Hospitals and health systems across the country are telling some Medicare and Medicaid patients that they can’t schedule telehealth appointments due to the federal government’s shutdown, now heading into its second week. That’s because Medicare reimbursement for telehealth expired on September 30, leaving health systems with the choice of pausing such visits or keeping them going in hopes of retroactive reimbursement after the shutdown ends.

Reimbursement for the Hospital at Home program, which allows patients to receive care without being admitted to a hospital, also lapsed with the shutdown. That led to providers scrambling to discharge patients under the program or admit them to a hospital. Mayo Clinic, for example, had to move around 30 patients from their homes in Arizona, Florida and Wisconsin to its facilities.

At issue in the government shutdown is healthcare, specifically tax credits for middle- and lower-income Americans that enable them to afford health insurance on the federal exchanges set up by the Affordable Care Act. Democrats want to extend those tax credits, which are set to expire at the end of the year, while Republicans want to reopen the government first and then negotiate about the tax credits in a final budget.

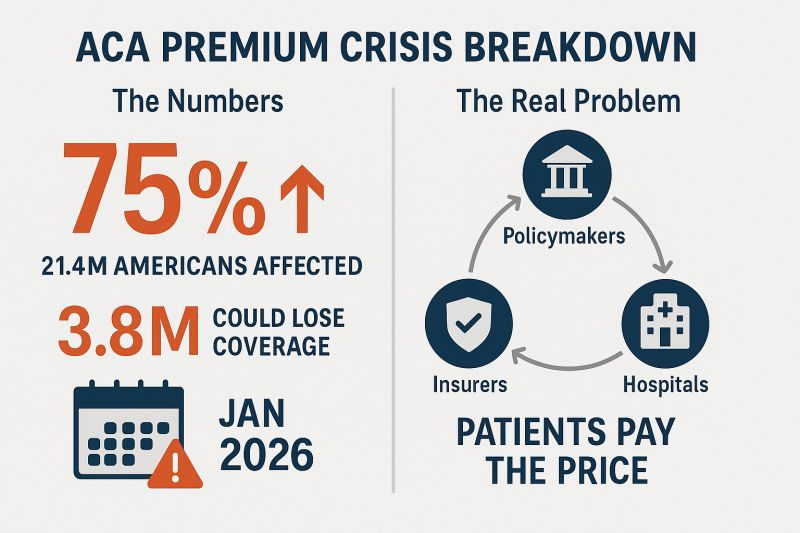

The impasse has prevented the Senate from overcoming a filibuster, despite a Republican majority. Around 24 million Americans get their health insurance through the ACA, and the loss of tax credits will cause their premiums to rise an average of 75%–and as high as 90% in rural areas–and likely cause at least 4 million people to lose coverage entirely.

The government’s closure has reverberated through its operations in healthcare. The Department of Health and Human Services has furloughed some 41% of its staff, making it harder to run oversight operations. CDC’s lack of staff will hinder surveillance of public health threats. And FDA won’t accept any new drug applications until funding is restored.

When the government might reopen remains unclear. Most shutdowns are relatively brief, but the longest one, which lasted 35 days, came during Donald Trump’s first term. Senate majority leader John Thune, R-S.D., and Speaker of the House Mike Johnson, R-La., have both said they won’t negotiate with Democrats, and the House won’t meet again until October 14.Bettors on Polymarket currently expect it to last until at least October 15. Pressure on Congress will increase after that date because there won’t be funds available to pay active military members.

People who buy health insurance through the Affordable Care Act (ACA) are set to see a median premium increase of 18 percent, more than double last year’s 7 percent median proposed increase, according to an analysis of preliminary filings by KFF.

The proposed rates are preliminary and could change before being finalized in late summer. The analysis includes proposed rate changes from 312 insurers in all 50 states and DC.

It’s the largest rate change insurers have requested since 2018, the last time that policy uncertainty contributed to sharp premium increases. On average, ACA marketplace insurers are raising premiums by about 20 percent in 2026, KFF found.

Insurers said they wanted higher premiums to cover rising health care costs, like hospitalizations and physician care, as well as prescription drug costs. Tariffs on imported goods could play a role in rising medical costs, but insurers said there was a lot of uncertainty around implementation, and not many insurers were citing tariffs as a reason for higher rates.

But they are adding in higher increases due to changes being made by the Trump administration and Republicans in Congress. For instance, the majority of insurers said they are taking into account the potential expiration of enhanced premium tax credits.

Those subsidies, put in place during the COVID-19 pandemic, are set to expire at the end of the year, and there are few signs that Republicans are interested in tackling the issue at all.

If Congress takes no action, premiums for subsidized enrollees are projected to increase by over 75 percent starting in January 2026, according to KFF.

But some states are pushing back.

Arkansas Gov. Sarah Huckabee Sanders (R) on Wednesday called on the state’s insurance commissioner to disapprove the proposed increases from Centene and Blue Cross Blue Shield. The companies filed increases of up to 54 percent and 25.5 percent, respectively, she said.

“Arkansas’ Insurance Commissioner is required to disapprove of proposed rate increases if they are excessive or discriminatory, and these are both,” Huckabee Sanders said in a statement.

“I’m calling on my Commissioner to follow the law, reject these insane rate increases, and protect Arkansans.”

The recently passed One Big Beautiful Bill Act, which makes deep cuts to the Medicaid program, also puts the food assistance that 41 million low-income Americans rely on in jeopardy. Many of the families currently getting food provided by the Supplemental Nutrition Assistance Program (SNAP) stand to lose that support.

SNAP may well disappear for some families as the federal government moves to trim it. “The cuts are massive and extremely cruel when families need more support, not less,” says Signe Anderson, senior director of nutrition advocacy, at the Tennessee Justice Center in Nashville.

Government food assistance was established during the Great Depression, but it wasn’t until 1977 that the program became more accessible when the requirement that recipients had to pay for a portion of their food stamps was ended. Throughout its history, foes of the program have tried to dismantle it and may have succeeded as a result of provisions in the bill President Trump signed on July 4.

The new legislation calls for cutting spending for food stamps by $186 billion through 2034. “Everyone on food stamps will be affected in some way, and many will lose benefits,” Anderson says. “I don’t think the Congress understands the level of necessity in the community for food, health care and mental health treatment, some for the rest of their lives.”

One major change is being made to work requirements that have historically been part of the Medicaid program, which is administered and partially funded by the states. Anderson points out that under the new arrangements, participants may find the task of enrolling and staying enrolled more onerous. “We see a lot of people cut off already because too many life circumstances make it difficult for them to meet work requirements.”

Indeed when you look at the changes to SNAP, the first word that might come to mind is ‘draconian.’

To receive benefits those new to the program, and those already on it who are between 55 and 64 and do not have dependent children or who have children 14 and older, will have to prove they work. Or they will have to volunteer at least 20 hours a week or enroll in training programs. Parents of school-aged children will now be required to work.

Some five million people, including about 800,000 children and about a half million adults who are 65 and older, could lose their food benefits.

The programs the new law targets have been a lifeline for some. Nikole Ralls, a 43-year-old woman in Nashville, who was once a drug addict but now counsels others who need help, says, “I got my life turned around because of Medicaid and SNAP.”

In a recent memo to state agencies administering the SNAP program, Agriculture Secretary Brooke Rollins said she was concerned about what was described as abuse of the waiver system by states, noting that the new approach for the SNAP program would prioritize work, education and volunteering over what the department characterized as “idleness and excessive spending.”

Anderson said, “The public doesn’t understand what hunger looks like and are misinformed about how well-run and streamlined the SNAP program is.”

“Most of the people who can, do work. We have parents working two and three jobs,” Anderson said. For families in this predicament food banks, which have become default grocery stores, may be of little help. They, too, are stretched thin. The Wall Street Journal reported food banks across the country are already straining under rising demand, and some worry there won’t be enough food to meet demand.

The “Big Beautiful Budget Bill” appears headed for passage with cuts to Medicaid and potentially Medicare likely elements.

The economy is slowing, with a mild recession a possibility as consumer confidence drops, the housing market slows and uncertainty about tariffs mounts.

And partisan brinksmanship in state and federal politics has made political hostages of public and rural health safety net programs as demand increases for their services.

Last Wednesday, amidst mounting anxiety about the aftermath of U.S. bunker-bombing in Iran and escalating conflicts in Gaza and Ukraine, the Centers for Medicare and Medicaid Services (CMS) released its report on healthcare spending in 2024 and forecast for 2025-2033:

“National health expenditures are projected to have grown 8.2% in 2024 and to increase 7.1% in 2025, reflecting continued strong growth in the use of health care services and goods.

During the period 2026–27, health spending growth is expected to average 5.6%, partly because of a decrease in the share of the population with health insurance (related to the expiration of temporarily enhanced Marketplace premium tax credits in the Inflation Reduction Act of 2022) and partly because of an anticipated slowdown in utilization growth from recent highs. Each year for the full 2024–33 projection period, national health care expenditure growth (averaging 5.8%) is expected to outpace that for the gross domestic product (GDP; averaging 4.3%) and to result in a health share of GDP that reaches 20.3% by 2033 (up from 17.6% in 2023) …

Although the projections presented here reflect current law, future legislative and regulatory health policy changes could have a significant impact on the projections of health insurance coverage, health spending trends, and related cost-sharing requirements, and they thus could ultimately affect the health share of GDP by 2033.”

As has been the case for 20 years, spending for healthcare grew faster than the overall economy in 2024. And it is forecast to continue through 2033:

2024Baseline

2033Forecast

% Nominal Chg.2024-2033

National Health Spending

$5,263B

$8,585B

+63.1%

US Population

337,2M

354.8M

+5.2%

Per capita personal health spending

$13,227

$20,559

+55.7%

Per capita disposable personal income

$21,626

$31,486

+45.6%

NHE as % of US GDP

18.0%

20.3%

+12.8%

In its defense, industry insiders call attention to the uniqueness of the business of healthcare:

‘Healthcare is a fundamental need: the health system serves everyone.’

‘Our aging population, chronic disease prevalence and socioeconomic disparities are drive increased demand for the system’s products and services.’

‘The public expects cutting edge technologies, modern facilities, effective medications and the best caregivers and they’re expensive.’

‘Burdensome regulatory compliance costs contribute to unnecessary spending and costs.’

And they’re right.

Critics argue the U.S. health system is the world’s most expensive but its results (outcomes) don’t justify its costs. They acknowledge the complexity of the industry but believe “waste, fraud and abuse” are pervasive flaws routinely ignored. And they remind lawmakers that the health economy is profitable to most of its corporate players (investor-owned and not-for-profits) and its executive handsomely compensated.

Healthcare has been hit by a perfect storm at a time when a majority of the public associates it more with corporatization and consolidation than caring. This coalition includes Gen Z adults who can’t afford housing, small employers who’ve cut employee coverage due to costs and large, self-insured employers who trying to navigate around the 10-20% employee health cost increase this year, state and local governments grappling with health costs for their public programs and many more. They’re tired of excuses and think the health system takes advantage of them.

As a percentage of the nation’s GDP and household discretionary spending, healthcare will continue to be disproportionately higher and increasingly concerning. Spending will grow faster than other industries until lawmakers impose price controls and other mechanisms like at least 8 states have begun already.

Most insiders are taking cover and waiting ‘til the storm passes. Some are content to cry foul and blame others. Others will emerge with new vision and purpose centered on reality.

Storm damage is rarely predictable but always consequential. It cannot be ignored. The Perfect has Hit U.S. healthcare. Its impact is not yet known but is certain to be a game changer.

New Medicaid funding rules proposed by Congress this week would halt efforts at the state level to better fund rural hospitals and deliver services to the most vulnerable populations in those areas. You can be certain that the administrators and staff of those hospitals, as well as leaders of the communities they serve, are watching closely to see if the cuts are enacted.

Lawmakers at the federal level are trying to make deeper cuts to Medicaid spending in an effort to lower the amount of deficit spending that would be created by President Trump’s spending plan. Trump has dubbed the plan his “big beautiful bill.”

Feds Would Strip Rural Hospitals of Lifeline Funds

Republican members of the Senate Finance Committee this week released their version of the bill that would drain funding for rural hospitals, which rely heavily on Medicaid funds to treat patients. It’s estimated that 25 to 40 percent of services provided by such hospitals are funded by Medicaid.

The federal government and states share the up-front medical costs for Medicaid patients. The federal government then reimburses states up to 50 percent of their Medicaid spending every year.

Many states fund their portion of the cost by taxing entities that provide those services to Medicaid patients.

The latest proposal in Congress would not only restrict how many patients could receive benefits, but it would also stop states from implementing those provider tax programs to help fund Medicaid services provided to residents.

At the federal level, the thinking is that if states keep taxing providers to fund Medicaid services, then the federal government will have to keep reimbursing states a portion of those costs.

The downside to that is many experts, along with several Republicans in Congress, namely Sens. Susan Collins of Maine, Lisa Murkowski of Alaska and Josh Hawley of Missouri, have predicted it will decimate rural hospitals.

West Virginia Republican Sen. Jim Justice went a step further, saying that the plan to limit states’ use of provider taxes will “really hurt a lot of folks.” Despite that statement, Justice said he is OK with the freeze.

State Lawmakers Sound the Alarm

There are 39 states with at least three or more provider taxes used to help fund Medicaid services. Alaska is the only state with no such tax.

Some states, such as Ohio, have set up a new rural hospital fund using provider taxes to help rural hospitals deliver Medicaid services to patients.

Ohio Governor Mike DeWine and the Republican-led state legislature set up a pilot program called the Rural Ohio Hospital Tax Pilot Program. The measure would allow counties to levy a tax on their local hospitals that would then be used to fund Medicaid services.

DeWine said the pilot program would help ease the financial stress rural hospitals face in Ohio. The plan contained in Ohio House Bill 96 has the blessing of the Ohio Hospital Association.

A group of Republican state lawmakers recently sent a letter to their federal counterparts pleading with them to remove the bill language because it would “torpedo” plans to keep rural hospitals functioning.

The American Hospital Association, a 130-year-old trade group of more than 5,000 hospitals and health care providers, this month released the impact on rural hospitals if this plan went into effect.

More than $50 billion would be lost by 2034, and more than 1.8 million rural Americans would lose health benefits.

Kentucky residents would be impacted the most, with 143,000 losing benefits, followed by 135,000 Californians. More than 86,000 Ohioans would lose Medicaid coverage under the plan by 2034, making it the third most impacted state.

To blunt the effects of the cuts, Collins reportedly is proposing the establishment of a $100 billion relief fund that could provide financial support to affected providers, rural hospitals in particular. Whether that or a similar but smaller fund will wind up in the final draft of the legislation apparently will be decided this weekend. Meanwhile, the Senate parliamentarian has ruled against many of the provisions of the Senate version of the bill, including the Finance Committee’s provider tax framework, which puts the whole thing in flux.

Senate leaders say they plan a long series of votes on amendments of the bill on Sunday. The “vote-arama” likely will go on throughout Sunday night and into Monday. If the Senate does pass its version of the bill, it will have to go back to the House. Lawmakers are under a self-imposed deadline to get the legislation to Trump by the July 4 holiday.

Medicaid serves as a vital source of health insurance coverage for Americans living in rural areas, including children, parents, seniors, individuals with disabilities, and pregnant women. Congressional lawmakers are currently considering more than $800 billion in cuts to the Medicaid program, which would reduce Medicaid funding and terminate coverage for vulnerable Americans.

The proposed changes would also result in a significant reduction in Medicaid reimbursement that could result in rural hospital closures.

The National Rural Health Association recently partnered with experts from Manatt Health to shed light on the potential impacts of those cuts on rural residents and the hospitals that care for them over the next decade.

NRHA held a press conference on June 24 that can be accessed with passcode MBTZf4$H. NRHA chief policy officer Carrie Cochran-McClain discussed the findings with Manatt Health partner and former deputy administrator at CMS Cindy Mann and the real world implications of the details of this report with three NRHA member hospital and health system leaders

Report findings provide insight into the impact on rural America at a critical moment in the Congressional debate over the future of the reconciliation package.

The report shows the significant impact from coverage losses that rural communities will face given:

Medicaid plays an outsized role in rural America, covering a larger share of children and adults in rural communities than in urban ones.

Nearly half of all children and one in five adults in small towns and rural areas rely on Medicaid or CHIP for their health insurance.

Medicaid covers nearly one-quarter of women of childbearing age and finances half of all births in these communities.

According to Manatt’s estimates, rural hospitals will lose 21 cents out of every dollar they receive in Medicaid funding due to the One Big Beautiful Bill Act. Total cuts in Medicaid reimbursement for rural hospitals—including both federal and state funds—over the ten-year period outlined in the bill would reach almost $70 billion for hospitals in rural areas.

Reductions in Medicaid funding of this magnitude would likely accelerate rural hospital closures and reduce access to care for rural residents, exacerbating economic hardship in communities where hospitals are major employers.

As a key insurer in rural communities, Medicaid provides a financial lifeline for rural health care providers — including hospitals, rural health clinics, community health centers, and nursing homes—that are already facing significant financial distress. These cuts may lead to more hospitals and other rural facility closures, and for those rural hospitals that remain open, lead to the elimination or curtailment of critical services, such as obstetrics.

“Medicaid is a substantial source of federal funds in rural communities across the country. The proposed changes to Medicaid will result in significant coverage losses, reduce access to care for rural patients, and threaten the viability of rural facilities,” said Alan Morgan, CEO of the National Rural Health Association.

“It’s very clear that Medicaid cuts will result in rural hospital closures resulting in loss of access to care for those living in rural America.”

A media briefing will be held on Tuesday, June 24, from noon to 1:00 PMEST to provide more information about the analysis. This event will feature representatives from NRHA, Manatt Health, and rural hospital leaders across the country. Questions may be submitted in advance, as well as during the press conference. To register for and join the media briefing, click on the Zoom link here.

NRHA is a non-profit membership organization that provides leadership on rural health issues with tens of thousands of members nationwide. Our membership includes nearly every component of rural America’s health care, including rural community hospitals, critical access hospitals, doctors, nurses, and patients. We work to improve rural America’s health needs through government advocacy, communications, education, and research. Learn more about the association at RuralHealth.US.

About Manatt Health

Manatt Health is a leading professional services firm specializing in health policy, health care transformation, and Medicaid redesign. Their modeling draws upon publicly available state data including Medicaid financial management report data from the Centers for Medicare and Medicaid Services, enrollment and expenditure data from the Medicaid Budget and Expenditure System, and data from the Medicaid and CHIP Payment and Access Commission. The Manatt Health Model is tailored specifically to rural health and has been reviewed in consultation with states and other key stakeholders.

Nearly 12 million people would lose their health insurance under President Trump’s “big, beautiful bill,” an erosion of the social safety net that would lead to more unmanaged chronic illnesses, higher medical debt and overcrowding of hospital emergency departments.

Why it matters:

The changes in the Senate version of the bill could wipe out most of the health coverage gains made under the Affordable Care Act and slash state support for Medicaid and SNAP.

“We are going back to a place of a lot of uncompensated care and a lot of patchwork systems for people to get care,” said Ellen Montz, a managing director at Manatt Health who oversaw the ACA federal marketplace during the Biden administration.

The big picture:

The stakes are huge for low-income and working-class Americans who depend on Medicaid and subsidized ACA coverage.

Without health coverage, more people with diabetes, heart disease, asthma and other chronic conditions will likely go without checkups and medication to keep their ailments in check.

Those who try to keep up with care after losing insurance will pay more out of pocket, driving up medical debt and increasing the risk of eviction, food insecurity and depleted savings.

Uninsured patients have worse cancer survival outcomes and are less likely to get prenatal care. Medicaid also is a major payer of behavioral health counseling and crisis intervention.

Much of the coverage losses from the bill will come from new Medicaid work reporting requirements, congressional scorekeepers predict. Work rules generally will have to be implemented for coverage starting in 2027, but could be earlier or later depending on the state.

Past experiments with Medicaid work rules show that many eligible people fall through the cracks verifying they’ve met the requirements or navigating new state bureaucracies.

Often, people don’t find out they’ve lost coverage until they try to fill a prescription or see their doctor. States typically provide written notices, but contacts can be out of date.

Nearly 1 in 3 adults who were disenrolled from Medicaid after the COVID pandemic found out they no longer had health insurance only when they tried to access care, per a KFF survey.

Zoom out:

The Medicaid and ACA changes will also affect people who keep their coverage.

The anticipated drop-off in preventive care means the uninsured will be more likely to go to the emergency room when they get sick. That could further crowd already bursting ERs, resulting in even longer wait times.

Changes to ACA markets in the bill, along with the impending expiration of enhanced premium subsidies, may drive healthier people to drop out, Montz said, skewing the risk pool and driving up premiums for remaining enrollees.

States will likely have to make further cuts to their safety-net programs if the bill passes in order to keep state budgets functioning with less federal Medicaid funding.

The other side:

The White House and GOP proponents of the bill say the health care changes will fight fraud, waste and abuse, and argue that coverage loss projections are overblown.

Conservative health care thinkers also posit that there isn’t strong enough evidence that public health insurance improves health.

Reality check:

Not all insurance is created equally, and many people with health coverage still struggle to access care. But the bill’s impact would take the focus off ways to improve the health system, Montz said.

“This is taking us catastrophically backward, where we don’t get to think about the things that we should be thinking about how to best keep people healthy,” she said.

The bottom line:

The changes will unfold against a backdrop of Health Secretary Robert F. Kennedy Jr.’s purported focus on preventive care and ending chronic illness in the U.S.

But American health care is an insurance-based system, said Manatt Health’s Patricia Boozang. Coverage is what unlocks access.

Scrapping millions of people’s health coverage “seems inconsistent with the goal of making America healthier,” she said.

Medicaid is critical to our nation’s healthcare system, providing necessary care for more than 72 million Americans – including our neighbors and friends.

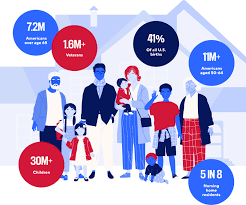

Who it Affects

Medicaid covers children, seniors in nursing homes, veterans, people with long-term chronic illnesses, those with mental health issues and working families.

The program helps keep Americans healthy at all stages of life, providing healthcare to families in need — especially as the country continues to recover from record-high inflation.

The Problem

Some policymakers are considering Medicaid cuts that would undermine coverage for countless patients and threaten Americans’ access to comprehensive, 24/7 hospital care.

Medicaid covers health services for patients who otherwise wouldn’t be able to pay for care. Coverage of services is essential for hospitals, and helps ensure all Americans have access to high-quality, 24/7 care, no matter where they live.

Who Medicaid covers

Providing Lifesaving Healthcare Services

Medicaid covers patients with complex and chronic illnesses in need of long-term care, as well as emergency services and prescription coverage.

As the nation faces a growing mental health crisis, Medicaid also ensures millions of Americans — including veterans — have access to mental healthcare and substance abuse services.

Without access to affordable mental healthcare through Medicaid, veterans often lack the long-term support they deserve, and are left to deal with complex health issues years after their service.

In these areas, where primary care providers are few and far between, hospitals become even more vital sites of care — and in some cases, the only sites of care available.

Rural hospitals, already more likely to be at risk of closure, rely on Medicaid funding to stay open and to continue providing lifesaving care to their patients. Nearly 150 rural hospitals have closed or converted since 2010 alone. Further cuts to care would eliminate a lifeline for Americans across the country — with devastating consequences for rural communities.

The Solution

Cuts to Medicaid funding will create irreparable harm for our nation’s most vulnerable communities, including millions of children, veterans, those with chronic illnesses, seniors in nursing homes, and working families. Medicaid helps provide security to these Americans, keeping them healthy at every stage of life.

Congress should vote against efforts to reduce Medicaid funding and instead focus on policies that strengthen access to 24/7 care, rather than take it away.

The GOP’s reconciliation bill, the “One Big Beautiful Bill Act” (yes, it’s actually called that), is a cruel exercise in slashing benefits for the poor, the elderly, and the sick to free up fiscal space for yet more tax cuts for the rich. Compounding the harm, these benefit cuts are nowhere near enough to pay for the bill’s tax cuts for the wealthy.

Central to this effort are massive cuts to Medicaid and the Affordable Care Act (ACA) marketplaces that, as I argued in my recent paper, will exacerbate our ongoing medical debt crisis.

The GOP reconciliation package that the Senate and House recently agreed to instructed the House Energy and Commerce Committee, which oversees spending on health-care programs including Medicaid and the Children’s Health Insurance Program (CHIP), to identify up to $880 billion in savings over the next 10 years.

Under the rules of the budget reconciliation process, Republicans need to offset any tax cuts they wish to make permanent with an equal dollar value in cuts to spending so as to remain deficit neutral. Trillions of dollars in tax cuts for the wealthier therefore necessitate trillions of dollars in cuts to spending that fall mostly on the social safety net.

Although they did not quite reach that target, the committee still returned a proposed package of deep cuts and changes to Medicaid and to the ACA marketplaces that would reduce federal medical spending by at least $715 billion over 10 years, with about $625 billion in reduced Medicaid spending.1

After public backlash, Republicans seem to have backed off some of their most radical plans for Medicaid (at least for now—one of the challenges of taking health care from people is that it’s terrible politics, so the precise details of the cuts are likely to remain a moving target until the bill passes).

But all options they are close to settling on would still do horrific damage to the well-being of working-class families.

This includes requiring all Medicaid recipients above the federal poverty line to “cost share” by paying (larger) premiums and copayments,2 cutting federal matching to states that provide public health insurance coverage to undocumented and perhaps documented immigrants (on their own dime), and imposing harsh work requirements on “able-bodied adults without dependent children.” This latter provision will cut federal Medicaid spending by roughly $300 billion over 10 years even though the vast majority (92 percent) of nondisabled, non-elderly adult Medicaid recipients are already working, studying full time, or serving as caregivers. This is because work requirements create burdensome reporting requirements to demonstrate compliance that will cause Medicaid recipients who are already employed to lose their insurance as well—blaming the victim for losing their health care, in essence.

The Congressional Budget Office estimates that the reconciliation bill would decrease Medicaid enrollment by 10.3 million in 2034(the end of the reconciliation bill budget window).

According to this same analysis, most of these individuals would not obtain other insurance (e.g., through an employer) and would thus become uninsured.

When combined with the bill’s changes to the ACA marketplace and the expiration of the enhanced premium tax credits—a wildly successful policy that was introduced as part of the American Rescue Plan Act (ARPA) and one that Republicans have shown no inclination to extend—this would result in an additional 13.7 million uninsured individuals in 2034, a 30 percent increase, according to KFF estimates.

Republicans seem hell-bent on undoing the remarkable progress made in the 15 years since the passage of the ACA in reducing the non-elderly uninsured rate from 17.8 percent in 2010 to roughly 9.5 percent today (plus ça change).

But we’ve seen less focus on how this will affect the problem of underinsurance.

Republicans’ Medicaid cost-sharing requirements, the changes they have proposed to the ACA marketplaces, and their determination to let the ARPA premium tax credit enhancements expire will also worsen the problem of underinsurance, an area where we have made considerably less progress.

Taken together, this will worsen the ongoing medical crisis because medical debt is driven by uninsurance and underinsurance.

Medical debt is, unlike in most other countries, and despite the successes of the ACA, a major problem in the United States. KFF found that 20 million adults (almost 1 in 12) owed “significant” medical debt to a health-care provider.3 This number rises when we consider a more expansive definition of medical debt including credit card balances and bank loans used to pay medical providers. Under that definition, an estimated 41 percent of American adults (~107 million people) carried some form of medical debt and 24 percent of American adults (~62 million people) had medical debt that was past due or that they were unable to pay. Among those with medical debt using this more expansive definition, nearly half (44 percent) reported owing at least $2,500, and about one in eight (12 percent) said they owe $10,000 or more. The poor, the sick, the middle-aged, and Black and Hispanic individuals disproportionately bear the brunt of this problem.

The crisis of medical debt and underinsurance is so widely recognized by Americans that a state attorney general candidate can go viral just by talking about the reality of a GoFundMe health-care system millions of Americans face.

The consequences of all this debt are dire—and reflect a health-care system that heals people physically but leaves many permanently scared financially. In 2022, medical debt (using the narrow definition) made up an estimated 58 percent of all debts that had gone to collections, and 62 percent of bankruptcies were attributed in part to medical debt. Medical debt also damages credit scores, leading to a wide variety of negative impacts on financial well-being that can follow families for years.

A poor credit score means that families may be unable to obtain a mortgage or a car loan or may end up paying much higher interest rates.

Credit scores are commonly used by landlords to screen tenants and by employers as part of a background check during the hiring process. Even for those who manage to maintain their credit after taking on medical debt, there are real costs. For those with limited income and assets, debt service may displace spending on food, clothing, and other essentials, leading to material hardship. It can make savings impossible and limit economic mobility.

Medical debt is a problem largely generated by poor policy decisions including, as I argue in my paper, prioritizing and incentivizing health insurance coverage through the private market rather than through Medicaid and Medicare, which offer comprehensive coverage more cheaply. The problem would rapidly disappear if we could extend comprehensive health insurance coverage to the millions of uninsured and underinsured people who live with the constant risk that a sudden medical event could ruin their finances and constrain their futures.

But rather than fix the problem, the GOP plans to throw millions off Medicaid and saddle those who remain with higher costs and more limited coverage. The results of these poor policy decisions will be more sickness, more debt, and higher costs for everyone in exchange for on-paper “savings.” And all this in service of tax cuts for the wealthy they haven’t even bothered to justify.

If you ask Eleanor

“If the old people cannot afford their medical care under their own Social Security allowances, then the burden is going to fall on their children who are in their earning years. This will mean that just at the time when these children who may be having young children of their own and needing medical care, a young couple will also have to consider shouldering the burden for parents as well. This is not fair, and leads to both the children and the older people not getting full coverage, since both will try to shave a little off their needs in order not to make the burden impossible to carry.”

Most Americans believe their healthcare is private, and the majority prefers it that way. Gallup polling shows more Americans favor a system based on private insurance rather than government-run healthcare.

But here’s a surprising reality: 91% of Americans receive government-subsidized healthcare.

Unless you’re among the uninsured or the few who receive no subsidies, government dollars are helping pay your medical bills — whether your insurance comes from an employer, a privately managed care organization or the online marketplace.

Now, as lawmakers face mounting budget pressures, those subsidies (and your coverage) could be at risk. If the government scales back its healthcare spending, your medical costs could skyrocket.

Here’s a closer look at the five ways the U.S. government funds healthcare. If you have health insurance, you’re almost certainly benefiting from one of them:

Medicare, the government-run healthcare program for those 65 and older, covers 67 million Americans at a cost of more than $1 trillion annually. Approximately half of enrollees are covered through the traditional fee-for-service plan and the other half in privately managed Medicare Advantage plans.

Medicaid and CHIP provide health coverage for around 80 million low-income and disabled Americans, including tens of millions of children. Even though 41 states have turned over their Medicaid programs over to privately managed care organizations, the cost remains public. Total Medicaid spending is $900 billion annually — the federal government pays 70% with states footing the rest.

The online healthcare marketplace is for Americans whose employer doesn’t provide medical coverage or who are self-employed. This Affordable Care Act program offers federal subsidies to 92% of its 23 million enrollees, which help lower the cost of premiums and, for many, subsidize their out-of-pocket expenses. The Congressional Budget Office projects that a permanent extension of these subsidies, which are scheduled to end this year, would cost $383 billion over the next 10 years.

Veterans and military families also benefit from government healthcare through TRICARE and VA Care, programs covering roughly 16 million individuals at a combined cost of $148 billion for the federal government annually.

Employer-sponsored health insurance comes with a significant, yet often overlooked, government subsidy. For nearly 165 million American workers and their families, U.S. companies pay the majority of their health insurance premiums. However, those dollars are excluded from employees’ taxable income. This tax break, which originated during World War II and was formally codified in the 1950s, subsidizes workers at an annual government cost of approximately $300 billion. For a typical family of four, this translates into approximately $8,000 per year of added take-home pay.

With 91% of Americans receiving some form of government healthcare assistance, the idea that U.S. healthcare is predominantly “private” is an illusion.

Now, as the new administration searches for ways to rein in the growing federal deficit, all five of these programs (collectively funding healthcare for 9 in 10 Americans) will be in the crosshairs.

Twelve percent of the federal budget already goes toward debt interest payments, and this share is expected to rise sharply. Many of the bonds used to finance existing debt were issued back when interest rates were much lower. As those bonds mature and are refinanced at today’s higher rates, federal interest payments are projected to double within the next decade, according to the Congressional Budget Office.

With deficits mounting and borrowing costs soaring, most economists agree this trajectory is unsustainable. Lawmakers will eventually need to rein in spending, and healthcare subsidies will almost certainly be among the first targets. Policy experts predict Medicaid, which the House has already proposed cutting by $880 billion over the next decade, and ACA subsidies for out-of-pocket costs will likely be the first on the chopping block. But given the CBO’s projections, these cuts won’t be the last.

A Better Way: Three Solutions To Lower Healthcare Costs Without Cuts

Cutting some or all of these healthcare subsidies may seem like the simplest way to reduce the deficit. In reality, it merely shifts costs elsewhere, making medical care more expensive for everyone and increasing future government spending. Here’s why:

Eliminating subsidies doesn’t eliminate the need for care. Under the Emergency Medical Treatment and Labor Act (EMTALA), hospitals must treat emergency patients regardless of their ability to pay. When millions lose insurance, more turn to ERs for medical care they can’t afford. The cost of that uncompensated care doesn’t vanish. It gets passed on to state governments, hospitals and privately insured patients through higher taxes, inflated hospital bills and rising insurance premiums.

Delaying care drives up long-term costs. People who can’t afford doctor visits skip preventive care, screenings and early treatments. Manageable conditions like high blood pressure and diabetes then spiral into costly, life-threatening complications including heart attacks, strokes and kidney failures, which ultimately increase government spending.

The solution isn’t cutting coverage. It’s fixing the root causes of high healthcare costs. Here are three ways to achieve this:

1. Address The Obesity Epidemic

Obesity is a leading driver of diabetes, heart disease, stroke and breast cancer, which kill millions of Americans and cost the U.S. healthcare system hundreds of billions annually. Congress can take two immediate steps to reverse this crisis:

Tax high-calorie, highly processed foods and use the revenue to subsidize healthier options, making nutritious food more affordable for all Americans.

2. Enhance Chronic Disease Management With Technology

In every other industry, broad adoption of generative AI technology is already increasing quality while reducing costs. Healthcare could do the same by applying generative AI to more effectively manage chronic disease. According to the Centers for Disease Control and Prevention, improved control of these lifelong conditions could cut the frequency of heart attacks, strokes, kidney failures and cancers by up to 50%.

With swift and reasonable Food and Drug Administration approval, generative AI and wearable monitors would revolutionize how these conditions are managed, providing real-time updates on patient health and identifying when medications need adjustment. Instead of waiting months for their next in-office visit, patients with chronic diseases would receive continuous monitoring, preventing costly and life-threatening complications. Rather than restricting AI’s role in healthcare, Congress can streamline the FDA’s approval process and allocate National Institutes of Health funding to accelerate these advancements.

3. Reform Healthcare Payment Models

Under today’s fee-for-service system, doctors and hospitals are paid based on the how often they see patients for the same problem and the number of procedures performed. This approach rewards the volume of care, not the best and most effective treatments. A better alternative is a pay-for-value model like capitation, in which providers do best financially when they help keep patients healthy. To encourage participation, Congress should fund pilot programs and create financial incentives for insurers, doctors and hospitals willing to transition to this system. By aligning financial incentives with long-term health, this model would encourage doctors to prioritize prevention and effective chronic disease control, ultimately lowering medical costs by improving overall health.

The Time For Change Is Now

If Congress slashes healthcare subsidies this year, restoring them will be nearly impossible. Once the cuts take effect, the financial and political pressures driving them will only intensify, making reversal unlikely.

The voices shaping this debate can’t come solely from industry lobbyists. Elected officials need to hear from the 91% of Americans who rely on government healthcare assistance for some or all of their medical coverage. Now is the time to speak up.