Tonight at midnight, thousands of federal workers face the possibility their jobs will be eliminated as part of the Department of Government Efficiency (DOGE) federal cost reduction initiative under Elon Musk’ leadership. Already, thousands who serve in federal healthcare roles at the NIH, CDC and USAID have been terminated and personnel in agencies including CMS, HHS and the FDA are likely to follow.

The federal healthcare workforce is large exceeding more than 2.5 million who serve agencies and programs as providers, clerks, administrators, scientists, analysts, counselors and more. More than half work on an hourly basis, and 95% work outside DC in field offices and clinics. For the vast majority, their work goes unnoticed except when “government waste” efforts like DOGE spring up. In those times, they’re relegated to “expendables” status and their numbers are cut.

The same can be said for the larger private U.S. healthcare workforce. Per the U.S. Bureau of Labor Statistics, industry employment was 21.4 million, or 12.8% of total U.S. employment in 2023 and is expected to reach 24 million by 2030. It’s the largest private employer in the U.S. economy and includes many roles considered “expendable” in their organizations.

Facts about the U.S. healthcare workforce:

- More than 70% of the healthcare workforce work in provider settings including 7.4 million who work in hospitals.

- More than half work in non-clinical roles.

- Home health aides is the highest growth cohort and hospitals employ the biggest number (7.4 million).

- 29% of physicians and 15% of nurses are foreign born, almost three-fourths of the workforce are women, two-thirds are non-Hispanic whites, and the majority are older than 50.

- Its licensed professions enjoy public trust ranking among Gallup’s highest rated though all have declined:

| % 2023 | ‘19-‘23 | ’23 Rank | % 2023 | ‘19-‘23 | ’23 Rank | ||

| Nurses | 78 | -7 | 1 | Pharmacists | 55 | -9 | 6 |

| Dentists | 59 | -2 | Psychiatrists | 36 | -7 | 9 | |

| Medical doctors | 56 | -9 | 5 | Chiropractors | 33 | -8 | 10 |

The Perfect storm

The healthcare workforce is unsteady: while stress and burnout are associated with doctors and nurses primarily, they cut across every workgroup and setting.

Eight fairly recent issues complicate efforts to achieve healthcare workforce stability:

Increased costs of living:

Consumers are worried about their costs of living: it hits home hardest among young, low-income households including dual eligible seniors for whom gas, food and transportation are increasing faster than their incomes, and rents exceed 50% of their income. The healthcare workforce takes a direct hit: one in five we employ cannot pay their own medical bills.

Slowdown in consolidation:

The Federal Trade Commission’s new pre-merger notification mandate that went in effect today essentially requires greater pre-merger/acquisition disclosures and a likely slowdown in deals. Organizations anticipating deals might default to layoffs to strengthen margins while the regulatory consolidation dust settles. Expendables will take a hit.

Uncertainty about Medicaid cuts:

In the House’ budget reconciliation plan, Medicaid cuts of up to $880 billion/10 years are contemplated. A cut of that magnitude will accelerate closure of more than 400 rural hospitals already at risk and throw the entire Medicaid program into chaos for the 79 million it serves—among them 3 million low-hourly wage earners in the healthcare workforce and at least 2 million in-home unpaid caregivers who can’t afford paid assistance. The impact of Medicaid cuts on the healthcare workforce is potentially catastrophic for their jobs and their health.

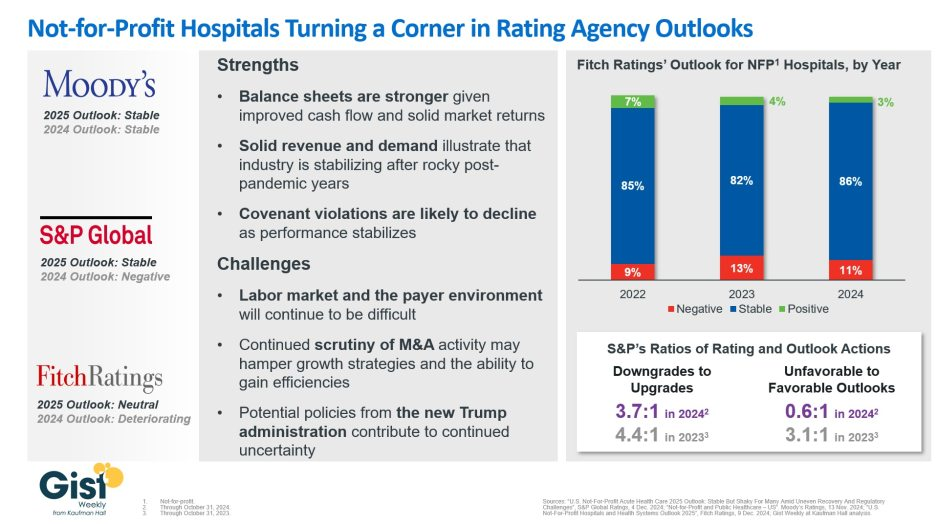

Heightened attention to tax exemptions for not-for-profit hospitals:

Large employers sent this recommendation to Congressional leaders last week as spending cuts were being considered: “Nonprofit hospitals, despite their tax-exempt status, frequently prioritize profits over patient care. Many have deeply questionable arrangements with for-profit entities such as management companies or collections agencies, while others have “joint ventures” with Wall Street hedge funds or other for-profit provider or staffing companies. Nonprofit hospitals often shift the burden of their costs onto taxpayers and the communities they serve by overcharging for health care services, or abusing programs intended to provide access to low-cost care and prescription drugs for low-income patients. By eliminating nonprofit hospital status, resources could be more evenly distributed across the healthcare system, ensuring that hospitals are held accountable for their charitable care both to their communities and the tax laws that govern them.” Pressures on NFP hospitals to lower costs and operate more transparently are gaining momentum in state legislatures and non-healthcare corporate boardrooms. Belt tightening is likely. Layoffs are underway.

Heightened attention to executive compensation in healthcare organizations:

Executive compensation, especially packages for CEO’s, is a growing focus of shareholder dissent, Congressional investigation, media coverage and employee disgruntlement. Compensation committee deliberations and fair market comparison data will be more publicly accessible to communities, rank and file employees, media, regulators and payers intensifying disparities between “labor” and “management”.

Increased tension between providers and insurers:

Health insurers are now recovering from 2 years of higher utilization and lower profits; hospitals did the same in 2022 and 2023. Neither is out of the woods and both are migrating to tribal warfare based on ownership (not-for-profit vs. investor owned vs. government owned), scale and ambition. Bigger, better-capitalized organizations in their ranks are faring better while many struggle. The workforce is caught in the crossfire.

Increased pressure on private equity-backed employers to exit:

The private equity market for healthcare services has experienced a slow recovery after 2 disappointing years peppered by follow-on offerings in down rounds. Exit strategies are front and center to PE sponsors; workforce stability and retention is a means to an end to consummate the deal—that’s it.

The AI Yellow Brick Road:

Last and potentially the most disruptive is the role artificial intelligence will play in redefining healthcare tasks and reorganizing the system’s processes based on large-language models and massive investments in technology. Job insecurity across the entire healthcare workforce is more dependent on geeks and less on licensed pro’s going forward.

These eight combine to make life miserable most days in health human resource management. DOGE will complicate matters more. It’s a concern in every sector of healthcare, and particularly serious in hospitals, medical practices, long-term and home care settings.

‘Modernizing the healthcare workforce’ sounds appealing, but for now, navigating these issues requires full attention. They require Board understanding and creative problem-solving by managers. And they merit a dignified and respectful approach to interactions with workers displaced by these circumstances: they’re not expendables, they’re individuals like you and me.