits but also restrict care in a way traditional Medicare is not allowed to do. Still, the plans have steadily grown in popularity and now cover more than half of the 68 million Americans in Medicare.

“Your directive to cut federal health care spending should come from reducing waste, fraud, and abuse like upcoding by for-profit insurance companies, not by cutting health care benefits for American families who rely on Medicaid to make ends meet,” the Democrats’ letter reads.

The letter cites a Wall Street Journal investigation into upcoding published last year that found MA insurers frequently added diagnoses for their members for which their members never received treatment or that went against doctors’ observations. The practice drove a total of $50 billion in additional payments to the private insurers over three years, according to the investigation.

Similarly, influential congressional advisory group MedPAC found CMS paid MA insurers $84 billion more in 2024 than the government would have if those members had been in traditional Medicare. Upcoding was responsible for almost half of those overpayments.

Traditionally, Republicans broadly support MA, which was created on the premise that private insurers could help the government manage Medicare more economically. However, there’s been rising bipartisan support for reforming the program in light of growing evidence of practices like upcoding that inflate government reimbursement to plans without helping enrollees.

In his confirmation hearing, Dr. Mehmet Oz, the surgeon and television personality tapped by Trump as the administrator of the CMS, agreed that tackling fraud, waste and abuse in MA was a “rational” way of lowering federal healthcare spending.

“We’re actually apparently paying more for Medicare Advantage than we’re paying for regular Medicare. So it’s upside down,” Oz said in front of the Senate Finance Committee in March.

Republicans in the House are currently trying to figure out how to achieve desired savings without slashing Medicaid, given the program’s political popularity, including among Republican voters.

GOP leadership recently appeared to rule out two Medicaid policies that would cause significant upheaval for enrollees in the program: lowering the portion of Medicaid costs borne by the federal government for the Medicaid expansion population, and per-capita caps on benefits for beneficiaries in expansion states.

“Moving forward with this dangerous plan to rip health care away from low- and middle-income Americans would be a man-made disaster for the health of the nation and the economy,” the Democrats’ letter reads. “We urge you instead to listen to Administrator Oz and tackle real fraud, waste, and abuse by private, for-profit health insurers in MA.”

House E&C is expected to hold its reconciliation markup next week.

This week, the House Energy and Commerce and Ways and Means Committees begins work on the reconciliation bill they hope to complete by Memorial Day. Healthcare cuts are expected to figure prominently in the committee’s work.

And in San Diego, America’s Physician Groups (APG) will host its spring meeting “Kickstarting Accountable Care: Innovations for an Urgent Future” featuring Presidential historian Dorris Kearns Goodwin and new CMS Innovation Center Director Abe Sutton. Its focus will be the immediate future of value-based programs in Trump Healthcare 2.0, especially accountable care organizations (ACOs) and alternative payment models (APMs).

Central to both efforts is the administration’s mandate to reduce federal spending which it deems achievable, in part, by replacing fee for services with value-based payments to providers from the government’s Medicare and Medicaid programs. The CMS Center for Medicare and Medicaid Innovation (CMMI) is the government’s primary vehicle to test and implement alternative payment programs that reduce federal spending and improve the quality and effectiveness of services simultaneously.

Pledges to replace fee-for-service payments with value-based incentives are not new to Medicare. Twenty-five years ago, they were called “pay for performance” programs and, in 2010, included in the Affordable Care as alternative payment models overseen by CMMI. But the effectiveness of APMs has been modest at best: of 50+ models attempted, only 6 proved effective in reducing Medicare spending while spending $5.4 billion on the programs. Few were adopted in Medicaid and only a handful by commercial payers and large self-insured employers. Critics argue the APMs were poorly structured, more costly to implement than potential shared savings payments and sometimes more focused on equity and DEI aims than actual savings.

The question is how the Mehmet Oz-Abe Sutten version of CMMI will approach its version of value-based care, given modest APM results historically and the administration’s focus on cost-cutting.

Context is key:

Recent efforts by the Trump Healthcare 2.0 team and its leadership appointments in CMS and CMMI point to a value-agenda will change significantly. Alternative payment models will be fewer and participation by provider groups will be mandated for several. Measures of quality and savings will be fewer, more easily measured and and standardized across more episodes of care. Financial risks and shared savings will be higher and regulatory compliance will be simplified in tandem with restructuring in HHS, CMS and CMMI to improve responsiveness and consistency across federal agencies and programs.

Sutton’s experience as the point for CMMI is significant. Like Adam Boehler, Brad Smith and other top Trump Healthcare 2.0 leaders, he brings prior experience in federal health agencies and operating insight from private equity-backed ventures (Honest Health, Privia, Evergreen Nephrology funded through Nashville-based Rubicon Founders). Sutton’s deals have focused on physician-driven risk-bearing arrangements with Medicare with funding from private investors.

The Trump Healthcare 2.0 team share a view that the healthcare system is unnecessarily expensive and wasteful, overly-regulated and under-performing. They see big hospitals and drug companies as complicit—more concerned about self-protection than consumer engagement and affordability. They see flawed incentives as a root cause, and believe previous efforts by CMS and CMMI veered inappropriately toward DEI and equity rather than reducing health costs. And they think physicians organized into risk bearing structures with shared incentives, point of care technologies and dependable data will reduce unnecessary utilization (spending) and improve care for patients (including access and affordability).

There’s will be a more aggressive approach to spending reduction and value-creation with Medicare as the focus: stronger alternative payment models and expansion of Medicare Advantage will book-end their collective efforts as Trump Healthcare 2.0 seeks cost-reduction in Medicare.

What’s ahead?

Trump Healthcare 2.0 value-based care is a take-no prisoners strategy in which private insurers in Medicare Advantage have a seat at their table alongside hospitals that sponsor ACOs and distribute the majority of shared savings to the practicing physicians. But the agenda will be set, and re-set by the administration and link-minded physician organizations like America’s Physician Groups and others that welcome financial risk-sharing with Medicare and beyond.

The results of the Trump Healthcare 2.0 value agenda will be unknown to voters in the November 2026 mid-term but apparent by the Presidential campaign in 2028. In the interim, surrogate measures for performance—like physician participation and projected savings–will be used to show progress and the administration will claim success. It will also spark criticism especially from providers who believe access to needed specialty care will be restricted, public and rural health advocates whose funding is threatened, teaching and clinical research organizations who facing DOGE cuts and regulatory uncertainty, patient’s right advocacy groups fearing lack of attention and private payers lacking scalable experience in Medicare Advantage and risk-based relationships with physicians.

Last week, the American Medical Association named Dr. John Whyte its next President replacing widely-respected 12-year CEO/EVP Jim Madara. When he assumes this office in July, he’ll inherit an association that has historically steered clear of major policy issues but the administration’s value-based care agenda will quickly require his attention.

Physicians including AMA members are restless: at last fall’s House of Delegates (HOD), members passed a resolution calling for constraints on not-for-profit hospital’ tax exemptions due to misleading community benefits reporting and more consistency in charity care reporting by all hospitals. The majority of practicing physicians are burned-out due to loss of clinical autonomy and income pressures—especially the 75% who are employees of hospitals and private-equity backed groups. And last week, the American College of Physicians went on record favoring “collective action” to remedy physician grievances. All impact the execution of the administration’s value-based agenda.

Arguably, the most important key to success for the Trump Healthcare 2.0 is its value agenda and physician support—especially the primary care physicians on whom the consumer engagement and appropriate utilization is based. It’s a tall order.

The Trump Healthcare 2.0 value agenda is focused on near-term spending reductions in Medicare. Savings in federal spending for Medicaid will come thru reconciliation efforts in Congress that will likely include work-requirements for enrollees, elimination of subsidies for low-income adults and drug formulary restrictions among others. And, at least for the time being, attention to those with private insurance will be on the back burner, though the administration favors insurance reforms adding flexible options for individuals and small groups.

The Trump Healthcare 2.0 value-agenda is disruptive, aggressive and opportunistic for physician organizations and their partners who embrace performance risk as a permanent replacement for fee for service healthcare. It’s a threat to those that don’t.

Last week, President-elect Donald Trump announced that Robert F. Kennedy, Jr. would be his nominee for Secretary of Health and Human Services (HHS). He followed this up on Tuesday with his selection of Dr. Mehmet Oz as his nominee for the Centers for Medicare and Medicaid Services (CMS) Administrator. If confirmed, the two men would replace Xavier Becerra and Chiquita Brooks-LaSure, respectively.

Kennedy, who ended his independent presidential campaign and endorsed Trump in August, has become known for his heterodox views on public health, including vaccine skepticism and opposition to water fluoridization.

Dr. Oz, first famous as a TV personality and more recently a Republican candidate for Pennsylvania Senator, is a strong proponent of Medicare Advantage, having co-authored an op-ed advocating for “Medicare Advantage for All” in 2020.

The Gist:

These nominees, especially Kennedy, hold a number of personal beliefs at odds with the public health consensus.

They are both likely to be confirmed, however, as the last cabinet nominee to be rejected by the Senate was John Tower in 1989. (This does not include nominees who have chosen to withdraw themselves from consideration, as former Representative Matt Gaetz has just done.)

Should they be confirmed, they will be responsible for implementing not their own but President Trump’s agenda, the specific priorities of which also remain relatively undefined.

However, possible consensus points between Trump and his nominees include public health cuts and deregulation, greater scrutiny of pharmaceutical companies, and a favoring of Medicare Advantage over traditional Medicare.

On Wednesday, the Centers for Medicare & Medicaid Services (CMS) issued its proposed annual changes to physician payments in its 2025 Medicare Physician Fee Schedule Proposed Rule. Required by statute to maintain budget neutrality, CMS is proposing to reduce the conversion factor—which translates the cost of providing medical services into physician payments—by 2.8%.

This is expected to lower physician payments by 2.93% on average. The proposed rule also includes new telehealth flexibilities, changes allowing eligible accountable care organizations access to a quarterly advance on their earned savings, and new payments for providers that help patients at high risk of overdose or suicide.

The Gist: With CMS proposing to reduce physician payments for the fifth straight year, the American Medical Association and other physician groups are once again calling on Congress to avert these cuts.

Congress has previously responded with “Band-Aid” solutions to temporarily reduce or eliminate reductions for the next calendar year, but physician groups are demanding a more comprehensive fix that ties Medicare payment updates to the Medicare Economic Index, a measure of practice cost inflation.

Medicare physician pay has declined 20% relative to practice costs from 2000 to 2021, and post-COVID inflation has only worsened the issue. Although lawmakers on Capitol Hill have explored various means of doing so, structural changes to Medicare budgetary policy face an uphill legislative battle in a presidential election year.

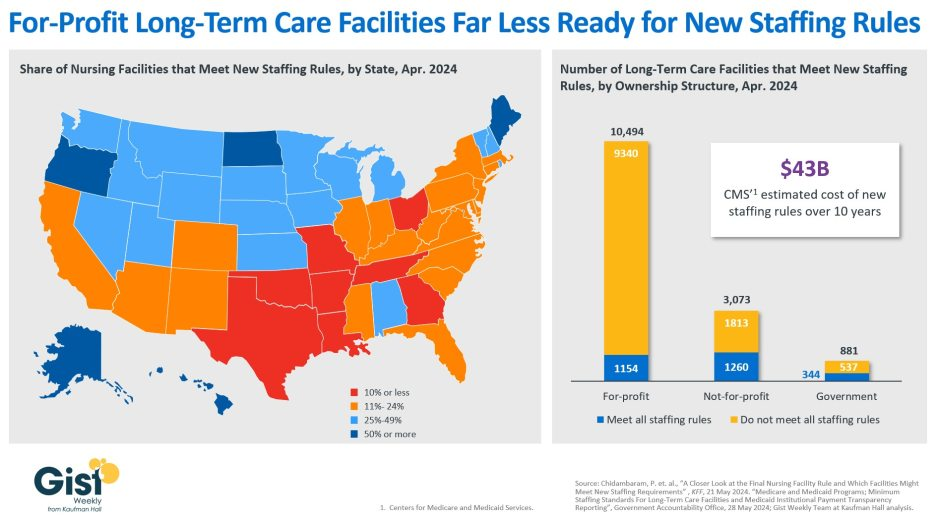

In late April, the Centers for Medicare & Medicaid Services (CMS) establishednew staffing standards for long-term care (LTC) facilities, mandating a minimum of 3.48 hours of nursing care per patient per day, with 33 minutes of that care from a registered nurse, at least one of whom must be always on site. The rule is slated to go into effect in two years for urban nursing homes and three years for rural nursing homes, with some facilities able to apply for hardship exemptions.

Although about one in five LTC facilities nationwide currently meet these staffing standards, staffing levels vary greatly by both state and facility ownership profile. In 28 states, fewer than a quarter of LTC facilities meet the new standards, and in eight states fewer than 10% of facilities are already in compliance.

Facilities in Texas are the least ready, with only 4% meeting the new staffing minimums. In terms of ownership structure, only 11% of for-profit facilities—which constitute nearly three quarters of all LTC facilities nationwide—have staffing levels that meet the new staffing minimums.

The Government Accountability Office projects this new rule will cost LTC facilities $43B over the first ten years, a significant expense at a time when recruiting and retaining nursing talent is already challenging.

Citing the risk of mass closures from facilities unable to comply, nursing home trade groups are suing to stop the mandate from going into effect, and there is also a bill advancing in the House that would repeal the staffing ratios.

That bill is backed by the American Hospital Association, which fears the mandate “would have serious negative, unintended consequences, not only for nursing home patients and facilities, but the entire health continuum.”

Published in Health Affairs last month, this piece explores the history of hospital at home (HaH) programs and examines some of the barriers currently limiting their growth.

HaH programs were introduced in the US back in the 1990s but remained rare due to a lack of reimbursement. That changed in 2020 when the Centers for Medicare and Medicaid Services (CMS) introduced the Acute Hospital Care at Home waiver, which allows fee-for-service Medicare reimbursement for providing inpatient-level care at home, prompting the number of HaH programs nationwide to swell from about 20 to more than 320 today.

Although early findings from this initiative have been positive, the future of many of HaH programs is in doubt, as the waiver is set to expire at the end of 2024, barring congressional action.

The authors argue that making the Medicare waiver program permanent is essential to overcome HaH’s “common agency problem,” which prevents many hospitals from building out their home-based programs to scale if they cannot receive reimbursement for all eligible patients.

The Gist: The Medicare waiver program has incubated many new HaH programs, but most of these programs remain very small; even for systems with the most robust programs, HaH volume only represents a sliver of their total inpatient volume.

Without guaranteed fee-for-service Medicare reimbursement, the average health system will find it difficult to devote the significant resources and investment that program creation and expansion requires.

If Congress moves to make the waiver program permanent, or at least extends it for several more years, state Medicaid programs and private payers may be more incentivized to follow suit and provide reimbursement for the care model.

Although legislation has been introduced to this end in Congress, action on this front in an election year is going to be challenging.

More than 20% of Medicare Advantage patients could be affected by the rule, report finds.

The Centers for Medicare and Medicaid Services’ January expansion of the two-midnight rule to include Medicare Advantage plans has contributed to higher inpatient volumes and revenue growth in the first quarter of the year, according to a Strata Decision Technology report.

This is because inpatient services have higher reimbursement levels compared to outpatient services and the two-midnight rule concerns inpatient care.

CMS published the final rule in April 2023, which for the first time expanded the rule to include Medicare Advantage plans. The rule requires patients to be admitted as an inpatient if the treating clinician determines they require hospital care that extends beyond two midnights, rather than being held under observation status as an outpatient.

The expansion now includes more than 30 million people enrolled in Medicare Advantage managed care plans. Prior to the final rule, the two-midnight rule only explicitly applied to traditional Medicare.

More than 20% of Medicare Advantage patients could be affected by the rule, the report found. An analysis of Medicare Advantage encounters from 2023 – before the rule was expanded to those patients – found that 22.3% were held in observation status for two days or more. By comparison, 8.7% of Medicare patients and 11.3% of patients covered by commercial plans had observation lengths of stay of two days or more in 2023.

WHAT’S THE IMPACT?

Looking at trends in hospital gross revenues, year-over-year growth in inpatient revenue surpassed outpatient revenue in March for the first time in more than two years. Inpatient revenue rose 3.7% versus March 2023, while outpatient revenue was up 2.4% year-over-year. Overall gross operating revenue increased 3.1% and 2.2% over the same periods, respectively.

March marked the 11th consecutive month of year-over-year increases for all three metrics, which contributed to stronger margins in recent months, data showed.

Revenue growth varied widely for hospitals in different regions. For example, hospitals in the Northeast and Mid-Atlantic areas saw inpatient revenue jump 5.4% year-over-year in March, while outpatient revenue was nearly flat, down just 0.1%.

Adjusted revenues increased year-over-year, but were down month-over-month. Net patient service revenue per adjusted discharge increased 2.5% year-over-year, and decreased 1.7% versus the previous month, while NPSR per adjusted patient day rose 4.9% from March 2023 to March 2024, and was down 0.5% from February to March 2024.

Hospital operating margins showed strong performance throughout the first quarter. The median year-to-date operating margin was 4.7% for the month, down slightly from a peak of 5.2% in January, but up significantly compared to margins of less than 1% in early 2023.

While actual operating margin increased overall, the median change in the metric was nearly flat both year-over-year and month-over-month when looking at the national data. The median change in operating margin decreased 0.1 percentage point from March 2023 to March 2024, and was down 0.3 percentage point compared to February 2024. The median change in operating earnings before interest, taxes, depreciation, and amortization (EBITDA) margin decreased 0.4% year-over-year and 0.5% versus the prior month.

THE LARGER TREND

CMS initially implemented the two-midnight Rule for Medicare in 2013 to help remove barriers to patients receiving medically necessary care.

Medicare’s two-midnight rule states that inpatient services are generally payable under Medicare Part A if a physician expects a patient to require medically necessary hospital care that spans at least two midnights.