The nonprofit health system narrowed its operating loss while continuing to grapple with financial and policy pressures as it progresses towards profitability.

KEY TAKEAWAYS

Providence cut its operating loss in the second quarter to $21 million, improving from a $123 million loss a year ago.

Revenue rose 3% year-over-year to $7.91 billion, driven by higher patient volumes and better commercial rates.

The health system faces ongoing “polycrisis” challenges, including rising supply costs, staffing mandates, insurer denials, and looming Medicaid cuts, which have already prompted layoffs, hiring pauses, and leadership restructuring.

Providence made promising strides toward financial sustainability in the second quarter as higher patient volumes helped trim an operating loss that has weighed heavily on its balance sheet.

Yet the Renton, Washington-based health system warned that a compounding set of external pressures, which it labeled a “polycrisis,” still poses formidable challenges to its mission and future.

For the three months ended June 30, the nonprofit reported an operating loss of $21 million, equating to an operating margin of –0.3%, representing a marked improvement from the $123 million loss (–1.6%) posted over the same period in 2024. Compared with the previous quarter, the gain was even starker as Providence trimmed its deficit by $223 million. Through the first six months of the year, the health system had an operating loss of $265 million (-1.7%).

Revenue growth was fueled by higher patient volumes and improved commercial rates, Providence highlighted. Operating revenue rose 3% year-over-year to $7.91 billion as inpatient admissions (up 3%), outpatient visits (up 3%), case mix–adjusted admissions (up 3%), physician visits (up 8%), and outpatient surgeries (up 5%) all contributed.

On the expense side, Providence managed a 2% rise in operating costs to $7.93 billion, thanks largely to productivity gains, including a 43% reduction in agency contract labor. However, supply costs swelled by 9% and pharmacy expenses jumped by 12% year-over-year.

Providence, along with the healthcare industry at large, faces what CEO Erik Wexler called a “polycrisis” due to a mix of inflation, tariff-driven supply pressures, new state laws on staffing and charity care, insurer reimbursement delays and denials, and looming federal Medicaid cuts, especially from the One Big Beautiful Bill Act, which the health system said “threatens to intensify health care pressures.”

Those factors are significantly influencing hospitals’ and health systems’ decision-making. Providence has made staffing adjustments that include cutting 128 jobs in Oregon earlier this month, a restructuring in June that eliminated 600 full-time equivalent positions, apause on nonclinical hiring in April, and leadership reorganization since Wexler took over as CEO in January.

Accounts receivable is another area that has been indicative of headwinds, with Providence noting that while it improved in the second quarter, it “remains elevated compared to historical trends.”

Even with the roadblocks in its path, Providence is working towards profitability after being in the red for several years running.

“I’m incredibly proud of the progress we’ve made and grateful to our caregivers and teams across Providence St. Joseph Health for their continued dedication,” Wexler said in the news release. “The strain remains, especially with emerging challenges like H.R.1, but we will continue to respond to the times and answer the call while transforming for the future.”

For the past six years, Kaufman Hall has been publishing its monthly National Hospital Flash Report, which is designed to provide a pulse on the health of the healthcare industry and to highlight meaningful and pertinent trends for hospital and health system leaders. The data that powers the report is taken from over 1,300 hospitals, which are reflective of all geographic locations, hospital sizes and types. To ensure the content is digestible and understandable, Kaufman Hall aggregates the data into larger cohorts and measures a select set of key metrics that are most important for understanding the health of the industry. Industry groups and system leaders use these reports both for peer review purposes but also to paint an overall story for their boards and communities.

Through a detailed review of the Flash Report data, each month Kaufman Hall develops findings that healthcare leaders may find instructive as they determine how to adjust to changing market conditions. In 2024 it was reasonably obvious that there was a widening divide between the highest performing hospitals and the lowest performers.While a significant cadre of hospitals and health systems have recovered to pre-Covid financial success, 37% of American hospitals continue to lose money.

We are often asked what the successful hospitals are doing—and importantly—what the data tell us about those that are less successful. Using 2024 data, we have drawn two important conclusions around the role of leading management teams and what separates their organizations from others.

These teams have:

A sophisticated and balanced approach to the management of departmental performance: and

An understanding of the management of shared service costs.

A sophisticated and balanced approach to the management of departmental performance

It turns out that current data demonstrate that the management of departmental performance is critical to overall hospital financial performance but in a more nuanced manner than expected.

Our analysis was conducted as follows:

First, we looked at data across hospitals nationwide to understand the difference in departmental performance between top and bottom performing hospitals.

Second, we ranked each department in a hospital from 0 to 100, with 100 representing the best performance based on expense per unit of service.

Third, we then grouped all hospitals based on their bottom-line operating margin into three cohorts: those hospitals that fell into the bottom quartile of financial performance, those between the bottom and top quartile, and those in the top quartile.

Finally, we created a histogram of the average composition of departmental performance across each of the three margin cohorts.

The findings demonstrate that organizations with top financial performance have departmental results that look like a normal curve around the median. Said more simply, in top-performing hospitals the number of lower-performing departments is roughly equal to the number of higher-performing departments, with most departments operating near the national departmental medians. In contrast, hospitals with the lowest financial performance show a much greater number of departments operating with high cost per units of service and a few departments that operate extremely efficiently.

It appears that poorer performing hospitals focus on the management of the largest clinical and nursing areas. These are the departments that tend to be the “easiest” to manage because they are the “easiest” to benchmark. But the data show that these same hospitals tend to have poor performance over the remainder of the departments, which leads to poor financial results for the total hospital.

Hospitals with top quartile financial performance tend to manage all departments as close to the benchmark median as possible. Such a result means spending more managerial time on the harder to manage departments, especially those departments that are more “unique” and where overall performance is harder to characterize and benchmark.

The observations that can be drawn here are important and as follows:

First, oversight and management of individual departments is critical to the financial success of the entire hospital or system.

Second, the overall organizational structure of departmental administration is critical as well. The more complicated your departmental structure and the more individual departments you maintain and administer, the more difficult it will be to manage a majority of departments to “median” results.

The data suggest a perhaps unexpected operational conclusion. The achievement of median national departmental benchmarks is leading to overall positive hospital financial operating margins. This outcome offers significant budgeting advice and over the course of a fiscal year should prove to be a remarkably useful administrative lesson.

Understanding the management of shared service costs

Given the growing costs of shared services and related overhead, Kaufman Hall wanted a closer look at how well hospital organizations were scaling shared service costs related to the organization’s size. Unexpectedly, shared service costs were not highly correlated to the size of the hospital or hospital system. This suggests that the management of shared service costs on a per unit basis is difficult and that this aspect of expense management requires diligent focus to enact and sustain cost change. Our data often indicates a wide variation of cost performance among shared services of similar types within different large organizations. This suggests that standardization of such services is not well developed and that there may be a certain level of wishful thinking that increases in organizational size will automatically correlate to lower per unit costs.

The data did indicate, however, that larger organizations can achieve higher performance over smaller organizations relative to shared service expenses. This is an indication that size can be leveraged for superior performance but that such results are not automatic. The takeaway here is that the total spend for shared service functions is very substantial and growing. In that regard, it is most important to proactively address expenses in these areas, build appropriate management plans, and understand how to focus on the right buttons and levers. To the extent that organizations are assuming that growth (both organic and inorganic) will create economies of scale with the overall shared service apparatus, the data demonstrate that such an outcome is possible but only with strong planning and execution.

Operating hospitals in 2025 is flat-out hard and likely to get harder over the year. Hospital executives right now should use every managerial advantage available. A close look at the National Hospital Flash Report data identifies important relationships that provide for a more nuanced and sophisticated operation of both individual departments and the bundle of shared services. The data clearly demonstrate that better results in both these areas will lead to improved financial performance within the hospital overall. The data also indicate key managerial strategies that will lead to such improvement.

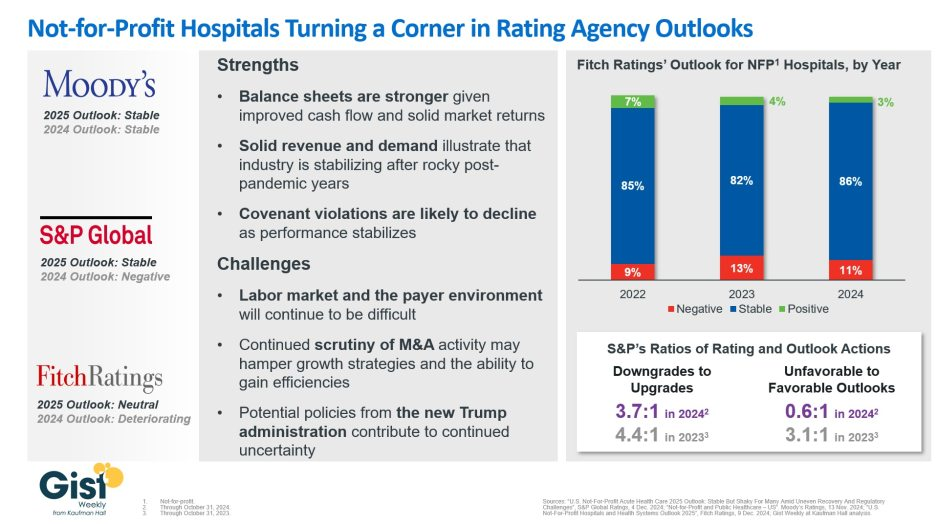

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

Here are 67 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating is based on the Altamonte Springs, Fla.-based system’s competitive market position—especially in its core Florida markets—and its financial profile, Fitch said.

Advocate Health members Advocate Aurora Health and Atrium Health have “Aa3” ratings and positive outlooks with Moody’s. The ratings are supported by the Charlotte, N.C.-based system’s significant scale, strong market share across several major metro areas, and good financial performance and liquidity, Moody’s said.

AnMed Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Anderson, S.C.-based system’s strong and stable operating performance and leading market position in a sound service area, Fitch said.

Ann & Robert H. Lurie Children’s Hospital of Chicago has an “AA” rating and stable outlook with Fitch. The rating is supported by the system’s strong balance sheet with low leverage ratios derived from modest debt, Fitch said.

Atlantic Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Morristown, N.J.-based system’s fundamental strengths, including strong operating performance with high single digit operating cash flow margins and favorable liquidity of over 300 days cash on hand, Moody’s said.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

BayCare Health System has an “AA” rating and stable outlook with Fitch. The Clearwater, Fla.-based system on June 30 moved to a new corporate legal structure, replacing a joint operating agreement between multiple hospitals that were responsible for the creation of BayCare in 1997. Fitch views the dissolution of the JOA and the move to the new structure as a credit positive.

Beacon Health System has an “AA-” rating and stable outlook with Fitch. Fitch said the rating reflects the strength of the South Bend, Ind.-based system’s balance sheet.

Bon Secours Mercy Health has an “AA-” rating and stable outlook with Fitch. The Cincinnati-based system has a favorable and stable payor mix, leading or secondary market share position in nine of its 11 U.S. markets with improving market share positions in eight, and adequate cash flows to support the system’s strategic plans, Fitch said.

BJC Health System has an “Aa2” rating and stable outlook with Moody’s. The St. Louis-based system reflects its reputation as a leading academic medical center with a long-standing affiliation with Washington University School of Medicine, Moody’s said.

Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area and Fitch’s expectation that the system will sustain its strong capital-related ratios in the context of the system’s midrange revenue defensibility and strong operating risk profile assessments.

Carilion Clinic has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Roanoke, Va.-based system’s scale, regional significance as a tertiary referral system with broad geographic capture, and a highly integrated physician base with a well-defined culture, Moody’s said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals, and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence, and pediatric trauma status, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The rating reflects the Minneapolis-based system’s strong balance sheet, robust liquidity position, and dominant pediatric market position, Fitch said.

Cincinnati Children’s Hospital Medical Center has an “Aa2” rating and stable outlook with Moody’s. The rating is supported by its national and international reputation in clinical services and research, Moody’s said.

Cleveland Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the system’s strength as an international brand in highly complex clinical care and research and centralized governance model, the ratings agency said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth, Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

Corewell Health has an “Aa3” rating and stable outlook with Fitch. The rating reflects the Grand Rapids and Southfield, Mich.-based system’s significant scale as a provider and payer in Michigan, Moody’s said. The organization also has good and stable financial performance and liquidity.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

Froedtert ThedaCare Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s solid market position, track record of strong utilization and operations, and strong financial profile, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by its strong operating risk assessment, leading market position in its immediate service area, and strong financial profile, Fitch said.

Holland (Mich.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects Holland Hospital’s stable and strong liquidity and capital-related metrics despite sector-wide operating pressures, Fitch said.

Indiana University Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Indianapolis-based health system’s sustained track record of strong operating margins, ratings agency said.

Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The Falls Church, Va.-based system’s rating is anchored by its role as one of the largest health systems in Virginia with a leading market position in a rapidly growing region with unusually high commercial business, Moody’s said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Mullica Hill, N.J.-based system will return to strong operating cash flows following the operating challenges of 2022 and 2023, as well as the successful integration of Inspira Medical Center of Mannington (formerly Salem Medical Center).

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Kaiser Permanente has an “AA-” rating and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by its strong financial profile, bolstered by a large and diversified revenue base, Fitch said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Rochester, Minn.-based system’s preeminent reputation for clinical care and research, including new discoveries and cutting-edge treatment, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

McLeod Health has an “AA-” rating and stable outlook with Fitch. The Florence, S.C.-based system maintains a leading and growing market position in its primary service area and is expanding the Carolina’s Forest campus in an area that is expected to experience rapid growth over the coming years, Fitch said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Memorial Healthcare System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects that the Hollywood, Fla.-based system will continue to benefit from good strategic positioning of its large, diversified geographic footprint.

Memorial Hermann Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Houston-based system’s leading and expanding market position and strong demand in a growing region, Moody’s said.

Methodist Health System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects the Dallas-based system’s consistently strong operating performance, excellent liquidity, and very good market position.

Monument Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Rapid City, S.D.-based system has a dominant inpatient market position as the leading acute care provider in its geographically broad primary service area

Nationwide Children’s Hospital has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Columbus, Ohio-based system’s strong market position in pediatric services, growing statewide and national reputation, and continued expansion strategies.

Nicklaus Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Miami-based system’s position as the “premier pediatric hospital in South Florida with a leading and growing market share,” Fitch said.

North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The rating reflects the Tupelo-based system’s strong cash position and strong market position with a leading market share in its primary services area, Fitch said.

Northwestern Memorial HealthCare has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Chicago-based system’s growing market position, single operating model and financial discipline, Moody’s said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research, and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Parkland Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Dallas-based system will remain the leading provider of public (safety net) services in the vast Dallas County service area, supported by its tax levy.

Phoenix Children’s has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong cash flow generation that has significantly improved its balance sheet in recent years, Fitch said.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rady Children’s Hospital has an “Aa3” rating and stable outlook with Moody’s. The San Diego-based system’s rating reflects its well-established strengths, including an “extremely high” market share in all of San Diego County, Moody’s said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing position in a stable service area with good population growth and demand for acute care services, Fitch said.

Sarasota (Fla.) Memorial Health Care System has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s leading market position in a growing service area, robust historical operating cash flow levels and strong liquidity position, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

St. Elizabeth Medical Center has an “AA” rating and stable outlook with Fitch. The rating reflects the Edgewood, Ky.-based system’s strong liquidity, leading market position, and strong financial management, Fitch said.

St. Tammany Parish Hospital has an “AA-” rating and stable outlook with Fitch. The Covington, La.-based system has a strong operating risk assessment and very strong financial profile supported by consistently robust operating cash flows, Fitch said.

Stanford Health Care has an “Aa3” rating and positive outlook with Moody’s. The rating reflects the Palo Alto, Calif.-based system’s clinical prominence, patient demand, and its location in an affluent and well-insured market, Moody’s said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong financial profile in the context of its broad and growing reach for high-acuity services, Fitch said.

University Health has an “AA+” rating and stable outlook with Fitch. The San Antonio-based system’s outlook is based on the Bexar County Hospital District’s significant tax margin, good cost management, and strong leverage position relative to its liquidity and outstanding debt.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

University of Kansas Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects Kansas City-based system’s flagship hospital’s important presence as the only academic medical center in Kansas and a major provider of many high end and unique services to a large geographic area, Fitch said.

UW Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Madison, Wis.-based system’s strong clinical reputation, high acuity services, and important role as the academic medical center affiliated with the state’s flagship public university, Moody’s said.

VCU Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Richmond, Va.-based system’s status as one of Virginia’s leading academic medical centers and essential role as its largest safety net provider, supporting excellent patient demand at high acuity levels, Moody’s said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

Walgreens Boots Alliance is considering selling all of its VillageMD primary care clinics, according to a filing with the Securities and Exchange Commission.

The company is evaluating options in light of ongoing investments into VillageMD and its substantial ongoing and expected future cash requirements, Walgreens said in the August 7 filing.

“These options could include a sale of all or part of the VillageMD businesses, possible restructuring options and other strategic opportunities,” Walgreens said.

WHY THIS MATTERS

Walgreens has been facing financial pressure due to a changing retail environment and increased regulatory and reimbursement challenges on the pharmacy end, according to its Q3 earnings report from June.

VillageMD, as well as some other pharmacy clinics, have faced the challenge of making the clinics a scalable solution.

On August 5, Walgreens Boots Alliance stock hit a 52-week low of $10.62, according to Seeking Alpha. Year to date, shares are down about 59%.

In the recent SEC filing, Walgreens acknowledged the existence of defaults under the VillageMD Secured Loan. On January 3, 2023, Walgreens had provided VillageMD senior secured credit facilities in the aggregate amount of $2.25 billion. This consisted of a senior secured term loan in an aggregate principal amount of $1.75 billion and a senior secured credit facility in an aggregate original committed amount of $500 million.

Walgreens is actively engaged in discussions with VillageMD’s stakeholders and other third parties with respect to the future of its investment in VillageMD, it said.

On August 8, Walgreens announced the pricing of an underwritten public offering of senior unsecured notes consisting of $750M aggregate principal amount of 8.125% notes due 2029. The sale of the notes is expected to close on August 12.

WBA said it intends to use the net proceeds from the offering, together with cash on hand, for the repayment and/or retirement of its outstanding 3.800% notes due 2024, and to use any remaining amounts for general corporate purposes.

On August 1, WBA announced it had sold all of its remaining unencumbered shares of Cencora, a drug wholesale company, for $818 million, and, subject to the completion of the sale, a concurrent share repurchase by Cencora in the amount of $250 million.

Proceeds will be used primarily for debt paydown and general corporate purposes, as the company continues to build out a more capital-efficient health services strategy rooted in its retail pharmacy footprint, Walgreens said.

THE LARGER TREND

During the Q3 earnings call on June 27, CEO Tim Wentworth said the company intended to reduce its stake in VillageMD. This was part of a strategy announced earlier in the year to close unprofitable VillageMD clinics in order to cut $1 billion in costs.

Walgreens also announced at that time plans to shutter up to 25% of its retail stores that were unprofitable.

Kaiser Permanente showed year-to-year financial improvement in Q2, reporting an operating income of $908 million (up from $741 million in Q2 2023), and an operating margin of 3.1% (up from 2.9% a year ago).

The news comes months after Kaiser Foundation Health plan reported a data breach affecting over 13 million people. Certain online technologies, previously installed on its websites and mobile applications, may have transmitted personal information to third-party vendors Google, Microsoft Bing and X (Twitter) when members and patients accessed its websites or mobile applications, the health system said in April.

Despite that hardship, Kaiser Foundation Health Plan, Kaiser Foundation Hospitals and assorted subsidiaries and affiliates reported operating revenues of $29.1 billion and operating expenses of $28.2 billion, compared to operating revenues of $25.2 billion and operating expenses of $24.4 billion in the same period last year.

According to Kaiser, favorable financial market conditions drove other income (net of other expense) of $1.2 billion in the second quarter of 2024. Other income Q2 2023 was $1.3 billion. For the second quarter of 2024, net income was $2.1 billion, identical to last year.

Kaiser’s financial results in the second quarter include Geisinger, which joined subsidiary Risant Health on March 31.

WHAT’S THE IMPACT?

Kaiser said that it typically experiences higher operating margins in the first half of the year due to the annual enrollment cycle. Lower operating margins in the second half of the year are not uncommon, because expenses usually increase, in part due to the impact of seasonal care, while revenues stay relatively flat.

Kaiser Permanente membership was more than 12.5 million as of June 30, while membership for Risant Health affiliates was nearly 552,000.

Capital spending in the second quarter was $889 million, compared to $824 million in the same period of the prior year, as the organization continued to invest strategically in facilities and technology.

Though Kaiser logged a strong Q2, in May it announced plans to sell up to $3.5 billion of holdings in private-equity funds due to cash constraints, according to unnamed sources in The Wall Street Journal. Kaiser is reportedly working with investment bank Jefferies Financial Group to offload up to $3.5 billion of stakes to secondary buyers.

However, a Kaiser spokesman said at the time, “None of our decisions have been driven by liquidity needs; we maintain liquidity that is appropriate for a AA- rated organization. We will continue to make prudent, thoughtful investment decisions.”

THE LARGER TREND

Kaiser’s Q1 financial results showed operating income of $935 million, compared to $233 million for Q1 2023.

In March, Kaiser Permanente and Town Hall Ventures said they would be launching an organization called Habitat Health, which is designed to help older adults overcome the challenges of aging at home. Operating as a Program of All-Inclusive Care for the Elderly, Habitat Health is designed to help participants live independently in their homes, with comprehensive care the companies say will lead to better health outcomes.

Habitat Health plans to begin serving older adults in Sacramento and Los Angeles in 2025, and will aim to keep low-income participants in their homes to receive personalized support.

Some of America’s largest hospital systems saw their financials soar in the first half of 2024. And yet, more than 700 facilities across the country still are at risk of closing.

Why it matters:

It’s a familiar tale of the rich getting richer, as big, mostly for-profit health systems see improved margins while smaller facilities in outlying areas are barely hanging on.

That could worsen access for some of the most vulnerable Americans — and hasten consolidation in an industry that’s been a magnet for M&A.

The big picture:

Health systems with big footprints, including large academic medical centers, have weathered the pandemic and economic headwinds and are seeing margins as good or better than before COVID-19.

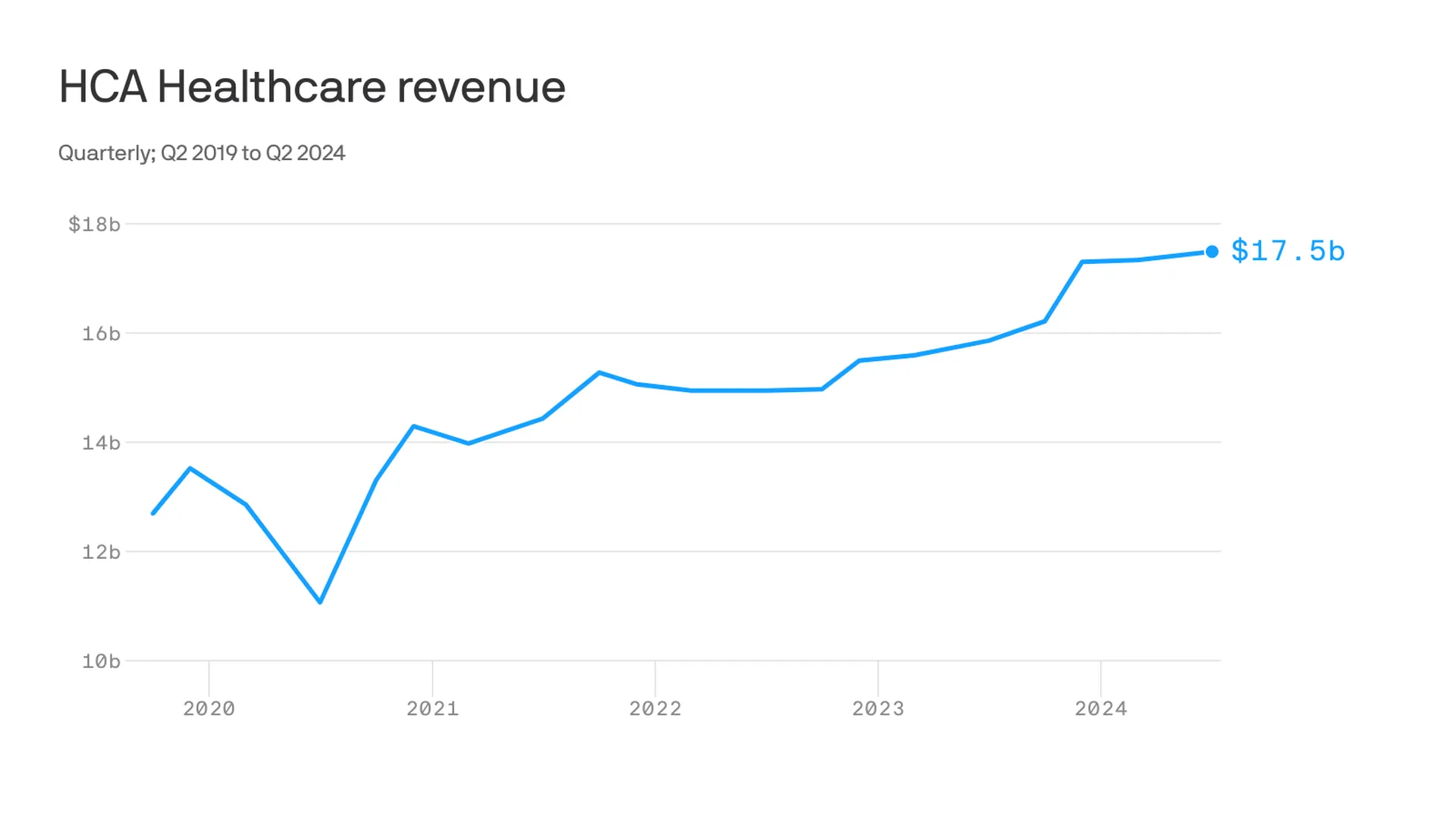

Nashville-based industry behemoth HCA Healthcare posted 23% year-over-year profit growth for the quarter, revising its forecast for the rest of the year, projecting it’ll reach as much as $6 billion. It posted a 10% year-over-year increase in revenue.

King of Prussia, Pennsylvania-based Universal Health Services similarly reported a strong quarter, posting nearly 69% growth on its bottom line over the same period last year while Dallas-based Tenet Healthcare reported a 111% jump in its net income over the same quarter last year.

Yes, but:

Smaller nonprofit hospitals, especially in rural areas, that made it through the crisis with the help of government aid are paring services like maternity wards and struggling to stay open.

“There are a lot of hospitals that survived, but their balance sheets are so weakened, their margin for error is basically zero at this point,” said Mike Eaton, senior vice president of strategy at population health company Navvis.

Hospitals that once could manage their expenses and the needs of communities are “going to really struggle to invest in what comes next,” he said.

Between the lines:

The biggest health systems have benefited from less volatility, seeing stabilizing drug prices and more predictable supply chains and labor costs, per a new report from Strata Decision Technology.

“It’s at least something you can manage to,” Steve Wasson, Strata’s chief data and intelligence officer, told Axios.

Revenues already were up thanks to renegotiated contracts health systems struck with payers last year, Wasson said.

There also have been changes on the federal side that boosted Medicare admissions and put some hospitals in line to be reimbursed for billions in underpayments from the 340B drug discount program.

Zoom in:

It’s all translated to operating margins that are up 17% year-to-date compared with the same time period in 2023, according to the latest Kaufman Hall National Hospital Flash Report.

Volumes as measured by hospital discharges per day are up 4% year-to-date.

Expenses per day are also up 6% year to date, including labor (4%), supplies (8%) and drugs (8%), but are far less volatile and thus easier to plan for, said Erik Swanson, senior vice president at Kaufman Hall.

But there’s a growing gulf between the top third of U.S. hospitals, which are seeing outsize growth, and the rest, Swanson said.

Threat level: A new report from the Center for Healthcare Quality and Payment Reform estimated 703 hospitals — or more than one-third of rural hospitals — are at risk of closure, based on Centers for Medicare and Medicaid Services financial information from July. Losses on privately insured patients are the biggest culprit.

“We’re looking at 50% of rural operating in the red. The situation is very challenging,” Michael Topchik, partner at Chartis Center for Rural Health, told Axios.

These smaller hospitals may still be there, but there will continue to be a steady erosion of the kinds of services they offer, such as obstetrics, cancer care and general surgery, he said.

What’s next:

Private equity investment in rural health care is already booming and with it, prospects for service and staffing cuts.

The South generally has the highest concentration of private equity-owned rural hospitals, often with lower patient satisfaction and fewer full-time staff compared with non-acquired hospitals, according to the Private Equity Stakeholder Project.

Congress is ramping up oversight of private equity investments in the sector, though most lawmakers are loath to take steps to actually halt deals.

UnitedHealth Group, the largest health insurance conglomerate by far, continues to show how rewarding it is for shareholders when corporate lawyers find loopholes in well-intentioned legislation – and game the Medicare Advantage program in ways most lawmakers and regulators didn’t anticipate and certainly didn’t intend – to boost profits.

UnitedHealth announced this morning that it made $15.8 billion in operating profits between the first of January and the end of June this year. That compares to $4.6 billion it made during the same period in 2014. One way the company is able to reward its shareholders so richly these days is by steering millions of people enrolled in its health plans to the tens of thousands of doctors it now employs and to the clinics and pharmacy operations it now owns.

This is the result of the hundreds of acquisitions UnitedHealth has made over the past 10 years in health care delivery as part of its aggressive “vertical integration” strategy.

The other big way the company has become so profitable is by rigging the Medicare Advantage program in a way that enables it to get more money from the federal government in a scheme – detailed in a big investigative report by the Wall Street Journal a few days ago – in which it claims its Medicare Advantage enrollees are sicker than they really are. The WSJ calculated that Medicare Advantage insurers bilked the government out of more than $50 billion in the three years ending in 2021 by engaging in this scheme, and it said UnitedHealth has grabbed the lion’s share of those billions. In many if not most instances, those enrollees were not treated for the conditions and illnesses UnitedHealth and other insurers claimed they had. As the newspaper reported:

Insurer-driven diagnoses by UnitedHealth for diseases that no doctor treated generated $8.7 billion in 2021 payments to the company, the Journal’s analysis showed. UnitedHealth’s net income that year was about $17 billion.

By far, most of UnitedHealth’s health plan enrollment growth over the past 10 years has come from the Medicare Advantage program, and it now takes in nearly twice as much revenue from the 7.8 million people enrolled in that program as it does from the 29.6 million enrolled in its commercial insurance plans in the United States.

Since the second quarter of 2014, UnitedHealth’s commercial health plan enrollment has increased by 720,000 people. During that same time, enrollment in its Medicare Advantage plans has increased by 4.8 million.

UnitedHealth and other insurers that participate in the Medicare Advantage program know a cash cow when they see one.

As the Kaiser Family Foundation noted in a recent report, the highest gross margins among insurers come from Medicare Advantage, which, as Health Finance News reported, boasted gross margins per enrollee of $1,982 on average by the end of 2023, compared to $1,048 in the individual (commercial) market and $753 in the Medicaid managed care market.

UnitedHealth has significant enrollment in all of those areas. Enrollment in the Medicaid plans it administers in several states increased from 4.7 million at the end of the second quarter of 2014 to 7.4 million this past quarter.

In its disclosure today, UnitedHealth did not break out its health plan revenue as it has in past quarters, but you can see how public programs like Medicare Advantage and Medicaid have become so lucrative by comparing revenue reported by the company at the end of the second quarter of 2013 to the second quarter of 2023. Over that time, total revenues for commercial plans (employer and individual) increased by slightly more than $5.6 billion, from $11.1 billion in 2Q 2013 to $16.8 billion in 2Q 2023. Total revenues from Medicaid increased by $14.2 billion, from $4.5 billion to $18.7 billion, and total revenues from Medicare increased by $21.4 billion, from $11.1 billion to $32.4 billion.

Here’s another way of looking at this: At the end of 2Q 2013, UnitedHealth took in almost exactly the same revenue from its commercial business and its Medicare business ($11.053 from Medicare and $11.134 from its commercial plans.

At the end of 2Q 2023, the company took in nearly twice as much from its Medicare business ($32.4 billion from Medicare compared to $16.8 billion from its commercial plans.)

The change is even more stark when you add in Medicaid. At the end 2Q 2023, UnitedHealth’s Medicare and Medicaid (community and state) revenues totaled $51.1 billion; It’s commercial revenues, as noted, totaled $16.8 billion). It’s now getting three times as much revenue from taxpayer-supported programs as from its commercial business.

As impressive for shareholders as all of that is, growth in the company’s other big division, Optum, which encompasses its pharmacy benefit manager (Optum Rx) and the physician practices and clinics it owns) has been even more eye-popping. At the end of 2Q 2014, Optum contributed $11.7 billion to the company’s total revenues. At the end of 2Q 2024, it contributed $62.9 billion, an increase of $51.2 billion. At that rate of growth, it’s only a matter of a few quarters before Optum is both the biggest and most profitable division of the company.

And here’s the way the company benefits from that loophole in federal law I mentioned above. The Affordable Care Act requires insurers to spend 80%-85% of health plan revenue on patient care. UnitedHealth is consistently able to meet that threshold by paying itself, as HEALTH CARE un-coveredexplained in December. The billions UnitedHealthcare (the health plan division) pays Optum every quarter are categorized as “eliminations” in its quarterly reports. In 2Q 2024, 27.7% of the company’s revenues fell into that category.

The more it is able to steer its health plan enrollees into businesses it owns on the Optum side, the more it can defy Congressional intent – and profit greatly by it.

Wall Street loves how UnitedHealth has pulled all this off. It’s stock price jumped $33.50 to $548.87 a share during today’s trading at the New York Stock Exchange, an increase of 6.5% – in one day.

The drugstore retailer faces debt maturities, while the upending of some strategies introduces new uncertainties, analysts said.

S&P Global Ratings analysts have downgraded Walgreens Boot Alliance by two notches, to ‘BB’ from ‘BBB-’, which puts the drugstore company into speculative-grade territory.

Analysts Diya Iyer and Hanna Zhang cited guidance for the year “notably below” their expectations, and said “material strategic changes, limited cash flow generation, and large maturities in coming years are key risks to the business.”

The company is struggling in its retail business as well as its pharmacy operations, they said in a Friday client note. In the U.S., margins are taking a hit on the pharmacy side from reimbursement pressure and on the retail side from declining sales volume and higher shrink. They expect Walgreens’ S&P Global Ratings-adjusted EBITDA margin to decline more than 100 basis points this fiscal year, dipping below 5%, from 6% last year, though the company’s cost cuts will counter that somewhat.

Walgreens’ debt and its need to refinance much of it represent another “key risk,” they said. This November, Walgreens faces $1.4 billion in maturities, mostly U.S. bonds. Another $2.8 billion comes due in fiscal 2026 and $1.8 billion in fiscal 2027. The analysts called Walgreens’ move to consolidate cash “prudent” in case refinancing isn’t possible.

“We will be monitoring how Walgreens’ new management addresses this large debt load closely amid its persistently weak performance and higher interest rates,” Iyer and Zhang said.

Beyond those financial realities, though, are strategic weaknesses. Ex-Cigna executive Tim Wentworth took over as CEO last fall and this year has overseen a strategic review that has entailed more layoffs and store closures.

Walgreens has also upended some of its plans to expand its medical care operations, divesting of or shrinking many of its original investments and plans. Last month, for example, the company announced it would reduce its stake in value-based medical chain VillageMD, saying it will no longer be the company’s majority owner, after closing dozens of the clinics last year. The company first poured $1 billion into VillageMD in 2020 and more than doubled its stake for another $5.2 billion the following year, but the banner’s waning value helped drive a $6 billion loss in Q2.

Despite such moves, Iyer and Zhang said they continue to see the VillageMD banner as “a significant drag on profitability due to the rising cost of labor, pressures from reimbursement, and lower volumes.”

Walgreens’ acquisition streak led the S&P analysts to believe that it would divest of its Boots U.K. business, which could have helped pay down $8 billion to $10 billion in debt. But the company called off the idea about two years ago.

“We believe these frequent and large changes to the company’s strategic plans diminish management’s credibility to execute on a sustainable and cohesive operating model for Walgreens in both the near and long term,” Iyer and Zhang said.

Gains that Walgreens has managed to eke from its medical operations haven’t managed to offset declines on the retail said, they also said, adding that they are closely watching what it does next with its massive footprint. The company last year announced that it would close 150 stores in the U.S. and 300 in the U.K. and just last month said it was reviewing 25% of its current footprint, with plans to shutter a “significant portion” of its roughly 8,700 stores.

“Our ratings continue to reflect Walgreens’ large scale and its efforts to address its credit metric profile. With almost $140 billion in sales in fiscal 2023 and a diverse array of global businesses, Walgreens remains prominent in the drugstore space,” they said. “However, we think its scale is providing less protection to profitability at least partly due to inconsistent strategic direction.”

Nonprofit hospital margins hit 4.3% in April, up 33% year over year, according to Kaufman Hall’s “National Hospital Flash Report” released June 3.

Kaufman Hall examined data from 1,300 hospitals in Syntellis Performance Solutions’ database and found that while hospital margins are improving overall, so is the gap between the highest and lowest performing hospitals. The best performing hospitals had a margin of 28.9%, compared to -16.1% for the worst performing hospitals.

“While financial performance looks solid on the surface, a closer examination of the data shows a greater divide between high- and low-performing hospitals,” said Erik Swanson, senior vice president of data and analytics at Kaufman Hall. “Forty percent of hospitals in the United States are losing money.

Organizations who have weathered the challenges of the last few years have adopted a wide range of proactive and growth-related strategies, including improving discharge transitions and building a larger outpatient footprint.”

Operating margins were up 7% month over month and year to date operating margins were 21% higher than in 2023. Operating EBITDA margin year to date was up 14% over the same period last year, and flat with hospital performance in 2021.

Net operating revenue per calendar day jumped 9% year to date in April compared, and 5% over March 2024. Inpatient revenue climbed 12 percent year over year in April.

Hospital operating margin index also increased in April to 4.3% after three months of decline.

Of note, the data revealed:

1. Outpatient revenue increased 10% year over year in April. 2. Average length of stay dropped 4% year over year in April. 3. Emergency department visits increased to hit pre-pandemic levels.