What can we do about infant mortality and disparities in health care? This week we take a look at a recent study in JAMA that may have an answer.

What can we do about infant mortality and disparities in health care? This week we take a look at a recent study in JAMA that may have an answer.

The findings jibe with recent data from the Centers for Disease Control’s National Health Interview Survey, which showed more than 1.1 million Americans lost health coverage in 2018, pushing the total number of uninsured from 29.3 million in 2017 to 30.4 million last year. Among surveyed adults between 18 and 64 years old, 13.3% were uninsured, 19.4% had public health coverage and 68.9% had private coverage.

The trend coincides with Trump administration efforts to weaken the ACA by eliminating several mechanisms meant to stabilize payers participating in ACA exchanges and pushing stripped-down, noncompliant health plans. The result has been rising premiums and a resurgence in the number of uninsured.

Adding to uncertainty about the ACA’s future is the U.S. Department of Justice’s support for a Texas federal district court that ruled the law unconstitutional without its individual mandate penalty, which a Republican-led Congress removed in 2017. A previous Urban Institute report estimated up to 20 million Americans would lose health insurance if the lawsuit prevails — a majority of whom are currently covered through Medicaid expansions and ACA exchanges.

While the ACA remains in legal jeopardy, Democrats and presidential candidates are looking at ways to increase the numbers of insured Americans, from shoring up the ACA to implementing some type of single-payer system or “Medicaid for All.”

According to the Urban Institute, participation in Medicaid/CHIP among children increased from 88.7% in 2013 to 93.7% in 2016, and from 67.6% to 79.9% for parents. Those gains reversed in 2017, however, with Medicaid/CHIP participation dropping to 93.1% among children and remaining unchanged for parents.

Among those who did not enroll in Medicaid/CHIP in 2017, 2 million children and 1.7 million parents were eligible for the programs — versus 1.9 million and a steady 1.7 million, respectively, in 2016.

More than half of the uninsured children and parents who were eligible for the Medicaid/CHIP lived in California, Florida, Georgia, Illinois, Indiana, New York, Pennsylvania and Texas, according to combined 2016-2017 data.

Parents were more than twice as likely to be uninsured as children in 2017. For example, children’s uninsurance rate was less than 5% in most states and under 10% in nearly every state, while parents’ uninsurance was less than 5% in just four states and over 10% in close to half the states, the report says.

The decline in improvement was worse among certain subgroups. “In 2017, the uninsurance rate was nearly 6% or higher among adolescents, Hispanic and American Indian/Alaska Native children, citizen children with noncitizen parents, and noncitizen children,” according to the report. “And consistent with prior years, one in six parents or more who were ages 19 5o 24, Hispanic or American Indian/Alaska Native, below 100 percent of FPL [federal poverty level], receiving SNAP [Supplemental Nutrition Assistance Program] benefits, or noncitizen were uninsured in 2017.”

https://www.healthcaredive.com/news/number-of-uninsured-adults-reaches-post-aca-high/546653/

The Affordable Care Act helped the U.S. reach historical lows for the rate of uninsured adults, but that figure has continued to tick back up as the Trump administration has undermined the law.

In all, the 2.8 percentage point increase since 2016’s low point represents about 7 million more uninsured Americans. Most of those 7 million became uninsured in 2017, which experienced the largest single-year increase (1.3 percentage points) since Gallup began polling Americans on the question in 2008.

The continued rise in the uninsured rate is reversing the gains made under the Affordable Care Act.

The ACA ushered in a time when people could buy insurance not tied to a job — without having to worry about being denied for having a pre-existing condition such as diabetes or cancer. Plus, it allowed states to expand Medicaid to low-income residents who otherwise could not afford to purchase private coverage on their own.

During that time of record-low uninsured rates, many Americans were required to have health insurance or risked incurring a financial penalty.

But once President Donald Trump was elected he began working to overturn the law. In December 2017, the GOP’s tax bill eliminated the financial penalty for not having insurance.

A separate Commonwealth Fund report found that the uninsured rate was up significantly among working adults in states that did not expand Medicaid.

CFO Lynn Krutak said the system’s most significant challenge is its payer mix.

Luckily, she says, Virginia’s decision to expand Medicaid will help somewhat in terms of recouping from years of cuts.

Ballad Health also has a $308 million, 10-year spending plan in the works.

Last year, Mountain States Health Alliance (MSHA) and Wellmont Health System, merged to form Ballad Health. The fact that the two rural systems merged was not typical because it formed under a certificate of public advantage (COPA).

This legal agreement governs the merger through joint oversight from both the state of Tennessee and Virginia and also includes “enforceable commitments” to invest in population health, expand patient access, and boost research and education opportunities.

According to the Millbak Memorial Fund, the COPA acts as a “state-monitored monopoly—or a public utility model of healthcare delivery.”

Related: Ballad Health Launches Changes Across Newly Merged Hospital Network

Lynn Krutak, who served as CFO for both MSHA and its corporate parent Blue Ridge Medical Management, was elevated as CFO at Ballad Health. In an interview with HealthLeaders, Krutak emphasized how she implemented effective cost-cutting strategies within a challenging payer mix and low-wage index area.

This transcript has been lightly edited for brevity and clarity.

HealthLeaders: Can you describe the challenges and opportunities for Ballad Health in its provider market?

Krutak: The majority of our hospitals are either in southwest Virginia or northeast Tennessee, so we have high-use rates. From the payer standpoint, as more people move into managed Medicare and managed Medicaid, we know those use rates are going to fall.

Our population growth is flat to even declining; a lot of our counties in southwest Virginia are coal counties that have been hit hard by the [employment] reductions. So, with the use-rates decline, population decline, and the reimbursement decline that we’re all faced with, we know that there are going to be issues going forward.

As far as our payer mix, we’re heavily governmental. Over 70% of our payer mix is Medicare, Medicaid, or self-pay. We can continue to see the payer mix decline as well. We are also faced with high-deductible health plans out there now, with the patient portion of those deductibles being so high our bad debt has increased over 30%.

Fortunately, Virginia has implemented a Medicaid expansion program, so we will get some relief. However, we’ve had years of ACA cuts and this is a small portion. With the cuts that we’ve had versus what we’re going to gain back from Medicaid expansion, we’ll still be in the red.

Our wage index with Medicare is another hurdle we have. We are in the fourth-lowest wage index area in the country; we’re getting about half of what other [systems] are getting. We’ve done a good job of controlling our costs because we have to.

We’re excited about the potential with some of the things that we’re going to be able to do as a merged organization. We have $308 million in spending commitments over the next 10 years, but we have about twice as much in estimated savings. We’ve been able to achieve a lot of that already and we’re working hard on our continued integration.

This merger’s unique and what we’re going to be able to do is take costs out of the system, as far as redundant and duplicative costs go, and then reinvest them back.

HL: Can you describe some initiatives Ballad is looking to pursue in the next few years?

Krutak: As far as the labor costs, we’ve done a great job controlling our labor by not using contract labor for nursing. During the nursing shortage, other systems were using contract labor, it was something that MSHA did not have to do.

We have East Tennessee State University right in our backyard in Johnson City, where we work with them to develop nursing programs and offer scholarships to students in return for a work commitment.

Of the investments through COPA, where we have committed $308 million over a 10-year period, [is] $75 million is going to common health issues facing children. We’ve made a commitment to bring on specialists—specifically pediatrics—and be able to keep these patients and their families in the region and not have to send them elsewhere.

We’ve also committed $140 million to mental health, addiction, or rural health [initiatives] with $85 million going to behavioral health. That’s an issue for our service area in northeast Tennessee and southwest Virginia.

Finally, we have $8 million set for clinical effectiveness and patient engagement mainly related to health information exchange. Wellmont was on Epic, MSHA was on Cerner, so we agreed to convert the whole system to Epic, which will happen in April 2020.

HL: How is Ballad best positioned to navigate the direction healthcare is going while still providing the best quality service to its patients?

Krutak: We’ve been working with our state representatives to craft a fair wage index bill, where Ballad would get some relief and revamp how those calculations are done. In other words, you would not be penalized if you do a good job controlling your costs.

Our CEO, Alan Levine was secretary of health in Florida and secretary of health in Louisiana. We have Tony Keck, who is the executive vice president of our development, innovation, and population health improvement, who was secretary of health in South Carolina. We have a lot of insight on the [governmental] side of things from them.

We’re positioning ourselves to take costs out of the system but also to switch over from fee-for-service plans to looking at risk-based contracts. How do we get paid more for showing better patient outcomes? We’re looking over the next five years to transition into more of that than your traditional payments.

HL: What advice would you give to CFOs from rural systems to make the most of what are sometimes challenging financial situations?

Krutak: As a result of the merger, I’m relieved that we’re going to be able to have these savings to reinvest in rural areas. The largest issue we face with the payer mix shift is that it’s hard to get physicians in rural areas.

My advice to them is just make sure that you are controlling your costs as much as you possibly can and look to partner with other systems that may be near you that could provide physician-sharing arrangements.

For the reimbursement side, it’s always actively looking at how you’re being paid and what you’re being paid. Work with your government officials and partner with your hospital associations, to say, ‘Hey, if we’re going to continue to keep these rural hospitals and provide access, then there’s going to have to be changes as far as how that reimbursement is calculated and how those facilities are compensated.’

On the cost side, make sure that that you’ve situated yourself appropriately and then as things transition to outpatient, be sure the investments that you’re making are being made in the right places.

Red states are getting creative as they look for new ways to limit the growth of Medicaid. But in the process those states are taking legal, political and practical risks that could ultimately leave them paying far more, to cover far fewer people.

Why it matters: Medicaid and the Children’s Health Insurance Program cover more than 72 million Americans, thanks in part to the Affordable Care Act’s Medicaid expansion. Rolling back the program is a high priority for the Trump administration, and it needs states’ help to get there.

Celina became the 11th rural hospital in Tennessee to close in recent years — more than in any state but Texas. Both states have refused to expand Medicaid in a way that covers more of the working poor.

The closest hospital is now 18 miles away. That adds another 30 minutes through mountain roads for those who need an X-ray or bloodwork. For those in the back of an ambulance, that bit of time could mean the difference between life or death.

When a rural community loses its hospital, health care becomes harder to come by in an instant. But a hospital closure also shocks a small town’s economy. It shuts down one of its largest employers. It scares off heavy industry that needs an emergency room nearby. And in one Tennessee town, a lost hospital means lost hope of attracting more retirees.

Seniors, and their retirement accounts, have been viewed as potential saviors for many rural economies trying to make up for lost jobs. But the epidemic of rural hospital closures is threatening those dreams in places like Celina, Tenn. The town of 1,500, whose 25-bed hospital closed March 1, has been trying to position itself as a retiree destination.

“I’d say, look elsewhere,” said Susan Scovel, a Seattle transplant who arrived with her husband in 2015.

Scovel’s despondence is especially noteworthy given she leads the local chamber of commerce effort to attract retirees like herself. She considers the wooded hills and secluded lake to hold scenic beauty comparable to the Washington coast — with dramatically lower costs of living; she and a small committee plan getaway weekends for prospects to visit.

When she first toured the region before moving in 2015, Scovel and her husband, who had Parkinson’s, made sure to scope out the hospital, on a hill overlooking the sleepy town square. And she has rushed to the hospital four times since he died in 2017.

“I have very high blood pressure, and they’re able to do the IVs to get it down,” Scovel said. “This is an anxiety thing since my husband died. So now — I don’t know.”

She can’t in good conscience advise a senior with health problems to come join her in Celina, she said.

When Seconds Count, Delays In Care

Celina’s Cumberland River Hospital had been on life support for years, operated by the city-owned medical center an hour away in Cookeville, which decided in late January to cut its losses after trying to find a buyer. Cookeville Regional Medical Center executives explain that the facility faced the grim reality for many rural providers.

“Unfortunately, many rural hospitals across the country are having a difficult time and facing the same challenges, like declining reimbursements and lower patient volumes, that Cumberland River Hospital has experienced,” CEO Paul Korth said in a written statement.

Celina became the 11th rural hospital in Tennessee to close in recent years — more than in any state but Texas. Both states have refused to expand Medicaid in a way that covers more of the working poor. Even some Republicans now say the decision to not expand Medicaid has added to the struggles of rural health care providers.

The closest hospital is now 18 miles away. That adds another 30 minutes through mountain roads for those who need an X-ray or bloodwork. For those in the back of an ambulance, that bit of time could mean the difference between life or death.

“We have the capability of doing a lot of advanced life support, but we’re not a hospital,” said Natalie Boone, Clay County’s emergency management director.

The area is already limited in its ambulance service, with two of its four trucks out of service.

Once a crew is dispatched, Boone said, it’s committed to that call. Adding an hour to the turnaround time means someone else could likely call with an emergency and be told — essentially — to wait in line.

“What happens when you have that patient that doesn’t have that extra time?” Boone asked. “I can think of at least a minimum of two patients [in the last month] that did not have that time.”

Residents are bracing for cascading effects. Susan Bailey hasn’t retired yet, but she’s close. She has spent nearly 40 years as a registered nurse, including her early career at Cumberland River.

“People say, ‘You probably just need to move or find another place to go,'” she said.

Bailey and others are concerned that losing the hospital will soon mean losing the only three physicians in town. The doctors say they plan to keep their practices going, but for how long? And what about when they retire?

“That’s a big problem,” Bailey said. “The doctors aren’t going to want to come in and open an office and have to drive 20 or 30 minutes to see their patients every single day.”

Closure of the hospital means 147 nurses, aides and clerical staff have to find new jobs. Some employees come to tears at the prospect of having to find work outside the county and are deeply sad that their hometown is losing one of its largest employers — second only to the local school system.

Dr. John McMichen is an emergency physician who would travel to Celina to work weekends at the ER and give the local doctors a break.

“I thought of Celina as maybe the ‘Andy Griffith Show’ of healthcare,” he said.

McMichen, who also worked at the now-shuttered Copper Basin Medical Center, on the other side of the state, said people at Cumberland River knew just about anyone who would walk through the door. That’s why it was attractive to retirees.

“It reminded me of a time long ago that has seemingly passed. I can’t say that it will ever come back,” he said. “I have hopes that there’s still some hope for small hospitals in that type of community. But I think the chances are becoming less of those community hospitals surviving.”

“UNFORTUNATELY, RURAL HOSPITALS ACROSS THE COUNTRY ARE HAVING A DIFFICULT TIME AND FACE THE SAME CHALLENGES, LIKE DECLINING REIMBURSEMENTS AND LOWER PATIENT VOLUMES THAT CUMBERLAND RIVER HOSPITAL HAS EXPERIENCED.”

A year after facing a federal funding cliff, CHCs in expansion states are thriving.

CHCs provide care to 27 million patients each year, according to the Health Resources and Services Administration.

The financial stability of CHCs, which serve medically vulnerable communities, is a benefit for health systems.

Community health centers (CHC) operating in states that expanded Medicaid under the ACA are 28% more likely to report improvements to their financial stability, according to a Commonwealth Fund report released Thursday morning.

CHCs in Medicaid expansion states reported were more likely to report improvements in their ability to provide affordable care to patients, 76%, than their counterparts in non-expansion states, 52%.

More than 60% of CHCs in expansion states reported improved ability to fund service or site expansions and upgrades for facilities, while only 46% of CHCs in non-expansion states said the same.

These facilities reported higher levels of unfilled job openings for mental health professional and social workers, while also implying a greater openness to operating under a value-based payment model.

The success and viability of CHCs are essential for larger health systems, according to Melinda K. Abrams, M.S., vice president and director of the Commonwealth Fund’s Health Care Delivery System Reform program, adding that CHCs act as a strong foundation for providing primary care to medically vulnerable populations in rural communities.

Abrams said that by making sure patients are insured and receiving care up front, rather than delaying treatment and exacerbating their condition, they are less likely to end up in a hospital emergency room and contribute to a rise in uncompensated care for hospitals.

She also told HealthLeaders that populations with higher enrollment rates make it easier for CHCs to innovate, invest in technology, hire new staff, train existing the workforce, and adopt new models of care.

“[Medicaid expansion] makes it a lot easier to provide high-quality comprehensive care when [a CHC’s] patients have health insurance,” Abrams said. “In this particular instance, it’s a lot easier to innovate and have financial stability when you have more paying patients, which means that it is easier if you are [a CHC] in a state that has expanded Medicaid.”

The Commonwealth Fund report provides a welcome note of positivity for CHCs, which serve vulnerable populations primarily composed by the uninsured, but have faced funding challenges in the past.

During the budget battles that produced multiple government shutdowns throughout the early portion of 2018, advocates wondered anxiously whether Congress would provide long term funding to the nearly 1,400 CHCs operating at nearly 12,000 service delivery sites across the country.

According to the Health Resources and Services Administration, CHCs provide care to more than 27 million patients annually.

The Community Health Center Fund (CHCF), created in 2010 as a result of the ACA, is the largest source of comprehensive primary care for medically underserved communities, according to the Kaiser Family Foundation.

However, Abrams said that Medicaid expansion has also been a beneficial tool for CHCs, as they have begun to see more insured patients while also benefiting from Medicaid reimbursements, even though they are low compared to other reimbursement rates.

CHCs in states that expanded Medicaid have been able to grow the services that are offered while assisting in the ongoing fight against the opioid epidemic, according to the Commonwealth Fund report.

Abrams said that one downside to the growing success of CHCs have been the unfilled positions, mostly for mental health providers, that are falling behind rising demand levels, though she added that this finding is not surprising.

“I think it’s in part because the supply of the workforce is lagging a little bit behind the demand,” Abrams said. “There’s no reason to think that over time that this gap wouldn’t be closed. But we did find that as a challenge, that [CHCs] have a lot of positions open [yet] they’re hiring. A number of these CHCs are in economically depressed areas, so the good news is that there are some jobs available.”

CHCs are much more likely to participate in value-based payment models as a result of Medicaid expansion, with Abrams explaining that changes in payments and delivery models are common during insurance expansions.

She sees the continued progress made on the value-based front by CHCs as a way to “promote better healthcare and save money” over time.

Hospitals, physicians and insurer groups are united in wanting to preserve the Affordable Care Act and have defended it in briefs filed with the Fifth Circuit Court of Appeals.

The American Hospital Association, the American Medical Association and America’s Health Insurance Plans are among groups that are fighting a lower court ruling in Texas that struck down the law.

On the other side is the Department of Justice, which last month reversed an earlier opinion and sided with the Texas judge who ruled that without the individual mandate, the entire ACA has no constitutional standing.

WHY THIS MATTERS

The ACA has insured millions who otherwise may not have been insured, allowing them to get care when needed instead of going to the more expensive emergency room when they have a medical crisis.

Hospitals and physicians see less uncompensated care under the ACA.

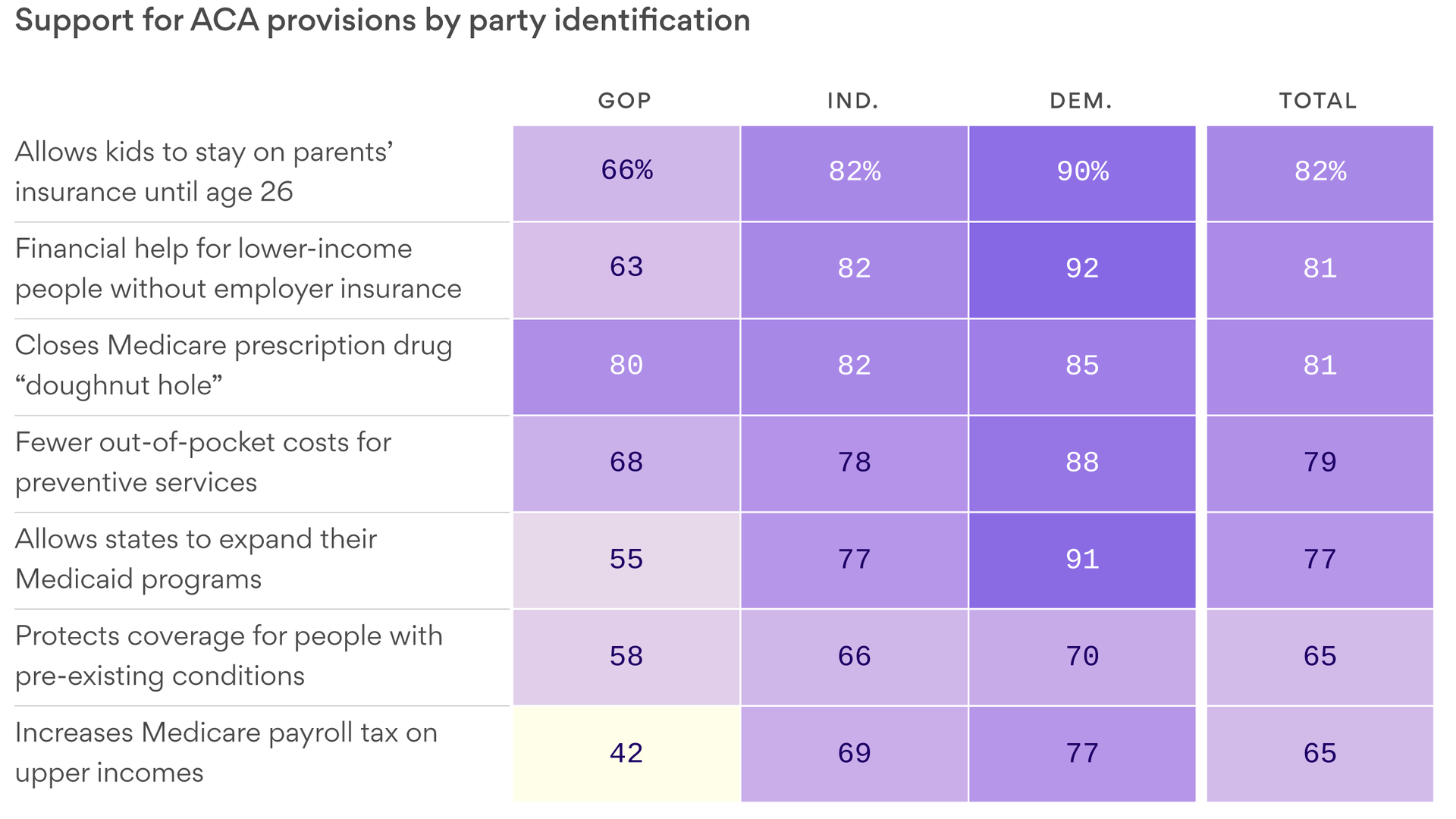

Without the ACA, patients would no longer have protections for pre-existing conditions, children would no longer have coverage under their parents’ health insurance plan until age 26, insurers would no longer be held to the 85 percent medical loss ratio, 100 percent coverage for certain preventive services would cease and individual marketplace and subsidies based on income would be eliminated.

Also, federal funding for Medicaid expansion would end.

TREND

Republicans under President Trump have tried unsuccessfully to repeal and replace the law.

The lawsuit, brought by 19 Republican governors, puts the GOP in a political bind over supporting the repeal of a law that is popular with consumers and their constituents. President Donald Trump recently said Republicans would unveil an ACA replacement after the 2020 election.

Democrats are also facing a crisis within their party over healthcare as it becomes a priority issue in the presidential election. Some of the leading candidates, such as Senator Kamala Harris, support Medicare for all. The Medicare for All Act of 2019 has been introduced in the Democratic-led House of Representatives.

Veteran politician and attorney Earl Pomeroy said he believes the Texas versus United States appeal changes the political course for 2020. The entire MFA argument will move to the back burner because of the Texas lawsuit, he said.

“The fight is going to be trying to underscore the Congressional importance of the provisions of the ACA and enhancing them,” Pomeroy said. “I do not believe that supporting Medicare for all is an advantageous position for a Democratic candidate running in a district that is not a secure Democratic seat. I believe Kamala Harris will spend much of the campaign walking back her comments on health insurance.”

Pomeroy is a former member of the U.S. House of Representatives for North Dakota’s at-large district, a North Dakota Insurance Commissioner and senior counsel in the health policy group with Alston & Bird.

“The safe political ground is defending a law people have warmed up to,” he said. “All politics is local but all healthcare is personal. There is little risk tolerance in the middle class for bold experiments in healthcare.”

BACKGROUND

The lawsuit was brought by Texas and the 19 other Republican-led states, based on the end of the individual mandate. In February, U.S. District Court Judge Reed O’Connor agreed that the federal law cannot stand without the individual mandate because if there is no penalty for not signing up for coverage, then the rest of the law is unconstitutional.

Twenty-one Democratic attorneys general appealed and the House of Representatives has intervened to defend the ACA in the case.

Either outcome in the appeals court may see the case headed to the U.S. Supreme Court.

WHAT THE PROVIDERS AND INSURERS ARE TELLING THE COURT

In a court brief filed by the AHA, the Federation of American Hospitals, The Catholic Health Association of the United States, America’s Essential Hospitals, and the Association of American Medical Colleges urged the Fifth Circuit Court of Appeals to reject a district court decision they said would have a harmful impact on the American healthcare system.

“Those without insurance coverage forgo basic medical care, making their condition more difficult to treat when they do seek care. This not only hurts patients; it has severe consequences for the hospitals that provide them care. Hospitals will bear a greater uncompensated-care burden, which will force them to reallocate limited resources and compromise their ability to provide needed services,” they said.

In a separate friend-of-the-court brief, 24 state hospital associations also urged the Fifth Circuit to reverse, highlighting specific innovative programs and initiatives for more coordinated care.

The American Medical Association, the American College of Physicians, American Academy of Family Physicians, American Academy of Pediatrics and the American Psychiatric Association filed a brief. AMA President Dr. Barbara L. McAneny said, “The district court ruling that the individual mandate is unconstitutional and inseverable from the remainder of the ACA would wreak havoc on the entire healthcare system, destabilize health insurance coverage, and roll back federal health policy to 2009. The ACA has dramatically boosted insurance coverage, and key provisions of the law enjoy widespread public support.”

AHIP said the law impacts not only the individual and group markets, but also other programs such as Medicaid, Medicare and Part D coverage.

“Since its passage in 2010, the ACA has transformed the nation’s healthcare system,” AHIP said. “It has restructured the individual and group markets for purchasing private health care coverage, expanded Medicaid, and reformed Medicare. Health insurance providers (like AHIP’s members) have invested immense resources into adjusting their business models, developing new lines of business, and building products to implement and comply with those reforms.”

The only plausible explanation for President Trump’s renewed effort through the courts to do away with the Affordable Care Act, other than muscle memory, is a desire to play to his base despite widely reported misgivings in his own administration and among Republicans in Congress.

Reality check: But the Republican base has more complicated views about the ACA than the activists who show up at rallies and cheer when the president talks about repealing the law. The polling is clear: Republicans don’t like the ACA, but just like everyone else, they like its benefits and will not want to lose them.

After repeatedly trying and failing to repeal the ACA legislatively, President Trump and congressional Republicans have resorted to attacking and weakening the law through executive action, federal waivers to the states to undermine Medicaid expansion, and budget proposals to gut funding levels.

Once again, Trump’s budget proposes massive cuts—$777 billion over 10 years—from repealing the ACA and slashing Medicaid.

Like in his previous two budgets, Trump goes beyond these two measures to attack traditional Medicaid, seeking to restrict federal funding on a per-beneficiary basis or transition to block grant funding. Both of these things would lead to a significant decrease in federal funding and could cause millions of people to lose their health care coverage.

Like in last year’s budget, he encourages states to take Medicaid away from jobless and underemployed Americans, including laid-off workers, people who are going to school, and those who are taking care of children or family members. Medicaid is a lifeline for millions of Americans—including children, veterans, people with disabilities, and individuals affected by the opioid crisis. Tearing down this vital program will make it more difficult for people to access the health care they need to find work, including by preventing people with disabilities from accessing the long-term services and supports they need to participate in the labor market.

After he repeatedly promised to protect Medicare as a candidate, Trump makes changes to Medicare that would shrink the program by $845 billion over the coming decade.