Walmart is closing Walmart Health and Walmart Health Virtual Care, saying the business model was not profitable nor sustainable.

The Walmart Health centers opened in 2019.

“Through our experience managing Walmart Health centers and Walmart Health Virtual Care, we determined there is not a sustainable business model for us to continue,” the company said by statement. “The decision to close all 51 health centers across five states and shut down the virtual care offering was not easy.”

WHY THIS MATTERS

Walmart said the challenging reimbursement environment and escalating operating costs created a lack of profitability.

It does not yet have a specific date for when each center will close, but would share that information “as soon as decisions are made.”

Its priority, Walmart said, was “ensuring the people and communities who are impacted are treated with the utmost respect, compassion and support throughout the transition. Today and in the coming days, we are focused on continuity of care for patients and providing impacted associates with respect and assistance as we begin the closing process of the healthcare centers.”

The clinics will continue to serve patients while they are open.

“Through their respective employers, these providers will be paid for 90 days, after which eligible providers will receive transition payments,” Walmart said.

All associates are eligible to transfer to any other Walmart or Sam’s Club location. They will be paid for 90 days, unless they transfer to another location during that time or leave the company, Walmart said. After 90 days, if they do not transfer or leave, eligible associates will receive severance benefits.

“We understand this change affects lives – the patients who receive care, the associates and providers who deliver care and the communities who supported us along the way,” Walmart said.

THE LARGER TREND

Moving forward, Walmart said it would take what it has learned to provide health and wellness services across the country through its nearly 4,600 pharmacies and more than 3,000 vision centers. Both have been in operation for 40 years.

“Over the past few years, the importance of pharmacies has continued to grow, and we have expanded the clinical capabilities of the services we provide,” Walmart said. “We continue to offer immunizations and have grown to provide testing and treatment services, access to specialty pharmacy medication and care, as well as other essential services such as medication therapy management and a variety of health screenings. With more than 4,000 of our stores in medical provider shortage areas, our pharmacies are often the front door of healthcare.”

Walmart said it plans to launch more services such as the Walmart Healthcare Research Institute and health programs to join its fresh food and over-the-counter offerings.

Among the country’s largest grocers, Walmart plans this year to introduce a line of premium food called Bettergoods to compete against Trader Joe’s and Whole Foods, according to The Wall Street Journal.

However, share prices last week fell for Walmart and Kroger after Amazon unveiled a low-cost grocery delivery program, according to Seeking Alpha. Amazon is expanding its fresh-food business through a delivery subscription benefit in the United States for its Prime members and customers using an EBT (electronic benefits transfer) card. It outlined the $9.99 monthly plan last Tuesday, according to the report. Share prices for Walmart were down 1.55% as of this morning.

On Wednesday, e-commerce giant Amazon announced that its 167M US-based Prime members can now access One Medical primary care services for $9 per month, or $99 per year, which amounts to a 50 percent annual discount on One Medical membership. (Additional Prime family members can join for $6/month or $66/year.)

One Medical, which Amazon purchased for $3.9B last year, provides its 800K members with 24/7 virtual care as well as app-based provider communication and access to expedited in-person care, though clinic visits are either billed through insurance or incur additional charges. Amazon also recently started offering virtual care services through its Amazon Clinic platform, at cash prices ranging from $30 to $95 per visit.

The Gist:After teasing this type of bundle with a Prime Day sale earlier this year, Amazon has made the long-expected move to integrate One Medical into its suite of Prime add-ons, using a similar pricing model as its $5-per-month RxPass for generic prescription medications.

At such a low price, Amazon risks flooding One Medical’s patient population with demand it may struggle to meet. But if Amazon can scale One Medical, while maintaining its quality and convenience, it may be able to make the provider organization profitable.

Known for its willingness to take risks and absorb financial losses, Amazon is continuing to build a healthcare ecosystem focused on hybrid primary care and pharmacy services that delivers a strong consumer value proposition based on convenience and low cost.

Costco is now offering members online health checkups for as low as $29.

The retailer is offering the new service in partnership with Sesame, a direct-to-consumer health care marketplace that connects medical providers nationwide with consumers.

Sesame, in a release, said Costco members beginning Monday can book health care visits directly through their memberships in all 50 states.

The New York-based company said its platform doesn’t accept health insurance because it primarily caters to uninsured Americans and those with high-deductible plans who prefer to pay cash for their health care. It said its model helps keep prices of services low for its users.

The services listed on Costco Pharmacy’s homepage, include virtual primary care visits for $29, health checkups (a standard lab panel and a virtual follow-up consultation with a provider) for just $72 and online mental health visits for $79.

“Quality, great value, and low price are what the Costco brand is known for,” David Goldhill, Sesame’s co-founder and CEO, said in a statement. “When it comes to health care, Sesame also delivers high quality and great value – and a low price that will be appreciated by Costco Members when it comes to their own care.”

Amazon, in August, announced that its virtual clinic was now also available nationwide. Amazon Clinic launched last November offering 24/7 access to third-party health-care providers directly on Amazon’s website and mobile app.

Amazon customers, through the clinic, can access telehealth treatment for dozens of common conditions, such as pink eye, urinary tract infections and hair loss, the retailer said.

Other retailers, including CVS to Walgreens to Walmart, have made similar moves.

Amazon announced that it has expanded its direct-to-consumer virtual care platform to all 50 states and the District of Columbia. Amazon Clinic, which the e-commerce giant launched in 32 states last November, connects consumers to third-party clinicians via Amazon’s website or mobile app. Through video call or message-based visits (the latter of which are only available in some states), it offers diagnosis and treatment for a range of low-acuity, common health conditions like pink eye and sinus infections. The clinic features flat, upfront cash pricing, and doesn’t currently accept insurance. On the provider side, Amazon is partnering with telehealth companies Wheel, SteadyMD, Curai Health, and Hello Alpha.

The Gist: This is the kind of venture at which Amazon excels: creating a marketplace convenient for buyers and sellers (patients and telemedicine providers, respectively), pricing it competitively to pursue scale over margins, and upselling customers by pairing care with Amazon’s other products or services (like Amazon Pharmacy).

We’ll be watching for how Amazon builds on this service, and whether it connects Amazon Clinic to its Prime membership and One Medical assets. In the meantime, in addition to its consumer-focused offerings,Amazon is also simultaneously expanding its enterprise workflow offerings through its AWS for Health division, recently launching HealthScribe and HealthImaging.

This annual look at high-impact trends affecting healthcare in the coming year is based on evaluation of current industry research data. Healthcare Finance Trendsfor2023 (Trends) explores eight themes identified by CommerceHealthcare® ranging across four areas:

Financial. Providers enter the year contending with multiple financial stress points. They will also seek growth in technology-enabled remote care.

Patient financial experience. The need to drive not only improvement but also personalization of the financial experience is paramount. A central role will be played by patient financing programs which will see growing demand in 2023.

Trust. Building trust with all constituencies is explored as a linchpin for long-term provider success. The latest findings on cybersecurity show that this contributor to trust will continue to consume leadership attention.

Digital transformation. Pursuit of digital-first operations is accelerating, with the finance area an important focus. Emerging payment modes are finding a home in healthcare’s digital finance landscape.

This report’s consistent message is that these trends intersect in ways that compound both the challenges and the upside potential of strategies that address them.

1. Multiple Financial Stress Points Will Constrain Options

Healthcare’s financial predicament for the next 12–18 months is being described in strong terms. Citing $450 billion of EBITDA that could be in jeopardy, more than half of the industry’s project profit pool by 2027, one analyst suggests “a gathering storm.” Another perceives “broad and serious threats” as “elevated expenses” erode margins and exact “a profound financial toll.” Fitch Ratings issued a “deteriorating” outlook for nonprofit health systems.

These financial headwinds are upending healthcare’s traditional status as “recession-proof.” It is helpful to probe the multiple forces in play, the urgent workforce management challenge, and the varied solution set.

Multiple stress factors at work

Observing that margins will be down 37% in 2022 relative to pre-pandemic, a recent stark assessment concluded, “U.S. hospitals are likely to face billions of dollars in losses — which would result in the most difficult year for hospitals and health systems since the beginning of the pandemic.”

A confluence of factors is exacerbating the stress for 2023:

Rising acuity levels. Over two-thirds of surveyed C-suite executives said patient health has worsened from pandemic-induced delayed care. The upshot, stated by 27% of CFOs, is rising expenses due to higher acuity. Inpatient days are projected to increase at an 8% rate over the coming decade.

Reimbursement gaps and inflation. Commercial and government reimbursement rates are not keeping pace with rising costs. Surging inflation is widening this gap. Hospitals are also reporting substantial insurer payment delays and denials.

Investment declines. Stock and bond market declines have removed a cushion for operating weakness. Market uncertainty will complicate 2023 portfolio management.

Persistent workforce concerns remain center stage

Burnout and shortages have disrupted the clinical workforce. Nearly 60% of physician, advanced practice provider and nurse survey respondents said their teams are not adequately staffed, and 40% lack resources to operate at full potential. Many providers face extreme to moderate shortages of allied health professionals.

The problem extends beyond the clinical. A survey saw 48% of respondents experiencing severe labor deficiencies in revenue cycle management (RCM) and billing, and one in four finance leaders must fill over 20 positions to be fully staffed.

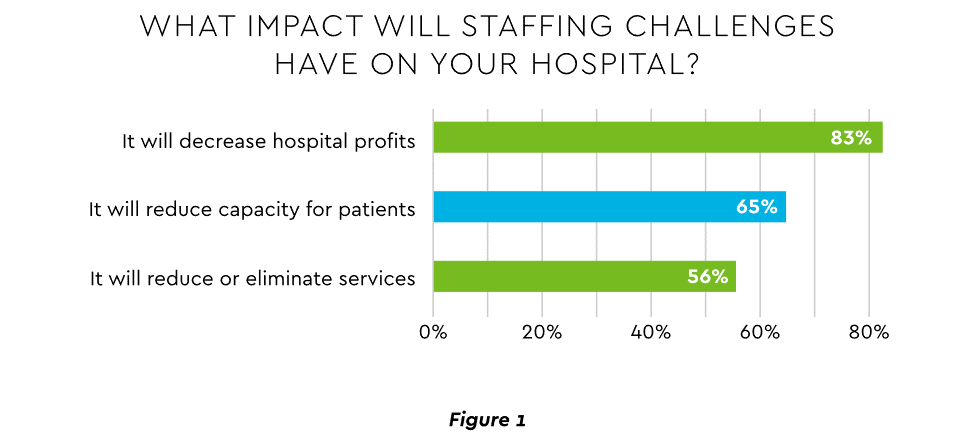

An executive outlook highlighted demonstrable impact on financial performance and growth from these workforce problems, citing reductions in profitability, capacity and service (Figure 1).1

Expenses. Hospital employee expense is expected to increase $57 billion from 2021 to 2022, with contract labor ballooning another $29 billion. Average weekly earnings are up 21.1% since early 2022. Half of medical practices budgeted higher staff cost-of-living increases in 2022. Shortages plague post-acute facilities as well. Their reduced capability to accept discharged patients is lengthening many hospitals’ patient stays.

Capacity constraint. Two-thirds of healthcare leaders identify “ability to meet demand” as their top workforce concern, suggesting a “looming capacity gap between future demand and labor supply.”

Range of measures being deployed

Health systems, hospitals and practices will vigorously pursue at least four direct actions to overcome the financial and staffing hurdles:

Cost cutting. Expense control will be paramount and “hospitals will be forced to take aggressive cost-cutting measures.” McKinsey estimates total industry administrative savings of $1 trillion through multiple aggressive changes.

Service line rationalization. Providers are rethinking how they deliver services to optimize efficiency. One path is utilizing “lower level” healthcare professionals in ways that free RNs and LPAs for more complex work suited to their top skills. Integrating remote care into the mix is another core element of the strategy.

Recruitment and retention programs. Attracting and retaining talent is crucial. Compensation is one avenue. Over two-thirds of organizations are offering signing bonuses for allied health professionals. Some are instituting value-based payments for physicians, offering salary floors to protect from drops in patient volume. CFOs and CNOs are joining forces to invest in nurse retention strategies.

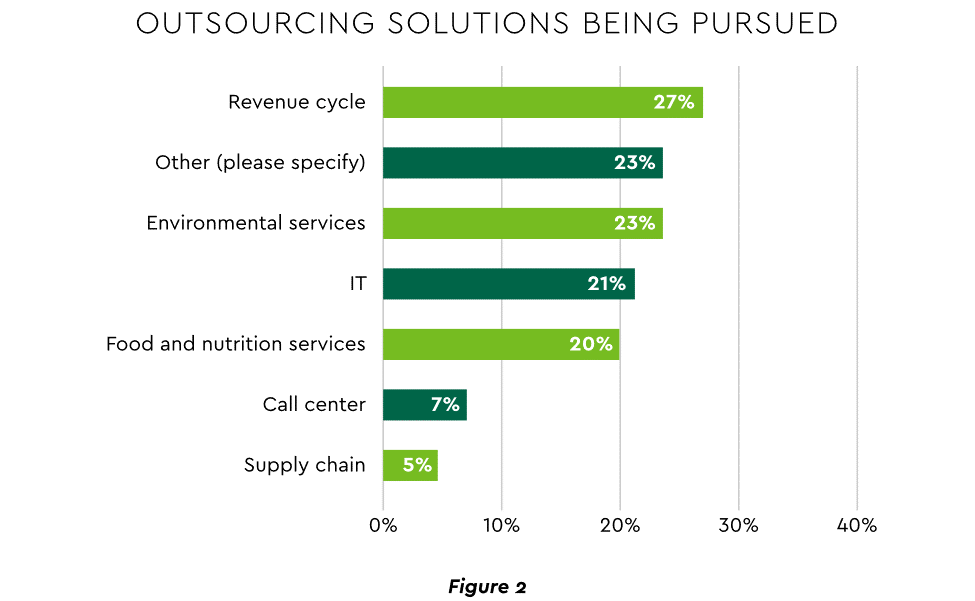

Staffing management. An increasingly popular tool to reduce labor cost and optimize staff resources is outsourcing. Figure 2 shows that RCM is leading the way among those using the solution.

2. Growth Strategies Favor Outpatient, Virtual, Acute Home Care

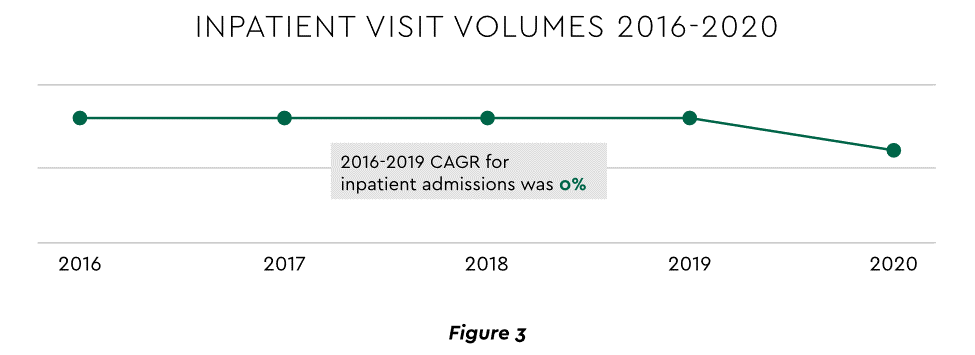

Pursuing top line growth in tandem with reining in expenses is essential. Inpatient volume growth has been tepid for several years ─ essentially flat in the 2016–20 period (Figure 3).

Leaders have been pivoting to outpatient and virtual care to diversify revenue streams. Two high-potential 2023 growth tracks in this sector merit deeper assessment.

Telehealth

Considerable evidence attests to strong commitment to telehealth and remote care. Sixty-three percent of physicians worldwide expect most consultations to be performed remotely within 10 years. Approximately 40% of health centers are using remote patient monitoring today. Consumers are also positive: 94% definitely or probably will use telehealth again, 57% prefer it for regular mental health visits and 61% use it for convenient care.

Telehealth is still in early stages of maturity. Only 4% of surveyed top executives consider their organization proficient at implementing remote care. Healthcare is also recognizing that a full telehealth ecosystem must be constructed. A physician leader explained that the industry’s early telehealth incarnations failed to build “virtual-only environments or really drive e-consults as a way of doing things.” A vital ecosystem demands alterations to current contracts, coding, collections, patient financing, staff training and other business practices.

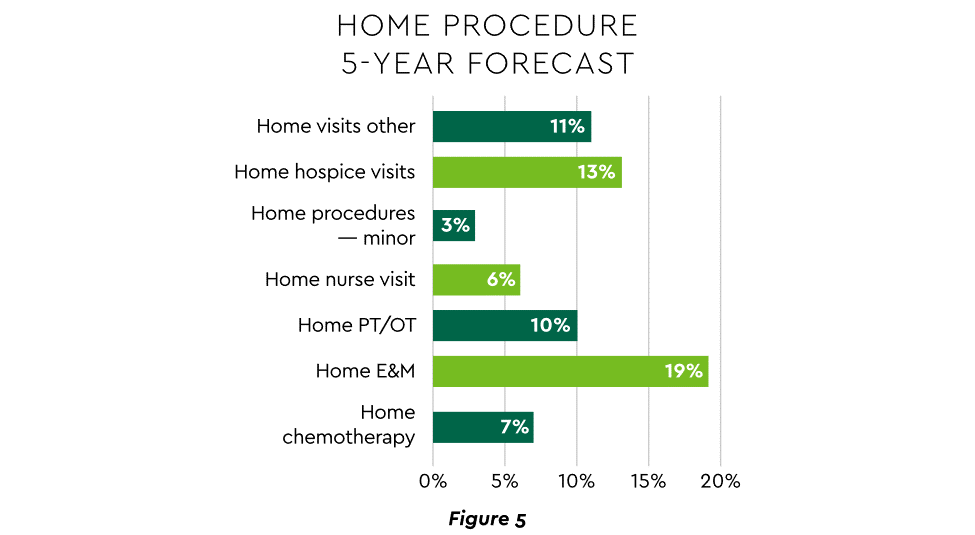

Hospital-at-Home (HaH)

Health systems see particularly promising growth in the provision of acute care in patients’ home settings, including post-surgical and cancer treatment. The federal government has already allowed waivers to 114 systems and 256 hospitals to obtain inpatient-level reimbursement for acute care at home. However, these waivers were prompted by the pandemic and are slated to end in early 2023. The renewal uncertainty has stymied some activity and represents an overhang on the opportunity. However, enthusiasm appears strong, and 33% of hospitals in a recent poll said they would be prone to continue HaH even without renewal.

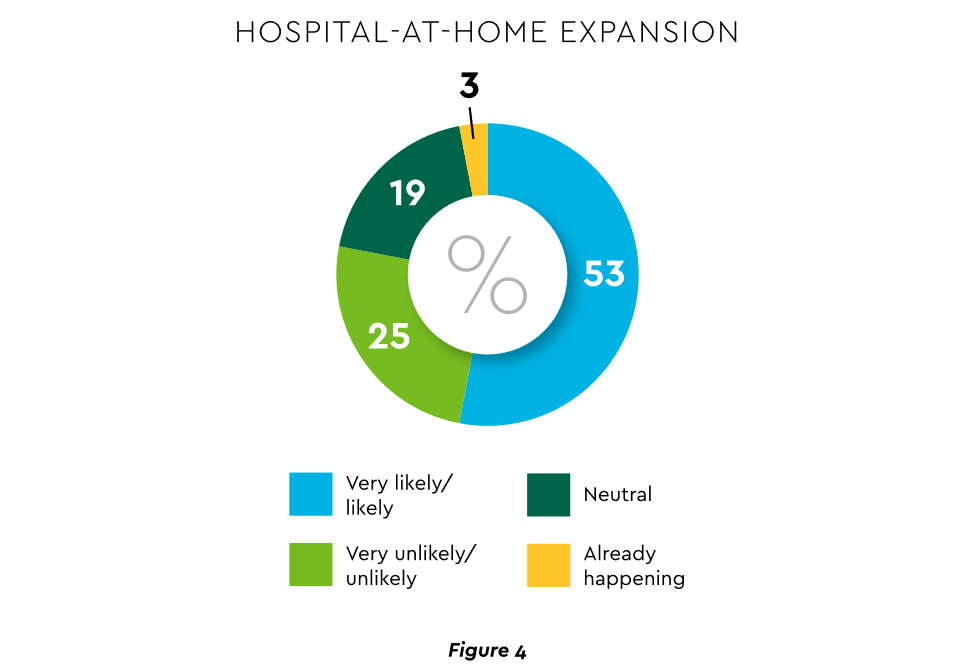

The forecasts are encouraging. Over half of hospitals believe it likely they will utilize HaH for at least half of their chronically ill patients over the next several years (Figure 4).

Harvesting the HaH potential will require implementation of current and emerging enabling technologies in remote monitoring, high-speed networks and artificial intelligence that generates algorithmic guidance for caregivers and patients alike.

3. Strong Drive to Improve and Personalize the Patient Financial Experience

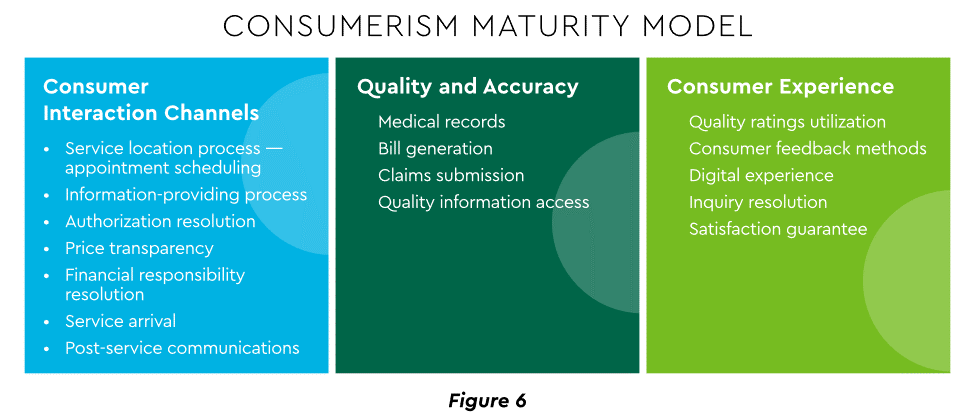

Today’s healthcare market dynamics place a premium on positive patient experiences. The goal is to deliver “an empathetic relationship between customers and brands built on what the customer wants and how they want to be treated.” It is a complex undertaking, with numerous touchpoints as captured in HFMA’s Consumerism Maturity Model (Figure 6).

An array of studies underscores the value proposition for intense provider focus on patient financial experience:

Sixty-one percent of consumers said that ease of making payments is very or somewhat important in decisions to continue seeing a doctor. Over half of patients also said text message reminders make them very or somewhat more likely to pay a bill faster than usual.

Thirty-five percent of respondents “have changed or would change healthcare providers to get a better digital patient administrative experience.”

A quality financial experience encompasses “simplified explanations, consolidated bills that match one’s health plan benefits, clear language displaying patient liability and payment options.”35

Significantly improving the financial experience requires a unified strategy, not just a collection of individual initiatives. Three threads to such a strategy will be prominent in 2023.

Using a Digital Front Door

Organizations have been moving swiftly to channel many patient financial transactions through an integrated Digital Front Door (DFD). This approach offers patients a singular online point of access and intelligent navigation to needed services. Growth is accelerating. A DFD is their patients’ first contact point for 55% of responding organizations, according to one technology survey. A leading forecaster sees 65% of patients engaging services via digital front doors by 2023.

Expanding price transparency

Mandates for full price transparency and “no surprises” billing are in effect, but estimates of compliance are mixed. An analysis of 2,000 hospitals determined that only 16% met the requirement to post an online “machine readable” file displaying clear charges for 300 “shoppable services.” Another assessment showed a more substantial 76% of hospitals had posted files, and 55% were deemed “complete.” One provision of interest to practices is the “good faith estimate” of expected charges required to be given to uninsured and self-pay individuals when they schedule visits. CommerceHealthcare® has worked with clients to enhance the patient financial experience by complementing their website pricing data with clear information on patient financing options and enrollment access. Bill pay information can also be added for one-stop guidance.

Personalizing the experience

Beyond choice and convenience, the deeper objective is truly personalized experiences throughout the care journey. The words of leading analysts best define the drive to personalize:

“Tomorrow’s healthcare experience will be built by patients tailoring their own experience.”

“By 2024, 30% of chronic care patients will truly own and openly leverage their personal health information to advocate for, secure, and realize better personalized care.”

Opportunities abound to personalize the patient financial experience. Automating manual processes establishes a foundation. Patient financing with no- or low-interest credit lines and flexible terms can produce monthly payment schedules tailored to each patient’s needs. Refunds can be made through multiple payment modes to meet varying patient preferences.

4. Evidence Underscores Growing Demand for Patient Financing

Emphasizing patient financing as part of the overall experience is powerful. Patients continue to struggle paying for care. Recent granular data details three related forces at work.

Meeting care costs difficult for many patients

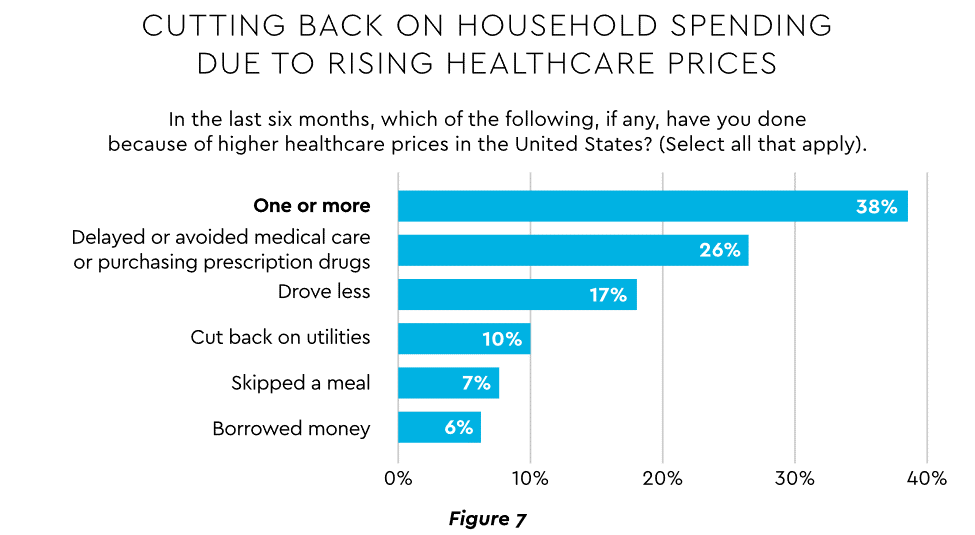

Commonwealth Fund found that 42% of individuals had problems paying medical bills or were paying off medical debt during the past year, while 49% were unable to pay an unexpected $1,000 medical bill.42 Health costs trigger reduction in a range of personal expenditures, led by deferring or avoiding care and drugs (Figure 7).

Twenty-eight percent of Americans now describe themselves as less prepared than last year to pay for routine or unanticipated care.

Patient obligation for care costs still rising

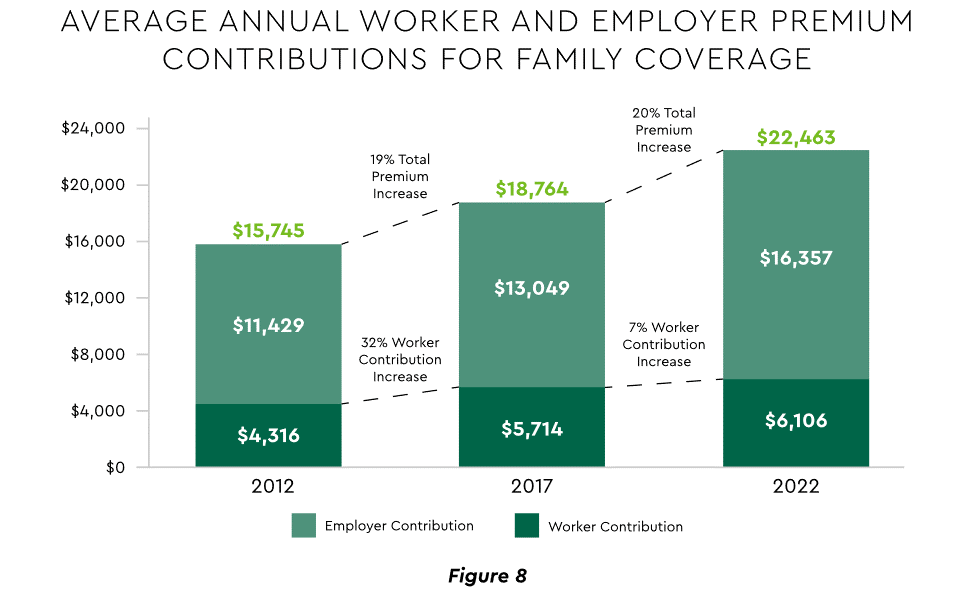

Patient obligation continues its upward march. Insurance premiums have climbed steadily for both the insured and their employers, and employees now pay over $6,000 annually on average for family coverage (Figure 8).45

High deductible health plans (HDHP) also place substantial burden on the patient. Through 2021, 28% of workers were enrolled in an HDHP with an average family deductible of $4,705. Employer satisfaction with these plans is high, auguring further expansion.

Providers feeling the financial effects

Patient payment difficulties are clearly impacting provider financials. A recent in-depth analysis uncovered substantial self-pay issues:

Self-pay accounts represented 60% of 2021 patient bad debt, up from 11% in 2018.

Nearly 18% of patient balances were over $7,500 and 17% over $14,000. Collections were noticeably lower at these balances.

Multiple chronic conditions add to the problem. A recent extensive analysis concluded: “Among individuals with medical debt in collections, the estimated amount increased with the number of chronic conditions ($784 for individuals with no conditions to $1,252 for individuals with 7–13).”

For their part, providers will be encouraged to broaden patient financing programs. Patients are certainly interested. When asked, 62% of consumers indicated they would use financing options or creative payment plans if available for large bill amounts. Many health systems, hospitals and practices will turn to outside help to satisfy the demand. A recent analysis recommended that health systems “consider keeping shorter-term payment plans in-house and extended term plans through external partnerships.”

Organizations will also need to step up their communications. A survey revealed that 64% of patients were unaware that their doctors and hospitals offered payment plans or financial help.

5. Building Trust Becoming a Critical Success Factor

Trust has emerged as a paramount issue today for most organizations as they encounter an “imperative to build trust and transparency among different stakeholder groups — employees, customers, suppliers, regulators and the communities in which they operate.” Healthcare is no exception, and the trust issue is growing in both complexity and urgency.

Healthcare’s trust gap

Trust in healthcare took a hit from the COVID-19 experience. A spring 2022 HFMA survey recorded 44% of finance leaders saying they perceived decreased patient trust. Between April 2020 and December 2021, the percentage of Americans who trusted information from doctors “a great deal” declined by 23%, from hospitals 21%, and from nurses 16%. The patient financial experience also faces “drivers of mistrust,” according to surveyed leaders who cited general payment confusion (58%), surprise billing (39%), high prices of commodity items (28%) and lack of price transparency (26%). Building trust reaps dividends. People who trust their providers are five times more likely to stay with them than those who are neutral or distrustful.

Strategies for building trust

Industry experts promote several approaches to galvanize trust among all constituencies:

Commitment. Embedding trust deeply in the organization requires full support from senior leadership.

Data transparency and governance. IDC predicts that “by end of 2023, 20% of expenses on care integration solutions will be centered around ‘trust’ to protect data, workflows and transactions.”

Reliance on fewer business partners. Many health systems, hospitals and practices are reducing their number of vendors in order to focus on a set of trusted long-term partners. For example, almost two-thirds of surveyed providers said they were seeking to streamline the number of software solutions over the next year.

The bank partner advantage

A provider’s banking relationship can yield valuable collaboration in the trust-building endeavor. Banks enjoy solid trust among consumers. As an example, 53.4% of consumers rated banks as most trusted to provide payment “super apps” and financial digital front doors ─ exceeding the next closest source by 10 points.

6. Cybersecurity in 2023: No Rest for the Weary

Cybersecurity is part of the trust calculus and has become an evergreen topic in healthcare. Compromised data and ransomware attacks are ongoing and leaders must continually refine their understanding in at least three areas: the overall security landscape, particular financially related considerations and contemporary security defenses.

The current landscape

The latest statistics quantify the cyber assault on healthcare:

Incidence. 89% of organizations suffered at least one attack in the past 12 months with the average number at 43.

Cost. A provider’s most serious attack costs an average of $4.4 million. IBM calculated healthcare’s average total cost of a breach at $10.1 million, up 42% since 2020.

Attack Characteristics. Healthcare data types most commonly compromised are personal (58%), medical (46%), and credentials (29%). Organizations have an exposure to an average of over 26,000 network-connected devices. A disturbing finding is that those healthcare institutions that paid ransom got back only 65% of their data in 2021.

Specific financial considerations

Finance leaders will also need awareness of the following:

Cyberattacks could affect credit ratings and are often a component of Environmental, Social and Governance assessments.

Financial outsourcing requires monitoring. A recent news story chronicled an accounts receivable firm’s breach that exposed individual information, account balances and payments.

Cyber insurance premiums are likely to increase substantially.

Responses/tools

Beyond a host of management and monitoring tools being deployed, a strategic philosophy is rapidly gaining ground. The “zero trust” model sounds counter to the trust-building mindset described earlier, but it has become essential. It “denies access to applications and data by default,” and 58% of hospitals and health systems have a zero trust initiative in place. Another 37% intend to implement one within 12–18 months.

Cybersecurity investment will challenge CFOs in 2023, especially in areas such as talent. Cybersecurity worker availability is estimated to satisfy only 68% of open positions. Banking partners will also be expected to play an important role. Over the years, major banks have become “leaders in enhancing cyber strategy and investing in cyber defenses, processes and talent.”

7. Digital Transformation of Finance In Focus

Digital transformation is fundamental to healthcare’s business and care delivery model changes. IBM’s website succinctly captures the goal, “Digital transformation means adopting digital-first customer, business partner, and employee experiences.” A leading forecaster believes 70% of healthcare organizations will rely on digital-first strategies by 2027.

Transformation efforts need to accelerate. One study showed that “digital, technology and analytics strategies exist for nearly all organizations, yet only 30% have begun to execute on those plans.”

One functional segment ramping up digital transformation is finance. According to a recent survey, 94% of CFOs and senior leaders stated that such efforts will be at the forefront of financial operations and strategy for 2023–2024, and 79% described it as an “absolute need” for “commercial stabilization and long-term survival of their healthcare organization.”

Advanced technology is gaining traction. Many see optimization in combining robotic process automation (RPA), artificial intelligence and machine learning to create “intelligent automation.” Together, these technologies create algorithms to automate decisions that guide “robotic” software to perform financial actions and thereby reduce manual labor.

Getting to digital-first in finance and across the enterprise has several critical success factors. These include sustained commitment, a platform-centric mindset and effective governance.

Commitment

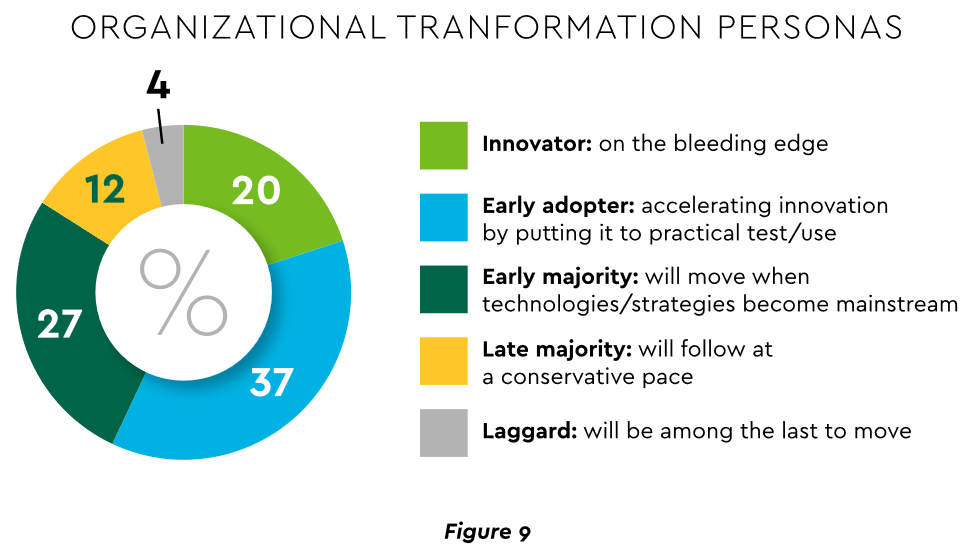

Some assert that few healthcare executives have “created digital strategies that look far enough into the future.” Speed of change is also important. Health systems, hospitals and practices exhibit varying risk appetites and change rates. When asked to self-identify “transformation personas,” a little over half regarded themselves as being on the innovative “early mover” end of the spectrum, while the remainder will adapt as technologies prove themselves (Figure 9). Slower organizations will likely need to increase the pace.

Implementing enterprise platforms rather than proliferating “point solutions” is obligatory. Organizations must be “prepared to compete in the platform economy as platform-based business models have changed the way we live, work and receive care.”

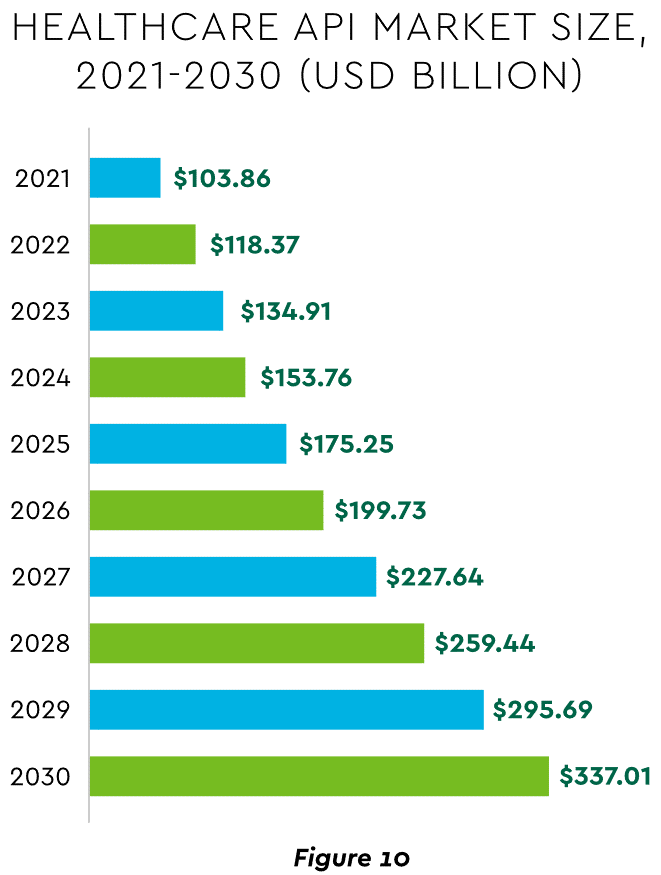

There are still too many tools and applications. A survey of top decision-makers at health systems found that 60% use over 50 software solutions just in operations (24% have over 150). System integration is one answer. Use of application programming interfaces (API) helps this effort substantially. API-first is fast becoming the norm among solution providers, with global API investment expected to nearly triple by 2030 (Figure 10)

Effective governance is vital to constructing a platform-based transformative model and to ensuring wide user adoption. Healthcare has seen the rise of new senior roles such as Chief Digital Officer and Chief Transformation Officer, positions focusing on initiatives like ownership of technology success at the department level and devising user incentives.

8. Digital Payments on the Horizon for Healthcare

A variety of emerging digital payment modes will further the transformation of finance. These payments are expected to grow almost 23% annually in healthcare. ACH payments have been on a strong upward trajectory in healthcare for several years, especially for business transactions. In 2021, ACH tallied a yearly increase of 18% in volume and 5% in dollars.

Notable technologies and payment rails to watch for expected crossover from consumer markets to healthcare include:

Mobile payments. The market for mobile payment technologies has been growing at a 16% compound annual clip and should reach $90 billion in 2023, powered by wide smartphone use, 5G networks and convenience. This category encompasses technologies such as e-wallets, forecasted to grow 23% annually worldwide through 2030.

Real-time payments (RTP). These digital transactions are settled nearly instantaneously through platforms such as The Clearing House. One forecast sees 30.4% compound RTP growth in the U.S. from 2022 to 2030.

Buy Now Pay Later (BNPL). This growing mode offers consumers short-term financing to stretch payments over several installments. A recent survey established that 23% of American adult respondents have used a BNPL service. BNPL is just entering healthcare and is currently regarded as an option for certain elective or cosmetic procedures or for specific individual credit scenarios.

Earned Wage Access (EWA). Using an RTP approach, employers are beginning to offer on-demand pay which enables “instant access to earned wages right after the work is performed, at the end of the shift, or upon completion of a project.” It is not a loan or advance pay. A 2021 poll conducted by Harris found that 83% of U.S. workers feel they should be able to access earned wages at the end of each day. Millennials were particularly interested: 80% would like daily automatic pay streaming to their bank accounts, and 78% said free EWA would boost loyalty to their employer. Given its pressing workforce concerns, healthcare is likely to find EWA a tool to promote retention.

Seeking the right use cases for these payment technologies offers many potential provider benefits.

Conclusion

The connected forces discussed and quantified here create major challenges to address in 2023. The strategic agenda calls for balancing tight cost control with investment in growth opportunities, significantly enhancing patient financial experience by meeting growing patient financial need, shoring up trusted relationships and cybersecurity, and accelerating the digital transformation of finance.

There is no shortage of challenges to confront in healthcare today, from workforce shortages and burnout to innovation and health equity (and so much more). We’re committed to giving industry leaders a platform for sharing best practices and exchanging ideas that can improve care, operations and patient outcomes.

Check out this podcast interview with Ketul J. Patel, CEO at Virginia Mason Franciscan Health and division president, Pacific Northwest at CommonSpirit Health, for his insights on where healthcare is headed in the future.

In this episode, we are joined by Ketul J. Patel, Division President, Pacific Northwest; Chief Executive Officer, CommonSpirit Health; Virginia Mason Franciscan Health, to discuss his background & what led him to executive healthcare leadership, challenges surrounding workforce shortages, the importance of having a strong workplace culture, and more.

The executives featured in this article are all speaking at the Becker’s Healthcare 13th Annual Meeting April 3-6, 2023, at the Hyatt Regency in Chicago.

Question: What will hospitals and health systems look like in 10 years? What will be different and what will be the same?

Michael A. Slubowski. President and CEO of Trinity Health (Livonia, Mich.): In 10 years, inpatient hospitals will be more focused on emergency care, intensive/complex care following surgery or complex medical conditions, and short-stay/observation units. Only the most complex surgical cases and complex medical cases will be inpatient status. Most elective surgery and diagnostic services will be done in freestanding surgery, procedural and imaging centers. Many patients with chronic medical conditions will be managed at home using digital monitoring. More seniors will be cared for in homes and/or in PACE programs versus skilled nursing facilities.

Mark A. Schuster, MD, PhD. Founding Dean and Chief Executive Officer of Kaiser Permanente Bernard J. Tyson School of Medicine (Pasadena, Calif.): The future of hospitals might not actually unfold in hospitals. I expect that more and more of what we now do in hospitals will move into the home. The technology that makes this transition possible is already out there: Remote monitoring of vital signs and lab tests, remote visual exams, and videoconferencing with patients. And all of this technology will improve even more over the next 10 years — turning at-home care from a dream into a reality.

Imagine no longer being kept awake all night by beeps and alarms coming from other patients’ rooms or kept away from family by limited visiting hours. The benefits are especially welcome for people who live in rural places and other areas with limited medical facilities. Who knows? Maybe robotics will make some in-home surgeries not so far off!

Of course, not all patients have a safe or stable home environment where they could receive care, so hospitals aren’t going away anytime soon. I’m not suggesting that most current patients could be cared for remotely in a decade — but I do think we’re moving in that direction. So those of us who work in education will need to train medical, nursing, and other students for a healthcare future that looks quite different from the healthcare present and takes place in settings we couldn’t imagine 10 years ago.

Shireen Ahmad. System Director, Operations and Finance of CommonSpirit Health (Chicago): The biggest change I anticipate is a continuation in the decentralization of health services delivery that has typically been provided by hospitals. This will result in a reduction of hospitals with fewer services performed in acute settings and with more services provided in non-acute ones.

With recent reimbursement changes, CMS is helping to set the tone of where care is delivered. Hospitals are beginning to rationalize services, including who and where care is delivered. For example, pharmacies often carry clinics that provide vaccinations, but in France, one can go to a pharmacy for care and sterilization of minor wounds while only paying for bandages, medication and other supplies used in the visit. I would not be surprised if, in 10 years, one could get an MRI at their local Walmart or schedule routine screenings and tests at the grocery store with faster, more accurate results as they check out their produce.

If the pandemic has taught us anything, there will always be a need for acute care and our society will always need hospitals to provide care to sick patients. This is not something I would anticipate changing. However, the need to provide most care in a hospital will change with the result leading to fewer hospitals in total. Far from being a bleak outlook, however, I believe that healthier, sustainable health systems will prevail if they are able to provide a greater spectrum of care in broader settings focussing on quality and convenience.

Gerard Brogan. Senior Vice President and Chief Revenue Officer of Northwell Health (New Hyde Park, N.Y.): Operationally, hospitals and health systems will be more designed around the patient experience rather than the patient accommodating to the hospital design and operations. Specifically, more geared toward patient choice, shopping for services, and price competition for out-of-pocket expenses. In order to bring costs down, rational control of utilization will be more important than ever. Hopefully, we will be able to shrink the administrative costs of delivering care. Structurally, more care will continue to be done ambulatory, with hospitals having a greater proportion of beds having critical care capability and single rooms for infection control, putting pressure on the cost per square foot to operate. Sustainable funding strategies for safety net hospitals will be needed.

Mike Gentry. Executive Vice President and COO of Sentara Healthcare (Norfolk, Va.): During the next 10 years, more rural hospitals will become critical assessment facilities. The legislation will be passed to facilitate this transition. Relationships with larger sponsoring health systems will support easy transitions to higher acuity services as required. In urban areas, fewer hospitals with greater acuity and market share will often match the 50 percent plus market share of health plans. The ambulatory transition will have moved beyond only surgical procedures into outpatient but expanded historical medical inpatient status in ED/observation hubs.

The consumer/patient experience will be vastly improved. Investments in mobile digital applications will provide greatly enhanced communication, transparency of clinical status, timelines, the likelihood of expected outcomes and cost. Patients will proactively select from a menu of treatment options provided by predictive AI. The largest 10 health systems will represent 25 percent of the total U.S. acute care market share, largely due to consumer-centric strategic investments that have outpaced their competitors. Health systems will have vastly larger pharma operations/footprints.

Ketul J. Patel. CEO of Virginia Mason Franciscan Health (Seattle) and Division President, Pacific Northwest of CommonSpirit Health (Chicago): This is a transformative time in the healthcare industry, as hospitals and healthcare systems are evolving and innovating to meet the growing and changing needs of the communities we serve. The pandemic accelerated the digital transformation of healthcare. We have seen the proliferation of new technologies — telemedicine, artificial intelligence, robotics, and precision medicine — becoming an integral part of everyday clinical care. Healthcare consumers have become empowered through technology, with greater control and access to care than ever before.

Against this backdrop, in the next decade we’ll see healthcare consumerism influencing how health systems transform their hospitals. We will continue incorporating new technologies to improve healthcare delivery, offering more convenient ways to access high-quality care, and lowering the overall cost of care.

SMART hospitals, including at Virginia Mason Franciscan Health, are utilizing AI to harness real-time data and analysis to revolutionize patient and provider experiences and improve the quality of care. VMFH was the first health system in the Pacific Northwest to introduce a virtual hospital nearly a decade ago, which provides virtual services in the hospital across the continuum of care to improve quality and safety through remote patient monitoring and care delivery.

As hospitals become more high-tech, more nimble, and more efficient over the next 10 years, there will be less emphasis on brick-and-mortar buildings as we continue to move care away from the hospital toward more convenient settings for the patient. We recently launched VMFH Home Recovery Care, which brings all the essential elements of hospital-level care into the comfort and convenience of patients’ homes, offering a safe and effective alternative to the traditional inpatient stay.

Health systems and hospitals must simplify the care experience while reducing the overall cost of care. VMFH is building Washington state’s first hybrid emergency room/urgent care center, which eliminates the guesswork for patients unsure of where to go for care. By offering emergent and urgent care in a single location, patients get the appropriate level of care, at the right price, in one convenient location.

As healthcare delivery becomes more sophisticated in this digital age, we must not lose sight of why we do this work: our patients. There is no device or innovation that can truly replace the care and human intelligence provided by our nurses, APPs and physicians. So, while hospitals and health systems might look and feel different in 2033, our mission will remain the same: to provide exceptional, compassionate care to all — especially the most vulnerable.

David Sylvan. President of University Hospitals Ventures (Cleveland): American healthcare is facing an imperative. It’s clear that incremental improvements alone won’t manifest the structural outcomes that are largely overdue. The good news is that the healthcare industry itself has already initiated the disruption and self-disintermediation. I would hope that in the next 10 years, our offerings in healthcare truly reflect our efforts to adopt consumerism and patient choice, alleviate equity barriers and harness efficiencies while reducing time waste.

We know that some of this will come about through technology design, build and adoption, especially in the areas of generative artificial intelligence. But we also know that some of this will require a process overhaul, with learnings gleaned from other industries that have already solved adjacent challenges. What won’t change in 10 years will be the empathy and quality of care that the nation’s clinicians provide to patients and their caregivers daily.

Joseph Webb. CEO of Nashville (Tenn.) General Hospital: The United States healthcare industry operates within a culture that embraces capitalism as an economic system. The practice of capitalism facilitates a framework that is supported by the theory of consumerism. This theory posits that the more goods and services are purchased and consumed, the stronger an economy will be. With that in mind, healthcare is clearly a driver in the U.S. economy, and therefore, major capital and technology are continuously infused into healthcare systems. Healthcare is currently approaching 20 percent of the U.S. gross domestic product and will continue to escalate over the next 10 years.

Also, in 10 years, there will be major shifts in ownership structures, e.g., mergers, acquisitions, and consolidations. Many healthcare organizations/hospitals will be unable to sustain operations due to shrinking profit margins. This will lead to a higher likelihood of increasing closures among rural hospitals due to a lack of adequate reimbursement and rising costs associated with salaries for nurses, respiratory therapists, etc., as well as purchasing pharmaceuticals.

Aging baby boomers with chronic medical conditions will continue to dominate healthcare demand as a cohort group. To mitigate the rising costs of care, healthcare systems and providers will begin to rely even more heavily on artificial intelligence and smart devices. Population health initiatives will become more prevalent as the cost to support fragmented care becomes cost-prohibitive and payers such as CMS will continue to lead the way toward value-based care.

Because of structural and social conditions that tend to drive social determinants of health, which are fundamental causes of health disparities, achieving health equity will continue to be a major challenge in the U.S. Health equity is an elusive goal that can only be achieved when there is a more equitable distribution of SDOH.

Gary Baker. CEO, Hospital Division of HonorHealth (Scottsdale, Ariz.): In 10 years, I would expect hospitals in health systems to become more specialized for higher acuity service lines. Providing similar acute services at multiple locations will become difficult to maintain. Recruiting and retaining specialty clinical talent and adopting new technologies will require some redistribution of services to improve clinical quality and efficiency. Your local hospital may not provide a service and will be a navigator to the specialty facilities. Many services will be provided in ambulatory settings as technology and reimbursement allow/require. Investment in ambulatory services will continue for the next 10 years.

Michael Connelly. CEO Emeritus of Bon Secours Mercy Health (Cincinnati): Our society will be forced to embrace economic limits on healthcare services. The exploding elderly population, in combination with a shrinking workforce to fund Medicare/Medicaid and Social Security, will force our health system to ration care in new ways. These realities will increase the role of primary care as the needed coordinator of health services for patients. Diminishing fragmented healthcare and redundant care will become an increasing focus for health policy.

David Rahija. President of Skokie Hospital, NorthShore University HealthSystem (Evanston, Ill.): Health systems will evolve from being just a collection of hospitals, providers, and services to providing and coordinating care across a longitudinal care continuum. Health systems that are indispensable health partners to patients and communities by providing excellent outcomes through seamless, coordinated, and personalized care across a disease episode and a life span will thrive. Providers that only provide transactional care without a holistic, longitudinal relationship will either close or be consolidated. Care tailored to the personalized needs of patients and communities using team care models, technology, genomics, and analytics will be key to executing a personalized, seamless, and coordinated model of care.

Alexa Kimball, MD. President and CEO of Harvard Medical Faculty Physicians at Beth Israel Deaconess Medical Center (Boston): Ten years from now, hospitals will largely look the same — at least from the outside. Brick-and-mortar buildings aren’t going away anytime soon. What will differ is how care is delivered beyond the traditional four walls. Expect to see a more patient-centered and responsive system organized around what individuals need — when and where they need it.

Telehealth and remote patient monitoring will enable greater accessibility for patients in underserved areas and those who cannot get to a doctor’s office. Technology will not only enable doctors to deliver more personalized treatment plans but will also dramatically reshape physician workflows and processes. These digital tools will streamline administrative tasks, integrate voice commands, and provide more conducive work environments. I also envision greater access to data for both providers and patients. New self-service solutions for care management, scheduling, pricing, shopping for services, etc., will deliver a more proactive patient experience and make it easier to navigate their healthcare journey.

Ronda Lehman, PharmD. President of Mercy Health – Lima (Ohio):

This is a highly challenging question to address as we continue to reevaluate how healthcare is being delivered following several difficult years and knowing that financial challenges still loom. That said, when I am asked what it will look like, I am keenly aware of the fact that it only will look that way if we can envision a better way to improve the health of our communities. So 10 years from now, we need to have easier and more patient-driven access to care.

We will need to stop doing ‘to people’ and start caring ‘with people.’ Artificial intelligence and proliferous information that is readily available to consumers will continue to pave the way to patients being more empowered and educated about their options. So what will differentiate healthcare of the future? Enabling patients to make informed decisions.

Undoubtedly, technology will continue to advance, and along with it, the associated costs of research and development, but healthcare can only truly change if providers fundamentally shift their approach to how we care for patients. It is imperative that we need to transform from being the gatekeepers of valuable resources and services to being partners with patients on their journey. If that is what needs to be different, then what needs to be the same? We need the same highly motivated, highly skilled and perhaps most importantly, highly compassionate caregivers selflessly caring for one another and their communities.

Mike Young. President and CEO of Temple University Health System (Philadelphia): Cell therapy, gene therapy, and immunotherapy will continue to rapidly improve and evolve, replacing many traditional procedures with precise therapies to restore normal human function — either through cell transfer, altering of genetic information, or harnessing the body’s natural immune system to attack a particular disease like cancer, cystic fibrosis, heart disease, or diabetes. As a result, hospitals will decrease in footprint, while the labs dedicated to defining precision medicine will multiply in size to support individual- and disease-specific infusion, drug, and manipulative therapies.

Hospitals will continue to shepherd the patient journey through these therapies and also will continue to handle the most complex cases requiring high-tech medical and surgical procedures. Medical education will likely evolve in parallel, focusing more on genetic causation and treatment of disease, as well as proficiency with increasingly sophisticated AI diagnostic technologies to provide adaptive care on a patient-by-patient basis.

Tom Siemers. Chief Executive Officer of Wilbarger General Hospital (Vernon, Texas): My predictions include the national healthcare landscape will be dominated by a dozen or so large systems. ‘Consolidation’ will be the word that describes the healthcare industry over the next 10 years. Regional systems will merge into large, national systems. Independent and rural hospitals will become increasingly rare. They simply won’t be able to make the capital investments necessary to replace outdated facilities and equipment while vying with other organizations for scarce, licensed personnel.

Jim Heilsberg. CFO of Tri-State Memorial Hospital & Medical Campus (Clarkston, Wash.): Tri-State Hospital continues to expand services for outpatient services while maintaining traditionally needed inpatient services. In 10 years, there will be expanded outpatient services that include leveraged technology that will allow the patient to be cared for in a yet-to-be-seen care model, including traditional hospital settings and increasing home care setting solutions.

Jennifer Olson. COO of Children’s Minnesota (St. Paul, Minn.): I believe we will see more and better access to healthcare over the next 10 years. Advances in diagnostics, monitoring, and artificial intelligence will allow patients to access services at more convenient times and locations, including much more frequently at home, thereby extending health systems’ reach well beyond their walls.

What I don’t think will ever change is the heart our healthcare professionals bring with them to work every day. I see it here at Children’s Minnesota and across our industry: the unwavering commitment our caregivers have to help people live healthier lives.

If I had one wish for the future, it would be that we become better equipped to address the social determinants of health: all of the factors outside the walls of our hospitals and clinics that affect our patients’ well-being. Part of that means relaxing regulations to allow better communication and sharing of information among healthcare providers and public and private entities, so we can take a more holistic approach to improve health and decrease disparities. It also will require a fundamental shift in how health and healthcare are paid for.

Stonish Pierce. COO of Holy Cross Health, Trinity Health Florida: Over the next decade, many health systems will pivot from being ‘hospital’ systems to true ‘health’ systems. Based largely on responding to The Joint Commission’s New Requirements to Reduce Health Care Disparities, many health systems will place greater emphasis on reducing health disparities, enhanced attention to providing culturally competent care, addressing social determinants of health (including, but not limited to food, housing and transportation) and health equity. I’m proud to work for Trinity Health, a system that has already directed attention toward addressing health disparities, cultural competency and health equity.

Many systems will pivot from offering the full continuum of services at each hospital and instead focus on the core services for their respective communities, which enables long-term financial sustainability. At the same time, we will witness the proliferation of partnerships as adept health systems realize that they cannot fulfill every community’s needs alone. Depending upon the specialty and region of the country, we may see some transitioning away from the RVU physician compensation model to base salaries and value-based compensation to ensure health systems can serve their communities in the long term.

Driven largely by continued workforce supply shortages, we will also see innovation achieve its full potential. This will include, but not be limited to, virtual care models, robots to address functions currently performed by humans, and increased adoption of artificial intelligence and remote monitoring. Healthcare overall will achieve parity in technological adoption and innovation that we take for granted and have grown accustomed to in industries such as banking and the consumer service industries.

For what will remain the same, we can anticipate that government reimbursement will still not cover the cost of providing care, although systems will transition to offering care models and services that enable the best long-term financial sustainability. We will continue to see payers and retail pharmacies continue to evolve as consumer-friendly providers. We will continue to see systems make investments in ambulatory care and the most critically ill patients will remain in our hospitals.

Jamie Davis. Executive Director, Revenue Cycle Management of Banner Health (Phoenix): I think that we will see a continued shift in places of service to lower-cost delivery sources and unfavorable payer mix movement to Medicare Advantage and health exchange plans, degrading the value of gross revenue. The increased focus on cost containment, value-based care, inflation, and pricing transparency will hopefully push payers and providers to move to a more symbiotic relationship versus the adversarial one today. Additionally, we may see disruption in the technology space as the venture capital and private equity purchase boom that happened from 2019 to 2021 will mature and those entities come up for sale. If we want to continue to provide the best quality health outcomes to our patients and maintain profitability, we cannot look the same in 10 years as we do today.

James Lynn. System Vice President, Facilities and Support Services of Marshfield Clinic Health System (Wis.): There will be some aspects that will be different. For instance, there will be more players in the market and they will begin capturing a higher percentage of primary care patients. Walmart, Walgreens, CVS, Amazon, Google and others will begin to make inroads into primary care by utilizing VR and AI platforms. More and more procedures will be the same day. Fewer hospital stays will be needed for recovery as procedures become less invasive and faster. There will be increasing pressure on the federal government to make healthcare a right for all legal residents and it will be decoupled from employment status. On the other hand, what will stay the same is even though hospital stays will become shorter for some, we will also be experiencing an ever-aging population, so the same number of inpatient beds will likely be needed.

On Monday, San Francisco-based Carbon Health—a virtual-first primary and urgent care company with 125 clinics across 13 states—announced a partnership with CVS Health, which includes a $100M investment, as well as plans to pilot its operating model in select CVS stores. The announcement came just days after Carbon reported its second round of layoffs in the past year, as it scales back on less profitable business segments to focus on expanding its primary care model.

The Gist: It’s been over a year since CVS CEO Karen Lynch said the company was moving with “speed and urgency” to construct a physician-staffed primary care model. Last fall it purchased in-home health evaluation company Signify Health for $8B, after rumors that it had been close to acquiring One Medical.

Between its convenient retail footprint, insurance arm, and Signify’s risk-assessment tools, a nationwide primary care physician network is the last puzzle piece CVS needs to field a comprehensive and formidable primary care strategy.

While it’s currently rumored to be evaluating a $10B acquisition of Oak Street Health, this partnership with Carbon Health is a better bet to deliver value quickly, as CVS should be able to more easily integrate and leverage Carbon’s retail health expertise across its growing care delivery platform.

We expect 2023 to be a pivotal year for the industry, as the accelerated acceptance of virtual care and demographic trends, such as an aging population, increasing chronic illnesses and healthcare worker shortages, sustain demand for medtech-enabled solutions.

The combination of rapid developments in novel healthcare technology and heightened demand for integrated tech-enabled care has continued to fuel innovation in the medtech industry. At the same time, medtech innovators – whether in digital health, wearables and AI-driven offerings in healthcare, or diagnostics, telemedicine and health IT solutions – continue to face a patchwork of laws, rules and norms across the world. Life sciences and healthcare innovators and regulators are also looking to medtech to increase access to care and health equity. Here are ten global medtech themes we are tracking in the coming year:

Focus on digital tuck-in acquisitions in medtech M&A

Despite continued uncertainty in the overall financial market, medtech M&A activity continued at a steady pace in 2022. This year witnessed a rise in tuck-in acquisitions of smaller companies that can be easily integrated into buyers’ existing infrastructure and product offerings, as opposed to significantly sized takeovers of businesses that aren’t squarely aligned with buyers’ existing businesses lines. Medtech acquirers have been particularly focused on developing their digital capabilities to innovate and reach customers in new ways. As digitization continues to transform the industry, we expect acquirers to continue to prioritize the value of digital and data assets as they evaluate potential targets.

Continued interest by private equity and other financial sponsors

Private equity firms, healthcare-focused funds and other financial sponsors have continued to display a strong appetite for investing in Medtech companies, with top targets in subsectors such as diagnostics and healthcare IT solutions. Later-stage medtech companies in particular are gaining a larger share of venture capital funding, as later-stage investments allow financial sponsors to focus on businesses with higher yields, as well as less time to market and capital reimbursement. Demographic trends, including an aging population and the increasing prevalence of chronic diseases, coupled with healthcare technology advancements have created robust demand for medtech-enabled solutions. Additionally, medtech offerings have broad applications that can extend beyond stakeholders in a specific therapy area, product category or care setting, offering the ability to satisfy unmet needs with large patient bases.

Strategic medtech collaborations as the new norm

Strategic medtech collaborations and partnerships have become the new norm in our increasingly connected digital healthcare ecosystem. In response to heightened consumer demand for tech-enabled care, pharmaceutical and medtech companies are collaborating to use digital technologies to engage with consumers, unlocking a vast range of treatments such as personalized medicine. Additionally, as the market rapidly evolves towards data-driven healthcare, we expect medtech companies to continue to work collaboratively to address existing barriers to data sharing and promote interoperability of healthcare data.

Continued scrutiny by antitrust and competition authorities

As expected, global antitrust and competition authorities continued to focus on the tech, life sciences and medtech sectors in 2022. The US, UK and EU authorities have stepped up efforts to investigate and challenge conduct by large pharma and technology companies pursuing mergers and acquisitions. We expect these authorities to assess similar concerns in the digital health context in an effort to account for the value of combined datasets and the interoperability of various offerings that could be derived from digital health mergers and acquisitions. Furthermore, geopolitical tensions have resulted in new and expanded foreign investment regimes to improve the resilience of domestic healthcare systems. Notably this year, the UK government implemented the National Security and Investment Act that allows it to restrict transactions that may threaten national security, including in the AI and data infrastructure sectors. Sensitive data continues to be a recurring theme for foreign investment review for Committee on Foreign Investment in the US and that of the EU as well.

Growing importance of data privacy and security

Increasing regulatory attention to sensitive health data and the escalating rise of ransomware attacks has made data privacy and security more important than ever for medtech innovators. The Federal Trade Commission has issued several statements about its willingness to “fully” enforce the law against the illegal use and sharing of highly sensitive data. Additionally, several state privacy laws coming into effect in 2023 create new categories of sensitive personal data, including health data, and impose novel obligations on innovators to obtain data-related consents. As ransomware continues to pose security-related threats, the US Department of Health and Human Services renewed calls for all covered entities and business associates to prioritize cybersecurity. New standards, such as cybersecurity label rating programs for connected devices, aim to address security risks. In the EU, medtech providers will need to consider how the launch of the European Health Data Space and newly proposed data regulation, such as the Data Act and AI Act, could impact their data use and sharing practices.

More active engagement with FDA/EMA/MHRA

We expect companies active in the medtech sector, particularly those that make use of AI and other advanced technologies, to continue their conversations with the U.S. Food and Drug Administration (“FDA”), the European Medicines Agency (“EMA”), the Medicines and Healthcare Products Regulatory Agency (“MHRA”) and other regulators as such companies grow their medtech business lines and establish their associated regulatory compliance infrastructure. Given the unique regulatory issues arising from the implementation of digital health technologies, we expect the FDA, EMA and MHRA to provide additional guidance on AI/ML-based software-as-a-medical device and the remote management of clinical trials. 2022 saw stakeholders in the life sciences and medtech industries collaborate with regulatory authorities to push forward the acceptance of digital endpoints that rely on sensor-generated data collected outside of a clinical setting. As the industry shifts to decentralized clinical trials, we expect both innovators and regulators to work together to evaluate the associated clinical, privacy and safety risks in the development and use of such digital endpoints.

Increasing medtech localization in the Asia Pacific region

2022 saw multinational companies (“MNCs”), including American pharma/device makers make an active effort to expand their medtech business lines in the Asia Pacific region. At the same time, government authorities in the region have been increasingly focused on incentivizing local innovation, approving government grants and prohibiting the importation of non-approved medical equipment. In light of MNCs’ market share of the medical device market in the Asia Pacific region, especially in China, we expect the emergence of the domestic medtech industry to prompt discussions among MNCs, local innovators and government authorities over the long-term development of the global market for medical technology.

Long-term adoption of telehealth and remote patient monitoring technologies

The Covid-19 pandemic saw the rise of telehealth and remote patient monitoring technologies as key modes of healthcare delivery. The telehealth industry remains focused on enabling remote consultations and long-term patient management for patients with chronic conditions. Looking forward, we expect to see increased innovation in non-invasive technologies that can provide early diagnostics and ongoing disease management in a low-friction manner. At the same time, we anticipate telehealth companies to face increasing scrutiny from regulatory authorities around the world for fraud and abuse by patients and providers. Consumer and patient data privacy and security in connection with telehealth and remote patient monitoring continue to remain top of mind for regulators as well.

Women’s health and privacy concerns for medtech

We expect to see increased consumer health tech adoption for reproductive care, especially in light of the U.S. Supreme Court’s decision to overturn Roe v. Wade. Following the Dobbs decision, a number of states introduced or passed legislation that prohibits or restricts access to reproductive health services beyond abortion. In response, women’s health-focused companies are expanding their virtual fertility and pregnancy, telemedicine and other services to patients. At the same time, such companies need to assess the legal risks stemming from the collection and storage of their customers’ personal health information, which could then be used as evidence to prosecute customers for obtaining illegal reproductive health services. We expect companies active in this space to take steps to navigate the patchwork of data privacy and security laws across jurisdictions while establishing clear digital health governance mechanisms to safeguard their customers’ data privacy and security.

Addressing inequities in the implementation of digital healthcare technologies

Medtech innovators and regulators have been increasingly focused on addressing inequities in the healthcare system and the data used to train AI and ML-based digital healthcare technologies. In 2022, a number of medtech companies collaborated to provide technologies that result in improved patient outcomes across all populations, as well as boost participation of diverse populations in clinical trials. In parallel, we are seeing increased interest from regulators to reduce bias in digital health technologies and the accompanying datasets, as evidenced by the EU’s proposed AI Act and the UK’s health data strategy. In the US, which currently lacks comprehensive government regulation of AI in healthcare, there have been increasing calls for institutional commitments in the area of algorithmovigilance. Because of the inaccurate conclusions that may result from biased technologies and data, MedTech companies must prioritize health equity in the implementation of digital healthcare technologies so that everyone can benefit from the latest scientific advances.

In conclusion, the medtech industry has remained resilient amidst the challenging macroeconomic environment. We expect 2023 to be a pivotal year for the industry, as the accelerated acceptance of virtual care and demographic trends, such as an aging population, increasing chronic illnesses and healthcare worker shortages, sustain demand for medtech-enabled solutions. At the same time, the rapidly changing legal and regulatory landscape will continue to be a key issue for medtech innovators moving forward. Adopting a global, forward-thinking regulatory compliance strategy can help MedTech companies stay competitive and ultimately, achieve better outcomes for patients.

Telemedicine is supposed to make consumers’ lives easier, right? One of us had the opposite experience when managing a sick kid this week. My 14-year-old has been sick with a bad respiratory illness for over a week. We saw her pediatrician in-person, testing negative for COVID (multiple times), flu, and strep. Over the week, her symptoms worsened, and rather than haul her back to the doctor, we decided to give our health plan’s telemedicine service a try. To the plan’s credit, the video visit was easy to schedule, and we were connected to a doctor within minutes. He agreed that symptoms and timeline warranted an antibiotic, and said he was sending the prescription to our pharmacy as we wrapped up the call.

Here’s where the challenges began. We went to our usual CVS a few hours later, and they had no record of the prescription. (Note to telemedicine users: write down the name of your provider. The pharmacy asked to search for the script by the doctor’s name, which I didn’t remember—and holding up the line of a dozen other customers to fumble with the app seemed like the wrong call.)

We left and contacted the telemedicine service to see if the prescription had been transmitted, and after a half hour on hold, were finally transferred to pharmacy support. It turns out that the telemedicine service transmits their prescriptions via “e-fax”, so it was difficult to confirm if the pharmacy had received it. Not to be confused with e-prescribing, e-fax is literally an emailed image of a prescription, with none of the safeguards and communication capabilities of true electronic prescribing.

The helpful service representative kindly offered to call the pharmacy and placed us on hold—only to get a message that the pharmacy was closed for lunch and not accepting calls! Several hours later, which included being on hold for 75 minutes (!!!) with our CVS, my daughter finally got her medication.

Despite the slick app and teleconferencing system, the operations behind the virtual visit still relied on the very analog processes of phone trees and faxes—which created a level of irritation that rivaled trying to land Taylor Swift tickets for the same kid. It was a stark reminder of how far healthcare has to go to deliver a truly digital, consumer-centered experience.