The GOP’s reconciliation bill, the “One Big Beautiful Bill Act” (yes, it’s actually called that), is a cruel exercise in slashing benefits for the poor, the elderly, and the sick to free up fiscal space for yet more tax cuts for the rich. Compounding the harm, these benefit cuts are nowhere near enough to pay for the bill’s tax cuts for the wealthy.

Central to this effort are massive cuts to Medicaid and the Affordable Care Act (ACA) marketplaces that, as I argued in my recent paper, will exacerbate our ongoing medical debt crisis.

The GOP reconciliation package that the Senate and House recently agreed to instructed the House Energy and Commerce Committee, which oversees spending on health-care programs including Medicaid and the Children’s Health Insurance Program (CHIP), to identify up to $880 billion in savings over the next 10 years.

Under the rules of the budget reconciliation process, Republicans need to offset any tax cuts they wish to make permanent with an equal dollar value in cuts to spending so as to remain deficit neutral. Trillions of dollars in tax cuts for the wealthier therefore necessitate trillions of dollars in cuts to spending that fall mostly on the social safety net.

Although they did not quite reach that target, the committee still returned a proposed package of deep cuts and changes to Medicaid and to the ACA marketplaces that would reduce federal medical spending by at least $715 billion over 10 years, with about $625 billion in reduced Medicaid spending.1

After public backlash, Republicans seem to have backed off some of their most radical plans for Medicaid (at least for now—one of the challenges of taking health care from people is that it’s terrible politics, so the precise details of the cuts are likely to remain a moving target until the bill passes).

But all options they are close to settling on would still do horrific damage to the well-being of working-class families.

This includes requiring all Medicaid recipients above the federal poverty line to “cost share” by paying (larger) premiums and copayments,2 cutting federal matching to states that provide public health insurance coverage to undocumented and perhaps documented immigrants (on their own dime), and imposing harsh work requirements on “able-bodied adults without dependent children.” This latter provision will cut federal Medicaid spending by roughly $300 billion over 10 years even though the vast majority (92 percent) of nondisabled, non-elderly adult Medicaid recipients are already working, studying full time, or serving as caregivers. This is because work requirements create burdensome reporting requirements to demonstrate compliance that will cause Medicaid recipients who are already employed to lose their insurance as well—blaming the victim for losing their health care, in essence.

The Congressional Budget Office estimates that the reconciliation bill would decrease Medicaid enrollment by 10.3 million in 2034(the end of the reconciliation bill budget window).

According to this same analysis, most of these individuals would not obtain other insurance (e.g., through an employer) and would thus become uninsured.

When combined with the bill’s changes to the ACA marketplace and the expiration of the enhanced premium tax credits—a wildly successful policy that was introduced as part of the American Rescue Plan Act (ARPA) and one that Republicans have shown no inclination to extend—this would result in an additional 13.7 million uninsured individuals in 2034, a 30 percent increase, according to KFF estimates.

Republicans seem hell-bent on undoing the remarkable progress made in the 15 years since the passage of the ACA in reducing the non-elderly uninsured rate from 17.8 percent in 2010 to roughly 9.5 percent today (plus ça change).

But we’ve seen less focus on how this will affect the problem of underinsurance.

Republicans’ Medicaid cost-sharing requirements, the changes they have proposed to the ACA marketplaces, and their determination to let the ARPA premium tax credit enhancements expire will also worsen the problem of underinsurance, an area where we have made considerably less progress.

Taken together, this will worsen the ongoing medical crisis because medical debt is driven by uninsurance and underinsurance.

Medical debt is, unlike in most other countries, and despite the successes of the ACA, a major problem in the United States. KFF found that 20 million adults (almost 1 in 12) owed “significant” medical debt to a health-care provider.3 This number rises when we consider a more expansive definition of medical debt including credit card balances and bank loans used to pay medical providers. Under that definition, an estimated 41 percent of American adults (~107 million people) carried some form of medical debt and 24 percent of American adults (~62 million people) had medical debt that was past due or that they were unable to pay. Among those with medical debt using this more expansive definition, nearly half (44 percent) reported owing at least $2,500, and about one in eight (12 percent) said they owe $10,000 or more. The poor, the sick, the middle-aged, and Black and Hispanic individuals disproportionately bear the brunt of this problem.

The crisis of medical debt and underinsurance is so widely recognized by Americans that a state attorney general candidate can go viral just by talking about the reality of a GoFundMe health-care system millions of Americans face.

The consequences of all this debt are dire—and reflect a health-care system that heals people physically but leaves many permanently scared financially. In 2022, medical debt (using the narrow definition) made up an estimated 58 percent of all debts that had gone to collections, and 62 percent of bankruptcies were attributed in part to medical debt. Medical debt also damages credit scores, leading to a wide variety of negative impacts on financial well-being that can follow families for years.

A poor credit score means that families may be unable to obtain a mortgage or a car loan or may end up paying much higher interest rates.

Credit scores are commonly used by landlords to screen tenants and by employers as part of a background check during the hiring process. Even for those who manage to maintain their credit after taking on medical debt, there are real costs. For those with limited income and assets, debt service may displace spending on food, clothing, and other essentials, leading to material hardship. It can make savings impossible and limit economic mobility.

Medical debt is a problem largely generated by poor policy decisions including, as I argue in my paper, prioritizing and incentivizing health insurance coverage through the private market rather than through Medicaid and Medicare, which offer comprehensive coverage more cheaply. The problem would rapidly disappear if we could extend comprehensive health insurance coverage to the millions of uninsured and underinsured people who live with the constant risk that a sudden medical event could ruin their finances and constrain their futures.

But rather than fix the problem, the GOP plans to throw millions off Medicaid and saddle those who remain with higher costs and more limited coverage. The results of these poor policy decisions will be more sickness, more debt, and higher costs for everyone in exchange for on-paper “savings.” And all this in service of tax cuts for the wealthy they haven’t even bothered to justify.

If you ask Eleanor

“If the old people cannot afford their medical care under their own Social Security allowances, then the burden is going to fall on their children who are in their earning years. This will mean that just at the time when these children who may be having young children of their own and needing medical care, a young couple will also have to consider shouldering the burden for parents as well. This is not fair, and leads to both the children and the older people not getting full coverage, since both will try to shave a little off their needs in order not to make the burden impossible to carry.”

Moody’s on Friday downgraded its credit rating of the United States by a notch to “Aa1” from “Aaa”, citing rising debt and interest “that are significantly higher than similarly rated sovereigns.”

The rating agency had been the last among major ratings agencies to keep a top, triple-A rating for U.S. sovereign debt, though it had lowered its outlook in late 2023 due to wider fiscal deficit and higher interest payments.

“Successive US administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs,” Moody’s said on Friday, as it changed its outlook on the U.S. to “stable” from “negative.”

Since his return to the White House on January 20, President Donald Trump has pledged to balance the U.S. budget while his Treasury Secretary, Scott Bessent, has repeatedly said the current administration aims to lower U.S. government funding costs.

The administration’s mix of revenue-generating tariffs and spending cuts through Elon Musk’s Department of Government Efficiency have highlighted a keen awareness of the risks posed by mounting government debt, which, if unchecked, could trigger a bond market rout and hinder the administration’s ability to pursue its agenda.

The downgrade comes as Trump’s sweeping tax bill failed to clear a key procedural hurdle on Friday, as hardline Republicans demanding deeper spending cuts blocked the measure in a rare political setback for the Republican president in Congress.

“We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration,” Moody’s said, while forecasting federal debt burden to rise to about 134% of GDP by 2035, compared with 98% in 2024.

The cut follows a downgrade by rival Fitch, which in August 2023 also cut the U.S. sovereign rating by one notch, citing expected fiscal deterioration and repeated down-to-the-wire debt ceiling negotiations that threaten the government’s ability to pay its bills.

On January 17, 2025, a list of potential cost reductions to the federal budget was released by Republicans on the House Budget Committee. The list is long and covers the federal budget waterfront, but it spends considerable time focusing on reductions to healthcare spending. This laundry list of cost reductions is important because the highest priority of the Trump administration is a further reduction in federal taxes. A reduction in taxes would, of course, reduce federal revenue; if federal expenses are not proportionately reduced then the federal deficit will increase. When the deficit increases then the federal debt must increase and at that point the overall impact on the American economy becomes concerning and possibly damaging. There has already been much public speculation as to how the Federal Reserve might react to such a scenario.

It is not possible right now to highlight and describe all of the House budget proposals, but one proposal absolutely stands out: The suggestion to eliminate the tax-exempt status for interest payments on all municipal bonds, or potentially in a more targeted manner, for private activity bonds, including those issued by not-for-profit hospitals. Siebert Williams Shank, an investment banking firm, described the elimination of tax exemption for municipal bonds as “the most alarming of the proposed reforms impacting non-profit and municipal issuers.”[1] This is certainly true for hospitals, since over the past 60 years the growth and capability of America’s hospitals has been substantially constructed on the foundation of flexible and relatively inexpensive tax-exempt debt. Given all of this, it is not too early to begin speculating on the impact of the elimination of tax-exempt debt on hospital finances and strategy.

We should also point out that a separate topic is under discussion, related to the potential loss of not-for-profit status for hospitals and health systems. Such a maneuver could potentially expose hospitals to income taxes, property taxes, and higher funding costs. For now, that is beyond the scope of this blog but may be something we write about in future posts.

Below is a series of important questions related to the elimination of tax-exempt financing and some speculations on the overall impact:

What immediately happens if 501(c)(3) hospitals lose the ability to issue tax-exempt bonds? Let’s treat fixed rate debt first. Assume for now that only newly issued debt would be affected and that all currently outstanding tax-exempt fixed rate debt would remain tax-exempt. We could see an effort to apply any changes retroactively to existing bonds, but we view that as unlikely. Therefore, our current expectation is that outstanding fixed-rate debt would not see a change in interest expense.

However, it is possible that outstanding floating rate debt would immediately begin to trade based on the taxable equivalent. Historically the tax-exempt floating rate index trades at about 65% of the taxable index. The difference between the tax-exempt and taxable floating rate indices in the current market is 175 basis points. For every $100 million of debt, this would increase interest expense by $1.75m annually.

How would new hospital debt be issued? New debt would be issued in the municipal market on a taxable basis or in the corporate taxable market. The taxable municipal market would need to adapt and expand to accommodate a significant level of new issuance. The concern in the corporate taxable market is greater. Currently, the corporate market requires issuance of significant dollar size and generally the issuer brings significant name recognition to the market. Many hospitals may have difficulty meeting the issuance size of the corporate debt market and/or the necessary market recognition. As such, smaller and less frequent issuers would expect to pay a penalty of 25-50 basis points for issuing in the corporate market.

If tax-exempt debt goes away will certain hospitals be advantaged and others disadvantaged? Larger hospitals with national or regional name recognition that issue bonds with sufficiently large transaction size and frequency will likely borrow at better terms and lower rates. Smaller- to medium-sized hospitals may find borrowing much more difficult, and borrowing may come with more problematic terms and/or amortization schedules and likely higher interest rates.

Will borrowing costs go up? The cost of funds for new borrowings would increase for all hospital borrowers. For a typical A-rated hospital, annual interest expense would increase by approximately 30%. For example, in the current market, on $100 million of new debt, average annual interest expense would increase by $815,000 annually.

Will debt capacity go down? All other things being equal, interest rates will go up and hospital debt capacity will go down. Also, if the taxable market shortens amortization schedules, then that will decrease overall debt capacity as well.

What would the impact of the elimination of tax-exempt debt be on synthetic fixed rate structures? Hospitals have long employed derivative structures to hedge interest rate risk on outstanding variable rate bonds and loans. The loss of tax-exemption for outstanding variable rate bonds and loans would precipitate an adjustment to taxable rates, but corresponding swap cash flows are not designed to adjust. Interest rate risk is hedged, but tax reform risk is not. The net effect to borrowers would be an increase in cost similar to the cost contemplated above for variable rate bonds.

What are the rating implications of the elimination of the tax-exempt market? Rating implications will be varied. Hospitals with strong financial performance and liquidity are likely to absorb the increased interest expense of a taxable borrowing with little to no rating impact. In fact, over the past decade, many larger health systems in the AA rating categories have successfully issued debt in the taxable market without rating implications despite a higher borrowing rate. Even amid the pandemic chaos of 2021, numerous AA and A rated systems issued sizable, taxable debt offerings to bolster liquidity as proceeds were for general corporate purposes and not restricted by a third-party, such as a bond trustee.

Lower-rated hospitals with modest performance and below-average liquidity will be at greater risk for a downgrade. These hospitals may not be able to absorb the increased interest expense and maintain their ratings. While interest expense is typically a small percentage of a hospital’s total expenses, it is a use of cash flow.

We do not anticipate the rating agencies will take wholesale downgrade action on the rated portfolio as there would likely be a phase-in period before the elimination occurs. Rather, we expect the rating agencies will take a measured approach with a case-by-case evaluation of each rated organization through the normal course of surveillance, as they did during the pandemic and liquidity crisis in 2008. A dialogue on capital budgets and funding sources, typically held at the end of a rating meeting, would be moved to the top of the agenda, as it will have a direct impact on long-term viability.

How would the loss of the tax-exempt market impact the pace of consolidation in the hospital industry? If a hospital cannot afford the taxable market, then large capital projects would need to be funded through cash and operations. This inevitably will limit organizational liquidity, which will lead to downward rating pressure. Some hospitals, in such a situation, will be unable to both fund capital and adequately serve their local community and, therefore, will need to find a partner who can. We anticipate that the loss of the tax-exempt bond market will lead to further consolidation in the industry.

Let’s indulge in one last bit of speculation. What is the probability that Congress will pass legislation that eliminates tax-exempt financing? Sources in Washington tell us that it is premature to wager on any of the items put forth by the Budget Committee. And it should be noted that over the years the elimination of tax-exempt financing has been proposed on several occasions and never advanced in Congress. However, one well-informed source noted that as the tax and related legislation moves forward, there is likely to be significant horse-trading (especially in the House) to secure the necessary votes to pass the entire package. What happens during that horse-trading process is anybody’s guess. So the best advice to our hospital readership right now is to not take anything for granted. But be absolutely assured that the maintenance of tax-exempt financing is an essential strategic component for the successful future of America’s hospitals.

Downgrades continued to outpace upgrades in 2024 although at a lower rate than in 2023. When combining the rating actions of the three rating agencies, the number of downgrades (95) declined while the number of upgrades (37) increased, compared to 116 and 33, respectively, in 2023. Many of the downgrades reflected ongoing expense pressure that exceeded revenue growth, even as volumes headed back to pre-pandemic levels and the use of contract labor declined. Other downgrades reflected outsized increases in debt to fund pivotal growth strategies. Most of the upgrades reflected mergers of lower-rated hospitals into higher-rated systems. Rating affirmations remained the majority rating action in 2024, as in prior years.

Key takeaways include:

The ratio of downgrades to upgrades narrowed at Moody’s (2.0-to-1 in 2024 from 3.2-to-1 in 2023) and Fitch (1.5-to-1 from 3.5-to-1). S&P saw a wider spread in the ratio: 4.5-to-1 in 2024 from 3.8-to-1 in 2023.

Downgrades reflected a wide swath of hospitals, from small independent providers to large regional systems. Large academic medical centers and children’s hospitals saw downgrades, even with exclusive tertiary services that provided differentiation with payers. Shared, recurring downgrade factors included weaker financial performance, payer mix shifts to more governmental and less commercial, and thinner reserves. Many of the downgrades were concentrated along the two coasts: California and the Pacific Northwest and New York and Pennsylvania. Many of the ratings were already in low or below investment grade categories.

Multi-notch downgrades continued in 2024, ranging from two to four notch movements in one rating action. One of the hospitals that experienced a four-notch downgrade subsequently defaulted on an interest payment (Jackson Hospital & Clinics, AL). Multi-notch upgrades reflected mergers into higher-rated systems, the largest being a seven-notch upgrade of a small, single-site hospital into a 19-hospital system in the Midwest.

Five hospitals experienced multiple rating actions in 2024, with rating committees convening not once but two and three times during the year. These were distressed credits whose financial performance and reserve levels dropped materially from quarter to quarter, a characteristic of high-yield or speculative rated borrowers.

While some of the upgrades followed mergers, other upgrades reflected improved financial performance and stable or growing liquidity. Likewise, some of the upgraded hospitals began receiving new supplemental funds known as Direct Payment Programs (DPPs). Unlike other supplemental funds, DPPs are subject to annual federal and state approval, making their long-term reliability uncertain. Numerous types of providers saw upgrades—including academic medical centers, independent hospitals and regional health systems—and were located across the U.S. Most of the upgraded hospitals (excluding those involved in mergers) were already investment grade.

As in past years, rating affirmations represented the overwhelming majority of rating actions in 2024. This is welcome news for the industry as many hospitals and health systems will turn to the bond market to borrow for their capital projects. Investors’ view of the industry should be bolstered by the change in industry outlooks. S&P moved to Stable from Negative and Fitch moved to Neutral from Deteriorating in December 2024, joining Moody’s revision to Stable from Negative in 2023.

We expect rating affirmations will again be the majority rating action in 2025. However, even with the stability viewed by the agencies, we expect downgrades to outpace upgrades given a growing reliance on government payers, labor challenges and a competitive environment. Policy and funding changes will also cast uncertainty into the mix in 2025 and may cause credit deterioration in future years.

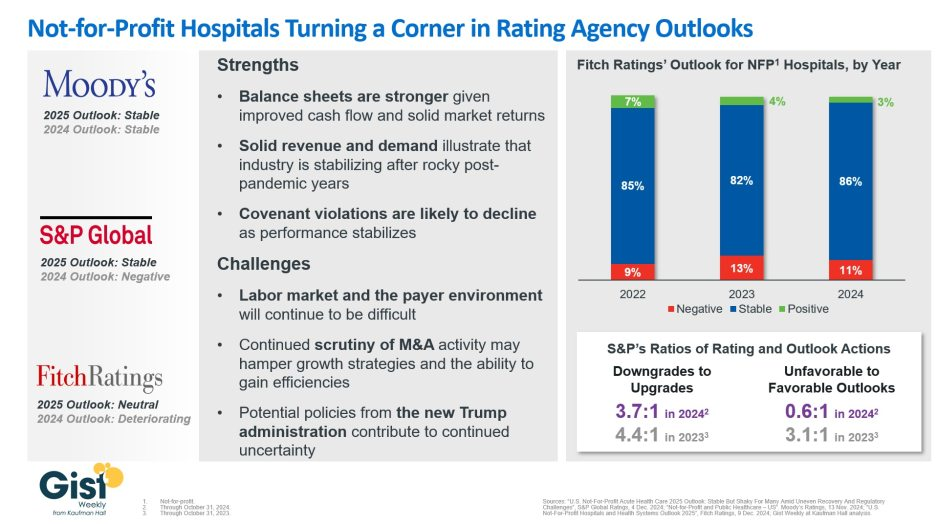

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

Here are 67 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating is based on the Altamonte Springs, Fla.-based system’s competitive market position—especially in its core Florida markets—and its financial profile, Fitch said.

Advocate Health members Advocate Aurora Health and Atrium Health have “Aa3” ratings and positive outlooks with Moody’s. The ratings are supported by the Charlotte, N.C.-based system’s significant scale, strong market share across several major metro areas, and good financial performance and liquidity, Moody’s said.

AnMed Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Anderson, S.C.-based system’s strong and stable operating performance and leading market position in a sound service area, Fitch said.

Ann & Robert H. Lurie Children’s Hospital of Chicago has an “AA” rating and stable outlook with Fitch. The rating is supported by the system’s strong balance sheet with low leverage ratios derived from modest debt, Fitch said.

Atlantic Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Morristown, N.J.-based system’s fundamental strengths, including strong operating performance with high single digit operating cash flow margins and favorable liquidity of over 300 days cash on hand, Moody’s said.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

BayCare Health System has an “AA” rating and stable outlook with Fitch. The Clearwater, Fla.-based system on June 30 moved to a new corporate legal structure, replacing a joint operating agreement between multiple hospitals that were responsible for the creation of BayCare in 1997. Fitch views the dissolution of the JOA and the move to the new structure as a credit positive.

Beacon Health System has an “AA-” rating and stable outlook with Fitch. Fitch said the rating reflects the strength of the South Bend, Ind.-based system’s balance sheet.

Bon Secours Mercy Health has an “AA-” rating and stable outlook with Fitch. The Cincinnati-based system has a favorable and stable payor mix, leading or secondary market share position in nine of its 11 U.S. markets with improving market share positions in eight, and adequate cash flows to support the system’s strategic plans, Fitch said.

BJC Health System has an “Aa2” rating and stable outlook with Moody’s. The St. Louis-based system reflects its reputation as a leading academic medical center with a long-standing affiliation with Washington University School of Medicine, Moody’s said.

Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area and Fitch’s expectation that the system will sustain its strong capital-related ratios in the context of the system’s midrange revenue defensibility and strong operating risk profile assessments.

Carilion Clinic has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Roanoke, Va.-based system’s scale, regional significance as a tertiary referral system with broad geographic capture, and a highly integrated physician base with a well-defined culture, Moody’s said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals, and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence, and pediatric trauma status, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The rating reflects the Minneapolis-based system’s strong balance sheet, robust liquidity position, and dominant pediatric market position, Fitch said.

Cincinnati Children’s Hospital Medical Center has an “Aa2” rating and stable outlook with Moody’s. The rating is supported by its national and international reputation in clinical services and research, Moody’s said.

Cleveland Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the system’s strength as an international brand in highly complex clinical care and research and centralized governance model, the ratings agency said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth, Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

Corewell Health has an “Aa3” rating and stable outlook with Fitch. The rating reflects the Grand Rapids and Southfield, Mich.-based system’s significant scale as a provider and payer in Michigan, Moody’s said. The organization also has good and stable financial performance and liquidity.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

Froedtert ThedaCare Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s solid market position, track record of strong utilization and operations, and strong financial profile, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by its strong operating risk assessment, leading market position in its immediate service area, and strong financial profile, Fitch said.

Holland (Mich.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects Holland Hospital’s stable and strong liquidity and capital-related metrics despite sector-wide operating pressures, Fitch said.

Indiana University Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Indianapolis-based health system’s sustained track record of strong operating margins, ratings agency said.

Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The Falls Church, Va.-based system’s rating is anchored by its role as one of the largest health systems in Virginia with a leading market position in a rapidly growing region with unusually high commercial business, Moody’s said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Mullica Hill, N.J.-based system will return to strong operating cash flows following the operating challenges of 2022 and 2023, as well as the successful integration of Inspira Medical Center of Mannington (formerly Salem Medical Center).

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Kaiser Permanente has an “AA-” rating and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by its strong financial profile, bolstered by a large and diversified revenue base, Fitch said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Rochester, Minn.-based system’s preeminent reputation for clinical care and research, including new discoveries and cutting-edge treatment, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

McLeod Health has an “AA-” rating and stable outlook with Fitch. The Florence, S.C.-based system maintains a leading and growing market position in its primary service area and is expanding the Carolina’s Forest campus in an area that is expected to experience rapid growth over the coming years, Fitch said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Memorial Healthcare System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects that the Hollywood, Fla.-based system will continue to benefit from good strategic positioning of its large, diversified geographic footprint.

Memorial Hermann Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Houston-based system’s leading and expanding market position and strong demand in a growing region, Moody’s said.

Methodist Health System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects the Dallas-based system’s consistently strong operating performance, excellent liquidity, and very good market position.

Monument Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Rapid City, S.D.-based system has a dominant inpatient market position as the leading acute care provider in its geographically broad primary service area

Nationwide Children’s Hospital has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Columbus, Ohio-based system’s strong market position in pediatric services, growing statewide and national reputation, and continued expansion strategies.

Nicklaus Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Miami-based system’s position as the “premier pediatric hospital in South Florida with a leading and growing market share,” Fitch said.

North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The rating reflects the Tupelo-based system’s strong cash position and strong market position with a leading market share in its primary services area, Fitch said.

Northwestern Memorial HealthCare has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Chicago-based system’s growing market position, single operating model and financial discipline, Moody’s said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research, and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Parkland Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Dallas-based system will remain the leading provider of public (safety net) services in the vast Dallas County service area, supported by its tax levy.

Phoenix Children’s has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong cash flow generation that has significantly improved its balance sheet in recent years, Fitch said.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rady Children’s Hospital has an “Aa3” rating and stable outlook with Moody’s. The San Diego-based system’s rating reflects its well-established strengths, including an “extremely high” market share in all of San Diego County, Moody’s said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing position in a stable service area with good population growth and demand for acute care services, Fitch said.

Sarasota (Fla.) Memorial Health Care System has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s leading market position in a growing service area, robust historical operating cash flow levels and strong liquidity position, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

St. Elizabeth Medical Center has an “AA” rating and stable outlook with Fitch. The rating reflects the Edgewood, Ky.-based system’s strong liquidity, leading market position, and strong financial management, Fitch said.

St. Tammany Parish Hospital has an “AA-” rating and stable outlook with Fitch. The Covington, La.-based system has a strong operating risk assessment and very strong financial profile supported by consistently robust operating cash flows, Fitch said.

Stanford Health Care has an “Aa3” rating and positive outlook with Moody’s. The rating reflects the Palo Alto, Calif.-based system’s clinical prominence, patient demand, and its location in an affluent and well-insured market, Moody’s said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong financial profile in the context of its broad and growing reach for high-acuity services, Fitch said.

University Health has an “AA+” rating and stable outlook with Fitch. The San Antonio-based system’s outlook is based on the Bexar County Hospital District’s significant tax margin, good cost management, and strong leverage position relative to its liquidity and outstanding debt.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

University of Kansas Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects Kansas City-based system’s flagship hospital’s important presence as the only academic medical center in Kansas and a major provider of many high end and unique services to a large geographic area, Fitch said.

UW Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Madison, Wis.-based system’s strong clinical reputation, high acuity services, and important role as the academic medical center affiliated with the state’s flagship public university, Moody’s said.

VCU Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Richmond, Va.-based system’s status as one of Virginia’s leading academic medical centers and essential role as its largest safety net provider, supporting excellent patient demand at high acuity levels, Moody’s said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

The drugstore retailer faces debt maturities, while the upending of some strategies introduces new uncertainties, analysts said.

S&P Global Ratings analysts have downgraded Walgreens Boot Alliance by two notches, to ‘BB’ from ‘BBB-’, which puts the drugstore company into speculative-grade territory.

Analysts Diya Iyer and Hanna Zhang cited guidance for the year “notably below” their expectations, and said “material strategic changes, limited cash flow generation, and large maturities in coming years are key risks to the business.”

The company is struggling in its retail business as well as its pharmacy operations, they said in a Friday client note. In the U.S., margins are taking a hit on the pharmacy side from reimbursement pressure and on the retail side from declining sales volume and higher shrink. They expect Walgreens’ S&P Global Ratings-adjusted EBITDA margin to decline more than 100 basis points this fiscal year, dipping below 5%, from 6% last year, though the company’s cost cuts will counter that somewhat.

Walgreens’ debt and its need to refinance much of it represent another “key risk,” they said. This November, Walgreens faces $1.4 billion in maturities, mostly U.S. bonds. Another $2.8 billion comes due in fiscal 2026 and $1.8 billion in fiscal 2027. The analysts called Walgreens’ move to consolidate cash “prudent” in case refinancing isn’t possible.

“We will be monitoring how Walgreens’ new management addresses this large debt load closely amid its persistently weak performance and higher interest rates,” Iyer and Zhang said.

Beyond those financial realities, though, are strategic weaknesses. Ex-Cigna executive Tim Wentworth took over as CEO last fall and this year has overseen a strategic review that has entailed more layoffs and store closures.

Walgreens has also upended some of its plans to expand its medical care operations, divesting of or shrinking many of its original investments and plans. Last month, for example, the company announced it would reduce its stake in value-based medical chain VillageMD, saying it will no longer be the company’s majority owner, after closing dozens of the clinics last year. The company first poured $1 billion into VillageMD in 2020 and more than doubled its stake for another $5.2 billion the following year, but the banner’s waning value helped drive a $6 billion loss in Q2.

Despite such moves, Iyer and Zhang said they continue to see the VillageMD banner as “a significant drag on profitability due to the rising cost of labor, pressures from reimbursement, and lower volumes.”

Walgreens’ acquisition streak led the S&P analysts to believe that it would divest of its Boots U.K. business, which could have helped pay down $8 billion to $10 billion in debt. But the company called off the idea about two years ago.

“We believe these frequent and large changes to the company’s strategic plans diminish management’s credibility to execute on a sustainable and cohesive operating model for Walgreens in both the near and long term,” Iyer and Zhang said.

Gains that Walgreens has managed to eke from its medical operations haven’t managed to offset declines on the retail said, they also said, adding that they are closely watching what it does next with its massive footprint. The company last year announced that it would close 150 stores in the U.S. and 300 in the U.K. and just last month said it was reviewing 25% of its current footprint, with plans to shutter a “significant portion” of its roughly 8,700 stores.

“Our ratings continue to reflect Walgreens’ large scale and its efforts to address its credit metric profile. With almost $140 billion in sales in fiscal 2023 and a diverse array of global businesses, Walgreens remains prominent in the drugstore space,” they said. “However, we think its scale is providing less protection to profitability at least partly due to inconsistent strategic direction.”

Here are 48 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating is based on the Altamonte Springs, Fla.-based system’s competitive market position—especially in its core Florida markets—and its financial profile, Fitch said.

Advocate Health members Advocate Aurora Health and Atrium Health have “Aa3” ratings and positive outlooks with Moody’s. The ratings are supported by the Charlotte, N.C.-based system’s significant scale, strong market share across several major metro areas, and good financial performance and liquidity, Moody’s said.

Ann & Robert H. Lurie Children’s Hospital of Chicago has an “AA” rating and stable outlook with Fitch. The rating is supported by the system’s strong balance sheet with low leverage ratios derived from modest debt, Fitch said.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

Beacon Health System has an “AA-” rating and stable outlook with Fitch. Fitch said the rating reflects the strength of the South Bend, Ind.-based system’s balance sheet.

Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area and Fitch’s expectation that the system will sustain its strong capital-related ratios in the context of the system’s midrange revenue defensibility and strong operating risk profile assessments.

Carilion Clinic has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Roanoke, Va.-based system’s scale, regional significance as a tertiary referral system with broad geographic capture, and a highly integrated physician base with a well-defined culture, Moody’s said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals, and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence, and pediatric trauma status, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The rating reflects the Minneapolis-based system’s strong balance sheet, robust liquidity position, and dominant pediatric market position, Fitch said.

Cincinnati Children’s Hospital Medical Center has an “Aa2” rating and stable outlook with Moody’s. The rating is supported by its national and international reputation in clinical services and research, Moody’s said.

Cleveland Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the system’s strength as an international brand in highly complex clinical care and research and centralized governance model, the ratings agency said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth, Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

Froedtert ThedaCare Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s solid market position, track record of strong utilization and operations, and strong financial profile, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by its strong operating risk assessment, leading market position in its immediate service area, and strong financial profile, Fitch said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Mullica Hill, N.J.-based system will return to strong operating cash flows following the operating challenges of 2022 and 2023, as well as the successful integration of Inspira Medical Center of Mannington (formerly Salem Medical Center).

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Rochester, Minn.-based system’s preeminent reputation for clinical care and research, including new discoveries and cutting-edge treatment, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Memorial Healthcare System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects that the Hollywood, Fla.-based system will continue to benefit from good strategic positioning of its large, diversified geographic footprint.

Memorial Hermann Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Houston-based system’s leading and expanding market position and strong demand in a growing region, Moody’s said.

Methodist Health System has an “Aa3” rating and stable outlook with Moody’s. Moody’s said the rating reflects the Dallas-based system’s consistently strong operating performance, excellent liquidity, and very good market position.

Nationwide Children’s Hospital has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Columbus, Ohio-based system’s strong market position in pediatric services, growing statewide and national reputation, and continued expansion strategies.

Nicklaus Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Miami-based system’s position as the “premier pediatric hospital in South Florida with a leading and growing market share,” Fitch said.

North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The rating reflects the Tupelo-based system’s strong cash position and strong market position with a leading market share in its primary services area, Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research, and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Parkland Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Dallas-based system will remain the leading provider of public (safety net) services in the vast Dallas County service area, supported by its tax levy.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing position in a stable service area with good population growth and demand for acute care services, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

St. Elizabeth Medical Center has an “AA” rating and stable outlook with Fitch. The rating reflects the Edgewood, Ky.-based system’s strong liquidity, leading market position, and strong financial management, Fitch said.

Stanford Health Care has an “Aa3” rating and positive outlook with Moody’s. The rating reflects the Palo Alto, Calif.-based system’s clinical prominence, patient demand, and its location in an affluent and well-insured market, Moody’s said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong financial profile in the context of its broad and growing reach for high-acuity services, Fitch said.

University Health has an “AA+” rating and stable outlook with Fitch. The San Antonio-based system’s outlook is based on the Bexar County Hospital District’s significant tax margin, good cost management, and strong leverage position relative to its liquidity and outstanding debt.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

VCU Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Richmond, Va.-based system’s status as one of Virginia’s leading academic medical centers and essential role as its largest safety net provider, supporting excellent patient demand at high acuity levels, Moody’s said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

The proposal would attempt to stop credit reporting companies from sharing medical debts with lenders.

The Consumer Financial Protection Bureau (CFPB) has proposed a rule intended to remove medical bills from most credit reports, increase privacy protections, help to increase credit scores and loan approvals and prevent debt collectors from using the credit reporting system to coerce people to pay.

The proposal would attempt to stop credit reporting companies from sharing medical debts with lenders and prohibit lenders from making lending decisions based on medical information.

CFPB framed the proposed rule as part of its efforts to address the burden of medical debt and what it called manipulative credit reporting practices.

WHAT’S THE IMPACT?

In 2003, Congress restricted lenders from obtaining or using medical information, including information about debts, through the Fair and Accurate Credit Transactions Act. But federal agencies then issued a special regulatory exception to allow creditors to use medical debts in their credit decisions.

The CFPB is proposing to close the regulatory loophole it said has kept vast amounts of medical debt information in the credit reporting system. The proposed rule is intended to ensure that medical information does not unjustly damage credit scores, and would help keep debt collectors from coercing payments for inaccurate or false medical bills.

Internal research from CFPB shows that a medical bill on a person’s credit report is not a good predictor of whether they will repay a loan. In fact, the analysis shows that medical debts penalize consumers by making underwriting decisions less accurate and leading to thousands of denied applications on mortgages that consumers would repay.

Since these are loans people will repay, the CFPB expects lenders will also benefit from improved underwriting and increased volume of safe loan approvals. In terms of mortgages, the CFPB expects the proposed rule would lead to the approval of approximately 22,000 additional, safe mortgages every year.

In December 2014, the CFPB released a report showing that medical debts provide less predictive value to lenders than other debts on credit reports. Then in March 2022, it released a report estimating that medical bills made up $88 billion of reported debts on credit reports. In that report, the CFPB announced that it would assess whether credit reports should include data on unpaid medical bills.

Since the March 2022 report, the three nationwide credit reporting conglomerates – Equifax, Experian and TransUnion – announced they would take many of those bills off credit reports, and FICO and VantageScore, the two major credit scoring companies, have decreased the degree to which medical bills impact a consumer’s score.

Despite these voluntary industry changes, 15 million Americans still have $49 billion in outstanding medical bills in collections appearing in the credit reporting system.

The complex nature of medical billing, insurance coverage and reimbursement, and collections means that medical debts that continue to be reported are often inaccurate or inflated, CFPB said.

Additionally, the changes by FICO and VantageScore have not eliminated the credit score difference between people with and without medical debt on their credit reports. CFPB expects that Americans with medical debt on their credit reports will see their credit scores rise by 20 points, on average, if the proposed rule is finalized.

Specifically, the proposed rule would remove the exception that broadly permits lenders to obtain and use information about medical debt to make credit eligibility determinations. Lenders would continue to be able to consider medical information related to disability income and similar benefits, as well as medical information relevant to the purpose of the loan, so long as certain conditions are met.

The rule would also prohibit credit reporting companies from including medical debt on credit reports sent to creditors when creditors are prohibited from considering it. Additionally, it would prohibit lenders from taking medical devices as collateral for a loan, and bans lenders from repossessing medical devices, like wheelchairs or prosthetic limbs, if people are unable to repay the loan.

THE LARGER TREND

The CFPB began its rulemaking in September 2023 with the goals of ending coercive debt collection practices and limiting the role of medical debt in the credit-reporting system.

The CFPB also published in 2022 a report describing the effects of medical debt, along with a bulletin on the No Surprises Act to remind credit reporting companies and debt collectors of their legal responsibilities under that legislation.

Here are 37 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

AdventHealth has an “AA” rating and stable outlook with Fitch. The rating is based on the Altamonte Springs, Fla.-based system’s competitive market position — especially in its core Florida markets — and its financial profile, Fitch said.

Advocate Health members Advocate Aurora Health and Atrium Health have “Aa3” ratings and positive outlooks with Moody’s. The ratings are supported by the Charlotte, N.C-based system’s significant scale, strong market share across several major metro areas and good financial performance and liquidity, Moody’s said.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

Carilion Clinic has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Roanoke, Va.-based system’s scale, regional significance as a tertiary referral system with broad geographic capture, and a highly integrated physician base with a well-defined culture, Moody’s said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence and pediatric trauma status, Fitch said.

Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The rating reflects the Minneapolis-based system’s strong balance sheet, robust liquidity position and dominant pediatric market position, Fitch said.

Cincinnati Children’s Hospital Medical Center has an “Aa2” rating and stable outlook with Moody’s. The rating is supported by its national and international reputation in clinical services and research, Moody’s said.

Cleveland Clinic has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the system’s strength as an international brand in highly complex clinical care and research and centralized governance model, the ratings agency said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by its strong operating risk assessment, leading market position in its immediate service area and strong financial profile,” Fitch said.

Inspira Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the Mullica Hill, N.J.-based system will return to strong operating cash flows following the operating challenges of 2022 and 2023, as well as the successful integration of Inspira Medical Center of Mannington (formerly Salem Medical Center).

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Memorial Hermann Health System has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Houston-based system’s leading and expanding market position and strong demand in a growing region, Moody’s said.

Nationwide Children’s Hospital has an “Aa2” rating and stable outlook with Moody’s. The rating reflects the Columbus, Ohio-based system’s strong market position in pediatric services, growing statewide and national reputation and continued expansion strategies.

Nicklaus Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating is supported by the Miami-based system’s position as the “premier pediatric hospital in South Florida with a leading and growing market share,” Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an”AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing positive in a stable service area with good population growth and demand for acute care services, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

St. Elizabeth Medical Center has an “AA” rating and stable outlook with Fitch. The rating reflects the Edgewood, Ky.-based system’s strong liquidity, leading market position and strong financial management, Fitch said.

Stanford Health Care has an “Aa3” rating and positive outlook with Moody’s. The rating reflects the Palo Alto, Calif.-based system’s clinical prominence, patient demand and its location in an affluent and well insured market, Moody’s said.

UChicago Medicine has an “AA-” rating and stable outlook with Fitch. The rating reflects the system’s strong financial profile in the context of its broad and growing reach for high-acuity services, Fitch said.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.