Tariffs and supply chain uncertainty are playing havoc with hospitals’ purchasing plans, especially for lower-margin products like gloves, gowns and syringes.

Why it matters:

The uncertainty is in some cases delaying spending decisions, including capital improvements, as health system administrators wait to see the effect of increased duties and whether manufacturers win exemptions from the Trump administration.

What they’re saying:

“Hospitals are definitely feeling a pinch,” Mark Hendrickson, director of Premier’s supply chain policy, told Axios. “We’ve never seen tariffs for this long a period of time for this broad a portfolio of products in basically all of our lifetimes.”

“It’s really an uncertain enough environment that we’re cautioning members from panic buying and buying ahead,” he added. “We don’t want to drive artificial shortages of products that could be avoided.”

The big picture:

The health care supply chain is already hard enough to navigate, with certain sterile injectable drugs and other essentials regularly going into shortage.

But President Trump’s existing and threatened tariffs are scrambling the calculus for health systems and the group purchasing organizations they contract with, as they seek a steady supply of what they need and identify possible new sources.

“Everyone in the supply chain, from hospitals to suppliers to manufacturers, is grappling with how to plan thoughtfully and proceed in a way that doesn’t either under- or over-correct for the potential impacts of these tariffs,” Akin Demehin, the American Hospital Association’s vice president of quality and patient safety policy, told Axios.

Between the lines:

So far, there haven’t been clear price hikes or shortages.

But certain types of products are being watched more closely, starting with low-cost, high-volume items often imported from China such as PPE and disposable medical devices.

“Are there going to be instances where those low margin products are just not worth manufacturing anymore?,” Hendrickson said.

U.S. manufacturing of protective gear picked up during the pandemic, to alleviate foreign supply chain disruptions. But some of those sources dried up with the end of mask mandates and other public health measures, when hospitals went back to buying from overseas.

The hospital association is particularly concerned about critical minerals and derivatives used in medical imaging, radioactive drugs and other applications, which could be subject to sectoral levies imposed in the interests of national security.

Last month, the AHA sent a letter to the Trump administration calling for medical exemptions.

The bottom line:

“We haven’t seen the bottom fall out,” Hendrickson said. “I’m hoping we don’t.”

With days before voters decide the composition of the 119th U.S. Congress and the next White House occupant, the immediate future for U.S. healthcare is both predictable and problematic:

It’s predictable that…

1-States will be the epicenter for healthcare legislation and regulation; federal initiatives will be substantially fewer.

At a federal level, new initiatives will be limited: continued attention to hospital and insurer consolidation, drug prices and the role of PBMs, Medicare Advantage business practices and a short-term fix to physician payments are likely but little more. The Affordable Care Act will be modified slightly to address marketplace coverage and subsidies and CMSs Center for Medicare and Medicaid Innovation (CMMI) will test new alternative payment models even as doubt about their value mounts. But “BIG FEDERAL LAWS” impacting the U.S. health system are unlikely.

But in states, activity will explode: for example…

In this cycle, 10 states will decide their abortion policies joining 17 others that have already enacted new policies.

3 will vote on marijuana legalization joining 24 states that have passed laws.

24 states have already passed Prescription Drug Pricing legislation and 4 are considering commissions to set limits.

40 have expanded their Medicaid programs

35 states and Washington, D.C., operate CON programs; in 12 states, CONs have been repealed.

14 have legislation governing mental health access.

5 have passed or are developing commissions to control health costs.

And so on.

Given partisan dysfunction in Congress and the surprising lack of attention to healthcare in Campaign 2024 (other than abortion coverage), the center of attention in 2025-2026 will be states. In addition to the list above, attention in states will address protections for artificial intelligence utilization, access to and pricing for weight loss medications, tax exemptions for not-for-profit health systems, telehealth access, conditions for private equity ownership in health services, constraints on contract pharmacies, implementation of site neutral payments, new 340B accountability requirements and much more. In many of these efforts, state legislatures and/or Governors will go beyond federal guidance setting the stage for court challenges, and the flavor of these efforts will align with a state’s partisan majorities: as of September 30th, 2024, Republicans controlled 54.85% of all state legislative seats nationally, while Democrats held 44.19%. Republicans held a majority in 56 chambers, and Democrats held the majority in 41 chambers. In 2024, 27 states are led by GOP governors and 23 by Dems and 11 face voters November 5. And going into the election, 22 states are considered red, 21 are considered blue and 7 are tagged as purple.

The U.S. Constitution affirms Federalism as the structure for U.S. governance: it pledges the pursuit of “life, liberty and the pursuit of happiness” as its purpose but leaves the lion’s share of responsibilities to states to figure out how. Healthcare may be federalism’s greatest test.

2-Large employers will take direct action to control their health costs.

Per the Kaiser Family Foundation’s most recent employer survey, employer health costs are expected to increase 7% this year for the second year in a row. Willis Towers Watson, predicts a 6.4% increase this year on the heels of a 6% bump last year. The Business Group on Health, which represents large self-insured employers, forecasts an 8% increase in 2025 following a 7% increase last year. All well-above inflation, ages and consumer prices this year.

Employers know they pay 254% of Medicare rates (RAND) and they’re frustrated. They believe their concerns about costs, affordability and spending are not taken seriously by hospitals, physicians, insurers and drug companies. They see lackluster results from federal price transparency mandates and believe the CMS’ value agenda anchored by accountable care organizations are not achieving needed results. Small-and-midsize employers are dropping benefits altogether if they think they can. For large employers, it’s a different story. Keeping health benefits is necessary to attract and keep talent, but costs are increasingly prohibitive against macro-pressures of workforce availability, cybersecurity threats, heightened supply-chain and logistics regulatory scrutiny and shareholder activism.

Maintaining employee health benefits while absorbing hyper-inflationary drug prices, insurance premiums and hospital services is their challenge. The old playbook—cost sharing with employees, narrow networks of providers, onsite/near site primary care clinics et al—is not working to keep up with the industry’s propensity to drive higher prices through consolidation.

In 2025, they will carefully test a new playbook while mindful of inherent risks. They will use reference pricing, narrow specialty specific networks, technology-enabled self-care and employee gainsharing to address health costs head on while adjusting employee wages. Federal and state advocacy about Medicare and Medicaid funding, insurer and hospital consolidation and drug pricing will intensify. And some big names in corporate America will step into a national debate about healthcare affordability and accountability.

Employers are fed up with the status quo. They don’t buy the blame game between hospitals, insurers and drug companies. And they don’t think their voice has been heard.

3-Private equity and strategic investors will capitalize on healthcare market conditions.

The plans set forth by the two major party candidates feature populist themes including protections for women’s health and abortion services, maintenance/expansion of the Affordable Care Act and prescription drug price controls. But the substance of their plans focus on consumer prices and inflation: each promises new spending likely to add to the national deficit:

Per the Non-Partisan Committee for a Responsible Federal Budget, over the next 10 years, the Trump plan would add $7.5 trillion to the deficit; the Harris plan would add $3.5 trillion.

Per the Wharton School at the University of Pennsylvania, Harris’ proposals would add $1.2 trillion to the national deficits over 10 years and Trump’s proposals would add $5.8 trillion over the same period

Per the Congressional Budget Office, federal budget deficit for FY2024 which ended September 30 will be $1.8 trillion– $139 billion more than FT 2023. Revenues increased by an estimated $479 billion (or 11 percent). Revenues in all major categories, but notably individual income taxes, were greater than they were in fiscal year 2023. Outlays rose by an estimated $617 billion (or 10 percent). The largest increase in outlays was for education ($308 billion). Net outlays for interest on the public debt rose by $240 billion to total $950 billion.

The federal government spent $6.75 trillion in 2024, a 10% increase from the prior year. Spending on Social Security (22% of total spending) and healthcare programs (28.5% of total spending) also increased substantially. The U.S. debt as of Friday was $37.77 trillion, or $106 thousand per citizen.

The non-partisan Congressional Budget Office (CBO) reports that federal debt held by the public averaged 48.3 % of GDP for the half century ending in 2023– far above its historic average. It projects next year’s national debt will hit 100% for the first time since the US military build-up in the second world war. And it forecast the debt reaching 122.4% in 2034 potentially pushing interest payments from 13% of total spending this year to 20% or more.

Adding debt is increasingly cumbersome for national lawmakers despite campaign promises, and healthcare is rivaled by education, climate and national defense in seeking funding through taxes and appropriations. Thus, opportunities for private investors in healthcare will increase dramatically in 2025 and 2026. After all, it’s a growth industry ripe for fresh solutions that improve affordability and cost reduction at scale.

Combined, these three predictions foretell a U.S. healthcare system that faces a significant pressure to demonstrate value.

They require every healthcare organization to assess long-term strategies in the likely context of reduced funding, increased regulation and heightened attention to prices and affordability. This is problematic for insiders accustomed to incrementalism that’s protected them from unwelcome changes for 3 decades.

Announcements last week by Walgreens and CVS about changes to their strategies going forward reflect the industry’s new normal: change is constant, success is not. In 2025, regardless of the election outcome, healthcare will be a major focus for lawmakers, regulators, employers and consumers.

This year, 316 million Americans (92.3% of the population) have health insurance: 61 million are covered by Medicare, 79 million by Medicaid/CHIP and 164 million through employment-based coverage. By 2032, the Congressional Budget Office predicts Medicare coverage will increase 18%, Medicaid and CHIP by 0% and employer-based coverage will increase 3.0% to 169 million. For some in the industry, that justifies seating Medicare on the front row for attention. And, for many, it justifies leaving employers on the back bench since the working age population use hospitals, physicians and prescription meds less than seniors.

Last week, the Business Group on Health released its 2025 forecast for employer health costs based on responses from 125 primarily large employers surveyed in June: Highlights:

“Since 2022, the projected increase in health care trend, before plan design changes, rose from 6% in 2022, 7.2% in 2024 to almost 8% for 2025. Even after plan design changes, actual health care costs continued to grow at a rate exceeding pre-pandemic increases. These increases point toward a more than 50% increase in health care cost since 2017. Moreover, this health care inflation is expected to persist and, in light of the already high burden of medical costs on the plan and employees, employers are preparing to absorb much of the increase as they have done in recent years.”.

Per BGH, the estimated total cost of care per employee in 2024 is $18,639, up $1,438 from 2023. The estimated out-of-pocket cost for employees in 2024 is $1,825 (9.8%), compared to $1,831 (10.6%) in 2023.

The prior week, global benefits firm Aon released its 2025 assessment based on data from 950 employers:

“The average cost of employer-sponsored health care coverage in the U.S. is expected to increase 9.0% surpassing $16,000 per employee in 2025–higher than the 6.4% increase to health care budgets that employers experienced from 2023 to 2024 after cost savings strategies. “

On average, the total health-plan cost for employers increased 5.8% to $14,823 per employee from 2023 to 2024: employer costs increased 6.4% to 80.7% of total while employee premiums increased 3.4% increase–both higher than averages from the prior five years, when employer budgets grew an average of 4.4% per year and employees averaged 1.2% per year.

Employee contributions in 2024 were $4,858 for health care coverage, of which $2,867 is paid in the form of premiums from pay checks and $1,991 is paid through plan design features such as deductibles, co-pays and co-insurance.

The rate of health care cost increases varies by industry: technology and communications industry have the highest average employer cost increase at 7.4%, while the public sector has the highest average employee cost increase at 6.7%. The health care industry has the lowest average change in employee contributions, with no material change from 2023: +5.8%

And in July, PWC’s Health Research Institute released its forecast based on interviews with 20 health plan actuaries. Highlights:

“PwC’s Health Research Institute (HRI) is projecting an 8% year-on-year medical cost trend in 2025 for the Group market and 7.5% for the Individual market. This near-record trend is driven by inflationary pressure, prescription drug spending and behavioral health utilization. The same inflationary pressure the healthcare industry has felt since 2022 is expected to persist into 2025, as providers look for margin growth and work to recoup rising operating expenses through health plan contracts. The costs of GLP-1 drugs are on a rising trajectory that impacts overall medical costs. Innovation in prescription drugs for chronic conditions and increasing use of behavioral health services are reaching a tipping point that will likely drive further cost inflation.”

Despite different methodologies, all three analyses conclude that employer health costs next year will increase 8-9%– well-above the Congressional Budget Office’ 2025 projected inflation rate (2.2%), GDP growth (2.4% and wage growth (2.0%). And it’s the largest one-year increase since 2017 coming at a delicate time for employers worried already about interest rates, workforce availability and the political landscape.

For employers, the playbook has been relatively straightforward: control health costs through benefits designs that drive smarter purchases and eliminate unnecessary services. Narrow networks, price transparency, on-site/near-site primary care, restrictive formularies, value-based design, risk-sharing contracts with insurers and more have become staples for employers.

But this playbook is not working for employers: the intrinsic economics of supply-driven demand and its regulated protections mitigate otherwise effective ways to lower their costs while improving care for their employees and families.

My take:

Last week, I reviewed the healthcare advocacy platforms for the leading trade groups that represent employers in DC and statehouses to see what they’re saying about their take on the healthcare industry and how they’re leaning on employee health benefits. My review included the U.S. Chamber of Commerce, National Federal of Independent Businesses, Business Roundtable, National Alliance of Purchaser Coalitions, Purchaser Business Group on Health, American Benefits Council, Self-Insurance Institute of America and the National Association of Manufacturers.

What I found was amazing unanimity around 6 themes:

Providing health benefits to employees is important to employers. Protecting their tax exemptions, opposing government mandates, and advocating against disruptive regulations that constrain employer-employee relationships are key.

Healthcare affordability is an issue to employers and to their employees, All see increasing insurance premiums, benefits design changes, surprise bills, opaque pricing, and employee out-of-pocket cost obligations as problems.

All believe their members unwillingly subsidize the system paying 1.6-2.5 times more than what Medicare pays for the same services. They think the majority of profits made by drug companies, hospitals, physicians, device makers and insurers are the direct result of their overpayments and price gauging.

All think the system is wasteful, inefficient and self-serving. Profits in healthcare are protected by regulatory protections that disable competition and consumer choices.

All think fee-for-service incentives should be replaced by value-based purchasing.

And all are worried about the obesity epidemic (123 million Americans) and its costs-especially the high-priced drugs used in its treatment. It’s the near and present danger on every employer’s list of concerns.

This consensus among employers and their advocates is a force to be reckoned. It is not the same voice as health insurers: their complicity in the system’s issues of affordability and accountability is recognized by employers. Nor is it a voice of revolution: transformational changes employers seek are fixes to a private system involving incentives, price transparency, competition, consumerism and more.

Employers have been seated on healthcare’s back bench since the birth of the Medicare and Medicaid programs in 1965. Congress argues about Medicare and Medicaid funding and its use. Hospitals complain about Medicare underpayments while marking up what’s charged employers to make up the difference. Drug companies use a complicated scheme of patents, approvals and distribution schemes to price their products at will presuming employers will go along. Employers watched but from the back row.

As a new administration is seated in the White House next year regardless of the winner, what’s certain is healthcare will get more attention, and alongside the role played by employers. Inequities based on income, age and location in the current employer-sponsored system will be exposed. The epidemic of obesity and un-attended demand for mental health will be addressed early on. Concepts of competition, consumer choice, value and price transparency will be re-defined and refreshed. And employers will be on the front row to make sure they are.

For employers, it’s crunch time: managing through the pandemic presented unusual challenges but the biggest is ahead. Of the 18 benefits accounted as part of total compensation, employee health insurance coverage is one of the 3 most expensive (along with paid leave and Social Security) and is the fastest growing cost for employers. Little wonder, employers are moving from the back bench to the front row.

Health systems have a big challenge: rising costs and reimbursement that doesn’t keep up with inflation. The amount spent on healthcare annually continues to rise while outcomes aren’t meaningfully better.

Some people outside of the industry wonder: Why doesn’t healthcare just act more like other businesses?

“There seems to be a widely held belief that healthcare providers respond the same as all other businesses that face rising costs,” said Cliff Megerian, MD, CEO of University Hospitals in Cleveland. “That is absolutely not true. Unlike other businesses, hospitals and health systems cannot simply adjust prices in response to inflation due to pre-negotiated rates and government mandated pay structures. Instead, we are continually innovating approaches to population health, efficiency and cost management, ensuring that we maintain delivery of high quality care to our patients.”

Nonprofit hospitals are also responsible for serving all patients regardless of ability to pay, and University Hospitals is among the health systems distinguished as a best regional hospital for equitable access to care by U.S. News & World Report.

“This commitment necessitates additional efforts to ensure equitable access to healthcare services, which inherently also changes our payer mix by design,” said Dr. Megerian. “Serving an under-resourced patient base, including a significant number of Medicaid, underinsured and uninsured individuals, requires us to balance financial constraints with our ethical obligations to provide the highest quality care to everyone.”

Hospitals need adequate reimbursement to continue providing services while also staffing the hospital appropriately. Many hospitals and health systems have been in tense negotiations with insurers in the last 24 months for increased pay rates to cover rising costs.

“Without appropriate adjustments, nonprofit healthcare providers may struggle to maintain the high standards of care that patients deserve, especially when serving vulnerable populations,” said Dr. Megerian. “Ensuring fair reimbursement rates supports our nonprofit industry’s aim to deliver equitable, high quality healthcare to all while preserving the integrity of our health systems.”

Industry outsiders often seek free market dynamics in healthcare as the “fix” for an expensive and complicated system. But leaving healthcare up to the normal ebbs and flows of businesses would exclude a large portion of the population from services. Competition may lead to service cuts and hospital closures as well, which devastates communities.

“A misconception is that the marketplace and utilization of competitive business model will fix all that ails the American healthcare system,”

said Scot Nygaard, MD, COO of Lee Health in Ft. Myers and Cape Coral, Fla.

“Is healthcare really a marketplace, in which the forces of competition will solve for many of the complex problems we face, such as healthcare disparities, cost effective care, more uniform and predictive quality and safety outcomes, mental health access, professional caregiver workforce supply?”

Without comprehensive reform at the state or federal level, many health systems have been left to make small changes hoping to yield different results. But, Dr. Nygaard said, the “evidence year after year suggests that this approach is not successful and yet we fear major reform despite the outcomes.”

The dearth of outside companies trying to enter the healthcare space hasn’t helped. People now expect healthcare providers to function like Amazon or Walmart without understanding the unique complexities of the industry.

“Unlike retail, healthcare involves navigating intricate regulations, providing deeply personal patient interactions and building sustained trust,” said Andreia de Lima, MD, chief medical officer of Cayuga Health System in Ithaca, N.Y. “Even giants like Walmart found it challenging to make primary care profitable due to high operating costs and complex reimbursement systems. Success in healthcare requires more than efficiency; it demands a deep understanding of patient care, ethical standards and the unpredictable nature of human health.”

So what can be done?

Tracea Saraliev, a board member for Dominican Hospital Santa Cruz (Calif.) and PIH Health said leaders need to increase efforts to simplify and improve healthcare economics.

“Despite increased ownership of healthcare by consumers, the economics of healthcare remain largely misunderstood,” said Ms. Saraliev. “For example, consumers erroneously believe that they always pay less for care with health insurance. However, a patient can pay more for healthcare with insurance than without as a result of the negotiated arrangements hospitals have with insurance companies and the deductibles of their policy.”

There is also a variation in cost based on the provider, and even with financial transparency it’s a challenge to provide an accurate assessment for the cost of care before services. Global pricing and other value-based care methods streamline the price, but healthcare providers need great data to benefit from the arrangements.

Based on payer mix, geographic location and contracted reimbursement rates, some health systems are able to thrive while others struggle to stay afloat. The variation mystifies some people outside of the industry.

“Healthcare economics very much remains paradoxical to even the most savvy of consumers,” said Ms. Saraliev.

Walmart’s announcement on April 30 that it was pulling the plug on Walmart Health stunned the healthcare ecosystem. [1] Few saw it coming.

Launched amid much fanfare in 2019, Walmart Health has operated 51 health centers in five states, with a robust virtual care platform. Walmart’s news release noted that “the challenging reimbursement environment and escalating operating costs create a lack of profitability that make the care business unsustainable for us at this time.” Despite its legendary supply-chain capabilities, expansive market presence and sizable consumer demand for affordable primary care services, Walmart couldn’t make its business model work in healthcare.

Just two weeks earlier with much less fanfare, and in stark contrast to Walmart, the big health insurer Elevance announced it was doubling-down on primary care. On April 15, Elevance issued a news release detailing a new strategic partnership with the private-equity firm Clayton, Dubilier & Rice (CD&R) to “accelerate innovation in primary care delivery, enhance the healthcare experience and improve health outcomes.” [2]

What gives? Why is Elevance expanding its primary care footprint when the retail behemoth Walmart believes investing in primary care is unprofitable? The answer lies at the heart of the debate over the future of U.S. healthcare. As a nation, the United States overinvests in healthcare delivery while underinvesting in preventive care and health promotion.

Enlightened healthcare companies, like Elevance, are attacking this imbalance aggressively.

Elevance isn’t alone. Other large health insurers — including UnitedHealthcare, CVS/Aetna and Humana — and some large health systems (e.g., AdventHealth, Corewell Health and Intermountain Healthcare) are investing in primary care services to support what I refer to as 3D-WPH, shorthand for “democratized and decentralized distribution of whole-person health.”

3D-WPH is the disruptive innovation that is rewiring U.S. healthcare to improve outcomes, lower costs, personalize care delivery and promote community wellbeing. It is an unstoppable force.

Transactional Versus Integrated Primary Care

Across multiple retail product and service categories — including groceries, clothing, electronics, financial services, generic drugs and vision care — Walmart applies ruthless efficiency management to increase consumer selection and lower prices. Consistent with the company’s mission of helping its customers to “save money and live better,”

Walmart Health provided routine, standalone primary care services at low, transparent prices. Despite scale and superior logistics, Walmart could not deliver these routine care services profitably.

Here’s the problem with applying Walmart’s retailing expertise to healthcare:

While exceptional primary care services are rarely profitable in their own right, they can reduce total care costs by limiting the need for subsequent acute care services. Preventive care works. Companies that invest in primary care can benefit by reducing total cost of care.

Unfortunately, few providers and payers practice this integrated approach to care delivery. Most providers rely on their primary care networks to refer patients for profitable specialty care services. Most payers use their primary care networks to deny access to these same specialty care services.

This competition between using primary care networks as referral and denial machines dramatically increases the intermediary costs of U.S. healthcare delivery. Patients get lost as these titanic payer-provider battles unfold, even as costs continue to rise, and health status continues to decline.

Whole-Person Health Works

A growing number of payers and providers, however, are recalibrating their business models to lower total care costs by integrating primary care services into a whole-person health delivery model.

In its news release, Elevance described its strategic partnership with CD&R as follows:

The strategic partnership’s advanced primary care models take a whole-health approach to address the physical, social and behavioral health of every person. The foundation of the new advanced primary care offering will be stronger patient-provider relationships supported by data-driven insights, care coordination and referral management, and integrated health coaching. It will also leverage realigned incentives through value-based care agreements that enable care providers, assist individuals in leading healthier lives, and make care more affordable.

“We know that when primary care providers are resourced and empowered, they guide consumers through some of life’s most vulnerable moments, while helping people to take control of their own health,” said Bryony Winn, president of health solutions at Elevance Health, in the news release. “By bringing a new model of advanced primary care to markets across the country, our partnership with CD&R will create a win-win for consumers and care providers alike.”

Whole health personalizes and integrates care delivery. I would suggest that transactional and fragmented primary care service provision cannot compete with 3D-WPH.

For all its strengths, Walmart Health is not positioned to advance whole-person health. Primary care service provision without connection to whole-person health is a recipe for financial disaster. Walmart Health’s demise confirms this market reality.

Countries with nationalized health systems practice whole-person health expansively. With one-third the per capita income and one-fifth the per capita healthcare expenditure, Portugal has a life expectancy that is more than five years longer than it is in the United States. [5] Portugal achieves better population health metrics than the United States by operating community health networks throughout the country that combine primary care and public health services.

The VA, Portugal and numerous other organizations and countries prove the thesis that investing in primary care lowers total care costs and improves health outcomes. The evidence supporting this thesis is both compelling and incontrovertible.

Solving Healthcare’s Primary Care Conundrum

Economists refer to a circumstance when individuals overuse scarce public goods as a tragedy of the commons.

Public grazing fields highlight the challenge posed by such a circumstance. [6] It is in the financial interest of individual ranchers to overgraze their herd on a public grazing field. Overgrazing by all, however, would obliterate the grazing field, which is against the public’s interest.

Societies address these “tragedies” by establishing and enforcing rules to govern public goods.

U.S. healthcare, however, reverses this type of economic tragedy. Advanced primary care services represent a public good. All acknowledge the benefits and societal returns, yet few providers and payers invest in advanced primary care services. Providers don’t invest because it leads to lower treatment volumes. Payers don’t invest because primary care’s higher costs trigger higher premiums, prompting their members to switch plans.

We can’t solve the primary care conundrum until we enable both providers and payers to benefit from investments in advanced primary care services. Fragmented, transactional medicine, even when delivered efficiently, is not cost-effective. Walmart Health discovered this economic reality the hard way and exited the business.

By contrast, Elevance is reorganizing itself to overcome healthcare’s reverse tragedy of the commons. They are betting that offering advanced primary care services within integrated delivery networks will both lower costs and improve health outcomes. Healthcare’s future belongs to the companies, like Elevance, that are striving to solve the industry’s primary care conundrum.

Last week, 2 important economic reports were released that provide a retrospective and prospective assessment of the U.S. health economy:

The CBO National Health Expenditure Forecast to 2032:

“Health care spending growth is expected to outpace that of the gross domestic product (GDP) during the coming decade, resulting in a health share of GDP that reaches 19.7% by 2032 (up from 17.3% in 2022). National health expenditures are projected to have grown 7.5% in 2023, when the COVID-19 public health emergency ended. This reflects broad increases in the use of health care, which is associated with an estimated 93.1% of the population being insured that year… During 2027–32, personal health care price inflation and growth in the use of health care services and goods contribute to projected health spending that grows at a faster rate than the rest of the economy.”

The Congressional Budget Office forecast that from 2024 to 2032:

National Health Expenditures will increase 52.6%: $5.048 trillion (17.6% of GDP) to $7,705 trillion (19.7% of GDP) based on average annual growth of: +5.2% in 2024 increasing to +5.6% in 2032

NHE/Capita will increase 45.6%: from $15,054 in 2024 to $21,927 in 2032

Physician services spending will increase 51.2%: from $1006.5 trillion (19.9% of NHE) to $1522.1 trillion (19.7% of total NHE)

Hospital spending will increase 51.6%: from $1559.6 trillion (30.9% of total NHE) in 2024 to $2366.3 trillion (30.7% of total NHE) in 2032.

Prescription drug spending will increase 57.1%: from 463.6 billion (9.2% of total NHE) to 728.5 billion (9.4% of total NHE)

The net cost of insurance will increase 62.9%: from 328.2 billion (6.5% of total NHE) to 534.7 billion (6.9% of total NHE).

The U.S. Population will increase 4.9%: from 334.9 million in 2024 to 351.4 million in 2032.

The Bureau of Labor Statistics CPI Report for May 2024 and Last 12 Months (May 2023-May2024):

“The Consumer Price Index for All Urban Consumers (CPI-U) was unchanged in May on a seasonally adjusted basis, after rising 0.3% in April… Over the last 12 months, the all-items index increased 3.3% before seasonal adjustment. More than offsetting a decline in gasoline, the index for shelter rose in May, up 0.4% for the fourth consecutive month. The index for food increased 0.1% in May. … The index for all items less food and energy rose 0.2% in May, after rising 0.3 % the preceding month… The all-items index rose 3.3% for the 12 months ending May, a smaller increase than the 3.4% increase for the 12 months ending April. The all items less food and energy index rose 3.4 % over the last 12 months. The energy index increased 3.7%for the 12 months ending May. The food index increased 2.1%over the last year.

Medical care services, which represents 6.5% of the overall CPI, increased 3.1%–lower than the overall CPI. Key elements included in this category reflect wide variance: hospital and OTC prices exceeded the overall CPI while insurance, prescription drugs and physician services were lower.

Physicians’ services CPI (1.8% of total impact): LTM: +1.4%

Hospital services CPI (1.0% of total impact): LTM: +7.3%

Prescription drugs (.9% of total impact) LTM +2.4%

Over the Counter Products (.4% of total impact) LTM 5.9%

Health insurance (.6% of total) LTM -7.7%

Other categories of greater impact on the overall CPI than medical services are Shelter (36.1%), Commodities (18.6%), Food (13.4%), Energy (7.0%) and Transportation (6.5%).

Three key takeaways from these reports:

The health economy is big and getting bigger. But it’s less obvious to consumers in the prices they experience than to employers, state and federal government who fund the majority of its spending. Notably, OTC products are an exception: they’re a direct OOP expense for most consumers. To consumers, especially renters and young adults hoping to purchase homes, the escalating costs of housing have considerably more impact than health prices today but directly impact on their ability to afford coverage and services. Per Redfin, mortgage rates will hover at 6-7% through next year and rents will increase 10% or more.

Proportionate to National Health Expenditure growth, spending for hospitals and physician services will remain at current levels while spending for prescription drugs and health insurance will increase. That’s certain to increase attention to price controls and heighten tension between insurers and providers.

There’s scant evidence the value agenda aka value-based purchases, alternative payment models et al has lowered spending nor considered significant in forecasts.

The health economy is expanding above the overall rates of population growth, overall inflation and the U.S. economy. GDP. Its long-term sustainability is in question unless monetary policies enable other industries to grow proportionately and/or taxpayers agree to pay more for its services. These data confirm its unit costs and prices are problematic.

As Campaign 2024 heats up with the economy as its key issue, promises to contain health spending, impose price controls, limit consolidation and increase competition will be prominent.

Public sector actions

will likely feature state initiatives to lower cost and spend taxpayer money more effectively.

Private sector actions

will center on employer and insurer initiatives to increase out of pocket payments for enrollees and reduce their choices of providers.

Thus, these reports paint a cautionary picture for the health economy going forward. Each sector will feel cost-containment pressure and each will claim it is responding appropriately. Some actually will.

PS: The issue of tax exemptions for not-for-profit hospitals reared itself again last week.

The Committee for a Responsible Federal Budget—a conservative leaning think tank—issued a report arguing the exemption needs to be ended or cut. In response,

the American Hospital Association issued a testy reply claiming the report’s math misleading and motivation ill-conceived.

This issue is not going away: it requires objective analysis, fresh thinking and new voices. For a recap, see the Hospital Section below.

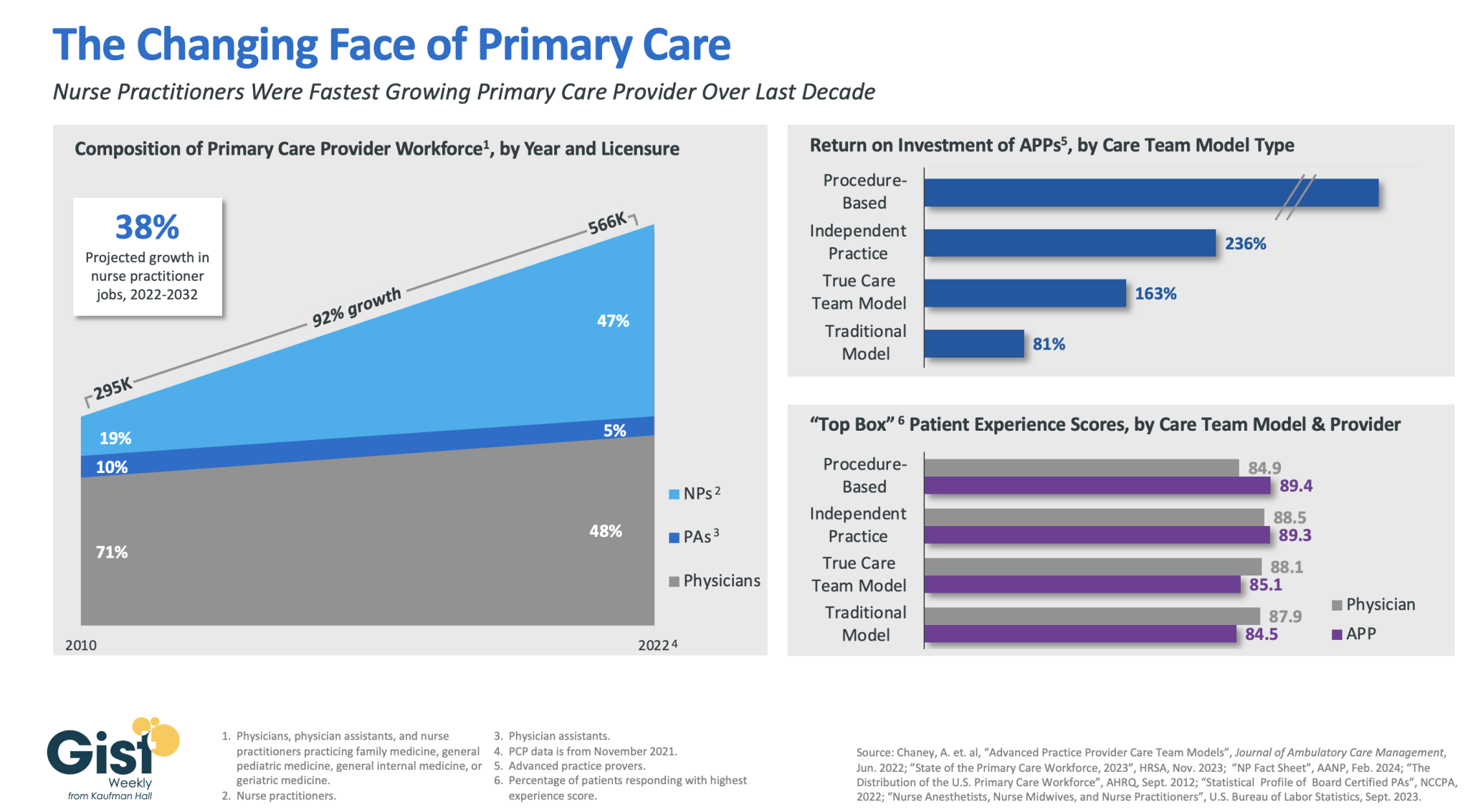

In this week’s graphic, we highlight how the primary care provider workforce has evolved over the past decade in both the pursuit of team-based care models and value-based care, as well as in response to rising labor costs and physician shortages.

In 2010, physicians made up more than 70 percent of the primary care workforce. But over the next 12 years, the number of primary care providers nearly doubled, largely driven by immense growth of nurse practitioners in the workforce.

As of 2022, more than half of primary care providers were advanced practice providers (APPs), who continue to have a strong job outlook across the next decade (especially nurse practitioners).This shift has been beneficial to many provider organizations.

In a study from the Mayo Clinic, the return on investment was positive across a variety of APP practice models, especially in procedural-based specialties but across both independent practice models and full care team models as well.

APPs also receive similar patient experience scores as their physician counterparts.

Continued integration of APPs in team-based care models remains a key strategy for health systems seeking to improve access while lowering costs, especially in primary care.

Tuesday, the, FTC, and DOJ announced creation of a task force focused on tackling “unfair and illegal pricing” in healthcare. The same day, HHS joined FTC and DOJ regulators in launching an investigation with the DOJ and FTC probing private equity’ investments in healthcare expressing concern these deals may generate profits for corporate investors at the expense of patients’ health, workers’ safety and affordable care.

Thursday’s State of the Union address by President Biden (SOTU) and the Republican response by Alabama Senator Katey Britt put the spotlight on women’s reproductive health, drug prices and healthcare affordability.

Friday, the Senate passed a $468 billion spending bill (75-22) that had passed in the House Wednesday (339-85) averting a government shutdown. The bill postpones an $8 billion reduction in Medicaid disproportionate share hospital payments for a year, allocates $4.27 billion to federally qualified health centers through the end of the year and rolls back a significant portion of a Medicare physician pay cut that kicked in on Jan. 1. Next, Congress must pass appropriations for HHS and other agencies before the March 22 shutdown.

And all week, the cyberattack on Optum’s Change Healthcare discovered February 21 hovered as hospitals, clinics, pharmacies and others scrambled to manage gaps in transaction processing. Notably, the American Hospital Association and others have amplified criticism of UnitedHealth Group’s handling of the disruption, having, bought Change for $13 billion in October, 2022 after a lengthy Department of Justice anti-trust review. This week, UHG indicates partial service of CH support will be restored. Stay tuned.

Just another week for healthcare: Congressional infighting about healthcare spending. Regulator announcements of new rules to stimulate competition and protect consumers in the healthcare market. Lobbying by leading trade groups to protect funding and disable threats from rivals. And so on.

At the macro level, it’s understandable: healthcare is an attractive market, especially in its services sectors. Since the pandemic, prices for services (i.e. physicians, hospitals et al) have steadily increased and remain elevated despite the pressures of transparency mandates and insurer pushback. By contrast, prices for most products (drugs, disposables, technologies et al) have followed the broader market pricing trends where prices for some escalated fast and then dipped.

While some branded prescription medicines are exceptions, it is health services that have driven the majority of health cost inflation since the pandemic.

UnitedHealth Group’s financial success is illustrative:

it’s big, high profile and vertically integrated across all major services sectors. In its year end 2023 financial report (January 12, 2024) it reported revenues of $371.6 Billion (up 15% Year-Over-Year), earnings from operations up 14%, cash flows from operations of $29.1 Billion (1.3x Net Income), medical care ratio at 83.2% up from 82% last year, net earnings of $23.86/share and adjusted net earnings of $25.12/share and guidance its 2024 revenues of $400-403 billion. They buy products using their scale and scope leverage to pay less for services they don’t own less and products needed to support them. It’s a big business in a buyer’s market and that’s unsettling to many.

Big business is not new to healthcare:

it’s been dominant in every sector but of late more a focus of unflattering regulator and media attention. Coupled with growing public discontent about the system’s effectiveness and affordability, it seems it’s near a tipping point.

David Johnson, one of the most thoughtful analysts of the health industry, reminded his readers last week that the current state of affairs in U.S. healthcare is not new citing the January 1970 Fortune cover story “Our Ailing Medical System”

“American medicine, the pride of the nation for many years, stands now on the brink of chaos. To be sure, our medical practitioners have their great moments of drama and triumph. But much of U.S. medical care, particularly the everyday business of preventing and treating routine illnesses, is inferior in quality, wastefully dispensed, and inequitably financed…

Whether poor or not, most Americans are badly served by the obsolete, overstrained medical system that has grown up around them helter-skelter. … The time has come for radical change.”

Johnson added: “The healthcare industry, however, cannot fight gravity forever. Consumerism, technological advances and pro-market regulatory reforms are so powerful and coming so fast that status-quo healthcare cannot forestall their ascendance. Properly harnessed, these disruptive forces have the collective power necessary for U.S. healthcare to finally achieve the 1970 Fortune magazine goal of delivering “good care to every American with little increase in cost.”

He’s right.

I believe the U.S. health system as we know it has reached its tipping point. The big-name organizations in every sector see it and have nominal contingency plans in place; the smaller players are buying time until the shoe drops. But I am worried.

I am worried the system’s future is in the hands of hyper-partisanship by both parties seeking political advantage in election cycles over meaningful creation of a health system that functions for the greater good.

I am worried that the industry’s aversion toprice transparency, meaningful discussion about affordability and consistency in defining quality, safety and value will precipitate short-term gamesmanship for reputational advantage and nullify systemness and interoperability requisite to its transformation.

I am worried that understandably frustrated employers will drop employee health benefits to force the system to needed accountability.

I am worried that the growing armies of under-served and dissatisfied populations will revolt.

I am worried that its workforce is ill-prepared for a future that’s technology-enabled and consumer centric.

I am worried that the industry’s most prominent trade groups are concentrating more on “warfare” against their rivals and less about the long-term future of the system.

I am worried that transformational change is all talk.

It’s time to start an adult conversation about the future of the system. The starting point: acknowledging that it’s not about bad people; it’s about systemic flaws in its design and functioning. Fixing it requires balancing lag indicators about its use, costs and demand with assumptions about innovations that hold promise to shift its trajectory long-term. It requires employers to actively participate: in 2009-2010, Big Business mistakenly chose to sit out deliberations about the Affordable Care Act. And it requires independent, visionary facilitation free from bias and input beyond the DC talking heads that have dominated reform thought leadership for 6 decades.

Or, collectively, we can watch events like last week’s roll by and witness the emergence of a large public utility serving most and a smaller private option for those that afford it. Or something worse.

P.S. Today, thousands will make the pilgrimage to Orlando for HIMSS24 kicking off with a keynote by Robert Garrett, CEO of Hackensack Meridian Health tomorrow about ‘transformational change’ and closing Friday with a keynote by Nick Saban, legendary Alabama football coach on leadership. In between, the meeting’s 24 premier supporters and hundreds of exhibitors will push their latest solutions to prospects and customers keenly aware healthcare’s future is not a repeat of its past primarily due to technology. Information-driven healthcare is dependent on technologies that enable cost-effective, customized evidence-based care that’s readily accessible to individuals where and when they want it and with whom.

And many will be anticipating HCA Mission Health’s (Asheville NC) Plan of Action response due to CMS this Wednesday addressing deficiencies in 6 areas including CMS Deficiency 482.12 “which ensures that hospitals have a responsible governing body overseeing critical aspects of patient care and medical staff appointments.” Interest is high outside the region as the nation’s largest investor-owned system was put in “immediate jeopardy” of losing its Medicare participation status last year at Mission. FYI: HCA reported operating income of $7.7 billion (11.8% operating margin) on revenues of $65 billion in 2023.

Companies grappling with liquidity concerns are looking to cut costs and streamline operations, according to a new survey.

Dive Brief:

Over three-quarters of healthcare chief financial officers expect to see profitability increases in 2024, according to a recent survey from advisory firm BDO USA. However, to become profitable, many organizations say they will have to reduce investments in underperforming service lines, or pursue mergers and acquisitions.

More than 40% of respondents said theywill decrease investments in primary care and behavioral health services in 2024, citing disruptions from retail players. They will shift funds to home care, ambulatory services and telehealth that provide higher returns, according to the report.

Nearly three-quarters of healthcare CFOs plan to pursue some type of M&A deal in the year ahead, despite possible regulatory threats.

Dive Insight:

Though inflationary pressures have eased since the height of the COVID-19 pandemic, healthcare CFOs remain cognizant of managing costs amid liquidity concerns, according to the report.

The firmpolled 100 healthcare CFOs serving hospitals, medical groups, outpatient services, academic centers and home health providers with revenues from $250 million to $3 billion or more in October 2023.

Just over a third of organizations surveyed carried more than 60 days of cash on hand. In comparison, a recent analysis from KFF found that financially strong health systems carried at least 150 days of cash on hand in 2022.

Liquidity is a concern for CFOs given high rates of bond and loan covenant violations over the past year. More than half of organizations violated such agreements in 2023, while 41% are concerned they will in 2024, according to the report.

To remain solvent, 44% of CFOs expect to have more strategic conversations about their economic resiliency in 2024, exploring external partnerships, options for service line adjustments and investments in workforce and technology optimization.

Most organizations are interested in exploring sales, according to the report. Financially struggling organizations are among the most likely to consider deals. Nearly one in three organizations that violated their bond or loan covenants in 2023 are planning a carve-out or divestiture this year. Organizations with less than 30 days of cash on hand are also likely to consider carve-outs.

Organizations will also turn to automation to cut costs. Ninety-eight percent of organizations surveyed had pilotedgenerative AI tools in a bid to alleviate resource and cost constraints, according to the consultancy.

“Healthcare leaders believe AI will be essential to helping clinicians operate at the top of their licenses, focusing their time on patient care and interaction over administrative or repetitive tasks,” authors wrote. Nearly one in three CFOs plan to leverage automation and AI in the next 12 months.

However, CFOs are keeping an eye on the risks. As more data flows through their organizations, they are increasingly concerned about cybersecurity. More than half of executives surveyed said data breaches are a bigger risk in 2024 compared to 2023.

Earlier this month, leaders from more than 400 organizations descended on San Francisco for J.P. Morgan‘s 42nd annual healthcare conference to discuss some of the biggest issues in healthcare today. Here’s how Advisory Board experts are thinking about Modern Healthcare’s 10 biggest takeaways — and our top resources for each insight.

How we’re thinking about the top 10 takeaways from JPM’s annual healthcare conference

Following the conference, Modern Healthcare provided a breakdown of the top-of-mind issues attendees discussed.

Here’s how our experts are thinking about the top 10 takeaways from the conference — and the resources they recommend for each insight.

1. Ambulatory care provides a growth opportunity for some health systems

By Elizabeth Orr, Vidal Seegobin, and Paul Trigonoplos

At the conference, many health system leaders said they are evaluating growth opportunities for outpatient services.

However, results from our Strategic Planner’s Survey suggest only the biggest systems are investing in building new ambulatory facilities. That data, alongside the high cost of borrowing and the trifurcation of credit that Fitch is predicting, suggests that only a select group of health systems are currently poised to leverage ambulatory care as a growth opportunity.

Systems with limited capital will be well served by considering other ways to reach patients outside the hospital through virtual care, a better digital front door, and partnerships. The efficiency of outpatient operations and how they connect through the care continuum will affect the ROI on ambulatory investments. Buying or building ambulatory facilities does not guarantee dramatic revenue growth, and gaining ambulatory market share does not always yield improved margins.

While physician groups, together with management service organizations, are very good at optimizing care environments to generate margins (and thereby profit), most health systems use ambulatory surgery center development as a defensive market share tactic to keep patients within their system.

This approach leaves margins on the table and doesn’t solve the growth problem in the long term. Each of these ambulatory investments would do well to be evaluated on both their individual profitability and share of wallet.

On January 24 and 25, Advisory Board will convene experts from across the healthcare ecosystem to inventory the predominant growth strategies pursued by major players, explore considerations for specialty care and ambulatory network development, understand volume and site-of-care shifts, and more. Register here to join us for the Redefining Growth Virtual Summit.

Also, check out our resources to help you plan for shifts in patient utilization:

2. Rebounding patient volumes further strain capacity

By Jordan Peterson, Eliza Dailey, and Allyson Paiewonsky

Many health system leaders noted that both inpatient and outpatient volumes have surpassed pre-pandemic levels, placing further strain on workforces.

The rebound in patient volumes, coupled with an overstretched workforce, underscores the need to invest in technology to extend clinician reach, while at the same time doubling down on operational efficiency to help with things like patient access and scheduling.

For leaders looking to leverage technology and boost operational efficiency, we have a number of resources that can help:

3. Health systems aren’t specific on AI strategies

By Paul Trigonoplos and John League

According to Modern Healthcare, nearly all health systems discussed artificial intelligence (AI) at the conference, but few offered detailed implementation plans and expectations.

Over the past year, a big part of the work for Advisory Board’s digital health and health systems research teams has been to help members reframe the fear of missing out (FOMO) that many care delivery organizations have about AI.

We think AI can and will solve problems in healthcare. Every organization should at least be observing AI innovations. But we don’t believe that “the lack of detail on healthcare AI applications may signal that health systems aren’t ready to embrace the relatively untested and unregulated technology,” as Modern Healthcare reported.

The real challenge for many care delivery organizations is dealing with the pace of change — not readiness to embrace or accept it. They aren’t used to having to react to anything as fast-moving as AI’s recent evolution. If their focus for now is on low-hanging fruit, that’s completely understandable. It’s also much more important for these organizations to spend time now linking AI to their strategic goals and building out their governance structures than it is to be first in line with new applications.

Check out our top resources for health systems working to implement AI:

Digital health companies like Teladoc, R1 RCM, Veradigm, and Talkspace all spoke out about their use of generative AI.

This does not surprise us at all. In fact, we would be more surprised if digital health companies were not touting their AI capabilities. Generative AI’s flexibility and ease of use make it an accessible addition to nearly any technology solution.

However, that alone does not necessarily make the solution more valuable or useful. In fact, many organizations would do well to consider how they want to apply new AI solutions and compare those solutions to the ones that they would have used in October 2022 — before ChatGPT’s newest incarnation was unveiled. It may be that other forms of AI, predictive analytics, or robotic process automation are as effective at a better cost.

Again, we believe that AI can and will solve problems in healthcare. We just don’t think it will solve every problem in healthcare, or that every solution benefits from its inclusion.

During the conference, providers criticized insurers for the rate of denials, Modern Healthcare reports.

Denials — along with other utilization management techniques like prior authorization — continue to build tension between payers and providers, with payers emphasizing their importance for ensuring cost effective, appropriate care and providers overwhelmed by both the administrative burden and the impact of denials on their finances.

Many health plans have announced major moves to reduce prior authorizations and CMS recently announced plans to move forward with regulations to streamline the prior authorization process. However, these efforts haven’t significantly impacted providers yet.

In fact, most providers report no decrease in denials or overall administrative burden. A new report found that claims denials increased by 11.99% in the first three quarters of 2023, following similar double digit increases in 2021 and 2022.

Our team is actively researching the root cause of this discrepancy and reasons for the noted increase in denials. Stay tuned for more on improving denials performance — and the broader payer-provider relationship — in upcoming 2024 Advisory Board research.

For now, check out this case study to see how Baptist Health achieved a 0.65% denial write-off rate.

6. Insurers are prioritizing Star Ratings and risk adjustment changes

By Mallory Kirby

Various insurers and providers spoke about “the fallout from star ratings and risk adjustment changes.”

2023 presented organizations focused on MA with significant headwinds. While many insurers prioritized MA growth in recent years, leaders have increased their emphasis on quality and operational excellence to ensure financial sustainability.

With an eye on these headwinds, it makes sense that insurers are upping their game to manage Star Ratings and risk adjustment. While MA growth felt like the priority in years past, this focus on operational excellence to ensure financial sustainability has become a priority.

We’ve already seen litigation from health plans contesting the regulatory changes that impact the bottom line for many MA plans. But with more changes on the horizon — including the introduction of the Health Equity Index as a reward factor for Stars and phasing in of the new Risk Adjustment Data Validation model — plans must prioritize long-term sustainability.

Check out our latest MA research for strategies on MA coding accuracy and Star Ratings:

Pharmacy benefit manager (PBM) leaders discussed the ways they are preparing for potential congressional action, including “updating their pricing models and diversifying their revenue streams.”

Healthcare leaders should be prepared for Congress to move forward with PBM regulation in 2024. A final bill will likely include federal reporting requirements, spread pricing bans, and preferred pricing restrictions for PBMs with their own specialty pharmacy. In the short term, these regulations will likely apply to Medicare and Medicaid population benefits only, and not the commercial market.

Congress isn’t the only entity calling for change. Several states passed bills in the last year targeting PBM transparency and pricing structures. The Federal Trade Commission‘s ongoing investigation into select PBMs looks at some of the same practices Congress aims to regulate. PBM commercial clients are also applying pressure. In 2023, Blue Cross Blue Shield of California‘s (BSC) decided to outsource tasks historically performed by their PBM partner. A statement from BSC indicated the change was in part due to a desire for less complexity and more transparency.

Here’s what this means for PBMs:

Transparency is a must

The level of scrutiny on transparency will force the hand of PBMs. They will have to comply with federal and state policy change and likely give something to their commercial partners to stay competitive. We’re already seeing this unfold across some of the largest PBMs. Recently, CVS Caremarkand Express Scripts launched transparent reimbursement and pricing models for participating in-network pharmacies and plan sponsors.

While transparency requirements will be a headache for larger PBMs, they might be a real threat to smaller companies. Some small PBMs highlight transparency as their main value add. As the larger PBMs focus more on transparency, smaller PBMs who rely on transparent offerings to differentiate themselves in a crowded market may lose their main competitive edge.

PBMs will have to try new strategies to boost revenue

PBM practice of guiding prescriptions to their own specialty pharmacy or those providing more competitive pricing is a key strategy for revenue. Stricter regulations on spread pricing and patient steerage will prompt PBMs to look for additional revenue levers.

PBMs are already getting started — with Express Scripts reporting they will cut reimbursement for wholesale brand name drugs by about 10% in 2024. Other PBMs are trying to diversify their business opportunities. For example, CVS Caremark’s has offered a new TrueCost model to their clients for an additional fee. The model determines drug prices based on the net cost of drugs and clearly defined fee structures. We’re also watching growing interest in cross-benefitutilization management programs for specialty drugs. These offerings look across both medical and pharmacy benefits to ensure that the most cost-effective drug is prescribed for patients.

At the conference, retailers such as CVS, Walgreens, and Amazon doubled down on their healthcare services strategies.

Typically, disruptors do not get into care delivery because they think it will be easy. Disruptors get into care delivery because they look at what is currently available and it looks so hard — hard to access, hard to understand, and hard to pay for.

Many established players still view so-called disruptors as problematic, but we believe that most tech companies that move into healthcare are doing what they usually do — they look at incumbent approaches that make it hard for customers and stakeholders to access, understand, and pay for care, and see opportunities to use technology and innovative business models in an attempt to target these pain points.

CVS, Walgreens, and Amazon are pursuing strategies that are intended to make it more convenient for specific populations to get care. If those efforts aren’t clearly profitable, that does not mean that they will fail or that they won’t pressure legacy players to make changes to their own strategies. Other organizations don’t have to copy these disruptors (which is good because most can’t), but they must acknowledge why patient-consumers are attracted to these offerings.

For more information on how disruptors are impacting healthcare, check out these resources:

9. Financial pressures remain for many health systems

By Vidal Seegobin and Marisa Nives

Health systems are recovering from the worst financial year in recent history. While most large health systems presenting at the conference saw their finances improve in 2023, labor challenges and reimbursement pressures remain.

We would be remiss to say that hospitals aren’t working hard to improve their finances. In fact, operating margins in November 2023 broke 2%. But margins below 3% remain a challenge for long-term financial sustainability.

One of the more concerning trends is that margin growth is not tracking with a large rebound in volumes. There are number of culprits: elevated cost structures, increased patient complexity, and a reimbursement structure shifting towards government payers.

For many systems, this means they need to return to mastering the basics: Managing costs, workforce retention, and improving quality of care. While these efforts will help bridge the margin gap, the decoupling of volumes and margins means that growth for health systems can’t center on simply getting bigger to expand volumes.

Maximizing efficiency, improving access, and bending the cost curve will be the main pillars for growth and sustainability in 2024.

To learn more about what health system strategists are prioritizing in 2024, read our recent survey findings.

Also, check out our resources on external partnerships and cost-saving strategies:

During the conference, MA insurers reported seeing a spike in utilization driven by increased doctor’s visits and elective surgeries.

These increased medical expenses are putting more pressure on MA insurers’ margins, which are already facing headwinds due to CMS changes in MA risk-adjustment and Star Ratings calculations.

However, this increased utilization isn’t all bad news for insurers. Part of the increased utilization among seniors can be attributed to more preventive care, such as an uptick in RSV vaccinations.

In UnitedHealth Group‘s* Q4 earnings call, CFO John Rex noted that, “Interest in getting the shot, especially among the senior population, got some people into the doctor’s office when they hadn’t visited in a while,” which led to primary care physicians addressing other care needs. As seniors are referred to specialty care to address these needs, plans need to have strategies in place to better manage their specialist spend.