Walmart is closing Walmart Health and Walmart Health Virtual Care, saying the business model was not profitable nor sustainable.

The Walmart Health centers opened in 2019.

“Through our experience managing Walmart Health centers and Walmart Health Virtual Care, we determined there is not a sustainable business model for us to continue,” the company said by statement. “The decision to close all 51 health centers across five states and shut down the virtual care offering was not easy.”

WHY THIS MATTERS

Walmart said the challenging reimbursement environment and escalating operating costs created a lack of profitability.

It does not yet have a specific date for when each center will close, but would share that information “as soon as decisions are made.”

Its priority, Walmart said, was “ensuring the people and communities who are impacted are treated with the utmost respect, compassion and support throughout the transition. Today and in the coming days, we are focused on continuity of care for patients and providing impacted associates with respect and assistance as we begin the closing process of the healthcare centers.”

The clinics will continue to serve patients while they are open.

“Through their respective employers, these providers will be paid for 90 days, after which eligible providers will receive transition payments,” Walmart said.

All associates are eligible to transfer to any other Walmart or Sam’s Club location. They will be paid for 90 days, unless they transfer to another location during that time or leave the company, Walmart said. After 90 days, if they do not transfer or leave, eligible associates will receive severance benefits.

“We understand this change affects lives – the patients who receive care, the associates and providers who deliver care and the communities who supported us along the way,” Walmart said.

THE LARGER TREND

Moving forward, Walmart said it would take what it has learned to provide health and wellness services across the country through its nearly 4,600 pharmacies and more than 3,000 vision centers. Both have been in operation for 40 years.

“Over the past few years, the importance of pharmacies has continued to grow, and we have expanded the clinical capabilities of the services we provide,” Walmart said. “We continue to offer immunizations and have grown to provide testing and treatment services, access to specialty pharmacy medication and care, as well as other essential services such as medication therapy management and a variety of health screenings. With more than 4,000 of our stores in medical provider shortage areas, our pharmacies are often the front door of healthcare.”

Walmart said it plans to launch more services such as the Walmart Healthcare Research Institute and health programs to join its fresh food and over-the-counter offerings.

Among the country’s largest grocers, Walmart plans this year to introduce a line of premium food called Bettergoods to compete against Trader Joe’s and Whole Foods, according to The Wall Street Journal.

However, share prices last week fell for Walmart and Kroger after Amazon unveiled a low-cost grocery delivery program, according to Seeking Alpha. Amazon is expanding its fresh-food business through a delivery subscription benefit in the United States for its Prime members and customers using an EBT (electronic benefits transfer) card. It outlined the $9.99 monthly plan last Tuesday, according to the report. Share prices for Walmart were down 1.55% as of this morning.

On Wednesday, e-commerce giant Amazon announced that its 167M US-based Prime members can now access One Medical primary care services for $9 per month, or $99 per year, which amounts to a 50 percent annual discount on One Medical membership. (Additional Prime family members can join for $6/month or $66/year.)

One Medical, which Amazon purchased for $3.9B last year, provides its 800K members with 24/7 virtual care as well as app-based provider communication and access to expedited in-person care, though clinic visits are either billed through insurance or incur additional charges. Amazon also recently started offering virtual care services through its Amazon Clinic platform, at cash prices ranging from $30 to $95 per visit.

The Gist:After teasing this type of bundle with a Prime Day sale earlier this year, Amazon has made the long-expected move to integrate One Medical into its suite of Prime add-ons, using a similar pricing model as its $5-per-month RxPass for generic prescription medications.

At such a low price, Amazon risks flooding One Medical’s patient population with demand it may struggle to meet. But if Amazon can scale One Medical, while maintaining its quality and convenience, it may be able to make the provider organization profitable.

Known for its willingness to take risks and absorb financial losses, Amazon is continuing to build a healthcare ecosystem focused on hybrid primary care and pharmacy services that delivers a strong consumer value proposition based on convenience and low cost.

Five years ago, I started the Fixing Healthcare podcast with the aim of spotlighting the boldest possible solutions—ones that could completely transform our nation’s broken medical system.

But since then, rather than improving, U.S. healthcare has fallen further behind its global peers, notching far more failures than wins.

In that time, the rate of chronic disease has climbed while life expectancy has fallen, dramatically. Nearly half of American adults now struggle to afford healthcare. In addition, a growing mental-health crisis grips our country. Maternal mortality is on the rise. And healthcare disparities are expanding along racial and socioeconomic lines.

Reflecting on why few if any of these recommendations have been implemented, I don’t believe the problem has been a lack of desire to change or the quality of ideas. Rather, the biggest obstacle has been the immense size and scope of the changes proposed.

To overcome the inertia, our nation will need to narrow its ambitions and begin with a few incremental steps that address key failures. Here are three actionable and inexpensive steps that elected officials and healthcare leaders can quickly take to improve our nation’s health:

1. Shore Up Primary Care

Compared to the United States, the world’s most-effective and highest-performing healthcare systems deliver better quality of care at significantly lower costs.

One important difference between us and them: primary care.

In most high-income nations, primary care makes up roughly half of the physician workforce. In the United States, it accounts for less than 30% (with a projected shortage of 48,000 primary care physicians over the next decade).

Primary care—better than any other specialty—simultaneously increases life expectancy while lowering overall medical expenses by (a) screening for and preventing diseases and (b) helping patients with chronic illness avoid the deadliest and most-expensive complications (heart attack, stroke, cancer).

But considering that it takes at least three years after medical school to train a primary care physician, to make a dent in the shortage over the next five years the U.S. government must act immediately:

The first action is to expand resident education for primary care. Congress, which authorizes the funding, would allocate $200 million annually to create 1,000 additional primary-care residency positions each year. The cost would be less than 0.2% of federal spending on healthcare.

The second action requires no additional spending. Instead, the Centers for Medicare & Medicaid Services, which covers the cost of care for roughly half of all American adults, would shift dollars to narrow the $108,000 pay gap between primary care doctors and specialists. This will help attract the best medical students to the specialty.

Together, these actions will bolster primary care and improve the health of millions.

2. Use Technology To Expand Access, Lower Costs

A decade after the passage of the Affordable Care Act, 30 million Americans are without health insurance while tens of millions more are underinsured, limiting access to necessary medical care.

Furthermore, healthcare is expected to become even less affordable for most Americans. Without urgent action, national medical expenditures are projected to rise from $4.3 trillion to $7.2 trillion over the next eight years, and the Medicare trust fund will become insolvent.

With costs soaring, payers (businesses and government) will resist any proposal that expands coverage and, most likely, will look to restrict health benefits as premiums rise.

Almost every industry that has had to overcome similar financial headwinds did so with technology. Healthcare can take a page from this playbook by expanding the use of telemedicine and generative AI.

At the peak of the Covid-19 pandemic, telehealth visits accounted for 69% of all physician appointments as the government waived restrictions on usage. And, contrary to widespread fears at the time, patients and doctors rated the quality, convenience and safety of these virtual visits as excellent. However, with the end of Covid-19, many states are now restricting telemedicine, particularly when clinicians practice in a different state than the patient.

To expand telemedicine use—both for physical and mental health issues—state legislators and regulators will need to loosen restrictions on virtual care. This will increase access for patients and diminish the cost of medical care.

It doesn’t make sense that doctors can provide treatment to people who drive across state lines, but they can’t offer the same care virtually when the individual is at home.

Similarly, physicians who faced a shortage of hospital beds during the pandemic began to treat patients in their homes. As with telemedicine, the excellent quality and convenience of care drew praise from clinicians and patients alike.

Building on that success, doctors could combine wearable devices and generative AI tools like ChatGPT to monitor patients 24/7. Doing so would allow physicians to relocate care—safely and more affordably—from hospitals to people’s homes.

Translating this technology-driven opportunity into standard medical practice will require federal agencies like the FDA, NIH and CDC to encourage pilot projects and facilitate innovative, inexpensive applications of generative AI, rather than restricting their use.

3. Reduce Disparities In Medical Care

American healthcare is a system of haves and have-nots, where your income and race heavily determine the quality of care you receive.

Black patients, in particular, experience poorer outcomes from chronic disease and greater difficulty accessing state-of-the-art treatments. In childbirth, black mothers in the U.S. die at twice the rate of white women, even when data are corrected for insurance and financial status.

Generative AI applications like ChatGPT can help, provided that hospitals and clinicians embrace it for the purpose of providing more inclusive, equitable care.

Previous AI tools were narrow and designed by researchers to mirror how doctors practiced. As a result, when clinicians provided inferior care to Black patients, AI outputs proved equally biased. Now that we understand the problem of implicit human bias, future generations of ChatGPT can help overcome it.

The first step will be for hospitals leaders to connect electronic health record systems to generative AI apps. Then, they will need to prompt the technology to notify clinicians when they provide insufficient care to patients from different racial or socioeconomic backgrounds. Bringing implicit bias to consciousness would save the lives of more Black women and children during delivery and could go a long way toward reversing our nation’s embarrassing maternal mortality rate (along with improving the country’s health overall).

The Next Five Years

Two things are inevitable over the next five years. Both will challenge the practice of medicine like never before and each has the potential to transform American healthcare.

First, generative AI will provide patients with more options and greater control. Faced with the difficulty of finding an available doctor, patients will turn to chatbots for their physical and psychological problems.

Already, AI has been shown to be more accurate in diagnosing medical problems and even more empathetic than clinicians in responding to patient messages. The latest versions of generative AI are not ready to fulfill the most complex clinical roles, but they will be in five years when they are 30-times more powerful and capable.

Second, the retail giants (Amazon, CVS, Walmart) will play an ever-bigger role in care delivery. Each of these retailers has acquired primary care, pharmacy, IT and insurance capability and all appear focused on Medicare Advantage, the capitated option for people over the age of 65. Five years from now, they will be ready to provide the businesses that pay for the medical coverage of over 150 million Americans the same type of prepaid, value-based healthcare that currently isn’t available in nearly all parts of the country.

American healthcare can stop the current slide over the next five years if change begins now. I urge medical leaders and elected officials to lead the process by joining forces and implementing these highly effective, inexpensive approaches to rebuilding primary care, lowering medical costs, improving access and making healthcare more equitable.

In a matter of months, ChatGPT has radically altered our nation’s views on artificial intelligence—uprooting old assumptions about AI’s limitations and kicking the door wide open for exciting new possibilities.

One aspect of our lives sure to be touched by this rapid acceleration in technology is U.S. healthcare. But the extent to which tech will improve our nation’s health depends on whether regulators embrace the future or cling stubbornly to the past.

Why our minds live in the past

In the 1760s, Scottish inventor James Watt revolutionized the steam engine, marking an extraordinary leap in engineering. But Watt knew that if he wanted to sell his innovation, he needed to convince potential buyers of its unprecedented power. With a stroke of marketing genius, he began telling people that his steam engine could replace 10 cart-pulling horses. People at time immediately understood that a machine with 10 “horsepower” must be a worthy investment. Watt’s sales took off. And his long-since-antiquated meaurement of power remains with us today.

Even now, people struggle to grasp the breakthrough potential of revolutionary innovations. When faced with a new and powerful technology, people feel more comfortable with what they know. Rather than embracing an entirely different mindset, they remain stuck in the past, making it difficult to harness the full potential of future opportunities.

Too often, that’s exactly how U.S. government agencies go about regulating advances in healthcare. In medicine, the consequences of applying 20th-century assumptions to 21st-century innovations prove fatal.

Here are three ways regulators do damage by failing to keep up with the times:

1. Devaluing ‘virtual visits’

Established in 1973 to combat drug abuse, the Drug Enforcement Administration (DEA) now faces an opioid epidemic that claims more than 100,000 lives a year.

One solution to this deadly problem, according to public health advocates, combines modern information technology with an effective form of addiction treatment.

Thanks to the Covid-19 Public Health Emergency (PHE) declaration, telehealth use skyrocketed during the pandemic. Out of necessity, regulators relaxed previous telemedicine restrictions, allowing more patients to access medical services remotely while enabling doctors to prescribe controlled substances, including buprenorphine, via video visits.

For people battling drug addiction, buprenorphine is a “Goldilocks” medication with just enough efficacy to prevent withdrawal yet not enough to result in severe respiratory depression, overdose or death. Research from the National Institutes of Health (NIH) found that buprenorphine improves retention in drug-treatment programs. It has helped thousands of people reclaim their lives.

But because this opiate produces slight euphoria, drug officials worry it could be abused and that telemedicine prescribing will make it easier for bad actors to push buprenorphine onto the black market. Now with the PHE declaration set to expire, the DEA has laid out plans to limit telehealth prescribing of buprenorphine.

The proposed regulations would let doctors prescribe a 30-day course of the drug via telehealth, but would mandate an in-person visit with a doctor for any renewals. The agency believes this will “prevent the online overprescribing of controlled medications that can cause harm.”

The DEA’s assumption that an in-person visit is safer and less corruptible than a virtual visit is outdated and contradicted by clinical research. A recent NIH study, for example, found that overdose deaths involving buprenorphine did not proportionally increase during the pandemic. Likewise, a Harvard study found that telemedicine is as effective as in-person care for opioid use disorder.

Of course, regulators need to monitor the prescribing frequency of controlled substances and conduct audits to weed out fraud. Furthermore, they should demand that prescribing physicians receive proper training and document their patient-education efforts concerning medical risks.

But these requirements should apply to all clinicians, regardless of whether the patient is physically present. After all, abuses can happen as easily and readily in person as online.

The DEA needs to move its mindset into the 21st century because our nation’s outdated approach to addiction treatment isn’t working. More than 100,000 deaths a year prove it.

2. Restricting an unrestrainable new technology

Technologists predict that generative AI, like ChatGPT, will transform American life, drastically altering our economy and workforce. I’m confident it also will transform medicine, giving patients greater (a) access to medical information and (b) control over their own health.

So far, the rate of progress in generative AI has been staggering. Just months ago, the original version of ChatGPT passed the U.S. medical licensing exam, but barely. Weeks ago, Google’s Med-PaLM 2 achieved an impressive 85% on the same exam, placing it in the realm of expert doctors.

With great technological capability comes great fear, especially from U.S. regulators. At the Health Datapalooza conference in February, Food and Drug Administration (FDA) Commissioner Robert M. Califf emphasized his concern when he pointed out that ChatGPT and similar technologies can either aid or exacerbate the challenge of helping patients make informed health decisions.

Worried comments also came from Federal Trade Commission, thanks in part to a letter signed by billionaires like Elon Musk and Steve Wozniak. They posited that the new technology “poses profound risks to society and humanity.” In response, FTC chair Lina Khan pledged to pay close attention to the growing AI industry.

Attempts to regulate generative AI will almost certainly happen and likely soon. But agencies will struggle to accomplish it.

To date, U.S. regulators have evaluated hundreds of AI applications as medical devices or “digital therapeutics.” In 2022, for example, Apple received premarket clearance from the FDA for a new smartwatch feature that lets users know if their heart rhythm shows signs of atrial fibrillation (AFib). For each AI product that undergoes FDA scrutiny, the agency tests the embedded algorithms for effectiveness and safety, similar to a medication.

ChatGPT is different. It’s not a medical device or digital therapy programmed to address a specific or measurable medical problem. And it doesn’t contain a simple algorithm that regulators can evaluate for efficacy and safety. The reality is that any GPT-4 user today can type in a query and receive detailed medical advice in seconds. ChatGPT is a broad facilitator of information, not a narrowly focused, clinical tool. Therefore, it defies the types of analysis regulators traditionally apply.

In that way, ChatGPT is similar to the telephone. Regulators can evaluate the safety of smartphones, measuring how much electromagnetic radiation it gives off or whether the device, itself, poses a fire hazard. But they can’t regulate the safety of how people use it. Friends can and often do give each other terrible advice by phone.

Therefore, aside from blocking ChatGPT outright, there’s no way to stop individuals from asking it for a diagnosis, medication recommendation or help with deciding on alternative medical treatments. And while the technology has been temporarily banned in Italy, that’s unlikely to happen in the United States.

If we want to ensure the safety of ChatGPT, improve health and save lives, government agencies should focus on educating Americans on this technology rather than trying to restrict its usage.

3. Preventing doctors from helping more people

Doctors can apply for a medical license in any state, but the process is time-consuming and laborious. As a result, most physicians are licensed only where they live. That deprives patients in the other 49 states access to their medical expertise.

The reason for this approach dates back 240 years. When the Bill of Rights passed in 1791, the practice of medicine varied greatly by geography. So, states were granted the right to license physicians through their state boards.

In 1910, the Flexner report highlighted widespread failures of medical education and recommended a standard curriculum for all doctors. This process of standardization culminated in 1992 when all U.S. physicians were required to take and pass a set of national medical exams. And yet, 30 years later, fully trained and board-certified doctors still have to apply for a medical license in every state where they wish to practice medicine. Without a second license, a doctor in Chicago can’t provide care to a patient across a state border in Indiana, even if separated by mere miles.

The PHE declaration did allow doctors to provide virtual care to patients in other states. However, with that policy expiring in May, physicians will again face overly restrictive regulations held over from centuries past.

Given the advances in medicine, the availability of technology and growing shortage of skilled clinicians, these regulations are illogical and problematic. Heart attacks, strokes and cancer know no geographic boundaries. With air travel, people can contract medical illnesses far from home. Regulators could safely implement a common national licensing process—assuming states would recognize it and grant a medical license to any doctor without a history of professional impropriety.

But that’s unlikely to happen. The reason is financial. Licensing fees support state medical boards. And state-based restrictions limit competition from out of state, allowing local providers to drive up prices.

To address healthcare’s quality, access and affordability challenges, we need to achieve economies of scale. That would be best done by allowing all doctors in the U.S. to join one care-delivery pool, rather than retaining 50 separate ones.

Doing so would allow for a national mental-health service, giving people in underserved areas access to trained therapists and helping reduce the 46,000 suicides that take place in America each year.

Regulators need to catch up

Medicine is a complex profession in which errors kill people. That’s why we need healthcare regulations. Doctors and nurses need to be well trained, so that life-threatening medications can’t fall into the hands of people who will misuse them.

But when outdated thinking leads to deaths from drug overdoses, prevents patients from improving their own health and limits access to the nation’s best medical expertise, regulators need to recognize the harm they’re doing.

Healthcare is changing as technology races ahead. Regulators need to catch up.

There is no shortage of challenges to confront in healthcare today, from workforce shortages and burnout to innovation and health equity (and so much more). We’re committed to giving industry leaders a platform for sharing best practices and exchanging ideas that can improve care, operations and patient outcomes.

Check out this podcast interview with Ketul J. Patel, CEO at Virginia Mason Franciscan Health and division president, Pacific Northwest at CommonSpirit Health, for his insights on where healthcare is headed in the future.

In this episode, we are joined by Ketul J. Patel, Division President, Pacific Northwest; Chief Executive Officer, CommonSpirit Health; Virginia Mason Franciscan Health, to discuss his background & what led him to executive healthcare leadership, challenges surrounding workforce shortages, the importance of having a strong workplace culture, and more.

The executives featured in this article are all speaking at the Becker’s Healthcare 13th Annual Meeting April 3-6, 2023, at the Hyatt Regency in Chicago.

Question: What will hospitals and health systems look like in 10 years? What will be different and what will be the same?

Michael A. Slubowski. President and CEO of Trinity Health (Livonia, Mich.): In 10 years, inpatient hospitals will be more focused on emergency care, intensive/complex care following surgery or complex medical conditions, and short-stay/observation units. Only the most complex surgical cases and complex medical cases will be inpatient status. Most elective surgery and diagnostic services will be done in freestanding surgery, procedural and imaging centers. Many patients with chronic medical conditions will be managed at home using digital monitoring. More seniors will be cared for in homes and/or in PACE programs versus skilled nursing facilities.

Mark A. Schuster, MD, PhD. Founding Dean and Chief Executive Officer of Kaiser Permanente Bernard J. Tyson School of Medicine (Pasadena, Calif.): The future of hospitals might not actually unfold in hospitals. I expect that more and more of what we now do in hospitals will move into the home. The technology that makes this transition possible is already out there: Remote monitoring of vital signs and lab tests, remote visual exams, and videoconferencing with patients. And all of this technology will improve even more over the next 10 years — turning at-home care from a dream into a reality.

Imagine no longer being kept awake all night by beeps and alarms coming from other patients’ rooms or kept away from family by limited visiting hours. The benefits are especially welcome for people who live in rural places and other areas with limited medical facilities. Who knows? Maybe robotics will make some in-home surgeries not so far off!

Of course, not all patients have a safe or stable home environment where they could receive care, so hospitals aren’t going away anytime soon. I’m not suggesting that most current patients could be cared for remotely in a decade — but I do think we’re moving in that direction. So those of us who work in education will need to train medical, nursing, and other students for a healthcare future that looks quite different from the healthcare present and takes place in settings we couldn’t imagine 10 years ago.

Shireen Ahmad. System Director, Operations and Finance of CommonSpirit Health (Chicago): The biggest change I anticipate is a continuation in the decentralization of health services delivery that has typically been provided by hospitals. This will result in a reduction of hospitals with fewer services performed in acute settings and with more services provided in non-acute ones.

With recent reimbursement changes, CMS is helping to set the tone of where care is delivered. Hospitals are beginning to rationalize services, including who and where care is delivered. For example, pharmacies often carry clinics that provide vaccinations, but in France, one can go to a pharmacy for care and sterilization of minor wounds while only paying for bandages, medication and other supplies used in the visit. I would not be surprised if, in 10 years, one could get an MRI at their local Walmart or schedule routine screenings and tests at the grocery store with faster, more accurate results as they check out their produce.

If the pandemic has taught us anything, there will always be a need for acute care and our society will always need hospitals to provide care to sick patients. This is not something I would anticipate changing. However, the need to provide most care in a hospital will change with the result leading to fewer hospitals in total. Far from being a bleak outlook, however, I believe that healthier, sustainable health systems will prevail if they are able to provide a greater spectrum of care in broader settings focussing on quality and convenience.

Gerard Brogan. Senior Vice President and Chief Revenue Officer of Northwell Health (New Hyde Park, N.Y.): Operationally, hospitals and health systems will be more designed around the patient experience rather than the patient accommodating to the hospital design and operations. Specifically, more geared toward patient choice, shopping for services, and price competition for out-of-pocket expenses. In order to bring costs down, rational control of utilization will be more important than ever. Hopefully, we will be able to shrink the administrative costs of delivering care. Structurally, more care will continue to be done ambulatory, with hospitals having a greater proportion of beds having critical care capability and single rooms for infection control, putting pressure on the cost per square foot to operate. Sustainable funding strategies for safety net hospitals will be needed.

Mike Gentry. Executive Vice President and COO of Sentara Healthcare (Norfolk, Va.): During the next 10 years, more rural hospitals will become critical assessment facilities. The legislation will be passed to facilitate this transition. Relationships with larger sponsoring health systems will support easy transitions to higher acuity services as required. In urban areas, fewer hospitals with greater acuity and market share will often match the 50 percent plus market share of health plans. The ambulatory transition will have moved beyond only surgical procedures into outpatient but expanded historical medical inpatient status in ED/observation hubs.

The consumer/patient experience will be vastly improved. Investments in mobile digital applications will provide greatly enhanced communication, transparency of clinical status, timelines, the likelihood of expected outcomes and cost. Patients will proactively select from a menu of treatment options provided by predictive AI. The largest 10 health systems will represent 25 percent of the total U.S. acute care market share, largely due to consumer-centric strategic investments that have outpaced their competitors. Health systems will have vastly larger pharma operations/footprints.

Ketul J. Patel. CEO of Virginia Mason Franciscan Health (Seattle) and Division President, Pacific Northwest of CommonSpirit Health (Chicago): This is a transformative time in the healthcare industry, as hospitals and healthcare systems are evolving and innovating to meet the growing and changing needs of the communities we serve. The pandemic accelerated the digital transformation of healthcare. We have seen the proliferation of new technologies — telemedicine, artificial intelligence, robotics, and precision medicine — becoming an integral part of everyday clinical care. Healthcare consumers have become empowered through technology, with greater control and access to care than ever before.

Against this backdrop, in the next decade we’ll see healthcare consumerism influencing how health systems transform their hospitals. We will continue incorporating new technologies to improve healthcare delivery, offering more convenient ways to access high-quality care, and lowering the overall cost of care.

SMART hospitals, including at Virginia Mason Franciscan Health, are utilizing AI to harness real-time data and analysis to revolutionize patient and provider experiences and improve the quality of care. VMFH was the first health system in the Pacific Northwest to introduce a virtual hospital nearly a decade ago, which provides virtual services in the hospital across the continuum of care to improve quality and safety through remote patient monitoring and care delivery.

As hospitals become more high-tech, more nimble, and more efficient over the next 10 years, there will be less emphasis on brick-and-mortar buildings as we continue to move care away from the hospital toward more convenient settings for the patient. We recently launched VMFH Home Recovery Care, which brings all the essential elements of hospital-level care into the comfort and convenience of patients’ homes, offering a safe and effective alternative to the traditional inpatient stay.

Health systems and hospitals must simplify the care experience while reducing the overall cost of care. VMFH is building Washington state’s first hybrid emergency room/urgent care center, which eliminates the guesswork for patients unsure of where to go for care. By offering emergent and urgent care in a single location, patients get the appropriate level of care, at the right price, in one convenient location.

As healthcare delivery becomes more sophisticated in this digital age, we must not lose sight of why we do this work: our patients. There is no device or innovation that can truly replace the care and human intelligence provided by our nurses, APPs and physicians. So, while hospitals and health systems might look and feel different in 2033, our mission will remain the same: to provide exceptional, compassionate care to all — especially the most vulnerable.

David Sylvan. President of University Hospitals Ventures (Cleveland): American healthcare is facing an imperative. It’s clear that incremental improvements alone won’t manifest the structural outcomes that are largely overdue. The good news is that the healthcare industry itself has already initiated the disruption and self-disintermediation. I would hope that in the next 10 years, our offerings in healthcare truly reflect our efforts to adopt consumerism and patient choice, alleviate equity barriers and harness efficiencies while reducing time waste.

We know that some of this will come about through technology design, build and adoption, especially in the areas of generative artificial intelligence. But we also know that some of this will require a process overhaul, with learnings gleaned from other industries that have already solved adjacent challenges. What won’t change in 10 years will be the empathy and quality of care that the nation’s clinicians provide to patients and their caregivers daily.

Joseph Webb. CEO of Nashville (Tenn.) General Hospital: The United States healthcare industry operates within a culture that embraces capitalism as an economic system. The practice of capitalism facilitates a framework that is supported by the theory of consumerism. This theory posits that the more goods and services are purchased and consumed, the stronger an economy will be. With that in mind, healthcare is clearly a driver in the U.S. economy, and therefore, major capital and technology are continuously infused into healthcare systems. Healthcare is currently approaching 20 percent of the U.S. gross domestic product and will continue to escalate over the next 10 years.

Also, in 10 years, there will be major shifts in ownership structures, e.g., mergers, acquisitions, and consolidations. Many healthcare organizations/hospitals will be unable to sustain operations due to shrinking profit margins. This will lead to a higher likelihood of increasing closures among rural hospitals due to a lack of adequate reimbursement and rising costs associated with salaries for nurses, respiratory therapists, etc., as well as purchasing pharmaceuticals.

Aging baby boomers with chronic medical conditions will continue to dominate healthcare demand as a cohort group. To mitigate the rising costs of care, healthcare systems and providers will begin to rely even more heavily on artificial intelligence and smart devices. Population health initiatives will become more prevalent as the cost to support fragmented care becomes cost-prohibitive and payers such as CMS will continue to lead the way toward value-based care.

Because of structural and social conditions that tend to drive social determinants of health, which are fundamental causes of health disparities, achieving health equity will continue to be a major challenge in the U.S. Health equity is an elusive goal that can only be achieved when there is a more equitable distribution of SDOH.

Gary Baker. CEO, Hospital Division of HonorHealth (Scottsdale, Ariz.): In 10 years, I would expect hospitals in health systems to become more specialized for higher acuity service lines. Providing similar acute services at multiple locations will become difficult to maintain. Recruiting and retaining specialty clinical talent and adopting new technologies will require some redistribution of services to improve clinical quality and efficiency. Your local hospital may not provide a service and will be a navigator to the specialty facilities. Many services will be provided in ambulatory settings as technology and reimbursement allow/require. Investment in ambulatory services will continue for the next 10 years.

Michael Connelly. CEO Emeritus of Bon Secours Mercy Health (Cincinnati): Our society will be forced to embrace economic limits on healthcare services. The exploding elderly population, in combination with a shrinking workforce to fund Medicare/Medicaid and Social Security, will force our health system to ration care in new ways. These realities will increase the role of primary care as the needed coordinator of health services for patients. Diminishing fragmented healthcare and redundant care will become an increasing focus for health policy.

David Rahija. President of Skokie Hospital, NorthShore University HealthSystem (Evanston, Ill.): Health systems will evolve from being just a collection of hospitals, providers, and services to providing and coordinating care across a longitudinal care continuum. Health systems that are indispensable health partners to patients and communities by providing excellent outcomes through seamless, coordinated, and personalized care across a disease episode and a life span will thrive. Providers that only provide transactional care without a holistic, longitudinal relationship will either close or be consolidated. Care tailored to the personalized needs of patients and communities using team care models, technology, genomics, and analytics will be key to executing a personalized, seamless, and coordinated model of care.

Alexa Kimball, MD. President and CEO of Harvard Medical Faculty Physicians at Beth Israel Deaconess Medical Center (Boston): Ten years from now, hospitals will largely look the same — at least from the outside. Brick-and-mortar buildings aren’t going away anytime soon. What will differ is how care is delivered beyond the traditional four walls. Expect to see a more patient-centered and responsive system organized around what individuals need — when and where they need it.

Telehealth and remote patient monitoring will enable greater accessibility for patients in underserved areas and those who cannot get to a doctor’s office. Technology will not only enable doctors to deliver more personalized treatment plans but will also dramatically reshape physician workflows and processes. These digital tools will streamline administrative tasks, integrate voice commands, and provide more conducive work environments. I also envision greater access to data for both providers and patients. New self-service solutions for care management, scheduling, pricing, shopping for services, etc., will deliver a more proactive patient experience and make it easier to navigate their healthcare journey.

Ronda Lehman, PharmD. President of Mercy Health – Lima (Ohio):

This is a highly challenging question to address as we continue to reevaluate how healthcare is being delivered following several difficult years and knowing that financial challenges still loom. That said, when I am asked what it will look like, I am keenly aware of the fact that it only will look that way if we can envision a better way to improve the health of our communities. So 10 years from now, we need to have easier and more patient-driven access to care.

We will need to stop doing ‘to people’ and start caring ‘with people.’ Artificial intelligence and proliferous information that is readily available to consumers will continue to pave the way to patients being more empowered and educated about their options. So what will differentiate healthcare of the future? Enabling patients to make informed decisions.

Undoubtedly, technology will continue to advance, and along with it, the associated costs of research and development, but healthcare can only truly change if providers fundamentally shift their approach to how we care for patients. It is imperative that we need to transform from being the gatekeepers of valuable resources and services to being partners with patients on their journey. If that is what needs to be different, then what needs to be the same? We need the same highly motivated, highly skilled and perhaps most importantly, highly compassionate caregivers selflessly caring for one another and their communities.

Mike Young. President and CEO of Temple University Health System (Philadelphia): Cell therapy, gene therapy, and immunotherapy will continue to rapidly improve and evolve, replacing many traditional procedures with precise therapies to restore normal human function — either through cell transfer, altering of genetic information, or harnessing the body’s natural immune system to attack a particular disease like cancer, cystic fibrosis, heart disease, or diabetes. As a result, hospitals will decrease in footprint, while the labs dedicated to defining precision medicine will multiply in size to support individual- and disease-specific infusion, drug, and manipulative therapies.

Hospitals will continue to shepherd the patient journey through these therapies and also will continue to handle the most complex cases requiring high-tech medical and surgical procedures. Medical education will likely evolve in parallel, focusing more on genetic causation and treatment of disease, as well as proficiency with increasingly sophisticated AI diagnostic technologies to provide adaptive care on a patient-by-patient basis.

Tom Siemers. Chief Executive Officer of Wilbarger General Hospital (Vernon, Texas): My predictions include the national healthcare landscape will be dominated by a dozen or so large systems. ‘Consolidation’ will be the word that describes the healthcare industry over the next 10 years. Regional systems will merge into large, national systems. Independent and rural hospitals will become increasingly rare. They simply won’t be able to make the capital investments necessary to replace outdated facilities and equipment while vying with other organizations for scarce, licensed personnel.

Jim Heilsberg. CFO of Tri-State Memorial Hospital & Medical Campus (Clarkston, Wash.): Tri-State Hospital continues to expand services for outpatient services while maintaining traditionally needed inpatient services. In 10 years, there will be expanded outpatient services that include leveraged technology that will allow the patient to be cared for in a yet-to-be-seen care model, including traditional hospital settings and increasing home care setting solutions.

Jennifer Olson. COO of Children’s Minnesota (St. Paul, Minn.): I believe we will see more and better access to healthcare over the next 10 years. Advances in diagnostics, monitoring, and artificial intelligence will allow patients to access services at more convenient times and locations, including much more frequently at home, thereby extending health systems’ reach well beyond their walls.

What I don’t think will ever change is the heart our healthcare professionals bring with them to work every day. I see it here at Children’s Minnesota and across our industry: the unwavering commitment our caregivers have to help people live healthier lives.

If I had one wish for the future, it would be that we become better equipped to address the social determinants of health: all of the factors outside the walls of our hospitals and clinics that affect our patients’ well-being. Part of that means relaxing regulations to allow better communication and sharing of information among healthcare providers and public and private entities, so we can take a more holistic approach to improve health and decrease disparities. It also will require a fundamental shift in how health and healthcare are paid for.

Stonish Pierce. COO of Holy Cross Health, Trinity Health Florida: Over the next decade, many health systems will pivot from being ‘hospital’ systems to true ‘health’ systems. Based largely on responding to The Joint Commission’s New Requirements to Reduce Health Care Disparities, many health systems will place greater emphasis on reducing health disparities, enhanced attention to providing culturally competent care, addressing social determinants of health (including, but not limited to food, housing and transportation) and health equity. I’m proud to work for Trinity Health, a system that has already directed attention toward addressing health disparities, cultural competency and health equity.

Many systems will pivot from offering the full continuum of services at each hospital and instead focus on the core services for their respective communities, which enables long-term financial sustainability. At the same time, we will witness the proliferation of partnerships as adept health systems realize that they cannot fulfill every community’s needs alone. Depending upon the specialty and region of the country, we may see some transitioning away from the RVU physician compensation model to base salaries and value-based compensation to ensure health systems can serve their communities in the long term.

Driven largely by continued workforce supply shortages, we will also see innovation achieve its full potential. This will include, but not be limited to, virtual care models, robots to address functions currently performed by humans, and increased adoption of artificial intelligence and remote monitoring. Healthcare overall will achieve parity in technological adoption and innovation that we take for granted and have grown accustomed to in industries such as banking and the consumer service industries.

For what will remain the same, we can anticipate that government reimbursement will still not cover the cost of providing care, although systems will transition to offering care models and services that enable the best long-term financial sustainability. We will continue to see payers and retail pharmacies continue to evolve as consumer-friendly providers. We will continue to see systems make investments in ambulatory care and the most critically ill patients will remain in our hospitals.

Jamie Davis. Executive Director, Revenue Cycle Management of Banner Health (Phoenix): I think that we will see a continued shift in places of service to lower-cost delivery sources and unfavorable payer mix movement to Medicare Advantage and health exchange plans, degrading the value of gross revenue. The increased focus on cost containment, value-based care, inflation, and pricing transparency will hopefully push payers and providers to move to a more symbiotic relationship versus the adversarial one today. Additionally, we may see disruption in the technology space as the venture capital and private equity purchase boom that happened from 2019 to 2021 will mature and those entities come up for sale. If we want to continue to provide the best quality health outcomes to our patients and maintain profitability, we cannot look the same in 10 years as we do today.

James Lynn. System Vice President, Facilities and Support Services of Marshfield Clinic Health System (Wis.): There will be some aspects that will be different. For instance, there will be more players in the market and they will begin capturing a higher percentage of primary care patients. Walmart, Walgreens, CVS, Amazon, Google and others will begin to make inroads into primary care by utilizing VR and AI platforms. More and more procedures will be the same day. Fewer hospital stays will be needed for recovery as procedures become less invasive and faster. There will be increasing pressure on the federal government to make healthcare a right for all legal residents and it will be decoupled from employment status. On the other hand, what will stay the same is even though hospital stays will become shorter for some, we will also be experiencing an ever-aging population, so the same number of inpatient beds will likely be needed.

On Monday, San Francisco-based Carbon Health—a virtual-first primary and urgent care company with 125 clinics across 13 states—announced a partnership with CVS Health, which includes a $100M investment, as well as plans to pilot its operating model in select CVS stores. The announcement came just days after Carbon reported its second round of layoffs in the past year, as it scales back on less profitable business segments to focus on expanding its primary care model.

The Gist: It’s been over a year since CVS CEO Karen Lynch said the company was moving with “speed and urgency” to construct a physician-staffed primary care model. Last fall it purchased in-home health evaluation company Signify Health for $8B, after rumors that it had been close to acquiring One Medical.

Between its convenient retail footprint, insurance arm, and Signify’s risk-assessment tools, a nationwide primary care physician network is the last puzzle piece CVS needs to field a comprehensive and formidable primary care strategy.

While it’s currently rumored to be evaluating a $10B acquisition of Oak Street Health, this partnership with Carbon Health is a better bet to deliver value quickly, as CVS should be able to more easily integrate and leverage Carbon’s retail health expertise across its growing care delivery platform.

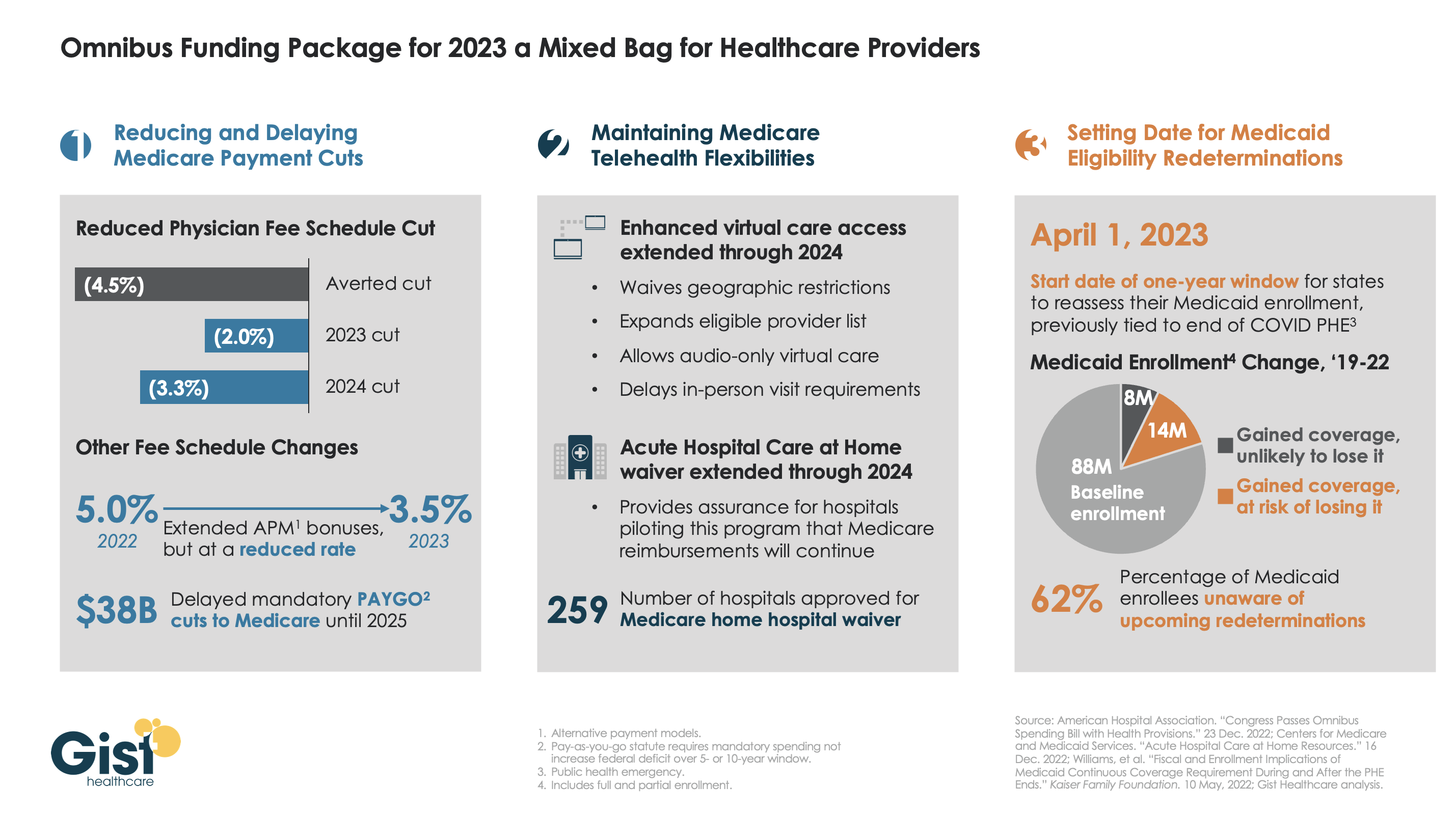

While healthcare wasn’t a top priority for lawmakers hammering out the Omnibus bill aimed at keeping the government open through next September, the graphic above outlines the bill’s three greatest areas of impact for providers.

The package reduces the planned 4.5 percent 2023 physician fee schedule cut to two percent, while also extending value-based care bonuses in alternative payment models (albeit at 3.5 percent, instead of five percent). It also delays the $38B Medicare spending cut required by the PAYGO sequester, pushing that cut out two years.

On the telehealth front, the bill extends Medicare’s pandemic-era virtual care flexibilities through 2024, including the “hospital at home” waiver. It also sets April 1, 2023 as the start date of a one-year window for states to reassess Medicaid enrollment,decoupling the start of eligibility redeterminations from the end of the federal COVID public health emergency. Medicaid enrollment grew by 25 percent over the course of the pandemic, but around two-thirds of new enrollees may lose eligibility after redeterminations.

Overall, the legislation is a mixed bag for providers.The uninsured population is expected to grow, at least in the short term. Physician groups had hopes for a complete reprieve from Medicare pay cuts, and the fact that they didn’t get it may signalgrowing Congressional hesitancy to intervene with the Medicare physician fee schedule in the future. But the telehealth extensions may encourage other wider adoption of reimbursement by private insurers, bolstering providers’ long-term virtual care investments.

Late last week, President Biden signed a $1.7T spending package to fund the federal government through next September. While around half the funds are dedicated to defense, some important healthcare items made it into the bill, including a reduction in planned Medicare physician pay cuts and a two-year postponement of the $38B Medicare spending cut required by the PAYGO sequester.

The law also decoupled several measures from the end of the federal COVID public health emergency (PHE), setting April 1st as the start date for states to begin Medicaid eligibility redeterminations, and extending Medicare’s telehealth flexibilities and the Acute Hospital Care at Home waiver program through the end of 2024. For more details on these changes, see our graphic below.

The Gist: Medical groups were hoping for more of a reprieve from the Medicare physician fee schedule cuts, but Congress proved unwilling to address concerns over rising practice costs. We’re relieved that Medicare’s new telehealth and hospital at home policies will continue beyond the PHE, given the early interest we’ve seen from the provider community in embracing these new, more consumer-friendly care models.

Once the new Congress finally gets underway, we’re expecting this to be an uneventful two years for federal healthcare legislation, with the emphasis of health policy likely to shift toward states, federal agency rulemaking, and judicial activity.

We expect 2023 to be a pivotal year for the industry, as the accelerated acceptance of virtual care and demographic trends, such as an aging population, increasing chronic illnesses and healthcare worker shortages, sustain demand for medtech-enabled solutions.

The combination of rapid developments in novel healthcare technology and heightened demand for integrated tech-enabled care has continued to fuel innovation in the medtech industry. At the same time, medtech innovators – whether in digital health, wearables and AI-driven offerings in healthcare, or diagnostics, telemedicine and health IT solutions – continue to face a patchwork of laws, rules and norms across the world. Life sciences and healthcare innovators and regulators are also looking to medtech to increase access to care and health equity. Here are ten global medtech themes we are tracking in the coming year:

Focus on digital tuck-in acquisitions in medtech M&A

Despite continued uncertainty in the overall financial market, medtech M&A activity continued at a steady pace in 2022. This year witnessed a rise in tuck-in acquisitions of smaller companies that can be easily integrated into buyers’ existing infrastructure and product offerings, as opposed to significantly sized takeovers of businesses that aren’t squarely aligned with buyers’ existing businesses lines. Medtech acquirers have been particularly focused on developing their digital capabilities to innovate and reach customers in new ways. As digitization continues to transform the industry, we expect acquirers to continue to prioritize the value of digital and data assets as they evaluate potential targets.

Continued interest by private equity and other financial sponsors

Private equity firms, healthcare-focused funds and other financial sponsors have continued to display a strong appetite for investing in Medtech companies, with top targets in subsectors such as diagnostics and healthcare IT solutions. Later-stage medtech companies in particular are gaining a larger share of venture capital funding, as later-stage investments allow financial sponsors to focus on businesses with higher yields, as well as less time to market and capital reimbursement. Demographic trends, including an aging population and the increasing prevalence of chronic diseases, coupled with healthcare technology advancements have created robust demand for medtech-enabled solutions. Additionally, medtech offerings have broad applications that can extend beyond stakeholders in a specific therapy area, product category or care setting, offering the ability to satisfy unmet needs with large patient bases.

Strategic medtech collaborations as the new norm

Strategic medtech collaborations and partnerships have become the new norm in our increasingly connected digital healthcare ecosystem. In response to heightened consumer demand for tech-enabled care, pharmaceutical and medtech companies are collaborating to use digital technologies to engage with consumers, unlocking a vast range of treatments such as personalized medicine. Additionally, as the market rapidly evolves towards data-driven healthcare, we expect medtech companies to continue to work collaboratively to address existing barriers to data sharing and promote interoperability of healthcare data.

Continued scrutiny by antitrust and competition authorities

As expected, global antitrust and competition authorities continued to focus on the tech, life sciences and medtech sectors in 2022. The US, UK and EU authorities have stepped up efforts to investigate and challenge conduct by large pharma and technology companies pursuing mergers and acquisitions. We expect these authorities to assess similar concerns in the digital health context in an effort to account for the value of combined datasets and the interoperability of various offerings that could be derived from digital health mergers and acquisitions. Furthermore, geopolitical tensions have resulted in new and expanded foreign investment regimes to improve the resilience of domestic healthcare systems. Notably this year, the UK government implemented the National Security and Investment Act that allows it to restrict transactions that may threaten national security, including in the AI and data infrastructure sectors. Sensitive data continues to be a recurring theme for foreign investment review for Committee on Foreign Investment in the US and that of the EU as well.

Growing importance of data privacy and security

Increasing regulatory attention to sensitive health data and the escalating rise of ransomware attacks has made data privacy and security more important than ever for medtech innovators. The Federal Trade Commission has issued several statements about its willingness to “fully” enforce the law against the illegal use and sharing of highly sensitive data. Additionally, several state privacy laws coming into effect in 2023 create new categories of sensitive personal data, including health data, and impose novel obligations on innovators to obtain data-related consents. As ransomware continues to pose security-related threats, the US Department of Health and Human Services renewed calls for all covered entities and business associates to prioritize cybersecurity. New standards, such as cybersecurity label rating programs for connected devices, aim to address security risks. In the EU, medtech providers will need to consider how the launch of the European Health Data Space and newly proposed data regulation, such as the Data Act and AI Act, could impact their data use and sharing practices.

More active engagement with FDA/EMA/MHRA

We expect companies active in the medtech sector, particularly those that make use of AI and other advanced technologies, to continue their conversations with the U.S. Food and Drug Administration (“FDA”), the European Medicines Agency (“EMA”), the Medicines and Healthcare Products Regulatory Agency (“MHRA”) and other regulators as such companies grow their medtech business lines and establish their associated regulatory compliance infrastructure. Given the unique regulatory issues arising from the implementation of digital health technologies, we expect the FDA, EMA and MHRA to provide additional guidance on AI/ML-based software-as-a-medical device and the remote management of clinical trials. 2022 saw stakeholders in the life sciences and medtech industries collaborate with regulatory authorities to push forward the acceptance of digital endpoints that rely on sensor-generated data collected outside of a clinical setting. As the industry shifts to decentralized clinical trials, we expect both innovators and regulators to work together to evaluate the associated clinical, privacy and safety risks in the development and use of such digital endpoints.

Increasing medtech localization in the Asia Pacific region

2022 saw multinational companies (“MNCs”), including American pharma/device makers make an active effort to expand their medtech business lines in the Asia Pacific region. At the same time, government authorities in the region have been increasingly focused on incentivizing local innovation, approving government grants and prohibiting the importation of non-approved medical equipment. In light of MNCs’ market share of the medical device market in the Asia Pacific region, especially in China, we expect the emergence of the domestic medtech industry to prompt discussions among MNCs, local innovators and government authorities over the long-term development of the global market for medical technology.

Long-term adoption of telehealth and remote patient monitoring technologies

The Covid-19 pandemic saw the rise of telehealth and remote patient monitoring technologies as key modes of healthcare delivery. The telehealth industry remains focused on enabling remote consultations and long-term patient management for patients with chronic conditions. Looking forward, we expect to see increased innovation in non-invasive technologies that can provide early diagnostics and ongoing disease management in a low-friction manner. At the same time, we anticipate telehealth companies to face increasing scrutiny from regulatory authorities around the world for fraud and abuse by patients and providers. Consumer and patient data privacy and security in connection with telehealth and remote patient monitoring continue to remain top of mind for regulators as well.

Women’s health and privacy concerns for medtech

We expect to see increased consumer health tech adoption for reproductive care, especially in light of the U.S. Supreme Court’s decision to overturn Roe v. Wade. Following the Dobbs decision, a number of states introduced or passed legislation that prohibits or restricts access to reproductive health services beyond abortion. In response, women’s health-focused companies are expanding their virtual fertility and pregnancy, telemedicine and other services to patients. At the same time, such companies need to assess the legal risks stemming from the collection and storage of their customers’ personal health information, which could then be used as evidence to prosecute customers for obtaining illegal reproductive health services. We expect companies active in this space to take steps to navigate the patchwork of data privacy and security laws across jurisdictions while establishing clear digital health governance mechanisms to safeguard their customers’ data privacy and security.

Addressing inequities in the implementation of digital healthcare technologies

Medtech innovators and regulators have been increasingly focused on addressing inequities in the healthcare system and the data used to train AI and ML-based digital healthcare technologies. In 2022, a number of medtech companies collaborated to provide technologies that result in improved patient outcomes across all populations, as well as boost participation of diverse populations in clinical trials. In parallel, we are seeing increased interest from regulators to reduce bias in digital health technologies and the accompanying datasets, as evidenced by the EU’s proposed AI Act and the UK’s health data strategy. In the US, which currently lacks comprehensive government regulation of AI in healthcare, there have been increasing calls for institutional commitments in the area of algorithmovigilance. Because of the inaccurate conclusions that may result from biased technologies and data, MedTech companies must prioritize health equity in the implementation of digital healthcare technologies so that everyone can benefit from the latest scientific advances.

In conclusion, the medtech industry has remained resilient amidst the challenging macroeconomic environment. We expect 2023 to be a pivotal year for the industry, as the accelerated acceptance of virtual care and demographic trends, such as an aging population, increasing chronic illnesses and healthcare worker shortages, sustain demand for medtech-enabled solutions. At the same time, the rapidly changing legal and regulatory landscape will continue to be a key issue for medtech innovators moving forward. Adopting a global, forward-thinking regulatory compliance strategy can help MedTech companies stay competitive and ultimately, achieve better outcomes for patients.