Abuses by payers are myriad, but these five areas could bear the most fruit for federal antitrust investigators.

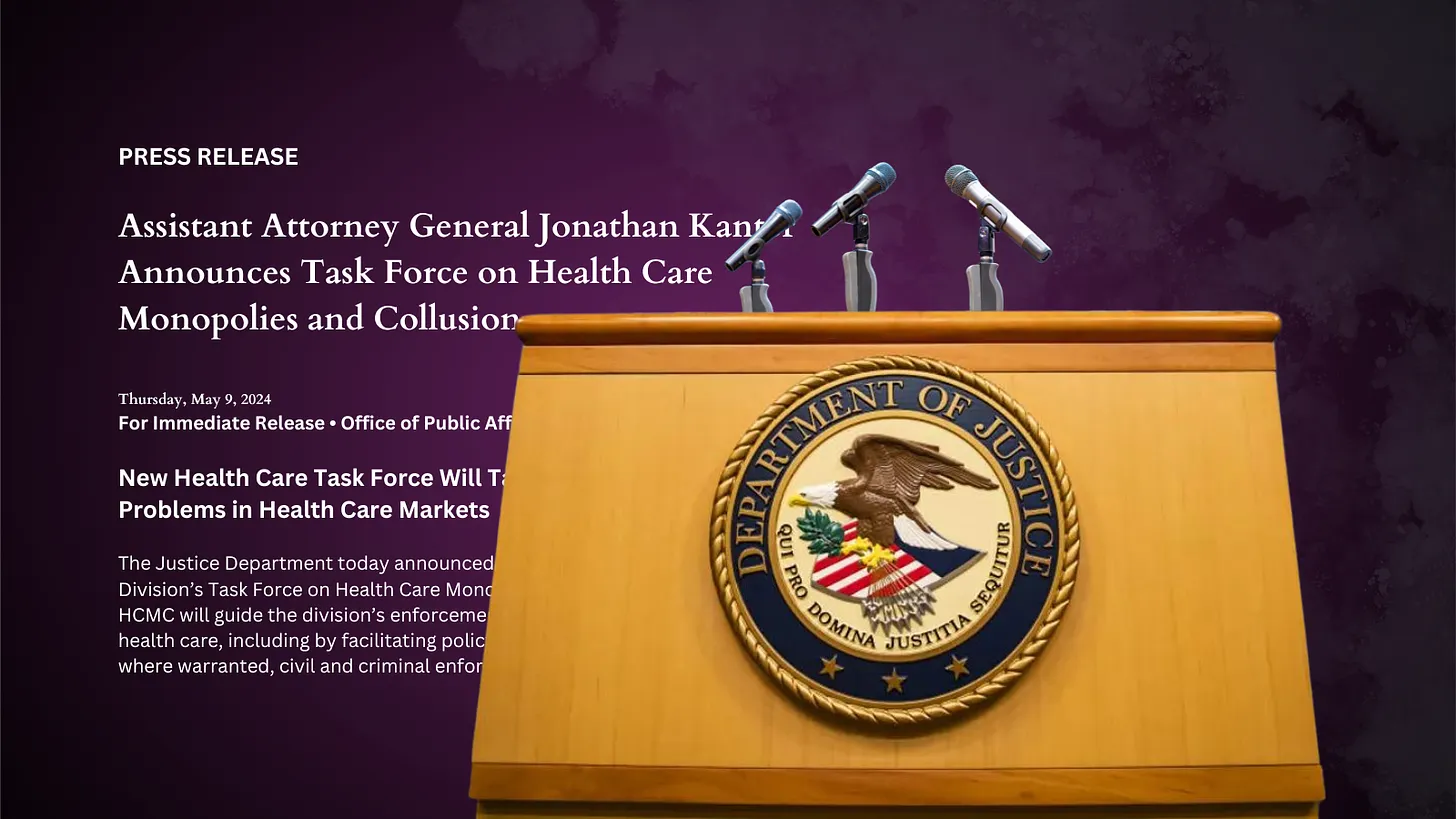

Earlier this month, the U.S. Department of Justice announced it has haunched an investigation into “issues regarding payer-provider consolidation” along with other problems associated with mergers and acquisitions in health care. This is significant. For years Washington has trained its oversight authority on pharmaceutical manufacturers, private equity investments in health care and, more recently, pharmacy benefits managers controlled by big insurers. This has held bad actors like Martin Skhreli and Steward Healthcare accountable. But, it has also let insurers grow ever larger, under the radar.

No longer.

This task force will specifically evaluate the following, as an example: “A health insurance company buys several medical practices that compete with each other. It also prohibits its medical practices from contracting with rival health insurance companies.” The government will also dig into “anticompetitive uses of health care data,” “preventing transparency,” “price fixing,” and other areas that could drag nefarious activities of insurers into the spotlight.

I applaud the Department of Justice’s continued focus on these issues, building on the Department’s action announced in February to begin an antitrust investigation into UnitedHealth Group. (If you haven’t read the piece we published in February on UnitedHealth’s self-dealing that helped lead DOJ to open that antitrust inquiry, you can do so here.) The following are a few areas of low-hanging fruit that I hope the task force will focus on as they consider the impact insurers’ ongoing vertical integration has had on the overall health care system.

1. Insurers purchasing physician practices

Once a low-profile issue, Congress and the Biden administration alike have increasingly turned their focus to insurance companies – often referred to as payers – that now own and operate physician practices and clinics – those being paid. Even for someone without a law degree, it is easy to see the conflict this creates, particularly at scale.

There is the oft-cited statistic that UnitedHealth has said that through its Optum division, the company employs or otherwise controls about 10 percent of doctors in the U.S. – around 130,000 physicians and other practitioners in 16 states. This prompted me to take a closer look at publicly available information on the number of doctors employed by other insurers to get a better handle on how much control of physician practices payers now have.

It is difficult to put a percentage on physicians employed by each insurer, but it is clear that the others are following UnitedHealth’s lead. CVS/Aetna purchased Signify Health in 2023, adding 10,000 clinicians to its portfolio. The company says it supports “more than 40,000 physicians, pharmacists, nurses and nurse practitioners.”

Clearly taking a page out of UnitedHealth’s playbook, Elevance (formerly Anthem), which owns Blue Cross Blue Shield plans in 14 states announced last month a “strategic partnership” with 900 providers across several states. Elevance did not disclose the terms of the deal except to say it, “will primarily be through a combination of cash and our equity interest in certain care delivery and enablement assets of Carelon Health.”

As insurers have acquired physician practices, they also have created a rinse-and-repeat strategy associated with kicking physicians they don’t own out of network, and in some cases targeting those same practices for acquisition. Aetna and Humana recently told investors they will be reviewing their networks of physicians, signaling they’ll soon be further narrowing their networks. A good question for this task force: when insurers review those contracts with doctors, do they ever kick the doctors they employ out of network? (Doubtful.) This could specifically draw attention from the task force’s focus on “health care contract language and other practices that restrict competition,” such as contract provisions that require or encourage patients to seek care from doctors directly employed or closely controlled by patients’ insurers.

Additionally, UnitedHealth CEO Andrew Witty recently told analysts, “As I think you see some of the funding changes play out across the — across the next few years, I suspect that may also create new opportunities for us as different companies assess their positions.” My translation: UnitedHealth’s burdensome business practices and the way it shortchanges doctors (those “funding changes” he referenced) contribute to the financial distress that is forcing many health care providers to “assess their positions.”

As the task force continues to consider the impact of private equity in health care monopolies, transactions like this one should receive equal consideration for their lack of transparency and overall impact on market consolidation.

2. Co-mingling of middlemen

I have watched with interest for over the past year as both Democrats and Republicans in Washington increasingly trained their fire on pharmacy benefit managers. The natural next area of focus in that space, which this new task force could advance, should be around how the

three PBMs that control 80 percent of market share are all combined with health insurance companies – namely CVS/Aetna (Caremark), UnitedHealth (Optum Rx), and Cigna (Express Scripts).

An important, and politically popular, area where this consolidation has played out is in the squeeze placed on small, independent pharmacists across the country. More than 300 community pharmacies have closed in the past year alone, out of an inability to operate or push back on unfair margins pushed by these PBM-insurer monopolies. As we have written here, the fees these PBMs charge have increased more than 100,000 percent over the past decade, and are quietly contributing significantly to the profits of the largest health insurers.

We still have little insight into how these business lines interact with each other, and the ultimate impact that has on patients. Given the enormous influence just three insurance companies have over what prescriptions Americans can receive, and how much should be paid for each prescription, the task force would do well to focus on what insurers and PBMs are doing behind the scenes to maximize profits and limit patient access to prescription drugs. It’s already gaining traction on Capitol Hill, with one Congressman recently saying, “I’ll continue to bust this up … this vertical integration in health care.”

3. Prior authorization requests

CVS/Aetna shares were hammered after the company reported a significant increase in payment of Medicare Advantage claims during the first three month is of this year. Expect all insurers to notice. And as they have seen their forecasts fall short of Wall Street’s expectations – particularly because of increasing scrutiny in Washington of Medicare Advantage – these corporations will look to increase their already aggressive use of prior authorization to limit claims payments.

It is not as though insurers make seeking the care you need easy. Far from it. Prior authorization has become “medical injustice disguised as paperwork,” as the New York Times said in a recent, excellent video detailing the widespread nature of this profiteering practice.

While not a stated direct focus of this task force, the increased impact of prior authorization in care delivery is a direct outgrowth of a few large health insurers effectively controlling the marketplace. As insurers directly employ more doctors and enroll more Americans in their plans, they can use prior authorization to increasingly determine whether a patient can get care, period.

Scrutiny in this space could add momentum to increasing activity in state legislatures and Washington to rein in excessive prior authorization. As of early March, nine states and the District of Columbia had passed bills to limit how far insurers could go with prior authorization. And earlier this year, the Centers for Medicare and Medicaid released a final rule that is expected to save physicians $15 billion over the next decade by putting limits on insurer prior authorization tactics.

4. Rising out-of-pocket costs

Regular readers of this newsletter know one of my crusades is to ensure folks who pay good money for health insurance – out of their paychecks or through their tax dollars – can use it when they need it. It was a big win earlier this year for the Lower Out of Pockets Now coalition (which I lead) when President Biden called for a cap on prescription drug out-of-pocket costs of $2,000 annually for everybody, not just Medicare beneficiaries.

If there was true competition and real consumer choice in health insurance, payers wouldn’t be able to get away with increasingly shifting patients into high-deductible plans. But the fact that a few big players control the health insurance market has allowed the oligopoly of payers to do just that, with ever-rising deductibles alongside ever-rising premiums.

The task force’s focus on price fixing, collusion, and transparency in health care costs will, I hope, include some focus on how insurers use their size and clout to drive up out-of-pocket costs and premiums simultaneously – with little recourse to employers or their employees.

5. Implementing crystal clear laws and rules in health care

You know you’re a monopoly or close to it when you can pretty much do whatever you want and get away with it. Look no further than America’s health insurance companies and implementation of the No Surprises Act.

As I wrote earlier this year, Congress and CMS have been clear about how out-of-network hospital bills should be negotiated between insurers and physicians. Yet in case after case, including many that have become the basis of lawsuits, insurers are clearly flouting the Act passed by Congress and the rules promulgated by CMS. Payers are doing this, doctors have said, simply because of their size and ability to weather criticism from physicians, regulators, and the courts – while doctors struggle to pay their bills with significant payments still owed pending out-of-network negotiations with insurers.

One would hope, at a minimum, this task force, focused on rooting out the ills of monopolies, would document how insurers are well aware of how they are supposed to implement legislation like the No Surprises Act, but flout it anyway.