The Federal Reserve cut its target interest rate Wednesday by an extra-large half-percentage point and projected more rate cuts this year and next, as its period of trying to put brakes on the economy to fight inflation comes to a close.

Why it matters:

The move lowers borrowing costs for consumers and businesses, as the central bank aims to keep the economy’s expansion going strong amid warning signs on the outlook.

What they’re saying:

“The labor market is actually in solid condition — and our intention with our policy move today is to keep it there,” Fed chair Jerome Powell told reporters at a press conference on Wednesday.

- “The U.S. economy is in good shape. It’s growing at a solid pace,” Powell added. “We want to keep it there.”

Zoom in:

The rate cut reflects the U.S. entering a new phase where the softening job market is the predominant economic risk — rather than elevated inflation.

- By going with an aggressive half-point cut instead of its more traditional quarter-point adjustment, the Fed moved to get ahead of some evident faltering in the job market.

- However, new projections imply the Fed will shift toward smaller quarter-point rate cuts from here.

- The cut also thrusts the Fed into election-year politics, as former President Trump has said the central bank should not ease monetary policy mere weeks before the election. Some Democrats have called for even more aggressive rate cuts.

Driving the news:

The policy-setting Federal Open Market Committee lowered its target range for the federal funds rate to 4.75%–5%, from the 5.25–5.5% range in place since last July.

- The central bank also released new projections that anticipated the rate will be cut an additional half-point by December — implying a quarter-point cut at each of its two remaining 2024 meetings.

- The median Fed officials anticipated their target rate will be down to 3.4% by the end of 2025, which implies four quarter-point rate cuts next year.

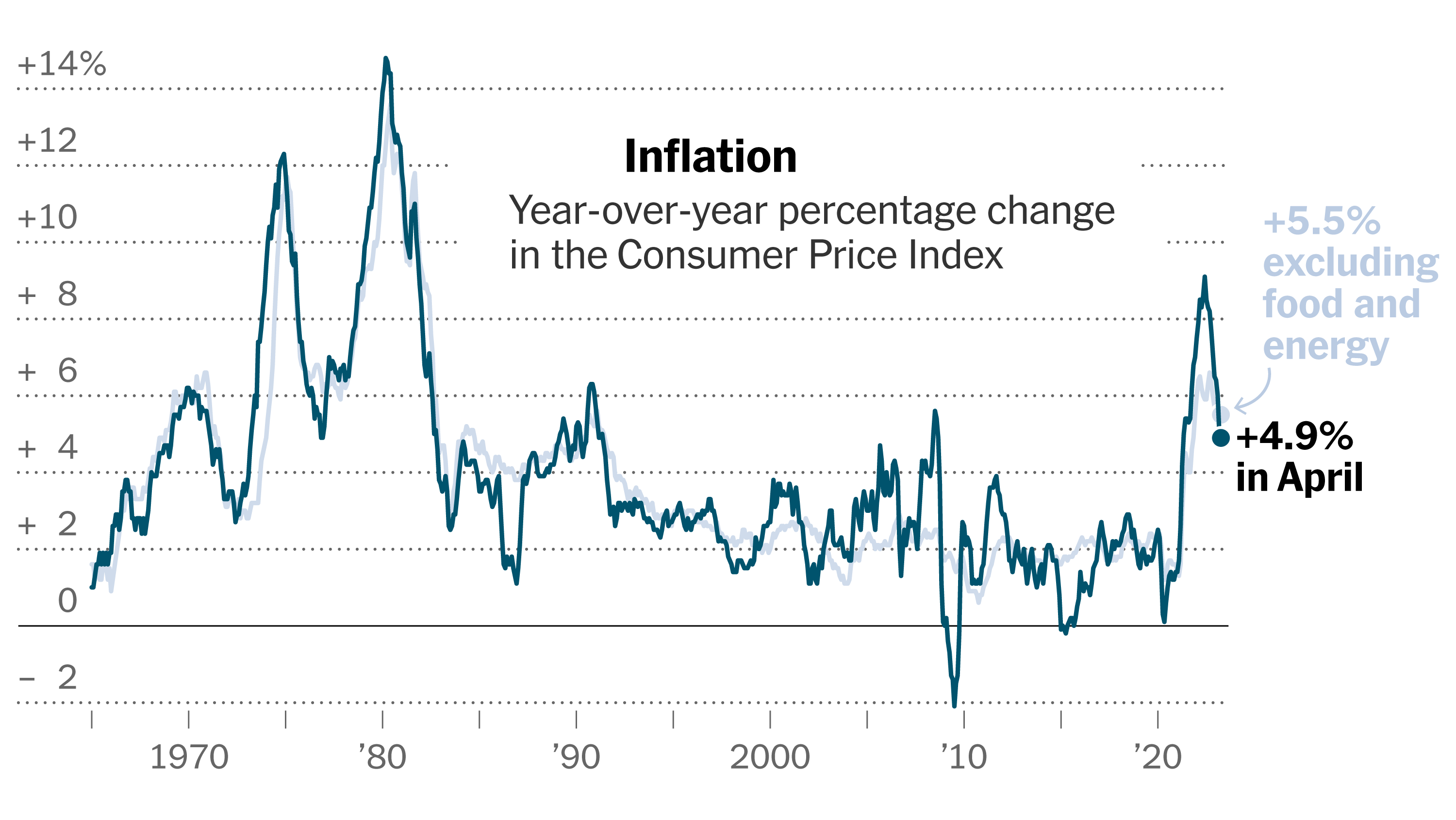

- “Job gains have slowed,” the Fed’s policy statement noted, adding that the committee “has gained greater confidence that inflation is moving sustainably toward 2 percent.”

Of note:

The Fed policy meeting marked the first dissent from a board member in more than two years. Michelle Bowman, a Trump-appointed governor who focuses on community banking issues, preferred to cut by only a quarter point.

- Bowman’s dissent is also the first by a member of the Fed’s seven-member Board of Governors — as opposed to a regional Fed bank president — since 2005.

- Christopher Waller, the other Trump-appointed governor on the board, supported the action.

By the numbers:

The median official saw inflation for the full year coming in at 2.3%, not far from the Fed’s 2% target. By contrast, in June, officials saw 2.6% inflation this year.

- They also anticipate slightly higher unemployment. The projections listed a 4.4% unemployment rate in the final quarter of the year. That rate was 4.2% in August, up from 3.7% at the start of the year.

- However, the Fed officials’ forecasts also imply the jobless rate leveling out at that point and being flat at 4.4% in the final months of 2025.

The bottom line:

Powell and his colleagues elected to take more aggressive action Wednesday in hopes that it will be enough to forestall any further deterioration in the job market of the sort seen over the last few months — and is betting that the Fed can move to a more gradualist approach from here.

- Speaking about the larger-than-anticipated rate cut, Powell said he was pleased the Fed made a strong start in lowering interest rates.

- “The logic of this — both from an economic standpoint and also from a risk management standpoint — was clear,” Powell said.

- He added: “We’re gonna take it meeting by meeting. … There’s no sense that the committee feels it’s in a rush to do this.”