Hospitals and health systems across the country are telling some Medicare and Medicaid patients that they can’t schedule telehealth appointments due to the federal government’s shutdown, now heading into its second week. That’s because Medicare reimbursement for telehealth expired on September 30, leaving health systems with the choice of pausing such visits or keeping them going in hopes of retroactive reimbursement after the shutdown ends.

Reimbursement for the Hospital at Home program, which allows patients to receive care without being admitted to a hospital, also lapsed with the shutdown. That led to providers scrambling to discharge patients under the program or admit them to a hospital. Mayo Clinic, for example, had to move around 30 patients from their homes in Arizona, Florida and Wisconsin to its facilities.

At issue in the government shutdown is healthcare, specifically tax credits for middle- and lower-income Americans that enable them to afford health insurance on the federal exchanges set up by the Affordable Care Act. Democrats want to extend those tax credits, which are set to expire at the end of the year, while Republicans want to reopen the government first and then negotiate about the tax credits in a final budget.

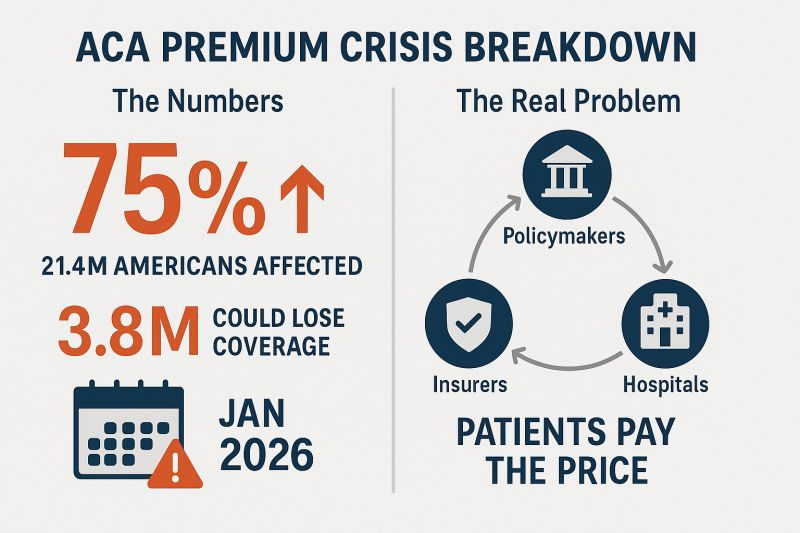

The impasse has prevented the Senate from overcoming a filibuster, despite a Republican majority. Around 24 million Americans get their health insurance through the ACA, and the loss of tax credits will cause their premiums to rise an average of 75%–and as high as 90% in rural areas–and likely cause at least 4 million people to lose coverage entirely.

The government’s closure has reverberated through its operations in healthcare. The Department of Health and Human Services has furloughed some 41% of its staff, making it harder to run oversight operations. CDC’s lack of staff will hinder surveillance of public health threats. And FDA won’t accept any new drug applications until funding is restored.

When the government might reopen remains unclear. Most shutdowns are relatively brief, but the longest one, which lasted 35 days, came during Donald Trump’s first term. Senate majority leader John Thune, R-S.D., and Speaker of the House Mike Johnson, R-La., have both said they won’t negotiate with Democrats, and the House won’t meet again until October 14.Bettors on Polymarket currently expect it to last until at least October 15. Pressure on Congress will increase after that date because there won’t be funds available to pay active military members.

People who buy health insurance through the Affordable Care Act (ACA) are set to see a median premium increase of 18 percent, more than double last year’s 7 percent median proposed increase, according to an analysis of preliminary filings by KFF.

The proposed rates are preliminary and could change before being finalized in late summer. The analysis includes proposed rate changes from 312 insurers in all 50 states and DC.

It’s the largest rate change insurers have requested since 2018, the last time that policy uncertainty contributed to sharp premium increases. On average, ACA marketplace insurers are raising premiums by about 20 percent in 2026, KFF found.

Insurers said they wanted higher premiums to cover rising health care costs, like hospitalizations and physician care, as well as prescription drug costs. Tariffs on imported goods could play a role in rising medical costs, but insurers said there was a lot of uncertainty around implementation, and not many insurers were citing tariffs as a reason for higher rates.

But they are adding in higher increases due to changes being made by the Trump administration and Republicans in Congress. For instance, the majority of insurers said they are taking into account the potential expiration of enhanced premium tax credits.

Those subsidies, put in place during the COVID-19 pandemic, are set to expire at the end of the year, and there are few signs that Republicans are interested in tackling the issue at all.

If Congress takes no action, premiums for subsidized enrollees are projected to increase by over 75 percent starting in January 2026, according to KFF.

But some states are pushing back.

Arkansas Gov. Sarah Huckabee Sanders (R) on Wednesday called on the state’s insurance commissioner to disapprove the proposed increases from Centene and Blue Cross Blue Shield. The companies filed increases of up to 54 percent and 25.5 percent, respectively, she said.

“Arkansas’ Insurance Commissioner is required to disapprove of proposed rate increases if they are excessive or discriminatory, and these are both,” Huckabee Sanders said in a statement.

“I’m calling on my Commissioner to follow the law, reject these insane rate increases, and protect Arkansans.”

Ahead of my Congressional testimony last week before the Senate HELP committee, I compiled data on the profits, revenues and CEO compensations of big health insurers in 2024. The curiosity from senators on both sides of the aisle signaled, to me, that lawmakers are as interested as I’ve ever seen in the industry’s rampant profiteering.

What I found was that the seven biggest publicly traded health insurance companies collectively made $71.3 billion in profits, up more than half a billion dollars from 2023. All while millions of Americans continued to skip their medications, rationed insulin and delayed care due to insurers’ out-of-pocket demands.

Let’s break it down.

You won’t be surprised to learn that shareholders are not the only ones benefiting from the care-restricting barriers insurers have erected to boost profits. The CEOs of those seven companies took home a combined $146.1 million in 2024 compensation. That’s enough to cover annual premiums for thousands of American families.

Here’s what the top brass made:

Meanwhile, patients across the country report increasing out-of-pocket costs, more aggressive prior authorizations and narrower provider networks. But for these executives, the real measure of success is how high they can push their stock prices and not how many people can afford to see a doctor.

So, What’s Driving the Revenue Surge?

One word: Gouging.

Insurers continued to jack up premiums for their commercial customers and overcharge the government. Despite watchdog warnings, Uncle Sam continues to pour money into private Medicare Advantage plans even as audits and investigations uncover widespread fraud and upcoding. And Medicaid managed care is a gold mine, too. These insurers now dominate state Medicaid contracts and can quietly extract billions through behind-the-scenes ownership of pharmacies, PBMs and providers.

It’s not just health insurance anymore — it’s a monopolized empire.

All that said, to the dismay of shareholders, the big seven insurers have had to admit that so far in 2025, they’ve paid more medical claims than they had expected, which means their profits were down somewhat during the first months of the year. I’ll shed more light on that in a future post. No need for you to shed any tears for them, though, because we’re still talking billions and billions in profits.

So if you’re wondering why your premiums, deductibles and costs at the pharmacy counter keep going up — just look at those 2024 numbers. We all paid more for health insurance and got less for the hard-earned money we had to shovel out for our “coverage.”

And expect even more financial pain (and difficulty getting the care you need) as these companies do all they can to get their profit margins back to where Wall Street wants them.

Imagine you’re facing your midyear performance review with your boss. You dread it, even though you’ve done all you thought possible and legal to help the company meet Wall Street’s profit expectations, because shareholders haven’t been pleased with your employer’s performance lately.

Now let’s imagine your employer is a health insurance conglomerate like, say, UnitedHealth Group. You’ve watched as the stock price has been sliding, sometimes a little and on some days crashing through lows not seen in years, like last Friday (down almost 5% in a single day, to $237.77, which is down a stunning 62% since a mid-November high of $630 and change).

You know what your boss is going to say. We all have to do more to meet the Street’s expectations. Something has changed from the days when the government and employers were overly generous, not questioning our value proposition, always willing to pick up the tab and pay many hidden tips, and we could pull our many levers to make it harder for people to get the care they need.

Despite government and media reports for years that the federal government has been overpaying Medicare Advantage plans like UnitedHealth’s – at least $84 billion this year alone – Congress has pretended not to notice. There is evidence that might be changing, with Republicans and Democrats alike making noises about cracking down on MA plans.

Employers have complained for ages about constantly rising premiums, but they’ve sucked it up, knowing they could pass much of the increase onto their workers – and make them pay thousands of dollars out of their own pockets before their coverage kicks in. Now, at least some of them are realizing they don’t have to work with the giant conglomerates anymore.

Doctors and hospitals have complained, too, about burdensome paperwork and not getting paid right and on time, but they’ve largely been ignored as the big conglomerates get bigger and are now even competing with them.

UnitedHealth is the biggest employer of doctors in the country. But doctors and hospitals are beginning to push back, too.

Since last fall, UnitedHealth and its smaller but still enormous competitors have found that “headwinds” are making it harder for them to maintain the profit margins investors demand. That is mainly because, despite the many barriers patients have to overcome to get the care they need, many of them are nevertheless using health care, often in the most expensive setting – the emergency room. They put off seeing a doctor so long because of insurers’ penny-wise-pound-foolishness that they had some kind of event that scared them enough to head straight to the ER.

It’s not just you who is dreading your midyear review. Everybody, regardless of their position on the corporate ladder, and even the poorly paid folks in customer service, are in the same boat. And so is your boss. Nobody will put the details of what has to be done in writing. They don’t have to. Your boss will remind you that you have to do your part to help the company achieve the “profitable growth” Wall Street demands, quarter after quarter after quarter. It never, ever ends. You know this because you and most other employees watch what happens after the company releases quarterly financials. You also watch your 401K balance and you see the financial consequences of a company that Wall Street isn’t happy with. And Wall Street is especially unhappy with UnitedHealth these days.

And when things are as bad as they are now at UnitedHealth’s headquarters in Minnesota, you know that a big consulting firm like McKinsey & Company has been called in, and that those suits will recommend some kind of “restructuring” and changes in leadership to get the ship back on course. You know the drill. Everybody already is subject to forced ranking, meaning that at the end of the year, some of your colleagues, regardless of job title, will fall below a line that means automatic termination. You pedal as fast as you can to stay above that line, often doing things you worry are not in the best interest of millions of people and might not even be lawful. But you know that if you have any chance of staying employed, much less getting a raise or bonus, you have to convince your superiors you are motivated and “engaged to win.” No one is safe. Look what happened to Sir Andrew Witty, whose departure as CEO to spend more time with his family (in London) was announced days after shareholders turned thumbs down on the company’s promises to return to an acceptable level of profitability.

If you are at UnitedHealth, you listened to what the once and again CEO, Stephen Hemsley, and CFO John Rex, who got shuffled to a lesser role of “advisor” to the CEO last week, laid out a new action plan to their bosses – big institutional investors who have been losing their shirts for months now. You know that what the C-Suite promised on their July 29 call will mean that you will have to “execute” to enable the company to deliver on those promises. And you know that you and your colleagues will have to inflict a lot more pain on everybody who is not a big shareholder – patients, taxpayers, employers, doctors, hospital administrators. That is your job. And you will try to do it because you have a mortgage, kids in college and maxed-out credit cards.

Here’s what Hemsley and his leadership team said, out loud in a public forum, although admittedly one that few people know about or can take an hour-and-a-half to listen to:

Even though UnitedHealth took in billions more in revenue, its margins shrank a little because it had to pay more medical claims than expected.

Still, the company made $14.3 billion in profits during the second quarter. That’s a lot but not as much as the $15.8 billion in 2Q 2024, and that made shareholders unhappy.

Enrollment in its commercial (individual and employer) plans increased just 1%, but enrollment in its Medicare Advantage plans increased nearly 8%. That’s normally just fine, but something happened that the company’s beancounters couldn’t stop.

Those seniors figured out how to get at least some care despite the company’s high barriers to care (aggressive use of prior authorization, “narrow” networks of providers, etc.)

To fix all of this, Hemsley and team promised:

To dump 600,000 or so enrollees who might need care next year

To raise premiums “in the double digits” – way above the “medical trend” that PriceWaterhouseCoopers predicts to be 8.5% (high but not double-digit high)

Boot more providers it doesn’t already own out of network

Reduce benefits

Throughout the call with investors (actually with a couple dozen Wall Street financial analysts, the only people who can ask questions), Hemsley and team went on and on about the “value-based care” the company theoretically delivers, without providing specifics. But here is what you need to know: If you are enrolled in a UnitedHealth plan of any nature – commercial, Medicare or Medicaid or VA (yes, VA, too) – expect the value of your coverage to diminish, just as it has year after year after year.

The term for this in industry jargon is “benefit buydown.”

That means that even as your premiums go up by double digits, you will soon have fewer providers to choose from, you likely will spend more out-of-pocket before your coverage kicks in, you might have to switch to a medication made by a drug company UnitedHealth will get bigger kickbacks from, and you might even be among the 600,000 policyholders who will get “purged” (another industry term) at the end of the year.

Why do we and our employers and Uncle Sam keep putting up with this?

Yes, we pay more for new cars and iPhones, but we at least can count on some improvements in gas mileage and battery life and maybe even better-placed cup holders. You can now buy a massive high-def TV for a fraction of what it cost a couple of years ago. Health insurance? Just the opposite.

As I will explain in a future post, all of the big for-profit insurers are facing those same headwinds UnitedHealth is facing. You will not be spared regardless of the name on your insurance card. If you still have one come January 1. Pain is on the way. Once again.

Nearly 12 million people would lose their health insurance under President Trump’s “big, beautiful bill,” an erosion of the social safety net that would lead to more unmanaged chronic illnesses, higher medical debt and overcrowding of hospital emergency departments.

Why it matters:

The changes in the Senate version of the bill could wipe out most of the health coverage gains made under the Affordable Care Act and slash state support for Medicaid and SNAP.

“We are going back to a place of a lot of uncompensated care and a lot of patchwork systems for people to get care,” said Ellen Montz, a managing director at Manatt Health who oversaw the ACA federal marketplace during the Biden administration.

The big picture:

The stakes are huge for low-income and working-class Americans who depend on Medicaid and subsidized ACA coverage.

Without health coverage, more people with diabetes, heart disease, asthma and other chronic conditions will likely go without checkups and medication to keep their ailments in check.

Those who try to keep up with care after losing insurance will pay more out of pocket, driving up medical debt and increasing the risk of eviction, food insecurity and depleted savings.

Uninsured patients have worse cancer survival outcomes and are less likely to get prenatal care. Medicaid also is a major payer of behavioral health counseling and crisis intervention.

Much of the coverage losses from the bill will come from new Medicaid work reporting requirements, congressional scorekeepers predict. Work rules generally will have to be implemented for coverage starting in 2027, but could be earlier or later depending on the state.

Past experiments with Medicaid work rules show that many eligible people fall through the cracks verifying they’ve met the requirements or navigating new state bureaucracies.

Often, people don’t find out they’ve lost coverage until they try to fill a prescription or see their doctor. States typically provide written notices, but contacts can be out of date.

Nearly 1 in 3 adults who were disenrolled from Medicaid after the COVID pandemic found out they no longer had health insurance only when they tried to access care, per a KFF survey.

Zoom out:

The Medicaid and ACA changes will also affect people who keep their coverage.

The anticipated drop-off in preventive care means the uninsured will be more likely to go to the emergency room when they get sick. That could further crowd already bursting ERs, resulting in even longer wait times.

Changes to ACA markets in the bill, along with the impending expiration of enhanced premium subsidies, may drive healthier people to drop out, Montz said, skewing the risk pool and driving up premiums for remaining enrollees.

States will likely have to make further cuts to their safety-net programs if the bill passes in order to keep state budgets functioning with less federal Medicaid funding.

The other side:

The White House and GOP proponents of the bill say the health care changes will fight fraud, waste and abuse, and argue that coverage loss projections are overblown.

Conservative health care thinkers also posit that there isn’t strong enough evidence that public health insurance improves health.

Reality check:

Not all insurance is created equally, and many people with health coverage still struggle to access care. But the bill’s impact would take the focus off ways to improve the health system, Montz said.

“This is taking us catastrophically backward, where we don’t get to think about the things that we should be thinking about how to best keep people healthy,” she said.

The bottom line:

The changes will unfold against a backdrop of Health Secretary Robert F. Kennedy Jr.’s purported focus on preventive care and ending chronic illness in the U.S.

But American health care is an insurance-based system, said Manatt Health’s Patricia Boozang. Coverage is what unlocks access.

Scrapping millions of people’s health coverage “seems inconsistent with the goal of making America healthier,” she said.

Health insurers are starting to notify states that tariffs will drive up the premiums they plan to charge individual and small group market enrollees next year.

Why it matters:

The Trump administration’s trade policy is adding another layer of uncertainty for health costs as Congress considers Medicaid cuts and is expected to sunset enhanced subsidies for Affordable Care Act coverage.

“There are sort of a perfect storm of factors that are driving prices up,” said Sabrina Corlette, research professor at Georgetown’s Center on Health Insurance Reforms.

The big picture:

Health insurers calculate monthly premiums in advance of each year based on the expected price of goods and services and projected demand for them.

Tariffs announced by President Trump are expected to drive up the cost of prescription drugs, medical devices and other medical products and services. Some of that difference ultimately would be passed down to enrollees.

Where it stands:

A handful of health insurers administering individual and small group plans have already explicitly told state regulators that tariffs are forcing plans to raise enrollee premiums more than they otherwise would next year, KFF policy analyst Matt McGough wrote in an analysis published Monday.

Independent Health Benefits Corporation told New York regulators in a filing last month that it plans to raise premiums for its individual market enrollees 38.4% next year.

About 3% of that is directly due to tariffs, based on projections of how much they’ll increase drug prices and the use of imported drugs, Frank Sava, a spokesperson for Independent Health, told Axios.

Similarly, UnitedHealthcare of Oregon said in a filing that nearly 3% of its planned 19.8% premium increase for small group enrollees next year is due to uncertainty around tariffs, particularly on how they’ll affect pharmaceutical prices.

Insurers “don’t have any historical precedent or data to project what this is going to mean for their business and health costs,” McGough said to Axios. “I think it really makes sense that they’re trying to hedge their bets.”

Insurers can’t change their premiums throughout the year. But if health plans do overshoot their premium estimates in rate filings, they have to pay enrollees back the difference in rebates.

While there may be a competitive advantage to keeping premiums lower, there isn’t really a way for insurers to make up for extra unplanned costs after the fact.

Yes, but:

Some insurers indicated that while they’re keeping a close eye on tariff-related impacts, they aren’t baking them into their premium rates yet.

“There is uncertainty around inflation and the economy due to possible tariffs however we did [not] put anything for this in this filing,” Kaiser Foundation Health Plan of the Northwest’s report to Oregon reads.

State regulators can also push back on insurers’ premium calculations before they’re finalized, McGough noted.

What we’re watching:

While some states have earlier deadlines, insurers have to submit their 2026 ACA marketplace plan rates to the federal regulators by July 16, and proposed rates will be posted by August 1.

That’s when we’ll get a better picture of how seriously tariffs are concerning health insurers.

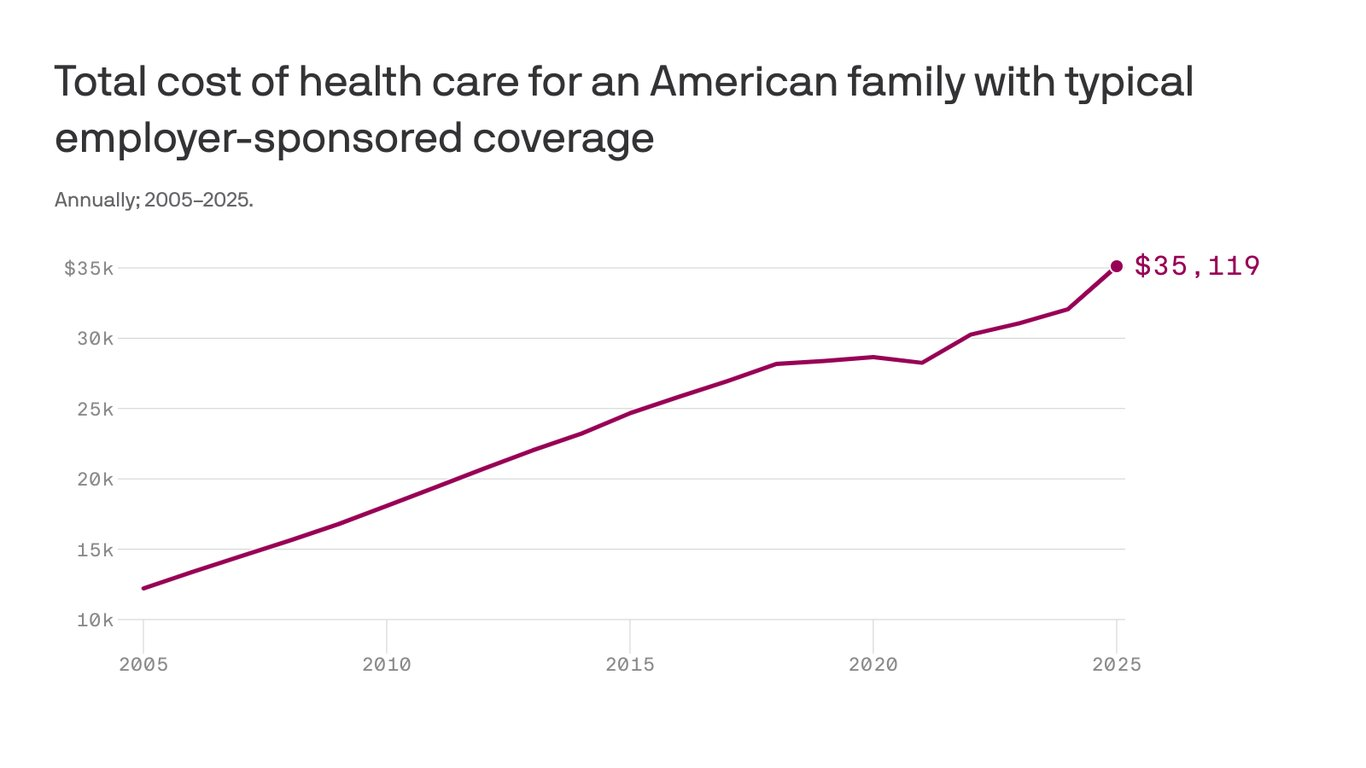

The cost to cover a family of four through workplace insurance now exceeds $35,000, nearly triple what it cost 20 years ago as annual growth in health costs have far outpaced wages.

The big picture:

Growing pharmacy and outpatient facility costs drove most of the increase, which includes employee and employer shares,according to the 2025 Milliman Medical Index.

Employers have been wary of passing health cost hikes to workers in a tight labor market, but the rising demand for costly care may force a reckoning.

State of play:

The $35,119 annual cost to cover a hypothetical family of four this year factors in drug costs, inpatient and outpatient care, and professional services, along with an “other” category that includes home health, ambulance transport, medical equipment and prosthetics.

A year of health care cost a family of four $12,214 in 2005, the year Milliman launched the index. The 20-year cumulative gain of 188% outpaced the 84% growth in wages over the same time.

Health costs have increased about 6% per year on average over the past two decades, according to Milliman, compared with an average inflation rate of 2.5% over that time.

Between the lines:

Employers in 2025 still shoulder 58% of employee health care costs, but their share has shrunk since 2005, when it was more than 60%.

Reality check:

Health care costs vary significantly by age, geography and pharmacy rebate arrangements.

Milliman calculates family cost based on a family with a 47-year-old male, 37-year-old female, and children ages 4 and under 1.

This was a “mathematically average” family in 2005, and Milliman continues to use that formula to keep data comparable year-to-year.

The firm has an online tool that allows readers to input other family configurations to see their estimated 2025 health care costs.

The analysis is based on Milliman’s proprietary research tools and analyzes commercialclaims data. The family cost figure reflects nationwide average negotiated provider fees and average PPO benefit levels.

Wall Street is speaking loudly to Medicare Advantage insurers: If you want us to stick with you, keep dumping seniors who are pinching your profit margins.

Investors continue to punish UnitedHealth Group since the company downgraded its 2025 profit expectations on April 17. On Friday, UnitedHealth’s stock price hit not only a 52-week low—$393.11—but its lowest point in years. The last time UnitedHealth’s stock price went below $400 a share was on October 14, 2021.

The company’s shares lost nearly 4.5% of their value during the past week, contributing to a decline that started soon after the company set an all-time high of $630.73 last November. UnitedHealth’s shares have lost more than 33% of their value since then.

Wall Street Sends a Message

Meanwhile, investors have once again embraced UnitedHealth’s top two rivals in the Medicare Advantage business–Humana and CVS/Aetna. Those companies told investors last year, when both were in the Wall Street dog house for spending more than investors expected on patients’ medical care, that they would dump hundreds of thousands of their costliest Medicare Advantage enrollees to improve their profits. They made good on that promise, shedding almost 650,000 seniors and people with disabilities by the end of the year.

Many of those people enrolled in a UnitedHealth Medicare Advantage plan. The company reported 400,000 more Medicare Advantage enrollees in the first quarter of 2025 than in the fourth quarter of 2024. That used to be a good thing, but UnitedHealth’s executives told investors on April 17 that it wouldn’t make as much money for them as the company had assured them just three months earlier because it likely will have to spend more than they expected on those new MA enrollees’ medical care. Investors responded by immediately dispatching the company’s shares to the cellar. Those shares lost about 23% of their value in a single day.

The Street had also punished Humana and CVS last year when they said they were paying more for seniors’ medical care than they’d expected. Shares of both companies cratered, losing around half their value. So, executives at both Humana and CVS started identifying Medicare markets to get out of entirely. The culling was ruthless. CVS shed 227,000 MA enrollees. Humana got rid of 419,000.

Locked Out of Traditional Medicare

Those seniors and disabled people had to scramble to find a new Medicare Advantage insurer because it is difficult for most people to go back to traditional Medicare and find an affordable Medicare supplement policy. Medicare supplement insurers must waive underwriting during the first six months of applicants’ eligibility for Medicare, but people who enroll in a Medicare Advantage plan and want or need to make a change months later find out that insurers will charge them more unless their health is nearly perfect.

Of the seven big for-profit health insurers, four (Cigna, CVS/Aetna, Humana and Centene) collectively cut 1.3 million of their Medicare Advantage enrollees adrift at the end of 2024 in an effort to stay in Wall Street’s good graces. Cigna dumped all 600,000 of its MA enrollees, selling them to the Blue Cross corporation HCSC. For-profit Blue Cross insurer Elevance picked up 227,000; Molina added 18,000, and, as noted, UnitedHealth signed up 400,000 new MA enrollees.

While UnitedHealth’s shares have lost a third of their value, CVS’s shares have increased more than 50% since the first of this year. They even set a 52-week high of $72.51 on Thursday. Humana’s shares closed Friday at $258.48, up 1.88% since January 1. They are out of the Wall Street dog house – for now, anyway.

Profits, Lobbying Soar

I trust you are not feeling sorry for UnitedHealth because of its misfortune on Wall Street. It is still a hugely profitable company–just not profitable enough lately to please investors. This huge corporation, the fourth largest in America, reported $9.1 billion in profits in just the first quarter of this year. If the company makes it more difficult for its health plan enrollees to get the care they need this year, it could make even more than the $34.4 billion in profits it made last year.

And as a group, the seven big for-profits, including those that spent more than Wall Street felt was necessary on patients’ medical care, made $70 billion in profits last year. (UnitedHealth made nearly as much as the other six combined.)

And collectively, those giant corporations took in a record $1.5 trillion in revenue from us as customers and taxpayers last year. They are doing quite well. But that won’t stop them from trying to keep lawmakers and Trump administration officials from cracking down this year on the widespread waste, fraud and abuse in the Medicare Advantage program. You can expect them to spend a record amount of our money on lobbying expenses in Washington this year to keep their Medicare Advantage cash cow well fed.

Wall Street is speaking loudly to Medicare Advantage insurers: If you want us to stick with you, keep dumping seniors who are pinching your profit margins.

Investors continue to punish UnitedHealth Group since the company downgraded its 2025 profit expectations on April 17. On Friday, UnitedHealth’s stock price hit not only a 52-week low—$393.11—but its lowest point in years. The last time UnitedHealth’s stock price went below $400 a share was on October 14, 2021.

The company’s shares lost nearly 4.5% of their value during the past week, contributing to a decline that started soon after the company set an all-time high of $630.73 last November. UnitedHealth’s shares have lost more than 33% of their value since then.

Wall Street Sends a Message

Meanwhile, investors have once again embraced UnitedHealth’s top two rivals in the Medicare Advantage business–Humana and CVS/Aetna. Those companies told investors last year, when both were in the Wall Street dog house for spending more than investors expected on patients’ medical care, that they would dump hundreds of thousands of their costliest Medicare Advantage enrollees to improve their profits. They made good on that promise, shedding almost 650,000 seniors and people with disabilities by the end of the year.

Many of those people enrolled in a UnitedHealth Medicare Advantage plan. The company reported 400,000 more Medicare Advantage enrollees in the first quarter of 2025 than in the fourth quarter of 2024. That used to be a good thing, but UnitedHealth’s executives told investors on April 17 that it wouldn’t make as much money for them as the company had assured them just three months earlier because it likely will have to spend more than they expected on those new MA enrollees’ medical care. Investors responded by immediately dispatching the company’s shares to the cellar. Those shares lost about 23% of their value in a single day.

The Street had also punished Humana and CVS last year when they said they were paying more for seniors’ medical care than they’d expected. Shares of both companies cratered, losing around half their value. So, executives at both Humana and CVS started identifying Medicare markets to get out of entirely. The culling was ruthless. CVS shed 227,000 MA enrollees. Humana got rid of 419,000.

Locked Out of Traditional Medicare

Those seniors and disabled people had to scramble to find a new Medicare Advantage insurer because it is difficult for most people to go back to traditional Medicare and find an affordable Medicare supplement policy. Medicare supplement insurers must waive underwriting during the first six months of applicants’ eligibility for Medicare, but people who enroll in a Medicare Advantage plan and want or need to make a change months later find out that insurers will charge them more unless their health is nearly perfect.

Of the seven big for-profit health insurers, four (Cigna, CVS/Aetna, Humana and Centene) collectively cut 1.3 million of their Medicare Advantage enrollees adrift at the end of 2024 in an effort to stay in Wall Street’s good graces. Cigna dumped all 600,000 of its MA enrollees, selling them to the Blue Cross corporation HCSC. For-profit Blue Cross insurer Elevance picked up 227,000; Molina added 18,000, and, as noted, UnitedHealth signed up 400,000 new MA enrollees.

While UnitedHealth’s shares have lost a third of their value, CVS’s shares have increased more than 50% since the first of this year. They even set a 52-week high of $72.51 on Thursday. Humana’s shares closed Friday at $258.48, up 1.88% since January 1. They are out of the Wall Street dog house – for now, anyway.

Profits, Lobbying Soar

I trust you are not feeling sorry for UnitedHealth because of its misfortune on Wall Street. It is still a hugely profitable company–just not profitable enough lately to please investors. This huge corporation, the fourth largest in America, reported $9.1 billion in profits in just the first quarter of this year. If the company makes it more difficult for its health plan enrollees to get the care they need this year, it could make even more than the $34.4 billion in profits it made last year.

And as a group, the seven big for-profits, including those that spent more than Wall Street felt was necessary on patients’ medical care, made $70 billion in profits last year. (UnitedHealth made nearly as much as the other six combined.)

And collectively, those giant corporations took in a record $1.5 trillion in revenue from us as customers and taxpayers last year. They are doing quite well. But that won’t stop them from trying to keep lawmakers and Trump administration officials from cracking down this year on the widespread waste, fraud and abuse in the Medicare Advantage program. You can expect them to spend a record amount of our money on lobbying expenses in Washington this year to keep their Medicare Advantage cash cow well fed.