The “Big Beautiful Budget Bill” appears headed for passage with cuts to Medicaid and potentially Medicare likely elements.

The economy is slowing, with a mild recession a possibility as consumer confidence drops, the housing market slows and uncertainty about tariffs mounts.

And partisan brinksmanship in state and federal politics has made political hostages of public and rural health safety net programs as demand increases for their services.

Last Wednesday, amidst mounting anxiety about the aftermath of U.S. bunker-bombing in Iran and escalating conflicts in Gaza and Ukraine, the Centers for Medicare and Medicaid Services (CMS) released its report on healthcare spending in 2024 and forecast for 2025-2033:

“National health expenditures are projected to have grown 8.2% in 2024 and to increase 7.1% in 2025, reflecting continued strong growth in the use of health care services and goods.

During the period 2026–27, health spending growth is expected to average 5.6%, partly because of a decrease in the share of the population with health insurance (related to the expiration of temporarily enhanced Marketplace premium tax credits in the Inflation Reduction Act of 2022) and partly because of an anticipated slowdown in utilization growth from recent highs. Each year for the full 2024–33 projection period, national health care expenditure growth (averaging 5.8%) is expected to outpace that for the gross domestic product (GDP; averaging 4.3%) and to result in a health share of GDP that reaches 20.3% by 2033 (up from 17.6% in 2023) …

Although the projections presented here reflect current law, future legislative and regulatory health policy changes could have a significant impact on the projections of health insurance coverage, health spending trends, and related cost-sharing requirements, and they thus could ultimately affect the health share of GDP by 2033.”

As has been the case for 20 years, spending for healthcare grew faster than the overall economy in 2024. And it is forecast to continue through 2033:

2024Baseline

2033Forecast

% Nominal Chg.2024-2033

National Health Spending

$5,263B

$8,585B

+63.1%

US Population

337,2M

354.8M

+5.2%

Per capita personal health spending

$13,227

$20,559

+55.7%

Per capita disposable personal income

$21,626

$31,486

+45.6%

NHE as % of US GDP

18.0%

20.3%

+12.8%

In its defense, industry insiders call attention to the uniqueness of the business of healthcare:

‘Healthcare is a fundamental need: the health system serves everyone.’

‘Our aging population, chronic disease prevalence and socioeconomic disparities are drive increased demand for the system’s products and services.’

‘The public expects cutting edge technologies, modern facilities, effective medications and the best caregivers and they’re expensive.’

‘Burdensome regulatory compliance costs contribute to unnecessary spending and costs.’

And they’re right.

Critics argue the U.S. health system is the world’s most expensive but its results (outcomes) don’t justify its costs. They acknowledge the complexity of the industry but believe “waste, fraud and abuse” are pervasive flaws routinely ignored. And they remind lawmakers that the health economy is profitable to most of its corporate players (investor-owned and not-for-profits) and its executive handsomely compensated.

Healthcare has been hit by a perfect storm at a time when a majority of the public associates it more with corporatization and consolidation than caring. This coalition includes Gen Z adults who can’t afford housing, small employers who’ve cut employee coverage due to costs and large, self-insured employers who trying to navigate around the 10-20% employee health cost increase this year, state and local governments grappling with health costs for their public programs and many more. They’re tired of excuses and think the health system takes advantage of them.

As a percentage of the nation’s GDP and household discretionary spending, healthcare will continue to be disproportionately higher and increasingly concerning. Spending will grow faster than other industries until lawmakers impose price controls and other mechanisms like at least 8 states have begun already.

Most insiders are taking cover and waiting ‘til the storm passes. Some are content to cry foul and blame others. Others will emerge with new vision and purpose centered on reality.

Storm damage is rarely predictable but always consequential. It cannot be ignored. The Perfect has Hit U.S. healthcare. Its impact is not yet known but is certain to be a game changer.

“We urge the Administration to consider the timing of these policies in the context of the broader scope of requirements and challenges facing the industry that require significant system changes.”

AHIP, March 13, 2023 (in a letter to CMS Administrator Chiquita Brooks-LaSure responding to CMS’s proposed rule on Advancing Interoperability and Improving Prior Authorization Processes, proposed Final Rule, CMS-0057-P)

“Health insurance plans today announced a series of commitments to streamline, simplify and reduce prior authorization – a critical safeguard to ensure their members’ care is safe, effective, evidence-based and affordable.”

After lobbying aggressively to delay implementation of the PA reforms proposed by the previous administration (successfully delayed one year and counting), AHIP, the big PR and lobbying group for health insurers, now claims the mantle of reformer, announcing a set of voluntary commitments to streamline prior authorization.

So naturally, the industry’s “commitments” deserve closer scrutiny. Let’s unpack them. As a former health insurance industry executive, I speak their language, so allow me to translate. AHIP, which has no enforcement power, by the way, claims that 48 large insurers will:

Develop and implement standards for electronic prior authorization using Fast Healthcare Interoperability Resources Application Programming Interfaces (FHIR APIs).Translation:CMS is already requiring all insurers to do this by 2027. We might as well take credit preemptively.

Reduce the volume of in-network medical authorizations. Translation:We already demand hundreds of millions of unnecessary prior authorizations for thousands of procedures and services, so cutting a few (who knows how many?) should be a layup and won’t cut into profits.

Enhance continuity of care when patients change health plans by honoring a PA decision for a 90-day transition period starting in 2026.Translation:We’re already required to do this in Medicare Advantage. And since we delayed implementation of e-authorization until 2027, we’re in the clear until then anyway.

Improve communications by providing members with clear explanations for authorization determinations and support for appeals. Translation:We’re already required by state and federal law to do this. We’ll double-check our materials.

Ensure 80% of prior authorizations are processed in real time and expand new API standards to all lines of business. Translation:We had to promise to hold ourselves accountable to at least one measurable goal. We will set the denominator – we’ll decide which procedures and medications require PA – so we’ll hit this goal, no problem, and we might even use more non-human AI algorithms to do it.

6. Ensuring medical review of non-approved requests. Translation:People will be relieved we’re not using robots. And we’ll avoid having Congress insist that reviews must be done by a same-specialty physician, as proposed in the Reducing Medically Unnecessary Delays in Care Act of 2025 (H.R. 2433).

Of course, I wasn’t in the room when AHIP drafted these commitments, so take my translations with a grain of salt. But let’s be honest: These promises are thin on specifics, short on accountability, and devoid of measurable impact.

It’s also rich coming from an industry still reliant on something called the X12 transaction standard – technology that is now over 40 years old – to process prior authorization requests, while simultaneously pointing the finger at providers for outdated technology and being slow to adopt modern systems. Many insurers did not start accepting electronic submissions of prior authorization until roughly 2019, nearly 20 years after clinicians started using online portals such as MyChart in their regular practice. The claim that providers are the ones behind on technology is another ploy by insurers to dodge scrutiny for their schemes.

We shouldn’t settle for incremental fixes when the system itself is the problem. Nor should we allow the industry that created this problem – and perpetuates it in its own self-interest – to dictate the pace or terms of reforming it.

As we argued in our recent piece, Congress should act to significantly curtail the use of prior authorization, limiting it to a narrow, evidence-based set of high-risk use cases. Insurers should also be required to rapidly adopt smarter, lower-friction cost-control methods, like gold-carding trusted clinicians (if it can be implemented with integrity and fairness), without compromising patient access or clinical autonomy.

Letting the fox design the hen house’s security perimeter won’t protect the hens. It’s time for Congress to build a better fence.

Health insurers and their lobbying arms have spent $476.5 million since 2020 to block reform, protect profits, and mislead the public — and it’s coming straight from our premiums and tax dollars.

AHIP, the big PR and lobbying outfit for most health insurers, undoubtedly believes the praise it got from Trump administration officials and some members of Congress this week – when it announced changes insurers presumably will make voluntarily to alleviate the burden of prior authorization demands on patients and health care providers – has taken the heat off insurers. AHIP’s message to Washington politicos: You don’t need to pass any new laws to make us do the right thing. You can trust us, despite our decades of engaging in untrustworthy behavior to maximize profits.

After all, AHIP is nothing more than a PR and lobbying shop with millions of our dollars to play with. It has zero ability to force insurers to do what AHIP claims they will do. I know this because I worked closely with AHIP during my 20 years in the industry and represented Cigna on its strategic communications committee.

From Fox to “Fixer”?

AHIP pulled off its big show on Monday – and got plenty of generally fawning press coverage – because of all the money it and affiliated insurers throw around Washington every year to protect what has become an incredibly profitable status quo.

Collectively, the seven biggest for-profit insurers reported $70 billion in profits last year.

(Beleauered UnitedHealth alone reported $34.4 million in operating earnings.) And that’s just seven among dozens. One way they make that kind of dough, for their shareholders and top executives, is by using prior authorization to avoid paying for patients’ medically necessary care. Many people die as a result, while investors get richer. It’s that simple and that cold.

So just how much money does AHIP and the insurance industry spend to bamboozle members of Congress and the White House every year? We’re talking stupid money. And orders of magnitude more than nonprofits that advocate for reforms that would benefit patients instead of shareholders.

Nearly Half a Billion Ways They Tip the Scale

To find out just how much, I turned to OpenSecrets and did some math. OpenSecrets, as a reminder, is the well-named organization that keeps tabs on campaign contributions and lobbying expenses.

What I discovered is that AHIP has spent almost $65 million lobbying Congress and the Biden and Trump administrations since 2020. Its cousin, the Blue Cross Blue Shield Association, has spent even more. More than twice as much more.

And that, folks, is just the tip of the iceberg, and it doesn’t even include the tens of millions the industry spends on massive advertising campaigns inside the DC beltway that it’s not required to report. Or the dark money ads and advocacy the industry bankrolls.

But just the lobbying totals are mind-blowing. When you factor in the money spent by the big seven insurers and the other PR and lobbying groups that insurers funnel money to, the total grows to almost $500 million. You read that right: nearly half a billion dollars.

Most of that spending was during the Biden administration, but the industry is on track to break spending records during the first year of the current Trump administration. They are lobbying not only to beat back new laws and regulations that could constrain their prior authorization practices but also to protect their biggest cash cows: Medicare Advantage and their pharmacy benefit managers (PBMs).

Three PBMs – owned by Cigna, CVS/Aetna and UnitedHealth –control 80% of the pharmacy benefit market and determine which drugs we’ll have access to and how much we have to pay out of pocket even with insurance.

The Big Number

$476.5 million – That’s the amount of money health insurance corporations and four of their PR and lobbying groups – AHIP, BCBSA (which includes contributions from Elevance/Anthem as well as numerous other BCBS companies), the Pharmaceutical Care Management Association and the Better Medicare Alliance – have collectively spent on lobbying Congress and federal regulators between January 1, 2020, and March 31, 2025.

Keep in mind that that money is not coming out of executives’ paychecks. It’s coming out of our pockets. Insurers skim money from our premiums and taxes to finance their propaganda and lobbying efforts to keep the gravy train rolling. And it’s in addition to all the campaign cash they dole out every year, which I tabulated recently.

This is not to say that reform is impossible. Scrappy advocacy groups with a tiny fraction of that total have scored important victories over the years. But it is why progress is so slow and setbacks are so frequent.

But just imagine how all that money could be put to better use to ensure that all Americans, including those with insurance, are able to get the care they need when they need it. It’s clear that in addition to reforming our health care system, we need political reforms that make it more difficult for big corporations and their trade groups to influence elections and public policy.

The House of Representatives’ reconciliation bill, passed by the powerful Energy and Commerce Committee today, cuts just about everything when it comes to health care – except the actual waste, fraud and abuse. Now the bill heads to the floor for a vote of the full House of Representatives before it must also be passed by the Senate to become law.

I know what you’re thinking: not another story about Medicaid. With the flood of articles detailing the devastating Medicaid cuts proposed by House Republicans —cuts that could strip 8.7 million people of their health coverage — there’s an important fact being overlooked: Members of Congress chose to sidestep policies aimed at reining in Big Insurance abuses and, instead, opted to cut Medicaid.

And the real irony of it all is they could have saved a ton of money if they would just address the elephant in the room.

Abuses by Big Insurance companies have been going on for decades but have only recently come under scrutiny. Insurance companies figured out how to take advantage of the structure of the Medicare Advantage program to receive higher payments from the government.

They do this in two ways:

They make their enrollees seem sicker than they are through a strategy called “upcoding” and;

They use care obstacles such as prior authorization and inadequate provider networks that eventually drive sicker people to drop their plans and leave them with healthier enrollees, referred to as “favorable selection.”

According to the Medicare Payment Advisory Commission (MedPAC) these tactics lead the government to overpay insurance corporations running MA plans by $84 billion a year. This number is expected to grow, and estimates show that overpayments will cost the government more than a $1 trillion from 2025-2034. That is $1 trillion dollars in potential savings Republicans could have included in their bill instead of cutting Medicaid spending that provides care for vulnerable communities.

These overpayments do not lead to better care in MA plans; in fact, research has shown that care quality and outcomes are often worse in MA compared to traditional Medicare. Even worse, these overpayments are tax dollars meant for health care that end up in the pockets of shareholders of big insurance corporations, which spend billions of taxpayer dollars on things like stock buybacks and executive bonuses.

One of the most frustrating parts of the lawmaker’s choice to target Medicaid rather than Big Insurance abuses is that there are multiple policies supported by both Republicans and Democrats to stop these abuses. Sen. Bill Cassidy (R-Louisiana), along with Sen. Jeff Merkley (D-Oregon), have introduced the NO UPCODE Act, which would cut down on the practice of upcoding explained above. President Trump’s Administrator of the Centers for Medicare and Medicaid Services, Dr. Mehmet Oz, said during his confirmation hearing that he supports efforts to crack down on practices used by insurers to upcode. And Rep. Mark Green (R-Tennessee) introduced a bipartisan bill to decrease improper prior authorization denials in MA.

In a somewhat cruel twist, the only mention of Medicare fraud in the Republican reconciliation bill proposals is a section claiming to crack down on improper payments in Medicare Parts A and B (which make up traditional Medicare) by using artificial intelligence.

The total improper payments in TM represent just over one-third of the overpayments going to MA plans each year, and many of the payments flagged as improper in TM are flagged due to missing documentation rather than questionable tactics that MA insurers use.

In reflecting on why Republicans in Congress ignored potential savings from Big Insurance reforms and instead pursued cuts to care for people depending on Medicaid, which do not save as much, my biggest question was, why?

Why would lawmakers swerve around a populist policy right in front of them to stop Big Insurance from profiting off of the federal government to instead propose a regressive policy that targets millions of working Americans and leaves health insurance corporations that make billions in profits each year untouched?

Unfortunately, the answer likely lies in money. Although people enrolled in Medicaid and the Children’s Health Insurance Program (CHIP) make up roughly one-third of the U.S. population, they account for just 0.5% of all political campaign contributions — about $60 million annually. This disparity is likely driven by financial constraints: Many of these individuals are rightly focused on covering basic needs such as housing, food, and childcare, especially as wages have not kept pace with the rising cost of living.

In contrast, the health care sector — which includes major players like big insurance, pharmaceutical and hospital companies—contributed $357 million during the 2020 election cycle, including $97 million to outside groups such as Super PACs. These outside spending groups are largely funded by corporations and wealthy individuals, who represent less than 1% of the population but wield significant political influence.

Super PACs spent more than $2 billion during the 2020 election cycle, amplifying the voices of industry-aligned donors. This stark imbalance in political spending may help explain why congressional proposals targeted Medicaid recipients while leaving the powerful health insurance industry largely untouched.

It is not only Republicans who have failed to stop Big Insurance from taking advantage of federal health programs, Democrats declined to take action when negotiating their health care legislation during President Biden’s term. Rather, it seems to be a failure of policymakers of both parties to pass legislation that makes it clear to Big Insurance that our health care is not an investment opportunity for Wall Street, and the dollars we pay in taxes to support Medicare are not pocket change for executives to use for stock buybacks.

The failure to include MA reform represents a missed opportunity to prioritize patient care over corporate profits. However, the growing strength and voices of patients across the nation will ultimately make it impossible for lawmakers to ignore this issue much longer. With continued momentum, the fight to put patients over Big Insurance profits will succeed.

Wall Street is speaking loudly to Medicare Advantage insurers: If you want us to stick with you, keep dumping seniors who are pinching your profit margins.

Investors continue to punish UnitedHealth Group since the company downgraded its 2025 profit expectations on April 17. On Friday, UnitedHealth’s stock price hit not only a 52-week low—$393.11—but its lowest point in years. The last time UnitedHealth’s stock price went below $400 a share was on October 14, 2021.

The company’s shares lost nearly 4.5% of their value during the past week, contributing to a decline that started soon after the company set an all-time high of $630.73 last November. UnitedHealth’s shares have lost more than 33% of their value since then.

Wall Street Sends a Message

Meanwhile, investors have once again embraced UnitedHealth’s top two rivals in the Medicare Advantage business–Humana and CVS/Aetna. Those companies told investors last year, when both were in the Wall Street dog house for spending more than investors expected on patients’ medical care, that they would dump hundreds of thousands of their costliest Medicare Advantage enrollees to improve their profits. They made good on that promise, shedding almost 650,000 seniors and people with disabilities by the end of the year.

Many of those people enrolled in a UnitedHealth Medicare Advantage plan. The company reported 400,000 more Medicare Advantage enrollees in the first quarter of 2025 than in the fourth quarter of 2024. That used to be a good thing, but UnitedHealth’s executives told investors on April 17 that it wouldn’t make as much money for them as the company had assured them just three months earlier because it likely will have to spend more than they expected on those new MA enrollees’ medical care. Investors responded by immediately dispatching the company’s shares to the cellar. Those shares lost about 23% of their value in a single day.

The Street had also punished Humana and CVS last year when they said they were paying more for seniors’ medical care than they’d expected. Shares of both companies cratered, losing around half their value. So, executives at both Humana and CVS started identifying Medicare markets to get out of entirely. The culling was ruthless. CVS shed 227,000 MA enrollees. Humana got rid of 419,000.

Locked Out of Traditional Medicare

Those seniors and disabled people had to scramble to find a new Medicare Advantage insurer because it is difficult for most people to go back to traditional Medicare and find an affordable Medicare supplement policy. Medicare supplement insurers must waive underwriting during the first six months of applicants’ eligibility for Medicare, but people who enroll in a Medicare Advantage plan and want or need to make a change months later find out that insurers will charge them more unless their health is nearly perfect.

Of the seven big for-profit health insurers, four (Cigna, CVS/Aetna, Humana and Centene) collectively cut 1.3 million of their Medicare Advantage enrollees adrift at the end of 2024 in an effort to stay in Wall Street’s good graces. Cigna dumped all 600,000 of its MA enrollees, selling them to the Blue Cross corporation HCSC. For-profit Blue Cross insurer Elevance picked up 227,000; Molina added 18,000, and, as noted, UnitedHealth signed up 400,000 new MA enrollees.

While UnitedHealth’s shares have lost a third of their value, CVS’s shares have increased more than 50% since the first of this year. They even set a 52-week high of $72.51 on Thursday. Humana’s shares closed Friday at $258.48, up 1.88% since January 1. They are out of the Wall Street dog house – for now, anyway.

Profits, Lobbying Soar

I trust you are not feeling sorry for UnitedHealth because of its misfortune on Wall Street. It is still a hugely profitable company–just not profitable enough lately to please investors. This huge corporation, the fourth largest in America, reported $9.1 billion in profits in just the first quarter of this year. If the company makes it more difficult for its health plan enrollees to get the care they need this year, it could make even more than the $34.4 billion in profits it made last year.

And as a group, the seven big for-profits, including those that spent more than Wall Street felt was necessary on patients’ medical care, made $70 billion in profits last year. (UnitedHealth made nearly as much as the other six combined.)

And collectively, those giant corporations took in a record $1.5 trillion in revenue from us as customers and taxpayers last year. They are doing quite well. But that won’t stop them from trying to keep lawmakers and Trump administration officials from cracking down this year on the widespread waste, fraud and abuse in the Medicare Advantage program. You can expect them to spend a record amount of our money on lobbying expenses in Washington this year to keep their Medicare Advantage cash cow well fed.

Wall Street is speaking loudly to Medicare Advantage insurers: If you want us to stick with you, keep dumping seniors who are pinching your profit margins.

Investors continue to punish UnitedHealth Group since the company downgraded its 2025 profit expectations on April 17. On Friday, UnitedHealth’s stock price hit not only a 52-week low—$393.11—but its lowest point in years. The last time UnitedHealth’s stock price went below $400 a share was on October 14, 2021.

The company’s shares lost nearly 4.5% of their value during the past week, contributing to a decline that started soon after the company set an all-time high of $630.73 last November. UnitedHealth’s shares have lost more than 33% of their value since then.

Wall Street Sends a Message

Meanwhile, investors have once again embraced UnitedHealth’s top two rivals in the Medicare Advantage business–Humana and CVS/Aetna. Those companies told investors last year, when both were in the Wall Street dog house for spending more than investors expected on patients’ medical care, that they would dump hundreds of thousands of their costliest Medicare Advantage enrollees to improve their profits. They made good on that promise, shedding almost 650,000 seniors and people with disabilities by the end of the year.

Many of those people enrolled in a UnitedHealth Medicare Advantage plan. The company reported 400,000 more Medicare Advantage enrollees in the first quarter of 2025 than in the fourth quarter of 2024. That used to be a good thing, but UnitedHealth’s executives told investors on April 17 that it wouldn’t make as much money for them as the company had assured them just three months earlier because it likely will have to spend more than they expected on those new MA enrollees’ medical care. Investors responded by immediately dispatching the company’s shares to the cellar. Those shares lost about 23% of their value in a single day.

The Street had also punished Humana and CVS last year when they said they were paying more for seniors’ medical care than they’d expected. Shares of both companies cratered, losing around half their value. So, executives at both Humana and CVS started identifying Medicare markets to get out of entirely. The culling was ruthless. CVS shed 227,000 MA enrollees. Humana got rid of 419,000.

Locked Out of Traditional Medicare

Those seniors and disabled people had to scramble to find a new Medicare Advantage insurer because it is difficult for most people to go back to traditional Medicare and find an affordable Medicare supplement policy. Medicare supplement insurers must waive underwriting during the first six months of applicants’ eligibility for Medicare, but people who enroll in a Medicare Advantage plan and want or need to make a change months later find out that insurers will charge them more unless their health is nearly perfect.

Of the seven big for-profit health insurers, four (Cigna, CVS/Aetna, Humana and Centene) collectively cut 1.3 million of their Medicare Advantage enrollees adrift at the end of 2024 in an effort to stay in Wall Street’s good graces. Cigna dumped all 600,000 of its MA enrollees, selling them to the Blue Cross corporation HCSC. For-profit Blue Cross insurer Elevance picked up 227,000; Molina added 18,000, and, as noted, UnitedHealth signed up 400,000 new MA enrollees.

While UnitedHealth’s shares have lost a third of their value, CVS’s shares have increased more than 50% since the first of this year. They even set a 52-week high of $72.51 on Thursday. Humana’s shares closed Friday at $258.48, up 1.88% since January 1. They are out of the Wall Street dog house – for now, anyway.

Profits, Lobbying Soar

I trust you are not feeling sorry for UnitedHealth because of its misfortune on Wall Street. It is still a hugely profitable company–just not profitable enough lately to please investors. This huge corporation, the fourth largest in America, reported $9.1 billion in profits in just the first quarter of this year. If the company makes it more difficult for its health plan enrollees to get the care they need this year, it could make even more than the $34.4 billion in profits it made last year.

And as a group, the seven big for-profits, including those that spent more than Wall Street felt was necessary on patients’ medical care, made $70 billion in profits last year. (UnitedHealth made nearly as much as the other six combined.)

And collectively, those giant corporations took in a record $1.5 trillion in revenue from us as customers and taxpayers last year. They are doing quite well. But that won’t stop them from trying to keep lawmakers and Trump administration officials from cracking down this year on the widespread waste, fraud and abuse in the Medicare Advantage program. You can expect them to spend a record amount of our money on lobbying expenses in Washington this year to keep their Medicare Advantage cash cow well fed.

You have three days left, if you got suckered in by those omnipresent ads for Medicare Advantage and left regular Medicare for the siren song of cheaper coverage, “free” vision, hearing, or dental, or even “free” money to buy groceries or rides to the doc.

The open enrollment period for real Medicare closes at the end of the day Saturday, December 7th; after that, you’re locked into the Medicare Advantage plan you may have bought until next year.

If you’ve had Medicare Advantage for a year or more, however, the open enrollment period is still “open” until December 7th, but you will want to make sure you can get a “Medigap” plan that fills in the 20% that real Medicare doesn’t cover.

Companies are required to write a Medigap policy for you at a reasonable price when you turn 65, no matter how sick you are or what preexisting conditions you may have, but if you’ve been “off Medicare” by being on Medicare Advantage for more than a year, they don’t have to write you a policy, so double-check that and sign up for a Medigap policy before making the switch back to real Medicare.

So, what’s this all about and why is it so complicated?

When George W. Bush and congressional Republicans (and a handful of bought-off Democrats) created Medicare Advantage in 2003, it was the fulfillment of half of Bush’s goal of privatizing Social Security and Medicare, dating all the way back to his unsuccessful run for Congress in 1978 and a main theme of his second term in office.

Medicare Advantage is not Medicare.

These plans are private health insurance provided by private corporations, who are then reimbursed at a fixed rate by the Medicare trust fund regardless of how much their customers use their insurance. Thus, the more they can screw their customers and us taxpayers by withholding healthcare payments, the more money they make.

With real Medicare,

if your doctor says you need a test, procedure, scan, or any other medical intervention you simply get it done and real Medicare pays the bill. No muss, no fuss, no permission needed. Real Medicare always pays, and if they think something’s not kosher, they follow up after the payment’s been made so as not to slow down the delivery of your healthcare.

With Medicare Advantage,

however, you’re subject to “pre-clearance,” meaning that the insurance company inserts itself between you and your doctor: You can’t get the medical help you need until or unless the insurance company pre-clears you for payment.

These companies thus make much of their billions in profit by routinely denying claims — 1.5 million, or 18 percent of all claims, were turned down in one year alone — leaving Advantage policy holders with the horrible choice of not getting the tests or procedures they need or paying for them out-of-pocket.

Given this, you’d think that most people would stay as far away from these private Medicare Advantage plans as they could. But Congress also authorized these plans to compete unfairly with real Medicare by offering things real Medicare can’t (yet). These include free or discounted dental, hearing, eyeglasses, gym memberships, groceries, rides to the doctor, and even cash rebates.

You and I pay for those freebies, but that’s only half of the horror story.

This year, as Matthew Cunningham-Cook pointed out in Wendell Potter’s brilliant Health Care un-covered Substack newsletter, we’re ponying up an additional $64 billion to give to these private insurance companies to “reimburse” them for the freebies they relentlessly advertise on television, online, and in print.

And here’s the most obscene part of the whole thing: the companies won’t tell the government (us!) how much of that $64 billion they’ve actually spent. They just take the money and say, “Thank you very much.” And then, presumably, throw a few extra million into the pockets of each of their already obscenely-well-paid senior executives.

For example, the former CEO of the nation’s largest Medicare Advantage provider, UnitedHealth, walked away with over a billion dollars in total compensation. With a “B.” One guy. His successor made off with over a half-billion dollars in pay and stock.

Good work if you can get it: all you need do is buy off a hundred or so members of Congress, courtesy of Clarence Thomas’ billionaire-funded tie-breaking vote on Citizens United, and threaten the rest of Congress with massive advertising campaigns for their opponents if they try to stop you.

And while the companies refuse to tell us how much of the $64 billion that we’re throwing at them this year to offer “free” dental, etc. is actually used, what we do know is that most of that money is not going to pay for the freebies they advertise. As Cunningham-Cook noted, in one study only 11 percent of Advantage policyholders who’d signed up with plans offering dental care used that benefit.

Another study showed over-the-counter-drug freebies were used only a third of the time, leaving $5 billion in the insurance companies money bins just for that “reimbursable” goodie. A later study found that at least a quarter of all Advantage policyholders failed to use any of the freebies they’d been offered when they signed up.

That’s an enormous amount of what the industry calls “breakage”; benefits offered and paid for by the government but not used. Billions of dollars left over every month. And, used or not, you and I sure paid for them.

And now it looks like things are about to get a whole lot worse.

When he was president last time, Donald Trump substantially expanded Medicare Advantage, calling real Medicare “socialism.” Project 2025 and candidate Trump both promised to end real Medicare “immediately” if Trump was re-elected; at the very least, they’ll make Medicare Advantage the “default” program people are steered into when they turn 65 and sign up for Medicare.

These giant insurance companies ripped off us taxpayers last year to the tune of an estimated $140 billion over and above what it would’ve cost us if people had simply been on real Medicare, according to a report from Physicians for a National Health Program (PNHP).

If there was no Medicare Advantage scam bleeding off all that cash to pay for executives’ private jets, real Medicare could be expanded to cover dental, vision, and hearing and even end the need for Medigap plans.

But for now, the privatization gravy train continues to roll along. The insurance giants use some of that money to buy legislators, and some of it for expensive advertising to dupe seniors into joining their programs. The company (Benefytt) that hired Joe Namath to pitch Medicare Advantage, for example, was recently hit with huge fines by the Federal Trade Commission for deceptive advertising.

“Benefytt pocketed millions selling sham insurance to seniors and other consumers looking for health coverage,” said Samuel Levine, Director of the FTC’s Bureau of Consumer Protection. “The company is being ordered to pay $100 million, and we’re holding its executives accountable for this fraud.”

And what was it that the Federal Trade Commission called “sham insurance”? Medicare Advantage. Nonetheless, the Centers for Medicare Services continues to let Benefytt and Namath market these products: welcome to the power of organized money.

And it’s huge organized money. Medicare Advantage plans are massive cash cows for the companies that run them. As Cigna prepares for a merger, for example, they’re being forced to sell off their Medicare Advantage division: it’s scheduled to go for $3.7 billion. Nobody pays that kind of money unless they expect enormous returns.

And how do they make those billions?

Most Medicare Advantage companies regularly do everything they can to intimidate you into paying yourself out-of-pocket. Often, they simply refuse payment and wait for you to file a complaint against them; for people seriously ill the cumbersome “appeals” process is often more than they can handle so they just write a check, pull out a credit card, or end up deeply in debt in their golden years.

As a result, hospitals and doctor groups across the nation are beginning to refuse to take Medicare Advantage patients. And in rural areas many hospitals are simply going out of business because Medicare advantage providers refuse to pay their bills.

California-based Scripps Health, for example, cares for around 30,000 people on Medicare Advantage and recently notified all of them that Scripps will no longer offer medical services to them unless they pay out-of-pocket or revert back to real Medicare.

They made this decision because over $75 million worth of services and procedures their physicians had recommended to their patients were turned down by Medicare Advantage insurance companies. In many cases, Scripps had already provided the care and is now stuck with the bills that the Advantage companies refuse to pay.

“We are a patient care organization and not a patient denial organization and, in many ways, the model of managed care has always been about denying or delaying care – at least economically. That is why denials, [prior] authorizations and administrative processes have become a very big issue for physicians and hospitals…”

Similarly, the Mayo Clinic has warned its customers in Florida and Arizona that they won’t accept Medicare Advantage any more, either. Increasing numbers of physician groups and hospitals are simply over being ripped off by Advantage insurance companies.

Traditional Medicare has been serving Americans well since 1965: it’s one of the most efficient single-payer systems to fund healthcare that’s ever been devised. But nobody was making a buck off it, so nobody could share those profits with greedy politicians. Enter Medicare Advantage, courtesy of George W. Bush and the GOP.

While several bills have been offered in Congress to do something about this — including Mark Pocan’s and Ro Khanna’s Save Medicare Act that would end these companies’ ability to use the word “Medicare” in their policy names and advertising — the amounts of money sloshing around DC in the healthcare space now are almost unfathomable.

So far this year, according to opensecrets.org, the insurance industry has spent $117,305,895 showering gifts and persuasion on our federal lawmakers to keep their obscene profits flowing.

It’s all one more example of how five corrupt Republicans on the US Supreme Court legalizing political bribery with Citizens Unitedhave screwed average Americans and made a handful of industry executives and investors fabulously rich.

They get away with it because when people choose to sign up for Medicare Advantage at 65 (or convert to these plans in their 60s or early 70s) they’re typically not sick — and thus cost the insurance companies little.

Tragically, the people signing up for these plans have no idea all the hassles, hoops, and troubles they might have to jump through when they do get sick, have an accident, or otherwise need medical assistance.

And since the last three years of life are typically the most expensive years for healthcare, the insurance denials are more likely to happen then — long after the person’s signed up with the Advantage company and it’s too late to go back to real Medicare.

This is why it typically takes a few years for people to figure out how badly they got screwed by not going with regular Medicare but instead putting themselves in the hands of private insurance companies.

“In spite of recommendations from Mr. Pauker’s doctors, his family said, Humana has repeatedly denied authorization for inpatient rehabilitation after hospitalization, saying at times he was too healthy and at times too ill to benefit.”

“Tens of millions of denials are issued each year for both authorization and reimbursements, and audits of the private insurers show evidence of ‘widespread and persistent problems related to inappropriate denials of services and payment,’ the investigators found.”

If you have “real” Medicare with a heavily regulated Medigap policy to cover the 20% Medicare doesn’t, you never have to worry.

Your bills get paid, you can use any doctor or hospital in the country who takes Medicare, and neither Medicare nor your Medigap provider will ever try to collect from you or force you to pay for what you thought was covered.

Neither you or your doctor will ever have to do the “pre-authorization” dance with real Medicare: those terrible experiences dealing with for-profit insurance companies are part of the past.

But if you have Medicare Advantage — which is not Medicare, but private health insurance — you’re on your own.

As the Times laid out:

“About 18 percent of [Advantage] payments were denied despite meeting Medicare coverage rules, an estimated 1.5 million payments for all of 2019. In some cases, plans ignored prior authorizations or other documentation necessary to support the payment. These denials may delay or even prevent a Medicare Advantage beneficiary from getting needed care…”

Buying a Medicare Advantage policy is a leap in the dark, and the federal government is not there to catch you. And it’s all perfectly legal, thanks to Bush’s 2003 law, so your state insurance commissioner usually can’t or won’t help.

Thus, here we are, handing billions of dollars a month to insurance industry executives so they can buy new Swiss chalets, private jets, and luxury yachts. And so they can compete — unfairly — with Medicare itself, driving LBJ’s most proud achievement into debt and crisis.

Enough is enough. Let your members of Congress know it’s beyond time to fix the Court and Medicare, so scams like Medicare Advantage can no longer rip off America’s seniors while making industry executives richer than Midas.

And if you got hooked into switching out of real Medicare and now find yourself in a Medicare Advantage plan, you have three days to back out and return to real Medicare. For more information, you can also contact the nonprofit and real-Medicare-supporting Medicare Rights Center at 800-333-4114.

There’s only one person in this photograph/video of a recent G7 meeting who represents a country where an illness can destroy an entire family, leaving them bankrupt and homeless, with the repercussions of that sudden fall into poverty echoing down through generations.

Most Americans have no idea that the United States is quite literally the only country in the developed world that doesn’t define healthcare as an absolute right for all of its citizens. That’s it. We’re the only one left.

The United States spends more on “healthcare” than any other country in the world: about 17% of GDP.

Switzerland, Germany, France, Sweden and Japan all average around 11%, and Canada, Denmark, Belgium, Austria, Norway, Netherlands, United Kingdom, New Zealand and Australia all come in between 9.3% and 10.5%.

We are literally the only developed country in the world with an entire multi-billion-dollar for-profit industry devoted to parasitically extracting money from us to then turn over to healthcare providers on our behalf. The for-profit health insurance industry has attached itself to us like a giant, bloodsucking tick.

They all failed, and when I did a deep dive into the topic two years ago for my book The Hidden History of American Healthcare I found two major barriers to our removing that tick from our backs.

The early opposition, more than 100 years ago, to a national healthcare system came from southern white congressmen (they were all men) and senators who didn’t want even the possibility that Black people could benefit, health-wise, from white people’s tax dollars. (This thinking apparently still motivates many white Southern politicians.)

The leader of that healthcare-opposition movement in the late 19th and early 20th centuries was a German immigrant named Frederick Hoffman, as I mentioned in a recent newsletter. Hoffman was a senior executive for the Prudential Insurance Company, and wrote several books about the racial inferiority of Black people, a topic he traveled the country lecturing about.

His most well-known book was titled Race Traits and Tendencies of the American Negro. It became a major best-seller across America when it was first published for the American Economic Association by the Macmillan Company in 1896, the same year the Supreme Court’s Plessy v. Ferguson decision legally turned the entire US into an apartheid state.

Hoffman taught that Black people, in the absence of slavery, were so physically and intellectually inferior to whites that if they were simply deprived of healthcare the entire race would die out in a few generations. Denying healthcare to Black people, he said, would solve the “race problem” in America.

Southern politicians quoted Hoffman at length, he was invited to speak before Congress, and was hailed as a pioneer in the field of “scientific racism.” Race Traits was one of the most influential books of its era.

By the 1920s, the insurance company he was a vice president of was moving from life insurance into the health insurance field, which brought an added incentive to lobby hard against any sort of a national healthcare plan.

Which brings us to the second reason America has no national healthcare system: profits.

And that’s just one of multiple giant insurance companies feeding at the trough of your healthcare needs.

Much of that money, and the pay for the multiple senior executives at that and other insurance companies who make over $1 million a year, came from saying “No!” to people who file claims for payment of their healthcare costs.

Companies offering such “primary” health insurance simply don’t exist (or are tiny) in almost every other developed country in the world. Mostly, where they do exist, they serve wealthier people looking for “extras” beyond the national system, like luxury hospital suites or air ambulances when overseas. (Switzerland is the outlier with exclusively private insurance, but it’s subsidized, mandatory, and non-profit.)

If Americans don’t know this, they intuit it.

In the 2020 election there were quite a few issues on statewide ballots around the country. Only three of them outpolled Joe Biden’s win, and expanding Medicaid to cover everybody was at the top of that list. (The other two were raising the minimum wage and legalizing pot.)

The last successful effort to provide government funded, single-payer healthcare insurance was when Lyndon Johnson passed Medicare and Medicaid (both single-payer systems) in the 1960s. It was a hell of an effort, but the health insurance industry was then a tiny fraction of its current size.

In 1978, when conservatives on the Supreme Court legalized corporations owning politicians with their Buckley v Belotti decision (written by Justice Louis Powell of “Powell Memo” fame), they made the entire process of replacing a profitable industry with government-funded programs like single-payer vastly more difficult, regardless of how much good they may do for the citizens of the nation.

The Court then doubled-down on that decision in 2010, when the all-conservative vote on Citizens Unitedcemented the power of billionaires and giant corporations to own politicians and even write and influence legislation and the legislative process.

Medicare For All, like Canada has, would save American families thousands every year immediately and do away with the 500,000+ annual bankruptcies in this country that happen only because somebody in the family got sick. But it would kill the billions every week in profits of the half-dozen corporate giants that dominate the health insurance industry.

This won’t be happening with a billionaire in the White House, but if we want to bring America into the 21st century with the next administration, we need to begin working, planning, and waking up voters now.

Last week, the Senate Permanent Subcommittee on Investigations, led by Sen. Richard Blumenthal (D-Connecticut), released a Majority Staff Report on rampant prior authorization (PA) abuses in Medicare Advantage (MA).

The report offers unique insight into recent trends in the use of prior authorization by Medicare Advantage plans and the strategy and motives behind insurance corporations’ use of it.

While the findings won’t surprise those who’ve been following health policy trends, it is immensely concerning that between 2019 and 2022, the prior authorization denial rate for post-acute care in UnitedHealth’s Medicare Advantage plans doubled.

The denial rate for long-term acute care hospitals in Humana’s Medicare Advantage plans increased by 54% from 2020 to 2022. During this time, UnitedHealth, CVS/Aetna, and Humana increased their use of artificial intelligence (AI) for prior authorization reviews, often resulting in increasing denial numbers and decreasing (or absent) review time by human beings.

The report recommends that the Centers for Medicare and Medicaid Services (CMS) collect additional data, conduct audits of prior authorization processes, and expand regulations on the use of technology in PA reviews. While these recommendations would be positive steps, the report’s findings call into question whether Big Insurance can ever be trusted or regulated enough to prevent abuse of patients through prior authorization and other mechanisms.

This report provides an in-depth look at insurers’ motivations. Sadly, those motivations are not to “make sure a service or prescription is a clinically appropriate option,” as UnitedHealth claims, but to decrease the amount spent on medical care to increase the corporations’ profits.

The report noted that CVS, which owns Aetna, saved $660 million in 2018 by denying Medicare Advantage patients’ claims for treatment at inpatient facilities. Around the same time, CVS found in its testing of a model to “maximize approvals,” which would be a good thing for patients, that the model jeopardized profits because it would lead to more care being covered. In 2022, CVS “deprioritized” a plan to increase auto-approvals because of the lost “savings” from denying patient care.

The report found that the motivation to increase profits, without regard for patient care, was not unique to CVS/Aetna.

UnitedHealth’s naviHealth subsidiary provided this directive to its employees: “IMPORTANT: Do NOT guide providers or give providers answers to the questions” when speaking to a patient’s doctor about a prior authorization request. Instead of working collaboratively with doctors to get patients the care they need, UnitedHealth told its workers not to bother. In a training session offered to Humana employees involved in prior authorization reviews, the company explained that reviewers should deny a request for post-acute care even if a patient needed more intensive treatment. Humana told reviewers that the lack of an in-network lower-level care facility for patients to go to was not a reason to approve post-acute care and that usually the situations can be “sorted out,” presumably by the patient with no help from the insurer.

All three companies (UnitedHealth, Humana and CVS/Aetna), which dominate the Medicare Advantage program, demonstrated a striking lack of motivation to protect and enhance patient care, instead showing a primary motivation to increase profits and margins.

The subcommittee’s report also noted that UnitedHealth, CVS/Aerna, and Humana are increasingly using AI to make care decisions and cutting humans, especially doctors, out of the process. The researchers found that in 2022, UnitedHealth looked into how using AI and machine learning could aid in predicting which denials of post-acute care requests were most likely to be overturned. One would hope this effort would be to decrease the number of wrongfully denied prior authorization requests and increase patient access to care.

However, the report includes a quote from a recap of a meeting on the project asking “what we could do in the clinical review process to change the outcome of the appeal,” meaning that UnitedHealth was interested in preventing the overturning of denials, not getting the decision right in the first place. The report also found evidence that naviHealth used artificial intelligence to help determine the coverage decisions for a patient’s post-acute care claim before any human post-acute care providers evaluated a case. The report’s authors found that denials for post-acute care facilities rose rapidly once naviHealth began managing these requests for UnitedHealth’s MA plans.

These are just some of the findings in the 54-page report on Big Insurance’s use of prior authorization to deny Medicare Advantage patient requests for post-acute care.

The report’s findings demonstrate the abuse of prior authorization by the insurers, the motivation to increase profit and decrease patient care, and the use of AI to increase denials. Further, the findings underscore that prior authorization is a tool used by Big Insurance primarily to maximize profits. The report puts forward recommendations to cut down on abusive denials, which would have some positive impact.

More importantly, I believe the report provides more evidence that it is becoming exceedingly less likely that private and for-profit insurance companies can be regulated and act in a way that promotes patient health over profits.

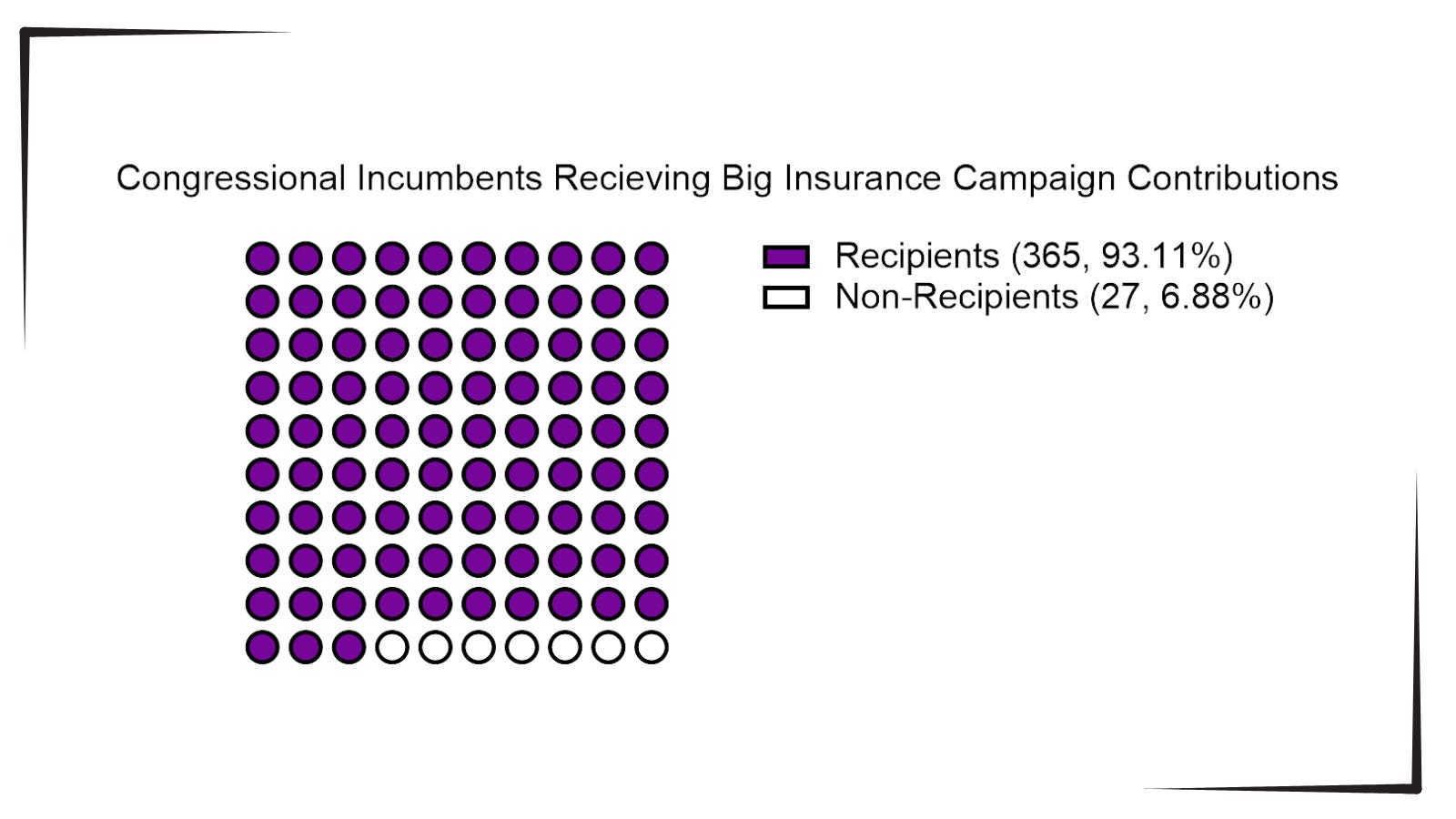

With the election looming and the beginning of annual open enrollment periods for health insurance plans, it is vital to pull back the curtain on the influx of money from Big Insurance corporations to political campaigns and lobbying.

Data available from OpenSecrets.com thus far in 2024 shows that 93% of Congressional incumbents running in 2024 received contributions from Big Insurance, including 100% of Senate incumbents. These insurance corporations run the ten largest Medicare Advantage plans in the country and are known to deny needed health care and defraud the government, but face little to no consequences.

Insurance corporations included in this analysis are UnitedHealth Group, Humana, CVS/Aetna, Kaiser Permanente, Elevance Health, Centene Corp, Cigna, Blue Cross Blue Shield Association (which represents many MA plans, including two of the largest: BCBSMichigan and Highmark), and SCAN.

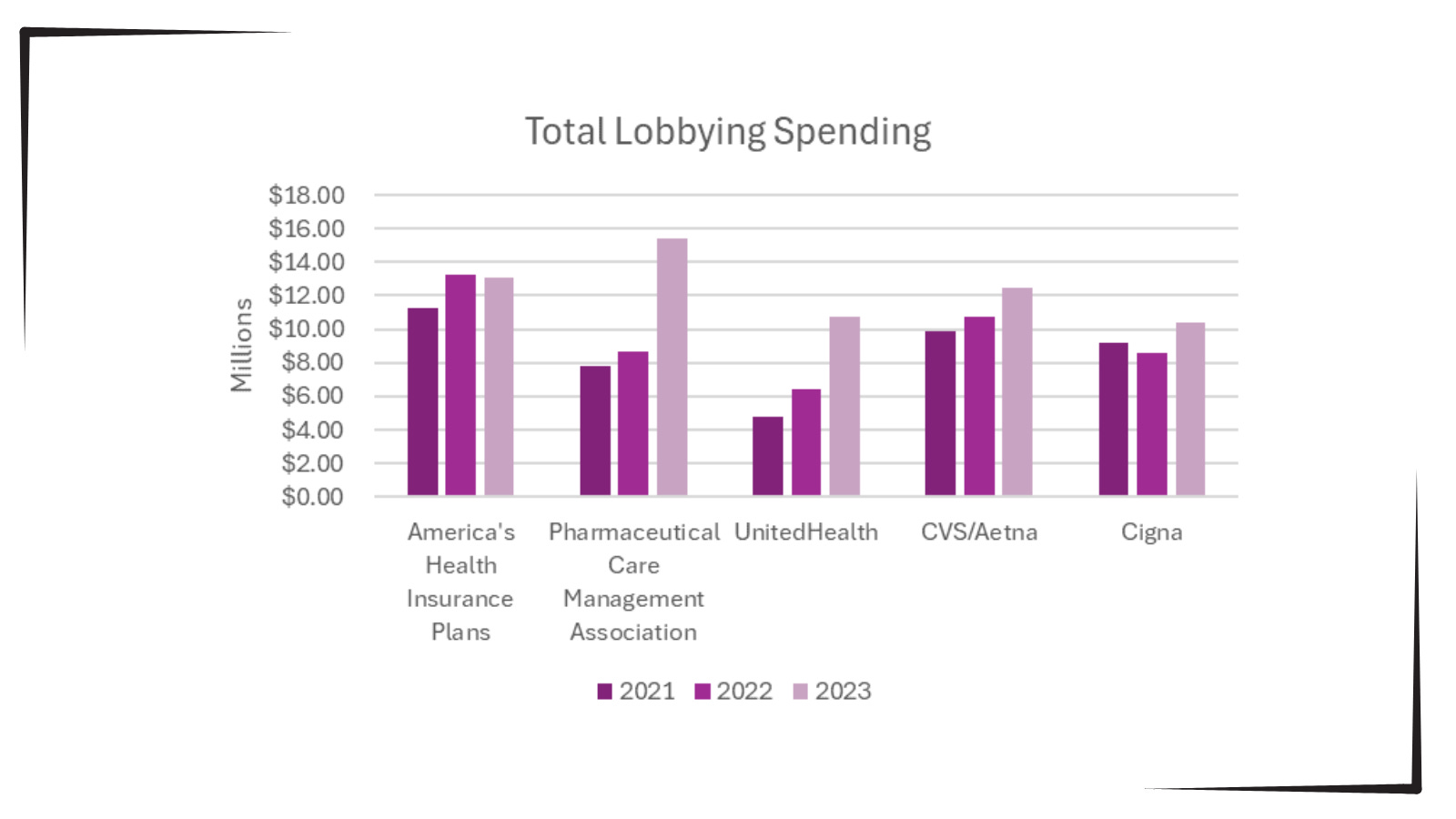

Additionally, as bipartisan scrutiny of pharmacy benefit managers (PBMs) and Medicare Advantage plans has intensified, spending by Big Insurance on lobbying has increased.

Total lobbying spending by America’s Health Insurance Plans; Pharmaceutical Care Management Association; UnitedHealth; CVS/Aetna; and Cigna for the years 2021, 2022 and 2023.

This open enrollment season, people struggling to choose a health insurance plan that they can afford and that provides the care they need may ask themselves, “Why is our health care system like this?” The immense amounts of money Big Insurance spends to blanket members of Congress with contributions and lobbying hold the answer.

Additional analysis following the election will allow evaluation of just how much Big Insurance spends on politics to help protect industry profits and will give health reform advocates an idea of how to overcome this influence to pass policies for patients, not profits.