The US labor market added more jobs than expected in May defying previous signs of a slowdown in the economy.

Data from the Bureau of Labor Statistics released Friday showed the labor market added 272,000 nonfarm payroll jobs in May, significantly more additions than the 180,000 expected by economists.

Meanwhile, the unemployment rate rose to 4% from 3.9% the month prior. May’s job additions came in significantly higher than the 165,000 jobs added in April.

The print highlights the difficulty the Federal Reserve faces in determining when to lower interest rates and how quickly. The economy and labor market has held up overall, and inflation has remained sticky, building the case for holding rates higher for longer. Yet some cracks have emerged, such as signs of inflation pressuring lower income consumers and rising household debt.

“They’re really walking a tight rope here,” Robert Sockin, Citi senior global economist, told Yahoo Finance of the central bank. He noted the longer the Fed holds rates steady, the more cracks could develop in the economy.

Wages, considered an important metric for inflation pressures, increased 4.1% year over year, reversing a downward trend in year-over-year growth from the month prior. On a monthly basis, wages increased 0.4%, an increase from the previous month’s 0.2% gain.

“To see more confidence that inflation could move lower over time, you’d really like to see the wage numbers look a little lower than we’ve seen them today,” Lauren Goodwin, New York Life Investments economist and chief market strategist, told Yahoo Finance.

Also in Friday’s report, the labor force participation rate slipped to 62.5% from 62.7% the month prior. However, participation among prime-age workers, ages 25-54, rose to 83.6%, its highest level in 22 years.

The largest jobs increases in Friday’s report were seen in healthcare, which added 68,000 jobs in. May. Meanwhile, government employment added 43,000 jobs. Leisure and hospitality added 42,000 jobs.

The report comes as the stock market has hit record highs amid a slew of softer-than-expected economic data, which had increased investor confidence that the Federal Reserve could cut interest rates as of September. After Friday’s labor report, that trend reversed with investors pricing in a 53% chance the Fed cuts rates in September, down from a roughly 69% chance seen just a day prior, per the CME FedWatch Tool.

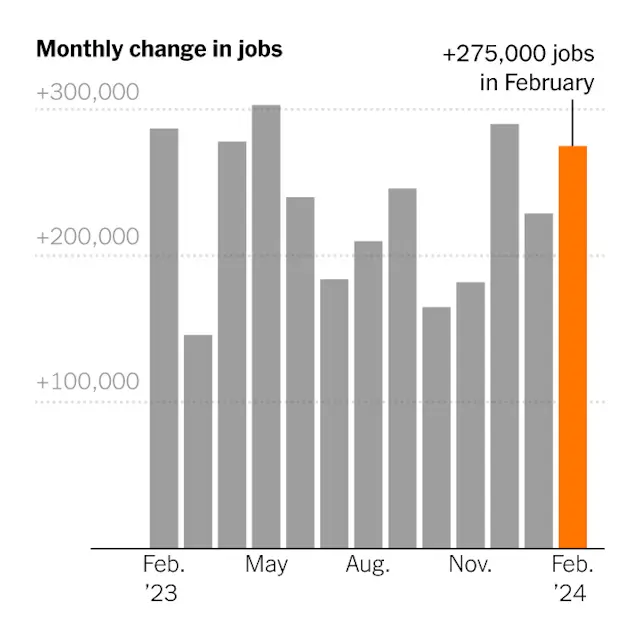

The labor market showed resiliency in February, adding 275,000 jobs, a sign that economic growth is still solid.

If the economy is slowing down, nobody told the labor market.

Employers added 275,000 jobs in February, the Labor Department reported Friday, in another month that exceeded expectations.

It was the third straight month of gains above 200,000, and the 38th consecutive month of growth — fresh evidence that after surging back from the pandemic shutdowns, America’s jobs engine still has plenty of steam.

“We’ve been expecting a slowdown in the labor market, a more material loosening in conditions, but we’re just not seeing that,” said Rubeela Farooqi, chief economist at High Frequency Economics.

The previous two months, December and January, were revised down by a combined 167,000 jobs, reflecting the higher degree of statistical volatility in the winter months. That does not disrupt a picture of consistent robust increases, which now looks slightly smoother..

At the same time, the unemployment rate, based on a survey of households, increased to a two-year high of 3.9 percent, from 3.7 percent in January. A more expansive measure of slack labor market conditions, which includes people working part time who would rather work full time, has been steadily rising and now stands at 7.3 percent.

The unemployment rate was driven by people losing or leaving jobs as well as those entering the labor force to look for work. The labor force participation rate for people in their prime working years — ages 25 to 54 — jumped back up to 83.5 percent, matching a level from last year that was the highest since the early 2000s.

Average hourly earnings rose by 4.3 percent over the year, although the pace of increases has been fading.

“We’ve recently seen gains in real wages, and that’s encouraged people to re-enter the labor market, and that’s a good development for workers,” said Kory Kantenga, a senior economist at the job search website LinkedIn. As wage growth slows, he said, the likelihood that more people will start looking for work falls.

As late as last fall, economists were predicting much more modest employment increases, with hiring concentrated in a few industries. But while some pandemic-inflated industries have shed jobs, expected downturns in sectors like construction haven’t materialized. Rising wages, attractive benefits and more flexible work schedules have drawn millions of workers off the sidelines.

Elevated levels of immigration have also added to the labor supply. According to an analysis by the Brookings Institution, the influx has approximately doubled the number of jobs that the economy could add per month in 2024 without putting upward pressure on inflation, to between 160,000 and 200,000.

Health care and government again led the payroll gains in February, while construction continued its steady increase. Retail and transportation and warehousing, which have been flat to negative in recent months, picked up.

No major industries lost a substantial number of jobs. Credit intermediation continued its downward slide — that sector, which mostly includes commercial banking, has lost about 123,000 jobs since early 2021.

That doesn’t mean the employment landscape looks rosy to everyone. Employee confidence, as measured by the company rating website Glassdoor, has been falling steadily as layoffs by tech and media companies have grabbed headlines. That’s especially true in white-collar professions like human resources and consulting, while those in professions that require working in person — such as health care, construction and manufacturing — are more upbeat.

“It is a two-track labor market,” said Aaron Terrazas, Glassdoor’s chief economist, noting that job searches are taking longer for people with graduate degrees. “For skilled workers in risk-intensive industries, anyone who’s been laid off is having a hard time finding new jobs, whereas if you’re a blue-collar or frontline service worker, it’s still competitive.”

The last few months have been studded with strong economic data, leading analysts surveyed by the National Association for Business Economics to raise their forecasts for gross domestic product and lower their expectations for the trajectory of unemployment. It’s occurred even as inflation has eased, leading the Federal Reserve to telegraph its plans for interest rate cuts sometime this year, which has raised growth expectations further.

Mervin Jebaraj, director of the Center for Business and Economic Research at the University of Arkansas, helped tabulate the survey responses. He said the mood was buoyed partly by fading trepidation over federal government shutdowns and draconian budget cuts, after several close calls since the fall. And he sees no obvious reason for the recovery to end soon.

“Once it starts going, it keeps going,” Mr. Jebaraj said. “You had this external stimulus with all the trillions of dollars of government spending, Now it’s sort of self-sustaining, even though the money’s gone.”

The U.S. economy added 353,000 jobs in January, while the unemployment rate held at 3.7%, the Labor Department said Friday.

Why it matters:

The first look at the 2024 labor market shows it’s on fire — not slowing down as previously thought.

Details:

The January payroll figures show hiring picked up from the 333,000 added the prior month, which itself was revised higher by 117,000.

Job gains in November were revised slightly higher, too, by 9,000 to 182,000 jobs added.

What’s new:

The hiring boom last month came amid strong job gains in health care, retail and professional and business services, while mining and oil and gas extraction are among the sectors that shed jobs.

Meanwhile, the labor force participation rate — the share of workers with or looking for a job — was 62.5% in January.

Average hourly earnings, a measure of wage growth, soared by 0.6%. Over the past 12 month, average hourly earnings increased by 4.5%.

The big picture:

The data is the latest in recent weeks to show that the economy is revving up, with fading inflation and steady hiring — a welcome development for the Biden administration that is touting its economic agenda ahead of the 2024 election.

The intrigue:

The strong growth in both jobs and earnings will make the Federal Reserve reluctant to cut interest rates soon, out of fear that labor market strength could reverse progress on inflation.

Already this week, Fed chair Jerome Powell threw cold water on the idea of a March rate cut.

The bottom line:

Despite high profile layoffs at media and technology companies, the report shows that broader labor market is heating up.

The U.S. economy added 216,000 jobs last month while the unemployment rate held at 3.7%, the Labor Department said on Friday.

Why it matters:

The final snapshot of the 2023 labor market shows hot hiring — the latest sign that the American job market continues to defy expectations of a slowdown.

The figure is well-above the roughly 170,000 jobs economists expected.

The big picture:

The Federal Reserve has hinted it likely won’t raise interest rates again with encouraging signs that inflation is easing and the labor market is cooling.

That concludes an aggressive rate hiking cycle that began in 2022 and lasted through much of last year.

For now, however, there is little evidence those rate hikes translated into pain for workers in 2022.

American consumers, however, remain dissatisfied with the economy — a problem that may continue to weigh on the Biden White House as the 2024 election heats up.

Details:

Friday’s jobs report shows the labor market stayed strong. Hiring increased in sectors including government, health care, and construction. Transportation and warehousing shed jobs.

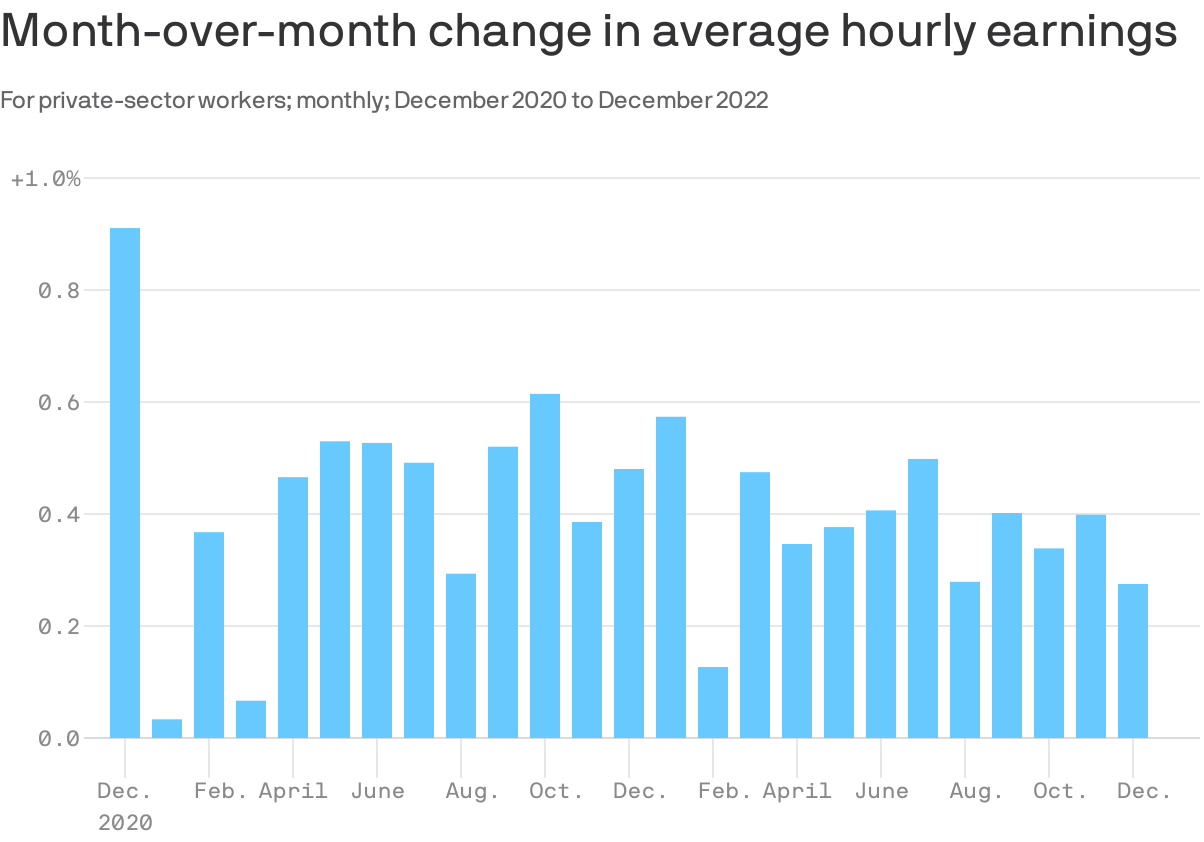

Average hourly earnings, a measure of wages, rose by 0.4% last month. Compared to the prior year, average hourly earnings rose 4.1%.

The share of the population with in the labor force — that is, with a job or looking for one — was 62.5% in December, roughly 0.3 percentage point less than the prior month.

The Labor Department also said the economy added a combined 71,000 fewer jobs than initially estimated in October and November.

The bottom line:

The hotter-than-expected jobs figures are one of several more key economic reports due before Federal Reserve officials meet at the end of the month.

Wednesday’s inflation print showed a March increase of 0.1% versus February and a year-over-year increase of 5.0%, both of which were better than expected. Markets rallied following the news, at least until the specter of recession caused a reversal of equity gains. The game remains the same: markets want easy money and inflation plus unemployment plus recession equals Fed policy and interest rate levels. Memories of the long 1970s slog through declining and then accelerating inflation levels suggest that it’s too early to declare victory (5.00% is still a long way from the Fed’s 2.00% target range). Nevertheless, hopes increased that the Fed may truly be at or very near the end of its tightening cycle.

Unsustainable Trends

The web version of The Wall Street Journal got rid of its special section on the “2023 Bank Turmoil,” which is a sign that we’re past the worst of this chapter in the Dickensian saga in which our financial system hero navigates all sorts of unfortunate characters and events in search of a new “normal.” Banking distrust ripples continue, with various clients sharing the work they are doing to peel back layers of counterparty risk to understand whether threats loom in downstream financial dependencies. Our regulatory infrastructure has shown itself to be a mile wide and an inch deep, which fuels the kind of skepticism about the reliability of designated watchdogs that leads to self-directed risk assessments.

At one level, this is a helpful and important exercise. The credit and financing structure of any complex healthcare organization is just another supply chain, and it is good to understand how yours works and whether there are vulnerabilities that should be investigated. But it is equally important to assess whether the progression of COVID to inflation to Silicon Valley Bank has caused your organization to drift from risk management into retrenchment. Organizations naturally migrate along a risk continuum as they shift between prioritizing returns or resiliency. The important question isn’t which of these bookends is right, but rather what shapes the migration; the defining event is the journey, and

the critical Board and C-suite conversation is whether your risk management program is enabling or constraining future growth.

We continue to monitor the extraordinary decline in not-for-profit healthcare debt issuance. Sources we rely on show healthcare public debt issuance through Q1 2023 down almost 70% versus Q1 2022. Similar data sources aren’t available, but anecdotal input from our team suggests a comparable drop-off in healthcare real estate as well as alternative funding channels. At the same time, although margins have recently improved, operating cash flow across the sector has been weak over the past 12-18 months. If capital formation from internal and external sources is a sign of vibrancy, healthcare is listless.

The primary culprit isn’t rates; the sector has raised capital in much higher rate environments with fewer financing channels (including most of the pre-2008 era). Instead, the rationale most frequently advanced is concern about the reaction from key credit market constituents during this time of unprecedented operating disruption. Of course, this makes sense, but sitting underneath this basic rationale is the question of what might be called “capital deployment conviction.” Long experience confirms that organizations armed with a growth thesis they believe in aren’t shy about “selling” their story to rating agencies and investors and are willing to suffer adverse outcomes on rates, ratings, or covenants, if that is the price of growth. This isn’t happening right now, which introduces the troubling idea that issuance trends are about much more than credit management.

No matter the root cause, recent capital formation is not sustainable.

Good risk management leads to caution in challenging times, but being too careful elevates the probability that temporary problems become permanent. $2.8 billion in quarterly external capital formation ($11.2 billion annualized—pause and let that annualized amount sink in) is not sufficient to maintain the not-for-profit healthcare sector’s care delivery infrastructure, especially when internal capital generation is equally anemic. But introduce any competitive paradigm and the underinvestment that accompanies this level of capital formation becomes a harbinger of hard times to come. To riff on Aristotle, capitalism abhors a vacuum, and organizations looking to avoid rating pressure today may be elevating the risk of competitive pressure tomorrow; and it is easier to cope with and eventually recover from rating pressure than it is to confront the long-term consequences of well-capitalized and aggressive competitors. Retrenchment might be the right risk management choice in times of crisis, but once that crisis moderates that same strategy can quickly become a risk driver.

Machiavelli, Sun-Tzu, Napoleon, George Washington, and other great tacticians all advanced some variation of the idea that “the best defense is a good offense.” In the world of risk response, this means that the better choice isn’t to de-risk and hibernate but rather to continuously reposition available risk capacity so that you keep the organization moving forward. Star Trek’s philosopher-king Captain James Tiberius Kirk captured the sentiment best when he said, “the best defense is a good offense, and I intend to start offending right now.”

While getting back on the capital horse is important, clearing rates, relative value ratios, risk premia, and flexibility drivers have all reset over the past 12-18 months, so recalibrating a good capital formation program requires reassessment and may lead to very different tactics.

This means that a critical step is to get organized around funding parameters:

debt versus real estate versus other channels; MTI versus non-MTI; tax-exempt versus taxable; public versus private; fixed versus floating. The other important part of this is gaining conviction about capital structure risk versus flexibility: do you want to retain flexibility at the “cost” of incurring the market risk embedded in short-tenor or floating rate structures or do you want to sell flexibility in exchange for capital structure risk reduction?

President Joe Biden last night highlighted several healthcare priorities during his State of the Union address, including efforts to reduce drug costs, a universal cap on insulin prices, healthcare coverage, and more.

COVID-19

In his speech, Biden acknowledged the progress the country has made with COVID-19 over the last few years.

“Two years ago, COVID had shut down our businesses, closed our schools, and robbed us of so much,” he said. “Today, COVID no longer controls our lives.”

Although Biden noted that the COVID-19 public health emergency (PHE) will come to an end soon, he said the country should remain vigilant and called for more funds from Congress to “monitor dozens of variants and support new vaccines and treatments.”

The Inflation Reduction Act

Biden highlighted several provisions of the Inflation Reduction Act (IRA), which passed last year, that aim to reduce healthcare costs for millions of Americans.

“You know, we pay more for prescription drugs than any major country on earth,” he said. “Big Pharma has been unfairly charging people hundreds of dollars — and making record profits.”

Under the IRA, Medicare is now allowed to negotiate the prices of certain prescription drugs, and out-of-pocket drug costs for Medicare beneficiaries are capped at $2,000 per year. Insulin costs for Medicare beneficiaries are also capped at $35 a month.

“Bringing down prescription drug costs doesn’t just save seniors money,” Biden said. “It will cut the federal deficit, saving tax payers hundreds of billions of dollars on the prescription drugs the government buys for Medicare.”

Caps on insulin costs for all Americans

Although the IRA limits costs for seniors on Medicare, Biden called for the policy to be made universal for all Americans. According to a 2022 study, over 1.3 million Americans skip, delay purchasing, or ration their insulin supply due to costs.

“[T]here are millions of other Americans who are not on Medicare, including 200,000 young people with Type I diabetes who need insulin to save their lives,” Biden said. “… Let’s cap the cost of insulin at $35 a month for every American who needs it.”

With the end of the COVID-19 PHE, HHS estimates that around 15 million people will lose health benefits as states begin the process to redetermine eligibility.

The opioid crisis

Biden also addressed the ongoing opioid crisis in the United States and noted the impact of fentanyl, in particular.

“Fentanyl is killing more than 70,000 Americans a year,” he said. “Let’s launch a major surge to stop fentanyl production, sale, and trafficking, with more drug detection machines to inspect cargo and stop pills and powder at the border.”

He also highlighted efforts by to expand access to effective opioid treatments. According to a White House fact sheet, some initiatives include expanding access to naloxone and other harm reduction interventions at public health departments, removing barriers to prescribing treatments for opioid addiction, and allowing buprenorphine and methadone to be prescribed through telehealth.

Access to abortion

In his speech, Biden called on Congress to “restore” abortion rights after the U.S. Supreme Court overturned Roe v. Wade last year.

“The Vice President and I are doing everything we can to protect access to reproductive healthcare and safeguard patient privacy. But already, more than a dozen states are enforcing extreme abortion bans,” Biden said.

He also added that he will veto a national abortion ban if it happens to pass through Congress.

Progress on cancer

Biden also highlighted the Cancer Moonshot, an initiative launched last year aimed at advancing cancer treatment and prevention.

“Our goal is to cut the cancer death rate by at least 50% over the next 25 years,” Biden said. “Turn more cancers from death sentences into treatable diseases. And provide more support for patients and families.”

According to a White House fact sheet, the Cancer Moonshot has created almost 30 new federal programs, policies, and resources to help increase screening rates, reduce preventable cancers, support patients and caregivers and more.

“For the lives we can save and for the lives we have lost, let this be a truly American moment that rallies the country and the world together and proves that we can do big things,” Biden said. “… Let’s end cancer as we know it and cure some cancers once and for all.”

Healthcare coverage

Biden commended the fact that “more American have health insurance now than ever in history,” noting that 16 million people signed up for plans in the Affordable Care Act marketplace this past enrollment period.

In addition, Biden noted that a law he signed last year helped millions of Americans save $800 a year on their health insurance premiums. Currently, this benefit will only run through 2025, but Biden said that we should “make those savings permanent, and expand coverage to those left off Medicaid.”

Advisory Board’s take

Our questions about the Medicaid cliff

President Biden extolled economic optimism in the State of the Union address, touting the lowest unemployment rate in five decades. With job creation on the rise following the incredible job losses at the beginning of the COVID-19 pandemic, there is still a question of whether the economy will continue to work for those who face losing Medicaid coverage at some point in the next year.

The public health emergency (PHE) is scheduled to end on May 11. During the PHE, millions of Americans were forced into Medicaid enrollment because of job losses. Federal legislation prevented those new enrollees from losing medical insurance. As a result, the percentage of uninsured Americans remained around 8%. The safety net worked.

Starting April 1, state Medicaid plans will begin to end coverage for those who are no longer eligible. We call that the Medicaid Cliff, although operationally, it will look more like a landslide. Currently, state Medicaid regulators and health plans are still trying to figure out exactly how to manage the administrative burden of processing millions of financial eligibility records. The likely outcome is that Medicaid rolls will decrease exponentially over the course of six months to a year as eligibility is redetermined on a rolling basis.

In the marketplace, there is a false presumption that all 15 million Medicaid members will seamlessly transition to commercial or exchange health plans. However, families with a single head of household, women with children under the age of six, and families in both very rural and impoverished urban areas will be less likely to have access to commercial insurance or be able to afford federal exchange plans. Low unemployment and higher wages could put these families in the position of making too much to qualify for Medicaid, but still not making enough to afford the health plans offered by their employers (if their employer offers health insurance). Even with the expansion of Medicaid and exchange subsidies, it, is possible that the rate of uninsured families could rise.

For providers, this means the payer mix in their market will likely not return to the pre-pandemic levels. For managed care organizations with state Medicaid contracts, a loss of members means a loss of revenue. A loss of Medicaid revenue could have a negative impact on programs built to address health equity and social determinants of health (SDOH), which will ultimately impact public health indicators.

For those of us who have worked in the public health and Medicaid space, the pandemic exposed the cracks in the healthcare ecosystem to a broader audience. Discussions regarding how to address SDOH, health equity, and behavioral health gaps are now critical, commonplace components of strategic business planning for all stakeholders across our industry’s infrastructure.

But what happens when Medicaid enrollment drops, and revenues decrease? Will these discussions creep back to the “nice to have” back burners of strategic plans?

The U.S. economy added 517,000 jobs in January, and the unemployment rate fell to 3.4% — the lowest level in over a half-century, the government said on Friday.

Why it matters:

Employers added jobs at an unexpectedly rapid pace, the latest sign of a hot labor market despite aggressive moves by the Federal Reserve to cool it down.

The numbers are more than double the 190,000 forecasters anticipated.

Details:

The extraordinary reportcomes as the Fed continues to dial back its pace of interest rates and prepares to raise rates further to restrain the economy and chill still-high inflation.

Fed chair Jerome Powell has acknowledged progress on slowing inflation in recent months while noting risks lie ahead. Among them is wage growth, which is rising at a pace still too swift for the Fed’s comfort.

In January, average hourly earnings rose 0.3% — or 4.4% over the previous year, according to Friday’s data.

The big picture:

The data also showed that employment in 2023 was even stronger than initially thought, with roughly 568,000 more jobs than previously reported.

The update was part of the Labor Department’s annual revisions, which incorporate more complete data from insurance records and updated seasonal adjustments.

The Goldilocks nature of these jobs numbers is particularly apparent in the wage data.

By the numbers: Average hourly earnings rose by 0.3% in December, and are up 4.6% over the last year. Over the last three months, worker pay rose at a 4.1% annual rate.

Wages are rising, but unlike a year ago, the pace is consistent with the economy settling into the 2% inflation that the Fed seeks.

For example, there were stretches in 2018 and 2019 that featured wage growth similar to that in Q4 paired with low inflation levels — which meant rising real wages for workers.

In other words, current pay growth, if sustained, would help diminish the Fed’s fears of an upward spiral of wages and prices. Also, it sets workers up to see gains in their real compensation, if and when inflation comes down.

The intrigue: It appears that a surge in earnings initially reported in November was a head fake. The Labor Department revised those numbers to show a 0.4% rise in hourly earnings, not the 0.6% first reported.

The original figures had been a source of alarm among Fed watchers, suggesting the central bank might need to step up its monetary tightening campaign.

It is a good reminder — for both policymakers and those of us in the media — to not overreact to single-month shifts in any volatile data series.

We really liked what we saw in the December jobs report, which made us more optimistic about the possibility the 2023 economy will hold up reasonably well. More details below.

Situational awareness: In less optimistic news, the Institute for Supply Management’s survey of service industry activity plunged in December, to 49.6% — down from 56.5% in November. This is the first time the index has been in negative territory since May 2020.

The U.S. labor market is extraordinarily strong, despite gloom-and-doom economic forecasts and high-profile layoffs.

That is the takeaway from December numbers, out this morning, that were outstanding in subtle and not-so-subtle ways.

Why it matters: If America’s economy is going to come in for a soft-landing — inflation dissipating without mass unemployment — you would expect to see numbers that look a lot like last month’s.

The economy continues to add a healthy number of new jobs, though the pace is moderating. Wages are rising, but not so quickly as to alarm economic policymakers. And more workers are entering the labor force, which — if sustained — could heal labor shortages.

The data has positive developments both for American workers — who continue to have abundant job opportunities — and for Fed officials seeking evidence that their inflation-fighting efforts are starting to cool job creation and wage growth to more sustainable rates.

The headline unemployment rate, at 3.5%, matched its lowest levels in decades. If you extend the calculation out a couple more decimal places, University of Michigan economist Justin Wolfers points out, it was 3.468%, the lowest since 1969!

It fell even as the labor force expanded by 439,000 workers, a welcome development on the supply front after months of little progress. More Americans working means fewer of the labor shortages that have contributed to inflation.

An additional 717,000 Americans reported being employed, helping resolve what had been a puzzling disconnect between different sources of labor market data — and in a positive direction.

A stunningly low jobless rate might raise some alarm bells at the Fed over the possibility the job market is too tight, and that this could fuel inflation. But the labor force growth and benign wage data (more on that below) may take the edge off those fears.

By the numbers: Employers are still hiring at a rapid pace — 223,000 in December — but slowing from early last year’s unsustainable numbers.

The economy has added roughly 247,000 jobs per month on average in the last three months, slower than the 366,000 in the prior three-month stretch, and less than half of the 539,000 jobs added each month in Q1 2022.

Evidence of tech layoffs did show up somewhat in the report, with the information sector shedding 5,000 jobs. Temporary help services employment fell by 35,000, the clearest sign employers are paring back demand for workers.

But most other sectors, including leisure and hospitality, construction and health care, continued to add jobs.

The bottom line: If we keep getting numbers like these, 2023 may not be such a rough year for workers after all.

The jobs market stayed strong last month: Employers added 263,000 jobs, while the unemployment rate held at 3.7%, near the lowest level in a half-century, the Labor Department said on Friday.

Why it matters: The figures are the latest signal of a roaring labor market that continues to defy fears of a recession.

November’s payroll gains are above the addition of 200,000 jobs that economists had expected.

By the numbers: Job growth last month was slightly slower than the 284,000, added in October, which was revised up by 23,000. In September, the economy added 269,000 jobs, 46,000 fewer than initially estimated.

Average hourly earnings, a measure of wage growth, rose by 0.6% in November — faster than the prior month, when earnings rose by 0.5%. Over the past year ending in November, average hourly earnings increased by 5.1%.

The share of people working or looking for work, known as the labor force participation rate, ticked down to 62.1%, compared to 62.2% in October.

The backdrop: Economists have been bracing for cracks in the labor market thathave yet to appear.

It has been an ugly stretch for layoffs in a handful of sectors like technology, with large-scale job cuts announced at Meta, Amazon and Twitter.

But overall, the booming job markethas continued for workers, even in the face of ultra-aggressive efforts by the Federal Reserve to try to cool demand for labor to help put a lid on inflation.

Last month, Fed chair Jerome Powell said that employers bidding up wages to attract workers is not “the principal story of why prices are going up.”

Still, the labor market may point to clues about how inflation will evolve in certain categories, including industries within the services sector where wages make up the biggest costs for businesses, Powell said on Wednesday.