When I talk to … Posted on August 11, 2025 by henrykotula • Posted in Importance, Leadership, Leadership Conversation, Leadership Culture, Leadership Listens • Leave a comment Share this: Share on X (Opens in new window) X Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Like Loading...

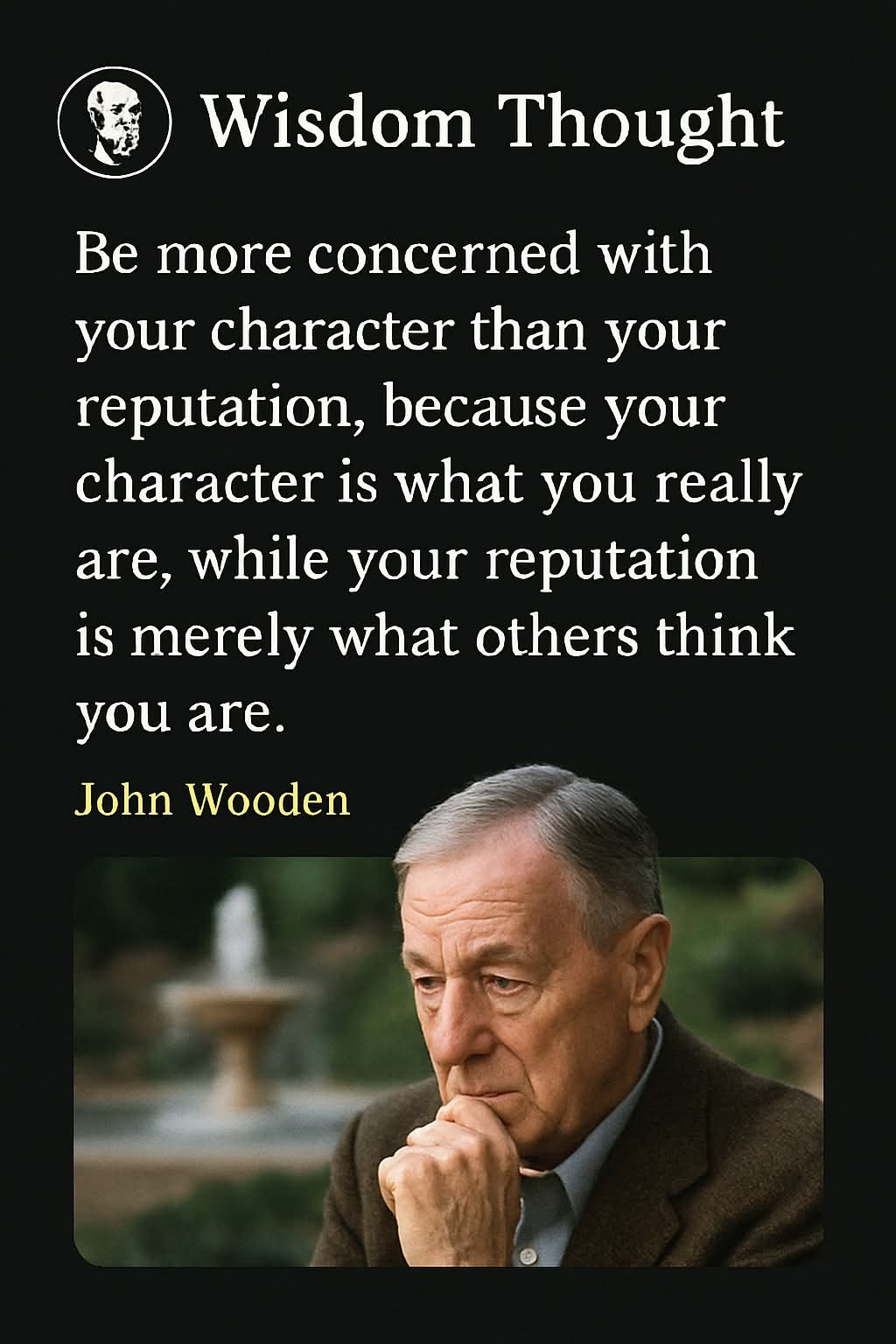

Wisdom Thought – Character vs Reputation Posted on August 5, 2025 by henrykotula • Posted in Character, Leadership, Leadership Integrity, Leadership Respect, Leadership Trust, Leadership Values, Reputation, Thought Leaders, Thought of the Day, Wisdom • Leave a comment Share this: Share on X (Opens in new window) X Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Like Loading...

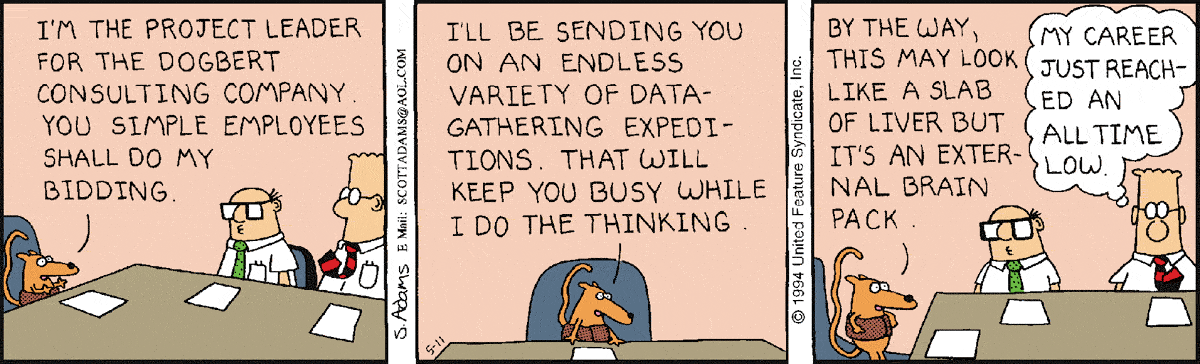

Cartoon – Importance of Project Leadership Posted on July 6, 2025 by henrykotula • Posted in Cartoon, Importance, Leadership, Leadership Problem Solving, Project Leadership • Leave a comment Share this: Share on X (Opens in new window) X Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Like Loading...

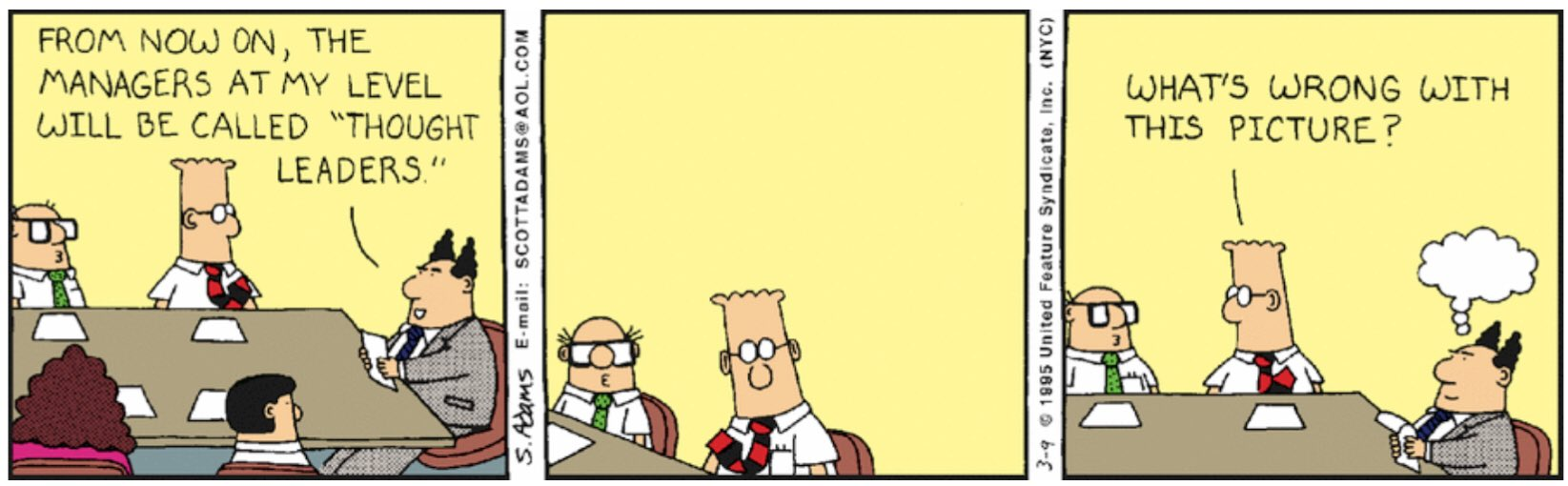

Cartoon – Thought Leadership Posted on July 6, 2025 by henrykotula • Posted in Cartoon, Leadership, Thought Leaders • Leave a comment Share this: Share on X (Opens in new window) X Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Like Loading...

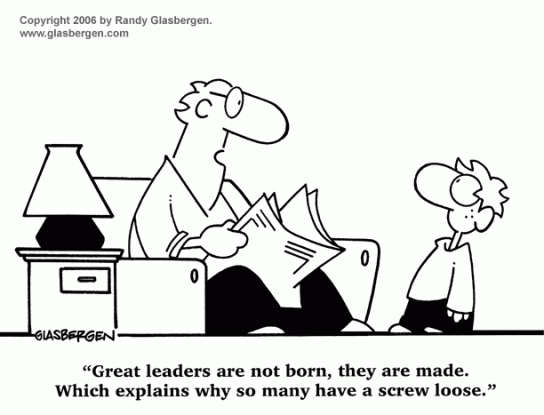

Cartoon – Great Leaders are not Born Posted on July 6, 2025 by henrykotula • Posted in Cartoon, Leadership, Sign of the Times, State of the Union • Leave a comment Share this: Share on X (Opens in new window) X Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Like Loading...

Buffet on Leadership Posted on July 3, 2025 by henrykotula • Posted in 2026 Mid Term Election Issues, 2028 Election Issues, Leadership, Leadership Character, Leadership Culture, Leadership Ethics, Leadership Integrity, Leadership Respect, Leadership Trust, Leadership Values, Uncategorized • Leave a comment Share this: Share on X (Opens in new window) X Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Like Loading...

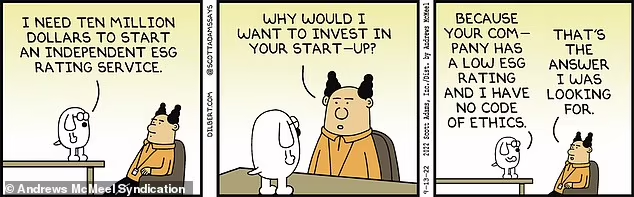

Cartoon – The Answer You were Looking For Posted on July 2, 2025 by henrykotula • Posted in Answer, Cartoon, Ethics, Investment, Leadership, Start-Up • Leave a comment Share this: Share on X (Opens in new window) X Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Like Loading...

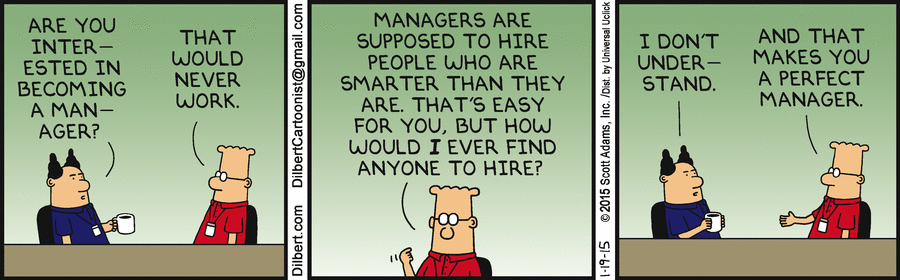

Cartoon – What makes you a Perfect Manager? Posted on July 2, 2025 by henrykotula • Posted in Cartoon, Leadership, Manager, Perfect, Smart • Leave a comment Share this: Share on X (Opens in new window) X Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Like Loading...

Cartoon – The Illusion of Leadership Posted on June 1, 2025 by henrykotula • Posted in Cartoon, Illusion, Jargon, Leadership, Leadership Rounding • Leave a comment Share this: Share on X (Opens in new window) X Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Like Loading...

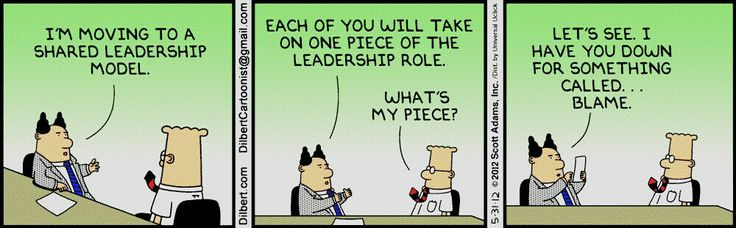

Cartoon – Shared Leadership Model Posted on June 1, 2025 by henrykotula • Posted in Blame, Cartoon, Leadership, Shared Leadership, Sign of the Times • Leave a comment Share this: Share on X (Opens in new window) X Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Like Loading...