Self-dealing is illegal in banks, real estate, and investment firms, but in health insurance, it’s not only legal, it’s widespread. Large insurers have spent decades consolidating the U.S. health care system, acquiring medical practices, pharmacies, and pharmacy benefit managers, all while sidestepping rules meant to protect patients and taxpayers.

For example, UnitedHealth Group has 2,694 subsidiaries, as documented in the Center for Health and Democracy’s Sunlight Report on UnitedHealth Group. Within this conglomerate, there are 589 clinician practice locations across 32 states acquired between 2007 and 2023. UnitedHealth Group also has 24 subsidiary pharmacy benefit managers and over 30 subsidiary pharmacies. Data and insider accounts suggest that UnitedHealth Group and other vertically integrated insurers engage in self-dealing to increase profits. The ways these subsidiaries interact closely resembles self-dealing practices that are prohibited by law in other industries, such as banking, real estate, and investment firms.

As Dr. Seth Glickman and I have explained in earlier pieces, when a health insurer owns or controls medical practices, pharmacy benefit managers, or pharmacies, it can circumvent medical loss ratio (MLR) regulations. MLR rules require insurance companies to spend 80–85% of premium dollars on medical costs, leaving the remainder for administrative fees and profits. Unitedhealth Group, for instance, reportedly pays its own subsidiary providers above-market rates for medical services. These payments count as “medical costs” under MLR rules, yet the subsidiaries retain the excess as profit. Similarly, when a patient uses Optum Rx, a UnitedHealth Group subsidiary, or a subsidiary pharmacy, the fees added by the PBM are counted as medical costs, even though they are retained as profit by the parent company.

In banking, such actions are expressly prohibited. Consider a bank CEO who owns a real estate development company and seeks a loan for a risky project. If the bank lends to the CEO’s company at a below-market interest rate, the loan violates federal law and could trigger millions in fines as well as civil and criminal charges for both the CEO and the bank. This scenario parallels UnitedHealth Group’s current operations. In both cases, customer money (depositor funds in a bank; premium dollars in insurance) is used to funnel profit to insiders or affiliates, bypassing the market discipline that governs arm’s-length transactions.

Real estate law similarly prohibits self-dealing. Imagine a real estate agent hired to sell a client’s home who secretly buys the property through an affiliate at a lower price than the market reflects. By underrepresenting the home’s value, the agent enriches themselves at the client’s expense. This violates state real estate laws and common law fiduciary duties. The parallel in Insurance is clear: insurers pay inflated prices to their owned practices, driving up care costs and premiums. In both cases, the fiduciary is using client assets (property or premium dollars) to generate hidden profits for themselves or their affiliates, avoiding fair-market competition.

Investment advisers are also prohibited from similar practices. If you hire a broker to get the best price for a stock trade, the broker cannot quietly route the trade to an affiliate at a worse price so the affiliate profits. Even small losses per trade scale into substantial gains for the broker’s affiliate, all at the client’s expense. These actions violate the Investment Advisers Act of 1940, the Securities Exchange Act of 1934, and SEC rules when proper disclosure or consent is not obtained. Similarly, insurers use premium dollars to channel profits to subsidiaries instead of relying on competitive market pricing.

The stark parallels between self-dealing in banks, real estate, and investment brokerages, which Congress regulated decades ago, and health insurance are damning. Health insurance conglomerates have built empires on paying themselves to the detriment of patients and taxpayers. Congress must act to regulate this type of self-dealing in insurance as it does in other industries.

Moreover, the depth of insurer control over the patient care system necessitates regulations to prevent vertical monopolies, where insurers dominate every stage of care delivery.

Imagine you’re facing your midyear performance review with your boss. You dread it, even though you’ve done all you thought possible and legal to help the company meet Wall Street’s profit expectations, because shareholders haven’t been pleased with your employer’s performance lately.

Now let’s imagine your employer is a health insurance conglomerate like, say, UnitedHealth Group. You’ve watched as the stock price has been sliding, sometimes a little and on some days crashing through lows not seen in years, like last Friday (down almost 5% in a single day, to $237.77, which is down a stunning 62% since a mid-November high of $630 and change).

You know what your boss is going to say. We all have to do more to meet the Street’s expectations. Something has changed from the days when the government and employers were overly generous, not questioning our value proposition, always willing to pick up the tab and pay many hidden tips, and we could pull our many levers to make it harder for people to get the care they need.

Despite government and media reports for years that the federal government has been overpaying Medicare Advantage plans like UnitedHealth’s – at least $84 billion this year alone – Congress has pretended not to notice. There is evidence that might be changing, with Republicans and Democrats alike making noises about cracking down on MA plans.

Employers have complained for ages about constantly rising premiums, but they’ve sucked it up, knowing they could pass much of the increase onto their workers – and make them pay thousands of dollars out of their own pockets before their coverage kicks in. Now, at least some of them are realizing they don’t have to work with the giant conglomerates anymore.

Doctors and hospitals have complained, too, about burdensome paperwork and not getting paid right and on time, but they’ve largely been ignored as the big conglomerates get bigger and are now even competing with them.

UnitedHealth is the biggest employer of doctors in the country. But doctors and hospitals are beginning to push back, too.

Since last fall, UnitedHealth and its smaller but still enormous competitors have found that “headwinds” are making it harder for them to maintain the profit margins investors demand. That is mainly because, despite the many barriers patients have to overcome to get the care they need, many of them are nevertheless using health care, often in the most expensive setting – the emergency room. They put off seeing a doctor so long because of insurers’ penny-wise-pound-foolishness that they had some kind of event that scared them enough to head straight to the ER.

It’s not just you who is dreading your midyear review. Everybody, regardless of their position on the corporate ladder, and even the poorly paid folks in customer service, are in the same boat. And so is your boss. Nobody will put the details of what has to be done in writing. They don’t have to. Your boss will remind you that you have to do your part to help the company achieve the “profitable growth” Wall Street demands, quarter after quarter after quarter. It never, ever ends. You know this because you and most other employees watch what happens after the company releases quarterly financials. You also watch your 401K balance and you see the financial consequences of a company that Wall Street isn’t happy with. And Wall Street is especially unhappy with UnitedHealth these days.

And when things are as bad as they are now at UnitedHealth’s headquarters in Minnesota, you know that a big consulting firm like McKinsey & Company has been called in, and that those suits will recommend some kind of “restructuring” and changes in leadership to get the ship back on course. You know the drill. Everybody already is subject to forced ranking, meaning that at the end of the year, some of your colleagues, regardless of job title, will fall below a line that means automatic termination. You pedal as fast as you can to stay above that line, often doing things you worry are not in the best interest of millions of people and might not even be lawful. But you know that if you have any chance of staying employed, much less getting a raise or bonus, you have to convince your superiors you are motivated and “engaged to win.” No one is safe. Look what happened to Sir Andrew Witty, whose departure as CEO to spend more time with his family (in London) was announced days after shareholders turned thumbs down on the company’s promises to return to an acceptable level of profitability.

If you are at UnitedHealth, you listened to what the once and again CEO, Stephen Hemsley, and CFO John Rex, who got shuffled to a lesser role of “advisor” to the CEO last week, laid out a new action plan to their bosses – big institutional investors who have been losing their shirts for months now. You know that what the C-Suite promised on their July 29 call will mean that you will have to “execute” to enable the company to deliver on those promises. And you know that you and your colleagues will have to inflict a lot more pain on everybody who is not a big shareholder – patients, taxpayers, employers, doctors, hospital administrators. That is your job. And you will try to do it because you have a mortgage, kids in college and maxed-out credit cards.

Here’s what Hemsley and his leadership team said, out loud in a public forum, although admittedly one that few people know about or can take an hour-and-a-half to listen to:

Even though UnitedHealth took in billions more in revenue, its margins shrank a little because it had to pay more medical claims than expected.

Still, the company made $14.3 billion in profits during the second quarter. That’s a lot but not as much as the $15.8 billion in 2Q 2024, and that made shareholders unhappy.

Enrollment in its commercial (individual and employer) plans increased just 1%, but enrollment in its Medicare Advantage plans increased nearly 8%. That’s normally just fine, but something happened that the company’s beancounters couldn’t stop.

Those seniors figured out how to get at least some care despite the company’s high barriers to care (aggressive use of prior authorization, “narrow” networks of providers, etc.)

To fix all of this, Hemsley and team promised:

To dump 600,000 or so enrollees who might need care next year

To raise premiums “in the double digits” – way above the “medical trend” that PriceWaterhouseCoopers predicts to be 8.5% (high but not double-digit high)

Boot more providers it doesn’t already own out of network

Reduce benefits

Throughout the call with investors (actually with a couple dozen Wall Street financial analysts, the only people who can ask questions), Hemsley and team went on and on about the “value-based care” the company theoretically delivers, without providing specifics. But here is what you need to know: If you are enrolled in a UnitedHealth plan of any nature – commercial, Medicare or Medicaid or VA (yes, VA, too) – expect the value of your coverage to diminish, just as it has year after year after year.

The term for this in industry jargon is “benefit buydown.”

That means that even as your premiums go up by double digits, you will soon have fewer providers to choose from, you likely will spend more out-of-pocket before your coverage kicks in, you might have to switch to a medication made by a drug company UnitedHealth will get bigger kickbacks from, and you might even be among the 600,000 policyholders who will get “purged” (another industry term) at the end of the year.

Why do we and our employers and Uncle Sam keep putting up with this?

Yes, we pay more for new cars and iPhones, but we at least can count on some improvements in gas mileage and battery life and maybe even better-placed cup holders. You can now buy a massive high-def TV for a fraction of what it cost a couple of years ago. Health insurance? Just the opposite.

As I will explain in a future post, all of the big for-profit insurers are facing those same headwinds UnitedHealth is facing. You will not be spared regardless of the name on your insurance card. If you still have one come January 1. Pain is on the way. Once again.

In a concession to Wall Street investors, starting this summer, UnitedHealth will stop paying commissions to agents and brokers for some new enrollees in nearly 200 UnitedHealthcare Medicare Advantage plans across 39 markets.

And it’s happening not because UnitedHealth can’t afford to pay.As we’ve published previously, the company reported $9.1 billion in profits during the first quarter of 2025 — up from $7.9 billion the year before. But that wasn’t enough to satisfy Wall Street, which punished UnitedHealth with the steepest one-day stock drop in 26 years — a $110 billion free fall in market value — after the company revised its full-year profit guidance downward.

Why the drop?

Because UnitedHealth admitted it may not squeeze quite as much profit from taxpayers this year as expected — mainly due to unexpectedly high care utilization from some of the new Medicare Advantage enrollees it brought on during the last open enrollment period. Particularly enrollees who, as then-CEO Andrew Witty described, came from other insurers exiting the market and hadn’t been properly coded. Yawn.

For Now, Brokers Are UNH’s Patsy

This recent commission cut is less about operational efficiency and more about damage control. UnitedHealth is signaling to investors that it’s willing to shrink its Medicare Advantage footprint — at least temporarily — if that helps preserve profit margins. And Wall Street analysts are eating it up, seeing it as a way to slow the flow of high-cost members and stabilize earnings, according to BarChart.

Off Wall Street, the move has already come under fire. As the National Association of Benefits and Insurance Professionals put it, UnitedHealth is “cutting off the very people best equipped to help” seniors — especially low-income and rural enrollees who depend on brokers to explain their options.

While we would warn seniors against enrolling in a Medicare Advantage plan in the first place – without brokers, many beneficiaries will be left to fend for themselves in a system that’s already infamously confusing, expensive and deadly.

A Strategic Retreat Disguised as a Cost-Containment Strategy

The problem is the perverse incentive structure UnitedHealth and other insurers helped build — one that rewards risk-coding gamesmanship more than it rewards delivering care. For years, the company thrived by maximizing revenue through “coding intensity” and by acquiring everything from doctors’ offices to behavioral health firms to control more of the health care ecosystem.

Now, UnitedHealth is responding the way Wall Street expects: by slashing anything that isn’t bolted down – including brokers.

So here we are:

UnitedHealth is still wildly profitable, still drawing billions from taxpayer-funded programs like Medicare and Medicaid — and now it’s cutting out the professionals who presumably help seniors navigate a convoluted health care system. All this, mind you, to appease jittery investors. And despite UnitedHealth’s current wobbly share price, analysts expect it to rebound, especially with a continuation of share buybacks on the horizon.

During the first quarter of this year alone, the company bought back $3 billion worth of its own shares. Over the past year, buybacks totaled more than $12 billion. When you factor in dividends, the company said it “returned” more than $16 billion to shareholders in 2024. That’s how you keep investors at least partially satisfied.

Last week, I made my once a decade trek to a dealership to buy a new car. I did my research in advance (and even negotiated the price) so I was hoping for a stress-free experience.

It was – up until the point where I got locked in the finance manager’s office for “the talk”. You know, the one where you are made to feel like a neglectful parent unless you pony up for all the fixin’s – everything from nitrogen filled tires to paint protection (just in case I encounter a flock of migratory geese on the drive home). I shook my head no about ten times before we got to the pre-paid maintenance plan options. I decided to be polite and listen (plus I was curious since I was purchasing a car from a manufacturer notorious for costly repairs). As compelling as it was to pay nearly $5,000 to what ultimately would amount to a few tire rotations for my electric vehicle, I held firm. The finance manager angrily handed me my signed documents and whisked me out of his office.

I guess I can’t blame car dealers for applying massive mark-ups for services that are inexpensive to provide. Except similar financial chicanery is currently playing out in our health insurance system. If you swap out the finance manager for a health insurer and replace me with the average everyday consumer, the dealer’s tactics are analogous to how insurers game medical loss ratio (MLR) requirements (except as a health care consumer, you can’t say “no”).

A bit of background is in order to understand why I thought about health insurance and car dealers in the same breath.

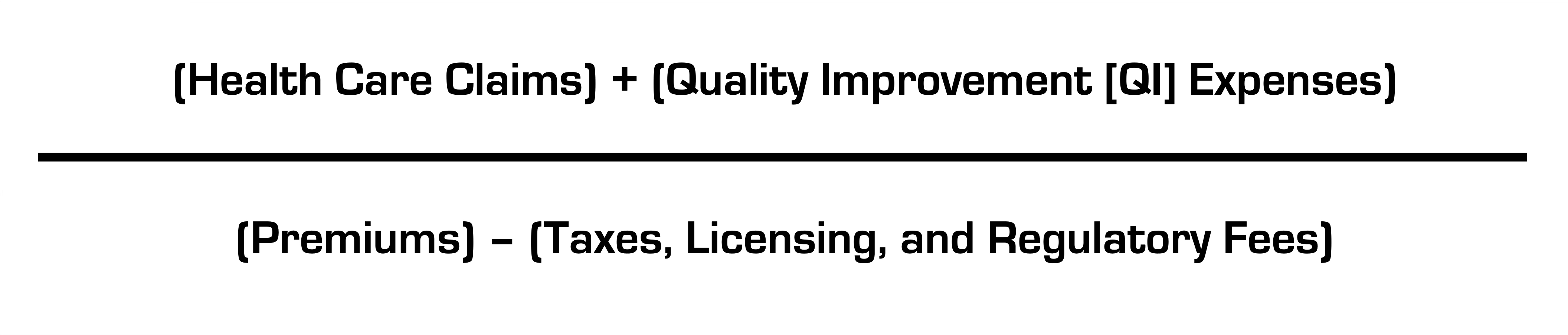

Insurance companies are required to spend a certain percentage of money they get from premiums on medical costs and quality improvement (QI); this is known as the medical loss ratio (MLR). If companies do not meet this ratio (usually 80-85%, depending on the product), they must refund the difference in the form of a rebate, or reduction in future premiums, to consumers.

Like any for-profit corporation in America today, a health insurer wants to avoid giving money back to consumers. Therefore, insurers have become adept at manipulating their MLRs through various accounting and financial engineering techniques. This manipulation optimizes their ability to meet MLR thresholds and avoid paying rebates, which runs afoul of its intended purpose: to ensure that patients receive the appropriate level of care.

So how do insurers game the system, and what evidence exists for this activity?

The current MLR formula is:

Health insurers do not control taxes and fees, but they can easily engineer the other variables. Below, I’ll explain how.

Step 1: Quality Improvement (QI) Expenses

The definition of allowable QI expenses is broad and includes activities to improve outcomes, patient safety, and reduce mortality (mom and apple pie stuff). Insurers played a big role in writing the MLR regulations after Congress enacted legislation and made sure they’d have wide latitude in what expenses are classified as QI (akin to the car dealer “option” list) and what product segments they assign them to.

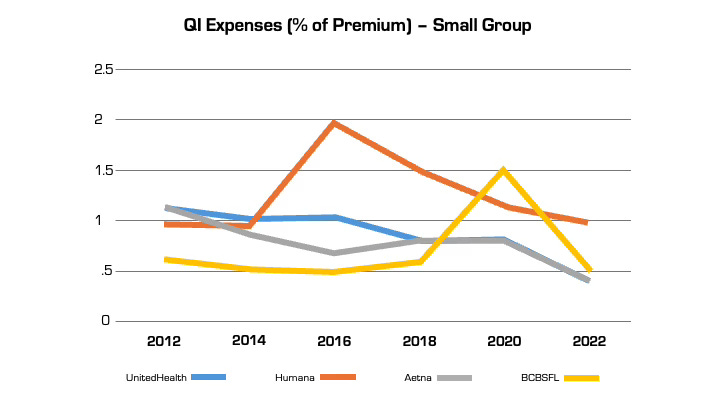

Looking at reported QI expenses sheds light on this practice. QI expenses vary between insurers. But they also vary widely for the same insurer from year to year (even after controlling for geography and product segment). In large part, this is attributable to financial engineering. QI costs can be effectively “transferred” on the income statement from one product segment to another, by adjusting the pro rata weightings). This enables them to optimize MLR performance across their insurance portfolio (i.e. by taking from a bucket with excess medical costs and putting it in another with insufficient costs) in a way that maximizes benefit to the insurer and is camouflaged from regulators and consumers. This is language from a recent UnitedHealth Group filing with the Securities and Exchange Commission: “Assets and liabilities jointly used are assigned to each reportable segment using estimates of pro-rata usage.”

Annual QI expenses across four insurers in Florida in the small group market.

Although these QI percentages are small, the associated dollar amounts are large. In 2022, UnitedHealth, Humana, and Aetna reported $494 million, $550 million, and $395 million respectively in allowable QI expenses for their national plans. While there is some legitimate QI activity at insurers (e.g., pharmacists who identify high risk medications in the elderly), the reality is that much of the QI work is already heavily resourced within provider organizations, where it is more effective. Insurers also can (and do) count “wellness and health promotion activities” despite limited evidence these programs improve health outcomes and are more often used by insurers as marketing tools.

Step 2. Health Care Claims

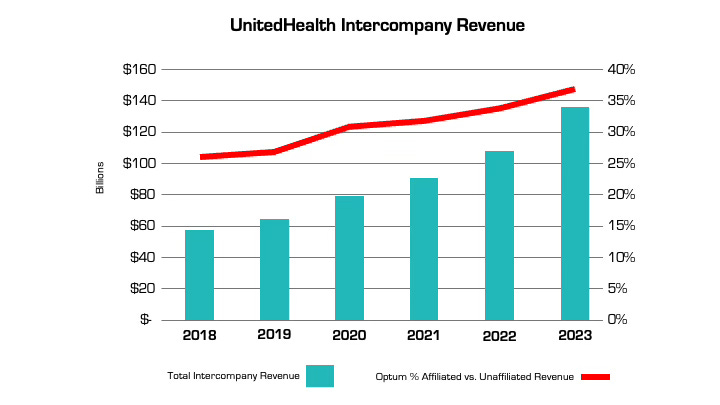

The other variable that insurers can manipulate is claims costs. The more an insurer is vertically integrated, the easier it is. The prime example is UnitedHealth, which has an insurance arm (UnitedHealthcare) and a big division that encompasses medical services, among many other things (Optum), as well as various other subsidiaries. Optum Health and Optum Rx receive a significant portion of their revenue from UnitedHealthcare for providing services like care and pharmacy benefit management to people enrolled in its health plans. In fact, the amount of UnitedHealth’s corporate “eliminations,” (meaning inter-company revenue that is reported on their consolidated financial statement) has more than doubled over the past five years (from $58.5 billion to $136.4 billion). The proportion of revenue Optum derives from UnitedHealthcare versus unaffiliated entities has increased by nearly 50% over the same period. A similar trend is playing out at every major insurer.

Take the example of the insurance company Aetna, the PBM CVS Caremark, and CVS Pharmacy, which are all vertically integrated and owned by CVS Health. If a patient goes to a CVS store to fill a prescription for Imatinib, a generic chemotherapy drug, the total cost the patient and insurance company pay is $17,710.21 for a 30-day supply. The same drug is sold by Cost Plus Drugs for $72.20 (the cost is calculated by adding the wholesale price and a 15% fee). When the patient fills the prescription at a CVS retail pharmacy, CVS Health can record that the patient paid a medical claim cost of $17,710.21 (even though the cost to acquire the drug is $70) and the remaining $17,640 can be retained as profits disguised as medical costs.

Insurers’ extensive acquisition of physician practices also facilitates gamification of the MLR via its ability to pay capitation (a set amount per person) to a risk-bearing provider organization (RBO) it owns, such as a medical group. This enables the insurer to lock in a set amount of premium as “medical expense” (usually around 85%) with the downstream provider group “managing” those costs. There’s a loophole, however. While the insurer has technically met its MLR requirement, the downstream RBO is subject to far fewer regulations on how it spends the money, which makes it easier to generate profits by skimping on care.

The regulations on RBOs vary by state. In many cases, while RBOs need to meet minimum capital requirements, they are not subject to the same MLR provisions as insurers. For a vertically integrated insurer that gets a huge amount of revenue from taxpayer-supported programs like Medicare Advantage and Medicaid, this essentially means that (1) the Center for Medicare and Medicaid Services puts the money into the insurer’s right pocket, (2) the insurer moves it to the left pocket, and (3) CMS checks the right pocket – and just the right pocket – at the end of the year to make sure it’s mostly empty (without regard to the fact that the left one may be busting at the seams).

The good news is there are ways to address these issues, both through updating the MLR provisions in the Affordable Care Act (which are long in the tooth) and more rigorous and comprehensive reporting requirements and regulation of vertically integrated insurers.

Just like I don’t want car dealers pushing unnecessary add-ons to increase their profit margins, consumers deserve that the required portion of their hard spent premium dollar actually goes toward their health care instead of further enriching huge corporations, executives, and Wall Street shareholders.

UnitedHealth executives made a valiant attempt yesterday to persuade investors that they have figured out how to improve customer service and keep Congress and the incoming Trump administration from passing laws that could shrink the company’s profit margins – and maybe even the company itself – but Wall Street wasn’t buying.

During their first call with investors since the murder of UnitedHealthcare CEO Brian Thompson, the company’s top brass pointed the finger of blame for rising health care costs everywhere but at themselves – primarily at hospitals and pharmaceutical companies – and made statements that simply were not true. Investors clearly did not find their comments reassuring or credible. By the end of the day shares of UnitedHealth’s stock were down more than 6% to $510.59. That marked a continuation of a slide that began after the stock price peaked at $630.73 on November 11 – a decline of almost 20%.

In a little more than two months, the company has lost an astonishing $110 billion in market capitalization, and shareholders have lost an enormous amount of the money they invested in UnitedHealth.

Earlier yesterday morning, the company released fourth-quarter and full-year 2024 earnings, which were slightly higher on a per share basis than Wall Street financial analysts had expected: $6.81 per share in the fourth quarter compared to analysts’ consensus estimate of $6.73 for the quarter. But the company posted lower revenue during the last three months of 2024 than analysts had expected. While revenue was up 7% over the same quarter in 2023, to $100.8 billion, analysts had expected revenue to grow to $101.6 billion.

And on a full-year basis, the company’s net profits fell an eye-popping 36%, from $22.4 billion in 2023 to $14.4 billion last year.

Bottom line: the company, which until last year had grown rapidly, actually shrank in some respects, especially in the division that operates the company’s health plans. UnitedHealthcare, which Thompson led, saw its revenue increase slightly but its profits fall. The other big division, Optum, which among other things owns and operates numerous physician practices and clinics and one of the country’s largest pharmacy benefit managers (PBMs), fared much better.

While Optum’s 2024 revenue was lower than UnitedHealthcare’s ($253 billion and $298 respectively), it made far more in profits on an operating basis ($16.7 billion and $15.6 respectively).

Optum’s operating profit margin was 6.6% while UnitedHealthcare’s was 5.2%.

The company’s executives blamed higher health care utilization, especially by people enrolled in its Medicare Advantage plans, for the decline in profits.

Witty and CFO John Rex pointed the finger of blame at hospitals and drug companies for rising medical prices. And they obscured the huge amounts of money the company’s PBM, Optum Rx, extracts from the pharmacy supply chain. While the company chose not to break out exactly how much of Optum’s revenues of $298 billion came from Optum Rx, it appears that more than half of it was contributed by the PBM. The company did note that Optum Rx revenues increased 15% during 2024.

Nevertheless, Witty and Rex blamed drug makers for high prices.

They also said that they would be changing the PBM’s business practices to pass through rebate discounts from drug makers to its customers, claiming that it already passes through 98% of them and will reach 100% by 2028. That clearly was a talking point aimed at Washington, where there is significant bipartisan support for legislation that would require all PBMs to do so. Despite UnitedHealth’s claim, there is no external verification to back up that they are passing 98% of rebates back to customers.

Another claim the executives made that is not true is that the Medicare Advantage program saves taxpayers money. Numerous government reports have shown the opposite, that the federal government spends considerably more on people enrolled in Medicare Advantage plans than those enrolled in the traditional Medicare program.

Reports have estimated that UnitedHealthcare, which is the largest Medicare Advantage company, and other MA plans are overpaid between $80 billion and $140 billion a year.

There is also growing bipartisan support to reform the Medicare Advantage program to reduce both the overpayments and the excessive denials of care at UnitedHealthcare and other MA insurers.

While company executives might be hoping that their fortunes will improve during the second Trump administration, Trump recently joined some Republican members of Congress, like Rep. Buddy Carter of Georgia, who are calling for significant reforms, especially to pharmacy benefit managers.

At a news conference last month, Trump promised to “knock out” those middlemen in the pharmacy supply chain.

“We are paying far too much, because we are paying far more than other countries,” he said. “We have laws that make it impossible to reduce [drug costs] and we have a thing called a ‘middleman’ … that makes more money than the drug companies, and they don’t do anything except they’re middlemen. We are going to knock out the middleman.”

A major health insurance company is backing off of a controversial plan to limit coverage of anesthesia, according to public officials.

Why it matters:

Anthem Blue Cross Blue Shield recently decided to “no longer pay for anesthesia care if the surgery or procedure goes beyond an arbitrary time limit, regardless of how long the surgical procedure takes,” according to the American Society of Anesthesiologists, which opposed the decision.

The decision was based on surgery time metrics from federal health data, NPR reported.

The policy applied to plans in Connecticut, New York and Missouri.

The latest:

“After hearing from people across the state about this concerning policy, my office reached out to Anthem, and I’m pleased to share this policy will no longer be going into effect here in Connecticut,” Connecticut Comptroller Sean Scanlon said Thursday on X.

Shortly afterward, New York Gov. Kathy Hochul issued a statement saying, “We pushed Anthem to reverse course and today they will be announcing a full reversal of this misguided policy.”

What they’re saying:

The initial coverage decision was very unusual for a major health insurer, said Marianne Udow-Phillips, who teaches insurance classes at the University of Michigan School of Public Health and formerly made coverage decisions at Blue Cross Blue Shield of Michigan.

The big picture:

Anthem’s initial decision was controversial at the time — but outrage erupted this week after the murder of UnitedHealthcare CEO Brian Thompson in New York City cast a spotlight on divisive insurance decisions.

On social media, critics of health insurers drew a direct line from controversial coverage decisions to the death of Thompson.

UnitedHealth Group has taken a beating on Wall Street this week after admitting that its Medicare Advantage plans had to pay out more in medical claims in the third quarter of this year than investors had expected. As I’ve noted many times, Wall Street can’t stand it and gets very spiteful when Big Insurance uses more of our premium dollars paying for patients’ care because that means there’s less money left over to enrich shareholders.

At the end of trading at the New York Stock Exchange Tuesday, UnitedHealth’s share price was down 8.11% — almost $50 a share — falling like a rock from $605.40 to $556.29 as soon as the market opened. It had reached a 52-week high just the day before but fell off a cliff Tuesday morning. This despite the fact that the company still made $8.7 billion in operating profits during the third quarter.

What investors didn’t like at all was the fact that UnitedHealthcare’s medical loss ratio (MLR) climbed to 85.2% from 82.3% for the same period last year.

By other measures, the company did just fine, especially when you look at how much money it made during the first nine months of this year: a whopping $24.5 billion in profits.

Enrollment in both the company’s commercial and Medicare Advantage plans increased, but it posted a significant decline in the number of people enrolled in the Medicaid plans its administers for several states. That’s because of the Medicaid “unwinding” that has been going on since the official end of the pandemic.

And here is another couple of numbers of note from the third quarter:

UnitedHealth’s Optum division, which encompasses its massive pharmacy benefit manager, Optum Rx, made more money for the parent company than the health plan division: $4.5 billion in profits vs. $4.2 billion for UnitedHealthcare.

PBMs have become even more of a cash cow for Big Insurance than Medicare Advantage, which despite the higher MLRs of late is still a reliable money-gushing ATM for the industry.

Health policy and politics are inextricably linked. Policy is about what the government can do to shift the financing, delivery, and quality of health care, so who controls the government has the power to shape those policies.

Elections, therefore, always have consequences for the direction of health policy – who is the president and in control of the executive branch, which party has the majority in the House and the Senate with the ability to steer legislation, and who has control in state houses. When political power in Washington is divided, legislating on health care often comes to a standstill, though the president still has significant discretion over health policy through administrative actions. And, stalemates at the federal level often spur greater action by states.

Health care issues often, but not always, play a dominant role in political campaigns. Health care is a personal issue, so it often resonates with voters. The affordability of health care, in particular, is typically a top concern for voters, along with other pocketbook issues, And, at 17% of the economy, health care has many industry stakeholders who seek influence through lobbying and campaign contributions. At the same time, individual policy issues are rarely decisive in elections.

Health “reform” – a somewhat squishy term generally understood to mean proposals that significantly transform the financing, coverage, and delivery of health care – has a long history of playing a major role in elections.

Harry Truman campaigned on universal health insurance in 1948, but his plan went nowhere in the face of opposition from the American Medical Association and other groups. While falling short of universal coverage, the creation of Medicare and Medicaid in 1965 under Lyndon Johnson dramatically reduced the number of uninsured people. President Johnson signed the Medicare and Medicaid legislation at the Truman Library in Missouri, with Truman himself looking on.

Later, Bill Clinton campaigned on health reform in 1992, and proposed the sweeping Health Security Act in the first year of his presidency. That plan went down to defeat in Congress amidst opposition from nearly all segments of the health care industry, and the controversy over it has been cited by many as a factor in Democrats losing control of both the House and the Senate in the 1994 midterm elections.

For many years after the defeat of the Clinton health plan, Democrats were hesitant to push major health reforms. Then, in the 2008 campaign, Barack Obama campaigned once again on health reform, and proposed a plan that eventually became the Affordable Care Act (ACA). The ACA ultimately passed Congress in 2010 with only Democratic votes, after many twists and turns in the legislative process. The major provisions of the ACA were not slated to take effect until 2014, and opposition quickly galvanized against the requirement to have insurance or pay a tax penalty (the “individual mandate”) and in response to criticism that the legislation contained so-called “death panels” (which it did not). Republicans took control of the House and gained a substantial number of seats in the Senate during the 2010 midterm elections, fueled partly by opposition to the ACA.

The ACA took full effect in 2014, with millions gaining coverage, but more people viewed the law unfavorably than favorably, and repeal became a rallying cry for Republicans in the 2016 campaign. Following the election of Donald Trump, there was a high profile effort to repeal the law, which was ultimately defeated following a public backlash. The ACA repeal debate was a good example of the trade-offs inherent in all health policies. Republicans sought to reduce federal spending and regulation, but the result would have been fewer people covered and weakened protections for people with pre-existing conditions. KFF polling showed that the ACA repeal effort led to increased public support for the law, which persists today.

The 2024 election presents the unusual occurrence of two candidates – current vice president Kamala Harris and former president Donald Trump – who have already served in the White House and have detailed records for comparison, as explained in this JAMA column. With President Joe Biden dropping out of the campaign, Harris inherits the record of the current administration, but has also begun to lay out an agenda of her own.

While Trump failed as president to repeal the ACA, his administration did make significant changes to it, including repealing the individual mandate penalty, reducing federal funding for consumer assistance (navigators) by 84% and outreach by 90%, and expanding short-term insurance plans that can exclude coverage of preexisting conditions.

In a strange policy twist, the Trump administration ended payments to ACA insurers to compensate them for a requirement to provide reduced cost sharing for low-income patients, with Trump saying it would cause Obamacare to be “dead” and “gone.” But, insurers responded by increasing premiums, which in turn increased federal premium subsidies and federal spending, likely strengthening the ACA.

In the 2024 campaign, Trump has vowed several times to try again to repeal and replace the ACA, though not necessarily using those words, saying instead he would create a plan with “much better health care.”

Although the Trump administration never issued a detailed plan to replace the ACA, Trump’s budget proposals as president included plans to convert the ACA into a block grant to states, cap federal funding for Medicaid, and allow states to relax the ACA’s rules protecting people with preexisting conditions. Those plans, if enacted, would have reduced federal funding for health care by about $1 trillion over a decade.

In contrast, the Biden-Harris administration has reinvigorated the ACA by restoring funding for consumer assistance and outreach and by increasing premium subsidies to make coverage more affordable, resulting in record enrollment in ACA Marketplace plans and historically low uninsured rates. The increased premium subsidies are currently slated to expire at the end of 2025, so the next president will be instrumental in determining whether they get extended. Harris has vowed to extend the subsidies, while Trump has been silent on the issue.

The health care issue most likely to figure prominently in the general election is abortion rights, with sharp contrasts between the presidential candidates and the potential to affect voter turnout. In all the states where voters have been asked to weigh in directly on abortion so far (California, Kansas, Kentucky, Michigan, Montana, Ohio, and Vermont), abortion rights have been upheld.

Trump paved the way for the US Supreme Court to overturn Roe v Wade by appointing judges and justices opposed to abortion rights. Trump recently said, “for 54 years they were trying to get Roe v Wade terminated, and I did it and I’m proud to have done it.” During the current campaign, Trump has said that abortion policy should now be left to the states.

As president, Trump had also cut off family planning funding to Planned Parenthood and other clinics that provide or refer for abortion services, but this policy was reversed by the Biden-Harris administration.

Harris supports codifying into federal the abortion access protections in Roe v Wade.

Addressing the High Price of Prescription Drugs and Health Care Services

Trump has often spotlighted the high price of prescription drugs, criticizing both the pharmaceutical industry and pharmacy benefit managers. Although he kept the issue of drug prices on the political agenda as president, in the end, his administration accomplished little to contain them.

The Trump administration created a demonstration program, capping monthly co-pays for insulin for some Medicare beneficiaries at $35. Late in his presidency, his administration issued a rule to tie Medicare reimbursement of certain physician-administered drugs to the prices paid in other countries, but it was blocked by the courts and never implemented. The Trump administration also issued regulations paving the way for states to import lower-priced drugs from Canada. The Biden-Harris administration has followed through on that idea and recently approved Florida’s plan to buy drugs from Canada, though barriers still remain to making it work in practice.

With Harris casting the tie-breaking vote in the Senate, President Biden signed the Inflation Reduction Act, far-reaching legislation that requires the federal government to negotiate the prices of certain drugs in Medicare, which was previously banned. The law also guarantees a $35 co-pay cap for insulin for all Medicare beneficiaries, and caps out-of-pocket retail drug costs for the first time in Medicare. Harris supports accelerating drug price negotiation to apply to more drugs, as well as extending the $35 cap on insulin copays and the cap on out-of-pocket drug costs to everyone outside of Medicare.

How Trump would approach drug price negotiations if elected is unclear. Trump supported federal negotiation of drug prices during his 2016 campaign, but he did not pursue the idea as president and opposed a Democratic price negotiation plan. During the current campaign, Trump said he “will tell big pharma that we will only pay the best price they offer to foreign nations,” claiming that he was the “only president in modern times who ever took on big pharma.”

Beyond drug prices, the Trump administration issued regulations requiring hospitals and health insurers to be transparent about prices, a policy that is still in place and attracts bipartisan support.

Ultimately, irrespective of the issues that get debated during the campaign, the outcome of the 2024 election – who controls the White House and Congress – will have significant implications for the future direction of health care, as is almost always the case.

However, even with changes in party control of the federal government, only incremental movement to the left or the right is the norm. Sweeping changes in health policy, such as the creation of Medicare and Medicaid or passage of the ACA, are rare in the U.S. political system. Similarly, Medicare for All, which would even more fundamentally transform the financing and coverage of health care, faces long odds, particularly in the current political environment. This is the case even though most of the public favors Medicare for All, though attitudes shift significantly after hearing messages about its potential impacts.

Importantly, it’s politically difficult to take benefits away from people once they have them. That, and the fact that seniors are a strong voting bloc, has been why Social Security and Medicare have been considered political “third rails.” The ACA and Medicaid do not have quite the same sacrosanct status, but they may be close.

UnitedHealth Group, the largest health insurance conglomerate by far, continues to show how rewarding it is for shareholders when corporate lawyers find loopholes in well-intentioned legislation – and game the Medicare Advantage program in ways most lawmakers and regulators didn’t anticipate and certainly didn’t intend – to boost profits.

UnitedHealth announced this morning that it made $15.8 billion in operating profits between the first of January and the end of June this year. That compares to $4.6 billion it made during the same period in 2014. One way the company is able to reward its shareholders so richly these days is by steering millions of people enrolled in its health plans to the tens of thousands of doctors it now employs and to the clinics and pharmacy operations it now owns.

This is the result of the hundreds of acquisitions UnitedHealth has made over the past 10 years in health care delivery as part of its aggressive “vertical integration” strategy.

The other big way the company has become so profitable is by rigging the Medicare Advantage program in a way that enables it to get more money from the federal government in a scheme – detailed in a big investigative report by the Wall Street Journal a few days ago – in which it claims its Medicare Advantage enrollees are sicker than they really are. The WSJ calculated that Medicare Advantage insurers bilked the government out of more than $50 billion in the three years ending in 2021 by engaging in this scheme, and it said UnitedHealth has grabbed the lion’s share of those billions. In many if not most instances, those enrollees were not treated for the conditions and illnesses UnitedHealth and other insurers claimed they had. As the newspaper reported:

Insurer-driven diagnoses by UnitedHealth for diseases that no doctor treated generated $8.7 billion in 2021 payments to the company, the Journal’s analysis showed. UnitedHealth’s net income that year was about $17 billion.

By far, most of UnitedHealth’s health plan enrollment growth over the past 10 years has come from the Medicare Advantage program, and it now takes in nearly twice as much revenue from the 7.8 million people enrolled in that program as it does from the 29.6 million enrolled in its commercial insurance plans in the United States.

Since the second quarter of 2014, UnitedHealth’s commercial health plan enrollment has increased by 720,000 people. During that same time, enrollment in its Medicare Advantage plans has increased by 4.8 million.

UnitedHealth and other insurers that participate in the Medicare Advantage program know a cash cow when they see one.

As the Kaiser Family Foundation noted in a recent report, the highest gross margins among insurers come from Medicare Advantage, which, as Health Finance News reported, boasted gross margins per enrollee of $1,982 on average by the end of 2023, compared to $1,048 in the individual (commercial) market and $753 in the Medicaid managed care market.

UnitedHealth has significant enrollment in all of those areas. Enrollment in the Medicaid plans it administers in several states increased from 4.7 million at the end of the second quarter of 2014 to 7.4 million this past quarter.

In its disclosure today, UnitedHealth did not break out its health plan revenue as it has in past quarters, but you can see how public programs like Medicare Advantage and Medicaid have become so lucrative by comparing revenue reported by the company at the end of the second quarter of 2013 to the second quarter of 2023. Over that time, total revenues for commercial plans (employer and individual) increased by slightly more than $5.6 billion, from $11.1 billion in 2Q 2013 to $16.8 billion in 2Q 2023. Total revenues from Medicaid increased by $14.2 billion, from $4.5 billion to $18.7 billion, and total revenues from Medicare increased by $21.4 billion, from $11.1 billion to $32.4 billion.

Here’s another way of looking at this: At the end of 2Q 2013, UnitedHealth took in almost exactly the same revenue from its commercial business and its Medicare business ($11.053 from Medicare and $11.134 from its commercial plans.

At the end of 2Q 2023, the company took in nearly twice as much from its Medicare business ($32.4 billion from Medicare compared to $16.8 billion from its commercial plans.)

The change is even more stark when you add in Medicaid. At the end 2Q 2023, UnitedHealth’s Medicare and Medicaid (community and state) revenues totaled $51.1 billion; It’s commercial revenues, as noted, totaled $16.8 billion). It’s now getting three times as much revenue from taxpayer-supported programs as from its commercial business.

As impressive for shareholders as all of that is, growth in the company’s other big division, Optum, which encompasses its pharmacy benefit manager (Optum Rx) and the physician practices and clinics it owns) has been even more eye-popping. At the end of 2Q 2014, Optum contributed $11.7 billion to the company’s total revenues. At the end of 2Q 2024, it contributed $62.9 billion, an increase of $51.2 billion. At that rate of growth, it’s only a matter of a few quarters before Optum is both the biggest and most profitable division of the company.

And here’s the way the company benefits from that loophole in federal law I mentioned above. The Affordable Care Act requires insurers to spend 80%-85% of health plan revenue on patient care. UnitedHealth is consistently able to meet that threshold by paying itself, as HEALTH CARE un-coveredexplained in December. The billions UnitedHealthcare (the health plan division) pays Optum every quarter are categorized as “eliminations” in its quarterly reports. In 2Q 2024, 27.7% of the company’s revenues fell into that category.

The more it is able to steer its health plan enrollees into businesses it owns on the Optum side, the more it can defy Congressional intent – and profit greatly by it.

Wall Street loves how UnitedHealth has pulled all this off. It’s stock price jumped $33.50 to $548.87 a share during today’s trading at the New York Stock Exchange, an increase of 6.5% – in one day.

The rebates that will be issued later this year will be larger than those issued in most prior years, the analysis found.

Health insurers are projected to pay about $1.1 billion in Affordable Care Act medical loss ratio rebates this year, a new KFF report finds.

The medical loss ratio (MLR) provision of the ACA limits the amount of premium income that insurers can keep for administration, marketing and profits. Insurers that fail to meet the applicable MLR threshold are required to pay back excess profits or margins in the form of rebates to individuals and employers that purchased coverage.

The $1.1 billion in estimated total rebates across commercial markets are similar to the $1 billion in total rebates issued in 2022, and the $950 million issued in 2023. Last year, rebates were issued to 1.7 million people with individual coverage and 4.1 million people with employer coverage. In the individual market, the 2023 average rebate per person was $196, while the average rebates per person for the small group market and the large group market were $201 and $104, respectively.

The rebates, to be issued later this year, will be larger than those issued in most prior years, the analysis found, but they’ll fall short of the recent rebate totals of $2.5 billion issued in 2020 and $2 billion issued in 2021, which coincided with the onset of the COVID-19 pandemic.

WHAT’S THE IMPACT?

In the individual and small group markets, insurers are required to spend at least 80% of their premium income on healthcare claims and quality improvement efforts, leaving the remaining 20% for administration, marketing expenses and profit.

The MLR threshold is higher for large group insurers, which have to spend at least 85% of their premium income on healthcare claims and quality-improvement efforts.

MLR rebates are based on a three-year average, meaning that rebates issued in 2024 will be calculated using insurers’ financial data in 2021, 2022 and 2023, and will go to people and businesses who bought health coverage in 2023.

In 2023, the average individual market simple loss ratio – meaning there’s no adjustment for quality improvement expenses or taxes, and doesn’t align perfectly with ACA MLR thresholds – was 84%. That shows insurers spent an average of 84% of their premium income in the form of health claims in 2023, according to KFF data.

However, rebates issued in 2024 are based on a three-year average of insurers’ experience in 2021-2023. Consequently, even insurers with high loss ratios in 2023 may expect to owe rebates if they were highly profitable in the prior two years.

In the small and large group markets, 2023 average simple loss ratios were 84% and 88%, respectively. Only fully insured group plans are subject to the ACA MLR rule, while roughly two-thirds of covered workers are in self-funded plans, to which the MLR threshold doesn’t apply.

THE LARGER TREND

KFF cautioned that the rebate amounts are still preliminary. Rebates and notices are mailed out by the end of September, and the federal government will post a summary of the total amount owed by each issuer in each state later in the year.

Insurers in the individual market can either issue rebates in the form of a check or premium credit. For people with employer coverage, the rebate can be shared between the employer and the employee, depending on the way in which they share premium costs.

If the amount of the rebate is exceptionally small – less than $5 for individual rebates and less than $20 for group rebates – insurers are not required to process the rebate, as it may not warrant the administrative burden required to do so, KFF said.