The drugstore retailer faces debt maturities, while the upending of some strategies introduces new uncertainties, analysts said.

S&P Global Ratings analysts have downgraded Walgreens Boot Alliance by two notches, to ‘BB’ from ‘BBB-’, which puts the drugstore company into speculative-grade territory.

Analysts Diya Iyer and Hanna Zhang cited guidance for the year “notably below” their expectations, and said “material strategic changes, limited cash flow generation, and large maturities in coming years are key risks to the business.”

The company is struggling in its retail business as well as its pharmacy operations, they said in a Friday client note. In the U.S., margins are taking a hit on the pharmacy side from reimbursement pressure and on the retail side from declining sales volume and higher shrink. They expect Walgreens’ S&P Global Ratings-adjusted EBITDA margin to decline more than 100 basis points this fiscal year, dipping below 5%, from 6% last year, though the company’s cost cuts will counter that somewhat.

Walgreens’ debt and its need to refinance much of it represent another “key risk,” they said. This November, Walgreens faces $1.4 billion in maturities, mostly U.S. bonds. Another $2.8 billion comes due in fiscal 2026 and $1.8 billion in fiscal 2027. The analysts called Walgreens’ move to consolidate cash “prudent” in case refinancing isn’t possible.

“We will be monitoring how Walgreens’ new management addresses this large debt load closely amid its persistently weak performance and higher interest rates,” Iyer and Zhang said.

Beyond those financial realities, though, are strategic weaknesses. Ex-Cigna executive Tim Wentworth took over as CEO last fall and this year has overseen a strategic review that has entailed more layoffs and store closures.

Walgreens has also upended some of its plans to expand its medical care operations, divesting of or shrinking many of its original investments and plans. Last month, for example, the company announced it would reduce its stake in value-based medical chain VillageMD, saying it will no longer be the company’s majority owner, after closing dozens of the clinics last year. The company first poured $1 billion into VillageMD in 2020 and more than doubled its stake for another $5.2 billion the following year, but the banner’s waning value helped drive a $6 billion loss in Q2.

Despite such moves, Iyer and Zhang said they continue to see the VillageMD banner as “a significant drag on profitability due to the rising cost of labor, pressures from reimbursement, and lower volumes.”

Walgreens’ acquisition streak led the S&P analysts to believe that it would divest of its Boots U.K. business, which could have helped pay down $8 billion to $10 billion in debt. But the company called off the idea about two years ago.

“We believe these frequent and large changes to the company’s strategic plans diminish management’s credibility to execute on a sustainable and cohesive operating model for Walgreens in both the near and long term,” Iyer and Zhang said.

Gains that Walgreens has managed to eke from its medical operations haven’t managed to offset declines on the retail said, they also said, adding that they are closely watching what it does next with its massive footprint. The company last year announced that it would close 150 stores in the U.S. and 300 in the U.K. and just last month said it was reviewing 25% of its current footprint, with plans to shutter a “significant portion” of its roughly 8,700 stores.

“Our ratings continue to reflect Walgreens’ large scale and its efforts to address its credit metric profile. With almost $140 billion in sales in fiscal 2023 and a diverse array of global businesses, Walgreens remains prominent in the drugstore space,” they said. “However, we think its scale is providing less protection to profitability at least partly due to inconsistent strategic direction.”

Health systems put an emphasis on strategy over scale in hospital transactions announced in the second quarter of 2024, according to a July 9 report from Kaufman Hall.

“As pressure intensifies to transform the current healthcare system to bring greater value to patients and communities, the impetus for M&A activity will rely less on seeking capital in traditional ways and instead move toward new, strategic partnership models,” Anu Singh, managing director and mergers & acquisitions practice leader with Kaufman Hall, said in a July 9 news release. “Many of these M&A transactions enable hospitals to sustain and enhance access to care, launch new services, or strengthen and stabilize systems, which allows for future growth.”

Five things to know:

1. There were 11 hospital transactions announced in the second quarter of 2024, below historic Q2 averages. There were 20 hospital transactions announced in the second quarter of 2023.

2. Despite fewer overall deals, total transacted revenue in the quarter remained near historic highs at $10.8 billion.

3. Three of the 11 announced transactions involved religiously affiliated acquirers. Two involved academic or university-affiliated acquirers. The other six involved not-for-profit health system acquirers.

4. For the first time since Kaufman Hall tracked this data, there were no for-profit health system acquirers in the quarter. Kaufman Hall said in the report that this continues a trend of low for-profit buy-side activity. In the first quarter of 2024, just one of the 20 announced transactions involved a for-profit acquirer.

5. The emphasis on strategy over scale “characterized the most significant transactions of Q2 2024 and built upon trends we have been commenting on in recent past reports,” Kaufman Hall said.

Those trends are:

Pursuit of intellectual capital and new or complementary capabilities through a strategic partnership, often involving an innovative partnership model.

Focus of large regional or national systems on market reorganization and strategic realignment of their system portfolios.

The development of networks involving academic health systems and community hospital partners to sustain and enhance access to care.

A health system CEO recently reached out to me with a specific complaint that’s become a hot-button issue for an increasing number of systems:

“Medicare Advantage (MA) is no longer a good payer for us. When you factor in all the pre-auths and denials, we’re now getting four points less yield from our MA patients than from our traditional Medicare patients.

But our market is swinging hard toward MA, and I know the program’s not going anywhere…so how can we rethink our MA business model to make it more profitable?

After more than a decade of rapid growth, MA plans are now running into headwinds that are reducing their margins and creating an even more contentious negotiating environment with providers. However, these heightened competitive pressures could also be seen as an opportunity for provider organizations.

Rather than treating all of their MA payers as a monolith, a health system or other larger provider organization should be reassessing its MA book of business with the goal of identifying priority MA payers with which to pursue deeper, mutually beneficial partnerships.

The first step here is usually for a system to undergo a holistic tiering or ranking exercise for all of their MA payers according to factors like market share, contribution margin, value-based incentives, overall relationship dynamic, and projected market growth.

This exercise will identify not only which MA payers may not be high-priority, long-term partners, but also which MA payers are suitable for developing deeper relationships with (e.g., simplifying administrative burden, better rewards for value-based care, creating a joint insurance product).

If your system is facing challenges with MA and is interested in rethinking its MA portfolio strategy, please don’t hesitate to reach out.

Hospitals’ business models are being upended by fundamental changes within the health care system, including one that presents a pretty existential challenge: People have far more options to get their care elsewhere these days.

Why it matters:

Health systems’ responses to major demographic, social and technological change have been controversial among policymakers and economists concerned about the impact on costs and competition.

Communities depend on having at least some emergency services available, making the survival of hospitals’ core services crucial.

But without adaptation — which is already underway in some cases — hospitals may be facing deep red balance sheets in the not-too-distant future, leading to facility closures and shutteredservices.

The big picture:

Many hospitals have recovered from the sector’s post-pandemic financial slump, which was driven primarily by staffing costs and inflation. But systemic, long-term trends will continue to challenge their traditional business model.

Many of the services that are shifting toward outpatient settings — like oncology, diagnostics and orthopedic care — are the ones that typically make hospitals the most money and effectively subsidize less profitable departments.

When hospitals lose these higher-margin services, “you’re starving the system that needs profits to provide services that we all might need, but particularly uninsured or underinsured people might need,” said UCLA professor Jill Horwitz.

And hospitals have long claimed that much higher commercial insurance rates make up for what they say are inadequate government rates.

But as the population ages and moves out of employer-sponsored health plans, fewer people will have commercial insurance, forcing hospitals to either cut costs or find new sources of revenue.

By the numbers:

Consulting firms are projecting a bleak decade for health systems.

Oliver Wyman recently predicted that under the status quo, hospitals will need to reduce their expenses by 15-20% by 2030 “to stay viable.”

Boston Consulting Group last year projected that health systems’ annual financial shortfall will total more than $200 billion by 2027, and their operating margins will have dropped by 10 percentage points.

To break even in 2027, a “typical” health system would need payment rate increases of between 5-8% annually — twice the rate growth over the last decade, according to BCG. If the load is borne solely by private insurers, hospitals will need a 10-16% year-over-year increase.

Between the lines:

This is the lens through which to view health systems’ spree of mergers and acquisitions, which have increasingly drawn criticism from policymakers, regulators and economists as being anticompetitive.

For better orworse, when hospitals have a larger market share, they are in a better position to negotiate and bring in more patients, and they can dilute some of the financial pain of poorer-performing facilities.

And when they acquire physician practices or other outpatient clinics, they’re still getting paid for delivering care even when patients aren’t receiving it in a traditional hospital setting.

“I think the hospitals have sort of said … ‘We can keep doing things the same way and we can just merge and get higher markups,'” said Yale economist Zack Cooper. “That push to consolidate is saying, ‘Let’s not move forward, let’s dig in.'”

Yes, but:

A big bonus of outpatient care is that it’s supposed to be cheaper. But when hospitals charge more for care than an independent physician’s office would have, or they tack on facility fees, costs don’t go down.

“They’ve protected their portfolio, and that’s added to the cost of health care,” said Johns Hopkins professor Gerard Anderson.

The other side:

Hospitals are typically on the losing end of negotiations with insurers right now, thanks to how large insurers have become, and are “in an extremely difficult competitive position,” said Ken Kaufman, co-founder of consulting agency Kaufman Hall.

Criticizing their mergers and acquisitions as anticompetitive is a “complete misunderstanding of the situation,” he said, and moving toward a new care model will take “an incredible amount of resources.”

Reality check:

Hospitals account for 30% of the country’s massive health spending tab, and they’ll have to be at the forefront of any real efforts to contain costs.

They’re also anchors in their communities and are powerful lobbyists, which helps explain why Congress has struggled to modestly reduce what Medicare pays hospital outpatient departments.

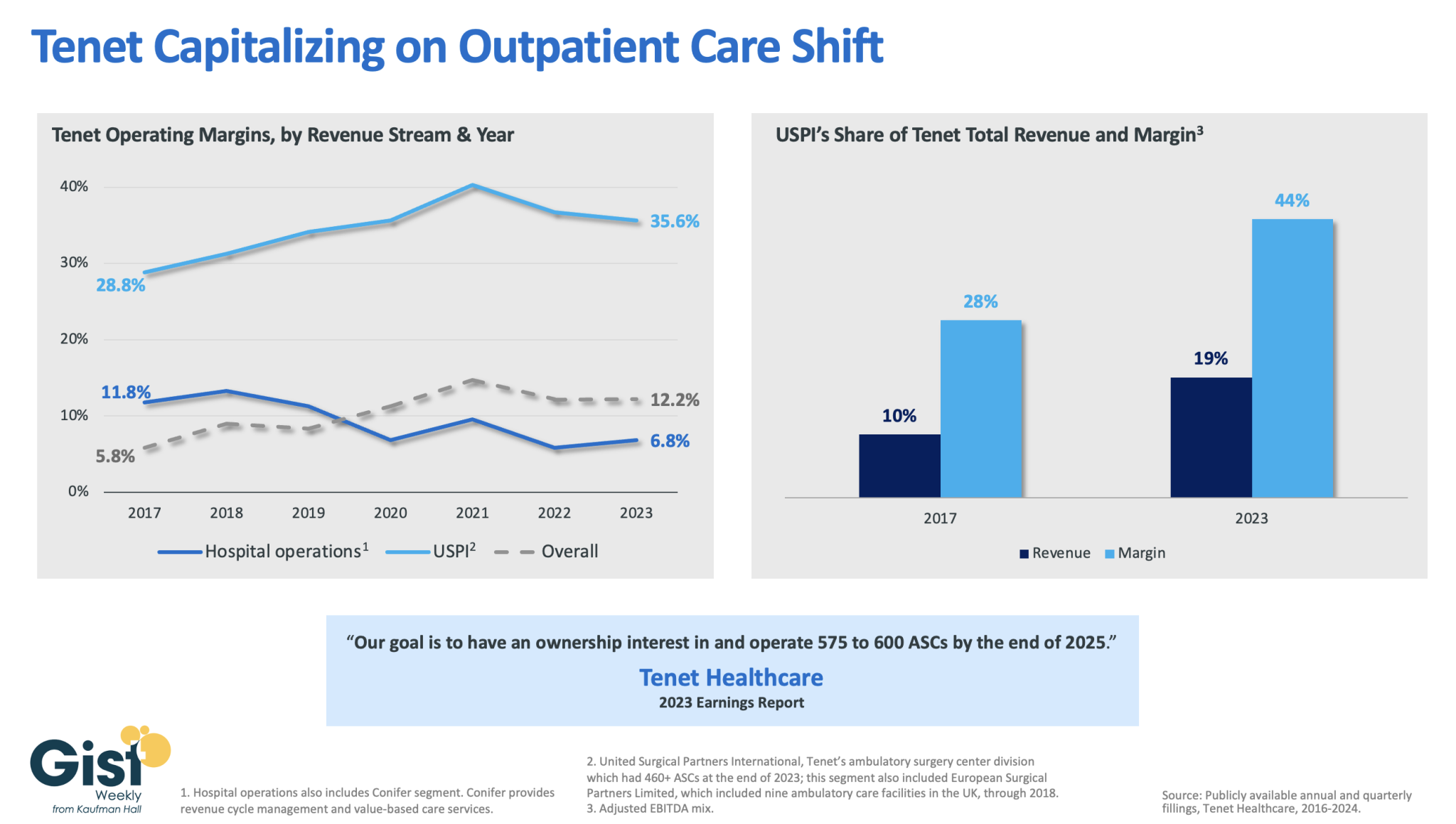

In this week’s graphic, we dive into recently released data on Tenet Healthcare’s 2023 financial performance. While the for-profit healthcare services company’s annual margin on hospital operations has declined since 2017, its overall profitability has more than doubled, thanks to strong performances from its ambulatory surgery center (ASC) chain,

United Surgical Partners International (USPI), which has consistently posted margins above 30 percent. Despite bringing in less than one fifth of Tenet’s total revenue, USPI is now responsible for almost half of Tenet’s overall margin.

Tenet has pursued this growth aggressively since buying USPI in 2015, swelling its ASC footprint from 249 locations in 2015 to more than 460 in 2023, with plans to increase that number to nearly 600 by the end of next year.

Tenet appears to be doubling down on its strategy of pursuing high-margin services over high-revenue services, especially as outpatient volumes are expected to far surpass growth in hospital-based care over the next decade.

Today is the federal income Tax Day. In 43 states, it’s in addition to their own income tax requirements. Last year, the federal government took in $4.6 trillion and spent $6.2 trillion including $1.9 trillion for its health programs. Overall, 2023 federal revenue decreased 15.5% and spending was down 8.4% from 2022 and the deficit increased to $33.2 trillion. Healthcare spending exceeded social security ($1.351 trillion) and defense spending ($828 billion) and is the federal economy’s biggest expense.

Along with the fragile geopolitical landscape involving relationships with China, Russia and Middle East, federal spending and the economy frame the context for U.S. domestic policies which include its health system. That’s the big picture.

Today also marks the second day of the American Hospital Association annual meeting in DC. The backdrop for this year’s meeting is unusually harsh for its members:

Increased government oversight:

Five committees of Congress and three federal agencies (FTC, DOJ, HHS) are investigating competition and business practices in hospitals, with special attention to the roles of private equity ownership, debt collection policies, price transparency compliance, tax exemptions, workforce diversity, consumer prices and more.

Medicare payment shortfall:

CMS just issued (last week) its IPPS rate adjustment for 2025: a 2.6% bump that falls short of medical inflation and is certain to exacerbate wage pressures in the hospital workforce. Per a Bank of American analysis last week, “it appears healthcare payrolls remain below pre-pandemic trend” with hospitals and nursing homes lagging ambulatory sectors in recovering.”

Persistent negative media coverage:

The financial challenges for Mission (Asheville), Steward (Massachusetts) and others have been attributed to mismanagement and greed by their corporate owners and reports from independent watchdogs (Lown, West Health, Arnold Ventures, Patient Rights Advocate) about hospital tax exemptions, patient safety, community benefits, executive compensation and charity care have amplified unflattering media attention to hospitals.

Physicians discontent:

59% of physicians in the U.S. are employed by hospitals; 18% by private equity-backed investors and the rest are “independent”. All are worried about their income. All think hospitals are wasteful and inefficient. Most think hospital employment is the lesser of evils threatening the future of their profession. And those in private equity-backed settings hope regulators leave them alone so they can survive. As America’s Physician Group CEO Susan Dentzer observed: “we knew we’re always going to need hospitals; but they don’t have to look or operate the way they do now. And they don’t have to be predicated on a revenue model based on people getting more elective surgeries than they actually need. We don’t have to run the system that way; we do run the healthcare system that way currently.”

The Value Agenda in limbo:

Since the Affordable Care Act (2010), the CMS Center for Innovation has sponsored and ultimately disabled all but 6 of its 54+ alternative payment programs. As it turns out, those that have performed best were driven by physician organizations sans hospital control. Last week’s release of “Creating a Sustainable Future for Value-Based Care: A Playbook of Voluntary Best Practices for VBC Payment Arrangements.” By the American Medical Association, the National Association of ACOs (NAACOs) and AHIP, the trade group representing America’s health insurance payers is illustrative. Noticeably not included: the American Hospital Association because value-pursuers think for hospitals it’s all talk.

National insurers hostility:

Large, corporate insurers have intensified reimbursement pressure on hospitals while successfully strengthening their collective grip on the U.S. health insurance sector. 5 insurers control 50% of the U.S. health insurance market: 4 are investor owned. By contrast, the 5 largest hospital systems control 17% of the hospital market: 1 is investor-owned. And bumpy insurer earnings post-pandemic has prompted robust price increases: in 2022 (the last year for complete data and first year post pandemic), medical inflation was 4.0%, hospital prices went up 2.2% but insurer prices increased 5.9%.

Costly capital:

The U.S. economy is in a tricky place: inflation is stuck above 3%, consumer prices are stable and employment is strong. Thus, the Fed is not likely to drop interest rates making hospital debt more costly for hospitals—especially problematic for public, safety net and rural hospitals. The hospital business is capital intense: it needs $$ for technologies, facilities and clinical innovations that treat medical demand. For those dependent on federal funding (i.e. Medicare), it’s unrealistic to think its funding from taxpayers will be adequate. Ditto state and local governments. For those that are credit worthy, capital is accessible from private investors and lenders. For at least half, it’s problematic and for all it’s certain to be more expensive.

Campaign 2024 spotlight:

In Campaign 2024, healthcare affordability is an issue to likely voters. It is noticeably missing among the priorities in the hospital-backed Coalition to Strengthen America’s Healthcare advocacy platform though 8 states have already created “affordability” boards to enact policies to protect consumers from medical debts, surprise hospital bills and more.

Understandably, hospitals argue they’re victims. They depend on AHA, its state associations, and its alliances with FAH, CHA, AEH and other like-minded collaborators to fight against policies that erode their finances i.e. 340B program participation, site-neutral payments and others. They rightfully assert that their 7/24/365 availability is uniquely qualifying for the greater good, but it’s not enough. These battles are fought with energy and resolve, but they do not win the war facing hospitals.

AHA spent more than $30 million last year to influence federal legislation but it’s an uphill battle. 70% of the U.S. population think the health system is flawed and in need of transformative change. Hospitals are its biggest player (30% of total spending), among its most visible and vulnerable to market change.

Some think hospitals can hunker down and weather the storm of these 8 challenges; others think transformative change is needed and many aren’t sure. And all recognize that the future is not a repeat of the past.

For hospitals, including those in DC this week, playing victim is not a strategy. A vision about the future of the health system that’s accessible, affordable and effective and a comprehensive plan inclusive of structural changes and funding is needed. Hospitals should play a leading, but not exclusive, role in this urgently needed effort.

Lacking this, hospitals will be public utilities in a system of health designed and implemented by others.

The Nelson A. Rockefeller Institute of Government is a public policy think tank founded in 1981 that conducts cutting-edge research and analysis to inform lasting solutions to the problems facing New York State and the nation.

Introduction & Definitions

In 2023, I noted10 trends within three broad categories in healthcare worth watching and provided a mid-year update on those trends. They included: the impact of unwinding the Public Health Emergency on insurance coverage, healthcare workforce shortages, price inflation, declining margins at hospitals, private equity in healthcare, consolidations, alternate payment models, attention to health equity, digital telehealth expansion, and the expansion of non-traditional providers in healthcare. These trends continue to be worth watching in 2024.

More significant than any one of these trends is the combined interaction of the trends in the industry overall—what I’ll call a “mega-trend,” which results in a trifurcation of the industry. Currently, there are parts of the healthcare industry struggling to exist. This is due to different factors, including high expenses, staffing challenges, and a lack of access to capital and technology, among other things. I call the types of healthcare entities that fall into this category “Today” entities because they exist now but may or may not exist in the future. In contrast, there is another set of entities in healthcare that have emerged in the last five or so years. They are becoming larger through consolidation and integration, and have greater access to capital and technology. I call these types of healthcare entities the “Tomorrow” entities because their size, resources, and forward-looking strategies are changing the future of healthcare.

In between these two categories, are existing and traditional entities in healthcare that seek sustaining strategies. I call these entities the “Striving Survivors” whose success and ability to persevere is still an open question. Most look like the healthcare entities of Today, but what distinguishes them is their ability to partner, use technology, and diversify what they offer. To understand the mega–trend phenomena of this trifurcation in healthcare and what’s happening within and across each of these three categories, this blog dissects how the trends I highlighted in 2023 are impacting the Today and the Tomorrow entities and discusses how the Striving Survivors are attempting to keep pace as the healthcare industry evolves.

The “Today” Healthcare Entities

As noted in my 2023 blog,price inflation and expense growth—particularly as they relate toworkforce and labor costs—were two trends impacting existing healthcare organizations. Today’s healthcare entities are heavily reliant on people, and, unsurprisingly, increased expenses for personnel, which had a major impact on organizations’ bottom lines for the past few years, as did general inflation and increased supply prices. However, for some providers, revenue and patient volume have returned to levels comparable to pre–pandemic. According to Kaufman Hall, a healthcare consulting firm, by the end of 2023, some hospitals’ margins were beginning to stabilize.

In looking at what may happen in 2024 for providers, however, the return of patient volume and, therefore, more predictable revenue may not be enough to yield positive margins. This is because expenses are predicted to be challenging. Industry experts estimate that healthcare prices will grow 7 percent in the coming year. The estimate reflects increases in pharmaceutical costs, growing provider expenses given the high labor and supply costs noted earlier, and insurer rate increases.

Another challenge to the healthcare entities of Today is the availability of capital to make strategic investments. More of this capital is now being provided by private equity firms, an estimated $750 billion in the last decade. To secure capital in the private market, bond rating agencies typically favor larger providers because they are less risky. This, among other factors, has contributed to growing consolidation in the industry among physician groups, insurers, and hospitals. Not only do these entities need capital for projects like upgrades to existing facilities, but to also make strategic investments. Such investments include acquisitions of other providers or companies that add to the revenue base, or technologies that allow improvements in care delivery.

The Today entities are increasingly challenged with adapting to consumer demands for tech–enabled care options. Consumers want more tech–supported smart applications that allow them to book appointments or get assistance with care more quickly via chatbots. Consumers also want new options for care at home—including hospital–at–home, which provides acute care in a home-based setting, and home–based care. As noted in my November blog on AI in healthcare, access to such technologies is not only creating further separation between healthcare entities, but can also create further inequities among consumers.

The “Tomorrow” Healthcare Entities

With the challenges for the healthcare entities of Today outlined above, it is important to note that those same challenges are not as significant for the healthcare players of Tomorrow. This is because most are substantial in size and have sufficient revenue, technology, and capital resources—often in the form of private equity. And many of them did not start in healthcare. They include, for example, Amazon—which started as an online bookstore and now has annual revenues of over $500 billion, CVS—which started as a retail pharmacy and now has revenues close to $300 billion; Uber—which started as a tech-enabled taxi-like transport application and now has revenues of over $30 billion, and Microsoft—which started as computer company but has expanded into healthcare with annual revenues of over $200 billion.

Some of these companies have entered healthcare by partnering with, or acquiring companies already in the sector such as Amazon’s 2023 acquisition of One Medical, a tech–enabled primary care entity; the 2022 partnership between United Health Group and Change Healthcare, a technology company; and CVS’s official 2023 acquisition of Signify, a home health organization. This was on top of CVS’s earlier (2018) merger with health insurance company Aetna, and its 2022 partnership announcement with Uber with the stated aim of improving access to care and decreasing health inequities in underserved communities across the country. Other entities have increased their footprint in healthcare by launching their products, such as Microsoft’s 2020 launch of Cloud services, specifically for healthcare. Some of these companies are now collaborating, including the 2021 partnership between CVS Health and Microsoft, which was designed to customize care further, enable frontline workers to more easily access and use data, and digitize operations.

In addition to these large nontraditional healthcare entities, the health insurance industry has also experienced large–scale consolidation and diversification that enables them to compete. One of the most notable companies in the world of healthcare integration is the nation’s largest insurer, United Health Group (UHG). UHG continued to outpace provider margins, with 2023 third quarter margins for UHG at levels 14 percent higher year-over-year. The continued growth at UHG was largely due to the increasing number of individuals served and a growing provider base of 90,000 physicians, or 10 percent of all physicians nationwide. This contrasts with one of the largest provider margins (Kaiser) whose 2023 third-quarter margin was only $239 million, an improvement from the $1.5 billion loss they experienced in the third quarter from the previous year. Although no other insurers are as big as UHG, the next biggest including, Aetna, Anthem, Cigna, and Humana all had 2023 third–quarter net incomes ranging from $1 billion to $1.4 billion.

The Striving Survivors

Not all traditional healthcare entities are being left behind; I call these the Striving Survivors. They may currently be considered Today entities, but they are attempting to put in place strategies so they can be Tomorrow entities in the future. Here are three primary strategies that may help these entities survive into the future:

Partnering—The number of independent hospitals as well as the number of independent physician groups has shrunk dramatically in the past decade, and there is increasing pressure for both to consider merging. A report by Kaufman Hall prepared at the request of the American Hospital Association, shows that merging can have advantages such as creating economies of scale, improving leverage to bargain for better payments from increasingly large insurance companies, and allowing better access to capital markets. Other advantages to partnering include diversifying what services can be offered to patients, allowing providers to assume risk for the care of a larger population, or leveraging complementary strengths for strategic investments. Although many of these consolidations used to be regional in nature (providers would merge with neighboring providers), new mergers are occurring across broader geographic areas, as was the case with the merger of west–coast–based Kaiser and Pennsylvania-based Geisinge.

Maximizing Technology—Striving Survivors are also seeking to compete and survive into the future by partnering to maximize technology. Technologies like telehealth, remote monitoring, artificial intelligence, and hospital–at–home, are growing because they are delivering care in ways that are preferable to consumers. As recently noted by Deloitte, “Adopting new technologies and business models—while under sustained financial pressure—might be the biggest challenge health care executives will face in 2024.” The good news for the healthcare players of Today is the use of data and technology in new and creative ways can counteract some of their current financial and care delivery challenges. Technology can make care more convenient for consumers, reduce costs, or provide care in places where it is sometimes inaccessible. Some recent examples of partnerships between technology companies and today’s healthcare entities include women’s health tech startup Tia’s partnership with Common Spirit, one of the largest healthcare systems in the country. Similarly, Strive Health is managing kidney patients for Bon Secours Mercy Health; Carbon Health is providing tech–enabled urgent care for Milwaukee–based Froedtert Health. Even Best Buy, a home electronics store, has begun offering homecare through several partnerships, including, for example, Mass General Brigham.

Revenue Diversification—Revenue diversification has long been a growth strategy in many industries. Up until recently, there hasn’t been the same pressure for such diversification for healthcare entities. That is changing, in part, because many of the healthcare entities of Tomorrow come from non–health–related industries. Diversification can occur using either of the strategies noted above (partnership or maximizing the use of technology). Diversification might also include providing services in areas of healthcare where demand is growing (e.g. urgent care or outpatient instead of legacy inpatient services). It might also include services that are not currently widely used but are likely to become more commonplace in the future, such as precision medicine or hospital–at–home.

Conclusion

In 2024, it will not only be important for healthcare policymakers to monitor single trends such as the continued focus on health equity, the expansion of alternate payment models, or the cost of the healthcare workforce, but it will also be important to understand how trends may be interacting with each other to create larger market trends. Such is the case for the emergence of non-traditional players in healthcare, the influx of private equity, digital expansion, and major consolidations— which when combined —are resulting in a mega trend of trifurcation of the industry into Today, Tomorrow, and Striving entities in healthcare that are seeking to survive into the future. For healthcare policymakers, all these trends along with their interaction will be worth monitoring and understanding so that effective policies can be developed that result in a healthcare system that supports innovation, protects patients, reduces inequities, and results in better health outcomes at lower cost.

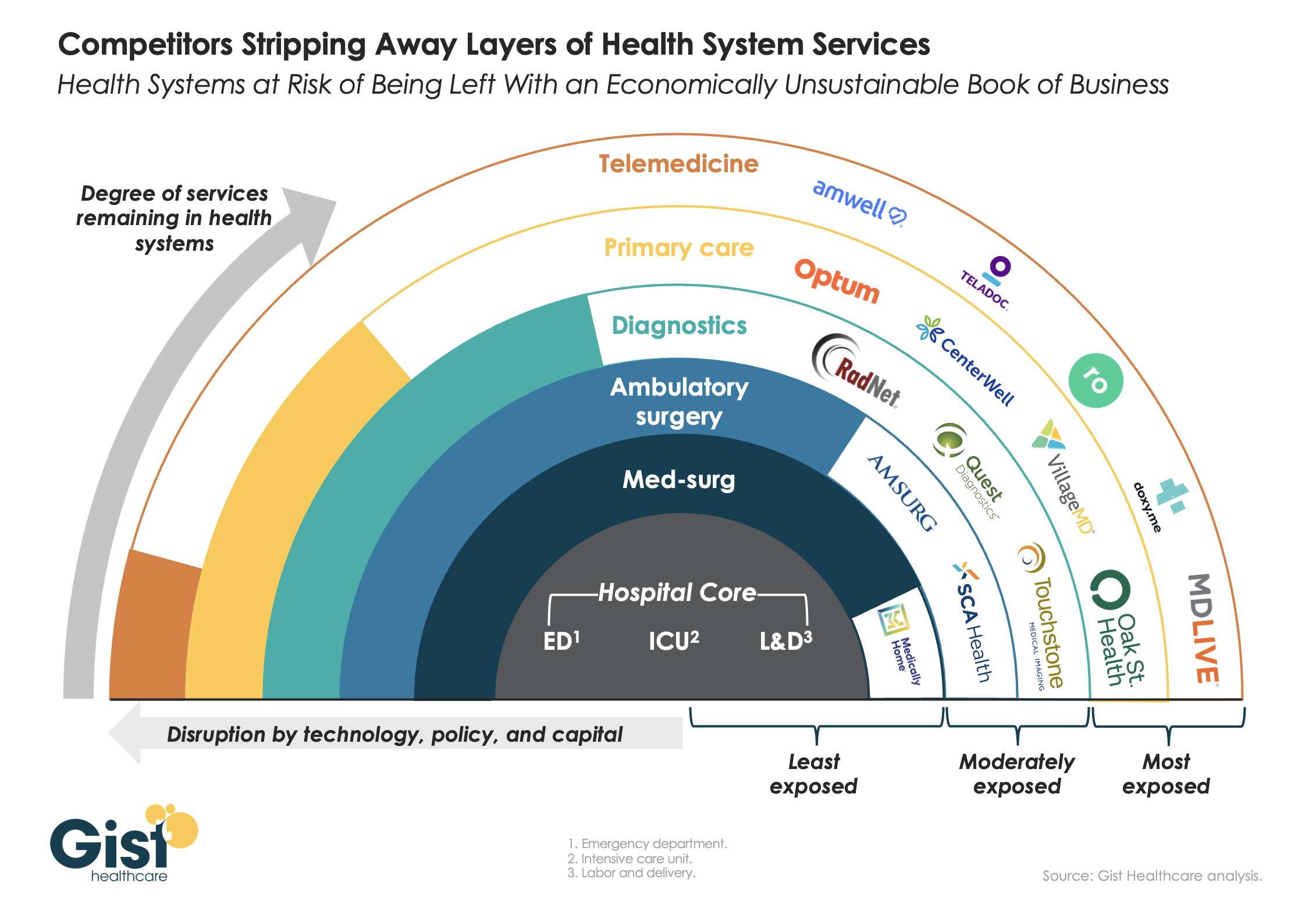

This week’s graphic features our assessment of the many emerging competitive challenges to traditional health systems.

Beyond inflation and high labor costs, health systems are struggling because competitors—ranging from vertically integrated payers to PE-backed physician groups—are effectively stripping away profitable services and moving them to lower-cost care sites. The tandem forces of technological advancement, policy changes, and capital investment have unlocked the ability of disruptors to enter market segments once considered safely within health system control.

While health systems’ most-exposed services, like telemedicine and primary care, were never key revenue sources (although they are key referral drivers), there are now more competitors than ever providing diagnostics and ambulatory surgery, which health systems have relied on to maintain their margins.

Moving forward, traditional systems run the risk of being “crammed down” into a smaller portfolio of (largely unprofitable) services: the emergency department, intensive care unit, and labor and delivery.

Health systems cannot support their operations by solely providing these core services, yet this is the future many will face if they don’temulate the strategies of disruptors by embracing the site-of-care shift, prioritizing high-margin procedures, rethinking care delivery within the hospital, and implementing lower-cost care models that enable them to compete on price.