Like everyone else, I am thankful the election end is in sight and a degree of “normalcy” might return. By next week, we should know who will sit in the White House, the 119th Congress and 11 new occupants of Governors’ offices. But a return to pre-election normalcy in politics is a mixed blessing.

“Normalcy” in our political system means willful acceptance that our society is hopelessly divided by income, education, ethnic and political views. It’s benign acceptance of a 2-party system, 3-branches of government (Executive, Legislative, Judicial) and federalism that imposes limits on federal power vis a vis the Constitution.

Our political system’ normalcy counts success by tribal warfare and election wins. Normalcy is about issues de jour prioritized by each tribe, not longer-term concern for the greater good in our country. Normalcy in our political system is near-sightedness—winning the next election and controlling public funds.

Comparatively, “normalcy” in U.S. healthcare is also tribal:

while the majority of U.S. adults believe the status quo is not working well but recognize its importance, each tribe has a different take on its future. The majority of the public think price transparency, limits on consolidation, attention to affordability and equitable access are needed but the major tribes—hospitals, insurers, drug companies, insurers, device-makers—disagree on how changes should be made. And each is focused on short-term issues of interest to their members with rare attention to longer-term issues impacting all.

Near-sightedness in healthcare is manifest in how executives are compensated, how partnerships are formed and how Boards are composed.

Organizational success is defined by 1-access to private capital (debt, private equity, strategic investors), 2-sustainnable revenue-growth, 4- scalable costs, 4-opportunities for consolidation (the exit strategy of choice for most) and 5-quarterly earnings. A long-term view of the system’s future is rarely deliberated by boards save attention to AI or the emergence of Big Tech. A vision for an organization’s future based on long-term macro-trends and outside-in methodologies is rare: long-term preparedness is “appreciated” but near-term performance is where attention is vested.

It pays to be near-sighted in healthcare: our complex regulatory processes keep unwelcome change at bay and our archaic workforce rules assure change resistance. …until it doesn’t. Industries like higher education, banking and retailing have experienced transformational changes that take advantage of new technologies and consumer appetite for alternatives that are new and better. The organizations winning in this environment balance near-sightedness with market attentiveness and vision.

Looking ahead, I have no idea who the winners and losers will be in this election cycle. I know, for sure, that…

The final result will not be known tomorrow and losers will challenge the results.

Short-term threats to the healthcare status quo will be settled quickly. First up: Congress will set aside Medicare pay cuts to physicians (2.8%) scheduled to take effect in January for the 5th consecutive year. And “temporary” solutions to extend marketplace insurance subsidies, facilitate state supervision of medication abortion services and telehealth access will follow quickly.

Think tanks will be busy producing white papers on policy changes supported by their funding sponsors.

And trade associations will produce their playbooks prioritizing legislative priorities and relationship opportunities with state and federal officials for their lobbyists.

Near-term issues for each tribe will get attention: the same is true in healthcare. Discussion about and preparation for healthcare’s longer-term future is a rarity in most healthcare C suites and Boardrooms. Consider these possibilities:

Medicare Advantage will be the primary payer for senior health: federal regulators will tighten coverage, network adequacy, premiums and cost sharing with enrollees to private insurers reducing enrollee choices and insurer profits.

To address social determinants of health, equitable access and comprehensive population health needs, regional primary care, preventive and public health programs will be fully integrated.

Large, organized groups/networks of physicians will be the preferred “hubs” for health services in most markets.

Interoperability will be fully implemented.

Physicians will unionize to assert their clinical autonomy and advance their economic interests.

The federal government (and some states) will limit tax exemptions for profitable not-for-profit health systems.

The prescription drug patent system will be modernized to expedite time-to-market innovations and price-value determinations.

The health insurance market will focus on individual (not group) coverage.

Congress/states will impose price controls on prescription drugs and hospital services.

Employers will significantly alter their employee benefits programs to reduce their costs and shift accountability to their employees. Many will exit altogether.

Regional integrated health systems that provide retail, hospital, physician, public health and health insurance services will be the dominant source of services.

Alternative-payment models used by Medicare to contract with providers will be completely overhauled.

Consumers will own and control their own medical records.

Consolidation premised on community benefits, consumer choices and lower costs will be challenged aggressively and reparation pursued in court actions.

Voters will pass Medicare for All legislation.

And many others.

A process for defining of the future of the U.S. health system and a bipartisan commitment by hospitals, physicians, drug companies, insurers and employers to its implementation are needed–that’s the point.

Near-sightedness in our political system and in our health, system is harmful to the greater good of our society and to the voters, citizens, patients, and beneficiaries all pledge to serve.

As respected healthcare marketer David Jarrard wrote in his blog post yesterday “As the aggravated disunity of this political season rises and falls, healthcare can be a unique convener that embraces people across the political divides, real or imagined. Invite good-minded people to the common ground of healthcare to work together for the common good that healthcare must be.”

Thinking and planning for healthcare’s long-term future is not a luxury: it’s an urgent necessity. It’s also not “normal” in our political and healthcare systems.

The drugstore retailer faces debt maturities, while the upending of some strategies introduces new uncertainties, analysts said.

S&P Global Ratings analysts have downgraded Walgreens Boot Alliance by two notches, to ‘BB’ from ‘BBB-’, which puts the drugstore company into speculative-grade territory.

Analysts Diya Iyer and Hanna Zhang cited guidance for the year “notably below” their expectations, and said “material strategic changes, limited cash flow generation, and large maturities in coming years are key risks to the business.”

The company is struggling in its retail business as well as its pharmacy operations, they said in a Friday client note. In the U.S., margins are taking a hit on the pharmacy side from reimbursement pressure and on the retail side from declining sales volume and higher shrink. They expect Walgreens’ S&P Global Ratings-adjusted EBITDA margin to decline more than 100 basis points this fiscal year, dipping below 5%, from 6% last year, though the company’s cost cuts will counter that somewhat.

Walgreens’ debt and its need to refinance much of it represent another “key risk,” they said. This November, Walgreens faces $1.4 billion in maturities, mostly U.S. bonds. Another $2.8 billion comes due in fiscal 2026 and $1.8 billion in fiscal 2027. The analysts called Walgreens’ move to consolidate cash “prudent” in case refinancing isn’t possible.

“We will be monitoring how Walgreens’ new management addresses this large debt load closely amid its persistently weak performance and higher interest rates,” Iyer and Zhang said.

Beyond those financial realities, though, are strategic weaknesses. Ex-Cigna executive Tim Wentworth took over as CEO last fall and this year has overseen a strategic review that has entailed more layoffs and store closures.

Walgreens has also upended some of its plans to expand its medical care operations, divesting of or shrinking many of its original investments and plans. Last month, for example, the company announced it would reduce its stake in value-based medical chain VillageMD, saying it will no longer be the company’s majority owner, after closing dozens of the clinics last year. The company first poured $1 billion into VillageMD in 2020 and more than doubled its stake for another $5.2 billion the following year, but the banner’s waning value helped drive a $6 billion loss in Q2.

Despite such moves, Iyer and Zhang said they continue to see the VillageMD banner as “a significant drag on profitability due to the rising cost of labor, pressures from reimbursement, and lower volumes.”

Walgreens’ acquisition streak led the S&P analysts to believe that it would divest of its Boots U.K. business, which could have helped pay down $8 billion to $10 billion in debt. But the company called off the idea about two years ago.

“We believe these frequent and large changes to the company’s strategic plans diminish management’s credibility to execute on a sustainable and cohesive operating model for Walgreens in both the near and long term,” Iyer and Zhang said.

Gains that Walgreens has managed to eke from its medical operations haven’t managed to offset declines on the retail said, they also said, adding that they are closely watching what it does next with its massive footprint. The company last year announced that it would close 150 stores in the U.S. and 300 in the U.K. and just last month said it was reviewing 25% of its current footprint, with plans to shutter a “significant portion” of its roughly 8,700 stores.

“Our ratings continue to reflect Walgreens’ large scale and its efforts to address its credit metric profile. With almost $140 billion in sales in fiscal 2023 and a diverse array of global businesses, Walgreens remains prominent in the drugstore space,” they said. “However, we think its scale is providing less protection to profitability at least partly due to inconsistent strategic direction.”

Steward Health Care’s Chapter 11 bankruptcy filing onMay 6, 2024, brought back bad memories of another large health system bankruptcy.

On July 21, 1998, Pittsburgh-based Allegheny Health and Education Research Foundation (AHERF) filed Chapter 11. AHERF grew very rapidly, acquiring hospitals, physicians, and medical schools in its vigorous pursuit of scale across Pennsylvania. Utilizing debt capacity and spending cash, AHERF quickly ran out of both, defaulted on its obligations, and then filed for bankruptcy. It was one of the largest bankruptcy filings in municipal finance and the largest in the rated not-for-profit hospital universe.

Steward Health Care is a for-profit, physician-owned hospital company, but its long-standing roots were in faith-based not-for-profit healthcare. Prior to the acquisition by Cerberus Capital Management in 2010, Caritas Christi Health Care System was comprised of six hospitals in eastern Massachusetts. Caritas was a well-regarded health system, providing a community alternative to the academic medical centers in downtown Boston. Over the next 14 years, Steward grew rapidly to 31 hospitals in eight states, most recently bolstered through an expansive sale-leaseback structure with a REIT. Per the bankruptcy filings, the company reported $9 billion in secured debt and leases on $6 billion of revenue.

Chapter 11 bankruptcy filings in corporate America are a means to efficiently sell assets or a path to re-emergence as a new streamlined company. A quick glance at Steward’s organizational structure shows a dizzying checkerboard of companies and LLCs that will require a massive untangling. Further, its capital structure includes both secured debt for operations and a separate and distinct lease structure for its facilities, and in bankruptcy, that signals significant complexity. Bankruptcy filings in not-for-profit healthcare are less common, although it is surprising that the industry did not see an increase after the pandemic. Not-for-profit hospitals that are in distress seem to hang on long enough to find a buyer, gain increased state funding, attain accommodations on obligations, or find some other escape route to avoid a payment default or filing.

Details regarding Steward’s undoing will unfold in the coming weeks as it moves through an auction process. But there are some early takeaways the not-for-profit industry can learn from this:

Remain essential in your local market. Hospitals must prove their value to their constituents, including managed care payers, especially in competitive urban markets, as Steward may have learned in eastern Massachusetts and Miami. Prior strategies of making a margin as an out-of-network provider are no longer viable as patients must shoulder more of the financial burden. Simply put, your organization should be asking one question: does a managed care plan need our existing network to sell a product in our market? If the answer is no, you need to develop strategies that make your hospital essential.

Embrace financial planning for long-term viability. Without it, a hospital or health system will be unable to afford the capital spending it needs to maintain attractive, patient-friendly, state-of-the art facilities or absorb long-term debt to fund the capital. Annual financial planning is more than just a trendline going forward. The scenarios and inputs must be well-founded, well-grounded in detail, and based on conservative assumptions. Increasing attention has to be paid to disrupters, innovators, specialized/segmented offerings, and expansion plans of existing and new competitors. Investors expect this from not-for-profit borrowers. Higher-performing hospitals and health systems of all sizes do this well.

Build capital capacity through improved cash flow. It is undoubtedly clear that Steward, like AHERF, was unable to afford the capital and debt they thought they could, either through flawed financial planning of its future state or, more concerning, the complete absence of it. Or they believed that rapid growth would solve all problems, not detailed financial planning, the use of benchmarks, or a sharp focus on operations. Increasing that capacity through sustained financial performance will allow an organization to de-leverage and build capital capacity.

When the case studies are written about Steward, a fact pattern will be revealed that includes the inability or unwillingness to attain synergies as a system, underspending on facility capital needs given a severe liquidity crunch, labor challenges, and a rapid payer mix shift.

Underlying all of this will undoubtedly be a failure of governance and leadership as we saw with AHERF. It will also likely indicate that one of the most precious assets healthcare providers may have is the management bandwidth to ensure strategic plans are appropriately made, tested, monitored, and executed.

While Steward and AHERF may be held up as extreme cases, not-for-profit hospital governance must continue to focus on checks-and-balances of management resources. Likewise, management must utilize benchmarks, data, and strong financial planning, given the challenges the industry faces.

Health systems are recovering from the worst financial year in recent history. We surveyed strategic planners to find out their top priorities for 2024 and where they are focusing their energy to achieve growth and sustainability. Read on to explore the top six findings from this year’s survey.

Research questions

With this survey, we sought the answers to five key questions:

How do health system margins, volumes, capital spending, and FTEs compare to 2022 levels?

How will rebounding demand impact financial performance?

How will strategic priorities change in 2024?

How will capital spending priorities change next year?

Bigger is Better for Financial Recovery

What did we find?

Hospitals are beginning to recover from the lowest financial points of 2022, where they experienced persistently negative operating margins. In 2023, the majority of respondents to our survey expected positive changes in operating margins, total margins, and capital spending. However, less than half of the sample expected increases in full-time employee (FTE) count. Even as many organizations reported progress in 2023, challenges to workforce recovery persisted.

40%

Of respondents are experiencing margins below 2022 levels

Importantly, the sample was relatively split between those who are improving financial performance and those who aren’t. While 53% of respondents projected a positive change to operating margins in 2023, 40% expected negative changes to margin.

One exception to this split is large health systems. Large health systems projected above-average recovery of FTE counts, volume, and operating margins. This will give them a higher-than-average capital spending budget.

Why does this matter?

These findings echo an industry-wide consensus on improved financial performance in 2023. However, zooming in on the data revealed that the rising tide isn’t lifting all boats. Unequal financial recovery, especially between large and small health systems, can impact the balance of independent, community, and smaller providers in a market in a few ways. Big organizations can get bigger by leveraging their financial position to acquire less resourced health systems, hospitals, or provider groups. This can be a lifeline for some providers if the larger organization has the resources to keep services running. But it can be a critical threat to other providers that cannot keep up with the increasing scale of competitors.

Variation in financial performance can also exacerbate existing inequities by widening gaps in access. A key stakeholder here is rural providers. Rural providers are particularly vulnerable to financial pressures and have faced higher rates of closure than urban hospitals. Closures and consolidation among these providers will widen healthcare deserts. Closures also have the potential to alter payer and case mix (and pressure capacity) at nearby hospitals.

Volumes are decoupled from margins

What did we find?

Positive changes to FTE counts, reduced contract labor costs, and returning demand led the majority of respondents in our survey to project organizational-wide volume growth in 2023. However, a significant portion of the sample is not successfully translating volume growth to margin recovery.

44%

Of respondents who project volume increases also predict declining margins

On one hand, 84% of our sample expected to achieve volume growth in 2023. And 38% of respondents expected 2023 volume to exceed 2022 volume by over 5%. But only 53% of respondents expected their 2023 operating margins to grow — and most of those expected that the growth would be under 5%. Over 40% of respondents that reported increases in volume simultaneously projected declining margins.

Why does this matter?

Health systems struggled to generate sufficient revenue during the pandemic because of reduced demand for profitable elective procedures. It is troubling that despite significant projected returns to inpatient and outpatient volumes, these volumes are failing to pull their weight in margin contribution. This is happening in the backdrop of continued outpatient migration that is placing downward pressure on profitable inpatient volumes.

There are a variety of factors contributing to this phenomenon. Significant inflationary pressures on supplies and drugs have driven up the cost of providing care. Delays in patient discharge to post-acute settings further exacerbate this issue, despite shrinking contract labor costs. Reimbursements have not yet caught up to these costs, and several systems report facing increased denials and delays in reimbursement for care. However, there are also internal factors to consider. Strategists from our study believe there are outsized opportunities to make improvements in clinical operational efficiency — especially in care variation reduction, operating room scheduling, and inpatient management for complex patients.

Strategists look to technology to stretch capital budgets

What did we find?

Capital budgets will improve in 2024, albeit modestly. Sixty-three percent of respondents expect to increase expenditures, but only a quarter anticipate an increase of 6% or more. With smaller budget increases, only some priorities will get funded, and strategists will have to pick and choose.

Respondents were consistent on their top priority. Investments in IT and digital health remained the number one priority in both 2022 and 2023. Other priorities shifted. Spending on areas core to operations, like facility maintenance and medical equipment, increased in importance. Interest in funding for new ambulatory facilities saw the biggest change, falling down two places.

Why does this matter?

Capital budgets for health systems may be increasing, but not enough. With the high cost of borrowing and continued uncertainty, health systems still face a constrained environment. Strategists are looking to get the biggest bang for their buck. Technology investments are a way to do that. Digital solutions promise high impact without the expense or risk of other moves, like building new facilities, which is why strategists continue to prioritize spending on technology.

The value proposition of investing in technology has changed with recent advances in artificial intelligence (AI), and our respondents expressed a high level of interest in AI solutions. New applications of AI in healthcare offer greater efficiencies across workforce, clinical and administrative operations, and patient engagement — all areas of key concern for any health system today.

Building is reserved for those with the largest budgets

What did we find?

Another way to stretch capital budgets is investing in facility improvements rather than new buildings. This allows health systems to minimize investment size and risk. Our survey found that, in general, strategists are prioritizing capital spending on repairs and renovation while deprioritizing building new ambulatory facilities.

When the responses to our survey are broken out by organization type, a different story emerges. The largest health systems are spending in ways other systems are not. Systems with six or more hospitals are increasing their overall capital expenditures and are planning to invest in new facilities. In contrast, other systems are not increasing their overall budgets and decreasing investments in new facilities.

AMCs are the only exception. While they are decreasing their overall budget, they are increasing their spending on new inpatient facilities.

Why does this matter?

Health systems seek to attract patients with new facilities — but only the biggest systems can invest in building outpatient and inpatient facilities. The high ranking of repairs in overall capital expenditure priorities suggests that all systems are trying to compete by maintaining or improving their current facilities. Will renovations be enough in the face of expanded building from better financed systems? The urgency to respond to the pandemic-accelerated outpatient shift means that building decisions made today, especially in outpatient facilities, could affect competition for years to come. And our survey responses suggest that only the largest health system will get the important first-mover advantage in this space.

AMCs are taking a different tack in the face of tight budgets and increased competition. Instead of trying to compete across the board, AMCs are marshaling resources for redeployment toward inpatient facilities. This aligns with their core identity as a higher acuity and specialty care providers.

Partnerships and affiliations offer potential solutions for health systems that lack the resources for building new facilities. Health systems use partnerships to trade volumes based on complexity. Partnerships can help some health systems to protect local volumes while still offering appropriate acute care at their partner organization. In addition, partnerships help health systems capture more of the patient journey through shared referrals. In both of these cases, partnerships or affiliations mitigate the need to build new inpatient or outpatient facilities to keep patients.

Eighty percent of respondents to our survey continued to lose patient volumes in 2023. Despite this threat to traditional revenue, health systems are turning from revenue diversification practices. Respondents were less likely to operate an innovation center or invest in early-stage companies in 2023. Strategists also reported notably less participation in downside risk arrangements, with a 27% decline from 2022 to 2023.

Why does this matter?

The retreat from revenue diversification and risk arrangements suggests that health systems have little appetite for financial uncertainty. Health systems are focusing on financial stabilization in the short term and forgoing practices that could benefit them, and their patients, in the long term.

Strategists should be cautious of this approach. Retrenchment on innovation and value-based care will hold health systems back as they confront ongoing disruption. New models of care, patient engagement, and payment will be necessary to stabilize operations and finances. Turning from these programs to save money now risks costing health systems in the future.

Market intelligence and strategic planning are essential for health systems as they navigate these decisions. Holding back on initiatives or pursuing them in resource-constrained environments is easier when you have a clear course for the future and can limit reactionary cuts.

Advisory Board’s long-standing research on developing strategy suggests five principles for focused strategy development:

Strategic plans should confront complexity. Sift through potential future market disruptions and opportunities to establish a handful of governing market assumptions to guide strategy.

Ground strategy development in answers to a handful of questions regarding future competitive advantage. Ask yourself: What will it take to become the provider of choice?

Communicate overarching strategy with a clear, coherent statement that communicates your overall health system identity.

A strategic vision should be supported by a limited number of directly relevant priorities. Resist the temptation to fill out “pro forma” strategic plan.

Pair strategic priorities with detailed execution plans, including initiative roadmaps and clear lines of accountability.

Strategists align on a strategic vision to go back to basics

What did we find?

Despite uneven recovery, health systems widely agree on which strategic initiatives they will focus more on, and which they will focus less on. Health system leaders are focusing their attention on core operations — margins, quality, and workforce — the basics of system success. They aim to achieve this mandate in three ways. First, through improving efficiency in care delivery and supply chain. Second, by transforming key elements of the care delivery system. And lastly, through leveraging technology and the virtual environment to expand job flexibility and reduce administrative burden.

Health systems in our survey are least likely to take drastic steps like cutting pay or expensive steps like making acquisitions. But they’re also not looking to downsize; divesting and merging is off the table for most organizations going into 2024.

Why does this matter?

The strategic priorities healthcare leaders are working toward are necessary but certainly not easy. These priorities reflect the key challenges for a health system — margins, quality, and workforce. Luckily, most of strategists’ top priorities hold promise for addressing all three areas.

This triple mandate of improving margins, quality, and workforce seems simple in theory but is hard to get right in practice. Integrating all three core dimensions into the rollout of a strategic initiative will amplify that initiative’s success. But, neglecting one dimension can diminish returns. For example, focusing on operational efficiency to increase margins is important, but it’ll be even more effective if efforts also seek to improve quality. It may be less effective if you fail to consider clinicians’ workflow.

Health systems that can return to the basics, and master them, are setting a strong foundation for future growth. This growth will be much more difficult to attain without getting your house in order first.

Vendors and other health system partners should understand that systems are looking to ace the basics, not reinvent the wheel. Vendors should ensure their products have a clear and provable return on investment and can map to health systems’ strategic priorities. Some key solutions health systems will be looking for to meet these priorities are enhanced, easy-to-follow data tools for clinical operations, supply chain and logistics, and quality. Health systems will also be interested in tools that easily integrate into provider workflow, like SDOH screening and resources or ambient listening scribes.

Going back to basics

Craft your strategy

1. Rebuild your workforce.

One important link to recovery of volume is FTE count. Systems that expect positive changes in FTEs overwhelmingly project positive changes in volume. But, on average, less than half of systems expected FTE growth in 2023. Meanwhile, high turnover, churn, and early retirement has contributed to poor care team communication and a growing experience-complexity gap. Prioritize rebuilding your workforce with these steps:

Recover: Ensure staff recover from pandemic-era experiences by investing in workforce well-being. Audit existing wellness initiatives to maximize programs that work well, and rethink those that aren’t heavily utilized.

Recruit: Compete by addressing what the next generation of clinicians want from employment: autonomy, flexibility, benefits, and diversity, equity, and inclusion (DEI). Keep up to date with workforce trends for key roles such as advance practice providers, nurses, and physicians in your market to avoid blind spots.

Retain: Support young and entry-level staff early and often while ensuring tenured staff feel valued and are given priority access to new workforce arrangements like hybrid and gig work. Utilize virtual inpatient nurses and virtual hubs to maintain experienced staff who may otherwise retire. Prioritize technologies that reduce the burden on staff, rather than creating another box to check, like ambient listening or asynchronous questionnaires.

2. Become the provider of choice with patient-centric care.

Becoming the provider of choice is crucial not only for returning to financial stability, but also for sustained growth. To become the provider of choice in 2024, systems must address faltering consumer perspectives with a patient-centric approach. Keep in mind that our first set of recommendations around workforce recovery are precursors to improving patient-centered care. Here are two key areas to focus on:

Front door: Ensure a multimodal front door strategy. This could be accomplished through partnership or ownership but should include assets like urgent care/extended hour appointments, community education and engagement, and a good digital experience.

Social determinants of health: A key aspect of patient-centered care is addressing the social needs of patients. Our survey found that addressing SDOH was the second highest strategic priority in 2023. Set up a plan to integrate SDOH screenings early on in patient contact. Then, work with local organizations and/or build out key services within your system to address social needs that appear most frequently in your population. Finally, your workforce DEI strategy should focus on diversity in clinical and leadership staff, as well as teaching clinicians how to practice with cultural humility.

3. Recouple volume and margins.

The increasingly decoupled relationship between volume and margins should be a concern for all strategists. There are three parts to improving volume related margins: increasing volume for high-revenue procedures, managing costs, and improving clinical operational efficiency.

Revenue growth: Craft a response to out-of-market travel for surgery. In many markets, the pool of lucrative inpatient surgical volumes is shrinking. Health systems are looking to new markets to attract patients who are willing to travel for greater access and quality. Read our findings to learn more about what you need to attract and/or defend patient volumes from out-of-market travel.

Cost reduction: Although there are many paths health systems can take to manage costs, focusing on tactics which are the most likely to result in fast returns and higher, more sustainable savings, will be key. Some tactics health systems can deploy include preventing unnecessary surgical supply waste, making employees accountable for their health costs, and reinforcing nurse-led sepsis protocols.

Clinical operational efficiency: The number one strategic priority in 2023, according to our survey, was clinical operational efficiency, no doubt in response to faltering margins. Within this area, the top place for improvement was care variation reduction (CVR). Ensure you’re making the most out of CVR efforts by effectively prioritizing where to spend your time. Improve operational efficiency outside of CVR by improving OR efficiency and developing protocols for complex inpatient management.

As 2023 comes to an end and prognostics for 2024 pepper Inboxes, high anxiety is understandable. The near-term environment for hospitals, especially public hospitals and not-for-profit health systems, is tepid at best: despite the November uptick in operating margins to 2% (Fitch, Syntellis), the future for hospitals is uncertain and it’s due to more than payer reimbursement, labor costs and regulatory changes.

Putting lipstick on the pig serves no useful purpose:

though state hospital associations, AHA, FAH, AEH and others have been effective in fending off unwelcome threats ranging from 340B cuts, site neutral payments and others at least temporarily, the welcoming environment for hospitals in the throes of the pandemic has been replaced by animosity and distrust.

The majority of the population believes U.S. the health system is heading in the wrong direction and think hospitals are complicit (See Polling data from Gallup and Keckley Poll below). They believe the system puts its profit above patient care and welcome greater transparency about prices and business practices. In states like Colorado (hospital expenditure report), Minnesota (billing and collection), and Oregon (nurse staffing levels), new regulations feed the public’s appetite for hospital accountability alongside bipartisan Congressional efforts to limit tax exemptions and funding for hospitals.

It’s a tsunami hospital boards must address if they are to carry out their fiduciary responsibilities:

Set Direction: The organization’s long-term strategy in the context of its vision, mission and values.

Secure Capital: The amount and sourcing of capital necessary to execute the strategy.

Hire a Competent CEO and Give Direction: Boards set direction; CEOs execute.

Regretfully, near-term pressures on hospitals have compromised long-term strategic planning in which the Board play’s the central role. But most hospital boards lack adequate preparedness to independently assess the long-term future for their organization i.e. analysis of trends and assumptions that cumulatively reshape markets, define opportunities and frame possible destinations for hospitals drawn from 5 zones of surveillance:

Clinical innovations.

Technology capabilities.

Capital Market Access and Deployment.

Regulatory Policy Changes.

Consumer Values, Preferences and Actions.

In reality, the near-term issues i.e. labor and supply chain costs, insurer reimbursement, workforce burnout et al—dominate board meetings; long-range strategic planning is relegated to an annual retreat where the management team and often a consultant present a recommendation for approval. But in many organizations, the long-term strategic plans (LTSPs) fall short:

Most LTSPs offer an incomplete assessment of clinical innovations and technologies that fundamentally alter how health services will be provided, where and by whom.

Most LTSPs are based on an acute-centric view of “the future” and lack input about other sectors and industries where the healthcare market is relevant and alternative approaches are executed.

Most LTSPs are aspirational and short on pragmatism. Risks are underestimated and strengths over-estimated.

Most LTSPs are designed to affirm the preferences of the hospital CEO without the benefit of independent, studied review and discussion with the board.

Most LTSPs don’t consider all relevant ‘future state’ options despite the Board’s fiduciary obligation to assure they do.

Most rely on data that’s inadequate/incomplete/misleading, especially in assessing how and chare capital markets are accessing and deploying capital in healthcare services.

Most LTSPs are not used as milestones for monitoring performance nor are underlying assumptions upon which LRSPs are based revisited.

My take:

The Board’s role in Long-Range Strategic Planning is, in many ways, it’s most important. It is the basis for deciding the capital requirements necessary to its implementation and the basis for hiring, keeping and compensating the CEO. But in most hospitals, the board’s desire to engage more directly around long-term strategy for the organization is not addressed. Understandable…

Boards are getting more media attention these days, and it’s usually in an unflattering context. Disclosures of Board malperformance in high profile healthcare organizations like Theranos, Purdue and others has been notable. Protocols for responding among Board members in investor-owned organizations is a priority, but less-so in many not-for-profit settings including hospitals often caught by surprise by media.

And Board members are asking for their organizations to engage them in more in strategy development. In the latest National Association of Corporate Directors’ survey, 81% of directors cited “oversight of strategic execution” and 80% “oversight of strategy development” as their top concerns from a list of 13 options. Hospital boards are no exception: they want to be engaged and cringe when treated as rubber stamps.

Hospital boards intuitively understand that surviving/thriving in 2024 is important but no guarantee of long-term stability given sobering realities with long-term impact:

The core business of hospitals–inpatient, outpatient and emergency services—is subject to market constraints on its prices, consumer and employer expectations and non-traditional competition. Bricks, sticks and clicks strategies will be deployed in a regulatory environment that’s agnostic to an organization’s tax status and competition is based on value that’s measured and publicly comparable.

The usefulness of artificial intelligence will widen in healthcare services displacing traditional operating models, staffing and resource allocation priorities.

Big tech (Apple (AAPL), Microsoft (MSFT), Alphabet (GOOG), Amazon (AMZN), Meta (META), Tesla (TSLA) and Nvidia (NVDA)—collectively almost 60% of all S&P 500 gains in 2023—will play a direct and significant role in how the healthcare services industry responds to macro-opportunities and near-term pressures. They’re not outside looking in; they’re inside looking out.

Private capital will play a bigger role in the future of the system and in capitalizing hospital services. Expanded scale and wider scope will be enabled through partnerships with private capital and strategic partners requiring governance and leadership adaptation. And, the near-term hurdles facing PE—despite success in fund-raising—will redirect their bets in health services and expectations for profits.

State and federal regulatory policies and compliance risks will be more important to execution. Growth through consolidation will face bigger hurdles, transparency requirements in all aspects of operations will increase and business-as-usual discontinued.

The scale, scope and effectiveness of an organization’s primary and preventive health services will be foundational to competing: managing ‘covered lives’, reducing demand, integrating social determinants and behavioral health, enabling consumer self-care, leveraging AI and enabling affordability will be key platform ingredients that enable growth and sustainability.

Media attention to hospital business practices including the role Boards play in LRSPs will intensify.

Granted: the issues facing hospitals are reliably short-term: as Congress returns next week, for instance, funding for the FDA, Community Health Center Fund, Teaching Health Center Graduate Medical Education Program, National Health Services Corps and Veterans Health is not authorized and $16 billion in cuts to Medicaid disproportionate share payments remains unsettled, so the short-term matters.

But arguably, engaging the hospital board in longer term planning is equally important. It’s not a luxury.

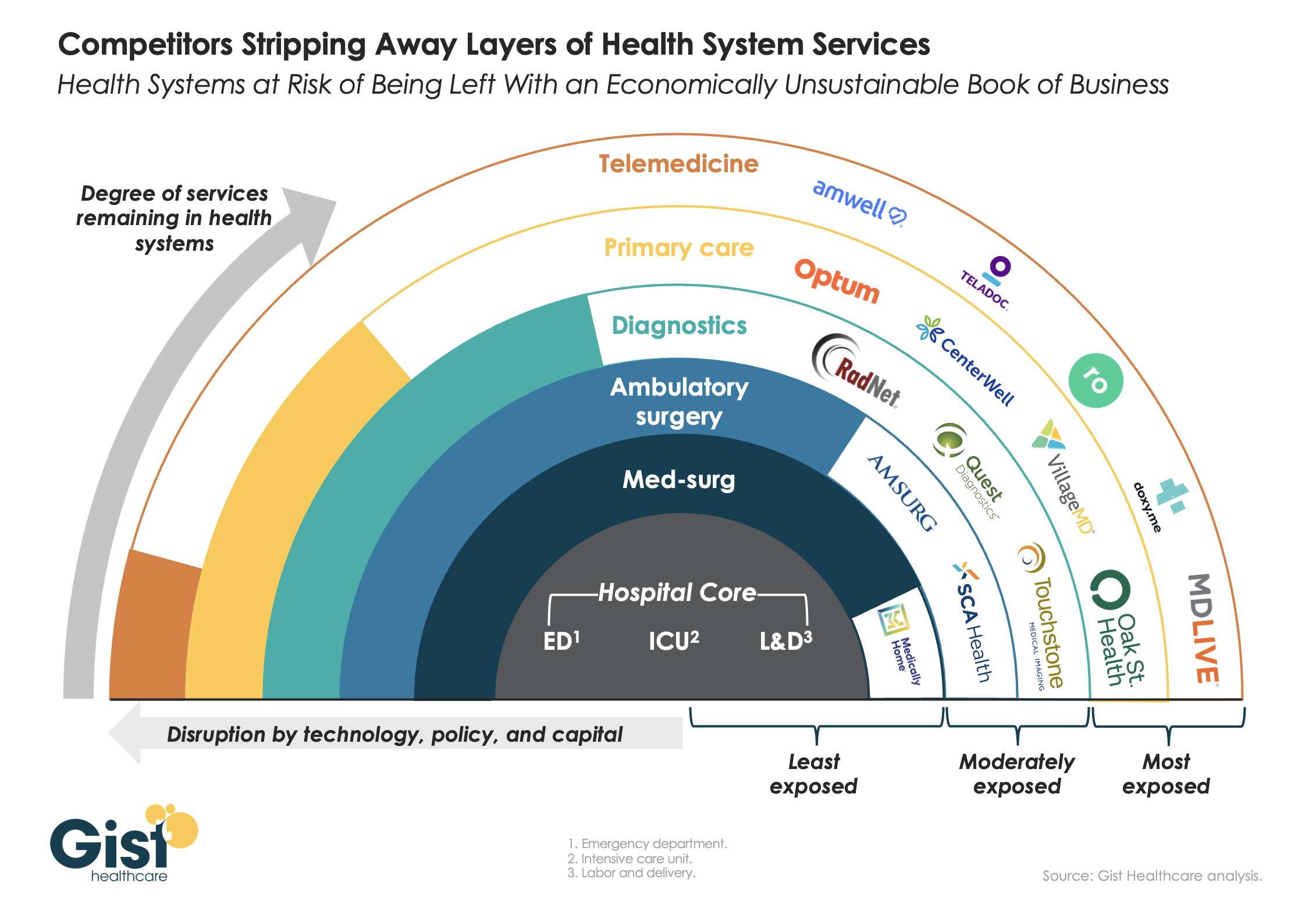

This week’s graphic features our assessment of the many emerging competitive challenges to traditional health systems.

Beyond inflation and high labor costs, health systems are struggling because competitors—ranging from vertically integrated payers to PE-backed physician groups—are effectively stripping away profitable services and moving them to lower-cost care sites. The tandem forces of technological advancement, policy changes, and capital investment have unlocked the ability of disruptors to enter market segments once considered safely within health system control.

While health systems’ most-exposed services, like telemedicine and primary care, were never key revenue sources (although they are key referral drivers), there are now more competitors than ever providing diagnostics and ambulatory surgery, which health systems have relied on to maintain their margins.

Moving forward, traditional systems run the risk of being “crammed down” into a smaller portfolio of (largely unprofitable) services: the emergency department, intensive care unit, and labor and delivery.

Health systems cannot support their operations by solely providing these core services, yet this is the future many will face if they don’temulate the strategies of disruptors by embracing the site-of-care shift, prioritizing high-margin procedures, rethinking care delivery within the hospital, and implementing lower-cost care models that enable them to compete on price.

Does hospital ownership matter? According to a study published last week in Health Affairs Scholar, NOT MUCH. That’s a problem for not-for-profit hospitals who claim otherwise.

58% of U.S. hospitals are not-for-profit hospitals; the rest are public (19%) or investor-owned (24%). In recent months, not-for-profit systems have faced growing antagonism from regulators and critics who challenge the worthwhileness of their tax exemptions and reasonableness of the compensation paid their top executives.

The lion’s share of this negative attention is directed at large, not-for-profit hospital system operators. Case in point: last week, Banner Health (AZ) joined the ranks of high-profile operators taken to task in the Arizona Republic for their CEO’s compensation contrasting it to not-for-profit sectors in which compensation is considerably lower.

Unflattering attention to NFP hospitals, especially the big-name systems, is unlikely to subside in the near-term. U.S. healthcare has become a winner-take-all battleground increasingly dominated by large-scale, investor-owned interests in hospitals, medical groups, insurance, retail health in pursuit of a piece of the $4.6 trillion pie.

The moral high ground once the domain of not-for-profit hospitals is shaky.

The NYU study examined whether hospital ownership influenced decisions made by consumers: they found “Fewer than one-third of respondents (29.5%) indicated that hospital status had ever been relevant to them in making decisions about where to seek care…significantly more important to respondents who indicated the lowest health literacy—74.7% of whom answered the key question affirmatively—than it was for people who indicated high health literacy, of whom only 18.3% found hospital ownership status to be relevant…also considerably more relevant for people working in health care than for those who did not work in health care (61.0% vs 24.5%)…

We found little evidence that hospital nonprofit status influenced Americans’ decisions about where to seek care. Ownership status was relevant for fewer than 30% of respondents and preference was greatest overall for public hospitals. Only 30–45% of respondents could correctly identify the ownership status of nationally recognized hospitals, and fewer than 30% could identify their local hospitals.

These findings suggest that contract failure does not currently provide a justification of nonprofit hospitals’ value; further scrutiny of tax exemption for nonprofit hospitals is warranted.”

Are NFP hospitals concerned? YES. It’s reality as systems address near term operational challenges and long-term questions about their strategies.

Last weekend, I facilitated the 4th Annual Chief Strategy Officers Roundtable in Austin TX sponsored by Lumeris. The group consisted of senior-level strategists from 11 not-for-profit systems and one for-profit. In one session, each reacted to 50 future state scenarios in terms of “likelihood” and “disruptive impact” in the NEAR term (3-5 years) and LONG TERM (8-10 years) using a 1 to 10 scale with 10 HI.

From these data and the discussion that followed, there’s consensus that the U.S. healthcare market is unlikely to change dramatically long-term, their short-term conditions will be tougher and their challenges unique.

‘Near-term cost containment is a priority. Hospitals are here-to-stay, but operating them will be harder.’

‘Increased scale and growth are necessary imperatives for their systems.’

‘Hospital systems will compete in a market wherein private capital and investor ownership will play a growing role, insurers will be hostile and value will the primary focus of cost-reduction by purchasers and policymakers.’

‘Distinctions betweennot-for-profit and for-profit hospitals are significant.’

‘Conditions for hospitals will be tougher as insurers play a stronger hand in shaping the future.’

Given the NYU study findings (above) concluding NFP ownership has marginal impact on hospital choices made by consumers, it’s understandable NFPs are anxious.

My take:

The issues facing not-for-profit hospitals in the U.S. are unique and complex. Per the commentary of the CSOs, their market conditions are daunting and major changes in their structure, funding and regulation unlikely.

That means lack of public understanding of their unique role is a conundrum.

Paul

PS: Issues about CEO compensation in healthcare are touchy and often unfair.

In every major NFP system, comp is set by the Independent Board Compensation Committee with outside consultative counsel. The vast majority of these CEOs aren’t in the job for the money joining their workforce in pursuit of the unique higher calling afforded service leaders in NFP healthcare.

This is Part 2 of a series by Cain Brothers about the first-ever collaboration conference between health systems and private equity (PE) investment firms. Part 1 of this series addressed the conference’s who, what and where. This commentary will focus on the why. We will explore the underlying forces uniting health systems with private equity during this period of unprecedented industry disruption.

Why Health Systems and PE Need Each Other

On June 13 and 14, 2023, Cain Brothers hosted the first-ever collaboration conference between health systems and private equity (PE) investment firms. Timing, market dynamics and opportunity aligned. The conference was an over-the-moon success. Along with its sponsors, Cain Brothers will seek to expand the conference and align initiatives through the coming years.

Why Now? Healthcare is Stuck and Needs Solutions

As a society, the U.S. is spending ever-higher amounts of money while its population is getting sicker. A maldistribution of facilities and practitioners creates inequitable access to healthcare services in lower-income communities with the highest levels of chronic disease.

New competitors and business models along with unfavorable macro forces, including high inflation, aging demographics and deteriorating payer mixes, are fundamentally challenging health systems’ status quo business practices.

Governments, particularly the federal government, have become healthcare’s largest payers, funding over 40% of healthcare’s projected $4.7 trillion expenditure in 2023. Individual patients often get lost in the massive payment shuffle between payers and providers.

Meanwhile, governments’ pockets are emptying. As a percentage of GDP, U.S. government debt obligations have grown from 55% in 2001 to 124% currently. With rising interest rates and the commensurate increase in debt service costs, as well as an aging population, there is little to suggest that new funding sources will emerge to fund expansive healthcare expenditures. Scarcity reigns where resources for healthcare providers were once plentiful.

As a consequence, the healthcare industry is entering a period of more fundamental economic limitations. Delaying transformation and expecting society to fund ongoing excess expenditure is not a sustainable long-term strategy. Current economic realities are forcing a dramatic reallocation of resources within the healthcare industry.

The healthcare industry will need to do more with less. Pleading poverty will fall on deaf ears. There will be winners and losers. The nation’s acute care footprint will shrink. For these reasons, health systems are experiencing unprecedented levels of financial distress. Indeed, parts of the system appear on the verge of collapse, particularly in medically underserved rural and urban communities.

More of the same approaches will yield more of the same dismal results. Waking up to this existential challenge, enlightened health systems have become more open to new business models and collaborative partnerships.

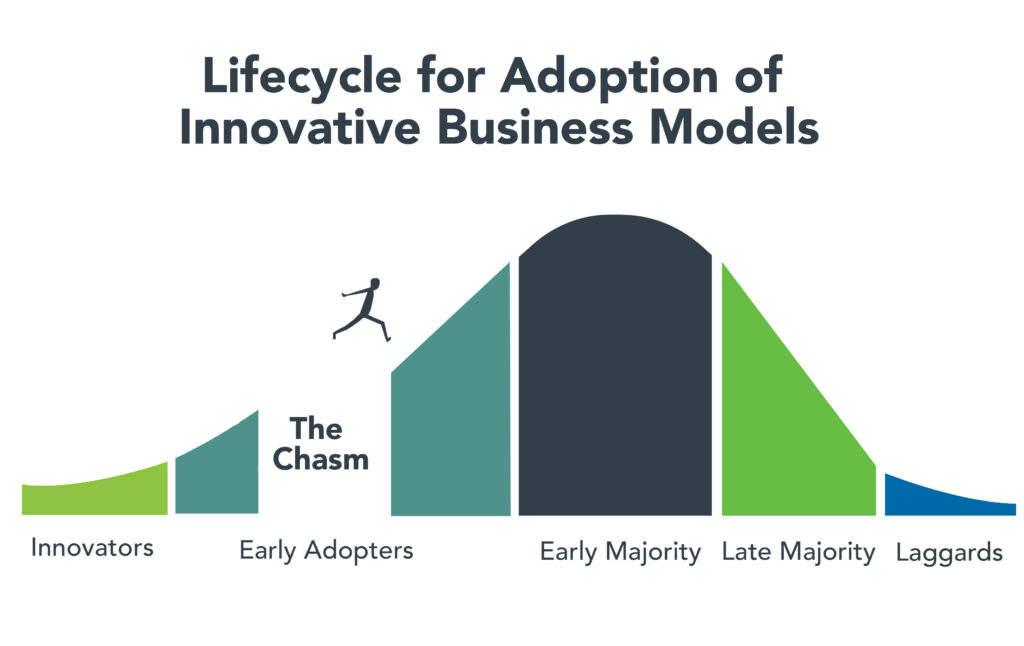

Necessity Stimulates Innovation

Two disruptive and value-based business models are on the verge of achieving critical mass. They are risk-bearing “payvider” companies (e.g. Kaiser, Oak Street Health and others) and consumer-friendly, digital-savvy delivery platforms (e.g. OneMedical and innumerable point-solution companies).

Value-based care providers and their investors have the scars and bruises to show for challenging entrenched business practices reliant on fee-for-service (FFS) business models and administrative services only (ASO) contracting. Incumbents have protected their privileged market position well through market leverage and outsized political influence.

Despite market resistance, “payvider” and digital platform companies are emerging from the proverbial “innovators’ chasm.” More early adopters, including those health systems attending the Nashville conference, are embracing value-creating business models. The chart below illustrates the well-trodden path innovation takes to achieve market penetration.

Ironically, during this period of industry disruption, health systems understand they need to deliver greater value to customers to maintain market relevance. It will require great execution and overcoming legacy practices to develop business platforms that incorporate the following value-creating capabilities:

Decentralized care delivery (to make care more accessible and lower cost).

Root-cause treatment of chronic conditions.

Integrated physical and mental healthcare services.

Consistent, high-quality consumer experience.

Coordinated service delivery.

Standardized protocols that improve care quality and outcomes.

A truly patient/customer-centric operating orientation.

It’s not what to do, it’s how to get it done that creates the vexing conundrum. Solutions require collaboration. Platform business models replete with strategic partnerships are emerging. Paraphrasing an African proverb, it’s going to take a village to fix healthcare. That’s why the moment for health systems and PE firms to collaborate is now.

PE to the Rescue?

Private equity has become the dominant investment channel for business growth across industries and nations. According to a recent McKinsey report, PE has more than $11.7 trillion in assets under management globally. This is a massive number that has grown steadily. PE changes markets. It turbocharges productivity. It is a relentless force for value creation.

By investing in a wide spectrum of asset classes, private equity has become a vital source of investment returns for pensions, endowments, sovereign wealth funds and insurance companies. Healthcare, given its size and inefficiencies, is a target-rich environment for PE investment and returns. This explains the PE’s growing interest in working with health systems to develop mutually beneficial, value-creating healthcare enterprises.

Despite reports to the contrary, PE firms must invest for the long term. Unlike the stock market, where investors can buy and sell a stock within a matter of seconds, PE firms do not have that luxury. To generate a return, they must acquire and grow businesses over a period of years to create suitable exit strategies.

Money talks. By definition, all buyers of new companies value their purchase more than the capital required for the acquisition. In making purchase decisions, buyers evaluate businesses’ past performance. They also assess how the new business will perform under their stewardship. PE or PE-backed acquirers also consider which future buyers will be most likely acquire the company after a five-plus year development period.

PE’s investment approach can align well with health systems looking to create sustainable long-term businesses tied to their brands and market positioning. PE firms buy and build companies that attract customers, employees and capital over the long term, far beyond their typical five- to seven-year ownership period. Health systems that partner with PE firms to develop companies are the logical acquirers of those companies if they succeed in the marketplace. In this way, a rising valuation creates value for both health systems and their PE partners.

It is important to note that not all PE are created the same. Like health systems, PE firms differ in size, market orientation, investment theses, experience and partner expectations. Given this inherent diversity, it takes time, effort and a shared commitment to value creation for health systems and PE firms to determine whether to become strategic partners. Not all of these partnerships will succeed, but some will succeed spectacularly.

For health system-PE partnerships to work, the principals must align on strategic objectives, governance, performance targets and reporting guidelines. Trust, honest communication and clear expectations are the key ingredients that enable these partnerships to overcome short-term hurdles on the road to long-term success.

Conclusion: Time to Slay Healthcare’s Dragons

Market corrections are hard. As a nation, the U.S. has invested too heavily in hospital-centric, disease-centric, volume-centric healthcare delivery. The result is a fragmented, high-cost system that fails both consumers and caregivers. The marketplace is working to reallocate resources away from failing business practices and into value-creating enterprises that deliver better care outcomes at lower costs with much less friction.

Progressive health systems and PE firms share the goal of creating better healthcare for more Americans. Cain Brothers is committed to advancing collaboration between health systems and PE-backed companies. In addition to the Nashville conference, the firm has combined its historically separate corporate and non-profit coverage groups to foster idea exchange, expand sector understanding and deliver higher value to clients.

The ability to connect and collaborate effectively with private equity to advance business models will differentiate winning health systems. In a consolidating industry, this differentiation is a prerequisite for sustaining competitiveness. It’s adapt or die time. Health systems that proactively embrace transformation will control their future destiny. Those that fail to do so will lose market relevance.

The future of healthcare is not a zero-sum equation. Markets evolve by creating more complex win-win arrangements that create value for customers. No industry requires restructuring more than healthcare. As a nation and an industry, we have the capacity to fix America’s broken healthcare system. The real question is whether we have the collective will, creativity and resourcefulness to power the transformation. We believe the answer to that question is yes.

Paraphrasing Rev. Theodore Parker, the economic arc of the marketplace is long but it bends toward value. Together, health systems and PE firms can power value-creation and transformation more effectively than either sector can do independently. Each needs the other to succeed. Slaying healthcare’s dragons will not be easy but it is doable. It’s going to take a village to fix healthcare.

The U.S. health system is big and getting bigger. It is labor intense, capital intense, and highly regulated. Each sector operates semi-independently protected by local, state and federal constraints that give incumbents advantages and dissuade insurgents.

Competition has been intramural:

Growth by horizontal consolidation within sectors has been the status quo for most to meet revenue and influence targets. In tandem, diversification aka vertical consolidation and, for some, globalization in each sector has distanced bigger players from smaller:

insurers + medical groups + outpatient facilities + drug benefit managers

retail pharmacies + primary & preventive care + health & wellbeing services + OTC products/devices

regulated medical devices + OTC products for clinics, hospitals, homes, workplaces and schools.

The landscape is no man’s land for the faint of heart but it’s golden for savvy private investors seeking gain at the expense of the system’s dysfunction and addictions—lack of price transparency, lack of interoperability and lack of definitive value propositions.

What’s ahead?

Everyone in the U.S. health system is aware that funding is becoming more scarce and regulatory scrutiny more intense, but few have invested in planning beyond tomorrow and the day after. Unlike drug and device manufacturers with global markets and long-term development cycles, insurers and providers are handicapped. Insurers respond by adjusting coverage, premiums and co-pays annually. Providers—hospitals, physicians, long-term care providers and public health programs– have fewer options. For most, long-range planning is a luxury, and even when attempted, it’s prone to self-protection and lack of objectivity.

Changes to the future state of U.S. healthcare are the result of shifts in these domains:

They apply to every sector in healthcare and define the context for the future of each organization, sector and industry as a whole:

The Clinical Domain: How health, diseases and treatments are defined and managed where and by whom; how caregivers and individuals interact; how clinical data is accessed, structured and translated through AI enabled algorithms; how medication management and OTC are integrated; how social determinants are recognized and addressed by caregivers and communities: and so on. The clinical domain is about more than doctors, nurses, facilities and pills.

The Technology Domain: How information technologies enable customization in diagnostics and treatments; how devices enable self-care; how digital platforms enable access; how systemness facilitates integration of clinical, claims and user experience data; how operating environments shift to automation lower unit costs; how sites of care emerge; how caregivers are trained and much more. Proficiency in the integration of technologies is the distinguishing feature of organizations that survive and those that don’t. It is the glue that facilitates systemness and key to the system’s transformation.

The Regulatory Domain: How affordability, value, competition, choice, healthcare markets, not-for-profit and effectiveness are defined; how local, state and federal laws, administrative orders by government agencies and executive actions define and change compliance risks; how elected officials assess and mitigate perceived deficiencies in a sector’s public accountability or social responsibility; how courts adjudicate challenges to the status quo and barriers to entry by outsiders/under-served populations; how shareholder ownership in healthcare is regulated to balance profit and the public good; et al. Advocacy on behalf of incumbents geared to current regulatory issues (especially in states) is compulsory table stakes requiring more attention; evaluating potential regulatory environment shifts that might fundamentally change the way a system is structured, roles played, funded and overseen is a luxury few enjoy.

The Capital Domain: how needed funding for major government programs (Medicare, Medicaid, Children’s, Military, Veterans, HIS, Dual Eligibles et al) is accessed and structured; how private investment in healthcare is encouraged or dissuaded; how monetary policies impact access to debt; how personal and corporate taxes impact capitalization of U.S. healthcare; how value-based programs reduce unnecessary costs and improve system effectiveness; how the employer tax exemption fares long-term as employee benefits shrink; how U.S. system innovations are monetized in global markets; how insurers structure premiums and out of pocket payments: et al. The capital domain thinks forward to the costs of capital it deploys and anticipated returns. But inputs in the models are wildly variable and inconsistent across sectors: hospitals/health systems vs. global private equity healthcare investors vs. national insurers’ capital strategies vary widely and each is prone to over-simplification about the others.

The Consumer Domain: how individuals, households and populations perceive and use the system; how they assess the value of their healthcare spending; how they vote on healthcare issues; how and where they get information; how they assess alternatives to the status quo; how household circumstances limit access and compromise outcomes; et al. The original sin of the U.S, health system is its presumption that it serves patients who are incapable/unwilling to participate effectively and actively in their care. Might the system’s effectiveness and value proposition be better and spending less if consumerization became core to its future state?

For organizations operating in the U.S. system, staying abreast of trends in these domains is tough. Lag indicators used to monitor trends in each domain are decreasingly predictive of the future. Most Boards stay focused on their own sector/subsector following the lead of their management and thought leadership from their trade associations. Most are unaware of broader trends and activities outside their sector because they’re busy fixing problems that impact their current year performance. Environmental assessments are too narrow and short-sighted. Planning processes are not designed to prompt outside the box thinking or disciplined scenario planning. Too little effort is invested though so much is at risk.

It’s understandable. U.S. healthcare is a victim of its success; maintaining the status quo is easier than forging a new path, however obvious or morally clear. Blaming others and playing the victim card is easier than corrective actions and forward-thinking planning.

In 10 years, the health system will constitute 20% of the entire U.S. economy and play an outsized role in social stability. It’s path to that future and the greater good it pursues needs charting with open minds, facts and creativity. Society deserves no less.

As hospital leaders convene in Seattle this weekend for the American Hospital Association Leadership Summit, their future is uncertain.

Last week’s court decision in favor of hospitals shortchanged by the 340B drug program and 1st half 2023 improvement in operating margins notwithstanding, the deck is stacked against hospitals—some more than others. And they’re not alone: nursing homes and physician practices face the same storm clouds:

Decreased reimbursement from government payers (Medicare and Medicaid) coupled with heightened tension with national health insurers seeking bigger discounts and direct control of hospital patient care.

Persistent medical-inflation driving costs for facilities, supplies, wages, technologies, prescription drugs and professional services (legal, accounting, marketing, et al) higher than reimbursement increases by payers.

Increased competition across the delivery spectrum from strategic aggregators, private equity and health insurers diversifying into outpatient, physician services et al.

Increased discontent and burnout among doctors, nurses and care teams who feel unappreciated, underpaid and overworked.

Escalating media criticism of not-for-profit hospitals/health system profitability, debt collection policies, lack of price transparency, consolidation, executive compensation, charity care, community benefits and more.

Declining trust in the system across the board.

Most hospitals soldier on: they’re aware of these and responding as best they can. But most are necessarily focused only on the near-term: bed needs, workforce recruitment and staffing, procurement costs for drugs and supplies and so on. Some operate in markets less problematic than others, but the trends hold true directionally in every one of America’s 290 HRR markets.

Planning for the long-term is paralyzed by the tyranny of the urgent:

survival and sustainability in 2023 and making guarded bets about 2024 dominate today’s plans. That’s reality. Though the healthcare pie is forecast to get bigger, it’s being carved up by upstarts pursuing profitable niches and mega-players with deep pockets and a take-no-prisoners approach to their growth strategies. The result is an industry nearing meltdown.

Each traditional sector thinks it’s moral virtue more honorable than others. Each blames the other for avoidable waste and inaction in weeding out its bad actors. Each is pays lip service to “value-based care” and “system transformation” while doubling-down on making sure changes are incremental and painless for the near-term. And each believes the long-term destination of the system will be different than the past but no two agree on what that is.

Hospitals control 31% of the spend directly and as much as 43% with their employed physicians included. So, they’re a logical focus of attention from outsiders. Whether not for profit, public or investor owned, all are thought to be expensive and non-transparent and increasingly many are seen as ‘Big Business’ with excessive profits. Complaints about heavy-handed insurer reimbursement and price-gauging by drug companies fall on death ears in most communities. That’s why most are focused on near-term survival and few have the luxury or tools to plan for the future.

As a start, answers to the questions below in the 3-5 (mid-term) and 8–10-year (long-term) time frames is imperative for every hospital leadership team and Board:

Is the status quo sustainable? With annual spending projected to increase at 5.4%/year through 2031– well above population and economic growth rates overall– will employers remain content to pay 224% of Medicare rates to produce profits for hospitals, doctors, drug and device makers and insurers? Will they continue to pass these costs through to their customers and employees while protecting their tax exemptions or will alternative strategies prompt activism? Might employers drive system transformation by addressing affordability, effectiveness, consumer self-care and systemness et al. with impunity toward discomfort created for insiders? Or, might voters reject the status quo in subsequent state/federal elections in favor of alternatives with promised improvement? And who will the winners and losers be?

Are social determinants a core strategy or distraction? 70% of costs in the health system are directly attributable to social needs unmet—food insecurity. loneliness et al. But in most communities, programs addressing SDOH and public health programs that serve less-privileged populations are step-children to better funded hospitals and retail services targeted to populations that can afford them. Is the destination incremental bridges built between local providers and public health programs to satisfy vocal special interest groups OR comprehensive integration of SDOH in every domain of operation? Private investors are wading into SDOH if they’re attached to a risk-based insurance programs like Medicare Advantage and others, but sparingly in other settings. Does the future necessitate re-definition of “community benefits” or new regulations prompting providers, drug companies and payers to fair-share performance. Is the future modest improvement in the “Health or Human Services” status quo OR is system of “Health and Social Services” that’s fully integrated? And might interoperability and connectivity in the entire population become “true north” for tech giants and EHR juggernauts seeking to evade anti-trust constraint and demonstrate their commitment to the greater good? There’s no debate that SDOH is central to community health and wellbeing but in most communities, it’s more talk than walk. Yesterday, SDOH was about risk factors; today, it’s about low-income populations who lack insurance; tomorrow, it’s everyone.

How should the health system of the future be funded? The current system of funding is a mess: In 2021, the federal government and households accounted for the largest shares of national health spending (34 % and 27%, respectively), followed by private businesses (17%), state and local governments (15%), and other private revenues (7%). It will spend $4.66 trillion, employ 19 million and impact every citizen (and non-citizen) directly. But 4 of 10 households have unpaid medical bills. Big employers in certain industries provide rich benefits while half of small businesses provide none. Medicare depends on employer payroll taxes for the lion’s share of its Part A (Hospital) funding exposing the “trust fund” to a shortfall in 2028 and insolvency fears…and so on. Increased public funding via taxes is problematic and debt is more costly as interest rates go up and the municipal bond market tightens. Voters and private employers don’t seem inclined to pay higher taxes for healthcare–:is it worth $13,998 per capita today? $20,426 in 2031? Will high-cost inpatient care and specialty drugs become regulated public utilities in which access and pricing is tightly controlled and directly funded by government? Will private investors and strategic aggregators be required to take invest in community benefits to offset the disproportionate costs borne by hospitals, public health clinics and others? Is there a better formula for funding U.S. healthcare? Other systems of the world spend more on social services and preventive health and less on specialty care. They spend a third less and get comparable if not better outcomes though each is stretched to deal with medical inflation. And in most, government funding is higher, private funding lower and privileged populations have access to private services they pay for directly. Where do we start, and who demands the question be answered?

How will innovations in therapeutics and information technology change how individuals engage with the system? Artificial intelligence will directly impact 60% of the traditional health delivery workforce, negating jobs for many/most. Non-allopathic therapies, technology-enabled self-care, precision medicines, non-invasive and minimally invasive surgical techniques are changing change how care is delivered, by whom and where. Thus, lag indicators based on visits, procedures, admissions and volume are increasingly useless. How will demand be defined in the future? Who will own the data and how will it be accessed? And how will the rights of patients (consumers) be protected in courts and in communities? In the future, information-driven healthcare will be much more than encounter data from medical records and claims-based analyses from payers. It will be sourced globally, housed centrally and accessed by innovators and consumers to know more about their health now and next. Within 10 years, generative AI coupled with therapeutic innovation will fundamentally change roles, payments and performance measurement in every domain of healthcare. Proficiency in leveraging the two will anchor system reputations and facilitate significant market share shifts to high value, high outcome, lower cost alternatives…whether local or not.

How will regulators and court decisions enact fair competition, consumer choices and antitrust protections? The current political environment is united around reforms that encourage price transparency and affordability. FTC and DOJ leaders are aligned on healthcare oversight with a decided bent toward heightened enforcement and tighter scrutiny of proposed deals (both vertical and horizontal integration). But their leaders’ terms are subject to political appointments and elections: that’s an unknown. And while recent rulings of the conservative leaning Supreme Court are problematic to many in healthcare, their rulings are perhaps more predictable than policies, rules and regulations directly impacted by election results.

For hospital leaders gathering in Seattle this week, and in local board meetings nationwide, necessary attention is being given the near-term issues all face. But longer-term issues lurk: the future does not appear a modernized version of the past for anyone in U.S. healthcare, especially hospitals. And among hospitals, fundamental precepts—like tax exemptions for “not-for-profit” hospitals, community benefits and charity care in exchange for tax exemption, EMTALA et al. regulations that require access without pre-condition are among many that will re-surface as the long-term view of the health system is re-considered.

To that end, the questions above deserve urgent discussion in every hospital board room and C suite. Trade-offs aren’t clear, potential future state hospital scenarios are not discreet and winners and losers unknown. But a fact-driven process recognizing a widening array of players with deep pockets and fresh approaches is necessary.