Hospitals and health systems across the country are telling some Medicare and Medicaid patients that they can’t schedule telehealth appointments due to the federal government’s shutdown, now heading into its second week. That’s because Medicare reimbursement for telehealth expired on September 30, leaving health systems with the choice of pausing such visits or keeping them going in hopes of retroactive reimbursement after the shutdown ends.

Reimbursement for the Hospital at Home program, which allows patients to receive care without being admitted to a hospital, also lapsed with the shutdown. That led to providers scrambling to discharge patients under the program or admit them to a hospital. Mayo Clinic, for example, had to move around 30 patients from their homes in Arizona, Florida and Wisconsin to its facilities.

At issue in the government shutdown is healthcare, specifically tax credits for middle- and lower-income Americans that enable them to afford health insurance on the federal exchanges set up by the Affordable Care Act. Democrats want to extend those tax credits, which are set to expire at the end of the year, while Republicans want to reopen the government first and then negotiate about the tax credits in a final budget.

The impasse has prevented the Senate from overcoming a filibuster, despite a Republican majority. Around 24 million Americans get their health insurance through the ACA, and the loss of tax credits will cause their premiums to rise an average of 75%–and as high as 90% in rural areas–and likely cause at least 4 million people to lose coverage entirely.

The government’s closure has reverberated through its operations in healthcare. The Department of Health and Human Services has furloughed some 41% of its staff, making it harder to run oversight operations. CDC’s lack of staff will hinder surveillance of public health threats. And FDA won’t accept any new drug applications until funding is restored.

When the government might reopen remains unclear. Most shutdowns are relatively brief, but the longest one, which lasted 35 days, came during Donald Trump’s first term. Senate majority leader John Thune, R-S.D., and Speaker of the House Mike Johnson, R-La., have both said they won’t negotiate with Democrats, and the House won’t meet again until October 14.Bettors on Polymarket currently expect it to last until at least October 15. Pressure on Congress will increase after that date because there won’t be funds available to pay active military members.

Since the murder of UnitedHealth executive Brian Thompson in New York City December 4, 2024, attention to health insurers has heightened. National media coverage has been brutal. Polls have chronicled the public’s disdain for rising premiums and increased denials. Hospitals and physicians have amped-up campaigns against prior authorization and inadequate reimbursement. For many health insurers, no news is a good news day. Here’s ChatGPT’s reply to how insurers are depicted:

“Media coverage of US health insurers focuses heavily on the challenges consumers face due to high costs, coverage denials, and complicated policies, often portraying insurers as profit-driven entities that hinder care access. Investigations reveal insurers using technology to deny claims and push for denials during prior authorization, while other reports highlight market concentration and the increasing influence of large companies like UnitedHealth Group and Centene. Media also covers the marketing efforts of insurers, particularly for Medicare Advantage plans, and public frustration with the industry. “

In some ways, it’s understandable. Insurance, by definition, is a bet, especially in healthcare. Private policyholders—individuals and employers– bet the premiums they pay pooled with others will cover the cost of a condition or accident that requires medical care. In the 1960’s, federal and state government made the same bet on behalf of seniors (Medicare) and lower-income or disabled kids and adults (Medicaid). But they’re bets.

But the rub is this: what healthcare products and services costs and their prices are hard to predict and closely-guarded secrets in an industry that declares itself the world’s best. Claims data—one source of tracking utilization—is nearly impossible to access even for employers who cover the majority of U.S. population (56%).

Spending for U.S. healthcare is forecast to increase 54% through 2033 from $5.6 trillion to $8.6 trillion— the result of higher costs for prescription drugs and hospital stays, medical inflation, technology, increased utilization (demand) and administrative costs (overhead). Insurers negotiate rates for these, add their margin and pass them thru to their customers—individuals, employers and government agencies. It’s all done behind the scenes.

The public’s working knowledge of how the health system operates, how it performs and what key players in the ecosystem do is negligible. For most, personal experience with the system is their context. We understand our personal healthiness if so inclined or fortunate to have a continuous primary care relationship. We understand our medications if they solve a problem or don’t. We understand our hospitals if we or a family member use them or occasionally visit, and we understand our insurance when we enroll choosing from affordable options that include the doctors and hospitals we like and when we’re denied services or billed for what insurance doesn’t cover.

Today, corporate names like UnitedHealth Group, Humana, Cigna, Elevance, CVS Aetna and Centene are the health insurance industry’s big brands, corralling more than 60% of the industry’s private and government enrollment with the rest divided among 1,149 smaller players. Today, the public’s perception of health insurers is negative: most consider insurance a necessary evil with data showing it’s no guarantee against financial ruin. Today, it’s an expensive employee benefit for employers who are looking for alternative options for workforce stability. And only 56% of enrollees trust their health insurer to do what’s best for them.

Ours is a flawed system that’s not sustainable: insurers are part of that problem. It’s premised on dependence:patients depend on providers to define their diagnosis and deliver the treatments/therapeutics and enrollees depend on insurers to handle the logistics of how much they get paid and when. At the point of service, patients pay co-pays and after the fact, get an “explanation of benefits” along with additional out of pocket obligations. Hospitals and physicians fight insurers about what’s reasonable and customary compensation, and patients unable to out-of-pocket obligations are handed off to “revenue cycle specialists” for collection. Wow. Great system! Mark it up, pass it thru and let the chips fall where they may—all under the presumed oversight of state insurance commissioners who are tasked to protect the public’s interests.

Do insurers deserve the animosity they’re facing from employers, hospitals, physicians and their enrollees? Yes, but certainly some more than others. Facts are facts:

Since 2020, health insurance premium costs have increased 2-4 times faster than household necessities and wages for the average household. Affordability is an issue.

Denials have increased.

Enrollee trust and satisfaction with insurers has plummeted.

And industry profits since 2023 have taken a hit due to post-pandemic pent-up demand, pricey drugs including in-demand GLP-1’s for obesity and increased negotiation leverage by consolidated health systems.

Most Americans think not having health insurance is a bigger risk than going without. But most also think healthcare is fundamental right and the government should guarantee access through universal coverage.

Having private insurance is not the issue: having insurance that ensures access to doctors and hospitals when needed reliably and affordably is their unmet need.

In the weeks ahead, employers will update their employee health benefits options for next year while facing 9-15% higher costs for their coverage. States will decide how they’ll implement work requirements in their Medicaid programs and assess the extent of lost coverage for millions. Insurers who sponsor market place plans suspended by the Big Beautiful Bill will raise their individual premiums hikes 20-70% for the 16 million who are losing their subsidies.

Medicare Advantage (Medicare Part C) insurers will skinny-down the supplements in their offerings and raise premiums alongside Part D increases, And, every insurer will inventory markets served and product portfolio profitability to determine investment opportunities or exit strategies. That’s the calculus every insurer applies every year, adjusting as conditions dictate.

Most private insurers pay little attention to the 8% of Americans who have no coverage; those inclined tend to be smaller community-based plans often associated with hospitals or provider organizations.

Most are concerned about continuity of care for their enrollees: they know 12% had a lapse in their coverage last year, 23% are under-insured and 43% missed a scheduled appointment or treatment due to out-of-pocket costs involved.

And all are concerned about the long-term financial viability of the entire health insurance sector: margins have plummeted since 2020 from 3.1% to 0.8%%, medical loss ratio’s have increased from 98.2% in 2023 to 100.1% last year, premiums increase grew 5.9% while hospital and medical expenses grew $8.9% and so on. The bigger players have residual capital to diversify and grow; others don’t.

Criticism of the health insurance industry is justified for the most part but the rest of the story is key. The U.S. system is broken and everyone knows it. But health insurers are not alone in bearing responsibility for its failure though their role is significant.

The urgent need is for a roadmap to a system of health where the healthiness and well-being of the entire population is true north to its ambition. It’s a system that’s comprehensive, connected, cost-effective and affordable. Protecting turf between sectors, blame and shame rhetoric and perpetuation of public ignorance are non-starters.

PS: Two important events last week weigh heavily on U.S. healthcare’s future:

In Verona, WI, the Epic User Group Meeting showcased the company’s plans for AI featuring 3 new generative AI tools — Emmie for patients, Art for clinicians and Penny for revenue cycle management. Per KLAS, the private company grew its market share to 42% of acute care hospitals and 55% of acute care beds at the end of 2024.

In Jackson Hole, WY, the Federal Reserve Bank of Kansas City’s annual economic symposium where Fed Chair Jay Powell signaled a likely interest rate cut in its September 16-17 meeting and changes to how the central bank will assess employment status going forward.

Healthcare is labor intense, capital intense and 26% of federal spending in the FY 2026 proposed budget. The Fed through its monetary policies has the power and obligation to foster economic stability. Epic is one of a handful of companies that has the potential to transform the U.S. health system. Transformation of the health system is essential to its sustainability and necessary to the U.S. economic stability since healthcare is 18% of the country’s GDP and its biggest private employer.

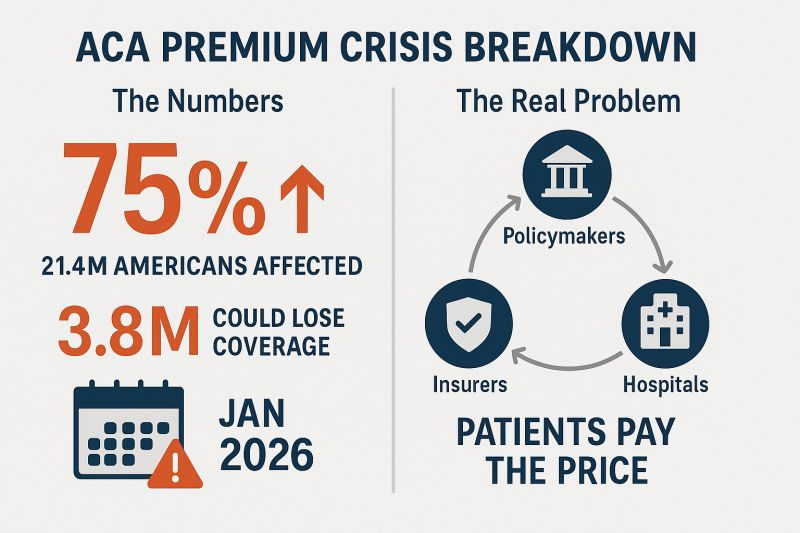

When Congress passed pandemic-era enhancements to Affordable Care Act (ACA) premium subsidies in 2021, it wasn’t just a policy tweak — it was a lifeline. But unless lawmakers act, those subsidies will vanish on January 1, 2026.

According to KFF, the average ACA enrollee could see premiums spike 75% overnight. For many, that will mean a choice between things like their health coverage and rent or food. The Congressional Budget Office estimates more than 4.2 million people could lose coverage over the next decade as a result. Below is where the expired subsidies will hurt the hardest:

1. Young adults… and their parents’ wallets

Young people who’ve aged out of their parents’ plans and buy coverage through the ACA marketplaces will see some of the steepest jumps.

If they decide to forgo coverage, as KFF Health News warns: The so-called “‘insurance cliff’ at age 26 can send young adults tumbling into being uninsured.”

The ACA is the only real option for many small-business owners, freelancers and gig workers. These are the folks that conservatives say we should encourage to build and grow their own businesses who make up the backbone of Main Street. Losing the enhanced subsidies means many will face premiums hundreds of dollars higher per month. Some will be forced to close shop and turn to jobs at out-of-town corporations flush enough to afford to offer subsidized coverage to their workers, a direct hit to local economies.

3. States already in crisis

States aren’t in a position to plug the gap.Politico reports that California, Colorado, Maryland, Washington, and others are scrambling to soften the blow, but even the most ambitious state-level plans can’t replace hundreds of millions in lost federal funding.

And this comes right after Medicaid cuts in the One Big Beautiful Bill Act that will hit hospitals, clinics and low-income communities. In Washington state alone, officials expect premiums to jump 75% when the subsidies expire, with one in four marketplace enrollees dropping coverage. That means more uninsured patients showing up in ERs, less preventive care, and more strain on already struggling rural hospitals.

4. (Already) disappearing alternatives to Big Insurance

The ACA marketplaces aren’t just a safety net for individuals but also home to smaller non-profit and regional health plans that give Americans an alternative to the “Big 7” Wall Street-run insurance conglomerates. These community-rooted plans are already facing financial headwinds from shrinking enrollment and Medicaid funding cuts. When premiums spike in 2026, many could lose enough members to be forced out of the market entirely.

And here’s the real danger: The Big 7 can weather this storm. Their huge market capitalizations, government contracts, pharmacy benefit manager (PBM) divisions and sprawling care delivery businesses give them insulation from ACA marketplace losses. In fact, they may see this as an opportunity to buy up the smaller competitors that fail, which would further consolidate their dominance over our health care system. Or they could just decide to flee the ACA marketplace entirely because the population will skewer sicker and older, creating a death spiral that the big insurers will not want to touch. What little consumer choice exists outside the big corporate insurers could vanish, and even that could disappear.

5. <65 year olds

Perhaps the most vulnerable group will be Americans in their 50s and early 60s who lose their jobs or retire early (often not by choice) and find themselves too young for Medicare but facing incredibly high premiums on the individual market. Under ACA rules, insurers can charge older enrollees up to three times more than younger adults for the same coverage. The enhanced subsidies have been the only thing keeping many of these premiums within reach.

Take those subsidies away, and a 60-year-old who loses employer coverage could see their monthly premium shoot into four figures. For those living off severance, savings or reduced income, choosing to gamble with their health and wait it out until 65 may be the only option.

Congress knows the stakes. Will they act?

Making the subsidies permanent would cost $383 billion over 10 years, which would be a political hurdle for a Congress intent on deep budget cuts. But the cost of inaction is far higher, both in human and economic terms. These subsidies have kept coverage affordable for millions, fueled small business growth, and stabilized state health systems during one of the most turbulent economic periods in recent memory. Without them, the hit to many folks could be a Frazier-level K.O.

But let’s face it — what I’m advocating for isn’t perfect either. The prospect of extending these subsidies raises a question: Should taxpayers be footing the bill for health insurance premiums when insurance corporations are reporting tens of billions in annual profits and paying hefty dividends to shareholders?

The short answer, for now, unfortunately, is yes. Because this is the deck we’ve been dealt and we can’t let Americans fall into medical debt, lose their homes – or their lives. Extending the ACA subsidies is not pretty. But for Americans, it’s just a bob and weave.

People who buy health insurance through the Affordable Care Act (ACA) are set to see a median premium increase of 18 percent, more than double last year’s 7 percent median proposed increase, according to an analysis of preliminary filings by KFF.

The proposed rates are preliminary and could change before being finalized in late summer. The analysis includes proposed rate changes from 312 insurers in all 50 states and DC.

It’s the largest rate change insurers have requested since 2018, the last time that policy uncertainty contributed to sharp premium increases. On average, ACA marketplace insurers are raising premiums by about 20 percent in 2026, KFF found.

Insurers said they wanted higher premiums to cover rising health care costs, like hospitalizations and physician care, as well as prescription drug costs. Tariffs on imported goods could play a role in rising medical costs, but insurers said there was a lot of uncertainty around implementation, and not many insurers were citing tariffs as a reason for higher rates.

But they are adding in higher increases due to changes being made by the Trump administration and Republicans in Congress. For instance, the majority of insurers said they are taking into account the potential expiration of enhanced premium tax credits.

Those subsidies, put in place during the COVID-19 pandemic, are set to expire at the end of the year, and there are few signs that Republicans are interested in tackling the issue at all.

If Congress takes no action, premiums for subsidized enrollees are projected to increase by over 75 percent starting in January 2026, according to KFF.

But some states are pushing back.

Arkansas Gov. Sarah Huckabee Sanders (R) on Wednesday called on the state’s insurance commissioner to disapprove the proposed increases from Centene and Blue Cross Blue Shield. The companies filed increases of up to 54 percent and 25.5 percent, respectively, she said.

“Arkansas’ Insurance Commissioner is required to disapprove of proposed rate increases if they are excessive or discriminatory, and these are both,” Huckabee Sanders said in a statement.

“I’m calling on my Commissioner to follow the law, reject these insane rate increases, and protect Arkansans.”

July 2025 will be the month U.S. healthcare leaders recognize as the industry’s modern turning point. Consider…

On July 4, the One Big Beautiful Bill Act was signed into law setting in motion $960 billion in Medicaid cuts over the decade and massive uncertainty among those most adversely impacted—low income and under-served populations dependent on public programs, 8 to 11 million who used now-suspended marketplace subsidies to buy insurance coverage, and hundreds of state and local health agencies left in funding limbo.

On July 15, the Bureau of Labor Statistics reported the June Consumer Price Index rose .3% bumping the LTM to 2.7% (lower than LTM of 3.4% for medical services). Prices have edged up.

On July 31, President Trump issued an Executive Order to 17 drug companies ordering them to reduce prices on their drugs by September 29 or else. And CMS issued final rules for FY2026 Medicare payments to hospitals, rehab and other providers reflecting increases ranging from 2.5-3.3% effective October 1.

And on the same day, the Bureau of Labor issued its July 2025 jobs report that showed a disappointing net gain of 73,000 jobs plus downward revisions for May and June of 258,000 sparking Wall Street anxiety and President Trump to call the results “rigged” before firing BLS head Erika McEntarfer. Note: healthcare added 55,000 in July—the biggest of any sector and more than its 42,000 average monthly increase.

Collectively, these actions reflect rejection of the health industry by the GOP-led Congress.

It follows 15 years of support vis a vis the Affordable Care Act (2010) and pandemic recovery emergency funding (2020-2021). In that 15-year period, the bigger players got bigger in each sector, investment of private equity in each sector became more prevalent, costs increased, affordability for consumers and employers decreased, and the public’s overall satisfaction with the health system declined precipitously.

For the four major players in the system, the passage of the “big, beautiful bill” was a disappointment. Their primary concerns were not addressed:

Physicians wanted relieffrom annual payment cuts by Medicare preferring reimbursement tied directly to medical inflation. And insurer’ prior authorization and provider reimbursement was a top issue. Status: Not much has changed though adjustments are promised.

Hospitals wanted continuation of federal Medicaid funding, protection of the 340B drug purchasing program, rejection of site-neutral payment policies, higher Medicare reimbursement and relief from insurer prior authorization frustrations. Status: Medicaid funding is being cut forcing the issue for states. CMS payment increases for 2026 are lower than operating cost increases. Insurers have promised prior-auth relief but details about how and when are unknown. And Congress posture toward hospitals seems harsh: price transparency compliance, safety event reporting, and cost concerns are bipartisan issues.

Insurers wanted sustained funding for state Medicaid and Medicare Advantage programs and federal pushback against drug prices and hospital consolidation. Status: Congress appears sympathetic to enrollee complaints and anxious to address insurer “waste, fraud and abuse” including overpayments in Medicare Advantage.

Drug companies oppose “Most Favored Nation” pricing and want protections of their patents and limits on how much insurers, pharmacy benefits managers, wholesalers, online distributors and other “middlemen” earn at their expense. Status: to date, little action despite sympathetic rhetoric by lawmakers. Status: to date, Congress has taken nominal action beyond the Inflation Reduction Act (2022) though 23 states have passed legislation requiring PBMs, insurers and manufacturers to disclose drug prices and 12 states have established Prescription Drug Affordability Boards to monitor prices.

My take:

The landscape for U.S. healthcare is fundamentally changed as a result of the July actions noted above. It is compounded by public anxiety about the economy at home and global tensions abroad.

These July actions were a turning point for the industry: responding appropriately will require fresh ideas and statesmanship. Transparency about prices, costs, incentives and performance is table stakes. Leaders dedicated to the greater good will be the difference.

Imagine you’re facing your midyear performance review with your boss. You dread it, even though you’ve done all you thought possible and legal to help the company meet Wall Street’s profit expectations, because shareholders haven’t been pleased with your employer’s performance lately.

Now let’s imagine your employer is a health insurance conglomerate like, say, UnitedHealth Group. You’ve watched as the stock price has been sliding, sometimes a little and on some days crashing through lows not seen in years, like last Friday (down almost 5% in a single day, to $237.77, which is down a stunning 62% since a mid-November high of $630 and change).

You know what your boss is going to say. We all have to do more to meet the Street’s expectations. Something has changed from the days when the government and employers were overly generous, not questioning our value proposition, always willing to pick up the tab and pay many hidden tips, and we could pull our many levers to make it harder for people to get the care they need.

Despite government and media reports for years that the federal government has been overpaying Medicare Advantage plans like UnitedHealth’s – at least $84 billion this year alone – Congress has pretended not to notice. There is evidence that might be changing, with Republicans and Democrats alike making noises about cracking down on MA plans.

Employers have complained for ages about constantly rising premiums, but they’ve sucked it up, knowing they could pass much of the increase onto their workers – and make them pay thousands of dollars out of their own pockets before their coverage kicks in. Now, at least some of them are realizing they don’t have to work with the giant conglomerates anymore.

Doctors and hospitals have complained, too, about burdensome paperwork and not getting paid right and on time, but they’ve largely been ignored as the big conglomerates get bigger and are now even competing with them.

UnitedHealth is the biggest employer of doctors in the country. But doctors and hospitals are beginning to push back, too.

Since last fall, UnitedHealth and its smaller but still enormous competitors have found that “headwinds” are making it harder for them to maintain the profit margins investors demand. That is mainly because, despite the many barriers patients have to overcome to get the care they need, many of them are nevertheless using health care, often in the most expensive setting – the emergency room. They put off seeing a doctor so long because of insurers’ penny-wise-pound-foolishness that they had some kind of event that scared them enough to head straight to the ER.

It’s not just you who is dreading your midyear review. Everybody, regardless of their position on the corporate ladder, and even the poorly paid folks in customer service, are in the same boat. And so is your boss. Nobody will put the details of what has to be done in writing. They don’t have to. Your boss will remind you that you have to do your part to help the company achieve the “profitable growth” Wall Street demands, quarter after quarter after quarter. It never, ever ends. You know this because you and most other employees watch what happens after the company releases quarterly financials. You also watch your 401K balance and you see the financial consequences of a company that Wall Street isn’t happy with. And Wall Street is especially unhappy with UnitedHealth these days.

And when things are as bad as they are now at UnitedHealth’s headquarters in Minnesota, you know that a big consulting firm like McKinsey & Company has been called in, and that those suits will recommend some kind of “restructuring” and changes in leadership to get the ship back on course. You know the drill. Everybody already is subject to forced ranking, meaning that at the end of the year, some of your colleagues, regardless of job title, will fall below a line that means automatic termination. You pedal as fast as you can to stay above that line, often doing things you worry are not in the best interest of millions of people and might not even be lawful. But you know that if you have any chance of staying employed, much less getting a raise or bonus, you have to convince your superiors you are motivated and “engaged to win.” No one is safe. Look what happened to Sir Andrew Witty, whose departure as CEO to spend more time with his family (in London) was announced days after shareholders turned thumbs down on the company’s promises to return to an acceptable level of profitability.

If you are at UnitedHealth, you listened to what the once and again CEO, Stephen Hemsley, and CFO John Rex, who got shuffled to a lesser role of “advisor” to the CEO last week, laid out a new action plan to their bosses – big institutional investors who have been losing their shirts for months now. You know that what the C-Suite promised on their July 29 call will mean that you will have to “execute” to enable the company to deliver on those promises. And you know that you and your colleagues will have to inflict a lot more pain on everybody who is not a big shareholder – patients, taxpayers, employers, doctors, hospital administrators. That is your job. And you will try to do it because you have a mortgage, kids in college and maxed-out credit cards.

Here’s what Hemsley and his leadership team said, out loud in a public forum, although admittedly one that few people know about or can take an hour-and-a-half to listen to:

Even though UnitedHealth took in billions more in revenue, its margins shrank a little because it had to pay more medical claims than expected.

Still, the company made $14.3 billion in profits during the second quarter. That’s a lot but not as much as the $15.8 billion in 2Q 2024, and that made shareholders unhappy.

Enrollment in its commercial (individual and employer) plans increased just 1%, but enrollment in its Medicare Advantage plans increased nearly 8%. That’s normally just fine, but something happened that the company’s beancounters couldn’t stop.

Those seniors figured out how to get at least some care despite the company’s high barriers to care (aggressive use of prior authorization, “narrow” networks of providers, etc.)

To fix all of this, Hemsley and team promised:

To dump 600,000 or so enrollees who might need care next year

To raise premiums “in the double digits” – way above the “medical trend” that PriceWaterhouseCoopers predicts to be 8.5% (high but not double-digit high)

Boot more providers it doesn’t already own out of network

Reduce benefits

Throughout the call with investors (actually with a couple dozen Wall Street financial analysts, the only people who can ask questions), Hemsley and team went on and on about the “value-based care” the company theoretically delivers, without providing specifics. But here is what you need to know: If you are enrolled in a UnitedHealth plan of any nature – commercial, Medicare or Medicaid or VA (yes, VA, too) – expect the value of your coverage to diminish, just as it has year after year after year.

The term for this in industry jargon is “benefit buydown.”

That means that even as your premiums go up by double digits, you will soon have fewer providers to choose from, you likely will spend more out-of-pocket before your coverage kicks in, you might have to switch to a medication made by a drug company UnitedHealth will get bigger kickbacks from, and you might even be among the 600,000 policyholders who will get “purged” (another industry term) at the end of the year.

Why do we and our employers and Uncle Sam keep putting up with this?

Yes, we pay more for new cars and iPhones, but we at least can count on some improvements in gas mileage and battery life and maybe even better-placed cup holders. You can now buy a massive high-def TV for a fraction of what it cost a couple of years ago. Health insurance? Just the opposite.

As I will explain in a future post, all of the big for-profit insurers are facing those same headwinds UnitedHealth is facing. You will not be spared regardless of the name on your insurance card. If you still have one come January 1. Pain is on the way. Once again.

The healthcare industry is still licking its wounds from $1 trillion in federal funding cuts included in the One Big Beautiful Bill Act (OBBBA) signed into law July 4.

Adding insult to injury, the Center for Medicare and Medicaid services issued a 913-page proposed rule last Tuesday that includes unwelcome changes especially troublesome for hospitals i.e. adoption of site neutral payments, expansion of hospital price transparency requirements, reduction of inpatient-only services, acceleration of hospital 340B discount repayment obligations and more.

The combination of the two is bad news for healthcare overall and hospitals especially: the timing is precarious:

Economic uncertainty: Economists believe a recession is less likely but uncertainty about tariffs, fear about rising inflation, labor market volatility a housing market slowdown and speculation about interest rates have capital markets anxious. Healthcare is capital intense: the impact of the two in tandem with economic uncertainty is unsettling.

Consumer spending fragility: Consumer spending is holding steady for the time being but housing equity values are dropping, rents are increasing, student loan obligations suspended during Covid are now re-activated, prices for hospital and physicians are increasing faster than other necessities and inflation ticked up slightly last month. Consumer out-of-pocket spending for healthcare products and services is directly impacted by purchases in every category.

Heightened payer pressures: Insurers and employers are expecting double-digit increases for premiums and health benefits next year blaming their higher costs on hospitals and drugs, OBBBA-induced insurance coverage lapses and systemic lack of cost-accountability. For insurers, already reeling from 2023-2024 financial reversals, forecasts are dire. Payers will heighten pressure on healthcare providers—especially hospitals and specialists—as a result.

Why healthcare appears to have borne the brunt of the funding cuts in the OBBBA is speculative:

Might a case have been made for cuts in other departments? Might healthcare programs other than Medicaid have been ripe for “waste, fraud and abuse” driven cuts? Might technology-driven administrative costs reductions across the expanse of federal and state government been more effective than DOGE- blunt experimentation?

Healthcare is 18% of the GDP and 28% of total federal spending: that leaves room for cuts in other industries.

Why hospitals, along with nursing homes and public health programs, are likely to bear the lion’s share of OBBBA’ cut fallout and CMS’ proposed rule disruptions is equally vexing. Might the high-profile successes of some not-for-profit hospital operators have drawn attention? Might Congress have been attentive to IRS Form 990 filings for NFP operators and quarterly earnings of investor-owned systems and assume hospital finances are OK? Might advocacy efforts to maintain the status quo with facility fees, 340B drug discounts, executive compensation et al been overshadowed by concerns about consolidation-induced cost increases and disregard for affordability? Hospital emergency rooms in rural and urban communities, nursing homes, public health programs and many physicians will be adversely impacted by the OBBBA cuts: the impact will vary by state. What’s not clear is how much.

My take:

Having read both the OBBBA and CMS proposed rules and observed reactions from industry, two things are clear to me:

The antipathy toward the healthcare industry among the public and in Congress played a key role in passage of the OBBBA and regulatory changes likely to follow.

Polls show three-fourths of likely voters want to see transformational change to healthcare and two-thirds think the industry is more concerned with its profit over their care: these views lend to hostile regulatory changes. The public and the majority of elected officials think the industry prioritizes protection of the status quo over obligations to serve communities and the greater good.

The result: winners and losers in each sector, lack of continuity and interoperability, runaway costs and poor outcomes.

No sector in healthcare stands as the surrogate for the health and wellbeing of the population. There are well-intended players in each sector who seek the moral high ground for healthcare, but their boards and leaders put short-term sustainability above long-term systemness and purpose. That void needs to be filled.

The timing of these changes is predictably political.

Most of the lower-cost initiatives in both the OBBBA changes and CMS proposals carry obligations to commence in 2026—in time for the November 2026 mid-term campaigns. Most of the results, including costs and savings, will not be known before 2028 or after. They’re geared toward voters inclined to think healthcare is systemically fraudulent, wasteful and self-serving.

And they’re just the start: officials across the Departments of Health and Human Services, Justice, Commerce, Labor and Veterans Affairs will add to the lists.

Medicaid cuts have received the lion’s share of attention from critics of Republicans’ sweeping tax cuts legislation, but the GOP’s decision not to extend enhanced ObamaCare subsidies could have a much more immediate impact ahead of next year’s midterms.

Extra subsidies put in place during the coronavirus pandemic are set to expire at the end of the year, and there are few signs Republicans are interested in tackling the issue at all.

To date, only Sens. Lisa Murkowski (R-Alaska) and Thom Tillis (R-N.C.) have spoken publicly about wanting to extend them.

The absence of an extension in the “big, beautiful bill” was especially notable given the sweeping changes the legislation makes to the health care system, and it gives Democrats an easy message: If Republicans in Congress let the subsidies expire at the end of the year, premiums will spike, and millions of people across the country could lose health insurance.

In a statement released last month as the House was debating its version of the bill, House and Senate Democratic health leaders pointed out what they said was GOP hypocrisy.

“Their bill extends hundreds of tax policies that expire at the end of the year. The omission of this policy will cause millions of Americans to lose their health insurance and will raise premiums on 24 million Americans,” wrote Senate Finance Committee ranking member Ron Wyden (D-Ore.), House Ways and Means Committee ranking member Richard Neal (D-Mass.) and House Energy and Commerce Committee ranking member Frank Pallone (D-N.J.).

“The Republican failure to stop this premium spike is a policy choice, and it needs to be recognized as such.”

More than 24 million Americans are enrolled in the insurance marketplace this year, and about 90 percent — more than 22 million people — are receiving enhanced subsidies.

“All of those folks will experience quite large out-of-pocket premium increases,” said Ellen Montz, who helped run the federal ObamaCare exchanges under the Biden administration and is now a managing director with Manatt Health.

“When premiums become less affordable, you have this kind of self-fulfilling prophecy where the youngest and the healthiest people drop out of the marketplace, and then premiums become even less affordable in the next year,” Montz said.

The subsidies have been an extremely important driver of ObamaCare enrollment. Experts say if they were to expire, those gains would be erased.

According to the Congressional Budget Office (CBO), 4.2 million people are projected to lose insurance by 2034 if the subsidies aren’t renewed.

Combined with changes to Medicaid in the new tax cut law, at least 17 million Americans could be uninsured in the next decade.

The enhanced subsidies increase financial help to make health insurance plans more affordable. Eligible applicants can use the credit to lower insurance premium costs upfront or claim the tax break when filing their return.

Premiums are expected to increase by more than 75 percent on average, with people in some states seeing their payments more than double, according to health research group KFF.

Devon Trolley, executive director of Pennie, the Affordable Care Act (ACA) exchange in Pennsylvania, said she expects at least a 30 percent drop in enrollment if the subsidies expire.

The state starts ramping up its open enrollment infrastructure in mid-August, she said, so time is running short for Congress to act.

“The only vehicle left for funding the tax credits, if they were to extend them, would be the government funding bill with a deadline of September 30, which we really see as the last possible chance for Congress to do anything,” Trolley said.

Trolley said three-quarters of enrollees in the state’s exchange have never purchased coverage without the enhanced tax credits in place.

“They don’t know sort of a prior life of when the coverage was 82 percent more expensive. And we are very concerned this is going to come as a huge sticker shock to people, and that is going to significantly erode enrollment,” Trolley said.

The enhanced subsidies were first put into effect during the height of the coronavirus pandemic as part of former President Biden’s 2021 economic recovery law and then extended as part of the Inflation Reduction Act.

The CBO said permanently extending the subsidies would cost $358 billion over the next 10 years.

Republicans have balked at the cost. They argue the credits hide the true cost of the health law and subsidize Americans who don’t need the help. They also argue the subsidies have been a driver of fraudulent enrollment by unscrupulous brokers seeking high commissions.

Sen. Bill Cassidy (R-La.), chair of the Senate Health, Education, Labor and Pensions Committee, last year said Congress should reject extending the subsidies.

The Republican Study Committee’s 2025 fiscal budget said the subsidies “only perpetuate a never-ending cycle of rising premiums and federal bailouts — with taxpayers forced to foot the bill.”

But since 2020, enrollment in the Affordable Care Act marketplace has grown faster in the states won by President Trump in 2024, primarily rural Southern red states that haven’t expanded Medicaid. Explaining to millions of Americans why their health insurance premiums are suddenly too expensive for them to afford could be politically unpopular for Republicans.

According to a recent KFF survey, 45 percent of Americans who buy their own health insurance through the ACA exchanges identify as Republican or lean Republican. Three in 10 said they identify as “Make America Great Again” supporters.

“So much of that growth has just been a handful of Southern red states … Texas, Florida, Georgia, the Carolinas,” said Cynthia Cox, vice president at KFF and director of the firm’s ACA program. “That’s where I think we’re going to see a lot more people being uninsured.”

The “Big Beautiful Budget Bill” appears headed for passage with cuts to Medicaid and potentially Medicare likely elements.

The economy is slowing, with a mild recession a possibility as consumer confidence drops, the housing market slows and uncertainty about tariffs mounts.

And partisan brinksmanship in state and federal politics has made political hostages of public and rural health safety net programs as demand increases for their services.

Last Wednesday, amidst mounting anxiety about the aftermath of U.S. bunker-bombing in Iran and escalating conflicts in Gaza and Ukraine, the Centers for Medicare and Medicaid Services (CMS) released its report on healthcare spending in 2024 and forecast for 2025-2033:

“National health expenditures are projected to have grown 8.2% in 2024 and to increase 7.1% in 2025, reflecting continued strong growth in the use of health care services and goods.

During the period 2026–27, health spending growth is expected to average 5.6%, partly because of a decrease in the share of the population with health insurance (related to the expiration of temporarily enhanced Marketplace premium tax credits in the Inflation Reduction Act of 2022) and partly because of an anticipated slowdown in utilization growth from recent highs. Each year for the full 2024–33 projection period, national health care expenditure growth (averaging 5.8%) is expected to outpace that for the gross domestic product (GDP; averaging 4.3%) and to result in a health share of GDP that reaches 20.3% by 2033 (up from 17.6% in 2023) …

Although the projections presented here reflect current law, future legislative and regulatory health policy changes could have a significant impact on the projections of health insurance coverage, health spending trends, and related cost-sharing requirements, and they thus could ultimately affect the health share of GDP by 2033.”

As has been the case for 20 years, spending for healthcare grew faster than the overall economy in 2024. And it is forecast to continue through 2033:

2024Baseline

2033Forecast

% Nominal Chg.2024-2033

National Health Spending

$5,263B

$8,585B

+63.1%

US Population

337,2M

354.8M

+5.2%

Per capita personal health spending

$13,227

$20,559

+55.7%

Per capita disposable personal income

$21,626

$31,486

+45.6%

NHE as % of US GDP

18.0%

20.3%

+12.8%

In its defense, industry insiders call attention to the uniqueness of the business of healthcare:

‘Healthcare is a fundamental need: the health system serves everyone.’

‘Our aging population, chronic disease prevalence and socioeconomic disparities are drive increased demand for the system’s products and services.’

‘The public expects cutting edge technologies, modern facilities, effective medications and the best caregivers and they’re expensive.’

‘Burdensome regulatory compliance costs contribute to unnecessary spending and costs.’

And they’re right.

Critics argue the U.S. health system is the world’s most expensive but its results (outcomes) don’t justify its costs. They acknowledge the complexity of the industry but believe “waste, fraud and abuse” are pervasive flaws routinely ignored. And they remind lawmakers that the health economy is profitable to most of its corporate players (investor-owned and not-for-profits) and its executive handsomely compensated.

Healthcare has been hit by a perfect storm at a time when a majority of the public associates it more with corporatization and consolidation than caring. This coalition includes Gen Z adults who can’t afford housing, small employers who’ve cut employee coverage due to costs and large, self-insured employers who trying to navigate around the 10-20% employee health cost increase this year, state and local governments grappling with health costs for their public programs and many more. They’re tired of excuses and think the health system takes advantage of them.

As a percentage of the nation’s GDP and household discretionary spending, healthcare will continue to be disproportionately higher and increasingly concerning. Spending will grow faster than other industries until lawmakers impose price controls and other mechanisms like at least 8 states have begun already.

Most insiders are taking cover and waiting ‘til the storm passes. Some are content to cry foul and blame others. Others will emerge with new vision and purpose centered on reality.

Storm damage is rarely predictable but always consequential. It cannot be ignored. The Perfect has Hit U.S. healthcare. Its impact is not yet known but is certain to be a game changer.

New Medicaid funding rules proposed by Congress this week would halt efforts at the state level to better fund rural hospitals and deliver services to the most vulnerable populations in those areas. You can be certain that the administrators and staff of those hospitals, as well as leaders of the communities they serve, are watching closely to see if the cuts are enacted.

Lawmakers at the federal level are trying to make deeper cuts to Medicaid spending in an effort to lower the amount of deficit spending that would be created by President Trump’s spending plan. Trump has dubbed the plan his “big beautiful bill.”

Feds Would Strip Rural Hospitals of Lifeline Funds

Republican members of the Senate Finance Committee this week released their version of the bill that would drain funding for rural hospitals, which rely heavily on Medicaid funds to treat patients. It’s estimated that 25 to 40 percent of services provided by such hospitals are funded by Medicaid.

The federal government and states share the up-front medical costs for Medicaid patients. The federal government then reimburses states up to 50 percent of their Medicaid spending every year.

Many states fund their portion of the cost by taxing entities that provide those services to Medicaid patients.

The latest proposal in Congress would not only restrict how many patients could receive benefits, but it would also stop states from implementing those provider tax programs to help fund Medicaid services provided to residents.

At the federal level, the thinking is that if states keep taxing providers to fund Medicaid services, then the federal government will have to keep reimbursing states a portion of those costs.

The downside to that is many experts, along with several Republicans in Congress, namely Sens. Susan Collins of Maine, Lisa Murkowski of Alaska and Josh Hawley of Missouri, have predicted it will decimate rural hospitals.

West Virginia Republican Sen. Jim Justice went a step further, saying that the plan to limit states’ use of provider taxes will “really hurt a lot of folks.” Despite that statement, Justice said he is OK with the freeze.

State Lawmakers Sound the Alarm

There are 39 states with at least three or more provider taxes used to help fund Medicaid services. Alaska is the only state with no such tax.

Some states, such as Ohio, have set up a new rural hospital fund using provider taxes to help rural hospitals deliver Medicaid services to patients.

Ohio Governor Mike DeWine and the Republican-led state legislature set up a pilot program called the Rural Ohio Hospital Tax Pilot Program. The measure would allow counties to levy a tax on their local hospitals that would then be used to fund Medicaid services.

DeWine said the pilot program would help ease the financial stress rural hospitals face in Ohio. The plan contained in Ohio House Bill 96 has the blessing of the Ohio Hospital Association.

A group of Republican state lawmakers recently sent a letter to their federal counterparts pleading with them to remove the bill language because it would “torpedo” plans to keep rural hospitals functioning.

The American Hospital Association, a 130-year-old trade group of more than 5,000 hospitals and health care providers, this month released the impact on rural hospitals if this plan went into effect.

More than $50 billion would be lost by 2034, and more than 1.8 million rural Americans would lose health benefits.

Kentucky residents would be impacted the most, with 143,000 losing benefits, followed by 135,000 Californians. More than 86,000 Ohioans would lose Medicaid coverage under the plan by 2034, making it the third most impacted state.

To blunt the effects of the cuts, Collins reportedly is proposing the establishment of a $100 billion relief fund that could provide financial support to affected providers, rural hospitals in particular. Whether that or a similar but smaller fund will wind up in the final draft of the legislation apparently will be decided this weekend. Meanwhile, the Senate parliamentarian has ruled against many of the provisions of the Senate version of the bill, including the Finance Committee’s provider tax framework, which puts the whole thing in flux.

Senate leaders say they plan a long series of votes on amendments of the bill on Sunday. The “vote-arama” likely will go on throughout Sunday night and into Monday. If the Senate does pass its version of the bill, it will have to go back to the House. Lawmakers are under a self-imposed deadline to get the legislation to Trump by the July 4 holiday.