In a surprising turn of events, sources say that CVS Health is exploring the possibility of breaking up its business empire — a move that could unravel years of aggressive vertical integration, including its $70 billion acquisition of health insurer Aetna back in 2017.

While details are still slim, such a move signals just how dire the situation has become for CVSHealth as it navigates mounting financial and regulatory pressures on multiple fronts.

It’s yet another chapter in a story that has seen CVSHealth evolve from a retail pharmacy chain into a health care behemoth — but perhaps one that grew too big, too fast. And to be honest, I’m not surprised. I’ve seen this movie before. In fact, I saw it many times – although each time with different stars – during my 20 years in the health insurance business. One of the most memorable featured Aetna, which in the late 1990s and early 2000s had to retrench, at Wall Street’s insistence, after a buying spree of smaller health insurers that brought the company a ton of unprofitable accounts and disappointing bottom lines. Aetna followed its buying spree with a purging spree, dumping as many as eight million health plan enrollees in short order to get back into Wall Street’s good graces.

It seems that CVSHealth also bought too much too fast. The results? Rising expenses, frustrated patients, and now potential cracks in the corporate structure itself.

CVS: A Cautionary Tale of Vertical Integration

Large corporations like CVS and its peers have used their size to dominate various aspects of health care—whether it’s insurance, retail pharmacy, physician practices and clinics, and controlling the drug supply chain. But as these mega-corporations continue to grow, they also become harder to manage, and their inefficiencies start to become evident.

CVS’s acquisition of Aetna was hailed at the time as a strategic masterstroke — a way to streamline health care by bringing together the different parts of the system under one corporate umbrella. It was supposed to deliver “efficiencies” that would benefit both the company and patients.

But it’s not just the purchase of Aetna. From pharmacy benefit manager Caremark to Aetna to health care providers Signify Health and Oak Street Health — CVS’s business model has become increasingly complex, making it difficult to navigate regulatory scrutiny, rising costs and fierce competition in the retail pharmacy space.

The latest reports suggest that CVS’s board is trying to figure out where Caremark would land in the event of a breakup. Would it stay with the retail side or with the insurance arm?

This isn’t just an internal debate; it’s emblematic of the broader issue—CVS has built a vertically integrated structure that was supposed to work together to improve care, but investors are now questioning how and even if these pieces should fit together.

It’s Been a Hard Few Years for CVS

Federal Trade Commission’s Legal Action Against CVS’s Caremark and Other PBMs

Instead, those supposed efficiencies have largely translated into higher costs for consumers and increased scrutiny from regulators, especially with CVS’s Caremark at the center of anti-competitive practices allegations by the Federal Trade Commission (FTC). PBMs like Caremark control the drug pricing landscape in ways that lack transparency and disproportionately affect patients and independent pharmacies.

Now, as CVS grapples with rising medical costs within its Aetna business — just like its biggest competitors, UnitedHealth and Humana —the company’s management appears to be in damage control mode. While nothing is certain, discussions about splitting the business have reached the boardroom level, according to sources familiar with the matter. This comes as activist investors, like Glenview Capital, push for structural changes to improve CVS’s declining financial performance.

CVS’s Aetna Medicare Advantage Loss in New York City

New York City Mayor Eric Adams had a plan to force city municipal retirees out of traditional Medicare and into a corporate Aetna Medicare Advantage plan. The NYC Organization of Public Service Retirees vehemently opposed the move and spent months fighting it.

In August, a Manhattan Supreme Court judge permanently halted the mayor and Aetna’s attempts.

Wall Street Woes

For CVS Health, 2024 started off bad. CVS missed Wall Street financial analyst’s earnings-per-share expectations for the first quarter of 2024 by several cents. Shareholders’ furor sent CVS’ stock price tumbling from $67.71 to a 15-year low of $54 at one point.

Also in August, CVS Health cut its 2024 forecast for a third time, citing troubles covering seniors via the company’s private Medicare Advantage business. Operating income for CVS Health’s insurance arm, Aetna, dropped a whopping 39% in Q3, which forced the company to shake up its leadership – moving CEO Karen Lynch into the role of managing insurance and publicly firing one of her lieutenants, Executive Vice President Brian Kane.

What’s Next?

The notion that CVS could split its operations would effectively unwind one of the most high-profile health care mergers in recent memory. A split up of the company would mark the end of an era in which health care conglomerates could grow unchecked. CVS’s struggle isn’t happening in isolation—other companies, like Walgreens and Rite Aid, are facing similar financial difficulties and structural questions.

CVS’s potential breakup could signal a broader industry trend toward unwinding massive, vertically integrated health care corporations.

Whether CVS breaks up or not, it’s clear that the model of health care mega-mergers, designed to consolidate power and increase corporate profits, is facing serious headwinds. Cigna recently announced that it is getting out of the Medicare Advantage business and Humana is getting out of the commercial insurance market. UnitedHealth, meanwhile, so far seems to be weathering those headwinds, but it, too, will be facing even more scrutiny by lawmakers and regulators in the months and years ahead.

Regular readers of HEALTH CARE un-covered know that I write frequently about the huge amounts of money the health insurance industry’s pharmacy benefit managers (PBMs) extract from the prescription drug supply chain. I also submitted a comment letter to the Federal Trade Commission two and a half years ago urging it to launch an investigation into PBM business practices that have contributed to the closure of hundreds of independent pharmacies across the country and to millions of Americans walking away from the pharmacy counter without their medications.

On a bipartisan basis, the FTC did launch an inquiry into the PBM business, and today the Commission issued a damning interim report that confirmed what industry critics, including me, have been saying:

Just six companies now control 95% of the pharmacy benefit market, and these Big Insurance-owned middlemen “profit at the expense of patients by inflating drug costs and squeezing Main Street pharmacies.” Below you’ll find the commission’s statement on its preliminary findings.

Last year, we also published a profile of one of the industry’s most vocal critics in Congress, Rep. Earl L. “Buddy” Carter (R-Ga.), a pharmacist by trade who has seen PBM’s profiteering firsthand. In a press release this morning, Carter said:

Since day one in Congress, I’ve been calling on the FTC to investigate PBMs, which use deceptive and anti-competitive practices to line their own pockets while reducing patients’ access to affordable, quality health care. I’m proud that the FTC launched a bipartisan investigation into these shadowy middlemen, and its preliminary findings prove yet again that it’s time to bust up the PBM monopoly. We are losing more than one pharmacy per day in this country, causing pharmacy deserts and taking the most accessible health care professionals in America out of people’s communities. I am calling on the FTC to promptly complete its investigation and begin enforcement actions if – and when – it uncovers illegal and anti-competitive PBM practices.

Carter and several other members of Congress have introduced bipartisan bills to rein in PBMs. The House has passed PBM reform legislation but the Senate has not yet done so, but there is growing support in both chambers to enact one or more bills by the end of the year. The FTC’s interim report should make that more likely to happen.

Read the FTC’s full press release below:

FTC Releases Interim Staff Report on Prescription Drug Middlemen

Report details how prescription drug middleman profit at the expense of patients by inflating drug costs and squeezing Main Street pharmacies

The Federal Trade Commission today published an interim report on the prescription drug middleman industry that underscores the impact pharmacy benefit managers (PBMs) have on the accessibility and affordability of prescription drugs.

The interim staff report, which is part of an ongoing inquiry launched in 2022 by the FTC, details how increasing vertical integration and concentration has enabled the six largest PBMs to manage nearly 95 percent of all prescriptions filled in the United States.

This vertically integrated and concentrated market structure has allowed PBMs to profit at the expense of patients and independent pharmacists, the report details.

“The FTC’s interim report lays out how dominant pharmacy benefit managers can hike the cost of drugs—including overcharging patients for cancer drugs,” said FTC Chair Lina M. Khan. “The report also details how PBMs can squeeze independent pharmacies that many Americans—especially those in rural communities—depend on for essential care. The FTC will continue to use all our tools and authorities to scrutinize dominant players across healthcare markets and ensure that Americans can access affordable healthcare.”

The report finds that PBMs wield enormous power over patients’ ability to access and afford their prescription drugs, allowing PBMs to significantly influence what drugs are available and at what price. This can have dire consequences, with nearly 30 percent of Americans surveyed reporting rationing or even skipping doses of their prescribed medicines due to high costs, the report states.

The interim report also finds that PBMs hold substantial influence over independent pharmacies by imposing unfair, arbitrary, and harmful contractual terms that can impact independent pharmacies’ ability to stay in business and serve their communities.

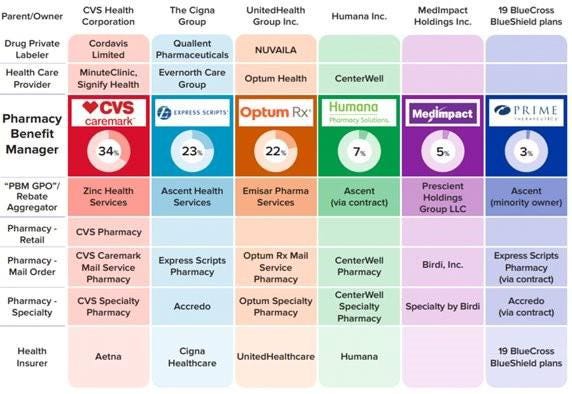

The Commission’s interim report stems from special orders the FTC issued in 2022, under Section 6(b) of the FTC Act, to the six largest PBMs—Caremark Rx, LLC; Express Scripts, Inc.; OptumRx, Inc.; Humana Pharmacy Solutions, Inc.; Prime Therapeutics LLC; and MedImpact Healthcare Systems, Inc. In 2023, the FTC issued additional orders to Zinc Health Services, LLC, Ascent Health Services, LLC, and Emisar Pharma Services LLC, which are each rebate aggregating entities, also known as “group purchasing organizations,” that negotiate drug rebates on behalf of PBMs.

PBMs are part of complex vertically integrated health care conglomerates, and the PBM industry is highly concentrated. As shown in the below image, this concentration and integration gives them significant power over the pharmaceutical supply chain. The percentages reflect the amount of prescriptions filled in the United States.

The interim report highlights several key insights gathered from documents and data obtained from the FTC’s orders, as well as from publicly available information:

Concentration and vertical integration: The market for pharmacy benefit management services has become highly concentrated, and the largest PBMs are now also vertically integrated with the nation’s largest health insurers and specialty and retail pharmacies.

The top three PBMs processed nearly 80 percent of the approximately 6.6 billion prescriptions dispensed by U.S. pharmacies in 2023, while the top six PBMs processed more than 90 percent.

Pharmacies affiliated with the three largest PBMs now account for nearly 70 percent of all specialty drug revenue.

Significant power and influence: As a result of this high degree of consolidation and vertical integration, the leading PBMs now exercise significant power over Americans’ ability to access and afford their prescription drugs.

The largest PBMs often exercise significant control over what drugs are available and at what price, and which pharmacies patients can use to access their prescribed medications.

PBMs oversee these critical decisions about access to and affordability of life-saving medications, without transparency or accountability to the public.

Self-preferencing: Vertically integrated PBMs appear to have the ability and incentive to prefer their own affiliated businesses, creating conflicts of interest that can disadvantage unaffiliated pharmacies and increase prescription drug costs.

PBMs may be steering patients to their affiliated pharmacies and away from smaller, independent pharmacies.

These practices have allowed pharmacies affiliated with the three largest PBMs to retain high levels of dispensing revenue in excess of their estimated drug acquisition costs, including nearly $1.6 billion in excess revenue on just two cancer drugs in under three years.

Unfair contract terms: Evidence suggests that increased concentration gives the leading PBMs leverage to enter contractual relationships that disadvantage smaller, unaffiliated pharmacies.

The rates in PBM contracts with independent pharmacies often do not clearly reflect the ultimate total payment amounts, making it difficult or impossible for pharmacists to ascertain how much they will be compensated.

Efforts to limit access to low-cost competitors: PBMs and brand drug manufacturers negotiate prescription drug rebates some of which are expressly conditioned on limiting access to potentially lower-cost generic and biosimilar competitors.

Evidence suggests that PBMs and brand pharmaceutical manufacturers sometimes enter agreements to exclude lower-cost competitor drugs from the PBM’s formulary in exchange for increased rebates from manufacturers.

The report notes that several of the PBMs that were issued orders have not been forthcoming and timely in their responses, and they still have not completed their required submissions, which has hindered the Commission’s ability to perform its statutory mission. FTC staff have demanded that the companies finalize their productions required by the 6(b) orders promptly. If, however, any of the companies fail to fully comply with the 6(b) orders or engage in further delay tactics, the FTC can take them to district court to compel compliance.

The FTC remains committed to providing timely updates as the Commission receives and reviews additional information.

The Commission voted 4-1 to allow staff to issue the interim report, with Commissioner Melissa Holyoak voting no. Chair Lina M. Khan issued a statement joined by Commissioners Rebecca Kelly Slaughter and Alvaro Bedoya. Commissioners Andrew N. Ferguson and Melissa Holyoak each issued separate statements. The Federal Trade Commission develops policy initiatives on issues that affect competition, consumers, and the U.S. economy. The FTC will never demand money, make threats, tell you to transfer money, or promise you a prize. Follow the FTC on social media, read consumer alerts and the business blog, and sign up to get the latest FTC news and alerts.

With a single ruling, the Federal Trade Commission removed the nation’s occupational handcuffs, freeing almost all U.S. workers from non-compete clauses. The medical profession will never be the same.

On April 23, the FTC issued a final rule, affecting not only new hires but also the 30 million Americans currently tethered to non-compete agreements. Scheduled to take effect in September—subject to the outcome of legal challenges by the U.S. Chamber of Commerce and other business groups—the ruling will dismantle longstanding barriers that have kept healthcare professionals from changing jobs.

The FTC projects that eliminating these clauses will boost medical wages, foster greater competition, stimulate job creation and reduce health expenditures by $74 billion to $194 billion over the next decade. This comes at a crucial moment for American healthcare, an industry in which 60% of physicians report burnout and 100 million people (41% of U.S. adults) are saddled with medical bills they cannot afford.

Like all major rulings, this one creates clear winners and losers—outcomes that will reshape careers and, potentially, alter the very structure of U.S. healthcare.

Winners: Newly Trained Clinicians

Undoubtedly, the FTC’s ruling is a win for younger doctors and nurses, many of whom join hospitals and health systems with the promise of future salary increases and more autonomy. However, by agreeing to stringent non-compete clauses, these newly trained clinicians have little choice but to place their trust in employers that, shielded by air-tight agreements, have no fear of breaking their promises.

Most newly trained clinicians enter the medical job market in their late 20s and early 30s, carrying significant student-loan debt—nearly $200,000 for the average doctor. Eager for stable, well-paying positions, these young professionals quickly settle into their careers and communities, forming strong relationships with friends and patients. Many start families.

But when these clinicians realize their jobs are falling short of the promises made early on, they face a tough decision: either endure subpar working conditions or uproot their lives. Taking a new job 25 or 50 miles away or moving to a different state are often are only options to avoid breaching a non-compete clause.

In a 570-page supplement to its ruling, the FTC published testimonials from dozens of healthcare professionals whose lives and careers were harmed by these clauses.

“Healthcare providers feel trapped in their current employment situation, leading to significant burnout that can shorten their career longevity,” said one physician working in rural Appalachia.

By banning non-competes, the FTC’s rule will boost career mobility for all clinicians within their own communities. This change will likely spur competition among employers—leading to improved pay and benefits to attract and, equally important, retain top talent. And with the reassurance that they can easily switch jobs if their current employer falls short of expectations, clinicians will enjoy greater professional satisfaction and less burnout.

Winners: Patients In Competitive Markets

Benefits that accrue to doctors and nurses from the FTC’s ban will translate directly to improved outcomes for patients. For example, we know that physicians who report symptoms of burnout are twice as likely to commit a serious medical error. Studies have shown the inverse is true, as well: healthcare providers who are satisfied with their jobs tend to have lower burnout rates, which is positively correlated with improved patient outcomes.

Once freed from restrictive non-compete clauses, many clinicians will practice elsewhere within the community. To attract patients, they will have to offer greater access, lower prices and more personalized service. Others with the freedom to choose will join outpatient centers that offer convenient and efficient alternatives for diagnostic tests, surgery and urgent medical care, often at a fraction of the cost of traditional hospital services. In both cases, increased competition will give patients improved medical care and added value.

Losers: Large Health Systems

Large health systems, which encompass several hospitals in a geographic area, have traditionally relied on non-compete agreements to maintain their market dominance. By barring high-demand medical professionals such as radiologists and anesthesiologists from joining competitors or starting independent practices, these systems have been able to suppress competition and force insurers to pay more for services.

Currently, these systems can demand high reimbursement rates from insurers while also maintaining relatively low wages for staff, creating a highly profitable model. Yale economist Zack Cooper’s research shows the consequence of the status quo: prices go up and quality declines in highly concentrated hospital markets.

The FTC’s ruling challenges those conditions, potentially dismantling monopolistic market controls. As a result, insurers will no longer be forced to contend with a single, dominant provider. And with health systems pushed to offer better wages and benefits to retain their top talent, bottom lines will shrink.

While nonprofit hospitals and health systems are not currently under the FTC’s jurisdiction, the agency has pointed out that these facilities might be at “a self-inflicted disadvantage in their ability to recruit workers.” Moreover, as Congress intensifies scrutiny on the nonprofit status of U.S. health systems, hospitals that do not voluntarily align with the FTC’s guidelines may find themselves compelled to do so through legislative actions.

Losers: Hospital Administrators

Individual hospitals have faced a unique challenge over the past decade. Across the country, inpatient numbers are falling, which makes it harder for hospital administrators to fill beds overnight. This trend has been driven by advancements in medical technology and new practices that enable more outpatient procedures, along with changes in insurance reimbursements favoring less costly outpatient care. As a result, hospital administrators have been compelled to adapt their financial strategies.

Nowadays, outpatient services account for about half of all hospital revenue. These range from physician consultations to specialized procedures like radiological and cardiac diagnostics, chemotherapy and surgeries.

Medicare and other insurers typically pay hospitals more for these outpatient services than they pay local doctors and other facilities. Knowing this, hospitals are hiring community doctors and acquiring diagnostic and procedural facilities, then boosting profitability by charging the higher hospital rates for the same services.

Hospital administrators know that this strategy only works if the newly hired clinicians are prohibited from quitting and returning to practice within the same community. If they do, their patients are likely to go with them. This is why the non-compete clauses are so essential to a hospital’s financial success.

As expected, the American Hospital Association opposes the FTC’s rule, arguing that non-compete clauses protect proprietary information. In practice, most of the doctors affected by the ban are providing standard medical care and have no proprietary knowledge that requires protection.

Looking Ahead

Today’s hospital systems are starkly divided between haves and have-nots. Facilities in affluent areas often enjoy high reimbursement rates from private insurers, boosting financial success and administrator salaries. In contrast, rural hospitals grapple with low patient volumes while facilities in economically disadvantaged, high-population areas face greater financial difficulties.

The current model is not working. The old ways of doing things—enforcing non-competes, charging higher fees for identical services and promoting market consolidation to hike prices—are not sustainable solutions.

The abolition of non-compete agreements will produce both winners and losers. In the healthcare sector, the ultimate measure of a policy’s impact should be its effect on patients—and the overwhelming evidence suggests that eliminating these clauses will benefit them greatly.

With the Federal Trade Commission (FTC) issuing a final rule last month that bans noncompete agreements nationwide, the graphic above is our attempt to categorize the current status of complex state noncompete laws that affect physicians.

Except in the event of a business sale, five states—California, North Dakota, Minnesota, Nebraska, and Oklahoma—ban all noncompete agreements for all employees, and at least 19 states either ban them for physicians or place varying limits on them for physicians.

Examples of these limits include a narrow law in Florida that allows noncompetes to be voided if there is only one employer of a physician specialty in a county, and a Tennessee law that only permits physician noncompetes that bar a physician from practicing at facilities where their former employer provides services.

As a noncompete agreement can restrict a physician’s ability to practice near a former employer for years, bans on physician noncompete agreements have been shown to improve community access to care. One study found that, compared to places that allow them, places that banned noncompetes for physicians saw increased physician employment, the opening of more physician practices, and a lower likelihood of practice closures.

Should the new FTC ban survive the mounting legal challenges it faces, its effect on the physician labor market may be limited, as not-for-profit organizations fall outside the FTC’s traditional enforcement jurisdiction. However, the agency has indicated a willingness to reevaluate an entity’s not-for-profit status and stated that “some portion” of tax-exempt hospitals could fall under the final rule’s purview.

Regulators sued the PE firm last year for consolidating anesthesiology services in Texas with its portfolio company, U.S. Anesthesia Partners. Now, a judge is holding Welsh Carson blameless.

A Texas federal judge has dismissed the Federal Trade Commission’s antitrust lawsuit against Welsh, Carson, Anderson and Stowe in a big win for the private equity firm. However, the government’s suit against Welsh Carson’s portfolio company U.S. Anesthesia Partners was allowed to continue.

Last year, the FTC sued Welsh Carson and USAP, alleging they pursued a buying spree of anethesiology practices in Texas to create a dominant provider that used its market power to suppress competition and increase the cost of anesthesiology services.

Welsh Carson, which formed USAP in 2012, has since whittled down its ownership of the provider from more than 50% to 23%, and argued that precludes it from being included in the suit. The FTC argued the firm effectively remains in control of USAP.

However, U.S. District Judge Kenneth Hoyt granted Welsh Carson’s motion to dismiss the suit on Tuesday, essentially finding that private equity firms are not liable for the actions of their portfolio companies.

The FTC was unable to prove “any authority for the proposition that receiving profits from an entity that may be violating antitrust laws is itself a violation of antitrust laws,” Hoyt wrote in his opinion.

Hoyt found that Welsh Carson holding a minority share in USAP does not reduce competition, despite USAP’s acquisitions potentially being anticompetitive themselves. In addition, comments from Welsh Carson executives expressing a desire to consolidate other healthcare markets don’t show that the PE firm plans to violate antitrust laws.

If Welsh Carson signals “beyond mere speculation and conjecture” that it’s actually about to violate the law, the FTC can lodge a new lawsuit, the judge wrote.

A spokesperson for Welsh Carson said the firm is “gratified” that the court dismissed the case.

”As we have said from the beginning, this case was without factual or legal basis,” the spokesperson said.

However, Hoyt denied USAP’s motion to dismiss.

The FTC is arguing that USAP — which is the largest anesthesia practice in Texas — leveraged its size to raise prices in the state, resulting in patients, employers and insurers paying tens of millions of dollars more each year for anesthesia services. In addition, USAP allegedly paid a competitor, Envision Healthcare, $9 million to stay out of the Dallas market for five years.

USAP has been criticized for using similar practices to grow in other states, including Colorado.

USAP argued the FTC was overreaching its authority, and regulators’ allegations of anticompetitive conduct were meritless. Hoyt disagreed, pointing out that USAP continues to own the acquired anesthesia groups and continues to charge high prices, including under price-setting agreements. Overall, USAP’s “monopolization scheme remains intact,” according to the opinion.

“The FTC has plausibly alleged acquisitions resulting in higher prices for consumers, along with a market allocation and price-setting scheme. It would be premature to dismiss these claims at this stage,” Hoyt said.

Either way, the dismissal against Welsh Carson is a setback for the FTC, which has taken a more aggressive stance against anticompetitive behaviors in the healthcare industry under the Biden administration.

In December, the FTC and the Department of Justice finalized new guidelines for merger reviews taking aim at previously overlooked practices. Those include private equity roll-ups, when firms acquire and merge multiple small businesses into one larger company — like Welsh Carson’s strategy to grow USAP.

PE firms have acquired hundreds of physician practices across the U.S. in recent years, despite controversy over negative effects on medical quality and cost. One study from 2022 found when private equity took over physician practices, they raised prices by 20% on average.

After UnitedHealth Group CEO Andrew Witty’s appearances at two congressional committee hearings last week, I had planned to write a story about what the lawmakers had to say. One idea I considered was to publish a compilation of some of the best zingers, and there were plenty, from Democrats and Republicans alike.

I reconsidered that idea because I know from the nearly half-century I have spent on or around Capitol Hill in one capacity or another that those zingers were carefully crafted by staffers who know how to write talking points to make them irresistible to the media. As a young Washington correspondent in the mid-to-late’70s, I included countless talking points in the stories I wrote for Scripps-Howard newspapers. After that, I wrote talking points for a gubernatorial candidate in Tennessee. I would go from there to write scads of them for CEOs and lobbyists to use with politicians and reporters during my 20 years in the health insurance business.

I know the game. And I know that despite all the arrows 40 members of Congress on both sides of the Hill shot at Witty last Wednesday, little if anything that could significantly change how UnitedHealth and the other big insurers do business will be enacted this year.

Money in politics is the elephant in any Congressional hearing room or executive branch office you might find yourself in (and it’s why I coauthored Nation on the Take with Nick Penniman).

You will hear plenty of sound and fury in those rooms but don’t hold your breath waiting for relief from ever-increasing premiums and out-of-pocket requirements and the many other barriers Big Insurance has erected to keep you from getting the care you need.

It is those same barriers doctors and nurses cite when they acknowledge the “moral injury” they incur trying to care for their patients under the tightening constraints imposed on them by profit-obsessed insurers, investors and giant hospital-based systems.

Funny not funny

Cartoonist Stephan Pastis captured the consequences of the corporate takeover of our government, accelerated by the Supreme Court’s 2010 landmark Citizens United vs. Federal Election Commission ruling, in his Pearls Before Swine cartoon strip Sunday.

Rat: Where are you going, Pig?

Pig: To a politician’s rally. I’m taking my magic translation box.

Rat: He doesn’t speak English?

Pig: He speaks politicianish. This translates it into the truth. Come see.

Politician: In conclusion, if you send me to Washington, I’ll clean up this corrupt system and fight for you everyday hard-working Americans. God bless you. God bless the troops. And God bless America.

Magic translation box: I am given millions of dollars by the rich and the powerful to keep this rigged system exactly as it is. Until you change that, none of this will ever change and we’ll keep hoping you’re too distracted to notice.

Politician’s campaign goon: We’re gonna need a word with you.

Magic translation box: This is too much truth for one comic strip. Prepare to be disappeared.

Rat: I don’t know him.

Back to Sir Witty’s time on the hot seat. It attracted a fair amount of media coverage, chock full of politicians’ talking points, including in The New York Times and The Washington Post. (You can read this short Reuters story for free.) Witty, of course, came equipped with his own talking points, and he followed his PR and legal teams’ counsel: to be contrite at every opportunity; to extol the supposed benefits of bigness in health care (UnitedHealth being by far the world’s largest health care corporation) all the while stressing that his company is not really all that big because it doesn’t, you know, own hospitals and pharmaceutical companies [yet]; and to assure us all that the fixes to its hacked claims-handling subsidiary Change Healthcare are all but in.

Congress? Meh. Paying for care? WTF!

Wall Street was relieved and impressed that Witty acquitted himself so well. Investors shrugged off the many barbs aimed at him and his vast international empire. By the end of the day Wednesday, the company’s stock price had actually inched up a few cents, to $484.11. A modest 2.7 million shares of UnitedHealth’s stock were traded that day, considerably fewer than usual.

Instead of punishing UnitedHealth, investors inflicted massive pain on its chief rival, CVS, which owns Aetna. On the same day Witty went to Washington, CVS had to disclose that it missed Wall Street financial analyst’s earnings-per-share expectations for the first quarter of 2024 by several cents. Shareholders’ furor sent CVS’ stock price tumbling from $67.71 to a 15-year low of $54 at one point Wednesday before settling at $56.31 by the time the New York Stock Exchange closed. An astonishing 65.7 million shares of CVS stock were traded that day.

Postscript: I do want to bring to your attention one exchange between Witty and Rep. Buddy Carter (R-Ga.) during the House Energy and Commerce committee hearing. Carter is a pharmacist who has seen firsthand how UnitedHealth’s virtual integration–operating health insurance companies with one hand and racking up physician practices and clinics with the other–and its PBM’s business practices have contributed to the closure of hundreds of independent pharmacies in recent years. He’s also seen patients walk away from the pharmacy counter without their medications because of PBMs’ out-of-pocket demands (often hundreds and thousands of dollars). And he’s seen other patients face life-threatenng delays because of industry prior authorization requirements. Carter was instrumental in persuading the Federal Trade Commission to investigate PBMs’ ownership and business practices. He told Witty:

I’m going to continue to bust this up…This vertical integration in health care in general has got to end.

Policymakers and the media have been increasingly attentive to mergers and acquisitions and other potentially anticompetitive practices of hospitals, physicians, and other health care providers.

Consolidation has the potential to increase efficiency and help some struggling providers to keep their doors open in relatively underserved areas, but it can also reduce market competition and ease pressure on providers to lower prices or invest in quality improvements. A substantial body of evidence shows that consolidation has led to higher prices without clear evidence of improvements in quality, which has implications for consumers and employers. As a result, some have proposed strengthening antitrust regulation—which aims to protect competitive markets—as a tool for tackling rising health care costs, increasing the affordability of care, and reducing the large number of adults with medical debt.

Federal and state antitrust agencies play a role in challenging anticompetitive practices of health care providers and other businesses. At the federal level, the Federal Trade Commission (FTC) and the Department of Justice (DOJ) share responsibility for enforcing federal antitrust laws, including the Sherman Act, the Clayton Act, and the FTC Act. State attorneys general (AG) offices also have the authority to bring action under federal antitrust law, as well as under state statutes, which sometimes expand upon federal law.

This issue brief explains the role of federal and state antitrust agencies in challenging anticompetitive practices among health care providers, including the legal authority of federal and state agencies, the role that they play in enforcing antitrust laws, and proposed options for strengthening their authority. The brief focuses on health care providers, though many of the principles discussed in this issue brief apply to the practices of other health care entities as well, such as health insurers and pharmacy benefit managers (PBMs) (which are currently being reviewed by the FTC). While the focus of this brief is on the role of government agencies, antitrust law also authorizes private parties, such as employer health plans, to challenge anticompetitive practices in the courts.

What types of anticompetitive practices do governments challenge and why?

Governments challenge anticompetitive practices to promote competitive markets, often for the benefit of consumers (e.g., patients and health plan enrollees).1 Governments seek to address a variety of anticompetitive practices that may lead to higher prices without commensurate improvements in quality of care. These include anticompetitive mergers and acquisitions (referred to as “mergers” in this brief), and other activities that hinder competition (referred to as “nonmerger anticompetitive practices” in this brief).

Provider consolidationcan be beneficial to consumers in some instances and detrimental in others. On the one hand, consolidation has the potential to increase efficiency, such as by allowing providers to purchase supplies in bulk at a discount or by facilitating the coordination of care across different providers. On the other hand, consolidation has the potential to lead to worse outcomes for consumers by increasing providers’ market power and decreasing competition, which enhances the ability of providers to negotiate for higher prices (increasing costs for consumers and employers) and reduces the pressure on providers to invest in quality improvements. A substantial body of evidence shows that consolidation has led to higher prices without clear indications of quality improvements, though the strength of this evidence varies based on the type of consolidation and provider.

There are three main types of mergers:

Horizontal mergers occur when there is consolidation between providers that offer the same or similar services, such as when a health system acquires a hospital or when two physician practices that provide overlapping services merge. Horizontal mergers can raise concerns about competition because they, by definition, reduce competitiveness when occurring between providers in the same market, and because consolidated entities can take actions to increase and protect their market power.

Vertical mergers occur when there is consolidation between providers that offer different services along the same supply chain, such as when a hospital acquires a physician practice. Vertical mergers can raise anticompetitive concerns, for example, if physicians refer patients to hospitals within their health system rather than to competing hospitals. Some mergers may entail both vertical and horizontal consolidation (e.g., if a health system acquires a physician group that provides services offered by the system’s existing physician group).

Cross-market mergers occur when there is consolidation between providers that operate in different geographic markets.2 Cross-market mergers may raise concerns about competition, for example, if a health system with providers in different areas of a state is able to use its dominant position in one market to negotiate higher prices in another when contracting with a given health plan (e.g., a state employee plan with enrollees that reside in several markets).

Governments also challenge other types of anticompetitive practices, such as the use of anticompetitive clauses in contracts between providers and insurers or providers and workers. Anticompetitive contract clauses give dominant parties an unfair advantage over potential competitors and can lead to higher prices. For example, some health systems have highly regarded hospitals (also known as “must have” hospitals) that insurers need to include in their provider networks in order to attract enrollees, which gives these systems substantial bargaining leverage over insurers. These health care systems can in turn use this bargaining leverage to pressure insurers to contract with all providers in the system (through “all-or-nothing clauses”), shielding expensive or low-quality members from competition with more desirable providers. The textbox below provides definitions of various anticompetitive contract clauses.

All-or-nothing clauses require an insurer that wants to contract with a particular provider in a system (such as a must-have hospital) to contract with all providers in that system.

Anti-tiering/anti-steering clauses prevent an insurer from putting a given provider in a non-preferred provider network tier or from using other incentives or tools to steer patients to competing providers. This can incentivize patients to use that provider, even if a higher-value provider is also in-network.

Exclusive contracting clauses prohibit an insurer from including competing providers in their provider network, so that a given provider is the only in-network option in a given area.

Non-compete clauses prevent a worker employed with a given provider from taking a job with a competing provider or starting a new practice within a certain distance for some duration of time.

Most favored nation clauses require a provider to offer an insurer the lowest rates of all the insurers with which it has contracted. While the examples above create favorable terms for providers in their contracts with insurers, most favored nation clauses create favorable terms for insurers in their contracts with providers.4

What federal antitrust laws govern anticompetitive practices?

There are three primary federal antitrust laws—the Sherman Act, the Clayton Act, and the FTC Act—that prohibit anticompetitive mergers and other anticompetitive practices.

The Sherman Act (1890) broadly prohibits anticompetitive practices. It has been used to challenge various anticompetitive practices, such as mergers, wage suppression, agreements among competing businesses to fix prices, and anticompetitive contracting clauses.

The Clayton Act(1914) builds on the Sherman Act by explicitly prohibiting anticompetitive mergers as well as other types of anticompetitive practices that are not clearly addressed by the Sherman Act (such as by barring the same individual from serving on the board of directors for two competing health systems, with some exceptions). Additionally, as amended under the Hart-Scott-Rodino Act in 1976, the law requires that merging entities report their plans in advance to federal regulators in certain cases where the transaction exceeds a specified value ($111.4 million in 2023), which gives regulators time to investigate and intervene if needed.

The Federal Trade Commission (FTC) Act(1914) created the FTC and prohibits “unfair methods of competition” and “unfair or deceptive acts or practices.” The FTC Act encompasses the same types of violations that are covered by the Sherman Act and the Clayton Act, in addition to other anticompetitive practices, and grants the FTC regulatory authority. Unlike the Sherman Act and the Clayton Act, the Act generally cannot be applied to nonprofit entities.5

Some forms of business practices, such as almost all instances where competitors coordinate to raise prices, are inherently illegal under federal law. The legality of other types of business practices depends on the context. For instance, when government agencies challenge a merger, courts assess whether the merger would likely harm competition in a given market.

What is the FTC’s role in enforcing federal antitrust law?

Two federal agencies—the FTC and DOJ—have overlapping, as well as distinct, authority to challenge anticompetitive practices under federal law. The FTC is the only entity that can enforce the FTC Act. Although this Act generally cannot be applied to nonprofit entities, the FTC has the authority to enforce the Clayton Act against nonprofit entities (in addition to for-profit entities), such as by challenging anticompetitive mergers among nonprofits. The DOJ has the authority to enforce the Sherman and Clayton Acts. States can also bring lawsuits under federal antitrust law, as can some private parties, such as competing providers.

The FTC focuses on “protecting the public from deceptive or unfair business practices and from unfair methods of competition.” This includes challenging activities such as misleading advertisements, violations of consumers’ data privacy, and efforts to accumulate market power through mergers and other anticompetitive practices. For instance, the FTC sued Facebook in 2020, alleging, in part, that the company had sought to maintain its monopoly power by buying up competitors, such as Instagram and WhatsApp.

The FTC plays a larger role than the DOJ in enforcing federal antitrust law in health care provider markets, though there are gaps in its authority. The FTC and DOJ have each developed expertise in certain areas and have tended to divide merger oversight accordingly, with the FTC typically overseeing provider markets and the DOJ typically overseeing insurance markets (see more below). However, although the FTC has broad authority to challenge anticompetitive mergers, its authority to challenge other anticompetitive practices often excludes nonprofits. Nonprofit ownership is common in provider markets. For example, nonprofits account for about three-fifths (58%) of community hospitals in 2023. The DOJ may fill in for the FTC when the FTC does not have the authority to challenge nonprofit providers that are engaging in certain anticompetitive practices (see example of Atrium Health below).

The FTC has successfully challenged several hospital mergers over the past two decades. Beginning in the 1990s and for several years afterwards, the FTC had difficulty challenging hospital mergers in the courts, allowing rapid consolidation in the hospital sector to continue unabated.6 Since the late 2000s, the FTC has since been more successful in challenging hospital mergers, reflecting advances in both economics and the FTC’s new legal strategies.7 However, the FTC challenges only a fraction of hospital mergers, and it is difficult to know the extent to which mergers that go unchallenged have an adverse impact on consumers, in terms of costs and quality. For instance, in 2022, the FTC challenged 3 hospital mergers and, in each case, the hospitals abandoned their plans to merge, while one analysis documented 53 hospital merger announcements in that year. The same analysis identified more hospital merger announcements in the years prior to the start of the COVID-19 pandemic (e.g., 92 in 2019).

Example: FTC & Advocate Health Care Network

In 2015, the FTC brought a legal challenge against a proposed merger of two Chicago-area health systems: Advocate Health Care Network and NorthShore University Health System. The FTC argued that the combined entity would control over half of the market for general acute care inpatient hospital services, compared to the next largest provider, which would have only controlled 15% of the market. The court placed a temporary block on the merger, and the systems ultimately abandoned their plans to merge before the case went to trial.

The FTC has played a smaller role in challenging physician mergers. A key challenge is that physician mergers tend to be smaller, and physician groups often grow slowly over time by acquiring small group practices and hiring new physicians. As a result, physician groups often do not need to report mergers to federal regulators as their transactions tend to fall below Hart-Scott-Rodino reporting thresholds (though regulators can still challenge mergers that they learn about in other ways). Additionally, because they tend to be small, any given merger may not have an appreciable effect on market power, even if the cumulative effect of these mergers leads to a large concentration of market power over time.

Vertical mergers in health care provider markets have largely escaped FTC enforcement and the FTC has never challenged a cross-market merger, though it has expressed interest in both practices. For instance, in 2021, the FTC announced that it would begin to study the effect of vertical mergers between health care facilities and physician groups. The FTC previously conducted studies of horizontal mergers in advance of successful litigation. The FTC has also investigated specific instances of cross-market mergers, although it has yet to bring a challenge.

Example: FTC & St. Luke’s Health System

In 2012, St. Luke’s Health System in Idaho attempted to acquire Saltzer Medical Group, a physician practice group. Although this proposed acquisition had elements of a vertical merger, the FTC challenged it as a horizontal merger, i.e., on the basis that St. Luke’s would obtain a dominant market share for adult primary care physician services. Courts ruled in favor of the FTC and ordered that St. Luke’s divest Saltzer Medical Group. This was the first time that the FTC received a court decision for a case challenging a hospital or health system’s acquisition of competing physician practices.

The FTC has not played a large role in overseeing nonmerger anticompetitive practices in nonprofit health care provider markets, such as the use of anticompetitive contract clauses. This may reflect the fact that the FTC’s authority to challenge and regulate nonmerger anticompetitive practices generally excludes nonprofit entities. Nonetheless, the FTC has brought legal challenges in some instances, such as cases where separate physician groups have coordinated with each other to raise prices. Relatedly, the FTC drew on its regulatory authority when it proposed a rule in 2023 that would ban non-compete clauses between employers and workers.

What is the DOJ’s role in enforcing federal antitrust law?

The DOJ enforces a wide range of laws on behalf of the federal government, including—through its Antitrust Division—anticompetitive practices. For instance, in one landmark antitrust case in the 1990s, the DOJ sued Microsoft, alleging that the company had illegally sought to protect its monopoly power. The DOJ argued that the company had done so, in part, by requiring computer manufacturers that wanted to use Microsoft’s popular Windows operating system to also include Internet Explorer as a default.

Although the FTC typically oversees the conduct of health care providers, the DOJ has occasionally done so as well (see example below).

Example: DOJ & Atrium Health

In 2016, the DOJ filed a lawsuit against Carolinas Healthcare System, also known as “Atrium Health.” The DOJ claimed that Atrium had violated federal antitrust law by, among other things, entering into contracts with insurers that contained anti-steering and anti-tiering clauses. Atrium Health system and the DOJ reached a settlement agreement before trial where the system agreed, in part, to stop using these contract clauses.

The DOJ typically takes the lead in promoting competition in health insurance markets. For instance, in 2017, the DOJ, along with some state governments, successfully prevented a proposed merger between Anthem and Cigna—which would have been the largest merger of health insurance companies on record—and a proposed merger between Aetna and Humana.

How do the FTC and DOJ work together on antitrust issues?

The FTC and DOJ have a clearance process to determine which agency will investigate and challenge a given merger. The FTC and DOJ have each developed expertise in different areas and have tended to divide merger oversight accordingly, with the FTC typically overseeing provider markets and the DOJ typically overseeing insurance markets. The division of labor is formalized through a clearance process that determines which agency will investigate a proposed transaction based on its expertise and other factors, such as its capacity and ties to a given case.

The FTC and DOJ collaborate on guidelines that establish how they determine whether to challenge a given merger. This includes the Horizontal Merger Guidelines, which, as the name suggests, outline the criteria that the FTC and DOJ consider when reviewing horizontal mergers. For instance, the guidelines indicate that the agencies evaluate the effects of a merger on market concentration based on a measure known as the “Herfindahl-Hirschman Index” (HHI) (see textbox below). The guidelines also indicate that the agencies consider the possible benefits of a given merger, such as whether a merger might allow research to be conducted more effectively.

Herfindahl-Hirschman Index (HHI)

The HHI is calculated based on provider market shares for a given product—such as inpatient general acute care services or inpatient orthopedic surgical services—and geographic market. The HHI for a market can range from nearly 0 (a perfectly competitive market) to 10,000 (a market with a single provider). The Horizontal Merger Guidelines define the level of market concentration as follows:

Unconcentrated: HHI < 1,500

Moderately concentrated: HHI between 1,500 and 2,500

Highly concentrated: HHI > 2,500

Although markets for inpatient hospital services are now often highly concentrated, there is wide variation across the country. For instance, one study estimated that, in 2021, the New York City metro area had an HHI of 753 for inpatient hospital services, while the Wilmington, North Carolina metro area had an HHI of 7,600.

The FTC and DOJ have also released a set of Vertical Merger Guidelines, though the FTC withdrew from these guidelines in 2021. Some economists are more critical of the Vertical Merger Guidelines than the Horizontal Merger Guidelines, perhaps reflecting the fact that there is less consensus about the effects of vertical consolidation and the proper role of antitrust enforcement.

In July 2023, the FTC and DOJ released a draft version of their updated merger guidelines, which would apply to both horizontal and vertical mergers and which indicate that the agencies will be scrutinizing a broader range of mergers. Among other changes, the draft guidelines expand the definition of highly concentrated markets, rely on a lower threshold for identifying large changes in market concentration, consider the combined effect of a series of acquisitions (e.g., of a health system acquiring several small physician practices over time), and add an explicit discussion of the agencies’ views on how workers may be negatively impacted when their employers merge. These guidelines might also be used to challenge cross-market mergers, although this is not yet clear. The deadline for public comments on the draft guidelines is September 18, 2023.

In addition to working together on general merger guidelines, the DOJ and FTC have in the past collaborated on antitrust policy statements that are specific to health care, though both agencies withdrew from these statements in February 2023 and July 2023, respectively, arguing that the statements are outdated based on changes in health care markets.8

What is the role of states in enforcing antitrust law?

States can bring legal challenges under federal antitrust law. States may do so through their AG offices as either a purchaser of health care (for instance, through state employee health plans) or on behalf of their residents. States sometimes file lawsuits jointly with each other or with the federal government, which can help overcome resource constraints. States and the federal government may play complementary roles, with the federal government providing greater resources and general antitrust expertise and states providing more specialized knowledge of local market conditions.

Most states have passed laws that expand oversight of provider mergers, which may lead to additional legal challenges. Thirty-four states and DC require that at least some hospitals notify state AG offices of their plans to merge, expanding on federal reporting requirements. For instance, Rhode Island requires all hospitals to do so, regardless of the value of the transaction. Additionally, thirteen states and DC require that some or all types of providers receive approval from the government prior to merging, instead of requiring that the government file a lawsuit to challenge a merger. Eleven states require AG offices to consider relatively expansive criteria when reviewing health care mergers. For instance, California law requires the AG office to consider criteria such as the general public’s interest and the effect of a merger on access to care.

Some states have prohibited certain types of anticompetitive contract clauses. These laws either broadly prohibit a given type of clause or ban their use in only specific circumstances. Regarding contracts between insurers and dominant providers, two states (Massachusetts and Nevada) have laws restricting at least some all-or-nothing clauses and anti-tiering or anti-steering provisions, and five states (Massachusetts, Minnesota, Nevada, New Hampshire, and Wisconsin) have laws restricting exclusive contracting. Additionally, 22 states restrict non-compete provisions—which dominant providers sometimes use in contracts with their workers—and 20 states restrict most favored nation clauses, which dominant insurers sometimes use in their contracts with providers.

Example: California & Sutter Health

In 2018, the California AG joined a lawsuit that had been initiated on behalf of some group health plans against Sutter Health, a large nonprofit health system in the state. The parties argued that Sutter had used anticompetitive contract clauses—such as all-or-nothing and anti-tiering provisions—to increase prices. In 2019, Sutter agreed to a settlement agreement that required the system to abandon the relevant contract clauses and to pay $575 million in damages, among other things.

Some states have enacted laws that have the potential to shield health care providers from antitrust scrutiny in certain instances. For example, 19 states have Certificate of Public Advantage (COPA) laws, which immunize a merger from antitrust challenges while directly regulating the merged entity for a period of time, such as by limiting price increases or prohibiting certain contracting practices. The intent of COPA laws is to facilitate mergers that are perceived as being beneficial overall while mitigating anticompetitive concerns through state oversight. However, the FTC and some researchers have been critical of these laws, arguing, for example, that states have not followed through in providing ongoing oversight following a given merger. Other state policies, such as Certificate of Need (CON) statutes—which attempt to reduce costs by restricting, for example, the construction of new facilities when they do not meet a community need—may also play a role in limiting competition or preventing antitrust scrutiny.

What are the potential remedies in antitrust enforcement?

Federal or state agencies challenging a merger can seek structural remedies or conduct remedies (also known as “behavioral remedies”).

Structural remedies mitigate consolidation by preventing a merger from moving forward, breaking up mergers that have already taken place, or requiring a merged entity to sell off a portion of its business.

Conduct remedies entail restrictions or requirements imposed on providers after a merger, such as by limiting the prices providers can charge, prohibiting providers from engaging in certain contracting practices, or requiring providers to spend a minimum amount on community benefits.

Conduct remediesmay be less effective than structural remedies in certain circumstances, as they tend to be time-limited and government agencies may not have the resources to monitor and enforce them. However, where markets are already concentrated and regulators are reluctant to break up merged entities, conduct remedies may be the only option.

When the government challenges proposed mergers before they occur, the recourse is typically to prevent the merger from moving forward. Antitrust enforcers have only infrequently attempted to unwind mergers that have already taken place, which the FTC describes as a “difficult and potentially ineffective” process.

There are other ways in which the government can be successful in challenging anticompetitive mergers. For example, the government and merging providers may avoid trial through a settlement agreement or consent decree. In this scenario, the government drops its legal challenge in exchange for structural or conduct remedies. Additionally, providers may abandon a merger after a lawsuit is announced or a court makes a preliminary ruling against the merger or may decide not to attempt to merge in the first place in anticipation that doing so would be successfully challenged in court.

Example: FTC & Phoebe Putney Health System

In 2011, Phoebe Putney Health System acquired a hospital from HCA in Albany, Georgia. The FTC challenged the merger and eventually reached a settlement agreement with the providers. The settlement agreement allowed the merger to persist but imposed conduct remedies, including that Phoebe Putney notify the FTC before acquiring other health care providers in the area.

The outcomes of successful legal challenges to nonmerger anticompetitive practices are similar, though the remedy would involve abandoning the relevant business practice (e.g., no longer using anticompetitive contract clauses).

What are some practical challenges facing antitrust enforcement?

There are at least a few challenges that may limit the ability of the federal government and states to foster competitive provider markets through antitrust enforcement:

It is difficult to break up mergers after they have already occurred, and many provider markets are already highly concentrated. For example, one study estimated that the vast majority (90%) of metropolitan statistical areas (MSAs) had highly concentrated hospital markets in 2016 (i.e., with an HHI above 2,500), most (65%) had highly concentrated specialist physician markets, and nearly two in five (39%) had highly concentrated markets for primary care physicians. Breaking up a merger after providers have already consolidated can be difficult. At the same time, regulating the behavior of merged providers—such as through restrictions on the prices they charge—may be difficult to do on an ongoing basis.

Some regions cannot support competitive provider markets. For instance, rural communities may not have enough residents to support several providers that offer the same service.

Antitrust litigation can be complex and expensive. Without adequate funding, it may be impractical to challenge a large number of provider business practices that raise anticompetitive concerns.

Antitrust agencies may have difficulty staying ahead of market trends. For example, it could take time for the government to develop strong guidelines for challenging vertical or cross-market mergers and to accumulate enough evidence to convince courts that these practices harm competition. In the meantime, these mergers will likely continue.

The benefits of competitive provider markets for individuals with health insurance will depend in part on the competitiveness of health insurance markets. The study referenced above also estimated that most MSAs (57%) had highly concentrated insurance markets in 2016. When insurance markets are not competitive, cost savings from competitive provider markets might not be fully passed along to consumers.

What policies have been proposed to strengthen antitrust law and enforcement?

Several federal and state policy proposals have been floated to help antitrust regulators more easily identify and challenge anticompetitive mergers and regulate markets that are already concentrated. One set of policies would make it easier for governments to enforce antitrust law, such as by requiring more providers to report any planned mergers, lowering the legal standards by which mergers are deemed anticompetitive, and mandating that providers receive approval from the government before merging. Another set of policies would increase the scope of antitrust law, such as by giving the FTC full authority to regulate nonprofit providers and outlawing certain anticompetitive contracting clauses. A third set of proposals would improve the infrastructure of antitrust enforcement, such as by increasing funding for antitrust agencies, creating agencies to monitor health care markets (as some states have done), and establishing specialized courts for antitrust cases.

Discussion

The FTC, DOJ, and states seek to promote competition in health care markets to encourage providers to lower costs for consumers and provide high quality medical care. Over the years, FTC, DOJ, and some states have challenged mergers as well as other anticompetitive practices. Nonetheless, there are inherent challenges to an approach that relies solely on efforts to foster competitive provider markets through antitrust regulation, particularly given the already high level of market concentration of providers across the country.

Several policy ideas have been floated at the federal and state level that are intended to strengthen antitrust regulation. However, given the challenges facing antitrust regulation and pro-competition policies, some policymakers have proposed a more direct regulatory approach, such as by capping prices or price growth or by establishing global budgets for hospitals. Someproponents of these approaches have highlighted that antitrust efforts and regulatory approaches could play complimentary roles. For instance, caps on health care prices could serve as a backstop in concentrated markets where at least some providers would not otherwise offer competitive rates or in small markets that are unable to support competition. Antitrust regulation may also play a useful role under price regulation, for example, by encouraging providers to compete for patients by offering higher quality care.

Last Tuesday (April 23), the Federal Trade Commission (FTC) issued a 570-page final rule in a partisan 3-2 vote prohibiting employers from binding most American workers to post-employment non-competition agreements (the “Final Rule”):

“Pursuant to sections 5 and 6(g) of the Federal Trade Commission Act (“FTC Act”), the Federal Trade Commission (“Commission”) is issuing the Non-Compete Clause Rule (“the final rule”). The final rule provides that it is an unfair method of competition—and therefore a violation of section 5—for persons to, among other things, enter into non-compete clauses (“non-competes”) with workers on or after the final rule’s effective date. With respect to existing non-competes—i.e., non-competes entered into before the effective date—the final rule adopts a different approach for senior executives than for other workers. For senior executives (in policy setting/executive positions who earned more than $151,164 last year), existing non-competes can remain in force, while existing non-competes with other workers are not enforceable after the effective date.” (p.1)

“Concerns about non-competes have increased substantially in recent years in light of empirical research showing that they tend to harm competitive conditions in labor, product, and service markets. … When a company interferes with free competition for one of its former employee’s services, the market’s ability to achieve the most economically efficient allocation of labor is impaired. Moreover, employee-noncompetition clauses can tie up industry expertise and experience and thereby forestall new entry… competes by employers tends to negatively affect competition in labor markets, suppressing earnings for workers across the labor force—including even workers not subject to noncompete. This research has also shown that non-competes tend to negatively affect competition in product and service markets, suppressing new business formation and innovation… Yet despite the mounting empirical and qualitative evidence confirming these harms and the efforts of many States to ban them, non-competes remain prevalent in the U.S. economy. Based on the available evidence, the Commission estimates that approximately one in five American workers—or approximately 30 million workers—is subject to a non-compete. The evidence also indicates that employers frequently use non-competes even when they are unenforceable under State law.” (p.6)

On its home page, the FTC says “with a comprehensive ban on new non-competes, Americans could see an increase in wages, new business formation, reduced health care costs and more.”(www.ftc.gov)

The rule takes effect 120 days following its publication in the Federal Register and is applicable to every employer including specified operations in not-for-profit organizations (which represents the majority of hospitals, nursing homes and others). The agency noted it received 26,000 comment letters since the proposed rule was published January 19, 2023 including significant reaction from healthcare organizations. By the end of last week, two lawsuits were filed: one by the Chamber of Commerce in the United States District Court for the Eastern District of Texas and the second by a global tax services and software company in the Northern District of Texas – each challenging the Final Rule and arguing that the FTC lacked the authority. Others are likely to follow and its implementation will be delayed as arguments about its merits and the FTC’s standing to make the rule find their way thru the courts.

Special attention to hospitals and physicians in the rule

Notably, the use of non-competes in healthcare is a central theme in the rule, particularly in tax-exempt hospital and medical practice settings. Noting that one in 5 workers (30 million) and up to 45% of physicians work under non-compete agreements today, the Commissioners illustrated the need for the rule by inserting vignettes from 14 workers in their introduction: 4 of these were healthcare workers– 2 physicians and employees of a hospital and electronic health record provider (p.11-13). Throughout its exhaustive commentary, the Commissioners took issue with assertions by healthcare organizations about the potential negative consequences of the rule citing lack of empirical evidence to justify opposition claims. References to tax-exempt hospitals, their for-profit activities and their employment arrangements with physicians are frequent in the commentary justifying the application of the rule as follows:

“Many commenters representing healthcare organizations and industry trade associations stated that the Commission should exclude some or all of the healthcare industry from the rule because they believe it is uniquely situated in various ways. The Commission declines to adopt an exception specifically for the healthcare industry. The Commission is not persuaded that the healthcare industry is uniquely situated in a way that justifies an exemption from the final rule. The Commission finds use of non-competes to be an unfair method of competition that tends to negatively affect labor and product and services markets, including in this vital industry; the Commission also specifically finds that non-competes increase healthcare costs. Moreover, the Commission is unconvinced that prohibiting the use of non-competes in the healthcare industry will have the claimed negative effects.” (p.303)

Not surprisingly rule, responses from the hospital trade groups were swift, direct and harshly critical:

American Hospital Association (www.aha.org):” The FTC’s final rule banning non-compete agreements for all employees across all sectors of the economy is bad law, bad policy, and a clear sign of an agency run amok. The agency’s stubborn insistence on issuing this sweeping rule — despite mountains of contrary legal precedent and evidence about its adverse impacts on the health care markets — is further proof that the agency has little regard for its place in our constitutional order. Three unelected officials should not be permitted to regulate the entire United States economy and stretch their authority far beyond what Congress granted it–including by claiming the power to regulate certain tax-exempt, non-profit organizations. The only saving grace is that this rule will likely be short-lived, with courts almost certain to stop it before it can do damage to hospitals’ ability to care for their patients and communities.”

Federation of American Hospitals (www.fah.org):“This final rule is a double whammy. In n a time of constant health care workforce shortages, the FTC’s vote today threatens access to high-quality care for millions of patients.”

By contrast, the American Medical Association (www.ama-assn.org) response was positive, linking its support for the rule to AMA’s ethical principles of physician independence and clinical autonomy.

Four implicit messages to healthcare are evident in the rule

It is unlikely the rule will become law in its current form. Opposing trade groups, employers dependent on non-competes for protections of trade secrets and business relationships and many others will actively pursue its demise in courts actions. But a review of the text makes clear the FTC is intensely focused on competition and consumer protections in healthcare akin to its ongoing challenges to hospital consolidation.

Four messages emerge from the text of the rule:

1-‘The healthcare industry is a business which needs more regulation to protect consumers and its workforce by lowering costs and stimulating competition. ‘

“Many commenters representing healthcare organizations and industry trade associations stated that the Commission should exclude some or all of the healthcare industry from the rule because they believe it is uniquely situated in various ways. The Commission declines to adopt an exception specifically for the healthcare industry. The Commission is not persuaded that the healthcare industry is uniquely situated in a way that justifies an exemption from the final rule. The Commission finds use of non-competes to be an unfair method of competition that tends to negatively affect labor and product and services markets, including in this vital industry; the Commission also specifically finds that non-competes increase healthcare costs. Moreover, the Commission is unconvinced that prohibiting the use of non-competes in the healthcare industry will have the claimed negative effects.” (p.373)

2-‘Physicians play a unique role in healthcare and deserve protection.’

“Some healthcare businesses and trade organizations opposing the rule argued that, without non-competes, physician shortages would increase physicians’ wages beyond what the commenters view as fair. The commenters provided no empirical evidence to support these assertions, and the Commission is unaware of any such evidence. Contrary to commenters’ claim that the rule would increase physicians’ earnings beyond a “fair” level, the weight of the evidence indicates that the final rule will lead to fairer wages by prohibiting a practice that suppresses workers’ earnings by preventing competition; that is, the final rule will simply help ensure that wages are determined via fair competition. The Commission also notes that it received a large number of comments from physicians and other healthcare workers stating that non-competes exacerbate physician shortages.” (p.157)

“Hundreds of physicians and other commenters in the healthcare industry stated that non-competes negatively affect physicians’ ability to provide quality care and limit patient access to care, including emergency care. Many of these commenters stated that non-competes restrict physicians from leaving practices and increase the risk of retaliation if physicians object to the practices’ operations, poor care or services, workload demands, or corporate interference with their clinical judgment. Other commenters from the healthcare industry said that, like other industries, non-competes bar competitors from the market and prevent providers from moving to or starting competing firms, thus limiting access to care and patient choice. Physicians and physician organizations said non-competes contribute to burnout and job dissatisfaction, and said burnout negatively impacts patient care.” (p.202)

“…the Commission notes that while the study finds that non-competes make physicians more likely to refer patients to other physicians within their practice—increasing revenue for the practice—it makes no findings on the impact on the quality of patient care. The Commission further notes that pecuniary benefits to a firm cannot justify an unfair method of competition.” (p.206)

3.’Tax exempt hospitals that operate like for-profit entities deserve special scrutiny from regulators and are thus subject to the rule’s provisions.’

“Merely claiming tax-exempt status in tax filings is not dispositive. At the same time, if the Internal Revenue Service (“IRS”) concludes that an entity does not qualify for tax-exempt status, such a finding would be meaningful to the Commission’s analysis of whether the same entity is a corporation under the FTC Act.” (p.53)

“As stated in Part II.E, entities claiming tax exempt status are not categorically beyond the Commission’s jurisdiction, but the Commission recognizes that not all entities in the healthcare industry fall under its jurisdiction. “(p.374)