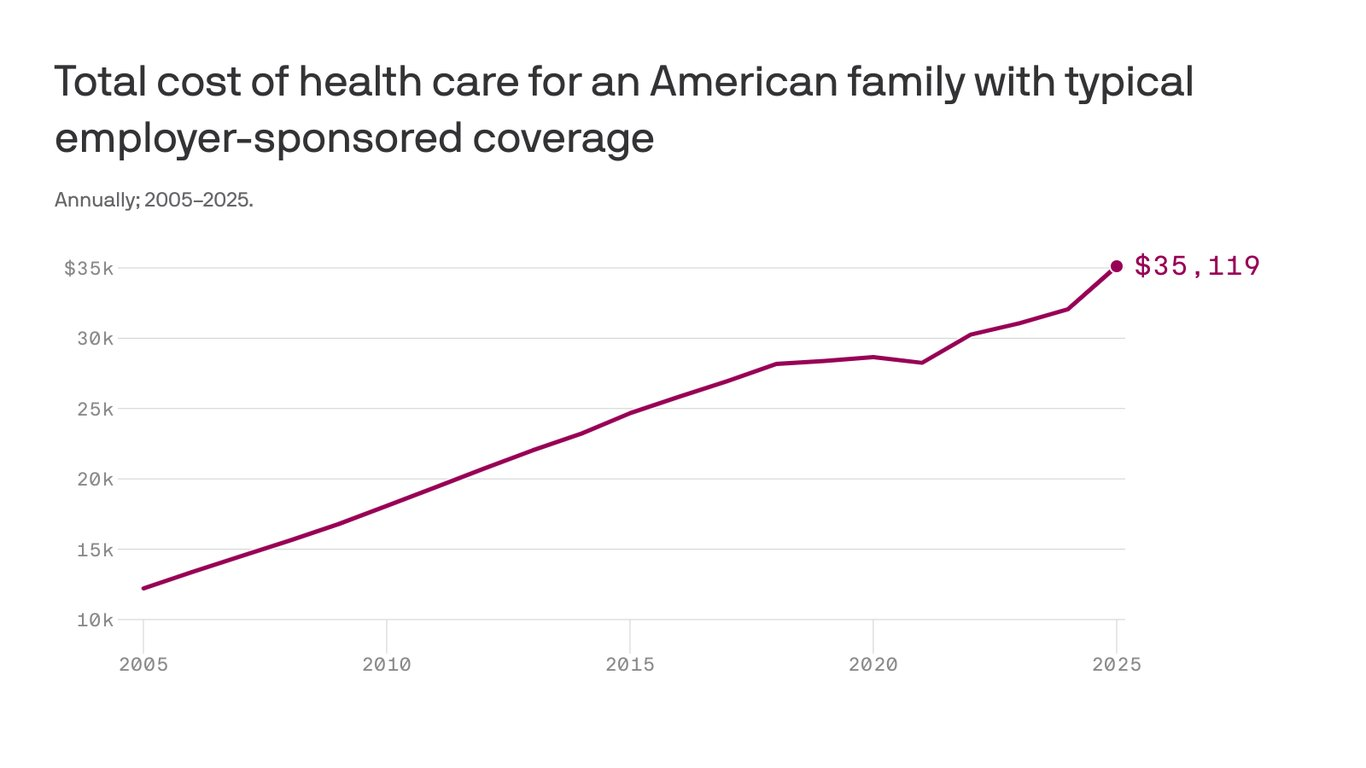

The cost to cover a family of four through workplace insurance now exceeds $35,000, nearly triple what it cost 20 years ago as annual growth in health costs have far outpaced wages.

The big picture:

Growing pharmacy and outpatient facility costs drove most of the increase, which includes employee and employer shares,according to the 2025 Milliman Medical Index.

Employers have been wary of passing health cost hikes to workers in a tight labor market, but the rising demand for costly care may force a reckoning.

State of play:

The $35,119 annual cost to cover a hypothetical family of four this year factors in drug costs, inpatient and outpatient care, and professional services, along with an “other” category that includes home health, ambulance transport, medical equipment and prosthetics.

A year of health care cost a family of four $12,214 in 2005, the year Milliman launched the index. The 20-year cumulative gain of 188% outpaced the 84% growth in wages over the same time.

Health costs have increased about 6% per year on average over the past two decades, according to Milliman, compared with an average inflation rate of 2.5% over that time.

Between the lines:

Employers in 2025 still shoulder 58% of employee health care costs, but their share has shrunk since 2005, when it was more than 60%.

Reality check:

Health care costs vary significantly by age, geography and pharmacy rebate arrangements.

Milliman calculates family cost based on a family with a 47-year-old male, 37-year-old female, and children ages 4 and under 1.

This was a “mathematically average” family in 2005, and Milliman continues to use that formula to keep data comparable year-to-year.

The firm has an online tool that allows readers to input other family configurations to see their estimated 2025 health care costs.

The analysis is based on Milliman’s proprietary research tools and analyzes commercialclaims data. The family cost figure reflects nationwide average negotiated provider fees and average PPO benefit levels.

With a single ruling, the Federal Trade Commission removed the nation’s occupational handcuffs, freeing almost all U.S. workers from non-compete clauses. The medical profession will never be the same.

On April 23, the FTC issued a final rule, affecting not only new hires but also the 30 million Americans currently tethered to non-compete agreements. Scheduled to take effect in September—subject to the outcome of legal challenges by the U.S. Chamber of Commerce and other business groups—the ruling will dismantle longstanding barriers that have kept healthcare professionals from changing jobs.

The FTC projects that eliminating these clauses will boost medical wages, foster greater competition, stimulate job creation and reduce health expenditures by $74 billion to $194 billion over the next decade. This comes at a crucial moment for American healthcare, an industry in which 60% of physicians report burnout and 100 million people (41% of U.S. adults) are saddled with medical bills they cannot afford.

Like all major rulings, this one creates clear winners and losers—outcomes that will reshape careers and, potentially, alter the very structure of U.S. healthcare.

Winners: Newly Trained Clinicians

Undoubtedly, the FTC’s ruling is a win for younger doctors and nurses, many of whom join hospitals and health systems with the promise of future salary increases and more autonomy. However, by agreeing to stringent non-compete clauses, these newly trained clinicians have little choice but to place their trust in employers that, shielded by air-tight agreements, have no fear of breaking their promises.

Most newly trained clinicians enter the medical job market in their late 20s and early 30s, carrying significant student-loan debt—nearly $200,000 for the average doctor. Eager for stable, well-paying positions, these young professionals quickly settle into their careers and communities, forming strong relationships with friends and patients. Many start families.

But when these clinicians realize their jobs are falling short of the promises made early on, they face a tough decision: either endure subpar working conditions or uproot their lives. Taking a new job 25 or 50 miles away or moving to a different state are often are only options to avoid breaching a non-compete clause.

In a 570-page supplement to its ruling, the FTC published testimonials from dozens of healthcare professionals whose lives and careers were harmed by these clauses.

“Healthcare providers feel trapped in their current employment situation, leading to significant burnout that can shorten their career longevity,” said one physician working in rural Appalachia.

By banning non-competes, the FTC’s rule will boost career mobility for all clinicians within their own communities. This change will likely spur competition among employers—leading to improved pay and benefits to attract and, equally important, retain top talent. And with the reassurance that they can easily switch jobs if their current employer falls short of expectations, clinicians will enjoy greater professional satisfaction and less burnout.

Winners: Patients In Competitive Markets

Benefits that accrue to doctors and nurses from the FTC’s ban will translate directly to improved outcomes for patients. For example, we know that physicians who report symptoms of burnout are twice as likely to commit a serious medical error. Studies have shown the inverse is true, as well: healthcare providers who are satisfied with their jobs tend to have lower burnout rates, which is positively correlated with improved patient outcomes.

Once freed from restrictive non-compete clauses, many clinicians will practice elsewhere within the community. To attract patients, they will have to offer greater access, lower prices and more personalized service. Others with the freedom to choose will join outpatient centers that offer convenient and efficient alternatives for diagnostic tests, surgery and urgent medical care, often at a fraction of the cost of traditional hospital services. In both cases, increased competition will give patients improved medical care and added value.

Losers: Large Health Systems

Large health systems, which encompass several hospitals in a geographic area, have traditionally relied on non-compete agreements to maintain their market dominance. By barring high-demand medical professionals such as radiologists and anesthesiologists from joining competitors or starting independent practices, these systems have been able to suppress competition and force insurers to pay more for services.

Currently, these systems can demand high reimbursement rates from insurers while also maintaining relatively low wages for staff, creating a highly profitable model. Yale economist Zack Cooper’s research shows the consequence of the status quo: prices go up and quality declines in highly concentrated hospital markets.

The FTC’s ruling challenges those conditions, potentially dismantling monopolistic market controls. As a result, insurers will no longer be forced to contend with a single, dominant provider. And with health systems pushed to offer better wages and benefits to retain their top talent, bottom lines will shrink.

While nonprofit hospitals and health systems are not currently under the FTC’s jurisdiction, the agency has pointed out that these facilities might be at “a self-inflicted disadvantage in their ability to recruit workers.” Moreover, as Congress intensifies scrutiny on the nonprofit status of U.S. health systems, hospitals that do not voluntarily align with the FTC’s guidelines may find themselves compelled to do so through legislative actions.

Losers: Hospital Administrators

Individual hospitals have faced a unique challenge over the past decade. Across the country, inpatient numbers are falling, which makes it harder for hospital administrators to fill beds overnight. This trend has been driven by advancements in medical technology and new practices that enable more outpatient procedures, along with changes in insurance reimbursements favoring less costly outpatient care. As a result, hospital administrators have been compelled to adapt their financial strategies.

Nowadays, outpatient services account for about half of all hospital revenue. These range from physician consultations to specialized procedures like radiological and cardiac diagnostics, chemotherapy and surgeries.

Medicare and other insurers typically pay hospitals more for these outpatient services than they pay local doctors and other facilities. Knowing this, hospitals are hiring community doctors and acquiring diagnostic and procedural facilities, then boosting profitability by charging the higher hospital rates for the same services.

Hospital administrators know that this strategy only works if the newly hired clinicians are prohibited from quitting and returning to practice within the same community. If they do, their patients are likely to go with them. This is why the non-compete clauses are so essential to a hospital’s financial success.

As expected, the American Hospital Association opposes the FTC’s rule, arguing that non-compete clauses protect proprietary information. In practice, most of the doctors affected by the ban are providing standard medical care and have no proprietary knowledge that requires protection.

Looking Ahead

Today’s hospital systems are starkly divided between haves and have-nots. Facilities in affluent areas often enjoy high reimbursement rates from private insurers, boosting financial success and administrator salaries. In contrast, rural hospitals grapple with low patient volumes while facilities in economically disadvantaged, high-population areas face greater financial difficulties.

The current model is not working. The old ways of doing things—enforcing non-competes, charging higher fees for identical services and promoting market consolidation to hike prices—are not sustainable solutions.

The abolition of non-compete agreements will produce both winners and losers. In the healthcare sector, the ultimate measure of a policy’s impact should be its effect on patients—and the overwhelming evidence suggests that eliminating these clauses will benefit them greatly.

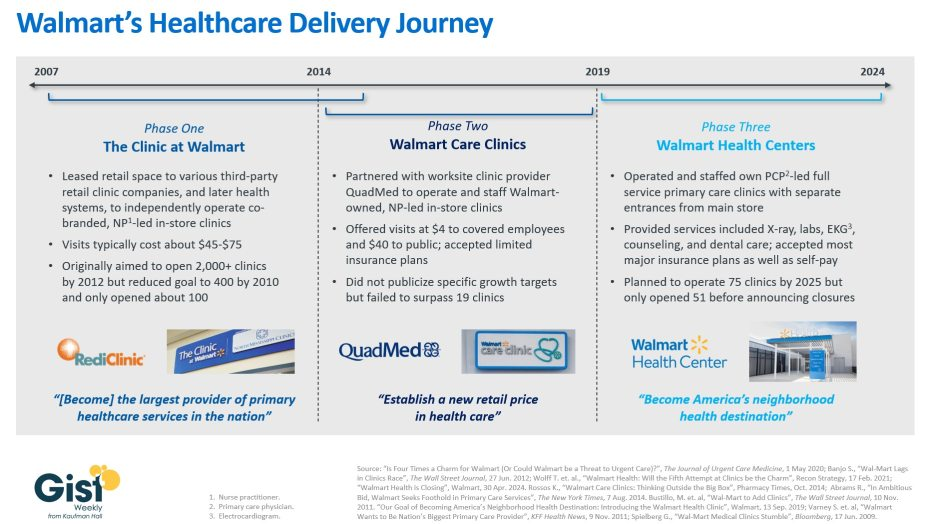

With Walmart’s announcement last week that it plans to shutter its Walmart Health business, this week’s graphic takes stock of the company’s healthcare delivery journey over nearly the past two decades.

In about 2007, Walmart launched “The Clinic at Walmart,” which leased retail space to various third-party retail clinic companies, and then later health systems, to provide basic primary care services inside Walmart stores, with the ambition of eventually becoming “the largest provider of primary healthcare services in the nation.”

However, low volumes and incompatible incentives between Walmart and its contractors led most of these clinics to close over time. In 2014 Walmart partnered with a single company, the worksite clinic provider QuadMed, to launch “Walmart Care Clinics.” These in-store clinics offered $4 visits for covered Walmart employees and $40 visits for the cash-paying public. Despite these low prices, this iteration of care clinic also suffered from low volumes, and Walmart scrapped the idea after opening only 19 of them.

The retail giant’s most recent effort at care delivery began in 2019 with its revamped “Walmart Health Centers,” which it announced alongside its goal to “become America’s neighborhood health destination.”

These health centers, which had separate entrances from the main store, featured physician-led, expanded primary care offerings including X-ray, labs, counseling, and dental services. As recently as April 2024, Walmart said it was planning to open almost two dozen more within the calendar year, until it announced it was shutting down its entire Walmart Health unit, which included virtual care offerings in addition to 51 health centers, citing an unfavorable operating environment.

Despite multiple rebranding efforts, consumers have thus far appeared unwilling to see affordability-focused Walmart as a healthcare provider.

Almost two decades of clinic experimentation have shown the company is willing to try things and admit failure, but it remains to be seen if this is just the end of Walmart’s latest phase or the end of the road for its healthcare delivery ambitions altogether.

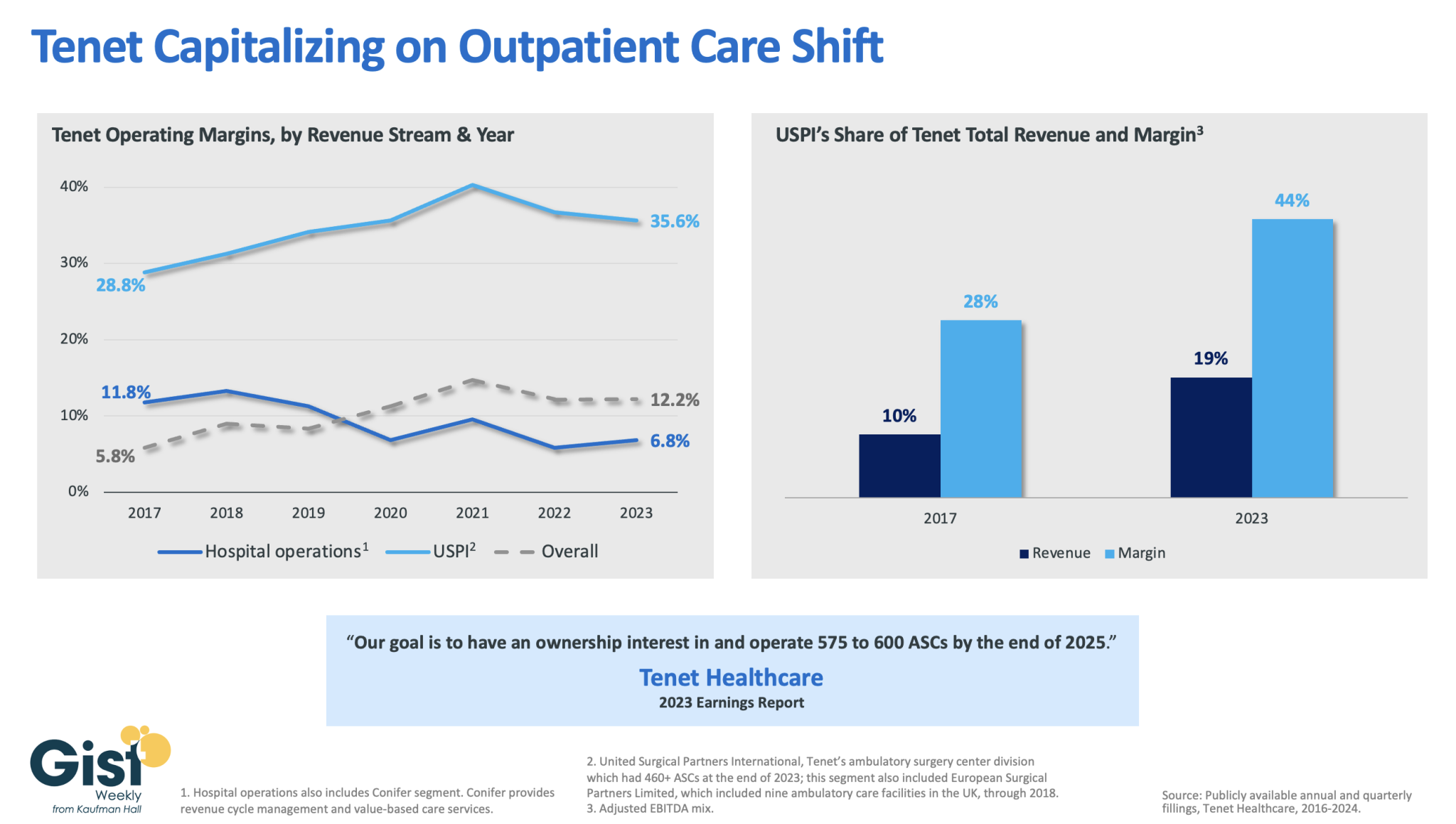

In this week’s graphic, we dive into recently released data on Tenet Healthcare’s 2023 financial performance. While the for-profit healthcare services company’s annual margin on hospital operations has declined since 2017, its overall profitability has more than doubled, thanks to strong performances from its ambulatory surgery center (ASC) chain,

United Surgical Partners International (USPI), which has consistently posted margins above 30 percent. Despite bringing in less than one fifth of Tenet’s total revenue, USPI is now responsible for almost half of Tenet’s overall margin.

Tenet has pursued this growth aggressively since buying USPI in 2015, swelling its ASC footprint from 249 locations in 2015 to more than 460 in 2023, with plans to increase that number to nearly 600 by the end of next year.

Tenet appears to be doubling down on its strategy of pursuing high-margin services over high-revenue services, especially as outpatient volumes are expected to far surpass growth in hospital-based care over the next decade.

U.S. Hospital YTD Operating Margin Index November 2021-December 2023

The observations and questions from this chart are both interesting and required reading for hospital executives:

Why were hospitals profitable at the 4% plus level through the worst of the 2021 Covid period?

What exactly happened between December of 2021 and January of 2022 that resulted in a profitability decrease from a positive 4.2% to a negative 3.4%?

Despite the best efforts of hospital executives, overall operating margins were negative throughout calendar year 2022 and did not return to positive territory until March of 2023.

Hospital margins remained positive throughout 2023 and into 2024. However, overall margins have remained below those experienced in both 2021 and in the pre-Covid year of 2019.

The above questions and observations have proven interesting, and the ongoing numbers have proven quite useful in many quarters of healthcare. But recently I was talking with Erik Swanson, who is the leader of the Kaufman Hall Flash Report and our executive behind the data, numbers, and statistics. Erik and I were speculating about all of the above observations, but our key speculation was whether the 2023 operating margin results actually reflected a hospital financial turnaround or, in fact, were there “numbers behind the numbers” that told a different and much more nuanced story. So Erik and I asked different questions and took a much deeper dive into the Flash Report numbers. The results of that dive were quite telling:

Too many hospitals are still losing money. Despite the fact that the Operating Margin Index median for 2023 and into 2024 was over 2%, when you look harder at the Flash Report data, you find that 40% of American hospitals continue to lose money from operations into 2024.

There is a group of hospitals that have substantially recovered financially. Interestingly, the data shows over time that the high-performing hospitals in the country are doing better and better. They are effectively pulling away from the pack.

This leads to the key question: Why are high-performing hospitals doing better? It turns out that several key strategic and managerial moves are responsible for high-performing hospitals’ better and growing operating profitability:

Outpatient revenue. Hospitals with higher and accelerating outpatient revenue were, in general, more profitable.

Contract labor. Hospitals that have lowered their percentage of contract labor most quickly are now showing better operating profitability.

An important managerial fact.The Flash Report found that hospitals with aggressive reductions in contract labor were also correlated to rising wage rates for full-time employees. In other words, rising wage rates have appeared to attract and retain full-time staff which, in turn, has allowed those hospitals to reduce contract labor more quickly, all of which has led to higher profitability.

Average length of stay.No surprise here. A lower average length of stay is correlated to improved profitability. Those hospitals that have hyper-focused on patient throughput, which has led to appropriate and prompt patient discharge, have also proven this to be a positive financial strategy.

Lower financial performers have financially stagnated throughout the pandemic. The data shows that throughout the pandemic, hospitals with good financial results improved those results, but of more consequence, hospitals with poor financial performance saw that performance worsen. The Flash Report documents that the poorest financially performing hospitals currently show negative operating margins ranging from negative 4% to negative 19%. Continuation of this level of financial performance is not only unstainable but also makes crucial re-investment in community healthcare impossible.

The urban hospital/rural hospital myth. A popular and often quoted hospital comparison is that there is an observable financial divide between urban and rural hospitals. Erik Swanson and I found that recent data does not support this common perception. When you compare “all rurals” to “all urbans” on the basis of average operating margin, no statistically significant difference emerges. However, what does emerge—and is a very important statistical observation—is that the lowest performing 20% of rural hospitals are, in fact, generating much lower margins then their urban counterparts this year. It is at this lowest level of rural hospital performance where the real damage is being done.

Rural hospitals and obstetrics. The data does confirm one very important American healthcare issue: Obstetrics and delivery services are one of the leading money losers of all hospital service offerings. And the data further confirms that rural hospitals are closing obstetric departments with more frequency in order to protect the financial viability of the overall rural hospital enterprise. This is a health policy issue of major and growing consequence.

The point here is that data, numbers, and statistics matter both to setting long-term social health policy agendas and to the strategic management of complex provider organizations. But the other point is that the quality and depth of the analysis is an equally important part of the process. A first glance at the numbers may suggest one set of outcomes. However, a deeper, more careful and penetrating analysis may reveal critical quantitative conclusions that are much more telling and sophisticated and can accurately guide first-class organizational decision-making. Hopefully the analytics here are a good example of this very point.

Health systems are recovering from the worst financial year in recent history. We surveyed strategic planners to find out their top priorities for 2024 and where they are focusing their energy to achieve growth and sustainability. Read on to explore the top six findings from this year’s survey.

Research questions

With this survey, we sought the answers to five key questions:

How do health system margins, volumes, capital spending, and FTEs compare to 2022 levels?

How will rebounding demand impact financial performance?

How will strategic priorities change in 2024?

How will capital spending priorities change next year?

Bigger is Better for Financial Recovery

What did we find?

Hospitals are beginning to recover from the lowest financial points of 2022, where they experienced persistently negative operating margins. In 2023, the majority of respondents to our survey expected positive changes in operating margins, total margins, and capital spending. However, less than half of the sample expected increases in full-time employee (FTE) count. Even as many organizations reported progress in 2023, challenges to workforce recovery persisted.

40%

Of respondents are experiencing margins below 2022 levels

Importantly, the sample was relatively split between those who are improving financial performance and those who aren’t. While 53% of respondents projected a positive change to operating margins in 2023, 40% expected negative changes to margin.

One exception to this split is large health systems. Large health systems projected above-average recovery of FTE counts, volume, and operating margins. This will give them a higher-than-average capital spending budget.

Why does this matter?

These findings echo an industry-wide consensus on improved financial performance in 2023. However, zooming in on the data revealed that the rising tide isn’t lifting all boats. Unequal financial recovery, especially between large and small health systems, can impact the balance of independent, community, and smaller providers in a market in a few ways. Big organizations can get bigger by leveraging their financial position to acquire less resourced health systems, hospitals, or provider groups. This can be a lifeline for some providers if the larger organization has the resources to keep services running. But it can be a critical threat to other providers that cannot keep up with the increasing scale of competitors.

Variation in financial performance can also exacerbate existing inequities by widening gaps in access. A key stakeholder here is rural providers. Rural providers are particularly vulnerable to financial pressures and have faced higher rates of closure than urban hospitals. Closures and consolidation among these providers will widen healthcare deserts. Closures also have the potential to alter payer and case mix (and pressure capacity) at nearby hospitals.

Volumes are decoupled from margins

What did we find?

Positive changes to FTE counts, reduced contract labor costs, and returning demand led the majority of respondents in our survey to project organizational-wide volume growth in 2023. However, a significant portion of the sample is not successfully translating volume growth to margin recovery.

44%

Of respondents who project volume increases also predict declining margins

On one hand, 84% of our sample expected to achieve volume growth in 2023. And 38% of respondents expected 2023 volume to exceed 2022 volume by over 5%. But only 53% of respondents expected their 2023 operating margins to grow — and most of those expected that the growth would be under 5%. Over 40% of respondents that reported increases in volume simultaneously projected declining margins.

Why does this matter?

Health systems struggled to generate sufficient revenue during the pandemic because of reduced demand for profitable elective procedures. It is troubling that despite significant projected returns to inpatient and outpatient volumes, these volumes are failing to pull their weight in margin contribution. This is happening in the backdrop of continued outpatient migration that is placing downward pressure on profitable inpatient volumes.

There are a variety of factors contributing to this phenomenon. Significant inflationary pressures on supplies and drugs have driven up the cost of providing care. Delays in patient discharge to post-acute settings further exacerbate this issue, despite shrinking contract labor costs. Reimbursements have not yet caught up to these costs, and several systems report facing increased denials and delays in reimbursement for care. However, there are also internal factors to consider. Strategists from our study believe there are outsized opportunities to make improvements in clinical operational efficiency — especially in care variation reduction, operating room scheduling, and inpatient management for complex patients.

Strategists look to technology to stretch capital budgets

What did we find?

Capital budgets will improve in 2024, albeit modestly. Sixty-three percent of respondents expect to increase expenditures, but only a quarter anticipate an increase of 6% or more. With smaller budget increases, only some priorities will get funded, and strategists will have to pick and choose.

Respondents were consistent on their top priority. Investments in IT and digital health remained the number one priority in both 2022 and 2023. Other priorities shifted. Spending on areas core to operations, like facility maintenance and medical equipment, increased in importance. Interest in funding for new ambulatory facilities saw the biggest change, falling down two places.

Why does this matter?

Capital budgets for health systems may be increasing, but not enough. With the high cost of borrowing and continued uncertainty, health systems still face a constrained environment. Strategists are looking to get the biggest bang for their buck. Technology investments are a way to do that. Digital solutions promise high impact without the expense or risk of other moves, like building new facilities, which is why strategists continue to prioritize spending on technology.

The value proposition of investing in technology has changed with recent advances in artificial intelligence (AI), and our respondents expressed a high level of interest in AI solutions. New applications of AI in healthcare offer greater efficiencies across workforce, clinical and administrative operations, and patient engagement — all areas of key concern for any health system today.

Building is reserved for those with the largest budgets

What did we find?

Another way to stretch capital budgets is investing in facility improvements rather than new buildings. This allows health systems to minimize investment size and risk. Our survey found that, in general, strategists are prioritizing capital spending on repairs and renovation while deprioritizing building new ambulatory facilities.

When the responses to our survey are broken out by organization type, a different story emerges. The largest health systems are spending in ways other systems are not. Systems with six or more hospitals are increasing their overall capital expenditures and are planning to invest in new facilities. In contrast, other systems are not increasing their overall budgets and decreasing investments in new facilities.

AMCs are the only exception. While they are decreasing their overall budget, they are increasing their spending on new inpatient facilities.

Why does this matter?

Health systems seek to attract patients with new facilities — but only the biggest systems can invest in building outpatient and inpatient facilities. The high ranking of repairs in overall capital expenditure priorities suggests that all systems are trying to compete by maintaining or improving their current facilities. Will renovations be enough in the face of expanded building from better financed systems? The urgency to respond to the pandemic-accelerated outpatient shift means that building decisions made today, especially in outpatient facilities, could affect competition for years to come. And our survey responses suggest that only the largest health system will get the important first-mover advantage in this space.

AMCs are taking a different tack in the face of tight budgets and increased competition. Instead of trying to compete across the board, AMCs are marshaling resources for redeployment toward inpatient facilities. This aligns with their core identity as a higher acuity and specialty care providers.

Partnerships and affiliations offer potential solutions for health systems that lack the resources for building new facilities. Health systems use partnerships to trade volumes based on complexity. Partnerships can help some health systems to protect local volumes while still offering appropriate acute care at their partner organization. In addition, partnerships help health systems capture more of the patient journey through shared referrals. In both of these cases, partnerships or affiliations mitigate the need to build new inpatient or outpatient facilities to keep patients.

Eighty percent of respondents to our survey continued to lose patient volumes in 2023. Despite this threat to traditional revenue, health systems are turning from revenue diversification practices. Respondents were less likely to operate an innovation center or invest in early-stage companies in 2023. Strategists also reported notably less participation in downside risk arrangements, with a 27% decline from 2022 to 2023.

Why does this matter?

The retreat from revenue diversification and risk arrangements suggests that health systems have little appetite for financial uncertainty. Health systems are focusing on financial stabilization in the short term and forgoing practices that could benefit them, and their patients, in the long term.

Strategists should be cautious of this approach. Retrenchment on innovation and value-based care will hold health systems back as they confront ongoing disruption. New models of care, patient engagement, and payment will be necessary to stabilize operations and finances. Turning from these programs to save money now risks costing health systems in the future.

Market intelligence and strategic planning are essential for health systems as they navigate these decisions. Holding back on initiatives or pursuing them in resource-constrained environments is easier when you have a clear course for the future and can limit reactionary cuts.

Advisory Board’s long-standing research on developing strategy suggests five principles for focused strategy development:

Strategic plans should confront complexity. Sift through potential future market disruptions and opportunities to establish a handful of governing market assumptions to guide strategy.

Ground strategy development in answers to a handful of questions regarding future competitive advantage. Ask yourself: What will it take to become the provider of choice?

Communicate overarching strategy with a clear, coherent statement that communicates your overall health system identity.

A strategic vision should be supported by a limited number of directly relevant priorities. Resist the temptation to fill out “pro forma” strategic plan.

Pair strategic priorities with detailed execution plans, including initiative roadmaps and clear lines of accountability.

Strategists align on a strategic vision to go back to basics

What did we find?

Despite uneven recovery, health systems widely agree on which strategic initiatives they will focus more on, and which they will focus less on. Health system leaders are focusing their attention on core operations — margins, quality, and workforce — the basics of system success. They aim to achieve this mandate in three ways. First, through improving efficiency in care delivery and supply chain. Second, by transforming key elements of the care delivery system. And lastly, through leveraging technology and the virtual environment to expand job flexibility and reduce administrative burden.

Health systems in our survey are least likely to take drastic steps like cutting pay or expensive steps like making acquisitions. But they’re also not looking to downsize; divesting and merging is off the table for most organizations going into 2024.

Why does this matter?

The strategic priorities healthcare leaders are working toward are necessary but certainly not easy. These priorities reflect the key challenges for a health system — margins, quality, and workforce. Luckily, most of strategists’ top priorities hold promise for addressing all three areas.

This triple mandate of improving margins, quality, and workforce seems simple in theory but is hard to get right in practice. Integrating all three core dimensions into the rollout of a strategic initiative will amplify that initiative’s success. But, neglecting one dimension can diminish returns. For example, focusing on operational efficiency to increase margins is important, but it’ll be even more effective if efforts also seek to improve quality. It may be less effective if you fail to consider clinicians’ workflow.

Health systems that can return to the basics, and master them, are setting a strong foundation for future growth. This growth will be much more difficult to attain without getting your house in order first.

Vendors and other health system partners should understand that systems are looking to ace the basics, not reinvent the wheel. Vendors should ensure their products have a clear and provable return on investment and can map to health systems’ strategic priorities. Some key solutions health systems will be looking for to meet these priorities are enhanced, easy-to-follow data tools for clinical operations, supply chain and logistics, and quality. Health systems will also be interested in tools that easily integrate into provider workflow, like SDOH screening and resources or ambient listening scribes.

Going back to basics

Craft your strategy

1. Rebuild your workforce.

One important link to recovery of volume is FTE count. Systems that expect positive changes in FTEs overwhelmingly project positive changes in volume. But, on average, less than half of systems expected FTE growth in 2023. Meanwhile, high turnover, churn, and early retirement has contributed to poor care team communication and a growing experience-complexity gap. Prioritize rebuilding your workforce with these steps:

Recover: Ensure staff recover from pandemic-era experiences by investing in workforce well-being. Audit existing wellness initiatives to maximize programs that work well, and rethink those that aren’t heavily utilized.

Recruit: Compete by addressing what the next generation of clinicians want from employment: autonomy, flexibility, benefits, and diversity, equity, and inclusion (DEI). Keep up to date with workforce trends for key roles such as advance practice providers, nurses, and physicians in your market to avoid blind spots.

Retain: Support young and entry-level staff early and often while ensuring tenured staff feel valued and are given priority access to new workforce arrangements like hybrid and gig work. Utilize virtual inpatient nurses and virtual hubs to maintain experienced staff who may otherwise retire. Prioritize technologies that reduce the burden on staff, rather than creating another box to check, like ambient listening or asynchronous questionnaires.

2. Become the provider of choice with patient-centric care.

Becoming the provider of choice is crucial not only for returning to financial stability, but also for sustained growth. To become the provider of choice in 2024, systems must address faltering consumer perspectives with a patient-centric approach. Keep in mind that our first set of recommendations around workforce recovery are precursors to improving patient-centered care. Here are two key areas to focus on:

Front door: Ensure a multimodal front door strategy. This could be accomplished through partnership or ownership but should include assets like urgent care/extended hour appointments, community education and engagement, and a good digital experience.

Social determinants of health: A key aspect of patient-centered care is addressing the social needs of patients. Our survey found that addressing SDOH was the second highest strategic priority in 2023. Set up a plan to integrate SDOH screenings early on in patient contact. Then, work with local organizations and/or build out key services within your system to address social needs that appear most frequently in your population. Finally, your workforce DEI strategy should focus on diversity in clinical and leadership staff, as well as teaching clinicians how to practice with cultural humility.

3. Recouple volume and margins.

The increasingly decoupled relationship between volume and margins should be a concern for all strategists. There are three parts to improving volume related margins: increasing volume for high-revenue procedures, managing costs, and improving clinical operational efficiency.

Revenue growth: Craft a response to out-of-market travel for surgery. In many markets, the pool of lucrative inpatient surgical volumes is shrinking. Health systems are looking to new markets to attract patients who are willing to travel for greater access and quality. Read our findings to learn more about what you need to attract and/or defend patient volumes from out-of-market travel.

Cost reduction: Although there are many paths health systems can take to manage costs, focusing on tactics which are the most likely to result in fast returns and higher, more sustainable savings, will be key. Some tactics health systems can deploy include preventing unnecessary surgical supply waste, making employees accountable for their health costs, and reinforcing nurse-led sepsis protocols.

Clinical operational efficiency: The number one strategic priority in 2023, according to our survey, was clinical operational efficiency, no doubt in response to faltering margins. Within this area, the top place for improvement was care variation reduction (CVR). Ensure you’re making the most out of CVR efforts by effectively prioritizing where to spend your time. Improve operational efficiency outside of CVR by improving OR efficiency and developing protocols for complex inpatient management.

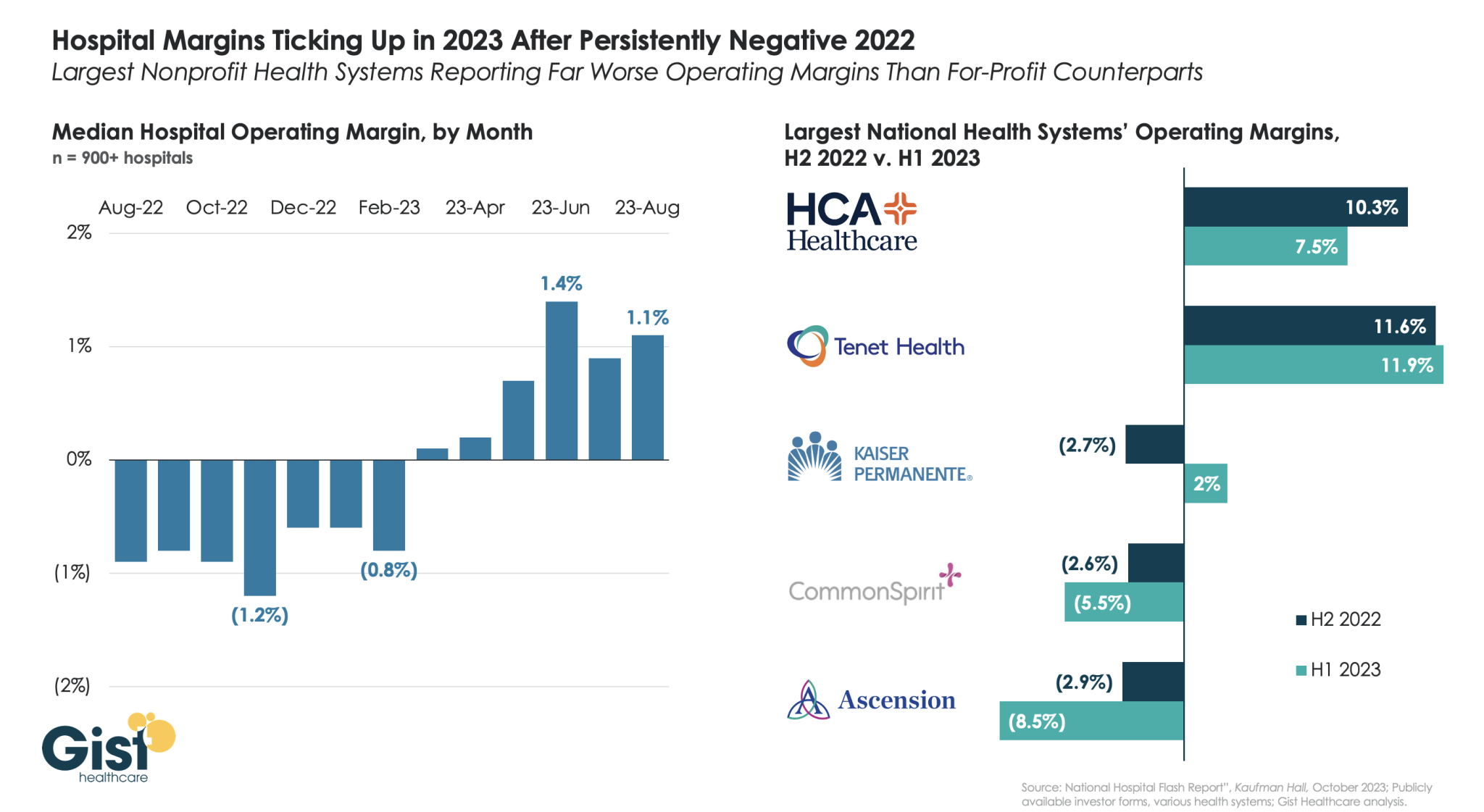

Using data from Kaufman Hall’s latest National Hospital Flash Report and publicly available investor reports for some of the nation’s largest health systems, the graphic below takes stock of the state of health system margins.

After the median hospital delivered negative operating margins for twelve-straight months, 2023 has made for a positive but slim year so far, with margins hovering around one percent. Amid this breakeven environment, fortunes have diverged between nonprofit and for-profit health systems.

The largest for-profit systems, HCA Healthcare and Tenet Healthcare, posted operating margins of around 10 percent between July 2022 and June 2023, while the three largest nonprofit systems, Kaiser Permanente, CommonSpirit Health, and Ascension, suffered net losses.

Although Kaiser Permanente’s margin bounced back in the first half of this year, CommonSpirit and Ascension’s margins continued to decline, more than doubling the operating losses of the prior six months.

One key to the recent success of the largest for-profit systems is their diversification away from inpatient care.

Case in point: almost half of Tenet’s profits in 2023 have come from its ambulatory division, driven by its United Surgical Partners International (USPI) ambulatory surgery center network, which has posted 40 percent margins over the past several quarters.

The pandemic accelerated the outpatient shift, which had been progressing steadily for decades, into a new gear, as safety-minded consumers avoided inpatient settings.

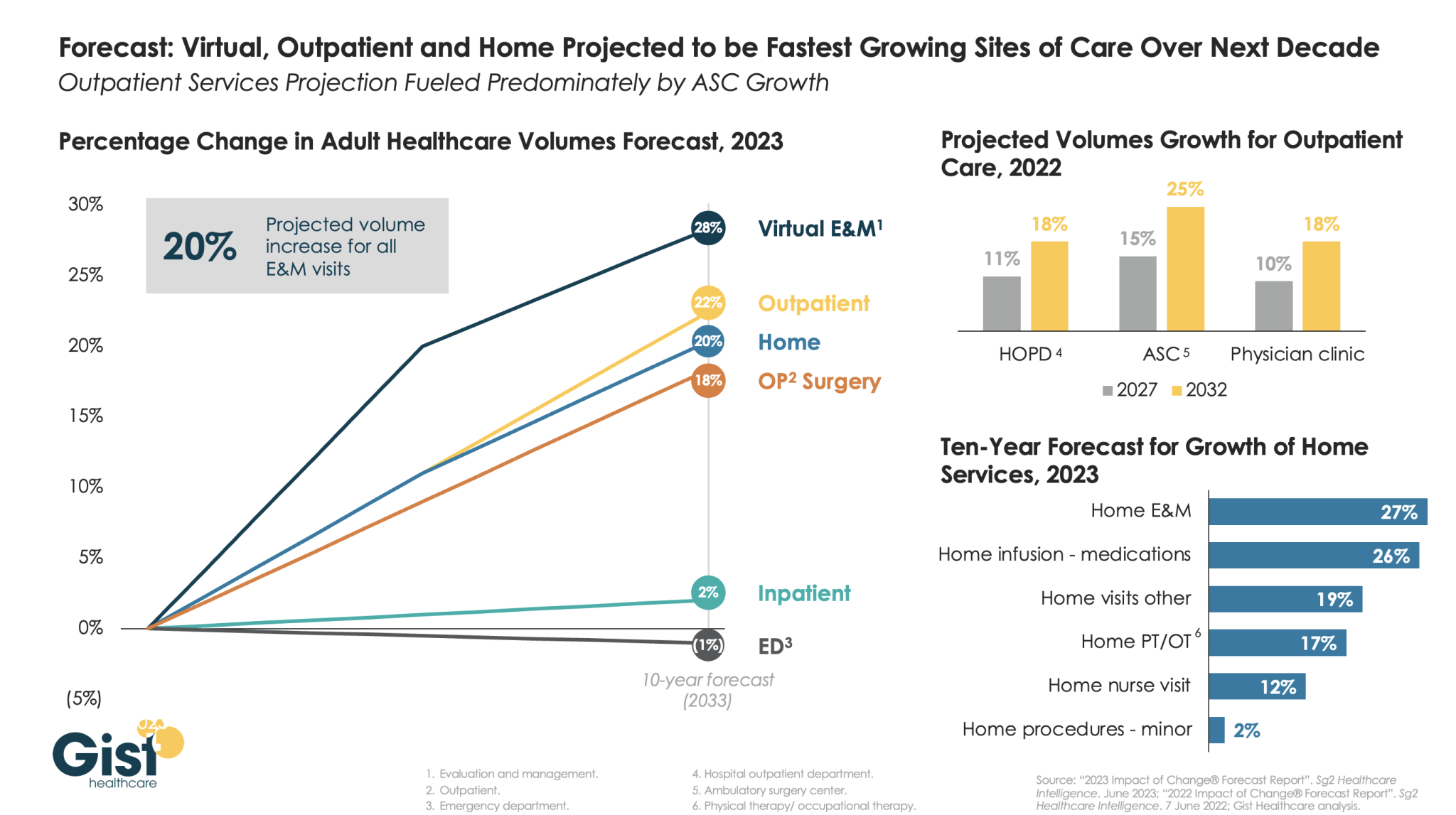

Using the latest forecasting data from strategic healthcare consulting firm Sg2, the graphic above illustrates how the outpatient shift will continue to accelerate in the coming years. With each projected to grow by 20 percent or more, outpatient, virtual, and home-based care services will continue far outpace growth in hospital-based care over the next decade.

Ambulatory surgery centers (ASCs) will be at the center of this care shift, reflected by a projected 25 percent rise in ASC volumes by 2032.

The breadth of care available at home will also expand as care delivery technology improves. With the population becoming older and sicker, higher incidence of chronic disease will be met by a rapid expansion of home evaluation and management services (E&M),reflecting a shift away from hospitals and doctors’ offices as hubs for complex care management.

Instead, the patients still coming to hospitals will present with increasingly acute conditions, driving up demand for resource-intensive critical care, as broader inpatient volume remains relatively flat.

This annual look at high-impact trends affecting healthcare in the coming year is based on evaluation of current industry research data. Healthcare Finance Trendsfor2023 (Trends) explores eight themes identified by CommerceHealthcare® ranging across four areas:

Financial. Providers enter the year contending with multiple financial stress points. They will also seek growth in technology-enabled remote care.

Patient financial experience. The need to drive not only improvement but also personalization of the financial experience is paramount. A central role will be played by patient financing programs which will see growing demand in 2023.

Trust. Building trust with all constituencies is explored as a linchpin for long-term provider success. The latest findings on cybersecurity show that this contributor to trust will continue to consume leadership attention.

Digital transformation. Pursuit of digital-first operations is accelerating, with the finance area an important focus. Emerging payment modes are finding a home in healthcare’s digital finance landscape.

This report’s consistent message is that these trends intersect in ways that compound both the challenges and the upside potential of strategies that address them.

1. Multiple Financial Stress Points Will Constrain Options

Healthcare’s financial predicament for the next 12–18 months is being described in strong terms. Citing $450 billion of EBITDA that could be in jeopardy, more than half of the industry’s project profit pool by 2027, one analyst suggests “a gathering storm.” Another perceives “broad and serious threats” as “elevated expenses” erode margins and exact “a profound financial toll.” Fitch Ratings issued a “deteriorating” outlook for nonprofit health systems.

These financial headwinds are upending healthcare’s traditional status as “recession-proof.” It is helpful to probe the multiple forces in play, the urgent workforce management challenge, and the varied solution set.

Multiple stress factors at work

Observing that margins will be down 37% in 2022 relative to pre-pandemic, a recent stark assessment concluded, “U.S. hospitals are likely to face billions of dollars in losses — which would result in the most difficult year for hospitals and health systems since the beginning of the pandemic.”

A confluence of factors is exacerbating the stress for 2023:

Rising acuity levels. Over two-thirds of surveyed C-suite executives said patient health has worsened from pandemic-induced delayed care. The upshot, stated by 27% of CFOs, is rising expenses due to higher acuity. Inpatient days are projected to increase at an 8% rate over the coming decade.

Reimbursement gaps and inflation. Commercial and government reimbursement rates are not keeping pace with rising costs. Surging inflation is widening this gap. Hospitals are also reporting substantial insurer payment delays and denials.

Investment declines. Stock and bond market declines have removed a cushion for operating weakness. Market uncertainty will complicate 2023 portfolio management.

Persistent workforce concerns remain center stage

Burnout and shortages have disrupted the clinical workforce. Nearly 60% of physician, advanced practice provider and nurse survey respondents said their teams are not adequately staffed, and 40% lack resources to operate at full potential. Many providers face extreme to moderate shortages of allied health professionals.

The problem extends beyond the clinical. A survey saw 48% of respondents experiencing severe labor deficiencies in revenue cycle management (RCM) and billing, and one in four finance leaders must fill over 20 positions to be fully staffed.

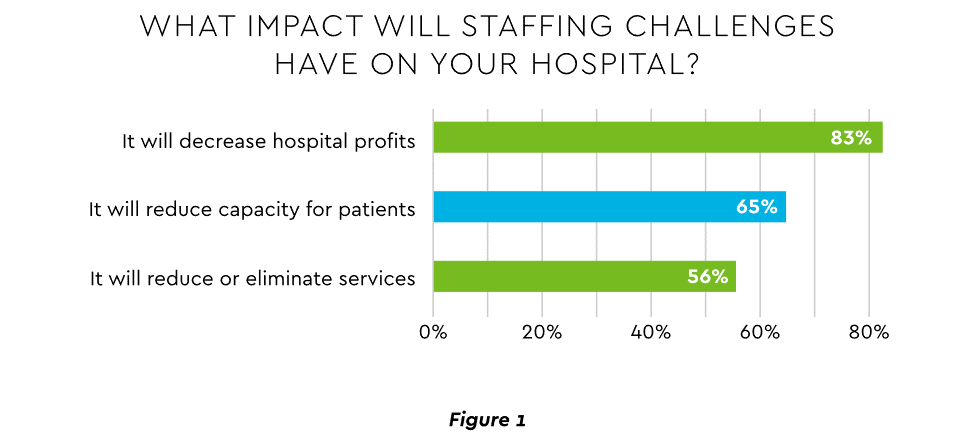

An executive outlook highlighted demonstrable impact on financial performance and growth from these workforce problems, citing reductions in profitability, capacity and service (Figure 1).1

Expenses. Hospital employee expense is expected to increase $57 billion from 2021 to 2022, with contract labor ballooning another $29 billion. Average weekly earnings are up 21.1% since early 2022. Half of medical practices budgeted higher staff cost-of-living increases in 2022. Shortages plague post-acute facilities as well. Their reduced capability to accept discharged patients is lengthening many hospitals’ patient stays.

Capacity constraint. Two-thirds of healthcare leaders identify “ability to meet demand” as their top workforce concern, suggesting a “looming capacity gap between future demand and labor supply.”

Range of measures being deployed

Health systems, hospitals and practices will vigorously pursue at least four direct actions to overcome the financial and staffing hurdles:

Cost cutting. Expense control will be paramount and “hospitals will be forced to take aggressive cost-cutting measures.” McKinsey estimates total industry administrative savings of $1 trillion through multiple aggressive changes.

Service line rationalization. Providers are rethinking how they deliver services to optimize efficiency. One path is utilizing “lower level” healthcare professionals in ways that free RNs and LPAs for more complex work suited to their top skills. Integrating remote care into the mix is another core element of the strategy.

Recruitment and retention programs. Attracting and retaining talent is crucial. Compensation is one avenue. Over two-thirds of organizations are offering signing bonuses for allied health professionals. Some are instituting value-based payments for physicians, offering salary floors to protect from drops in patient volume. CFOs and CNOs are joining forces to invest in nurse retention strategies.

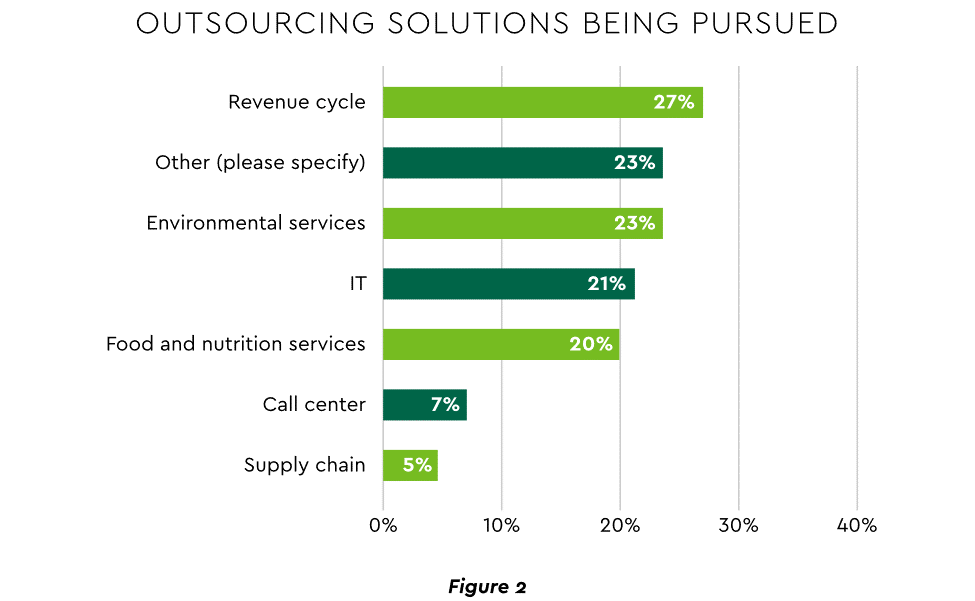

Staffing management. An increasingly popular tool to reduce labor cost and optimize staff resources is outsourcing. Figure 2 shows that RCM is leading the way among those using the solution.

2. Growth Strategies Favor Outpatient, Virtual, Acute Home Care

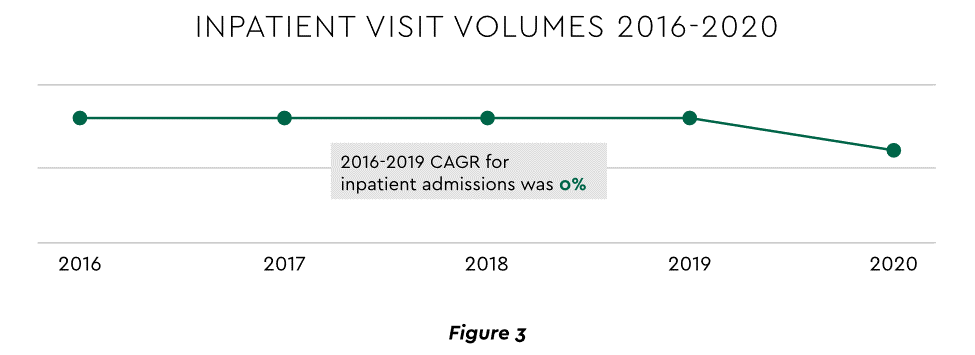

Pursuing top line growth in tandem with reining in expenses is essential. Inpatient volume growth has been tepid for several years ─ essentially flat in the 2016–20 period (Figure 3).

Leaders have been pivoting to outpatient and virtual care to diversify revenue streams. Two high-potential 2023 growth tracks in this sector merit deeper assessment.

Telehealth

Considerable evidence attests to strong commitment to telehealth and remote care. Sixty-three percent of physicians worldwide expect most consultations to be performed remotely within 10 years. Approximately 40% of health centers are using remote patient monitoring today. Consumers are also positive: 94% definitely or probably will use telehealth again, 57% prefer it for regular mental health visits and 61% use it for convenient care.

Telehealth is still in early stages of maturity. Only 4% of surveyed top executives consider their organization proficient at implementing remote care. Healthcare is also recognizing that a full telehealth ecosystem must be constructed. A physician leader explained that the industry’s early telehealth incarnations failed to build “virtual-only environments or really drive e-consults as a way of doing things.” A vital ecosystem demands alterations to current contracts, coding, collections, patient financing, staff training and other business practices.

Hospital-at-Home (HaH)

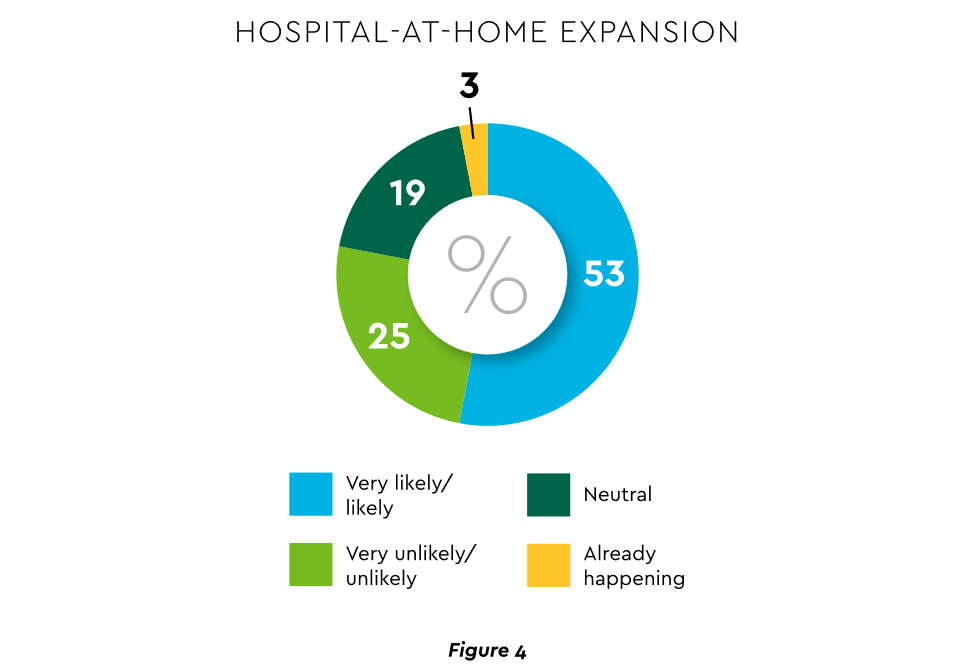

Health systems see particularly promising growth in the provision of acute care in patients’ home settings, including post-surgical and cancer treatment. The federal government has already allowed waivers to 114 systems and 256 hospitals to obtain inpatient-level reimbursement for acute care at home. However, these waivers were prompted by the pandemic and are slated to end in early 2023. The renewal uncertainty has stymied some activity and represents an overhang on the opportunity. However, enthusiasm appears strong, and 33% of hospitals in a recent poll said they would be prone to continue HaH even without renewal.

The forecasts are encouraging. Over half of hospitals believe it likely they will utilize HaH for at least half of their chronically ill patients over the next several years (Figure 4).

Harvesting the HaH potential will require implementation of current and emerging enabling technologies in remote monitoring, high-speed networks and artificial intelligence that generates algorithmic guidance for caregivers and patients alike.

3. Strong Drive to Improve and Personalize the Patient Financial Experience

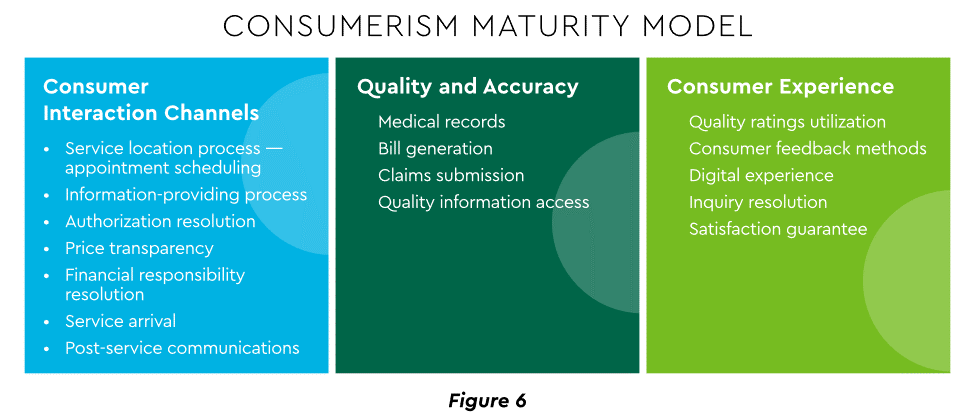

Today’s healthcare market dynamics place a premium on positive patient experiences. The goal is to deliver “an empathetic relationship between customers and brands built on what the customer wants and how they want to be treated.” It is a complex undertaking, with numerous touchpoints as captured in HFMA’s Consumerism Maturity Model (Figure 6).

An array of studies underscores the value proposition for intense provider focus on patient financial experience:

Sixty-one percent of consumers said that ease of making payments is very or somewhat important in decisions to continue seeing a doctor. Over half of patients also said text message reminders make them very or somewhat more likely to pay a bill faster than usual.

Thirty-five percent of respondents “have changed or would change healthcare providers to get a better digital patient administrative experience.”

A quality financial experience encompasses “simplified explanations, consolidated bills that match one’s health plan benefits, clear language displaying patient liability and payment options.”35

Significantly improving the financial experience requires a unified strategy, not just a collection of individual initiatives. Three threads to such a strategy will be prominent in 2023.

Using a Digital Front Door

Organizations have been moving swiftly to channel many patient financial transactions through an integrated Digital Front Door (DFD). This approach offers patients a singular online point of access and intelligent navigation to needed services. Growth is accelerating. A DFD is their patients’ first contact point for 55% of responding organizations, according to one technology survey. A leading forecaster sees 65% of patients engaging services via digital front doors by 2023.

Expanding price transparency

Mandates for full price transparency and “no surprises” billing are in effect, but estimates of compliance are mixed. An analysis of 2,000 hospitals determined that only 16% met the requirement to post an online “machine readable” file displaying clear charges for 300 “shoppable services.” Another assessment showed a more substantial 76% of hospitals had posted files, and 55% were deemed “complete.” One provision of interest to practices is the “good faith estimate” of expected charges required to be given to uninsured and self-pay individuals when they schedule visits. CommerceHealthcare® has worked with clients to enhance the patient financial experience by complementing their website pricing data with clear information on patient financing options and enrollment access. Bill pay information can also be added for one-stop guidance.

Personalizing the experience

Beyond choice and convenience, the deeper objective is truly personalized experiences throughout the care journey. The words of leading analysts best define the drive to personalize:

“Tomorrow’s healthcare experience will be built by patients tailoring their own experience.”

“By 2024, 30% of chronic care patients will truly own and openly leverage their personal health information to advocate for, secure, and realize better personalized care.”

Opportunities abound to personalize the patient financial experience. Automating manual processes establishes a foundation. Patient financing with no- or low-interest credit lines and flexible terms can produce monthly payment schedules tailored to each patient’s needs. Refunds can be made through multiple payment modes to meet varying patient preferences.

4. Evidence Underscores Growing Demand for Patient Financing

Emphasizing patient financing as part of the overall experience is powerful. Patients continue to struggle paying for care. Recent granular data details three related forces at work.

Meeting care costs difficult for many patients

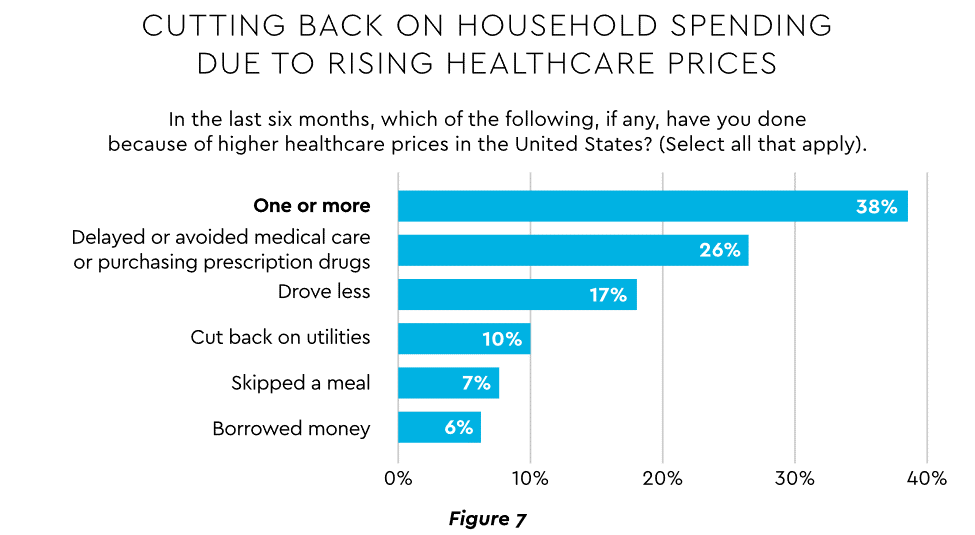

Commonwealth Fund found that 42% of individuals had problems paying medical bills or were paying off medical debt during the past year, while 49% were unable to pay an unexpected $1,000 medical bill.42 Health costs trigger reduction in a range of personal expenditures, led by deferring or avoiding care and drugs (Figure 7).

Twenty-eight percent of Americans now describe themselves as less prepared than last year to pay for routine or unanticipated care.

Patient obligation for care costs still rising

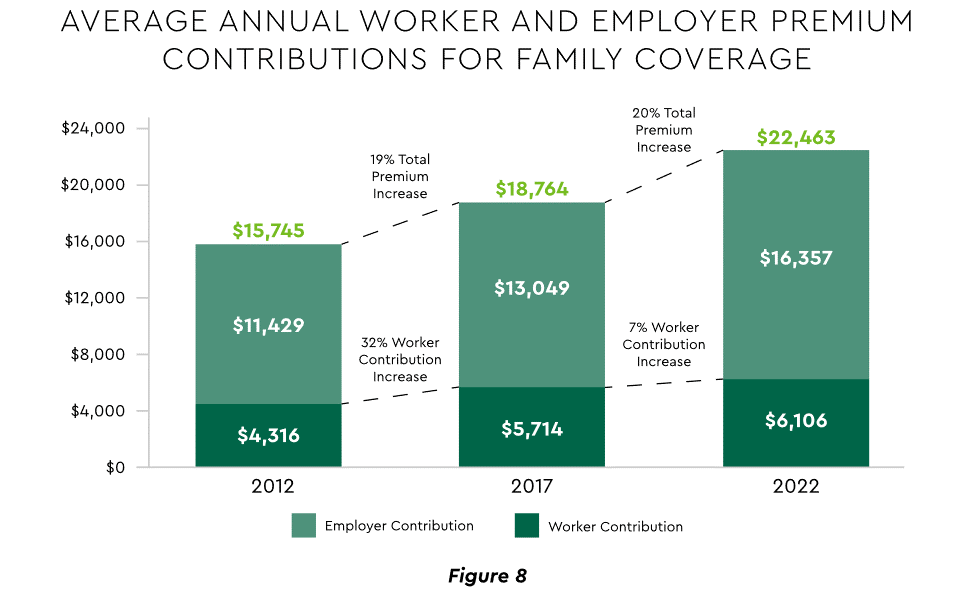

Patient obligation continues its upward march. Insurance premiums have climbed steadily for both the insured and their employers, and employees now pay over $6,000 annually on average for family coverage (Figure 8).45

High deductible health plans (HDHP) also place substantial burden on the patient. Through 2021, 28% of workers were enrolled in an HDHP with an average family deductible of $4,705. Employer satisfaction with these plans is high, auguring further expansion.

Providers feeling the financial effects

Patient payment difficulties are clearly impacting provider financials. A recent in-depth analysis uncovered substantial self-pay issues:

Self-pay accounts represented 60% of 2021 patient bad debt, up from 11% in 2018.

Nearly 18% of patient balances were over $7,500 and 17% over $14,000. Collections were noticeably lower at these balances.

Multiple chronic conditions add to the problem. A recent extensive analysis concluded: “Among individuals with medical debt in collections, the estimated amount increased with the number of chronic conditions ($784 for individuals with no conditions to $1,252 for individuals with 7–13).”

For their part, providers will be encouraged to broaden patient financing programs. Patients are certainly interested. When asked, 62% of consumers indicated they would use financing options or creative payment plans if available for large bill amounts. Many health systems, hospitals and practices will turn to outside help to satisfy the demand. A recent analysis recommended that health systems “consider keeping shorter-term payment plans in-house and extended term plans through external partnerships.”

Organizations will also need to step up their communications. A survey revealed that 64% of patients were unaware that their doctors and hospitals offered payment plans or financial help.

5. Building Trust Becoming a Critical Success Factor

Trust has emerged as a paramount issue today for most organizations as they encounter an “imperative to build trust and transparency among different stakeholder groups — employees, customers, suppliers, regulators and the communities in which they operate.” Healthcare is no exception, and the trust issue is growing in both complexity and urgency.

Healthcare’s trust gap

Trust in healthcare took a hit from the COVID-19 experience. A spring 2022 HFMA survey recorded 44% of finance leaders saying they perceived decreased patient trust. Between April 2020 and December 2021, the percentage of Americans who trusted information from doctors “a great deal” declined by 23%, from hospitals 21%, and from nurses 16%. The patient financial experience also faces “drivers of mistrust,” according to surveyed leaders who cited general payment confusion (58%), surprise billing (39%), high prices of commodity items (28%) and lack of price transparency (26%). Building trust reaps dividends. People who trust their providers are five times more likely to stay with them than those who are neutral or distrustful.

Strategies for building trust

Industry experts promote several approaches to galvanize trust among all constituencies:

Commitment. Embedding trust deeply in the organization requires full support from senior leadership.

Data transparency and governance. IDC predicts that “by end of 2023, 20% of expenses on care integration solutions will be centered around ‘trust’ to protect data, workflows and transactions.”

Reliance on fewer business partners. Many health systems, hospitals and practices are reducing their number of vendors in order to focus on a set of trusted long-term partners. For example, almost two-thirds of surveyed providers said they were seeking to streamline the number of software solutions over the next year.

The bank partner advantage

A provider’s banking relationship can yield valuable collaboration in the trust-building endeavor. Banks enjoy solid trust among consumers. As an example, 53.4% of consumers rated banks as most trusted to provide payment “super apps” and financial digital front doors ─ exceeding the next closest source by 10 points.

6. Cybersecurity in 2023: No Rest for the Weary

Cybersecurity is part of the trust calculus and has become an evergreen topic in healthcare. Compromised data and ransomware attacks are ongoing and leaders must continually refine their understanding in at least three areas: the overall security landscape, particular financially related considerations and contemporary security defenses.

The current landscape

The latest statistics quantify the cyber assault on healthcare:

Incidence. 89% of organizations suffered at least one attack in the past 12 months with the average number at 43.

Cost. A provider’s most serious attack costs an average of $4.4 million. IBM calculated healthcare’s average total cost of a breach at $10.1 million, up 42% since 2020.

Attack Characteristics. Healthcare data types most commonly compromised are personal (58%), medical (46%), and credentials (29%). Organizations have an exposure to an average of over 26,000 network-connected devices. A disturbing finding is that those healthcare institutions that paid ransom got back only 65% of their data in 2021.

Specific financial considerations

Finance leaders will also need awareness of the following:

Cyberattacks could affect credit ratings and are often a component of Environmental, Social and Governance assessments.

Financial outsourcing requires monitoring. A recent news story chronicled an accounts receivable firm’s breach that exposed individual information, account balances and payments.

Cyber insurance premiums are likely to increase substantially.

Responses/tools

Beyond a host of management and monitoring tools being deployed, a strategic philosophy is rapidly gaining ground. The “zero trust” model sounds counter to the trust-building mindset described earlier, but it has become essential. It “denies access to applications and data by default,” and 58% of hospitals and health systems have a zero trust initiative in place. Another 37% intend to implement one within 12–18 months.

Cybersecurity investment will challenge CFOs in 2023, especially in areas such as talent. Cybersecurity worker availability is estimated to satisfy only 68% of open positions. Banking partners will also be expected to play an important role. Over the years, major banks have become “leaders in enhancing cyber strategy and investing in cyber defenses, processes and talent.”

7. Digital Transformation of Finance In Focus

Digital transformation is fundamental to healthcare’s business and care delivery model changes. IBM’s website succinctly captures the goal, “Digital transformation means adopting digital-first customer, business partner, and employee experiences.” A leading forecaster believes 70% of healthcare organizations will rely on digital-first strategies by 2027.

Transformation efforts need to accelerate. One study showed that “digital, technology and analytics strategies exist for nearly all organizations, yet only 30% have begun to execute on those plans.”

One functional segment ramping up digital transformation is finance. According to a recent survey, 94% of CFOs and senior leaders stated that such efforts will be at the forefront of financial operations and strategy for 2023–2024, and 79% described it as an “absolute need” for “commercial stabilization and long-term survival of their healthcare organization.”

Advanced technology is gaining traction. Many see optimization in combining robotic process automation (RPA), artificial intelligence and machine learning to create “intelligent automation.” Together, these technologies create algorithms to automate decisions that guide “robotic” software to perform financial actions and thereby reduce manual labor.

Getting to digital-first in finance and across the enterprise has several critical success factors. These include sustained commitment, a platform-centric mindset and effective governance.

Commitment

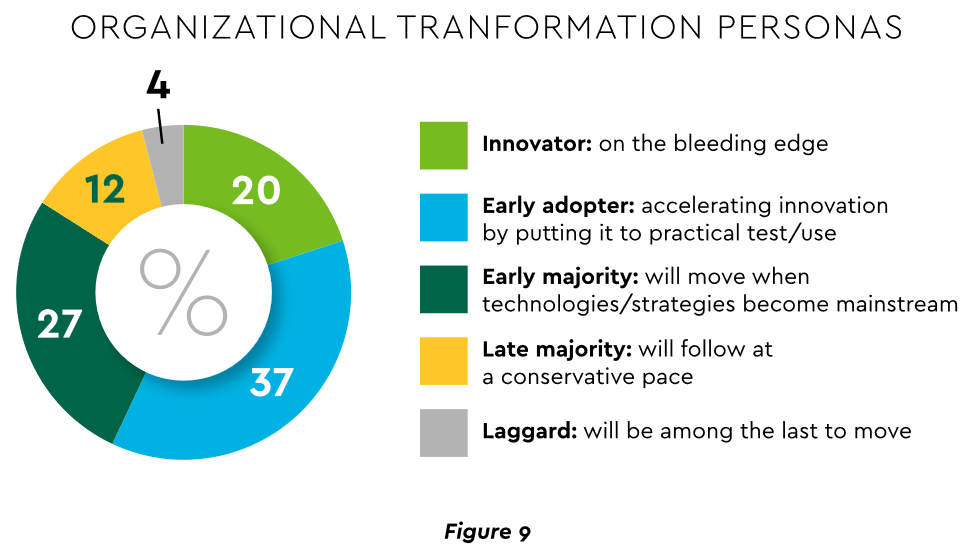

Some assert that few healthcare executives have “created digital strategies that look far enough into the future.” Speed of change is also important. Health systems, hospitals and practices exhibit varying risk appetites and change rates. When asked to self-identify “transformation personas,” a little over half regarded themselves as being on the innovative “early mover” end of the spectrum, while the remainder will adapt as technologies prove themselves (Figure 9). Slower organizations will likely need to increase the pace.

Implementing enterprise platforms rather than proliferating “point solutions” is obligatory. Organizations must be “prepared to compete in the platform economy as platform-based business models have changed the way we live, work and receive care.”

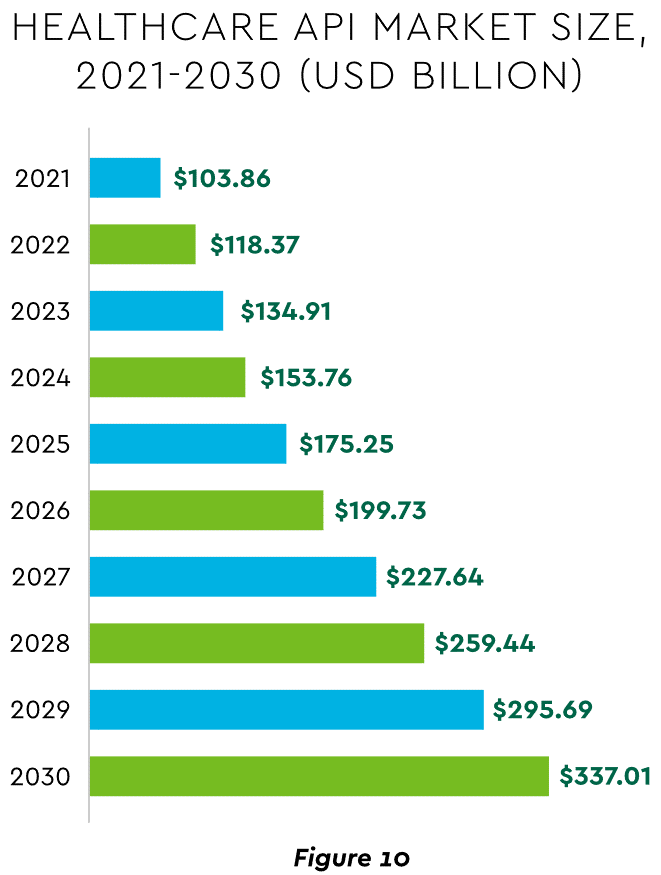

There are still too many tools and applications. A survey of top decision-makers at health systems found that 60% use over 50 software solutions just in operations (24% have over 150). System integration is one answer. Use of application programming interfaces (API) helps this effort substantially. API-first is fast becoming the norm among solution providers, with global API investment expected to nearly triple by 2030 (Figure 10)

Effective governance is vital to constructing a platform-based transformative model and to ensuring wide user adoption. Healthcare has seen the rise of new senior roles such as Chief Digital Officer and Chief Transformation Officer, positions focusing on initiatives like ownership of technology success at the department level and devising user incentives.

8. Digital Payments on the Horizon for Healthcare

A variety of emerging digital payment modes will further the transformation of finance. These payments are expected to grow almost 23% annually in healthcare. ACH payments have been on a strong upward trajectory in healthcare for several years, especially for business transactions. In 2021, ACH tallied a yearly increase of 18% in volume and 5% in dollars.

Notable technologies and payment rails to watch for expected crossover from consumer markets to healthcare include:

Mobile payments. The market for mobile payment technologies has been growing at a 16% compound annual clip and should reach $90 billion in 2023, powered by wide smartphone use, 5G networks and convenience. This category encompasses technologies such as e-wallets, forecasted to grow 23% annually worldwide through 2030.

Real-time payments (RTP). These digital transactions are settled nearly instantaneously through platforms such as The Clearing House. One forecast sees 30.4% compound RTP growth in the U.S. from 2022 to 2030.

Buy Now Pay Later (BNPL). This growing mode offers consumers short-term financing to stretch payments over several installments. A recent survey established that 23% of American adult respondents have used a BNPL service. BNPL is just entering healthcare and is currently regarded as an option for certain elective or cosmetic procedures or for specific individual credit scenarios.

Earned Wage Access (EWA). Using an RTP approach, employers are beginning to offer on-demand pay which enables “instant access to earned wages right after the work is performed, at the end of the shift, or upon completion of a project.” It is not a loan or advance pay. A 2021 poll conducted by Harris found that 83% of U.S. workers feel they should be able to access earned wages at the end of each day. Millennials were particularly interested: 80% would like daily automatic pay streaming to their bank accounts, and 78% said free EWA would boost loyalty to their employer. Given its pressing workforce concerns, healthcare is likely to find EWA a tool to promote retention.

Seeking the right use cases for these payment technologies offers many potential provider benefits.

Conclusion

The connected forces discussed and quantified here create major challenges to address in 2023. The strategic agenda calls for balancing tight cost control with investment in growth opportunities, significantly enhancing patient financial experience by meeting growing patient financial need, shoring up trusted relationships and cybersecurity, and accelerating the digital transformation of finance.

Health systems are ramping up investments in ambulatory surgery centers and forming joint ventures with outpatient partners to accelerate the development of new centers. The trend is picking up steam as complex procedures increasingly move to ASCs, which are steadily growing as the preferred site of service for physicians, patients and payers.

Tenet Healthcare, one of the largest for-profit health systems in the country, has been paying close attention to outpatient migration for years and has cemented itself as the leader in the ASC space. It now operates more than 445 ASCs — the most of any health system — and 24 surgical hospitals, according to its first-quarter earnings report.

United Surgical Partners International, Tenet’s ASC company, strengthened its footing in the ASC market after its $1.2 billion acquisition of Towson, Md.-based SurgCenter Development and its more than 90 ASCs in December 2021. Over the next several years, USPI will inject more than $250 million into ASC mergers and acquisitions and work with SurgCenter to develop at least 50 more ASCs, according to terms of the transaction.

The SurgCenter acquisition was completed shortly after Tenet sold five Florida hospitals to Dallas-based Steward Health Care for $1.1 billion. In 2022, Tenet also acquired Dallas-based Baylor Scott & White Health’s 5 percent equity position in USPI to own 100 percent of the company’s voting shares and paid $78 million to acquire ownership of eight Compass Surgical Partners ASCs.

These ASC investments and hospital sales make it clear that CEO Saum Sutaria, MD, sees surgery centers to become Tenet’s main growth driver in the coming years. Dr. Sutaria has described USPI as the company’s “gem for the future,” and aims to have 575 to 600 ASCs by the end of 2025.

While Tenet continues to increase its ASC market share, its closest competitor is Deerfield, Ill.-based SCA Health, which UnitedHealth Group’s Optum acquired for $2.3 billion several years ago.

SCA has more than 320 ASCs, but has expanded its focus on value-based care under Optum and is doubling down on supporting physicians across the specialty care continuum rather than operating as an ASC company “singularly focused on partnering with surgeons in their ASCs,” SCA CEO Caitlin Zulla told Becker’s.

While Tenet may operate the most ASCs among health systems, it lags behind Optum in terms of the number of physicians it employs. Optum is now affiliated with more than 70,000 physicians, making it the largest employer of physicians in the country, and is continuing to add to that through mergers and acquisitions.

Nashville, Tenn.-based HCA Healthcare, another for-profit system, employs or is affiliated with more than 47,000 physicians, but is also ramping up its surgery center portfolio. HCA comprises 2,300 ambulatory care facilities, including more than 150 ASCs, freestanding emergency rooms, urgent care centers and physician clinics, according to its first-quarter earnings report.

Like Tenet and Optum, HCA is heavily focused on expanding its outpatient portfolio. The company ended 2021 with 125 ASCs, four more than it had at the end of 2020, and added more than 25 ASCs last year. It is focused on both developing and acquiring surgery centers in the coming years.

The other big ASC operators include Nashville, Tenn.-based AmSurg, with more than 250 surgery centers, and Brentwood, Tenn.-based Surgery Partners, with more than 120 centers. Surgery Partners spent about $250 million on ASCs acquisitions last year and recently signed collaboration agreements with two large health systems —- Salt Lake City-based Intermountain Health and Columbus-based OhioHealth.

Oakland, Calif.-based Kaiser Permanente has 62 freestanding ASCs and outpatient surgery departments on its hospital campuses, a spokesperson for the health system told Becker’s.