Self-dealing is illegal in banks, real estate, and investment firms, but in health insurance, it’s not only legal, it’s widespread. Large insurers have spent decades consolidating the U.S. health care system, acquiring medical practices, pharmacies, and pharmacy benefit managers, all while sidestepping rules meant to protect patients and taxpayers.

For example, UnitedHealth Group has 2,694 subsidiaries, as documented in the Center for Health and Democracy’s Sunlight Report on UnitedHealth Group. Within this conglomerate, there are 589 clinician practice locations across 32 states acquired between 2007 and 2023. UnitedHealth Group also has 24 subsidiary pharmacy benefit managers and over 30 subsidiary pharmacies. Data and insider accounts suggest that UnitedHealth Group and other vertically integrated insurers engage in self-dealing to increase profits. The ways these subsidiaries interact closely resembles self-dealing practices that are prohibited by law in other industries, such as banking, real estate, and investment firms.

As Dr. Seth Glickman and I have explained in earlier pieces, when a health insurer owns or controls medical practices, pharmacy benefit managers, or pharmacies, it can circumvent medical loss ratio (MLR) regulations. MLR rules require insurance companies to spend 80–85% of premium dollars on medical costs, leaving the remainder for administrative fees and profits. Unitedhealth Group, for instance, reportedly pays its own subsidiary providers above-market rates for medical services. These payments count as “medical costs” under MLR rules, yet the subsidiaries retain the excess as profit. Similarly, when a patient uses Optum Rx, a UnitedHealth Group subsidiary, or a subsidiary pharmacy, the fees added by the PBM are counted as medical costs, even though they are retained as profit by the parent company.

In banking, such actions are expressly prohibited. Consider a bank CEO who owns a real estate development company and seeks a loan for a risky project. If the bank lends to the CEO’s company at a below-market interest rate, the loan violates federal law and could trigger millions in fines as well as civil and criminal charges for both the CEO and the bank. This scenario parallels UnitedHealth Group’s current operations. In both cases, customer money (depositor funds in a bank; premium dollars in insurance) is used to funnel profit to insiders or affiliates, bypassing the market discipline that governs arm’s-length transactions.

Real estate law similarly prohibits self-dealing. Imagine a real estate agent hired to sell a client’s home who secretly buys the property through an affiliate at a lower price than the market reflects. By underrepresenting the home’s value, the agent enriches themselves at the client’s expense. This violates state real estate laws and common law fiduciary duties. The parallel in Insurance is clear: insurers pay inflated prices to their owned practices, driving up care costs and premiums. In both cases, the fiduciary is using client assets (property or premium dollars) to generate hidden profits for themselves or their affiliates, avoiding fair-market competition.

Investment advisers are also prohibited from similar practices. If you hire a broker to get the best price for a stock trade, the broker cannot quietly route the trade to an affiliate at a worse price so the affiliate profits. Even small losses per trade scale into substantial gains for the broker’s affiliate, all at the client’s expense. These actions violate the Investment Advisers Act of 1940, the Securities Exchange Act of 1934, and SEC rules when proper disclosure or consent is not obtained. Similarly, insurers use premium dollars to channel profits to subsidiaries instead of relying on competitive market pricing.

The stark parallels between self-dealing in banks, real estate, and investment brokerages, which Congress regulated decades ago, and health insurance are damning. Health insurance conglomerates have built empires on paying themselves to the detriment of patients and taxpayers. Congress must act to regulate this type of self-dealing in insurance as it does in other industries.

Moreover, the depth of insurer control over the patient care system necessitates regulations to prevent vertical monopolies, where insurers dominate every stage of care delivery.

Ahead of my Congressional testimony last week before the Senate HELP committee, I compiled data on the profits, revenues and CEO compensations of big health insurers in 2024. The curiosity from senators on both sides of the aisle signaled, to me, that lawmakers are as interested as I’ve ever seen in the industry’s rampant profiteering.

What I found was that the seven biggest publicly traded health insurance companies collectively made $71.3 billion in profits, up more than half a billion dollars from 2023. All while millions of Americans continued to skip their medications, rationed insulin and delayed care due to insurers’ out-of-pocket demands.

Let’s break it down.

You won’t be surprised to learn that shareholders are not the only ones benefiting from the care-restricting barriers insurers have erected to boost profits. The CEOs of those seven companies took home a combined $146.1 million in 2024 compensation. That’s enough to cover annual premiums for thousands of American families.

Here’s what the top brass made:

Meanwhile, patients across the country report increasing out-of-pocket costs, more aggressive prior authorizations and narrower provider networks. But for these executives, the real measure of success is how high they can push their stock prices and not how many people can afford to see a doctor.

So, What’s Driving the Revenue Surge?

One word: Gouging.

Insurers continued to jack up premiums for their commercial customers and overcharge the government. Despite watchdog warnings, Uncle Sam continues to pour money into private Medicare Advantage plans even as audits and investigations uncover widespread fraud and upcoding. And Medicaid managed care is a gold mine, too. These insurers now dominate state Medicaid contracts and can quietly extract billions through behind-the-scenes ownership of pharmacies, PBMs and providers.

It’s not just health insurance anymore — it’s a monopolized empire.

All that said, to the dismay of shareholders, the big seven insurers have had to admit that so far in 2025, they’ve paid more medical claims than they had expected, which means their profits were down somewhat during the first months of the year. I’ll shed more light on that in a future post. No need for you to shed any tears for them, though, because we’re still talking billions and billions in profits.

So if you’re wondering why your premiums, deductibles and costs at the pharmacy counter keep going up — just look at those 2024 numbers. We all paid more for health insurance and got less for the hard-earned money we had to shovel out for our “coverage.”

And expect even more financial pain (and difficulty getting the care you need) as these companies do all they can to get their profit margins back to where Wall Street wants them.

Not long ago, Dr. Richard Menger, a neurosurgeon, was ready to operate on a 16-year-old with complex scoliosis. A team of doctors had spent months preparing for the surgery, consulting orthopedists and cardiologists, even printing a 3D model of the teen’s spine.

The surgery was scheduled for a Friday when Menger got the news: the teen’s insurer, Blue Cross Blue Shield of Alabama, had denied coverage of the surgery.

It wasn’t particularly surprising to Menger, who has been practicing in Alabama since 2019. Alabama essentially has one private insurer, Blue Cross Blue Shield of Alabama, which has a whopping 94% of the market of large-group insurance plans, according to the health policy nonprofit KFF. That dominance allows the insurer to consistently deny claims, many doctors say, charge people more for coverage, and pay lower rates to doctors and hospitals than they would in other states.

“It makes the natural problems for insurance that much more magnified because there’s no market competition or choice,” says Menger, who in 2023 wrote an op-ed in 1819 News, a local news site, arguing that ending Blue Cross Blue Shield of Alabama’s health insurance monopoly would make people in the state healthier.

Blue Cross Blue Shield of Alabama also has the largest share of individual insurance plans in the state, according to data from the Centers for Medicaid & Medicare Services. Perhaps not coincidentally, Alabama also had the highest denial rates for in-network claims by insurers on the individual marketplace in 2023, according to a KFF analysis: 34%. Neighboring Mississippi, where the majority insurer has less of the market share at 81%, has an average denial rate of 15%.

Alabama is an extreme case, but people in many other states face health insurance monopolies, too. One insurer, Premera Blue Cross Group, has a 94% share of the large-group market in Alaska, and Blue Cross Blue Shield of Wyoming has a 91% market share in that state. In 18 states, one insurer has 75% or more of the large-group health insurance marketplace, according to KFF data.

These monopolies drive up costs, says Leemore Dafny, a professor at Harvard Business School and Harvard Kennedy School who has long studied competition among health insurance companies and providers.

“More competitors tend to drive lower premiums and more generous benefits for consumers,” she says. “There’s a lot of concern from analysts like myself about concentration in a range of sectors, including health insurance.”

Bruce A. Scott, the immediate past president of the American Medical Association, has said that when the dominant insurer in his state of Kentucky was renegotiating its contract with his medical group, it offered lower rates than it had paid six years before. “This same type of financial squeeze play is found nationwide, and its frequency has been exacerbated by health insurance industry consolidation,” he wrote in The Hill in 2023.

What happened to competition? There used to be a lot more regional health insurers, Dafny says. But as costs started to rise, they didn’t have enough leverage to negotiate prices down with providers and stay profitable. As a result, many were happy to be acquired by larger companies. Then hospitals and doctor’s offices merged to get more leverage against the bigger insurers. Now, there’s a lot of concentration among both provider groups and insurers.

“None of this had anything to do with taking better care of patients,” she says. “It had to do with trying to get the upper hand.”

In a statement to TIME, Blue Cross Blue Shield of Alabama said that it was working to make the prior authorization process more transparent and reverse the requirement of prior authorization for certain in-network medical services. It will attempt to answer at least 80% of requests for prior authorization in near real-time by 2027, it says. (A coalition of major health insurers recently vowed to fix their prior authorization processes under pressure from the federal government.)

The insurer also says it welcomes competition. “We know Alabamians have a choice when it comes to choosing their health insurance carrier and we don’t take that for granted,” a spokesperson said in the statement. In the commercial and underwritten market—which represents the bulk of its business—Blue Cross Blue Shield Alabama competes with four other companies that sell individual, family, and group plans, the company says, and it competes with 68 companies who sell Medicare plans in Alabama. Its success in the state is partly because it sells policies in every county in Alabama, the insurer says, while others do not.

Other casualties of such a concentrated health-insurance marketplace are rural hospitals and providers. Small rural hospitals are often independent and have not merged with other systems like many of their large urban counterparts, so they have an even harder time negotiating with the one big insurer in the state, says Harold Miller, president and CEO of the Center for Healthcare Quality and Payment Reform, a national policy center that studies health-care costs. That means big insurers will often refuse to cover procedures or pay lower prices for services.

“I’ve had rural hospitals tell me they can’t even get the health plan on the phone,” Miller says.

In the past decade, the Department of Justice has stopped some mergers, but has not been very aggressive at stopping consolidation in the health-care industry, Dafny says. That may be in part because the courts require a high standard of evidence to block a transaction, and the government might have been worried it would have lost whatever cases it brought.

A few factors prevent insurers with a monopoly from driving costs too high, says Benjamin Handel, an economics professor at the University of California, Berkeley who studies health care. One is a regulation called minimum loss ratio that essentially requires insurers to spend a certain share of what they earn from premiums on medical care. Another is that an insurer with a monopoly that angers consumers might attract attention from regulators, he says.

Of course, there’s not a whole lot regulators can do to make a marketplace more competitive. A state could try to incentivize more insurers to enter their states with tax breaks or other sweeteners, but it’s very hard to enter a market and offer low rates right away. The establishment of the health-care marketplaces in the Affordable Care Act allowed new entrants, Dafny says, but many of them did not survive.

Menger, the Alabama doctor, says that he and his colleagues—and therefore their patients—are basically stuck. His staff has to spend 10-15 hours a week negotiating with the insurer to get prior authorizations that sometimes don’t come, even while patients pay higher premiums.

The teenage boy eventually got approved for the scoliosis surgery, but not after the family went through a lot of stress with postponements and uncertainty. “I think it’s pretty clear that the more competition, the better things are,” Menger says. “This prior authorization nonsense is really hurting patients.”

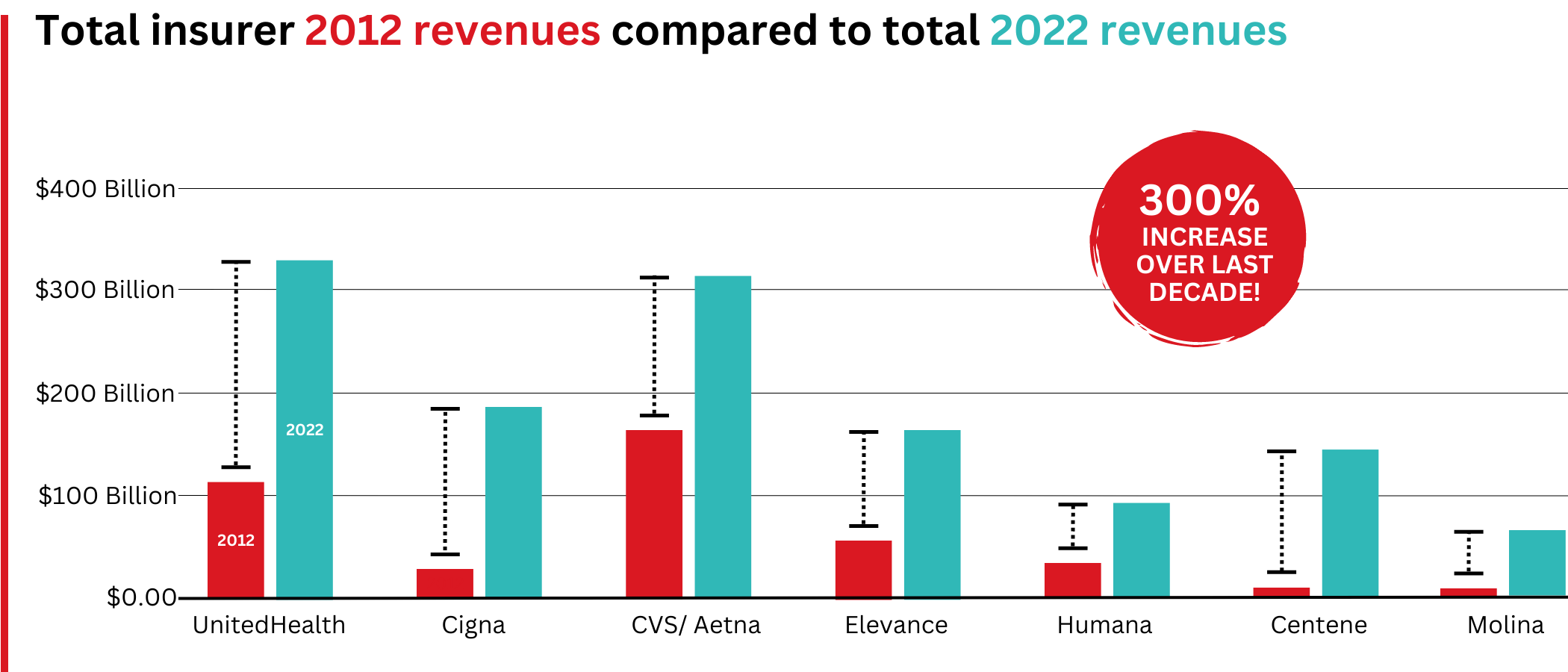

Big Insurance revenues and profits have increased by 300% and 287% respectively since 2012 due to explosive growth in the companies’ pharmacy benefit management (PBM) businesses and the Medicare replacement plans they call Medicare Advantage.

The for-profits now control more than 80% of the national PBM market and more than 70% of the Medicare Advantage market.

In 2022, Big Insurance revenues reached $1.25 trillion and profits soared to $69.3 billion.

That’s a 300% increase in revenue and a 287% increase in profits from 2012, when revenue was $412.9 billion and profits were $24 billion.

Big insurers’ revenues have grown dramatically over the past decade, the result of consolidation in the PBM business and taxpayer-supported Medicare and Medicaid programs.

Sucking billions out of the pharmacy supply chain – and taxpayers’ pockets

What has changed dramatically over the decade is that the big insurers are now getting far more of their revenues from the pharmaceutical supply chain and from taxpayers as they have moved aggressively into government programs. This is especially true of Humana, Centene, and Molina, which now get, respectively, 85%, 88%, and 94% of their health-plan revenues from government programs.

The two biggest drivers are their fast-growing pharmacy benefit managers (PBMs), the relatively new and little-known middleman between patients and pharmaceutical drug manufacturers, and the privately owned and operated Medicare replacement plans they market as Medicare Advantage.

With the exception of Humana, Centene, and Molina, most of the companies that constitute Big Insurance continue to make substantial amounts of money selling policies and services in what they refer to as their commercial businesses – to individuals, families, and employers – but the seven companies’ commercial revenue grew just 260%, or $176 billion, over 10 years (from $110.4 billion to $287.1 billion). While that’s significant, profitable growth in the commercial sector has become a major challenge for big insurers – so much so that Humana just last week announced it is exiting the employer-sponsored health-insurance marketplace entirely.

The percentage of U.S. employers providing some level of health benefits to their workers dropped from 69% to 51% between 1999 and 2022 – including a dramatic 8% decrease last year alone. Growth in this category is largely the result of insurers “stealing market share” from each other or from smaller competitors.

As a consequence of this segment’s relative stagnation, PBMs and government programs have become the new cash cows for Big Insurance.

Spectacular PBM Growth

PBM HIGHLIGHTS

Cigna now gets far more revenue from its PBM than from its health plans. CVS gets more revenue from its PBM than from either Aetna’s health plans or its nearly 10,000 retail stores.

UnitedHealth has the biggest share of both the PBM and Medicare markets and, through numerous acquisitions of physician practices, is now the largest U.S. employer of doctors.

PBMs are middlemen companies that manage prescription drug benefits for health insurers, Medicare Part D drug plans, employers, and, in some cases, unions. As the Commonwealth Fund has noted:

PBMs have a significant behind-the-scenes impact in determining total drug costs for insurers, shaping patients’ access to medications, and determining how much pharmacies are paid.

The Commonwealth Fund went on to say that PBMs have faced growing scrutiny about their role in rising prescription drug costs and spending. A big reason for the scrutiny – by Congress, state lawmakers and now also by the FTC – is that the biggest PBMs are now owned by Big Insurance.

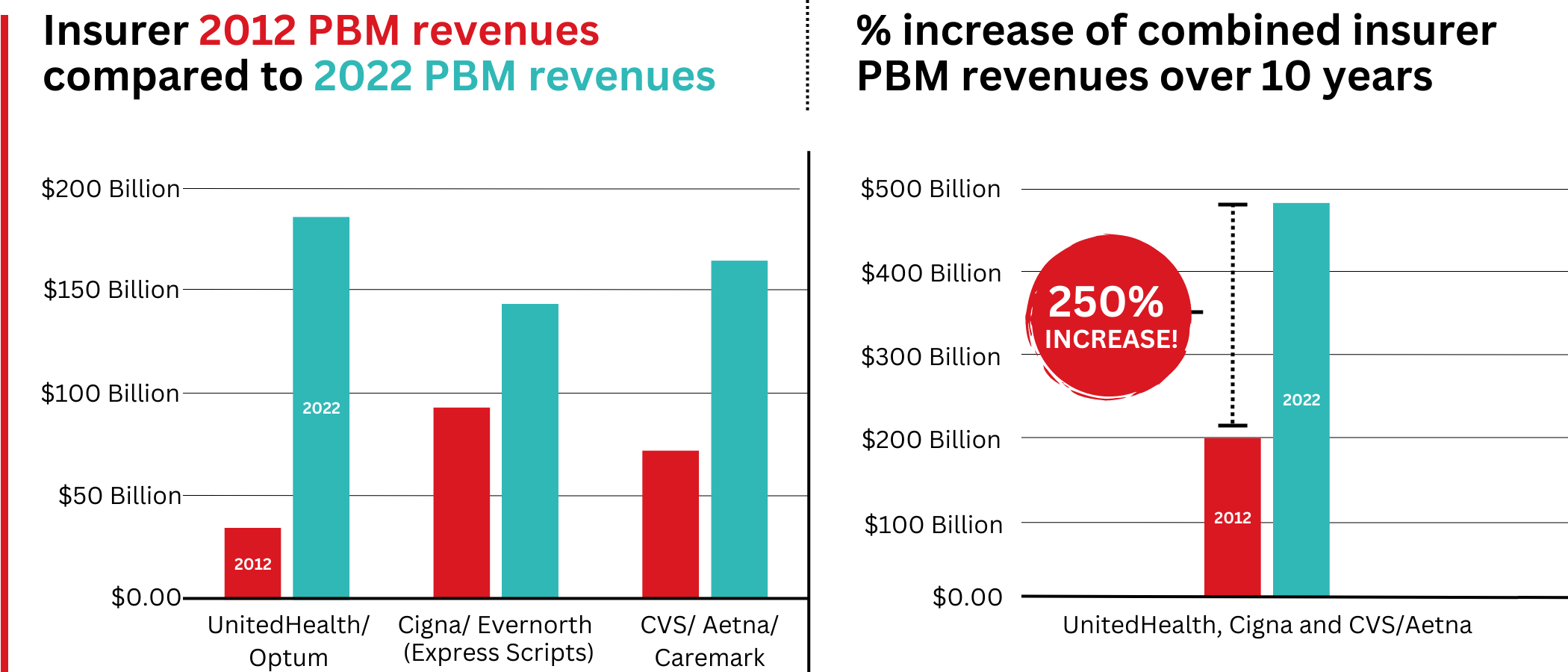

Through mergers and acquisitions in recent years, three of the seven for-profit insurers – Cigna, CVS/Aetna, and UnitedHealth – now control 80% of the U.S. pharmacy benefits market.

They determine which drugs will be listed in each of their formularies (lists of drugs they will “cover” based on secret deals they negotiate with pharmaceutical companies) and how much patients will have to pay out of their own pockets at the pharmacy counter – in many cases hundreds or thousands of dollars – before their coverage kicks in. The PBMs also “steer” health-plan enrollees to their preferred or owned pharmacies (and, increasingly, away from independent pharmacists), thereby capturing even more of what we spend on our prescription medications.

Cigna, CVS/Aetna, and UnitedHealth now control 80% of the U.S. PBM market. Correction: this graph was initially published with inaccurate numbers. The source for this information can be found here.

Ten years ago, PBMs contributed relatively little to the three companies’ revenues and profits. But since then, the rapid growth of PBMs has transformed all of the companies. The combined revenues from their PBM business units increased 250% between 2012 and 2022, from $196.7 billion to $492.4 billion.

Changes in PBM revenues between 2012 and 2022 for UnitedHealth Group, Cigna, and CVS/Aetna (Editor’s note: Cigna acquired PBM Express Scripts in 2018. To reflect revenue growth, Express Scripts’ pre-acquisition 2012 revenues are included in the Cigna total for that year.)

PBM Profit Generation

The PBM profit growth at the three companies over the past decade was even more dramatic than revenue growth. Collectively, their PBM profits increased 438%, from $6.3 billion in 2012 to $27.6 billion in 2022.

As a result of this fast growth, more than half (52%) of three companies’ profits in 2022 came from their PBM business units: Cigna’s Evernorth, CVS/Aetna’s Caremark, and UnitedHealth’s Optum. Cigna now gets far more revenue and profits from its PBM than from its health plans. And CVS gets more revenue from its PBM than from either Aetna’s health plans or its nearly 10,000 retail stores. (The companies’ business units that include their PBMs have also moved aggressively in recent years into health-care delivery through acquisitions of physician practices, clinics, dialysis centers, and other facilities. Notably, UnitedHealth Group is now the largest U.S. employer of physicians.)

Huge strides in privatizing both Medicare and Medicaid

GOVERNMENT PROGRAMS HIGHLIGHTS

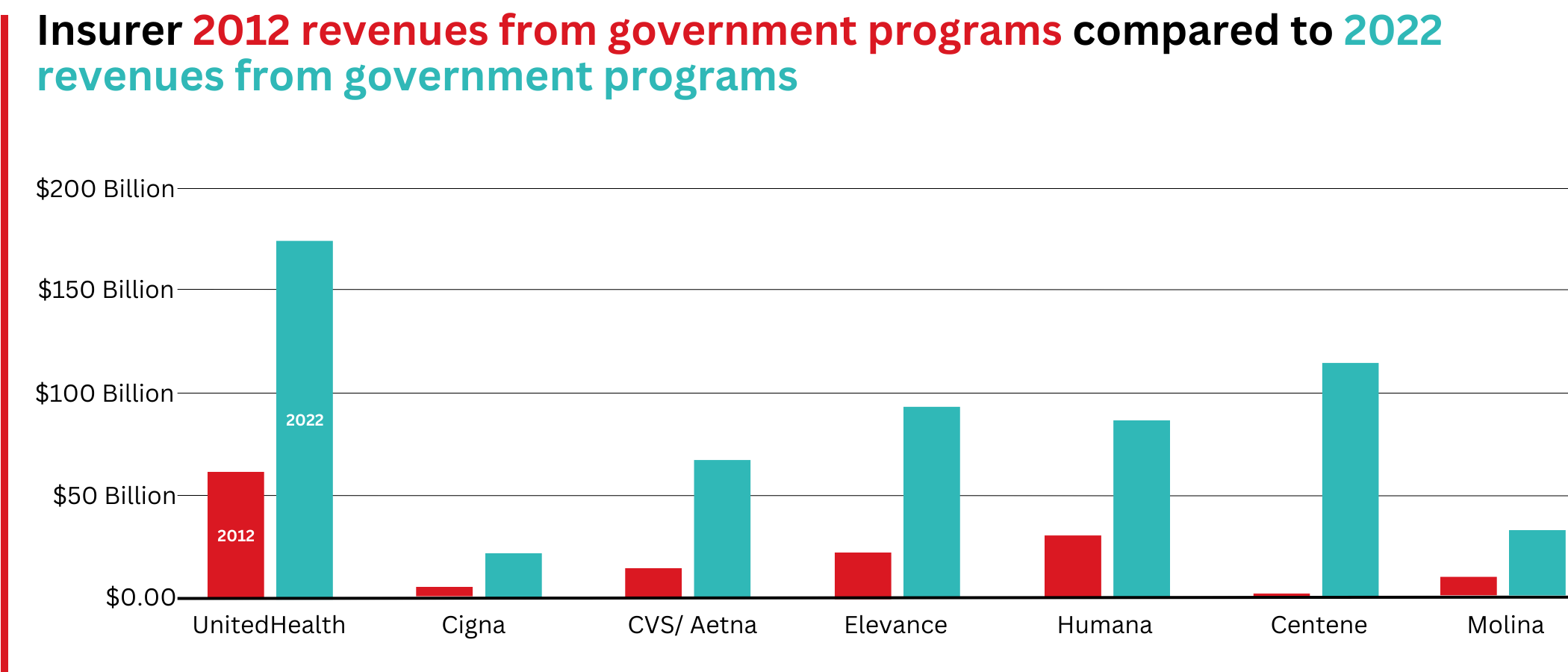

More than 90% of health-plan revenues at three of the companies come from government programs as they continue to privatize both Medicare and Medicaid, through Medicare Advantage in particular.

Enrollment in government-funded programs increased by 261% in 10 years; by contrast commercial enrollment increased by just 10% over the past decade.

Commercial enrollment actually declinedat both UnitedHealth and Humana.

85% of Humana’s health-plan members are in government-funded programs; at Centene, it is 88%, and at Molina, it is 94%.

The big insurers now manage most states’ Medicaid programs – and make billions of dollars for shareholders doing so – but most of the insurers have found that selling their privately operated Medicare replacement plans is even more financially rewarding for their shareholders.

Revenue growth from government programs has been dramatic over the past 10 years. (Note the numbers do not include revenue from the Medicare Part D program, federal subsidy payments for many ACA marketplace plan enrollees, or Medicare supplement policies.)

This is especially apparent when you see that the Big Seven’s combined revenues from taxpayer-supported programs grew 500%, from $116.3 billion in 2012 to $577 billion in 2022.

These numbers should be of interest to the Biden administration and members of Congress, many of whom are calling for much greater scrutiny of the Medicare Advantage program. Numerous media and government reports have shown that the federal government is overpaying private insurers billions of dollars a year, largely because of loopholes in laws and regulations that enable them to get more taxpayer dollars by claiming their enrollees are sicker than they really are. The companies also make aggressive use of prior authorization, largely unknown in traditional Medicare, to avoid paying for doctor-ordered care and medications.

In addition to their focus on Medicare and Medicaid, the companies also profit from the generous subsidies the government pays insurers to reduce the premiums they charge individuals and families who do not qualify for either Medicare or Medicaid or who work for an employer that does not offer subsidized coverage. But many people enrolled in those types of plans – primarily through the health insurance “marketplaces” established by the Affordable Care Act – cannot afford the deductibles and other out-of-pocket requirements they must pay before their insurers will begin paying their medical claims.

Dramatic Enrollment Shifts

Changes in health-plan enrollment over the past decade show how dramatic this shift has been. Between 2012 and 2022, enrollment in the companies’ private commercial plans increased by 10%, from 85.1 million in 2012 to 93.8 million in 2022.

By comparison, growth in enrollment in taxpayer-supported government programs increased 261%, from 27 million in 2012 to 70.4 million in 2022.

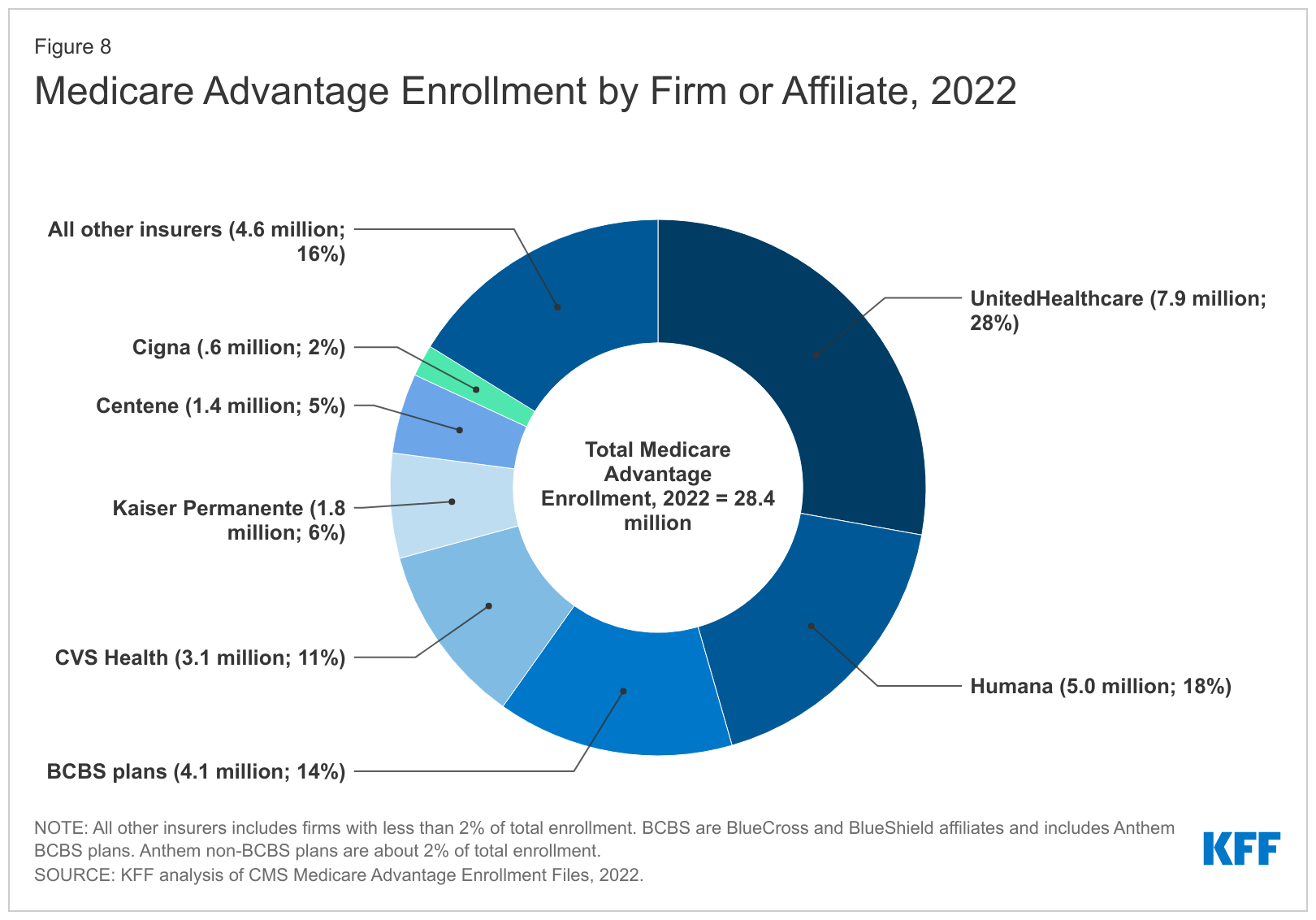

For-profit insurers dominate the Medicare Advantage market. Note that Anthem mentioned above is now known as Elevance. It owns 14 of the country’s Blue Cross Blue Shield plans.

Within that category, Medicare Advantage enrollment among the Big Seven increased 252%, from 7.8 million in 2012 to 19.7 million in 2022.

Nationwide, enrollment in Medicare Advantage plans increased to 28.4 million in 2022 (and to 30 million this year). That means that the Big Seven for-profit companies control more than 70% of the Medicare Advantage market.

UnitedHealth, Humana, Elevance, and CVS/Aetna have captured most of the Medicare Advantage market since the Affordable Care Act was passed in 2010.

The remaining growth in the government segment occurred in the Medicaid programs that a subset of the Big Seven (UnitedHealth, Elevance, Centene, and Molina in particular) manages for several states.

A few other facts and figures to keep in mind as Big Insurance thrives:

100 million of us – almost one of every three people in this country – now have medical debt.

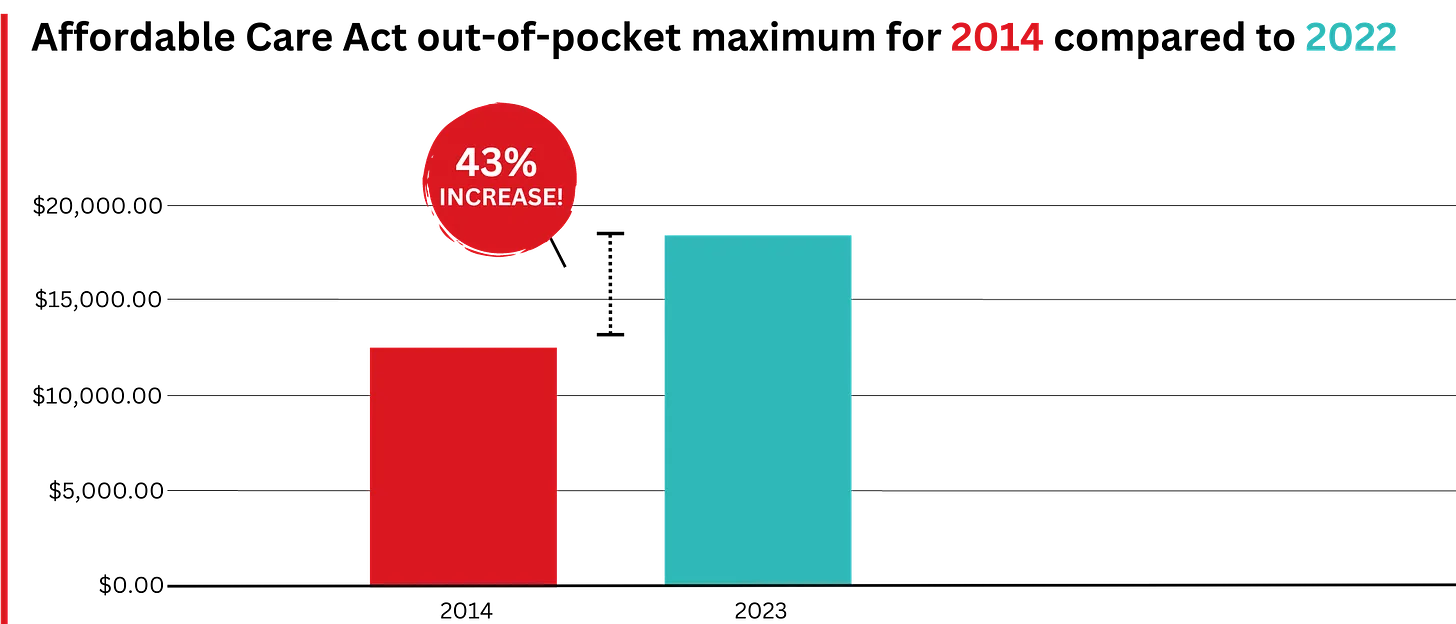

In 2023, U.S. families can be on the hook for up to $18,200 in out-of-pocket requirements before their coverage kicks in, up 43% since 2014 when it was $12,700.The Affordable Care Act allows the out-of-pocket maximum to increase annually – 43% since the maximum limit went into effect in 2014.

44% of people in the United States who purchased coverage through the individual market and (ACA) marketplaces were underinsured or functionally uninsured.

42% said they hadproblems paying medical bills or were paying off medical debt.

Half (49%) said they would be unable to pay an unexpected medical bill within 30 days, including 68% of adults with low income, 69% of Black adults, and 63% of Latino/Hispanic adults.

In 2021, about $650 million, or about one-third of all funds raised by GoFundMe, went to medical campaigns. That’s not surprising when you realize that in the United States, even people with insurance all too often feel they have no choice but to beg for money from strangers to get the care they or a loved one needs.

Even as we spend about $4.5 trillion on health care a year, Americans are now dying younger than people in other wealthy countries. Life expectancy in the United States actually decreased by 2.8 years between 2014 and 2021, erasing all gains since 1996, according to the Centers for Disease Control and Prevention.

BOTTOM LINE:

The companies that comprise Big Insurance are vastly different from what they were just 10 years ago, but policymakers, regulators, employers, and the media have so far shown scant interest in putting their business practices under the microscope.

Changes in federal law, including the Medicare Modernization Act of 2003, which created the lucrative Medicare Advantage market, and the Affordable Care Act of 2010, which gave insurers the green light to increase out-of-pocket requirements annually and restrict access to care in other ways, opened the Treasury and Medicare Trust Fund to Big Insurance. In addition, regulators have allowed almost all of their proposed acquisitions to go forward, which has created the behemoths they are today.

CVS/Health is now the 4th largest company on the Fortune 500 list of American companies. UnitedHealth Group is now No. 5 – and all the others are climbing toward the top 10.

Tomorrow night, the Presidential candidates square off in Philadelphia. Per polling from last week by the New York Times-Siena, NBC News-Wall Street Journal, Ipsos-ABC News and CBS News, the two head into the debate neck and neck in what is being called the “chaos election.”

Polls also show the economy, abortion and immigration are the issues of most concern to voters. And large majorities express dissatisfaction with the direction the country is heading and concern about their household finances.

The healthcare system per se is not a major concern to voters this year, but its affordability is. Out-of-pocket costs for prescription drugs, insurance premiums and co-pays and deductibles for hospitals and physician services are considered unreasonable and inexplicably high. They contribute to public anxiety about their financial security alongside housing and food costs. And majorities think the government should do more by imposing price controls and limiting corporate consolidation.

That’s where we are heading into this debate. And here’s what we know for sure about the 90-minute production as it relates to health issues and policies:

Each candidate will rail against healthcare prices, costs, and consolidation taking special aim at price gouging by drug companies and corporate monopolies that limit competition for consumers.

Each will promise protections for abortion services: Trump will defer to states to arbitrate those rights while Harris will assert federal protection is necessary.

Each will opine to the Affordable Care Act’s future: Trump will promise its repeal replacing it “with something better” and Harris will promise its protection and expansion.

Each will promise increased access to behavioral health services as memories of last week’s 26-minute shooting tirade at Apalachee High School fade and the circumstances of Colt Gray’s mental collapse are studied.

And each will promise adequate funding for their health priorities based on the effectiveness of their proposed economic plans for which specifics are unavailable.

That’s it in all likelihood. They’re unlikely to wade into root causes of declining life expectancy in the U.S. or the complicated supply-chain and workforce dynamics of the industry. And the moderators are unlikely to ask probative questions like these to discover the candidate’s forethought on matters of significant long-term gravity…

What are the most important features of health systems in the world that deliver better results at lower costs to their citizens that could be effectively implemented in the U.S. system?

How should the U.S. allocate its spending to improve the overall health and well-being of the entire population?

How should the system be funded?

My take:

I will be watching along with an audience likely to exceed 60 million. Invariably, I will be frustrated by well-rehearsed “gotcha” lines used by each candidate to spark reaction from the other. And I will hope for more attention to healthcare and likely be disappointed.

Misinformation, disinformation and AI derived social media messaging are standard fare in winner-take-all politics.

When used in addressing health issues and policies, they’re effective because the public’s basic level of understanding of the health system is embarrassingly low: studies show 4 in 5 American’s confess to confusion citing the system’s complexity and, regrettably, the inadequacy of efforts to mitigate their ignorance is widely acknowledged.

Thus, terms like affordability, value, quality, not-for-profit healthcare and many others can be used liberally by politicians, trade groups and journalists without fear of challenge since they’re defined differently by every user.

Given the significance of healthcare to the economy (17.6% of the GDP),

the total workforce (18.6 million of the 164 million) and individual consumers and households (41% have outstanding medical debt and all fear financial ruin from surprise medical bills or an expensive health issue), it’s incumbent that health policy for the long-term sustainability of the health system be developed before the system collapses. The impetus for that effort must come from trade groups and policymakers willing to invest in meaningful deliberation.

The dust from this election cycle will settle for healthcare later this year and in early 2025. States are certain to play a bigger role in policymaking: the likely partisan impasse in Congress coupled with uncertainty about federal agency authority due to SCOTUS; Chevron ruling will disable major policy changes and leave much in limbo for the near-term.

Long-term, the system will proceed incrementally. Bigger players will fare OK and others will fail. I remain hopeful thoughtful leaders will address the near and long-term future with equal energy and attention.

Regrettably, the tyranny of the urgent owns the U.S. health system’s attention these days: its long-term destination is out-of-sight, out-of-mind to most. And the complexity of its short-term issues lend to magnification of misinformation, disinformation and public ignorance.

That’s why this debate will frustrate healthcare voters.

PS: Congress returns this week to tackle the October 1 deadline for passing 12 FY2025 appropriations bills thus avoiding a shutdown. It’s election season, so a continuing resolution to fund the government into 2025 will pass at the last minute so politicians can play partisan brinksmanship and enjoy media coverage through September. In the same period, the Fed will announce its much anticipated interest rate cut decision on the heals of growing fear of an economic slowdown. It’s a serious time for healthcare!

Regular readers of HEALTH CARE un-covered know that I write frequently about the huge amounts of money the health insurance industry’s pharmacy benefit managers (PBMs) extract from the prescription drug supply chain. I also submitted a comment letter to the Federal Trade Commission two and a half years ago urging it to launch an investigation into PBM business practices that have contributed to the closure of hundreds of independent pharmacies across the country and to millions of Americans walking away from the pharmacy counter without their medications.

On a bipartisan basis, the FTC did launch an inquiry into the PBM business, and today the Commission issued a damning interim report that confirmed what industry critics, including me, have been saying:

Just six companies now control 95% of the pharmacy benefit market, and these Big Insurance-owned middlemen “profit at the expense of patients by inflating drug costs and squeezing Main Street pharmacies.” Below you’ll find the commission’s statement on its preliminary findings.

Last year, we also published a profile of one of the industry’s most vocal critics in Congress, Rep. Earl L. “Buddy” Carter (R-Ga.), a pharmacist by trade who has seen PBM’s profiteering firsthand. In a press release this morning, Carter said:

Since day one in Congress, I’ve been calling on the FTC to investigate PBMs, which use deceptive and anti-competitive practices to line their own pockets while reducing patients’ access to affordable, quality health care. I’m proud that the FTC launched a bipartisan investigation into these shadowy middlemen, and its preliminary findings prove yet again that it’s time to bust up the PBM monopoly. We are losing more than one pharmacy per day in this country, causing pharmacy deserts and taking the most accessible health care professionals in America out of people’s communities. I am calling on the FTC to promptly complete its investigation and begin enforcement actions if – and when – it uncovers illegal and anti-competitive PBM practices.

Carter and several other members of Congress have introduced bipartisan bills to rein in PBMs. The House has passed PBM reform legislation but the Senate has not yet done so, but there is growing support in both chambers to enact one or more bills by the end of the year. The FTC’s interim report should make that more likely to happen.

Read the FTC’s full press release below:

FTC Releases Interim Staff Report on Prescription Drug Middlemen

Report details how prescription drug middleman profit at the expense of patients by inflating drug costs and squeezing Main Street pharmacies

The Federal Trade Commission today published an interim report on the prescription drug middleman industry that underscores the impact pharmacy benefit managers (PBMs) have on the accessibility and affordability of prescription drugs.

The interim staff report, which is part of an ongoing inquiry launched in 2022 by the FTC, details how increasing vertical integration and concentration has enabled the six largest PBMs to manage nearly 95 percent of all prescriptions filled in the United States.

This vertically integrated and concentrated market structure has allowed PBMs to profit at the expense of patients and independent pharmacists, the report details.

“The FTC’s interim report lays out how dominant pharmacy benefit managers can hike the cost of drugs—including overcharging patients for cancer drugs,” said FTC Chair Lina M. Khan. “The report also details how PBMs can squeeze independent pharmacies that many Americans—especially those in rural communities—depend on for essential care. The FTC will continue to use all our tools and authorities to scrutinize dominant players across healthcare markets and ensure that Americans can access affordable healthcare.”

The report finds that PBMs wield enormous power over patients’ ability to access and afford their prescription drugs, allowing PBMs to significantly influence what drugs are available and at what price. This can have dire consequences, with nearly 30 percent of Americans surveyed reporting rationing or even skipping doses of their prescribed medicines due to high costs, the report states.

The interim report also finds that PBMs hold substantial influence over independent pharmacies by imposing unfair, arbitrary, and harmful contractual terms that can impact independent pharmacies’ ability to stay in business and serve their communities.

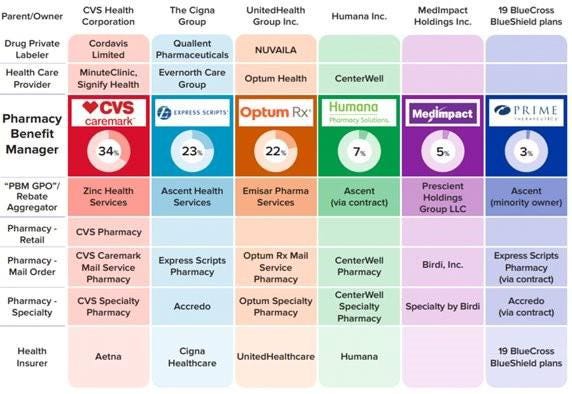

The Commission’s interim report stems from special orders the FTC issued in 2022, under Section 6(b) of the FTC Act, to the six largest PBMs—Caremark Rx, LLC; Express Scripts, Inc.; OptumRx, Inc.; Humana Pharmacy Solutions, Inc.; Prime Therapeutics LLC; and MedImpact Healthcare Systems, Inc. In 2023, the FTC issued additional orders to Zinc Health Services, LLC, Ascent Health Services, LLC, and Emisar Pharma Services LLC, which are each rebate aggregating entities, also known as “group purchasing organizations,” that negotiate drug rebates on behalf of PBMs.

PBMs are part of complex vertically integrated health care conglomerates, and the PBM industry is highly concentrated. As shown in the below image, this concentration and integration gives them significant power over the pharmaceutical supply chain. The percentages reflect the amount of prescriptions filled in the United States.

The interim report highlights several key insights gathered from documents and data obtained from the FTC’s orders, as well as from publicly available information:

Concentration and vertical integration: The market for pharmacy benefit management services has become highly concentrated, and the largest PBMs are now also vertically integrated with the nation’s largest health insurers and specialty and retail pharmacies.

The top three PBMs processed nearly 80 percent of the approximately 6.6 billion prescriptions dispensed by U.S. pharmacies in 2023, while the top six PBMs processed more than 90 percent.

Pharmacies affiliated with the three largest PBMs now account for nearly 70 percent of all specialty drug revenue.

Significant power and influence: As a result of this high degree of consolidation and vertical integration, the leading PBMs now exercise significant power over Americans’ ability to access and afford their prescription drugs.

The largest PBMs often exercise significant control over what drugs are available and at what price, and which pharmacies patients can use to access their prescribed medications.

PBMs oversee these critical decisions about access to and affordability of life-saving medications, without transparency or accountability to the public.

Self-preferencing: Vertically integrated PBMs appear to have the ability and incentive to prefer their own affiliated businesses, creating conflicts of interest that can disadvantage unaffiliated pharmacies and increase prescription drug costs.

PBMs may be steering patients to their affiliated pharmacies and away from smaller, independent pharmacies.

These practices have allowed pharmacies affiliated with the three largest PBMs to retain high levels of dispensing revenue in excess of their estimated drug acquisition costs, including nearly $1.6 billion in excess revenue on just two cancer drugs in under three years.

Unfair contract terms: Evidence suggests that increased concentration gives the leading PBMs leverage to enter contractual relationships that disadvantage smaller, unaffiliated pharmacies.

The rates in PBM contracts with independent pharmacies often do not clearly reflect the ultimate total payment amounts, making it difficult or impossible for pharmacists to ascertain how much they will be compensated.

Efforts to limit access to low-cost competitors: PBMs and brand drug manufacturers negotiate prescription drug rebates some of which are expressly conditioned on limiting access to potentially lower-cost generic and biosimilar competitors.

Evidence suggests that PBMs and brand pharmaceutical manufacturers sometimes enter agreements to exclude lower-cost competitor drugs from the PBM’s formulary in exchange for increased rebates from manufacturers.

The report notes that several of the PBMs that were issued orders have not been forthcoming and timely in their responses, and they still have not completed their required submissions, which has hindered the Commission’s ability to perform its statutory mission. FTC staff have demanded that the companies finalize their productions required by the 6(b) orders promptly. If, however, any of the companies fail to fully comply with the 6(b) orders or engage in further delay tactics, the FTC can take them to district court to compel compliance.

The FTC remains committed to providing timely updates as the Commission receives and reviews additional information.

The Commission voted 4-1 to allow staff to issue the interim report, with Commissioner Melissa Holyoak voting no. Chair Lina M. Khan issued a statement joined by Commissioners Rebecca Kelly Slaughter and Alvaro Bedoya. Commissioners Andrew N. Ferguson and Melissa Holyoak each issued separate statements. The Federal Trade Commission develops policy initiatives on issues that affect competition, consumers, and the U.S. economy. The FTC will never demand money, make threats, tell you to transfer money, or promise you a prize. Follow the FTC on social media, read consumer alerts and the business blog, and sign up to get the latest FTC news and alerts.

With both Republicans and Democrats taking on these Goliaths individually, this could be a watershed moment for bi-partisan action.

The push and pull between providers and insurance companies is as old as our health payment system. Doctors have long argued insurers pay too little and that they too often interfere in patient care.

Dramatic increases in prior authorization, aggressive payment negotiations and less-generous reimbursement to doctors by Medicare Advantage plans show there’s little question the balance of power in this equation has swung toward payers.

These practices have led some doctors to look for outside investment, namely private equity, to keep their cash flow healthy and their operations functional. The trend of private equity acquisitions of physician practices is worthy of the federal scrutiny it has attracted. Insurers have noticed this trend, too, and appear ready to propose a profitable partnership.

Bloomberg recentlyreported that CVS/Aetna is looking for a private equity partner to invest in Oak Street Health, the primary care business CVS acquired for $9.5 billion last year. Oak Street is a significant player in primary care delivery, particularly for Americans on Medicare, with more than 100 clinics nationwide. CVS is said to be exploring a joint venture with a private equity firm to significantly expand Oak Street’s footprint and therefore also expand the parent corporation’s direct control over care for millions of seniors and disabled Americans across hundreds of communities.

Republicans have led scrutiny of pharmacy benefit managers on Capitol Hill. And Democratic attacks on private equity in health care have recently intensified. I hope, then, that both parties would find common ground in being watchful of a joint venture between private equity and one of the country’s largest PBMs, Caremark, also owned by CVS/Aetna.

The combination of health insurers and PBMs over the last decade – United Healthcare and Optum; CVS/Aetna and Caremark, and Cigna and Express Scripts – has increasingly handed a few large corporations the ability to approve or deny claims, set payment rates for care, choose what prescriptions to dispense, what prescriptions should cost, and how much patients must pay out-of-pocket for their medications before their coverage kicks in.

As enrollment in Medicare Advantage plans has grown to include a majority of the nation’s elderly and disabled people, we have seen insurers source record profits off the backs of the taxpayer-funded program. But in recent months, insurers have told investors they have had higher than expected Medicare Advantage claims – in particular CVS/Aetna, which took a hammering on Wall Street recently because its Medicare Advantage enrollees were using more health care services than company executives had expected.

It is natural, then, that one of the largest insurer-owned PBMs is looking to expand its hold on primary care for older Americans. Primary care is often the gateway to our health care system, driving referrals to specialists and procedures that lead to the largest claims insurers and their employer customers have to pay. By employing a growing number of primary care providers, CVS/Aetna can increasingly influence referrals to specialists and therefore the care or pharmacy benefit costs those patients may incur.

Control of primary care doctors holds another benefit for insurers: determination of what primary care doctor a patient sees.

People enrolled in an Aetna Medicare Advantage or employer-sponsored plan may find that care is easier to access at Oak Street clinics. Unfortunately, while that feels monopolistic and ethically alarming, this vertical integration has received relatively little scrutiny by lawmakers and regulators.

No law prevents an insurance company or PBM from kicking doctors it does not own out of network while creating preferential treatment for doctors directly employed by or closely affiliated with the corporate mothership.

In fact, the system largely incentivizes this. And shareholders expect insurers to keep up with their peers. As UnitedHealth Group has become increasingly aggressive in its acquisitions of physician practices – now employing or affiliated with about one in ten of the nation’s doctors – it has also become increasingly aggressive in its contract negotiations with physicians it does not control, particularly the specialists who depend on the referrals that come from primary care physicians.

That’s another area where looking to expand Oak Street Health makes smart business sense for CVS/Aetna. Specialist physicians are historically accustomed to higher compensation than primary care doctors and are used to striking hard-fought deals with insurers to stay in-network.

By controlling the flow of primary care referrals to specialists, CVS/Aetna can control what insurers have long-desired greater influence over: patient utilization. As a key driver of referrals to specialists in a specific market, CVS/Aetna will have even more power in contract negotiations with specialists.

As Oak Street’s clinics grow market share in the communities they serve, specialists in that market will feel even more pressured to stay in-network with Aetna and to refer prescriptions to CVS pharmacies. That has the dual benefit for CVS/Aetna of helping to predict what patients will be treated for once they go to a specialist and control over what the insurer will have to pay that specialist.

With different corporate owners, this sort of model could easily run afoul of the federal Anti-Kickback Statute and Stark Law.

No doctor or physician practice is allowed to receive anything of value for the referral of a patient. But that law only applies when there is separate ownership between the referring doctor and the specialist.

CVS/Aetna would clearly be securing value – in the form of lower patient utilization and effective reimbursement rates – under this model. But with Oak Street owned by CVS/Aetna and specialists forced to agree to lower reimbursement rates through negotiations with an insurer that appears separate from Oak Street, there’s no basis for a claim under the Stark Law. There may be antitrust implications, but those are more difficult and take longer to prove – and the fact the federal government cleared CVS/Aetna to acquire Oak Street Health last year wouldn’t help that argument.

This model is already of concern, which is why I continue to urge examination of increasing insurer control of physicians across the country. Their embrace of private equity to accelerate this model is truly alarming. And given Democrats’ recent focus on private equity in health care, they should work with their Republican colleagues who are rightly alarmed about the increasingly anti-competitive, monopolistic health insurance industry.

Abuses by payers are myriad, but these five areas could bear the most fruit for federal antitrust investigators.

Earlier this month, the U.S. Department of Justice announced it has haunched an investigation into “issues regarding payer-provider consolidation” along with other problems associated with mergers and acquisitions in health care. This is significant. For years Washington has trained its oversight authority on pharmaceutical manufacturers, private equity investments in health care and, more recently, pharmacy benefits managers controlled by big insurers. This has held bad actors like Martin Skhreli and Steward Healthcare accountable. But, it has also let insurers grow ever larger, under the radar.

No longer.

This task force will specifically evaluate the following, as an example: “A health insurance company buys several medical practices that compete with each other. It also prohibits its medical practices from contracting with rival health insurance companies.” The government will also dig into “anticompetitive uses of health care data,” “preventing transparency,” “price fixing,” and other areas that could drag nefarious activities of insurers into the spotlight.

I applaud the Department of Justice’s continued focus on these issues, building on the Department’s action announced in February to begin an antitrust investigation into UnitedHealth Group. (If you haven’t read the piece we published in February on UnitedHealth’s self-dealing that helped lead DOJ to open that antitrust inquiry, you can do so here.) The following are a few areas of low-hanging fruit that I hope the task force will focus on as they consider the impact insurers’ ongoing vertical integration has had on the overall health care system.

1. Insurers purchasing physician practices

Once a low-profile issue, Congress and the Biden administration alike have increasingly turned their focus to insurance companies – often referred to as payers – that now own and operate physician practices and clinics – those being paid. Even for someone without a law degree, it is easy to see the conflict this creates, particularly at scale.

There is the oft-cited statistic that UnitedHealth has said that through its Optum division, the company employs or otherwise controls about 10 percent of doctors in the U.S. – around 130,000 physicians and other practitioners in 16 states. This prompted me to take a closer look at publicly available information on the number of doctors employed by other insurers to get a better handle on how much control of physician practices payers now have.

It is difficult to put a percentage on physicians employed by each insurer, but it is clear that the others are following UnitedHealth’s lead. CVS/Aetna purchased Signify Health in 2023, adding 10,000 clinicians to its portfolio. The company says it supports “more than 40,000 physicians, pharmacists, nurses and nurse practitioners.”

Clearly taking a page out of UnitedHealth’s playbook, Elevance (formerly Anthem), which owns Blue Cross Blue Shield plans in 14 states announced last month a “strategic partnership” with 900 providers across several states. Elevance did not disclose the terms of the deal except to say it, “will primarily be through a combination of cash and our equity interest in certain care delivery and enablement assets of Carelon Health.”

As insurers have acquired physician practices, they also have created a rinse-and-repeat strategy associated with kicking physicians they don’t own out of network, and in some cases targeting those same practices for acquisition. Aetna and Humana recently told investors they will be reviewing their networks of physicians, signaling they’ll soon be further narrowing their networks. A good question for this task force: when insurers review those contracts with doctors, do they ever kick the doctors they employ out of network? (Doubtful.) This could specifically draw attention from the task force’s focus on “health care contract language and other practices that restrict competition,” such as contract provisions that require or encourage patients to seek care from doctors directly employed or closely controlled by patients’ insurers.

Additionally, UnitedHealth CEO Andrew Witty recently told analysts, “As I think you see some of the funding changes play out across the — across the next few years, I suspect that may also create new opportunities for us as different companies assess their positions.” My translation:UnitedHealth’s burdensome business practices and the way it shortchanges doctors (those “funding changes” he referenced) contribute to the financial distress that is forcing many health care providers to “assess their positions.”

As the task force continues to consider the impact of private equity in health care monopolies, transactions like this one should receive equal consideration for their lack of transparency and overall impact on market consolidation.

2. Co-mingling of middlemen

I have watched with interest for over the past year as both Democrats and Republicans in Washington increasingly trained their fire on pharmacy benefit managers. The natural next area of focus in that space, which this new task force could advance, should be around how the

three PBMs that control 80 percent of market share are all combined with health insurance companies – namely CVS/Aetna (Caremark), UnitedHealth (Optum Rx), and Cigna (Express Scripts).

An important, and politically popular, area where this consolidation has played out is in the squeeze placed on small, independent pharmacists across the country. More than 300 community pharmacies have closed in the past year alone, out of an inability to operate or push back on unfair margins pushed by these PBM-insurer monopolies. As we have written here, the fees these PBMs charge have increased more than 100,000 percent over the past decade, and are quietly contributing significantly to the profits of the largest health insurers.

We still have little insight into how these business lines interact with each other, and the ultimate impact that has on patients. Given the enormous influence just three insurance companies have over what prescriptions Americans can receive, and how much should be paid for each prescription, the task force would do well to focus on what insurers and PBMs are doing behind the scenes to maximize profits and limit patient access to prescription drugs. It’s already gaining traction on Capitol Hill, with one Congressman recently saying, “I’ll continue to bust this up … this vertical integration in health care.”

3. Prior authorization requests

CVS/Aetna shares were hammered after the company reported a significant increase in payment of Medicare Advantage claims during the first three month is of this year. Expect all insurers to notice. And as they have seen their forecasts fall short of Wall Street’s expectations – particularly because of increasing scrutiny in Washington of Medicare Advantage – these corporations will look to increase their already aggressive use of prior authorization to limit claims payments.

It is not as though insurers make seeking the care you need easy. Far from it. Prior authorization has become “medical injustice disguised as paperwork,” as the New York Times said in a recent, excellent video detailing the widespread nature of this profiteering practice.

While not a stated direct focus of this task force, the increased impact of prior authorization in care delivery is a direct outgrowth of a few large health insurers effectively controlling the marketplace. As insurers directly employ more doctors and enroll more Americans in their plans, they can use prior authorization to increasingly determine whether a patient can get care, period.

Scrutiny in this space could add momentum to increasing activity in state legislatures and Washington to rein in excessive prior authorization. As of early March, nine states and the District of Columbia had passed bills to limit how far insurers could go with prior authorization. And earlier this year, the Centers for Medicare and Medicaid released a final rule that is expected to save physicians $15 billion over the next decade by putting limits on insurer prior authorization tactics.

4. Rising out-of-pocket costs

Regular readers of this newsletter know one of my crusades is to ensure folks who pay good money for health insurance – out of their paychecks or through their tax dollars – can use it when they need it. It was a big win earlier this year for the Lower Out of Pockets Now coalition (which I lead) when President Biden called for a cap on prescription drug out-of-pocket costs of $2,000 annually for everybody, not just Medicare beneficiaries.

If there was true competition and real consumer choice in health insurance, payers wouldn’t be able to get away with increasingly shifting patients into high-deductible plans. But the fact that a few big players control the health insurance market has allowed the oligopoly of payers to do just that, with ever-rising deductibles alongside ever-rising premiums.

The task force’s focus on price fixing, collusion, and transparency in health care costs will, I hope, include some focus on how insurers use their size and clout to drive up out-of-pocket costs and premiums simultaneously – with little recourse to employers or their employees.

5. Implementing crystal clear laws and rules in health care

You know you’re a monopoly or close to it when you can pretty much do whatever you want and get away with it. Look no further than America’s health insurance companies and implementation of the No Surprises Act.

As I wrote earlier this year, Congress and CMS have been clear about how out-of-network hospital bills should be negotiated between insurers and physicians. Yet in case after case, including many that have become the basis of lawsuits, insurers are clearly flouting the Act passed by Congress and the rules promulgated by CMS. Payers are doing this, doctors have said, simply because of their size and ability to weather criticism from physicians, regulators, and the courts – while doctors struggle to pay their bills with significant payments still owed pending out-of-network negotiations with insurers.

One would hope, at a minimum, this task force, focused on rooting out the ills of monopolies, would document how insurers are well aware of how they are supposed to implement legislation like the No Surprises Act, but flout it anyway.

Regulators sued the PE firm last year for consolidating anesthesiology services in Texas with its portfolio company, U.S. Anesthesia Partners. Now, a judge is holding Welsh Carson blameless.

A Texas federal judge has dismissed the Federal Trade Commission’s antitrust lawsuit against Welsh, Carson, Anderson and Stowe in a big win for the private equity firm. However, the government’s suit against Welsh Carson’s portfolio company U.S. Anesthesia Partners was allowed to continue.

Last year, the FTC sued Welsh Carson and USAP, alleging they pursued a buying spree of anethesiology practices in Texas to create a dominant provider that used its market power to suppress competition and increase the cost of anesthesiology services.

Welsh Carson, which formed USAP in 2012, has since whittled down its ownership of the provider from more than 50% to 23%, and argued that precludes it from being included in the suit. The FTC argued the firm effectively remains in control of USAP.

However, U.S. District Judge Kenneth Hoyt granted Welsh Carson’s motion to dismiss the suit on Tuesday, essentially finding that private equity firms are not liable for the actions of their portfolio companies.

The FTC was unable to prove “any authority for the proposition that receiving profits from an entity that may be violating antitrust laws is itself a violation of antitrust laws,” Hoyt wrote in his opinion.

Hoyt found that Welsh Carson holding a minority share in USAP does not reduce competition, despite USAP’s acquisitions potentially being anticompetitive themselves. In addition, comments from Welsh Carson executives expressing a desire to consolidate other healthcare markets don’t show that the PE firm plans to violate antitrust laws.

If Welsh Carson signals “beyond mere speculation and conjecture” that it’s actually about to violate the law, the FTC can lodge a new lawsuit, the judge wrote.

A spokesperson for Welsh Carson said the firm is “gratified” that the court dismissed the case.

”As we have said from the beginning, this case was without factual or legal basis,” the spokesperson said.

However, Hoyt denied USAP’s motion to dismiss.

The FTC is arguing that USAP — which is the largest anesthesia practice in Texas — leveraged its size to raise prices in the state, resulting in patients, employers and insurers paying tens of millions of dollars more each year for anesthesia services. In addition, USAP allegedly paid a competitor, Envision Healthcare, $9 million to stay out of the Dallas market for five years.

USAP has been criticized for using similar practices to grow in other states, including Colorado.

USAP argued the FTC was overreaching its authority, and regulators’ allegations of anticompetitive conduct were meritless. Hoyt disagreed, pointing out that USAP continues to own the acquired anesthesia groups and continues to charge high prices, including under price-setting agreements. Overall, USAP’s “monopolization scheme remains intact,” according to the opinion.

“The FTC has plausibly alleged acquisitions resulting in higher prices for consumers, along with a market allocation and price-setting scheme. It would be premature to dismiss these claims at this stage,” Hoyt said.

Either way, the dismissal against Welsh Carson is a setback for the FTC, which has taken a more aggressive stance against anticompetitive behaviors in the healthcare industry under the Biden administration.

In December, the FTC and the Department of Justice finalized new guidelines for merger reviews taking aim at previously overlooked practices. Those include private equity roll-ups, when firms acquire and merge multiple small businesses into one larger company — like Welsh Carson’s strategy to grow USAP.

PE firms have acquired hundreds of physician practices across the U.S. in recent years, despite controversy over negative effects on medical quality and cost. One study from 2022 found when private equity took over physician practices, they raised prices by 20% on average.

The U.S. Department of Justice has announced the formation of the Antitrust Division’s Task Force on Health Care Monopolies and Collusion (HCMC), which will guide the division’s enforcement strategy and policy approach in healthcare.

This will include facilitating policy advocacy, investigations and, where warranted, civil and criminal enforcement in healthcare markets.

“Every year, Americans spend trillions of dollars on healthcare, money that is increasingly being gobbled up by a small number of payers, providers and dominant intermediaries that have consolidated their way to power in communities across the country,” said Assistant Attorney General Jonathan Kanter of the Justice Department’s Antitrust Division.

The task force is intended to identify and root out monopolies, as well as any collusive practices that increase costs and decrease quality, according to the DOJ.

WHAT’S THE IMPACT

The HCMC will consider widespread competition concerns shared by patients, healthcare professionals, businesses and entrepreneurs, including issues regarding payer-provider consolidation, serial acquisitions, labor and quality of care, medical billing, healthcare IT services, and access to and misuse of healthcare data.

The task force will also bring together civil and criminal prosecutors, economists, healthcare industry experts, technologists, data scientists, investigators and policy advisors from across the division’s Civil, Criminal, Litigation and Policy Programs, and the Expert Analysis Group to identify and address pressing antitrust problems in healthcare markets.

The HCMC will be directed by Katrina Rouse, a long-serving antitrust prosecutor who joined the Antitrust Division in 2011. She previously served as chief of the division’s Defense, Industrials and Aerospace Section, assistant chief of the division’s San Francisco office, and a special assistant U.S. attorney and a trial attorney in the division’s Healthcare and Consumer Products Section.

Rouse holds degrees from Columbia University and Stanford Law School, and has clerked for federal judges in the U.S. District Court for the District of Maryland and the U.S. Court of Appeals for the Fifth Circuit. She will also serve as the division’s deputy director of civil enforcement and special counsel for healthcare.

The Antitrust Division said it welcomes input from the public, including from practitioners, patients, researchers, business owners and others who have direct insight into competition concerns in the healthcare industry.

Where appropriate, the division will refer matters to other federal and state law enforcers, the DOJ said.

Members of the public can share their experiences with the task force by visiting HealthyCompetition.gov.

THE LARGER TREND

Healthcare monopolies, which can be spurred by hospital consolidation, could have a detrimental effect on consumers’ premiums and out-of-pocket spending due to the resulting outpatient facility fees, a 2023 report found.

Consumer advocates, payers and state regulators flagged a range of issues related to outpatient facility fees. Both consumer advocates and regulators expressed concerns about the financial exposure facility fees created for consumers via increased out-of-pocket spending – driven by plans with high deductibles and other benefit design features that increase patients’ exposure to cost-sharing – and higher premiums resulting from increased spending on ambulatory services.