MA pays 10% to 15% less than what is paid by the government in original Medicare, report says.

A new study confirms what the American Medical Association and other medical groups have long been saying about physician pay: Medicare reimbursement is not keeping up with inflation.

In original Medicare, doctors are paid one-third less than a decade ago, the report said. Medicare reimbursement rates for outpatient procedures have decreased every year since 2016, for an overall decline of 10%.

Over the same period, inflation has risen by almost 30%, according to the report.

The report also sheds light on Medicare Advantage reimbursement. Medicare Advantage plans pay physicians an estimated 10% to 15% less than what is paid by the government in traditional Medicare, according to the 2025 Omniscient Health Physician Medicare Income Report.

This can create negative margins for physicians considering MA plans take roughly twice as long to reimburse providers compared to original Medicare along with factoring in prior authorization and denials, the report said.

An estimated 54% of Medicare beneficiaries are enrolled in a MA plan.

WHY THIS MATTERS

The MA reimbursement gap is driving shifts in network participation. A 2024 survey by the Healthcare Financial Management Association found that 19% of health systems have stopped accepting at least one MA plan, with another 61% planning to do so or actively considering it, according to the Omniscient report.

“Despite the rising demand for care from an aging U.S. population, the financial strain is forcing physicians to rethink whether they will continue serving Medicare patients,” said Meade Monger, CEO of Omniscient Health, a healthcare data science company. “High-volume Medicare practices, especially those in primary care and rural areas, are increasingly unable to sustain operations under current revenue structures.”

The federal government’s push toward streamlining and speeding up the prior authorization process and requiring an electronic process over paper represents improvement, the report said. Some insurers have announced plans to decrease the number of procedures that require prior auth.

But payment rates need to change, said Omniscient, which recommends policymakers index Medicare reimbursement rates to inflation and set payment standards for MA plans.

THE LARGER TREND

On Tuesday, the American Medical Association released what it called flawed proposals in the Centers for Medicare and Medicaid Services’ physician payment rule released in July.

Despite getting a 3.6% payment boost after five consecutive years of cuts, physician pay, after adjusting for practice-cost inflation, has plummeted since 2001, the AMA said.

The proposed 2026 Medicare Physician Fee Schedule includes a 2.5% cut in work relative-value units (RVUs, which measure a physician’s time, technical skill, mental effort, decision-making and stress) and physician intraservice time for most services, the AMA said. This reduction would affect 95% of the services that doctors provide.

The cut is based on an assumption of greater efficiency and less time involved for each service, an assumption that is not grounded in new data or physician input, the AMA said.

CMS also proposes a reduction in practice-expense RVUs, which are the costs of running a practice, such as staff, equipment, supplies, utilities and overhead.

The bottom line, the AMA said, is that physician payment for services performed in a facility will drop overall by 7%.

CMS is accepting comments on its proposed rule until Sept. 12.

This week, the House Energy and Commerce and Ways and Means Committees begins work on the reconciliation bill they hope to complete by Memorial Day. Healthcare cuts are expected to figure prominently in the committee’s work.

And in San Diego, America’s Physician Groups (APG) will host its spring meeting “Kickstarting Accountable Care: Innovations for an Urgent Future” featuring Presidential historian Dorris Kearns Goodwin and new CMS Innovation Center Director Abe Sutton. Its focus will be the immediate future of value-based programs in Trump Healthcare 2.0, especially accountable care organizations (ACOs) and alternative payment models (APMs).

Central to both efforts is the administration’s mandate to reduce federal spending which it deems achievable, in part, by replacing fee for services with value-based payments to providers from the government’s Medicare and Medicaid programs.

The CMS Center for Medicare and Medicaid Innovation (CMMI) is the government’s primary vehicle to test and implement alternative payment programs that reduce federal spending and improve the quality and effectiveness of services simultaneously.

Pledges to replace fee-for-service payments with value-based incentives are not new to Medicare. Twenty-five years ago, they were called “pay for performance” programs and, in 2010, included in the Affordable Care as alternative payment models overseen by CMMI.

But the effectiveness of APMs has been modest at best: of 50+ models attempted, only 6 proved effective in reducing Medicare spending while spending $5.4 billion on the programs. Few were adopted in Medicaid and only a handful by commercial payers and large self-insured employers. Critics argue the APMs were poorly structured, more costly to implement than potential shared savings payments and sometimes more focused on equity and DEI aims than actual savings.

The question is how the Mehmet Oz-Abe Sutten version of CMMI will approach its version of value-based care, given modest APM results historically and the administration’s focus on cost-cutting.

Context is key:

Recent efforts by the Trump Healthcare 2.0 team and its leadership appointments in CMS and CMMI point to a value-agenda will change significantly. Alternative payment models will be fewer and participation by provider groups will be mandated for several. Measures of quality and savings will be fewer, more easily measured and and standardized across more episodes of care. Financial risks and shared savings will be higher and regulatory compliance will be simplified in tandem with restructuring in HHS, CMS and CMMI to improve responsiveness and consistency across federal agencies and programs.

Sutton’s experience as the point for CMMI is significant. Like Adam Boehler, Brad Smith and other top Trump Healthcare 2.0 leaders, he brings prior experience in federal health agencies and operating insight from private equity-backed ventures (Honest Health, Privia, Evergreen Nephrology funded through Nashville-based Rubicon Founders). Sutton’s deals have focused on physician-driven risk-bearing arrangements with Medicare with funding from private investors.

The Trump Healthcare 2.0 team share a view that the healthcare system is unnecessarily expensive and wasteful, overly-regulated and under-performing. They see big hospitals and drug companies as complicit—more concerned about self-protection than consumer engagement and affordability.

They see flawed incentives as a root cause, and believe previous efforts by CMS and CMMI veered inappropriately toward DEI and equity rather than reducing health costs.

And they think physicians organized into risk bearing structures with shared incentives, point of care technologies and dependable data will reduce unnecessary utilization (spending) and improve care for patients (including access and affordability).

There’s will be a more aggressive approach to spending reduction and value-creation with Medicare as the focus: stronger alternative payment models and expansion of Medicare Advantage will book-end their collective efforts as Trump Healthcare 2.0 seeks cost-reduction in Medicare.

What’s ahead?

Trump Healthcare 2.0 value-based care is a take-no prisoners strategy in which private insurers in Medicare Advantage have a seat at their table alongside hospitals that sponsor ACOs and distribute the majority of shared savings to the practicing physicians. But the agenda will be set, and re-set by the administration and link-minded physician organizations like America’s Physician Groups and others that welcome financial risk-sharing with Medicare and beyond.

The results of the Trump Healthcare 2.0 value agenda will be unknown to voters in the November 2026 mid-term but apparent by the Presidential campaign in 2028. In the interim, surrogate measures for performance—like physician participation and projected savings–will be used to show progress and the administration will claim success. It will also spark criticism especially from providers who believe access to needed specialty care will be restricted, public and rural health advocates whose funding is threatened, teaching and clinical research organizations who facing DOGE cuts and regulatory uncertainty, patient’s right advocacy groups fearing lack of attention and private payers lacking scalable experience in Medicare Advantage and risk-based relationships with physicians.

Last week, the American Medical Association named Dr. John Whyte its next President replacing widely-respected 12-year CEO/EVP Jim Madara. When he assumes this office in July, he’ll inherit an association that has historically steered clear of major policy issues but the administration’s value-based care agenda will quickly require his attention.

Physicians including AMA members are restless:

At last fall’s House of Delegates (HOD), members passed a resolution calling for constraints on not-for-profit hospital’ tax exemptions due to misleading community benefits reporting and more consistency in charity care reporting by all hospitals.

The majority of practicing physicians are burned-out due to loss of clinical autonomy and income pressures—especially the 75% who are employees of hospitals and private-equity backed groups. And last week, the American College of Physicians went on record favoring “collective action” to remedy physician grievances. All impact the execution of the administration’s value-based agenda.

Arguably, the most important key to success for the Trump Healthcare 2.0 is its value agenda and physician support—especially the primary care physicians on whom the consumer engagement and appropriate utilization is based. It’s a tall order.

The Trump Healthcare 2.0 value agenda is focused on near-term spending reductions in Medicare. Savings in federal spending for Medicaid will come thru reconciliation efforts in Congress that will likely include work-requirements for enrollees, elimination of subsidies for low-income adults and drug formulary restrictions among others. And, at least for the time being, attention to those with private insurance will be on the back burner, though the administration favors insurance reforms adding flexible options for individuals and small groups.

The Trump Healthcare 2.0 value-agenda is disruptive, aggressive and opportunistic for physician organizations and their partners who embrace performance risk as a permanent replacement for fee for service healthcare. It’s a threat to those that don’t.

In my report June 10, I wrote: “The major sources of physician discontent are administrative hassles and unwelcome clinical oversight that create dissonance. They conflict with a false sense of autonomy that the majority of physicians imagined when choosing medicine. Cuts to reimbursement, participation in alternative payment models and medical inflation are manifestations of a system in which ‘suits’ are intruders who make rules, exact handsome salaries, generate corporate profits and distance physicians from patient care purposely… “

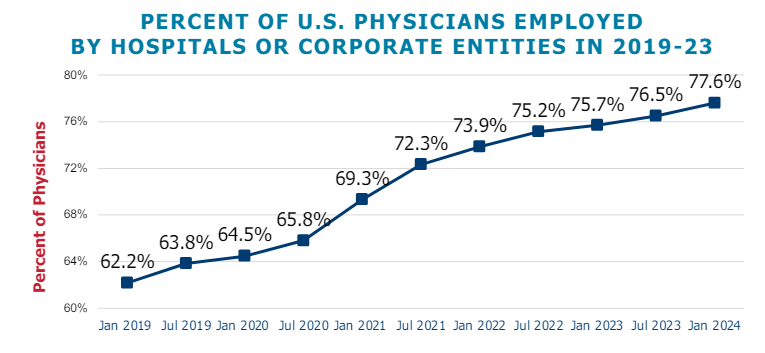

This assessment remains true today. Discontent among physicians is palpable and it’s magnified by a growing sense of financial despair among many clinicians. And it poses a unique challenge to hospitals that now employ more than half of America’s physician workforce.

In the “good ole days”, hospitals provided a place for physicians to ply their trade. They were credentialled to practice their chosen specialty, granted special parking, food and amenities and treated as the hospital’s most welcome customer. Made sense: physicians controlled most patient decisions about the hospital services they use. Physicians controlled the hospital’s revenue, sustainability and bonuses earned by administrators. Insurers brought privately-insured patients to doctors who charged them 1.6-2.5 times what Medicare paid and physician income was not threatened. That was then. This is now.

Today, insurers play a larger role. Consumer expectations have changed. Policymakers are paying more attention. And demand has shifted from inpatient services to outpatient, home and office settings for health and wellbeing services in addition to acute care. And the current forecast by CMS through 2032 predicts spending for hospitals will increase at a compound rate of 5.7% vs. 5.6% for physicians adding more hospital-physician financial tension to the system. Both well-above inflation and CDP growth prompting heightened pressure to spend less.

In anticipation, consolidation of hospitals into multi-hospital systems has been a staple in recent years: only 1 in 5 hospitals is independent these days, and most of these are small, rural or otherwise destined to independence for their uncertain future. Whether public, investor-owned or not-for-profit (or tax exempt as some prefer), the economic realities of running hospitals coupled with the regulatory constraints imposed by state and federal law forced all to re-think their future.And, for most, employing physicians directly was a means to an end of staying alive while the dust settles.

But the unintended consequence of physician employment is soured relationships between the employed physicians and their hospital:

their financial and emotional security has become tangled up by interactions with hospital leaders and former peers appointed to oversee their work.

And their views about their hospital have morphed to negativity based on four underlying beliefs:

Hospitals spend too much on overhead and executive salaries and not enough on direct patient care.

Hospitals are run poorly: we could run them better but they don’t listen to us.

Hospitals get rate increases from Medicare and physicians get screwed.

Hospitals need us more than we need them. But they don’t understand that.

On March 9, 2024, President Biden signed the Consolidated Appropriations Act, 2024, which included a 2.93% update to the CY 2024 Physician Fee Schedule (PFS) Conversion Factor (CF) for dates of service March 9 through December 31, 2024. But physicians saw that as not enough since their overhead increased even more. And for 2025, CMS is proposing to reduce average payment rates under the MPFS by2.93% compared to the average amount reimbursed for these services in CY 2024 based on CY 2025 MPFS conversion factor decrease of $0.93 (or 2.8%) from the current CY 2024 conversion factor.

Understandably, physicians are upset. They’re not delusional that private insurers will make up the difference nor imagining hospitals will divert funds their way from brick, stick and tech priorities. But they’re speaking out expressing their views to anyone who’ll listen.

For hospitals that employ physicians, the issue of their financial anxiety requires urgent attention–not as one of many alongside 340B, site neutral payments and others but as the one at the top of the list. The issue is not whether physician income relative to other professions and average households is high. The issue is about managing physician expectations about their livelihood realistically and practically while improving their clinical acumen as professionals.

The core beliefs held by employed physicians about their hospitals may not be fair, objective or accurate, but they’re no less deeply felt and impactful. Hospital boards and C suite leaders would be well-served to refresh plans accordingly.

Following the US Senate Finance Committee’s recent white paper on Medicare physician payment reform, the graphic above shows how Medicare payments to physicians have not kept pace with inflation.

The Medicare physician fee schedule conversion factor, which is used to assign dollar amounts to relative value units, decreased by eight percent between 2000 and 2024.

Over the same period, the Medicare Economic Index (MEI), which measures practice cost inflation, and Consumer Price Index rose 57 percent and 83 percent, respectively. Reductions to the conversion factor contributed to a 20 percent decline in Medicare physician pay relative to practice cost inflation from 2000 to 2021.

Physician practice margins in general have also worsened since COVID, not just due to Medicare payments.

Although net revenue per physician at system-affiliated clinics increased about 10 percent from 2020 to 2023,total expenses per physician rose about 27 percent, driven by a per physician clinical staffing expense increase of nearly the same amount.

Both the Senate Finance Committee’s white paper and a recently introduced House bill suggest tying the Medicare physician fee schedule conversion factor updates to the MEI, either partially or fully, but immediate legislative action in an election year appears unlikely.

In the meantime, physician practices continue to face a difficult operating environment with costs rising faster than revenues.

With a single ruling, the Federal Trade Commission removed the nation’s occupational handcuffs, freeing almost all U.S. workers from non-compete clauses. The medical profession will never be the same.

On April 23, the FTC issued a final rule, affecting not only new hires but also the 30 million Americans currently tethered to non-compete agreements. Scheduled to take effect in September—subject to the outcome of legal challenges by the U.S. Chamber of Commerce and other business groups—the ruling will dismantle longstanding barriers that have kept healthcare professionals from changing jobs.

The FTC projects that eliminating these clauses will boost medical wages, foster greater competition, stimulate job creation and reduce health expenditures by $74 billion to $194 billion over the next decade. This comes at a crucial moment for American healthcare, an industry in which 60% of physicians report burnout and 100 million people (41% of U.S. adults) are saddled with medical bills they cannot afford.

Like all major rulings, this one creates clear winners and losers—outcomes that will reshape careers and, potentially, alter the very structure of U.S. healthcare.

Winners: Newly Trained Clinicians

Undoubtedly, the FTC’s ruling is a win for younger doctors and nurses, many of whom join hospitals and health systems with the promise of future salary increases and more autonomy. However, by agreeing to stringent non-compete clauses, these newly trained clinicians have little choice but to place their trust in employers that, shielded by air-tight agreements, have no fear of breaking their promises.

Most newly trained clinicians enter the medical job market in their late 20s and early 30s, carrying significant student-loan debt—nearly $200,000 for the average doctor. Eager for stable, well-paying positions, these young professionals quickly settle into their careers and communities, forming strong relationships with friends and patients. Many start families.

But when these clinicians realize their jobs are falling short of the promises made early on, they face a tough decision: either endure subpar working conditions or uproot their lives. Taking a new job 25 or 50 miles away or moving to a different state are often are only options to avoid breaching a non-compete clause.

In a 570-page supplement to its ruling, the FTC published testimonials from dozens of healthcare professionals whose lives and careers were harmed by these clauses.

“Healthcare providers feel trapped in their current employment situation, leading to significant burnout that can shorten their career longevity,” said one physician working in rural Appalachia.

By banning non-competes, the FTC’s rule will boost career mobility for all clinicians within their own communities. This change will likely spur competition among employers—leading to improved pay and benefits to attract and, equally important, retain top talent. And with the reassurance that they can easily switch jobs if their current employer falls short of expectations, clinicians will enjoy greater professional satisfaction and less burnout.

Winners: Patients In Competitive Markets

Benefits that accrue to doctors and nurses from the FTC’s ban will translate directly to improved outcomes for patients. For example, we know that physicians who report symptoms of burnout are twice as likely to commit a serious medical error. Studies have shown the inverse is true, as well: healthcare providers who are satisfied with their jobs tend to have lower burnout rates, which is positively correlated with improved patient outcomes.

Once freed from restrictive non-compete clauses, many clinicians will practice elsewhere within the community. To attract patients, they will have to offer greater access, lower prices and more personalized service. Others with the freedom to choose will join outpatient centers that offer convenient and efficient alternatives for diagnostic tests, surgery and urgent medical care, often at a fraction of the cost of traditional hospital services. In both cases, increased competition will give patients improved medical care and added value.

Losers: Large Health Systems

Large health systems, which encompass several hospitals in a geographic area, have traditionally relied on non-compete agreements to maintain their market dominance. By barring high-demand medical professionals such as radiologists and anesthesiologists from joining competitors or starting independent practices, these systems have been able to suppress competition and force insurers to pay more for services.

Currently, these systems can demand high reimbursement rates from insurers while also maintaining relatively low wages for staff, creating a highly profitable model. Yale economist Zack Cooper’s research shows the consequence of the status quo: prices go up and quality declines in highly concentrated hospital markets.

The FTC’s ruling challenges those conditions, potentially dismantling monopolistic market controls. As a result, insurers will no longer be forced to contend with a single, dominant provider. And with health systems pushed to offer better wages and benefits to retain their top talent, bottom lines will shrink.

While nonprofit hospitals and health systems are not currently under the FTC’s jurisdiction, the agency has pointed out that these facilities might be at “a self-inflicted disadvantage in their ability to recruit workers.” Moreover, as Congress intensifies scrutiny on the nonprofit status of U.S. health systems, hospitals that do not voluntarily align with the FTC’s guidelines may find themselves compelled to do so through legislative actions.

Losers: Hospital Administrators

Individual hospitals have faced a unique challenge over the past decade. Across the country, inpatient numbers are falling, which makes it harder for hospital administrators to fill beds overnight. This trend has been driven by advancements in medical technology and new practices that enable more outpatient procedures, along with changes in insurance reimbursements favoring less costly outpatient care. As a result, hospital administrators have been compelled to adapt their financial strategies.

Nowadays, outpatient services account for about half of all hospital revenue. These range from physician consultations to specialized procedures like radiological and cardiac diagnostics, chemotherapy and surgeries.

Medicare and other insurers typically pay hospitals more for these outpatient services than they pay local doctors and other facilities. Knowing this, hospitals are hiring community doctors and acquiring diagnostic and procedural facilities, then boosting profitability by charging the higher hospital rates for the same services.

Hospital administrators know that this strategy only works if the newly hired clinicians are prohibited from quitting and returning to practice within the same community. If they do, their patients are likely to go with them. This is why the non-compete clauses are so essential to a hospital’s financial success.

As expected, the American Hospital Association opposes the FTC’s rule, arguing that non-compete clauses protect proprietary information. In practice, most of the doctors affected by the ban are providing standard medical care and have no proprietary knowledge that requires protection.

Looking Ahead

Today’s hospital systems are starkly divided between haves and have-nots. Facilities in affluent areas often enjoy high reimbursement rates from private insurers, boosting financial success and administrator salaries. In contrast, rural hospitals grapple with low patient volumes while facilities in economically disadvantaged, high-population areas face greater financial difficulties.

The current model is not working. The old ways of doing things—enforcing non-competes, charging higher fees for identical services and promoting market consolidation to hike prices—are not sustainable solutions.

The abolition of non-compete agreements will produce both winners and losers. In the healthcare sector, the ultimate measure of a policy’s impact should be its effect on patients—and the overwhelming evidence suggests that eliminating these clauses will benefit them greatly.

Today is the federal income Tax Day. In 43 states, it’s in addition to their own income tax requirements. Last year, the federal government took in $4.6 trillion and spent $6.2 trillion including $1.9 trillion for its health programs. Overall, 2023 federal revenue decreased 15.5% and spending was down 8.4% from 2022 and the deficit increased to $33.2 trillion. Healthcare spending exceeded social security ($1.351 trillion) and defense spending ($828 billion) and is the federal economy’s biggest expense.

Along with the fragile geopolitical landscape involving relationships with China, Russia and Middle East, federal spending and the economy frame the context for U.S. domestic policies which include its health system. That’s the big picture.

Today also marks the second day of the American Hospital Association annual meeting in DC. The backdrop for this year’s meeting is unusually harsh for its members:

Increased government oversight:

Five committees of Congress and three federal agencies (FTC, DOJ, HHS) are investigating competition and business practices in hospitals, with special attention to the roles of private equity ownership, debt collection policies, price transparency compliance, tax exemptions, workforce diversity, consumer prices and more.

Medicare payment shortfall:

CMS just issued (last week) its IPPS rate adjustment for 2025: a 2.6% bump that falls short of medical inflation and is certain to exacerbate wage pressures in the hospital workforce. Per a Bank of American analysis last week, “it appears healthcare payrolls remain below pre-pandemic trend” with hospitals and nursing homes lagging ambulatory sectors in recovering.”

Persistent negative media coverage:

The financial challenges for Mission (Asheville), Steward (Massachusetts) and others have been attributed to mismanagement and greed by their corporate owners and reports from independent watchdogs (Lown, West Health, Arnold Ventures, Patient Rights Advocate) about hospital tax exemptions, patient safety, community benefits, executive compensation and charity care have amplified unflattering media attention to hospitals.

Physicians discontent:

59% of physicians in the U.S. are employed by hospitals; 18% by private equity-backed investors and the rest are “independent”. All are worried about their income. All think hospitals are wasteful and inefficient. Most think hospital employment is the lesser of evils threatening the future of their profession. And those in private equity-backed settings hope regulators leave them alone so they can survive. As America’s Physician Group CEO Susan Dentzer observed: “we knew we’re always going to need hospitals; but they don’t have to look or operate the way they do now. And they don’t have to be predicated on a revenue model based on people getting more elective surgeries than they actually need. We don’t have to run the system that way; we do run the healthcare system that way currently.”

The Value Agenda in limbo:

Since the Affordable Care Act (2010), the CMS Center for Innovation has sponsored and ultimately disabled all but 6 of its 54+ alternative payment programs. As it turns out, those that have performed best were driven by physician organizations sans hospital control. Last week’s release of “Creating a Sustainable Future for Value-Based Care: A Playbook of Voluntary Best Practices for VBC Payment Arrangements.” By the American Medical Association, the National Association of ACOs (NAACOs) and AHIP, the trade group representing America’s health insurance payers is illustrative. Noticeably not included: the American Hospital Association because value-pursuers think for hospitals it’s all talk.

National insurers hostility:

Large, corporate insurers have intensified reimbursement pressure on hospitals while successfully strengthening their collective grip on the U.S. health insurance sector. 5 insurers control 50% of the U.S. health insurance market: 4 are investor owned. By contrast, the 5 largest hospital systems control 17% of the hospital market: 1 is investor-owned. And bumpy insurer earnings post-pandemic has prompted robust price increases: in 2022 (the last year for complete data and first year post pandemic), medical inflation was 4.0%, hospital prices went up 2.2% but insurer prices increased 5.9%.

Costly capital:

The U.S. economy is in a tricky place: inflation is stuck above 3%, consumer prices are stable and employment is strong. Thus, the Fed is not likely to drop interest rates making hospital debt more costly for hospitals—especially problematic for public, safety net and rural hospitals. The hospital business is capital intense: it needs $$ for technologies, facilities and clinical innovations that treat medical demand. For those dependent on federal funding (i.e. Medicare), it’s unrealistic to think its funding from taxpayers will be adequate. Ditto state and local governments. For those that are credit worthy, capital is accessible from private investors and lenders. For at least half, it’s problematic and for all it’s certain to be more expensive.

Campaign 2024 spotlight:

In Campaign 2024, healthcare affordability is an issue to likely voters. It is noticeably missing among the priorities in the hospital-backed Coalition to Strengthen America’s Healthcare advocacy platform though 8 states have already created “affordability” boards to enact policies to protect consumers from medical debts, surprise hospital bills and more.

Understandably, hospitals argue they’re victims. They depend on AHA, its state associations, and its alliances with FAH, CHA, AEH and other like-minded collaborators to fight against policies that erode their finances i.e. 340B program participation, site-neutral payments and others. They rightfully assert that their 7/24/365 availability is uniquely qualifying for the greater good, but it’s not enough. These battles are fought with energy and resolve, but they do not win the war facing hospitals.

AHA spent more than $30 million last year to influence federal legislation but it’s an uphill battle. 70% of the U.S. population think the health system is flawed and in need of transformative change. Hospitals are its biggest player (30% of total spending), among its most visible and vulnerable to market change.

Some think hospitals can hunker down and weather the storm of these 8 challenges; others think transformative change is needed and many aren’t sure. And all recognize that the future is not a repeat of the past.

For hospitals, including those in DC this week, playing victim is not a strategy. A vision about the future of the health system that’s accessible, affordable and effective and a comprehensive plan inclusive of structural changes and funding is needed. Hospitals should play a leading, but not exclusive, role in this urgently needed effort.

Lacking this, hospitals will be public utilities in a system of health designed and implemented by others.

A new generation of doctors struggling with ever-increasing workloads and crushing student debt is helping drive unionization efforts in a profession that historically hasn’t organized.

Why it matters:

Physicians in training, like their peers in other industries, increasingly see unions as a way to boost their pay and protect themselves against grueling working conditions as they launch their careers.

It also comes amid a wave of unionization and labor actions by nurses and other caregivers across a health care system that’s still dealing with high levels of burnout.

What they’re saying:

“We deserve an increased salary to be able to afford to live in one of the most expensive areas in the United States,” said Ali Duffens, a third-year internal medicine resident at Kaiser Permanente’s San Francisco Medical Center.

She’s among the 400 residents at Kaiser’s Northern California system filing to unionize earlier this month.

Duffens earns about $82,000 per year, while paying $3,000 a month for rent and facing $350,000 in medical school loans.

The big picture:

The Kaiser residents are part of a growing number of younger peers in medicine who have been unionizing in recent years.

The number of medical residents in unions has about doubled to more than 32,000 in three years, per CalMatters.

In the last year, residents at Montefiore Medical Center, Stanford Health Care, George Washington University and the University of Pennsylvania voted to unionize, per WBUR.

“The cost of day care … in a month is about half of my salary in total, and the cost of a nanny is essentially the entirety of my salary,” Leah Rethy, an internal medicine resident with Penn Medicine, told NPR last year.

Residents can work as much as 80 hours per week while earning far less than their older colleagues.

Yes, but: Just about 6%-7% of physicians are estimated to be in unions.

Historically, doctors have thought they could just suck up the long hours and relatively low pay in training as part of the tradition of medicine, said Robert Wachter, chair of the department of medicine at the University of California, San Francisco.

“For a new generation, they look at it and say, ‘That’s crazy. I can’t believe you did that. I want to work hard, but I also want a life and I want a family, and I want a reasonable income,'” he said.

And it’s not just younger doctors.

Those more established in their careers are also unionizing as they see the industry changing in ways that they think undermine their profession.

In recent months, attending physicians at Salem Hospital, owned by Mass General Brigham, and a Cedars Sinai-owned anesthesiology practice filed to unionize.

About 600 doctors at Allina Health in Minnesota and Wisconsin last fall agreed to form what appears to be the largest union of private sector physicians.

Zoom in:

The corporatization of American medicine is seen as a key driver. More than half of all U.S. doctors now work for a health system or large medical group rather than running an independent practice.

This shift has brought heavier workloads and less control over how they care for patients, said John August, director of health care labor relations in the Scheinman Institute on Conflict Resolution at the ILR School at Cornell.

That could mean demands to see more patients, limiting the time that doctors can spend with them.

“What you will hear from them 100% of the time in every conversation they have is they feel that they have lost control over the patient-physician relationship. I mean, every single physician says that now,” August said.

The other side:

Health systems and large practices generally say they value their doctors and the relationships they hold with patients.

Hospitals have also struggled with pandemic-era financial shortfalls, including increasing labor costs.

The bottom line:

While this is a labor issue, it ultimately trickles down to quality and safety for patients, said Rachel Flores, organizing director of the Union of American Physicians and Dentists.

“Patients should care because that’s less time to address their issues,” she said. “Patients should care because there’s not enough staff to support the physician.”

Chronic disinvestment and inadequate training have created a shortage of primary care workers.

As the presidential election nears, issues from the economy to climate change are vying for airtime, yet markedly absent from the headlines is a deepening crisis that threatens the future health and wellbeing of communities nationwide: a primary care sector on the brink of collapse.

Primary care is the cornerstone of community health. It helps us live longer lives, prevents disease and reduces health disparities. It is indispensable to strengthening our nation’s ability to withstand another deadly pandemic or climate disaster. And yet, over 100 million Americans report they lack access to a regular doctor or source of care.

Physicians and patients acutely feel the primary care workforce shortage. In recent interviews we heard an alarming refrain from clinicians and health executives: “I could spend all my time helping friends find doctors accepting new patients.” Another said, “I have 100 open staff positions and am in a bidding war for primary care physicians.”

Just in the past decade, there has been a 36% jump in the share of U.S. children without a usual source of care. Among adults it’s a 21% increase, according to a Milbank report.And with America’s rapidly aging population, access to critical primary care services is only expected to get worse.

Understanding what’s driving America’s primary care workforce shortage is key to finding effective, long-term solutions.

A workforce exodus amid chronic disinvestment

America is not producing enough primary care physicians to meet growing population needs. New primary care physicians are leaving for other fields at alarming rates. In 2021, only 15% of all physicians were practicing outpatient primary care three to five years after residency, according to a Milbank report.

When we look at the disparities in compensation rates and the nation’s chronic disinvestment in primary care, this workforce exodus shouldn’t come as a surprise. Specialists in the U.S. now routinely make two to three times what their primary care colleagues do, creating powerful incentives for physicians in training to “go for the gold.”

Primary care accounts for 35% of healthcare visits but receives only about 5% to 7% of total healthcare expenditures. For context, hospitals account for 30% of healthcare expenditures.Additionally, since 2019, the share of total spending by Medicare, Medicaid and commercial insurers in primary care has steadily declined; Medicare’s share has dropped by 15%, according to Milbank.

Inadequate training, disparities in access

Today, the vast majority of primary care residents train within hospitals and academic health centers, which do not expose them to the needs of underserved communities, nor provide them with the skills needed to successfully practice in challenging, real-world clinical environments. In 2021, only 15% of primary care residents spent a majority of their time training in community settings, outside of hospitals.

Moving forward, the solutions are clear. Congress and both the public and private sectors must work together to enact stronger federal and state policies in three critical primary care areas. First, Medicare and Medicaid physician reimbursement — which has led to our specialty-dominated healthcare system — must become more effective and efficient. We know that inadequate compensation is one reason why many medical students choose not to go into primary care.

Second, the billions in public dollars going to clinician training must be focused on creating a highly skilled primary care workforce with practical experience in community settings. This is essential to meet the complex health needs of our nation’s ever-changing and growing population.

And finally, we need to expand the footprint of community health centers, the linchpin to improving health outcomes in underserved communities. Currently, these centers provide care to 1 in 11 patients around the country, but that number needs to be vastly expanded.

It’s time to strengthen our fragile primary care system to ensure it delivers the comprehensive, affordable care Americans so desperately need. Access to high-quality primary care for everyone should not be an aspiration, but an expectation that we – as a nation – have an urgent duty to fulfill.

A recent engagement with a health system executive team to discuss an underperforming service line uncovered a serious issue that’s becoming more common across the industry.

“Our providers are more productive than ever,” the CFO informed our team, “and yet we keep losing money on the service line.”

After digging into their physician compensation model, we came upon one source of the system’s issue. Because it was incentivizing physician RVUs equally across all payers, its providers responded, quite rationally, by picking up market share where growth was easiest: Medicaid patients, who weren’t generating any margin.

“We recognize that we’ve been employing these physicians as loss leaders in order to generate downstream revenue,” the CFO shared, “but what’s the point of that revenue if there’s no longer any downstream margin?”

The economics of physician employment becomes a tough conversation very quickly; it’s a sensitive topic to many, and one with myriad facets.

But the loss leader physician employment model obviously only works when it produces positive downstream margins.

We’re in a critical window of time, where hospital margins are just beginning to recover as volumes return—but those volumes are not necessarily in the same places as before.

The opportunity is ripe for systems to work closely with their aligned physicians to reexamine the post-pandemic margin picture for individual service lines and ensure incentives are aligning all parties to hit operating margin goals.

Are these kinds of conversations taking place at your health system?

Nearly a quarter of health systems are appointing new executives to lead provider compensation — a function previously headed by COOs and CFOs, according to a recent report shared with Becker’s.

That stat comes from the American Association of Provider Compensation Professionals, which recently surveyed 75 U.S. health systems and medical groups to learn more about their management methods.

Health systems have been expanding their provider networks since the late 2000s and are continuing to work toward alignment, according to the report. Previously, COOs and CFOs might have led provider compensation strategy — but the arena has grown too complex and calls for an executive presence of its own.

As such, a number of roles specific to provider compensation have emerged, from the executive director level up to the senior vice presidency. Nearly 25% of health systems surveyed have created a new executive position to develop and lead a provider compensation department; 93% of these departments have sole responsibility for their organization’s compensation design and 84% have full control of compensation strategy, from management of fair market value to contract management.

“The core function of this new resource, department, and team was to build and manage compensation models developed for physicians. For many organizations, this expanded to include advanced practice providers,” the report says. “Over the years, organizations have understood the role to be much more strategic than initially proposed, which is why organizations across the country have developed roles [specific to provider compensation].”