Were you better off in 2022 than you were in 2017? I was for a lot of reasons. One thing that didn’t change over those five years, though, was my health insurance status. I had health insurance in 2017, and I had health insurance in 2022. And I still have health insurance today.

So do most Americans. In fact, according to the U.S. Census Bureau’s latest report on health insurance coverage in the U.S., 92.1% of us had some form of health insurance in 2022. That’s about 304 million people, per the report.

Conversely, 7.9% of us were uninsured last year. That’s a little more than 25.9 million people. That’s down from 8.3% and about 27.2 million people in 2021.

Some may see the decrease in both the percentage and number of uninsured as good news. And it is. Any time the uninsured figures go down, that’s good.

The bad news is, we’re back where we were in 2017. That’s also when 7.9% of us, or about 25.6 million people, were uninsured. Five years of trying to get more people insured and nothing to show for it.

The number of people with any type of private health insurance (employer-based or direct-purchase) crept up to 216.5 million last year from 216.4 million in 2021. The number of people with any type of public health insurance (Medicare, Medicaid, etc.) rose to 119.1 million last year from 117.1 million in 2021. Both headed in the right direction but too slow to push the uninsured rate significantly down.

If we want to get serious about achieving universal coverage, let’s get serious about it. If we don’t want to get serious about it because most of us already have health insurance, the only useful purpose of the Census Bureau’s annual reports on health insurance is to show us how little we really care.

As 41% of American adults face medical debt, residents of this southern Colorado city contend their local nonprofit hospitals aren’t providing enough charity care to justify the millions in tax breaks they receive.

The two hospitals in Pueblo, Parkview Medical Center and Centura St. Mary-Corwin, do not pay most federal or state taxes. In exchange for the tax break, they are required to spend money to improve the health of their communities, including providing free care to those who can’t afford their medical bills. Although the hospitals report tens of millions in annual community benefit spending, the vast majority of that is not spent on the types of things advocates and researchers contend actually create community benefits, such as charity care.

And this month, four U.S. senators called on the Treasury’s inspector general for tax administration and the Internal Revenue Service to evaluate nonprofit hospitals’ compliance with tax-exempt requirements and provide information on oversight efforts.

The average hospital in the U.S. spends 1.9% of its operating expenses on charity care, according to an analysis of 2021 data by Johns Hopkins University health policy professor Ge Bai. Last year, Parkview provided 0.75% of its operating expenses, about $4.2 million, in free care.

Centura Health, a chain of 20 tax-exempt hospitals, reports its community benefit spending to the federal government in aggregate and does not break out specific numbers for individual hospitals. But St. Mary-Corwin reported $2.3 million in charity care in fiscal year 2022, according to its state filing. The filing does not specify the hospital’s operating expenses.

The low levels of charity care have translated into more debt for low-income residents.

About 15% of people in Pueblo County have medical debt in collections, compared with 11% statewide and 13% nationwide, according to 2022 data from the Urban Institute. Those Puebloans have median medical debt of $975, about 40% higher than in Colorado and the U.S. as a whole. And all of those numbers are worse for people of color.

“How far into debt do people have to go to get any kind of relief?” said Theresa Trujillo, co-executive director at the Center for Health Progress’ Pueblo office. “Once you understand that there are tens of millions of dollars every single year that hospitals are extracting from our communities that are meant to be reinvested in our communities, you can’t go back from that without saying, ‘Oh my gosh, that is a thread we need to pull on.’”

Trujillo is organizing a group of fed-up residents to engage both hospitals on their community benefit spending. The group of at least a dozen residents believe the hospitals are ignoring the needs identified by the community — things like housing, addiction treatment, behavioral health care, and youth activities — and instead spending those dollars on things that mainly benefit the hospitals and their staffs.

For the fiscal year ending June 2022, with total revenue of $593 million, Parkview reported $100 million in community benefit spending. But most of that — more than $77 million — represented the difference between the hospital’s cost of providing care and what Medicaid paid for it.

IRS guidelines allow hospitals to claim Medicaid shortfall as a community benefit, but many academics and health policy experts argue such balance sheet shifts aren’t the same as providing charity care to patients.

Parkview also reported $4.7 million for educating its medical staff and $143,000 in incentives to recruit health professionals as community benefit. The hospital spent only $44,000 on community health improvement projects, which appear to have consisted mainly of launching a new mobile app to streamline appointments and referrals.

Meanwhile, the hospital recently spent $58 million on a new orthopedic facility and $43 million on a new cancer center. Parkview also wrote off $39 million in bad debt in fiscal 2022, although that is different from charity care. The bad debt is money the hospitals tried to collect from patients and ultimately decided they’d never get. But by that time, those patients would likely have been sent to collections and potentially had their credit damaged. And outstanding debt often keeps patients from seeking other needed care.

There is a disconnect between what the community said its biggest health needs were and where Parkview directed its spending. The hospital’s community needs assessment pegged access to care as the top concern, and the hospital said it launched the phone app in response.

The second-largest perceived health need was addressing alcohol and drug use. Yet, the only initiative Parkview cited in response was posting preventive health videos online, including some on alcohol and drug use. Meanwhile, the hospital shut down its inpatient psychiatric unit.

Parkview declined to answer questions about its charity care spending, but hospital spokesperson Todd Seip emailed a statement saying the hospital system “has been committed to providing extensive charity care to our community.”

Seip noted that 80% of Parkview’s patients are covered by Medicare or Medicaid, which pay lower rates than commercial insurance. The hospital posted a net loss of $6.7 million in the 2022 fiscal year, although its charity care wasn’t appreciably higher in previous years in which it posted a net gain.

Centura St. Mary-Corwin reported $16 million in Medicaid shortfall and $2 million in medical staff education in 2022, according to its state filing. The hospital spent about $38,000 for its community health improvement projects, primarily on emergency medical services outreach programs in rural areas. The hospital provided another $96,000 in services, mainly to promote covid-19 vaccination.

Centura also declined to answer questions about its charity care spending. Hospital spokesperson Lindsay Radford emailed a statement saying St. Mary-Corwin was aligning its community health needs assessment process with the Pueblo Department of Public Health and Environment “to develop shared implementation strategies for our community benefit funds, ensuring the resources are targeting the highest needs.”

Trujillo questioned how the hospital has conducted its community health assessments, relying on a social media poll to identify needs. After community members identified 12 concerns, she said, hospital leaders chose their priorities from the list.

“They talk about a community garden like they’re feeding the whole south side of the community,” Trujillo said. The hospital established a community garden in 2021, with 20 beds that could be adopted by residents to grow vegetables. Trujillo did praise the hospital for converting part of its building into dorms for a community college nursing program.

Trujillo’s group has spent much of the summer researching hospital charity spending and showing up at public meetings to have their views heard. They are working to gain seats on hospital and other state boards that influence how community benefit dollars are spent, and are urging hospitals to reconfigure their boards to better represent the demographics of their communities.

“We’ve made folks now aware that we want to be a part of those processes,” Trujillo said. “We’re willing to help them reach deeper into the community.”

Tax-exempt hospitals have been under increased state scrutiny for their charitable spending, especially after the Affordable Care Act and Medicaid expansion drove down the uninsured rate. That in turn cut the amount of care hospitals had to provide without being paid, potentially freeing up money to help more people without insurance or with high-deductible plans.

In Colorado, hospitals’ charity care spending and bad debt write-offs dropped from an average of $680 million a year in the five years prior to the ACA being fully implemented in 2014 to an average of $337 million in the years after, according to the Colorado Healthcare Affordability and Sustainability Enterprise Board, a state advisory group.

In states like Colorado, which used federal funding to expand the number of people covered by Medicaid, hospitals shifted more of their community benefit spending to cover Medicaid reimbursement shortfalls.

A January report from Colorado’s Department of Health Care Policy & Financing concluded that payments from public and private health plans help the state’s hospitals make more than enough money to offset lower Medicaid rates and still turn a profit while providing more true charity care.

Colorado has enacted two bills in the past five years to increase the transparency of hospitals’ charitable efforts with new reporting requirements.

“I think overall, we’re pleased with the amount of money that hospitals are reporting they spent,” said Kim Bimestefer, the executive director of the Department of Health Care Policy & Financing. “Is that money being expended in meaningful ways, ways that improve health and well-being of the community? Our reports right now can’t determine that.”

In an era of significant medical debt, rising healthcare costs and delayed treatments, our current healthcare system is ripe for solutions that alleviate the burden of paying patient bills.

Enter embedded finance. While not a new concept by any stretch – it has long existed in retail – fintechs and traditional banks are determined to give patients more options and a fundamentally better experience in the way they pay for healthcare services. In doing so, a financially strained domestic healthcare system stands to benefit from increased cash flow, improved health equity and optimized patient engagement.

Simply put, embedded finance is the integration of financial services – such as payment, lending, banking and insurance features – into another company’s normal service or products. We have all undoubtedly come across these offerings in our daily lives as consumers. Think private label credit cards with retail chains or airlines, digital wallet purchase options at the Amazon checkout, a buynow-pay-later (BNPL) plan from Affirm or Klarna, or insurance obtained from a car rental.

The goal of embedded finance:

is to improve a user’s experience by accessing financial services without leaving a brand’s platform. By layering application programming interface (API)-driven fintech or banking capabilities on top of a website or mobile app for, say, a hospital patient portal, the bundled solution allows the user to stay on one website or application to complete a financial transaction. Doing so removes friction in the experience and delivers a breadth of contextual information that a provider or payer can use to prompt further action on the patient’s medical journey.

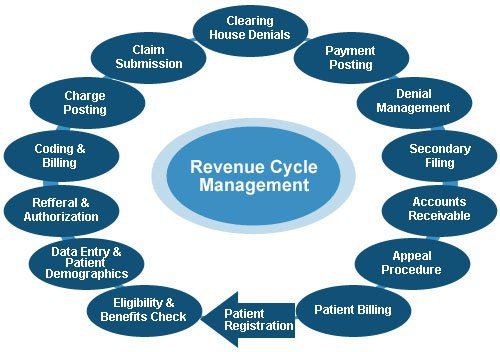

The implications for embedded finance in healthcare are vast and benefit every stakeholder across the revenue cycle value chain:

Patients: Flexibility and convenience to better structure and plan bill payment while receiving greater access to financial options and additional services that improve the care experience such as reminders and health tracking

Providers: Faster and higher rates of collections coupled with ongoing patient dialogue that cements loyalty, affords clinicians the opportunity to suggest customized treatment options, and improves revenue composition and potential valuation

Payers: More efficient claims processing cycle, automated processes and improved data security

The burden of patient bills and increasing medical costs are not new to our system. Yet there has been a confluence of fundamental changes that make embedded finance particularly attractive in healthcare going forward, including increased smartphone usage and Internet penetration, COVID19 adoption of fintech products across healthcare settings, rising inflation rates that reduce a patient’s ability to pay and the adoption of mobile-based apps among younger, digitally native consumers and lower income patients.

These tailwinds support a massive addressable market as healthcare is expected to comprise approximately 23% of a U.S. embedded finance industry set to exceed $230 billion by 2025, or a 10x increase from $23 billion in 2020.

Significant attention and capital investment are accelerating the rise of embedded finance in healthcare.

Punctuated by attractive elements at the intersection of technology, financial services and healthcare sectors, nimble fintech companies and large financial institutions alike are competing for market presence. For example, pioneering healthcare-focused fintech PayZen closed $220 million in fresh capital in late 20223, while banks such as Wells Fargo and Synchrony have launched the popular medical-focused credit cards Health Advantage and CareCredit, respectively. Cain Brothers’ parent company, KeyBank, has also advanced an embedded strategy to provide healthcare digital innovation at scale and enhance patient experiences by acquiring XUP Payments in 2021. The resulting U.S. landscape for healthcare embedded finance is one that is evolving rapidly and that we are monitoring closely for investment and eventual M&A consolidation.

With expanding options around the type of medical care received and where it is received, we expect the financial tools at a patient’s disposal to garner significant attention in the years to come.

Embedded finance is a leading solution positioned to improve health equity and the financial well-being of millions of patients across the U.S., as well as fuel sector growth. Just as we’re accustomed now to buying pretty much anything with a few clicks, so too will embedded finance become a ubiquitous part of the healthcare landscape.

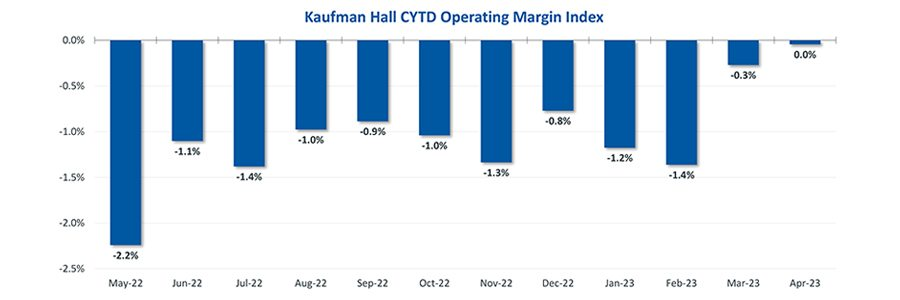

Hospital finances showed signs of stabilizing in May amid slightly improving operating margins, declining expenses and notable increases in outpatient visits.

The median Kaufman Hall Year-To-Date Operating Margin Index reflecting actual margins was 0.3% in May.

The National Hospital Flash Report uses both actual and budget data over the last three years, sampled from more than 900 hospitals on a recurring monthly basis from Syntellis Performance Solutions.

The sample of hospitals for this report is representative of all hospitals in the United States both geographically and by bed size. Additionally, hospitals of all types are represented, from large academic to small critical access. Advanced statistical techniques are used to standardize data, identify and handle outliers, and ensure statistical soundness prior to inclusion in the report.

While this report presents data in the aggregate, Syntellis Performance Solutions also has real-time data down to individual department, jobcode, paytype, and account levels, which can be customized into peer groups for unparalleled comparisons to drive operational decisions and performance improvement initiatives.

Key Takeaways

Hospitals broke even in April. The median operating margin for hospitals was 0% in April, leaving most hospitals with little to no financial wiggle room.

Volumes dropped while lengths of stay increased. Hospital volumes dropped across the board—including inpatient and outpatient. Emergency department volumes were the least affected.

Effects of Medicaid disenrollment could be materializing. Hospitals experienced increases in bad debt and charity care in April. Combined with anemic patient volumes, experts note this data could illustrate the effects of the start of widespread disenrollment from Medicaid following the end of the COVID-19 public health emergency.

Inflation continued to throttle hospital finances. Labor costs jumped in April and the costs of goods and services continued to be well above pre-pandemic levels. Though expenses generally fell in April, revenues declined at a faster rate.

National Non-Operating Results

Key Observations

At their May meeting, the Federal Open Market Committee (FOMC) raised the benchmark borrowing rate another 25 basis points, setting the range to 5.00-5.25% and marking the 10th consecutive hike in the cycle as well as a 16-year high

Fed officials acknowledged discussion of a potential pause in tightening while leaving wiggle room, saying “rates are going to come down” over a long period of time while also warning inflation “continues to run high” and the Fed will be taking a “data-dependent approach”

The consumer price index (CPI) rose 0.4% in April, a 4.9% increase year-over-year, an annual pace of inflation below 5% for the first time in two years

The labor market continued to show resilience in April as U.S. nonfarm payrolls grew by 253,000 and unemployment fell back to a 53-year low of 3.4%

Strong inflation, a robust labor market, continued banking sector woes, and a debt ceiling standoff further complicates credit conditions and may challenge the Fed to stabilize financial markets

Equities in April, as measured by the S&P 500, were up 1.5% in April and 8.6% YTD despite downbeat economic data, reoccurring banking sector fears, and mixed earnings

On April 1st, Medicaid’s pandemic-era continuous enrollment policy began to sunset, kicking off a 14-month window for states to reassess their Medicaid rolls. In this week’s graphic, we highlight new Congressional Budget Office projections showing the impact of Medicaid redeterminations on insurance coverage rates over the next decade for the under-65 population.

The Medicaid and Children’s Health Insurance Program (CHIP) coverage rate is expected to drop from 31 percent of all Americans under 65 in 2023, to 27 percent in 2024.

Meanwhile, after reaching an all-time low in 2023,the under-65 uninsured rate is projected to surpass nine percent in 2024 and climb to over 10 percent by 2033.

While over 15M Americans are expected to lose Medicaid coverage during redeterminations, a majority of those disenrolled will gain health insurance either through an employer-sponsored or non-group plan.

But over 6M people, nearly 40 percent of those losing Medicaid coverage, are projected to become uninsured, erasing nearly half the progress the country has made since 2019 at lowering the uninsured rate.

Minneapolis-based Allina Health System’s move to turn away patients with outstanding debt is a cost-saving measure is not uncommon, according to the Lown Institute.

Allina provides emergency care to indebted patients, but they can be cut off for other services if they have a certain amount of unpaid debt,The New York Times found. A spokesperson for Allina confirmed to the Times that it cut off patients only if they have at least $1,500 of unpaid debt three separate times.

A 2022 investigation from KFF Health News found 55 hospitals allow denials of nonemergency care for patients with medical debt, and 22 said the practice is allowed but not current practice.

Allina’s refusal of care for indebted patients could contribute to medical debt, the Lown Institute said in a June 2 report. Allina is a nonprofit hospital and is required to offer financial assistance to patients who cannot afford services. However, there are no federal regulations regarding how much hospitals have to spend on financial assistance or who can be eligible. When groups refuse care, it can make it harder for patients to get help.

According to the Lown Institute, Allina skirted $266 million in taxes in 2020 from its nonprofit status and spent $57 million on financial assistance and community investment. It could have spent $209 million more to reach its tax exemption value.

This brief examines past-due medical debt among nonelderly adults and their families using nationally representative survey data collected in June 2022. The analysis assesses the share of adults ages 18 to 64 with past-due medical bills owed to hospitals and other health care providers as well as the actions taken by hospitals to collect payment or make bills easier to settle.

It focuses on the experiences of adults with family incomes below and above 250 percent of the federal poverty level (FPL), approximating the income cutoff used by many hospitals to determine eligibility for free and discounted care.

WHY THIS MATTERS

In their efforts to protect patients from medical debt, policymakers have increasingly focused on the role of hospital billing and collection practices, with particular scrutiny directed toward nonprofit hospitals’ provision of charity care. Understanding the experiences of people with past-due bills owed to hospitals and other providers can shed light on the potential for new consumer protections to alleviate debt burdens.

WHAT WE FOUND

More than one in seven nonelderly adults (15.4 percent) live in families with past-due medical debt. Nearly two-thirds of these adults have incomes below 250 percent of FPL.

Nearly three in four adults with past-due medical debt (72.9 percent) reported owing at least some of that debt to hospitals, including 27.9 percent owing hospitals only and 45.1 percent owing both hospitals and other providers. Adults with past-due hospital bills generally have much higher total amounts of debt than those with past-due bills only owed to non-hospital providers.

Most adults (60.9 percent) with past-due hospital bills reported that a collection agency contacted them about the debt, but much smaller shares reported that the hospital filed a lawsuit against them (5.2 percent), garnished their wages (3.9 percent), or seized funds from a bank account (1.9 percent).

Though about one-third (35.7 percent) of adults with past-due hospital bills reported working out a payment plan, only about one-fifth (21.7 percent) received discounted care.

Adults with incomes below 250 percent of FPL were as likely as those with higher incomes to experience hospital debt collection actions and to have received discounted care.

The concentration of past-due medical debt among families with low incomes and the large share who owe a portion of that debt to hospitals suggests that expanded access to hospital charity care and stronger consumer protections could complement health insurance coverage expansions and other efforts to mitigate the impact of unaffordable medical bills.

HOW WE DID IT

This analysis draws on data from the June 2022 round of the Urban Institute’s Health Reform Monitoring Survey (HRMS), a nationally representative, internet-based survey of adults ages 18 to 64 that provides timely information on health insurance coverage, health care access and affordability, and other health topics. Approximately 9,500 adults participated in the June 2022 HRMS.

About 64% of adults in a Medicaid-enrolled family in December said they did not know they may lose coverage once pandemic-era policy ends and eligibility checks resume on April 1, according to a survey from the Robert Wood Johnson Foundation.

The percentage of respondents who said they heard nothing about upcoming Medicaid renewals rose from June, when 62% said they knew nothing about the changes, the survey found.

Awareness was low across the board regardless of geographic region or a state’s Medicaid expansion status, according to the survey.

Dive Insight:

The federal government barred states from resuming Medicaid eligibility checks amid widespread job losses and other challenges during the pandemic.

Once eligibility checks resume, as many as 18 million people are expected to lose coverage, according to the Robert Wood Johnson Foundation.

About 7 million of those people are expected to gain coverage through the individual markets or employer-sponsored plans, though 8 million will not and will likely become uninsured, according to a report from Moody’s Investor Services.

Awareness levels regarding looming redetermination checks remained low and varied only slightly regionally, the report found.

Similarly, above 60% of respondents reported unawareness of Medicaid redeterminations both in Medicaid expansion states and those that haven’t expanded Medicaid, “which suggests the need for widespread outreach and education efforts,” the report said.

“Reducing information gaps about the change is a critical first step,” the report said.

In non-expansion states, people will need help learning about navigating marketplace options, while in expansion states they’ll need information on how to stay enrolled, the report said.

The suspension of eligibility checks led Medicaid membership to rise substantially during the pandemic, growing from 70.7 million members in February 2020 to 90.9 million in September, according to the Moody’s Investor Services report.

The end of the policy is expected to deal a blow to payers that have touted recent enrollment growth while hospitals could see more self-pay patients and “higher bad debt” for facilities, the Moody’s report said.

Drawing on a report published by the North Carolina State Health Plan for Teachers and State Employees, a recent Kaiser Health News article shines a light on the lack of transparency in financial reporting of not-for-profit hospitals’ community benefit obligations.

The report claims many North Carolina hospitals—including the state’s largest system, Atrium Health—show profits on Medicare patients in their cost report filings, while at the same time claiming sizable unrecouped losses on Medicare patients as a part of their overall community benefit analyses.

The Gist: These kind of reporting discrepancies draw attention to the controversial issue of whether not-for-profit hospitals provide sufficient community benefit to compensate for their tax-exempt status, which was worth nearly $2 billion in 2020 for North Carolina hospitals alone.

Greater transparency around charity care, community benefit, and losses sustained from public payerscould go a long way toward shoring up stakeholder support for not-for-profit institutions at a time when their political goodwill has deteriorated. Hospitals should be proactive on this front, as political leaders increasingly train their sites on high hospital spending in the current tight economic environment.

Revenue cycle challenges “seem to have intensified over the past year,” according to Kaufman Hall’s “2022 State of Healthcare Performance Improvement” report, released Oct. 18.

The consulting firm said that in 2021, 25 percent of survey respondents said they had not seen any pandemic-related effects on their respective revenue cycles. This year, only 7 percent said they saw no effects.

The findings in Kaufman Hall’s report are based on survey responses from 86 hospital and health system leaders across the U.S.

Here are the top five ways leaders said the pandemic affected the revenue cycle in 2022:

1. Increased rate claim denials — 67 percent

2. Change in payer mix: Lower percentage of commercially insured patients — 51 percent

3. Increase in bad debt/uncompensated care — 41 percent

4. Change in payer mix: Higher percentage of Medicaid patients — 35 percent

5. Change in payer mix: Higher percentage of self-pay or uninsured patients — 31 percent