It’s no secret the brand name prescription drug costs are high. The rising costs have been blamed by health care analysts on kickbacks within the drug supply chain demanded by the federal government, drug distributors (wholesalers), health insurance companies and pharmacy benefit managers (PBMs).

How about $356 billion worth of pure glut in the prescription drug supply chain, according to the analysis by DCI. Simply put, the market price established for these drugs by manufacturers has $356 billion worth of markups that mainly accommodate the financial demands (i.e. kickbacks or rebates) of groups that profit off the prescription drug system in the United States, health insurers and their PBMs in particular.

And that’s an all-time record.

Why?

Get ready to choke on your popcorn.

In the 1990s the federal government mandated in the Medicaid program that drug manufacturers offer a minimum rebate of 23% off the purchase price of brand name drugs. The feds also mandated that if drug manufacturers offer a better rebate on those drugs to someone else, the government also gets that same rebate.

The thought was no one gets a better deal than the federal government.

Rebates expanded again as PBMs continued to gain more control over the drug supply chain. The PBMs now force drug manufacturers to offer significant concessions in order to get on the list of approved medications – known as a formulary – available to patients with health insurance.

To account for these demands, drug manufacturers set the list price for their brand name drugs with these price concessions baked into the number.

DCI’s analysis found that baking is $356 billion of goodies for health care companies paid for by the government and you.

It’s the same kind of concept as a U.S. popular clothing retailer that displays inflated retail costs on the tags of goods and then right below displaying a lower “sale” price to make the consumer think they got a deal.

Here’s another way of thinking of it: Just like Congress has a lot of “pork” in its spending bills, there’s also a lot of pork in prescription drug costs that have very little to do with anything, other than increase profits for the health care industry.

Though the federal government intended to create a better system for taxpayers back in the 1990s when it demanded rebates in the Medicaid system, it instead created a feeding frenzy for companies in the drug supply chain.

In the year 2000 just a handful of companies in the drug supply chain dotted the Fortune 100 list of most financially successful companies. Today there are four such companies in the top 10.

The Minnesota-based health care conglomerate UnitedHealth leads that pack. The company’s profits have soared in the last two decades largely due to increasing medical costs and prescription drug costs paid by Americans. It has leaped over companies like Exxon Mobile and Apple to become the third largest company in America. Only Walmart and Amazon take in more revenue.

The company employs more than 400,000, including doctors and clinicians and has its own pharmacy benefits manager called Optum Rx.

We reported last month that Americans spent $464 billion last year on prescription drugs. That was also an all-time record, which will likely be set again and again and again until reforms are enacted.

Health insurers and their lobbying arms have spent $476.5 million since 2020 to block reform, protect profits, and mislead the public — and it’s coming straight from our premiums and tax dollars.

AHIP, the big PR and lobbying outfit for most health insurers, undoubtedly believes the praise it got from Trump administration officials and some members of Congress this week – when it announced changes insurers presumably will make voluntarily to alleviate the burden of prior authorization demands on patients and health care providers – has taken the heat off insurers. AHIP’s message to Washington politicos: You don’t need to pass any new laws to make us do the right thing. You can trust us, despite our decades of engaging in untrustworthy behavior to maximize profits.

After all, AHIP is nothing more than a PR and lobbying shop with millions of our dollars to play with. It has zero ability to force insurers to do what AHIP claims they will do. I know this because I worked closely with AHIP during my 20 years in the industry and represented Cigna on its strategic communications committee.

From Fox to “Fixer”?

AHIP pulled off its big show on Monday – and got plenty of generally fawning press coverage – because of all the money it and affiliated insurers throw around Washington every year to protect what has become an incredibly profitable status quo.

Collectively, the seven biggest for-profit insurers reported $70 billion in profits last year.

(Beleauered UnitedHealth alone reported $34.4 million in operating earnings.) And that’s just seven among dozens. One way they make that kind of dough, for their shareholders and top executives, is by using prior authorization to avoid paying for patients’ medically necessary care. Many people die as a result, while investors get richer. It’s that simple and that cold.

So just how much money does AHIP and the insurance industry spend to bamboozle members of Congress and the White House every year? We’re talking stupid money. And orders of magnitude more than nonprofits that advocate for reforms that would benefit patients instead of shareholders.

Nearly Half a Billion Ways They Tip the Scale

To find out just how much, I turned to OpenSecrets and did some math. OpenSecrets, as a reminder, is the well-named organization that keeps tabs on campaign contributions and lobbying expenses.

What I discovered is that AHIP has spent almost $65 million lobbying Congress and the Biden and Trump administrations since 2020. Its cousin, the Blue Cross Blue Shield Association, has spent even more. More than twice as much more.

And that, folks, is just the tip of the iceberg, and it doesn’t even include the tens of millions the industry spends on massive advertising campaigns inside the DC beltway that it’s not required to report. Or the dark money ads and advocacy the industry bankrolls.

But just the lobbying totals are mind-blowing. When you factor in the money spent by the big seven insurers and the other PR and lobbying groups that insurers funnel money to, the total grows to almost $500 million. You read that right: nearly half a billion dollars.

Most of that spending was during the Biden administration, but the industry is on track to break spending records during the first year of the current Trump administration. They are lobbying not only to beat back new laws and regulations that could constrain their prior authorization practices but also to protect their biggest cash cows: Medicare Advantage and their pharmacy benefit managers (PBMs).

Three PBMs – owned by Cigna, CVS/Aetna and UnitedHealth –control 80% of the pharmacy benefit market and determine which drugs we’ll have access to and how much we have to pay out of pocket even with insurance.

The Big Number

$476.5 million – That’s the amount of money health insurance corporations and four of their PR and lobbying groups – AHIP, BCBSA (which includes contributions from Elevance/Anthem as well as numerous other BCBS companies), the Pharmaceutical Care Management Association and the Better Medicare Alliance – have collectively spent on lobbying Congress and federal regulators between January 1, 2020, and March 31, 2025.

Keep in mind that that money is not coming out of executives’ paychecks. It’s coming out of our pockets. Insurers skim money from our premiums and taxes to finance their propaganda and lobbying efforts to keep the gravy train rolling. And it’s in addition to all the campaign cash they dole out every year, which I tabulated recently.

This is not to say that reform is impossible. Scrappy advocacy groups with a tiny fraction of that total have scored important victories over the years. But it is why progress is so slow and setbacks are so frequent.

But just imagine how all that money could be put to better use to ensure that all Americans, including those with insurance, are able to get the care they need when they need it. It’s clear that in addition to reforming our health care system, we need political reforms that make it more difficult for big corporations and their trade groups to influence elections and public policy.

UnitedHealth executives made a valiant attempt yesterday to persuade investors that they have figured out how to improve customer service and keep Congress and the incoming Trump administration from passing laws that could shrink the company’s profit margins – and maybe even the company itself – but Wall Street wasn’t buying.

During their first call with investors since the murder of UnitedHealthcare CEO Brian Thompson, the company’s top brass pointed the finger of blame for rising health care costs everywhere but at themselves – primarily at hospitals and pharmaceutical companies – and made statements that simply were not true. Investors clearly did not find their comments reassuring or credible. By the end of the day shares of UnitedHealth’s stock were down more than 6% to $510.59. That marked a continuation of a slide that began after the stock price peaked at $630.73 on November 11 – a decline of almost 20%.

In a little more than two months, the company has lost an astonishing $110 billion in market capitalization, and shareholders have lost an enormous amount of the money they invested in UnitedHealth.

Earlier yesterday morning, the company released fourth-quarter and full-year 2024 earnings, which were slightly higher on a per share basis than Wall Street financial analysts had expected: $6.81 per share in the fourth quarter compared to analysts’ consensus estimate of $6.73 for the quarter. But the company posted lower revenue during the last three months of 2024 than analysts had expected. While revenue was up 7% over the same quarter in 2023, to $100.8 billion, analysts had expected revenue to grow to $101.6 billion.

And on a full-year basis, the company’s net profits fell an eye-popping 36%, from $22.4 billion in 2023 to $14.4 billion last year.

Bottom line: the company, which until last year had grown rapidly, actually shrank in some respects, especially in the division that operates the company’s health plans. UnitedHealthcare, which Thompson led, saw its revenue increase slightly but its profits fall. The other big division, Optum, which among other things owns and operates numerous physician practices and clinics and one of the country’s largest pharmacy benefit managers (PBMs), fared much better.

While Optum’s 2024 revenue was lower than UnitedHealthcare’s ($253 billion and $298 respectively), it made far more in profits on an operating basis ($16.7 billion and $15.6 respectively).

Optum’s operating profit margin was 6.6% while UnitedHealthcare’s was 5.2%.

The company’s executives blamed higher health care utilization, especially by people enrolled in its Medicare Advantage plans, for the decline in profits.

Witty and CFO John Rex pointed the finger of blame at hospitals and drug companies for rising medical prices. And they obscured the huge amounts of money the company’s PBM, Optum Rx, extracts from the pharmacy supply chain. While the company chose not to break out exactly how much of Optum’s revenues of $298 billion came from Optum Rx, it appears that more than half of it was contributed by the PBM. The company did note that Optum Rx revenues increased 15% during 2024.

Nevertheless, Witty and Rex blamed drug makers for high prices.

They also said that they would be changing the PBM’s business practices to pass through rebate discounts from drug makers to its customers, claiming that it already passes through 98% of them and will reach 100% by 2028. That clearly was a talking point aimed at Washington, where there is significant bipartisan support for legislation that would require all PBMs to do so. Despite UnitedHealth’s claim, there is no external verification to back up that they are passing 98% of rebates back to customers.

Another claim the executives made that is not true is that the Medicare Advantage program saves taxpayers money. Numerous government reports have shown the opposite, that the federal government spends considerably more on people enrolled in Medicare Advantage plans than those enrolled in the traditional Medicare program.

Reports have estimated that UnitedHealthcare, which is the largest Medicare Advantage company, and other MA plans are overpaid between $80 billion and $140 billion a year.

There is also growing bipartisan support to reform the Medicare Advantage program to reduce both the overpayments and the excessive denials of care at UnitedHealthcare and other MA insurers.

While company executives might be hoping that their fortunes will improve during the second Trump administration, Trump recently joined some Republican members of Congress, like Rep. Buddy Carter of Georgia, who are calling for significant reforms, especially to pharmacy benefit managers.

At a news conference last month, Trump promised to “knock out” those middlemen in the pharmacy supply chain.

“We are paying far too much, because we are paying far more than other countries,” he said. “We have laws that make it impossible to reduce [drug costs] and we have a thing called a ‘middleman’ … that makes more money than the drug companies, and they don’t do anything except they’re middlemen. We are going to knock out the middleman.”

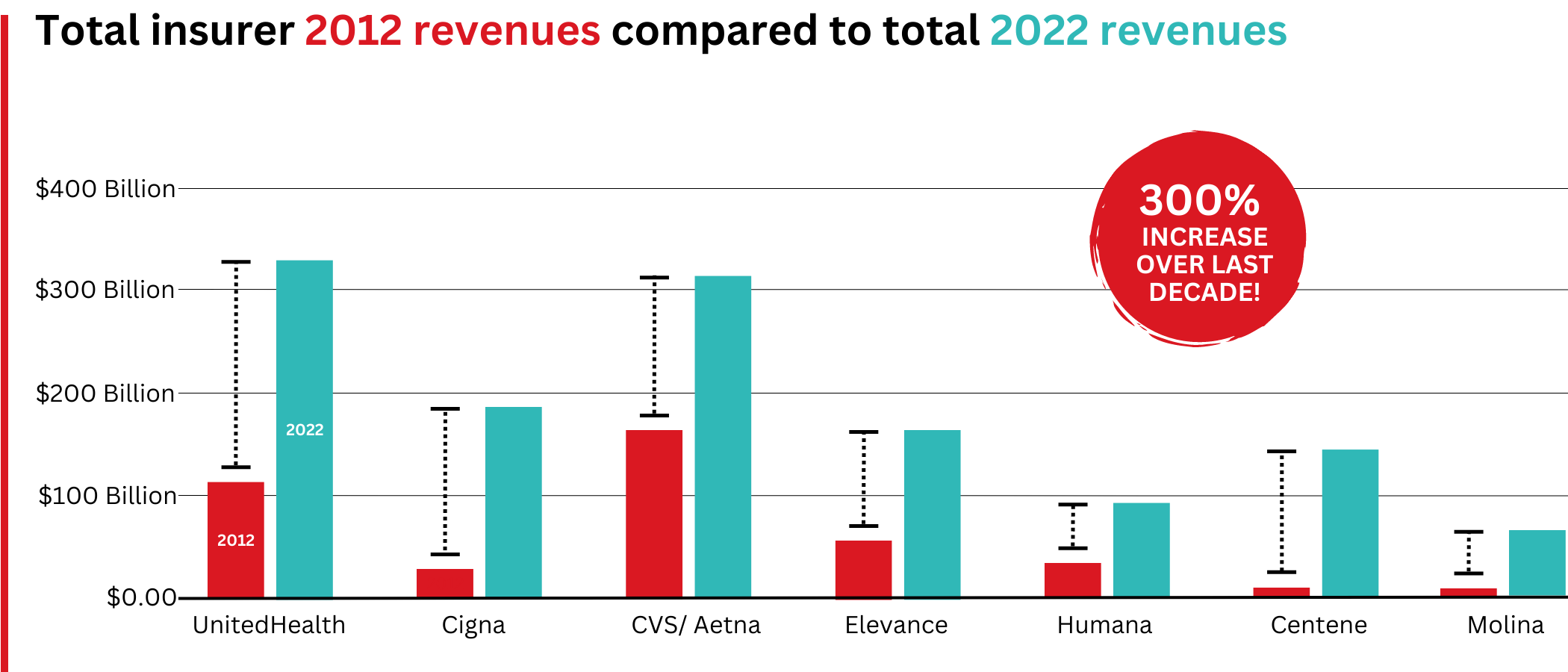

Big Insurance revenues and profits have increased by 300% and 287% respectively since 2012 due to explosive growth in the companies’ pharmacy benefit management (PBM) businesses and the Medicare replacement plans they call Medicare Advantage.

The for-profits now control more than 80% of the national PBM market and more than 70% of the Medicare Advantage market.

In 2022, Big Insurance revenues reached $1.25 trillion and profits soared to $69.3 billion.

That’s a 300% increase in revenue and a 287% increase in profits from 2012, when revenue was $412.9 billion and profits were $24 billion.

Big insurers’ revenues have grown dramatically over the past decade, the result of consolidation in the PBM business and taxpayer-supported Medicare and Medicaid programs.

Sucking billions out of the pharmacy supply chain – and taxpayers’ pockets

What has changed dramatically over the decade is that the big insurers are now getting far more of their revenues from the pharmaceutical supply chain and from taxpayers as they have moved aggressively into government programs. This is especially true of Humana, Centene, and Molina, which now get, respectively, 85%, 88%, and 94% of their health-plan revenues from government programs.

The two biggest drivers are their fast-growing pharmacy benefit managers (PBMs), the relatively new and little-known middleman between patients and pharmaceutical drug manufacturers, and the privately owned and operated Medicare replacement plans they market as Medicare Advantage.

With the exception of Humana, Centene, and Molina, most of the companies that constitute Big Insurance continue to make substantial amounts of money selling policies and services in what they refer to as their commercial businesses – to individuals, families, and employers – but the seven companies’ commercial revenue grew just 260%, or $176 billion, over 10 years (from $110.4 billion to $287.1 billion). While that’s significant, profitable growth in the commercial sector has become a major challenge for big insurers – so much so that Humana just last week announced it is exiting the employer-sponsored health-insurance marketplace entirely.

The percentage of U.S. employers providing some level of health benefits to their workers dropped from 69% to 51% between 1999 and 2022 – including a dramatic 8% decrease last year alone. Growth in this category is largely the result of insurers “stealing market share” from each other or from smaller competitors.

As a consequence of this segment’s relative stagnation, PBMs and government programs have become the new cash cows for Big Insurance.

Spectacular PBM Growth

PBM HIGHLIGHTS

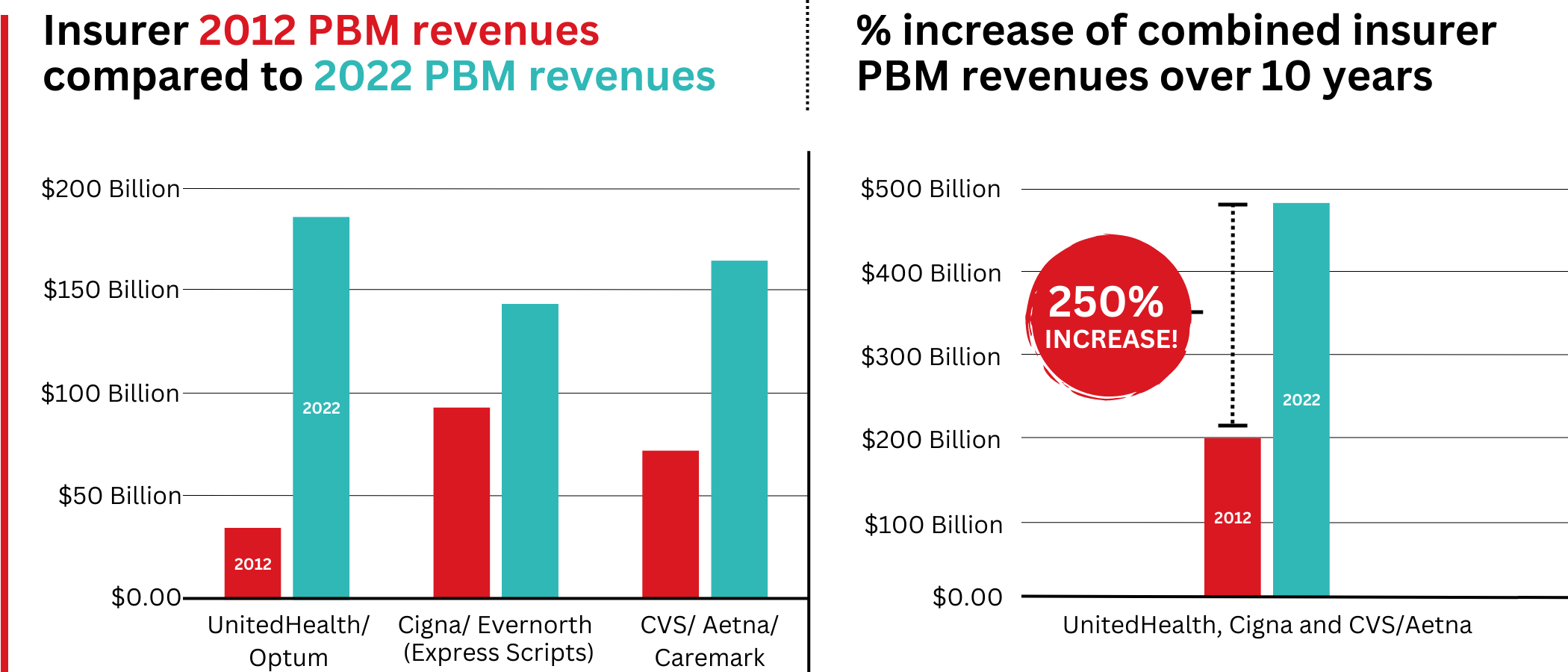

Cigna now gets far more revenue from its PBM than from its health plans. CVS gets more revenue from its PBM than from either Aetna’s health plans or its nearly 10,000 retail stores.

UnitedHealth has the biggest share of both the PBM and Medicare markets and, through numerous acquisitions of physician practices, is now the largest U.S. employer of doctors.

PBMs are middlemen companies that manage prescription drug benefits for health insurers, Medicare Part D drug plans, employers, and, in some cases, unions. As the Commonwealth Fund has noted:

PBMs have a significant behind-the-scenes impact in determining total drug costs for insurers, shaping patients’ access to medications, and determining how much pharmacies are paid.

The Commonwealth Fund went on to say that PBMs have faced growing scrutiny about their role in rising prescription drug costs and spending. A big reason for the scrutiny – by Congress, state lawmakers and now also by the FTC – is that the biggest PBMs are now owned by Big Insurance.

Through mergers and acquisitions in recent years, three of the seven for-profit insurers – Cigna, CVS/Aetna, and UnitedHealth – now control 80% of the U.S. pharmacy benefits market.

They determine which drugs will be listed in each of their formularies (lists of drugs they will “cover” based on secret deals they negotiate with pharmaceutical companies) and how much patients will have to pay out of their own pockets at the pharmacy counter – in many cases hundreds or thousands of dollars – before their coverage kicks in. The PBMs also “steer” health-plan enrollees to their preferred or owned pharmacies (and, increasingly, away from independent pharmacists), thereby capturing even more of what we spend on our prescription medications.

Cigna, CVS/Aetna, and UnitedHealth now control 80% of the U.S. PBM market. Correction: this graph was initially published with inaccurate numbers. The source for this information can be found here.

Ten years ago, PBMs contributed relatively little to the three companies’ revenues and profits. But since then, the rapid growth of PBMs has transformed all of the companies. The combined revenues from their PBM business units increased 250% between 2012 and 2022, from $196.7 billion to $492.4 billion.

Changes in PBM revenues between 2012 and 2022 for UnitedHealth Group, Cigna, and CVS/Aetna (Editor’s note: Cigna acquired PBM Express Scripts in 2018. To reflect revenue growth, Express Scripts’ pre-acquisition 2012 revenues are included in the Cigna total for that year.)

PBM Profit Generation

The PBM profit growth at the three companies over the past decade was even more dramatic than revenue growth. Collectively, their PBM profits increased 438%, from $6.3 billion in 2012 to $27.6 billion in 2022.

As a result of this fast growth, more than half (52%) of three companies’ profits in 2022 came from their PBM business units: Cigna’s Evernorth, CVS/Aetna’s Caremark, and UnitedHealth’s Optum. Cigna now gets far more revenue and profits from its PBM than from its health plans. And CVS gets more revenue from its PBM than from either Aetna’s health plans or its nearly 10,000 retail stores. (The companies’ business units that include their PBMs have also moved aggressively in recent years into health-care delivery through acquisitions of physician practices, clinics, dialysis centers, and other facilities. Notably, UnitedHealth Group is now the largest U.S. employer of physicians.)

Huge strides in privatizing both Medicare and Medicaid

GOVERNMENT PROGRAMS HIGHLIGHTS

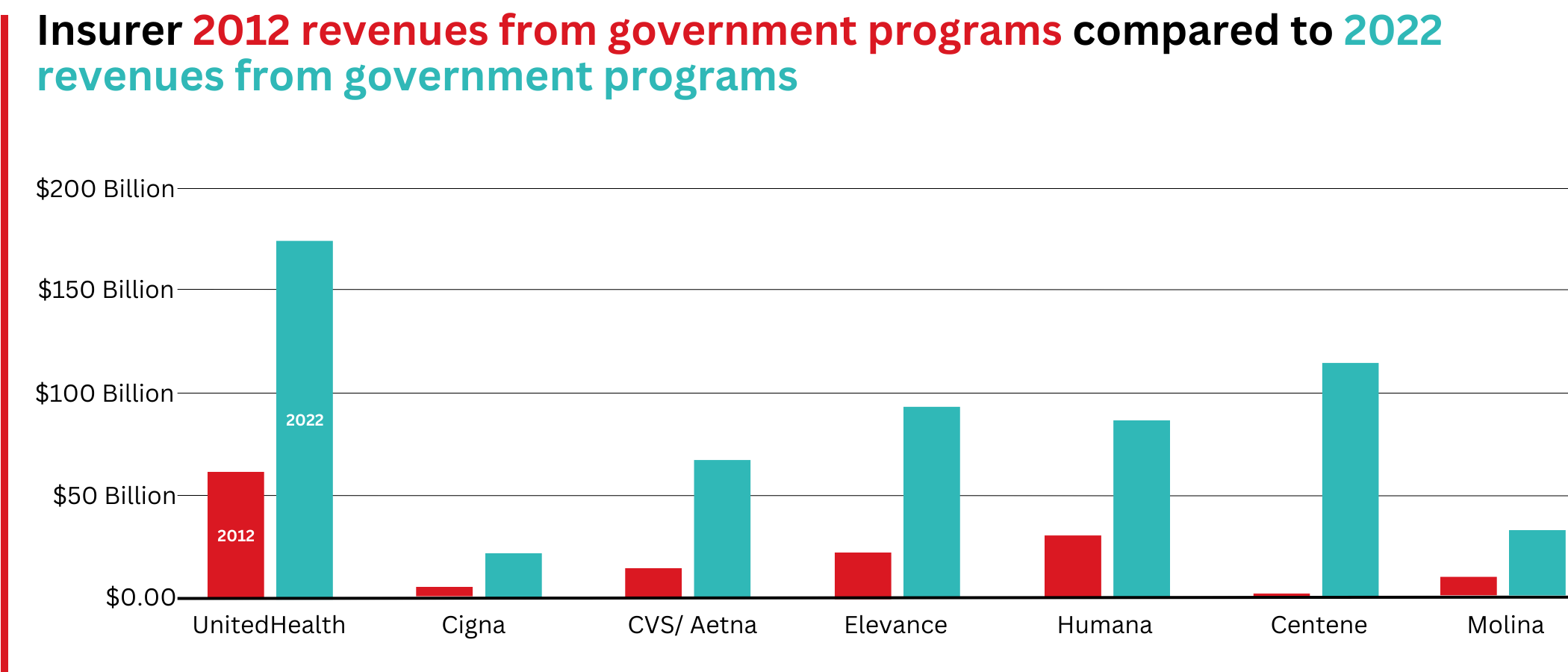

More than 90% of health-plan revenues at three of the companies come from government programs as they continue to privatize both Medicare and Medicaid, through Medicare Advantage in particular.

Enrollment in government-funded programs increased by 261% in 10 years; by contrast commercial enrollment increased by just 10% over the past decade.

Commercial enrollment actually declinedat both UnitedHealth and Humana.

85% of Humana’s health-plan members are in government-funded programs; at Centene, it is 88%, and at Molina, it is 94%.

The big insurers now manage most states’ Medicaid programs – and make billions of dollars for shareholders doing so – but most of the insurers have found that selling their privately operated Medicare replacement plans is even more financially rewarding for their shareholders.

Revenue growth from government programs has been dramatic over the past 10 years. (Note the numbers do not include revenue from the Medicare Part D program, federal subsidy payments for many ACA marketplace plan enrollees, or Medicare supplement policies.)

This is especially apparent when you see that the Big Seven’s combined revenues from taxpayer-supported programs grew 500%, from $116.3 billion in 2012 to $577 billion in 2022.

These numbers should be of interest to the Biden administration and members of Congress, many of whom are calling for much greater scrutiny of the Medicare Advantage program. Numerous media and government reports have shown that the federal government is overpaying private insurers billions of dollars a year, largely because of loopholes in laws and regulations that enable them to get more taxpayer dollars by claiming their enrollees are sicker than they really are. The companies also make aggressive use of prior authorization, largely unknown in traditional Medicare, to avoid paying for doctor-ordered care and medications.

In addition to their focus on Medicare and Medicaid, the companies also profit from the generous subsidies the government pays insurers to reduce the premiums they charge individuals and families who do not qualify for either Medicare or Medicaid or who work for an employer that does not offer subsidized coverage. But many people enrolled in those types of plans – primarily through the health insurance “marketplaces” established by the Affordable Care Act – cannot afford the deductibles and other out-of-pocket requirements they must pay before their insurers will begin paying their medical claims.

Dramatic Enrollment Shifts

Changes in health-plan enrollment over the past decade show how dramatic this shift has been. Between 2012 and 2022, enrollment in the companies’ private commercial plans increased by 10%, from 85.1 million in 2012 to 93.8 million in 2022.

By comparison, growth in enrollment in taxpayer-supported government programs increased 261%, from 27 million in 2012 to 70.4 million in 2022.

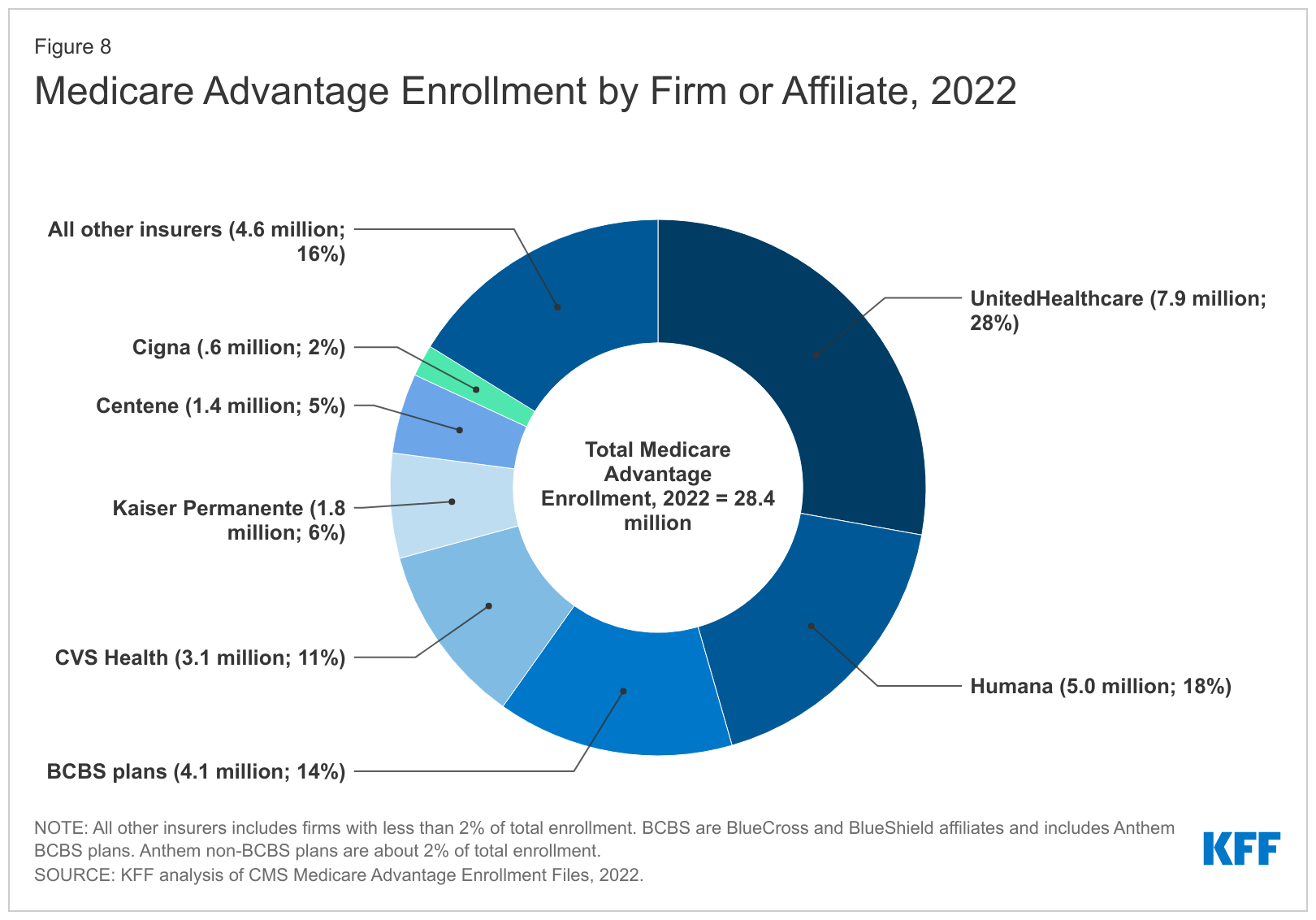

For-profit insurers dominate the Medicare Advantage market. Note that Anthem mentioned above is now known as Elevance. It owns 14 of the country’s Blue Cross Blue Shield plans.

Within that category, Medicare Advantage enrollment among the Big Seven increased 252%, from 7.8 million in 2012 to 19.7 million in 2022.

Nationwide, enrollment in Medicare Advantage plans increased to 28.4 million in 2022 (and to 30 million this year). That means that the Big Seven for-profit companies control more than 70% of the Medicare Advantage market.

UnitedHealth, Humana, Elevance, and CVS/Aetna have captured most of the Medicare Advantage market since the Affordable Care Act was passed in 2010.

The remaining growth in the government segment occurred in the Medicaid programs that a subset of the Big Seven (UnitedHealth, Elevance, Centene, and Molina in particular) manages for several states.

A few other facts and figures to keep in mind as Big Insurance thrives:

100 million of us – almost one of every three people in this country – now have medical debt.

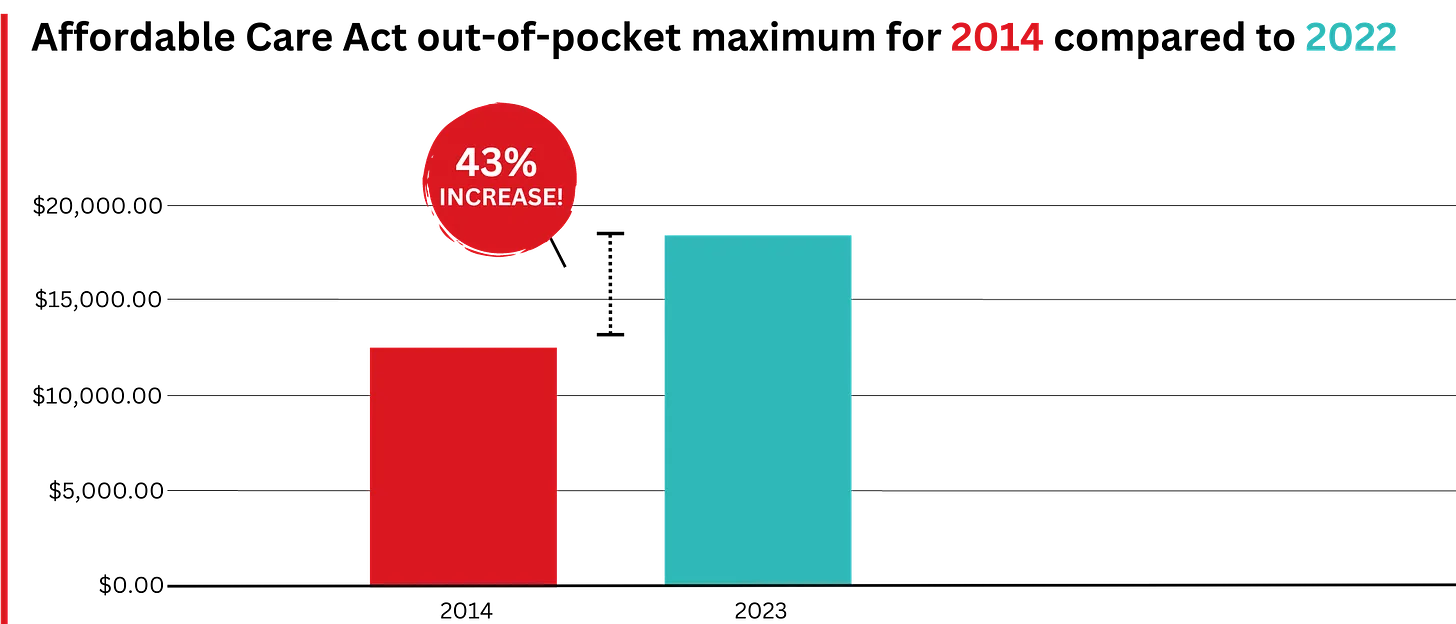

In 2023, U.S. families can be on the hook for up to $18,200 in out-of-pocket requirements before their coverage kicks in, up 43% since 2014 when it was $12,700.The Affordable Care Act allows the out-of-pocket maximum to increase annually – 43% since the maximum limit went into effect in 2014.

44% of people in the United States who purchased coverage through the individual market and (ACA) marketplaces were underinsured or functionally uninsured.

42% said they hadproblems paying medical bills or were paying off medical debt.

Half (49%) said they would be unable to pay an unexpected medical bill within 30 days, including 68% of adults with low income, 69% of Black adults, and 63% of Latino/Hispanic adults.

In 2021, about $650 million, or about one-third of all funds raised by GoFundMe, went to medical campaigns. That’s not surprising when you realize that in the United States, even people with insurance all too often feel they have no choice but to beg for money from strangers to get the care they or a loved one needs.

Even as we spend about $4.5 trillion on health care a year, Americans are now dying younger than people in other wealthy countries. Life expectancy in the United States actually decreased by 2.8 years between 2014 and 2021, erasing all gains since 1996, according to the Centers for Disease Control and Prevention.

BOTTOM LINE:

The companies that comprise Big Insurance are vastly different from what they were just 10 years ago, but policymakers, regulators, employers, and the media have so far shown scant interest in putting their business practices under the microscope.

Changes in federal law, including the Medicare Modernization Act of 2003, which created the lucrative Medicare Advantage market, and the Affordable Care Act of 2010, which gave insurers the green light to increase out-of-pocket requirements annually and restrict access to care in other ways, opened the Treasury and Medicare Trust Fund to Big Insurance. In addition, regulators have allowed almost all of their proposed acquisitions to go forward, which has created the behemoths they are today.

CVS/Health is now the 4th largest company on the Fortune 500 list of American companies. UnitedHealth Group is now No. 5 – and all the others are climbing toward the top 10.

Last week, President-elect Donald Trump announced that Robert F. Kennedy, Jr. would be his nominee for Secretary of Health and Human Services (HHS). He followed this up on Tuesday with his selection of Dr. Mehmet Oz as his nominee for the Centers for Medicare and Medicaid Services (CMS) Administrator. If confirmed, the two men would replace Xavier Becerra and Chiquita Brooks-LaSure, respectively.

Kennedy, who ended his independent presidential campaign and endorsed Trump in August, has become known for his heterodox views on public health, including vaccine skepticism and opposition to water fluoridization.

Dr. Oz, first famous as a TV personality and more recently a Republican candidate for Pennsylvania Senator, is a strong proponent of Medicare Advantage, having co-authored an op-ed advocating for “Medicare Advantage for All” in 2020.

The Gist:

These nominees, especially Kennedy, hold a number of personal beliefs at odds with the public health consensus.

They are both likely to be confirmed, however, as the last cabinet nominee to be rejected by the Senate was John Tower in 1989. (This does not include nominees who have chosen to withdraw themselves from consideration, as former Representative Matt Gaetz has just done.)

Should they be confirmed, they will be responsible for implementing not their own but President Trump’s agenda, the specific priorities of which also remain relatively undefined.

However, possible consensus points between Trump and his nominees include public health cuts and deregulation, greater scrutiny of pharmaceutical companies, and a favoring of Medicare Advantage over traditional Medicare.

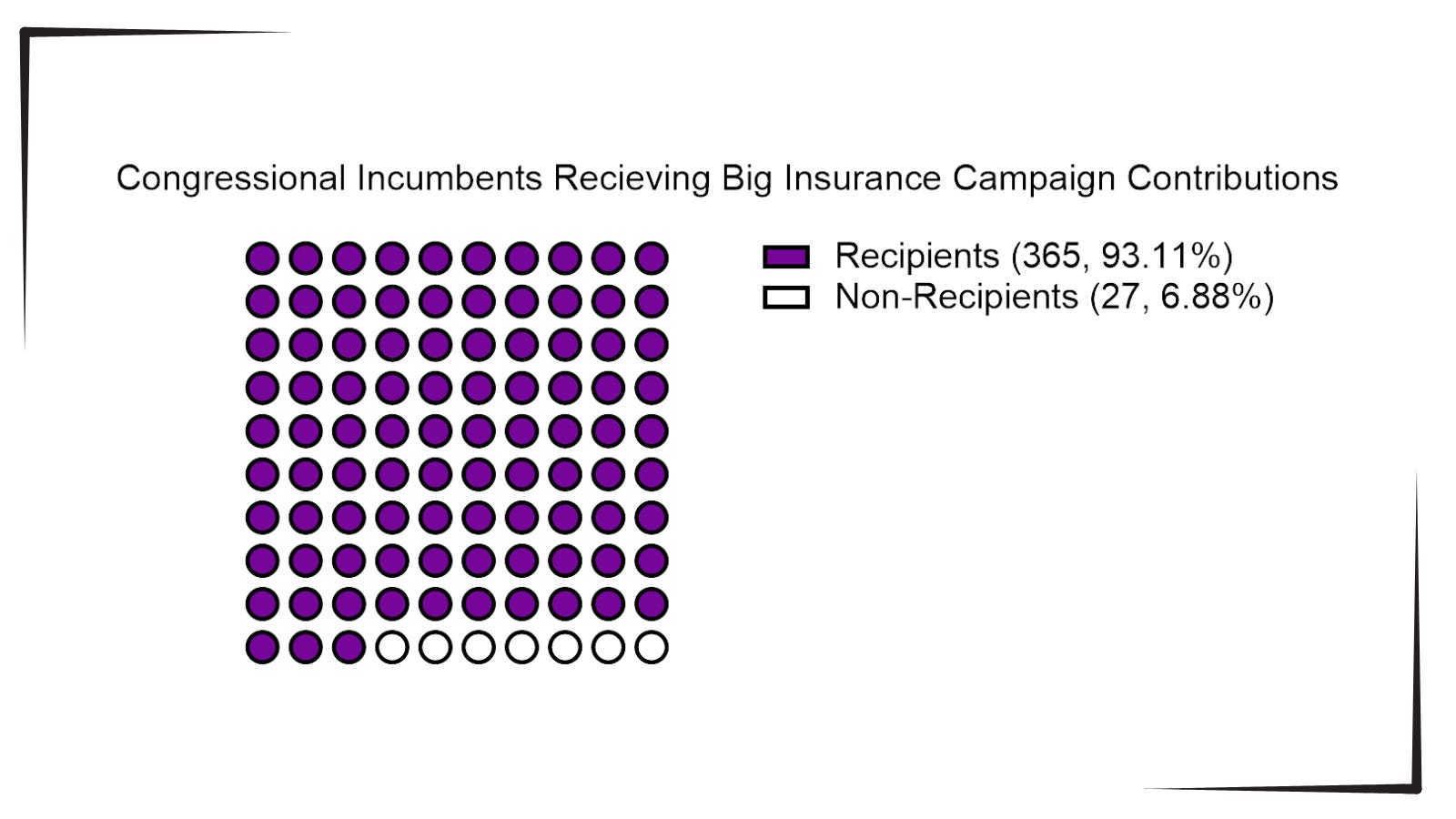

With the election looming and the beginning of annual open enrollment periods for health insurance plans, it is vital to pull back the curtain on the influx of money from Big Insurance corporations to political campaigns and lobbying.

Data available from OpenSecrets.com thus far in 2024 shows that 93% of Congressional incumbents running in 2024 received contributions from Big Insurance, including 100% of Senate incumbents. These insurance corporations run the ten largest Medicare Advantage plans in the country and are known to deny needed health care and defraud the government, but face little to no consequences.

Insurance corporations included in this analysis are UnitedHealth Group, Humana, CVS/Aetna, Kaiser Permanente, Elevance Health, Centene Corp, Cigna, Blue Cross Blue Shield Association (which represents many MA plans, including two of the largest: BCBSMichigan and Highmark), and SCAN.

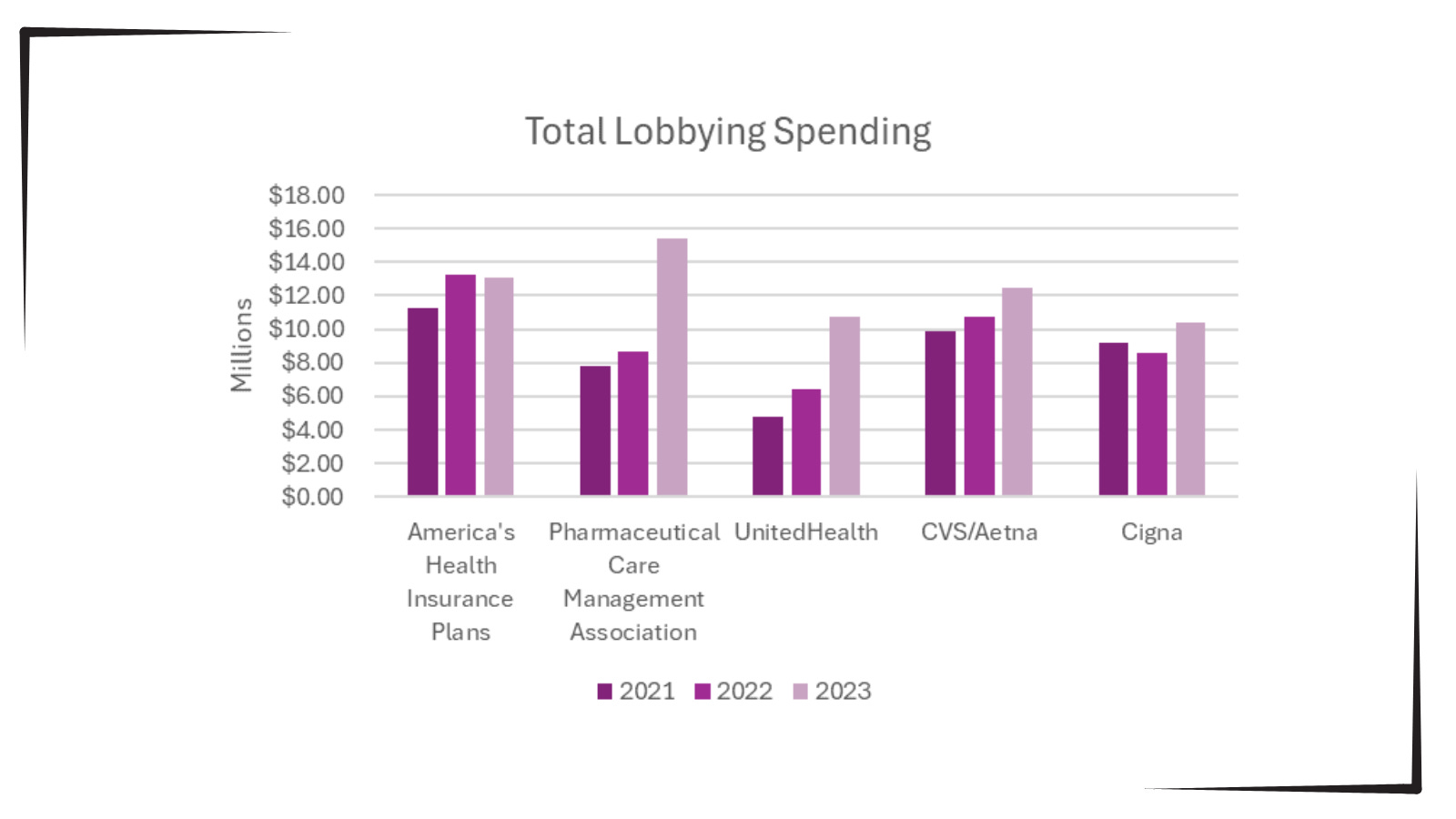

Additionally, as bipartisan scrutiny of pharmacy benefit managers (PBMs) and Medicare Advantage plans has intensified, spending by Big Insurance on lobbying has increased.

Total lobbying spending by America’s Health Insurance Plans; Pharmaceutical Care Management Association; UnitedHealth; CVS/Aetna; and Cigna for the years 2021, 2022 and 2023.

This open enrollment season, people struggling to choose a health insurance plan that they can afford and that provides the care they need may ask themselves, “Why is our health care system like this?” The immense amounts of money Big Insurance spends to blanket members of Congress with contributions and lobbying hold the answer.

Additional analysis following the election will allow evaluation of just how much Big Insurance spends on politics to help protect industry profits and will give health reform advocates an idea of how to overcome this influence to pass policies for patients, not profits.

While speculation swirls around key cabinet appointments in the incoming Trump administration, much is being written about how things might change for industries and the companies that compose them. Healthcare is no exception.

Speculation about possible changes originates from media coverage, healthcare trade associations, law firms, consultancies, think tanks and academics. Their views are primarily based on Trump Healthcare 1.0 initiatives (2017-2021), presumed Trump 2.0 leverage in the U.S. Senate, House and conservative Supreme Court and a belief by the Trump-team leaders that their mandate is to lower costs for “everyday Americans” and tighten border security.

Thus, Trump Healthcare 2.0 policy changes will be extensive, leveraging legislation, executive orders, agency administrative actions, court decisions and appropriations processes to reset the U.S. health system.

Context:

The red shift that enabled the 45th President to regain the White House was fueled by discontent and fear: discontent with prices paid by ordinary consumers and fear that illegal immigration was an existential threat. Abortion was an important concern to women but inflation and prices for gas, groceries, housing and healthcare mattered more. Exit polls indicate voter concern about how Trump 2.0 economic policies (tariffs et al) might inflate consumer prices or add up to $7 trillion to the national debt was low. And the fate of the Affordable Care Act was a non-issue: assurance about protection for pre-existing condition coverage neutered attention to other elements of the ACA that will get attention in Trump Healthcare 2.0 (i.e. subsidies, short-term plans, et al).

The Four Pillars of Trump Healthcare 2.0 Policy Changes

The new administration is inclined toward a transactional view of the U.S. health system. It does not envision transformational change; instead, it sees opportunity for the system to perform significantly better. Its policies, leadership appointments and actions will be predicated on these four pillars:

Access to the U.S. healthcare system is a right to be earned. Fundamentally, Trump Healthcare 2.0 builds on its moral conviction that there should be NO FREE LUNCHES whether it’s illegal immigrants or patients who use the health system without doing their part. Trump Healthcare 2.0 will advance mechanisms to enable self-care, increase personal responsibility, promote cheaper/better alternatives to traditional insurance and health delivery and challenge lawmakers to limit financial support to free-loaders. The fundamental notions of public health and community benefit will be revisited and restrictions enacted.

The status quo is not working. Change is needed. Polls show the majority of Americans are dissatisfied with the health system. Affordability is their major concern: escalating, inexplicable costs are forcing their employers to share more responsibility. Trump Healthcare 2.0 will implement changes that lower spending and costs for consumers and employers. They’ll leverage coalitions of working-class voters and businesses to enact policies that expose waste, fraud and abuse in the system and direct the U.S. Department of Health & Human Services to streamline its structure and prioritize cost-effectiveness (the HHS Strategic Plan for 2022-2026 is up for review).

Private solutions solve public problems better than government. Trump Healthcare 2.0 posits that government is broken including the federal and state agencies that control healthcare oversight and funding. Reducing regulatory barriers to consolidation and innovation and lessening risks for private investors whose ventures align with Trump Healthcare 2.0 priorities will be foci. Fundamentally, Trump Healthcare 2.0 believes the private sector is better able to address problems than government bureaucrats: key Trump Healthcare 2.0 leadership positions will be filled by successful private sector operators instead of re-cycled DC luminaries desiring attention.

Price transparency fuels competition and value. Trump Healthcare 1.0 mandated hospital price transparency via its 2019 Executive Order: Trump Healthcare 2.0 will expand the scope and usefulness of price transparency mandates in hospital, ancillary and outpatient services, physician services, insurance and others. It will facilitate accelerated use of Artificial Intelligence in decision-making by consumers, providers and payers. It will expand timely access to data on prices, direct costs, overhead, executive compensation, outcomes, user experiences and other elements of care management provided by hospitals, physicians and other providers. And it will move quickly to implement site neutral payments in the 119th Trump Healthcare 2.0 holds that providers, insurers and drug companies are not inclined to transparency despite strong support from elected officials and voters. They’ll advance these policy changes anticipating pushback from industry insiders. Trump Healthcare 2.0 believes price transparency in healthcare will produce transformational changes that enable more competition and lower costs.

Looking ahead:

The Trump 2.0 team’s immediate task is to assemble its Cabinet: that’s taken prior administrations 38 days on average to complete. In tandem, temporary fixes for CMS’ pending Physician Pay Cut and telehealth expansion will pass as Congress’ lame duck session begins this week.

Looking to 2025, the Trump Healthcare 2.0 team will focus initially on issues in Congress where Bipartisan support appears strong i.e. regulation of PBMs, implementation of site neutral payment policies, expansion of drugs subject to Inflation Reduction Act’s pricing limits and perhaps others. It will plan its legislative agenda coordinating with key committees (i.e. Senate HELP, House Ways and Means et al) and outside groups that share its predisposition. And it will use its political clout to build popular support for healthcare reforms that respond directly to consumer (voter) concern about affordability.

Trump Healthcare 2.0 will bring heightened transparency to the health system and be premised on pillars that are popular with working class voters. It will not be a duplicate of Trump Healthcare 1.0: it will be much more.

UnitedHealth Group has taken a beating on Wall Street this week after admitting that its Medicare Advantage plans had to pay out more in medical claims in the third quarter of this year than investors had expected. As I’ve noted many times, Wall Street can’t stand it and gets very spiteful when Big Insurance uses more of our premium dollars paying for patients’ care because that means there’s less money left over to enrich shareholders.

At the end of trading at the New York Stock Exchange Tuesday, UnitedHealth’s share price was down 8.11% — almost $50 a share — falling like a rock from $605.40 to $556.29 as soon as the market opened. It had reached a 52-week high just the day before but fell off a cliff Tuesday morning. This despite the fact that the company still made $8.7 billion in operating profits during the third quarter.

What investors didn’t like at all was the fact that UnitedHealthcare’s medical loss ratio (MLR) climbed to 85.2% from 82.3% for the same period last year.

By other measures, the company did just fine, especially when you look at how much money it made during the first nine months of this year: a whopping $24.5 billion in profits.

Enrollment in both the company’s commercial and Medicare Advantage plans increased, but it posted a significant decline in the number of people enrolled in the Medicaid plans its administers for several states. That’s because of the Medicaid “unwinding” that has been going on since the official end of the pandemic.

And here is another couple of numbers of note from the third quarter:

UnitedHealth’s Optum division, which encompasses its massive pharmacy benefit manager, Optum Rx, made more money for the parent company than the health plan division: $4.5 billion in profits vs. $4.2 billion for UnitedHealthcare.

PBMs have become even more of a cash cow for Big Insurance than Medicare Advantage, which despite the higher MLRs of late is still a reliable money-gushing ATM for the industry.

The confidential nature of the Biden administration’s drug price negotiations has made theprocess and outcome of thelong-sought Democratic policy goal something of a mystery.

Why it matters:

The administration is expected to announce the results of those negotiations this week, and there’s plenty of speculation about the actual savings that will be realized starting in 2026 — and how aggressive the Biden administration got on pharma in an election year.

Where it stands:

Drugmakers have indicated that the negotiated prices for this first 10 drugs won’t have much impact on their projected bottom lines.

But the results could hint at what’s to come in subsequent rounds, as the number of drugs up for negotiation expands, possibly to include blockbuster GLP-1 weight-loss drugs.

Context:

The Centers for Medicare and Medicaid Services last summer chose 10 drugs that account for some of the highest total costs for Medicare, including Bristol Myers Squibb and Pfizer’s blood-thinner Eliquis and Boehringer Ingelheim’s diabetes drug Jardiance.

CMS and drugmakers have been going back and forth since February on how to price the drugs. Meanwhile, the pharmaceutical industry and its allies have mounted a series of so far unsuccessful legal challenges to stop the talks.

Here are some key unanswered questions ahead of the announcement, expected Thursday morning:

What information will CMS release about the final drug prices? Analysts, policy experts and industry groups told Axios they’re watching for whether Medicare officials announce specific levels of savings they achieved on each drug.

If Medicare does announce levels of savings, it’ll matter whether they measure those against drugs’ current list prices, which are typically higher than what patients actually pay, or another figure that takes into account existing rebates and discounts, said TD Cowen analyst Rick Weissenstein.

Statutorily, Medicare officials have to release the final prices for the selected drugs by Sept. 1 and justify those prices by March 1.

“What data CMS chooses to release is a big question mark,” said Chris Meekins, an analyst at Raymond James.

How will pharmacy benefit middlemen and prescription drug insurance plans react to the new prices?

Medicare Part D insurers must cover all 10 selected drugs, but the Inflation Reduction Act doesn’t specify where they need to place the drugs on their formularies.

That could potentially lead to drug middlemen and insurers giving competing products more favorable placement on their formularies, said Lindsay Bealor Greenleaf, who leads federal and state policy at ADVI Health, which consults for pharmaceutical and biotech manufacturers.

CMS will require plans to justify their decision if they move the drugs to different tiers or add more restrictive utilization management tools, per KFF.

How will investors and drugmakersreact?

The release of the maximum fair drug prices could clarify how risk-averse large pharmaceutical companies need to be in future acquisitions of smaller biotech companies, said John Stanford, executive director of Incubate, the life sciences investor lobbying group.

How will Medicare-negotiated prices compare with international drug prices?

Branded drugs typically come with higher price tags in the United States than elsewhere in the world.

“I think it’s going to be very instructive to see how much the purchasing power of CMS gets us in terms of reduction,” said Anna Kaltenboeck, who leads the prescription drug reimbursement work at consulting firm ATI Advisory.

What’s next:

Negotiated prices will go into effect Jan 1., 2026. CMS will announce as many as 15 additional drugs for the second round of negotiation by Feb. 1, 2025.

Regular readers of HEALTH CARE un-covered know that I write frequently about the huge amounts of money the health insurance industry’s pharmacy benefit managers (PBMs) extract from the prescription drug supply chain. I also submitted a comment letter to the Federal Trade Commission two and a half years ago urging it to launch an investigation into PBM business practices that have contributed to the closure of hundreds of independent pharmacies across the country and to millions of Americans walking away from the pharmacy counter without their medications.

On a bipartisan basis, the FTC did launch an inquiry into the PBM business, and today the Commission issued a damning interim report that confirmed what industry critics, including me, have been saying:

Just six companies now control 95% of the pharmacy benefit market, and these Big Insurance-owned middlemen “profit at the expense of patients by inflating drug costs and squeezing Main Street pharmacies.” Below you’ll find the commission’s statement on its preliminary findings.

Last year, we also published a profile of one of the industry’s most vocal critics in Congress, Rep. Earl L. “Buddy” Carter (R-Ga.), a pharmacist by trade who has seen PBM’s profiteering firsthand. In a press release this morning, Carter said:

Since day one in Congress, I’ve been calling on the FTC to investigate PBMs, which use deceptive and anti-competitive practices to line their own pockets while reducing patients’ access to affordable, quality health care. I’m proud that the FTC launched a bipartisan investigation into these shadowy middlemen, and its preliminary findings prove yet again that it’s time to bust up the PBM monopoly. We are losing more than one pharmacy per day in this country, causing pharmacy deserts and taking the most accessible health care professionals in America out of people’s communities. I am calling on the FTC to promptly complete its investigation and begin enforcement actions if – and when – it uncovers illegal and anti-competitive PBM practices.

Carter and several other members of Congress have introduced bipartisan bills to rein in PBMs. The House has passed PBM reform legislation but the Senate has not yet done so, but there is growing support in both chambers to enact one or more bills by the end of the year. The FTC’s interim report should make that more likely to happen.

Read the FTC’s full press release below:

FTC Releases Interim Staff Report on Prescription Drug Middlemen

Report details how prescription drug middleman profit at the expense of patients by inflating drug costs and squeezing Main Street pharmacies

The Federal Trade Commission today published an interim report on the prescription drug middleman industry that underscores the impact pharmacy benefit managers (PBMs) have on the accessibility and affordability of prescription drugs.

The interim staff report, which is part of an ongoing inquiry launched in 2022 by the FTC, details how increasing vertical integration and concentration has enabled the six largest PBMs to manage nearly 95 percent of all prescriptions filled in the United States.

This vertically integrated and concentrated market structure has allowed PBMs to profit at the expense of patients and independent pharmacists, the report details.

“The FTC’s interim report lays out how dominant pharmacy benefit managers can hike the cost of drugs—including overcharging patients for cancer drugs,” said FTC Chair Lina M. Khan. “The report also details how PBMs can squeeze independent pharmacies that many Americans—especially those in rural communities—depend on for essential care. The FTC will continue to use all our tools and authorities to scrutinize dominant players across healthcare markets and ensure that Americans can access affordable healthcare.”

The report finds that PBMs wield enormous power over patients’ ability to access and afford their prescription drugs, allowing PBMs to significantly influence what drugs are available and at what price. This can have dire consequences, with nearly 30 percent of Americans surveyed reporting rationing or even skipping doses of their prescribed medicines due to high costs, the report states.

The interim report also finds that PBMs hold substantial influence over independent pharmacies by imposing unfair, arbitrary, and harmful contractual terms that can impact independent pharmacies’ ability to stay in business and serve their communities.

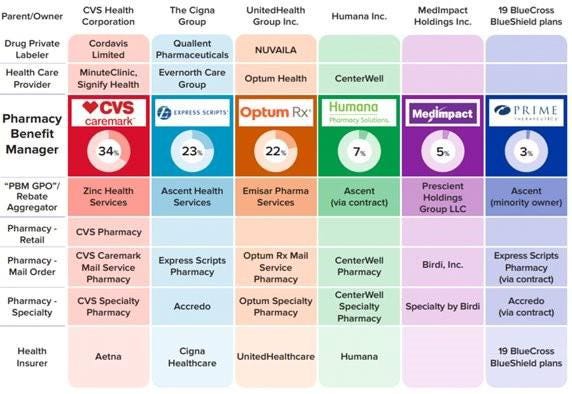

The Commission’s interim report stems from special orders the FTC issued in 2022, under Section 6(b) of the FTC Act, to the six largest PBMs—Caremark Rx, LLC; Express Scripts, Inc.; OptumRx, Inc.; Humana Pharmacy Solutions, Inc.; Prime Therapeutics LLC; and MedImpact Healthcare Systems, Inc. In 2023, the FTC issued additional orders to Zinc Health Services, LLC, Ascent Health Services, LLC, and Emisar Pharma Services LLC, which are each rebate aggregating entities, also known as “group purchasing organizations,” that negotiate drug rebates on behalf of PBMs.

PBMs are part of complex vertically integrated health care conglomerates, and the PBM industry is highly concentrated. As shown in the below image, this concentration and integration gives them significant power over the pharmaceutical supply chain. The percentages reflect the amount of prescriptions filled in the United States.

The interim report highlights several key insights gathered from documents and data obtained from the FTC’s orders, as well as from publicly available information:

Concentration and vertical integration: The market for pharmacy benefit management services has become highly concentrated, and the largest PBMs are now also vertically integrated with the nation’s largest health insurers and specialty and retail pharmacies.

The top three PBMs processed nearly 80 percent of the approximately 6.6 billion prescriptions dispensed by U.S. pharmacies in 2023, while the top six PBMs processed more than 90 percent.

Pharmacies affiliated with the three largest PBMs now account for nearly 70 percent of all specialty drug revenue.

Significant power and influence: As a result of this high degree of consolidation and vertical integration, the leading PBMs now exercise significant power over Americans’ ability to access and afford their prescription drugs.

The largest PBMs often exercise significant control over what drugs are available and at what price, and which pharmacies patients can use to access their prescribed medications.

PBMs oversee these critical decisions about access to and affordability of life-saving medications, without transparency or accountability to the public.

Self-preferencing: Vertically integrated PBMs appear to have the ability and incentive to prefer their own affiliated businesses, creating conflicts of interest that can disadvantage unaffiliated pharmacies and increase prescription drug costs.

PBMs may be steering patients to their affiliated pharmacies and away from smaller, independent pharmacies.

These practices have allowed pharmacies affiliated with the three largest PBMs to retain high levels of dispensing revenue in excess of their estimated drug acquisition costs, including nearly $1.6 billion in excess revenue on just two cancer drugs in under three years.

Unfair contract terms: Evidence suggests that increased concentration gives the leading PBMs leverage to enter contractual relationships that disadvantage smaller, unaffiliated pharmacies.

The rates in PBM contracts with independent pharmacies often do not clearly reflect the ultimate total payment amounts, making it difficult or impossible for pharmacists to ascertain how much they will be compensated.

Efforts to limit access to low-cost competitors: PBMs and brand drug manufacturers negotiate prescription drug rebates some of which are expressly conditioned on limiting access to potentially lower-cost generic and biosimilar competitors.

Evidence suggests that PBMs and brand pharmaceutical manufacturers sometimes enter agreements to exclude lower-cost competitor drugs from the PBM’s formulary in exchange for increased rebates from manufacturers.

The report notes that several of the PBMs that were issued orders have not been forthcoming and timely in their responses, and they still have not completed their required submissions, which has hindered the Commission’s ability to perform its statutory mission. FTC staff have demanded that the companies finalize their productions required by the 6(b) orders promptly. If, however, any of the companies fail to fully comply with the 6(b) orders or engage in further delay tactics, the FTC can take them to district court to compel compliance.

The FTC remains committed to providing timely updates as the Commission receives and reviews additional information.

The Commission voted 4-1 to allow staff to issue the interim report, with Commissioner Melissa Holyoak voting no. Chair Lina M. Khan issued a statement joined by Commissioners Rebecca Kelly Slaughter and Alvaro Bedoya. Commissioners Andrew N. Ferguson and Melissa Holyoak each issued separate statements. The Federal Trade Commission develops policy initiatives on issues that affect competition, consumers, and the U.S. economy. The FTC will never demand money, make threats, tell you to transfer money, or promise you a prize. Follow the FTC on social media, read consumer alerts and the business blog, and sign up to get the latest FTC news and alerts.