The U.S. health care industry is approaching a critical inflection point, according to veteran health care strategist Paul Keckley. In a candid and thought-provoking keynote at the 2025 Healthcare Marketing & Physician Strategies Summit (HMPS) in Orlando, Keckley outlined the challenges and potential opportunities health care leaders must navigate in an era of unprecedented economic uncertainty, regulatory disruption, and consumer discontent.

Drawing on decades of policy experience and his signature candid style, Keckley delivered a sobering yet actionable assessment of where the industry stands and what lies ahead.

Paul Keckley, PhD, health care research and policy expert and managing editor of The Keckley Report

Health care now accounts for a staggering 28 percent of the federal budget, with Medicaid expenditures alone ranging from the low 20s to 34 percent of individual state budgets. Despite its fiscal significance, Keckley points out that health care remains “not really a system, but a collection of independent sectors that cohabit the economy.”

In the article that follows, Keckley warns of a reckoning for those who remain entrenched in legacy assumptions. On the flip side, he notes, “The future is going to be built by those who understand the consumer, embrace transparency, and adapt to the realities of a post-institutional world.”

A Fractured System in a Fractured Economy

Fragmentation complicates any effort to meaningfully address rising costs or care quality. It also heightens the stakes in a political climate marked by what Keckley termed “MAGA, DOGE, and MAHA” factions, shorthand for various ideological forces shaping health care policy under the Trump 2.0 administration.

Meanwhile, macroeconomic conditions are only adding to the strain. At the time of Keckley’s address, the S&P 500 was down 8 percent, the Dow down 10 percent, and inflationary pressures were squeezing both provider margins and household budgets.

“Economic uncertainty is not just about Wall Street,” Keckley warns. “It’s about kitchen-table economics — how households decide between paying for care or paying the cable bill.”

Traditional Forecasting Is Failing

One of Keckley’s key messages was that conventional methods of strategic planning in health care, based on lagging indicators like utilization rates and demographics, are no longer sufficient. Instead, leaders must increasingly look to external forces such as capital markets, regulatory volatility, and consumer behavior.

“Think outside-in,” he urges. “Forces outside health care are shaping its future more than forces within.”

He encourages health systems to go beyond isolated market studies and adopt holistic scenario planning that considers clinical innovation, workforce shifts, AI and tech disruption, and capital availability as interconnected variables.

Affordability and Accountability: The Hospital Reckoning

Keckley pulls no punches in addressing the mounting criticism of hospitals on Capitol Hill, particularly not-for-profit health systems. Public perception is faltering, with hospital pricing increasing faster than other categories in health care and only a third of providers in full compliance with price transparency rules.

“Economic uncertainty is not just about Wall Street. It’s about kitchen-table economics — how households decide between paying for care or paying the cable bill.”

“We have to get honest about trust, transparency, and affordability,” he says. “I’ve been in 11 system strategy sessions this year. Only one even mentioned affordability on their website, and none defined it.”

Keckley also predicts that popular regulatory targets like site-neutral payments, the 340B program, and nonprofit tax exemptions will face intensified scrutiny.

“Hospitals are no longer viewed as sacred institutions,” he says. “They’re being seen as part of the problem, especially by younger, more educated, and more skeptical Americans.”

The Consumer Awakens

Perhaps the most urgent shift Keckley outlines is the redefinition of the health care consumer. “We call them patients,” he says, “but they are consumers. And they are not happy.”

Keckley cites polling data showing that two out of three Americans believe the health care system needs to be rebuilt from the ground up. Roughly 40 percent of U.S. households have at least one unpaid medical bill, with many choosing intentionally not to pay. Among Gen Y and younger households, dissatisfaction is particularly acute.

“[Consumers] expect digital, personalized, seamless experiences — and they don’t understand why health care can’t deliver.”

These consumers aren’t just passive recipients of care; they’re voters, payers, and critics. With 14 percent of health care spending now coming directly from households, Keckley argues, health systems must engage consumers with the same sophistication that retail and tech companies use.

“They expect digital, personalized, seamless experiences — and they don’t understand why health care can’t deliver.”

Tech Disruption Is Real

Keckley underscores the transformative potential of AI and emerging clinical technologies, noting that in the next five years, more than 60 GLP-1-like therapeutic innovations could come to market. But the deeper disruption, he warns, is likely to come from outside the traditional industry.

Citing his own son’s work at Microsoft, Keckley envisions a future where a consumer’s smartphone, not a provider or insurer, is the true hub of health information. “Health care data will be consumer-controlled. That’s where this is headed.”

The takeaway for providers: Embrace data interoperability and consumer-centric technology now, or risk irrelevance. “The Amazons and Apples of the world are not waiting for CMS to set the rules,” Keckley says.

Capital, Consolidation, and Private Equity

Capital constraints and the shifting role of private equity also featured prominently in Keckley’s remarks. With declining non-operating revenue and shrinking federal dollars, some health systems increasingly rely on investor-backed funding.

But this comes with reputational and operational risks. While PE investments have been beneficial to shareholders, Keckley says, they’ve also produced “some pretty dire results for consumers” — particularly in post-acute care and physician practice consolidation.

“Policymakers are watching,” he says. “Expect legislation that will limit or redefine what private equity can do in health care.”

Politics and Optics: Navigating the Policy Minefield

In the regulatory arena, Keckley emphasizes that perception often matters more than substance. “Optics matter often more than the policy itself,” he says.

He cautions health leaders not to expect sweeping policy reform but to brace for “de jure chaos” as the current administration focuses on symbolic populist moves — cutting executive compensation, promoting price transparency, and attacking nonprofit tax exemptions.

With the 2026 midterm elections looming large, Keckley predicts a wave of executive orders and rhetorical grandstanding. But substantive policy change will be incremental and unpredictable.

“Don’t wait for a rescue from Washington. The future is going to be built by those who understand the consumer, embrace transparency, and adapt to the realities of a post-institutional world.”

The Workforce Crisis That Wasn’t Solved

Keckley also addresses the persistent shortage of health care workers and the failure of Title V of the ACA, which had promised to modernize the workforce through new team-based models. “Our guilds didn’t want it,” Keckley notes, bluntly. “So nothing happened.”

He argues that states, not the federal government, will drive the next chapter of workforce reform, expanding the scope of practice for pharmacists, nurse practitioners, and even lay caregivers, particularly in behavioral health and primary care.

What Should Leaders Do Now?

Keckley closed his keynote with a challenge for marketers and strategists: Get serious about defining affordability, understand capital markets, and stop defaulting to legacy assumptions.

“Don’t wait for a rescue from Washington,” he says. “The future is going to be built by those who understand the consumer, embrace transparency, and adapt to the realities of a post-institutional world.”

He encouraged leaders to monitor shifting federal org charts, track state-level policy moves, and scenario-plan for a future where trust, access, and consumer empowerment define success.

Conclusion: A Health Care Reckoning in the Making

Keckley’s keynote was more than a policy forecast; it was a wake-up call. In a landscape shaped by economic headwinds, political volatility, and consumer rebellion, health care leaders can no longer afford to stay in their lane. They must engage, adapt, and transform, or risk becoming casualties of a system under siege.

“Health care is not just one of 11 big industries,” Keckley says. “It’s the one that touches everyone. And right now, no one is giving us a standing ovation.”

This annual look at high-impact trends affecting healthcare in the coming year is based on evaluation of current industry research data. Healthcare Finance Trendsfor2023 (Trends) explores eight themes identified by CommerceHealthcare® ranging across four areas:

Financial. Providers enter the year contending with multiple financial stress points. They will also seek growth in technology-enabled remote care.

Patient financial experience. The need to drive not only improvement but also personalization of the financial experience is paramount. A central role will be played by patient financing programs which will see growing demand in 2023.

Trust. Building trust with all constituencies is explored as a linchpin for long-term provider success. The latest findings on cybersecurity show that this contributor to trust will continue to consume leadership attention.

Digital transformation. Pursuit of digital-first operations is accelerating, with the finance area an important focus. Emerging payment modes are finding a home in healthcare’s digital finance landscape.

This report’s consistent message is that these trends intersect in ways that compound both the challenges and the upside potential of strategies that address them.

1. Multiple Financial Stress Points Will Constrain Options

Healthcare’s financial predicament for the next 12–18 months is being described in strong terms. Citing $450 billion of EBITDA that could be in jeopardy, more than half of the industry’s project profit pool by 2027, one analyst suggests “a gathering storm.” Another perceives “broad and serious threats” as “elevated expenses” erode margins and exact “a profound financial toll.” Fitch Ratings issued a “deteriorating” outlook for nonprofit health systems.

These financial headwinds are upending healthcare’s traditional status as “recession-proof.” It is helpful to probe the multiple forces in play, the urgent workforce management challenge, and the varied solution set.

Multiple stress factors at work

Observing that margins will be down 37% in 2022 relative to pre-pandemic, a recent stark assessment concluded, “U.S. hospitals are likely to face billions of dollars in losses — which would result in the most difficult year for hospitals and health systems since the beginning of the pandemic.”

A confluence of factors is exacerbating the stress for 2023:

Rising acuity levels. Over two-thirds of surveyed C-suite executives said patient health has worsened from pandemic-induced delayed care. The upshot, stated by 27% of CFOs, is rising expenses due to higher acuity. Inpatient days are projected to increase at an 8% rate over the coming decade.

Reimbursement gaps and inflation. Commercial and government reimbursement rates are not keeping pace with rising costs. Surging inflation is widening this gap. Hospitals are also reporting substantial insurer payment delays and denials.

Investment declines. Stock and bond market declines have removed a cushion for operating weakness. Market uncertainty will complicate 2023 portfolio management.

Persistent workforce concerns remain center stage

Burnout and shortages have disrupted the clinical workforce. Nearly 60% of physician, advanced practice provider and nurse survey respondents said their teams are not adequately staffed, and 40% lack resources to operate at full potential. Many providers face extreme to moderate shortages of allied health professionals.

The problem extends beyond the clinical. A survey saw 48% of respondents experiencing severe labor deficiencies in revenue cycle management (RCM) and billing, and one in four finance leaders must fill over 20 positions to be fully staffed.

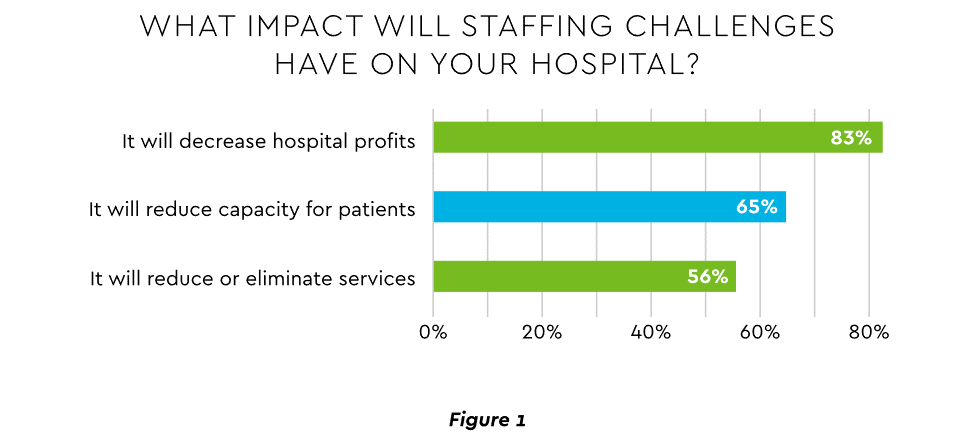

An executive outlook highlighted demonstrable impact on financial performance and growth from these workforce problems, citing reductions in profitability, capacity and service (Figure 1).1

Expenses. Hospital employee expense is expected to increase $57 billion from 2021 to 2022, with contract labor ballooning another $29 billion. Average weekly earnings are up 21.1% since early 2022. Half of medical practices budgeted higher staff cost-of-living increases in 2022. Shortages plague post-acute facilities as well. Their reduced capability to accept discharged patients is lengthening many hospitals’ patient stays.

Capacity constraint. Two-thirds of healthcare leaders identify “ability to meet demand” as their top workforce concern, suggesting a “looming capacity gap between future demand and labor supply.”

Range of measures being deployed

Health systems, hospitals and practices will vigorously pursue at least four direct actions to overcome the financial and staffing hurdles:

Cost cutting. Expense control will be paramount and “hospitals will be forced to take aggressive cost-cutting measures.” McKinsey estimates total industry administrative savings of $1 trillion through multiple aggressive changes.

Service line rationalization. Providers are rethinking how they deliver services to optimize efficiency. One path is utilizing “lower level” healthcare professionals in ways that free RNs and LPAs for more complex work suited to their top skills. Integrating remote care into the mix is another core element of the strategy.

Recruitment and retention programs. Attracting and retaining talent is crucial. Compensation is one avenue. Over two-thirds of organizations are offering signing bonuses for allied health professionals. Some are instituting value-based payments for physicians, offering salary floors to protect from drops in patient volume. CFOs and CNOs are joining forces to invest in nurse retention strategies.

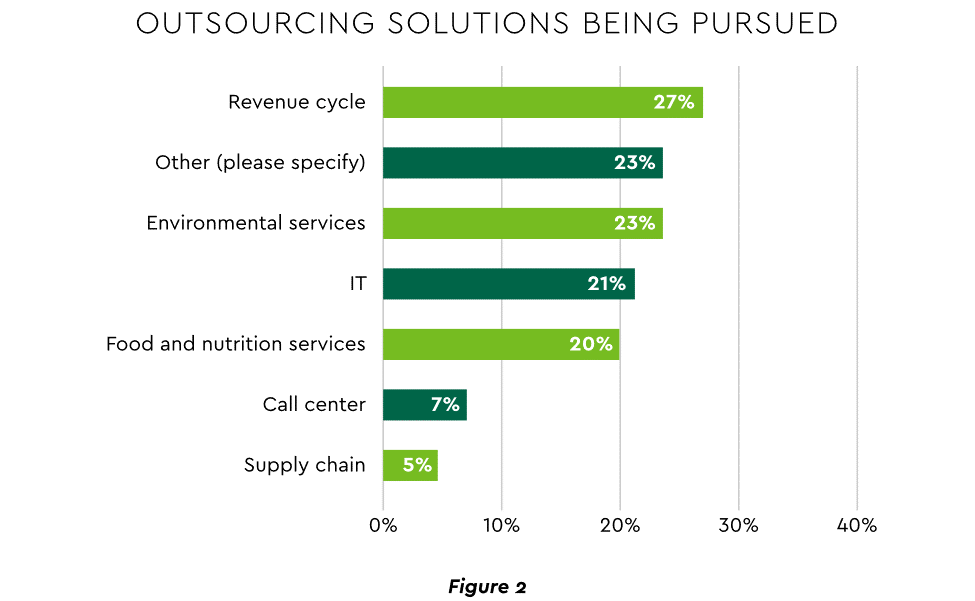

Staffing management. An increasingly popular tool to reduce labor cost and optimize staff resources is outsourcing. Figure 2 shows that RCM is leading the way among those using the solution.

2. Growth Strategies Favor Outpatient, Virtual, Acute Home Care

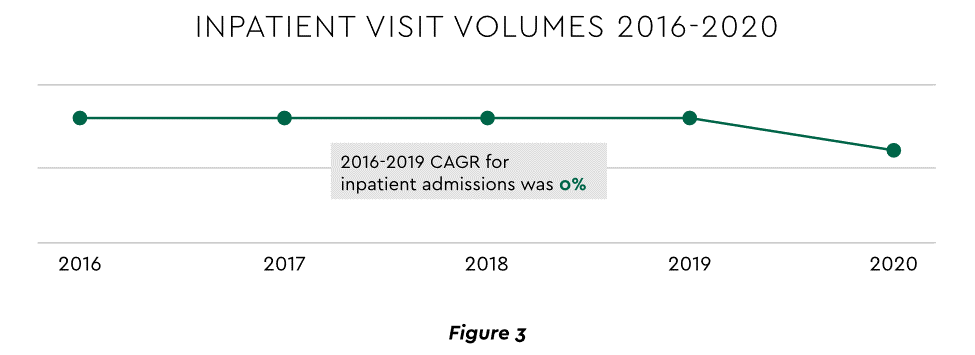

Pursuing top line growth in tandem with reining in expenses is essential. Inpatient volume growth has been tepid for several years ─ essentially flat in the 2016–20 period (Figure 3).

Leaders have been pivoting to outpatient and virtual care to diversify revenue streams. Two high-potential 2023 growth tracks in this sector merit deeper assessment.

Telehealth

Considerable evidence attests to strong commitment to telehealth and remote care. Sixty-three percent of physicians worldwide expect most consultations to be performed remotely within 10 years. Approximately 40% of health centers are using remote patient monitoring today. Consumers are also positive: 94% definitely or probably will use telehealth again, 57% prefer it for regular mental health visits and 61% use it for convenient care.

Telehealth is still in early stages of maturity. Only 4% of surveyed top executives consider their organization proficient at implementing remote care. Healthcare is also recognizing that a full telehealth ecosystem must be constructed. A physician leader explained that the industry’s early telehealth incarnations failed to build “virtual-only environments or really drive e-consults as a way of doing things.” A vital ecosystem demands alterations to current contracts, coding, collections, patient financing, staff training and other business practices.

Hospital-at-Home (HaH)

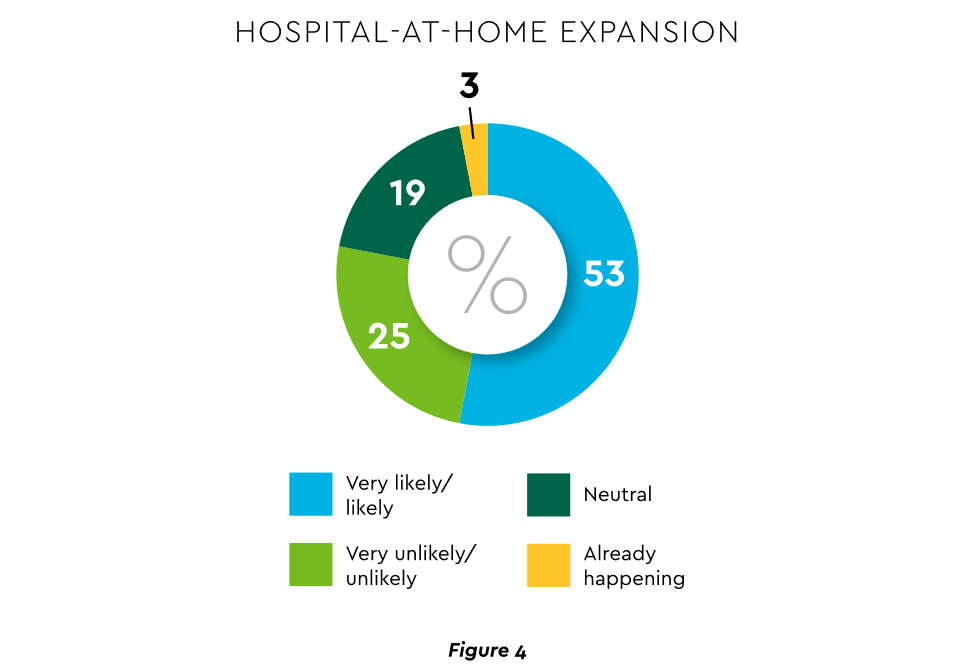

Health systems see particularly promising growth in the provision of acute care in patients’ home settings, including post-surgical and cancer treatment. The federal government has already allowed waivers to 114 systems and 256 hospitals to obtain inpatient-level reimbursement for acute care at home. However, these waivers were prompted by the pandemic and are slated to end in early 2023. The renewal uncertainty has stymied some activity and represents an overhang on the opportunity. However, enthusiasm appears strong, and 33% of hospitals in a recent poll said they would be prone to continue HaH even without renewal.

The forecasts are encouraging. Over half of hospitals believe it likely they will utilize HaH for at least half of their chronically ill patients over the next several years (Figure 4).

Harvesting the HaH potential will require implementation of current and emerging enabling technologies in remote monitoring, high-speed networks and artificial intelligence that generates algorithmic guidance for caregivers and patients alike.

3. Strong Drive to Improve and Personalize the Patient Financial Experience

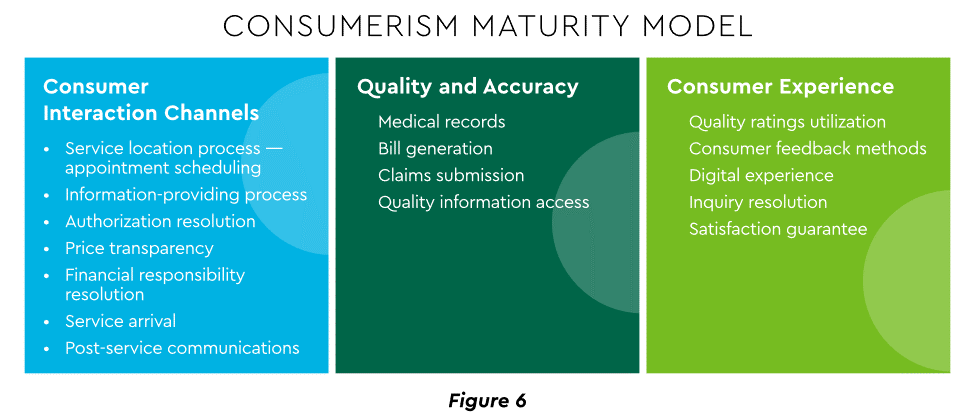

Today’s healthcare market dynamics place a premium on positive patient experiences. The goal is to deliver “an empathetic relationship between customers and brands built on what the customer wants and how they want to be treated.” It is a complex undertaking, with numerous touchpoints as captured in HFMA’s Consumerism Maturity Model (Figure 6).

An array of studies underscores the value proposition for intense provider focus on patient financial experience:

Sixty-one percent of consumers said that ease of making payments is very or somewhat important in decisions to continue seeing a doctor. Over half of patients also said text message reminders make them very or somewhat more likely to pay a bill faster than usual.

Thirty-five percent of respondents “have changed or would change healthcare providers to get a better digital patient administrative experience.”

A quality financial experience encompasses “simplified explanations, consolidated bills that match one’s health plan benefits, clear language displaying patient liability and payment options.”35

Significantly improving the financial experience requires a unified strategy, not just a collection of individual initiatives. Three threads to such a strategy will be prominent in 2023.

Using a Digital Front Door

Organizations have been moving swiftly to channel many patient financial transactions through an integrated Digital Front Door (DFD). This approach offers patients a singular online point of access and intelligent navigation to needed services. Growth is accelerating. A DFD is their patients’ first contact point for 55% of responding organizations, according to one technology survey. A leading forecaster sees 65% of patients engaging services via digital front doors by 2023.

Expanding price transparency

Mandates for full price transparency and “no surprises” billing are in effect, but estimates of compliance are mixed. An analysis of 2,000 hospitals determined that only 16% met the requirement to post an online “machine readable” file displaying clear charges for 300 “shoppable services.” Another assessment showed a more substantial 76% of hospitals had posted files, and 55% were deemed “complete.” One provision of interest to practices is the “good faith estimate” of expected charges required to be given to uninsured and self-pay individuals when they schedule visits. CommerceHealthcare® has worked with clients to enhance the patient financial experience by complementing their website pricing data with clear information on patient financing options and enrollment access. Bill pay information can also be added for one-stop guidance.

Personalizing the experience

Beyond choice and convenience, the deeper objective is truly personalized experiences throughout the care journey. The words of leading analysts best define the drive to personalize:

“Tomorrow’s healthcare experience will be built by patients tailoring their own experience.”

“By 2024, 30% of chronic care patients will truly own and openly leverage their personal health information to advocate for, secure, and realize better personalized care.”

Opportunities abound to personalize the patient financial experience. Automating manual processes establishes a foundation. Patient financing with no- or low-interest credit lines and flexible terms can produce monthly payment schedules tailored to each patient’s needs. Refunds can be made through multiple payment modes to meet varying patient preferences.

4. Evidence Underscores Growing Demand for Patient Financing

Emphasizing patient financing as part of the overall experience is powerful. Patients continue to struggle paying for care. Recent granular data details three related forces at work.

Meeting care costs difficult for many patients

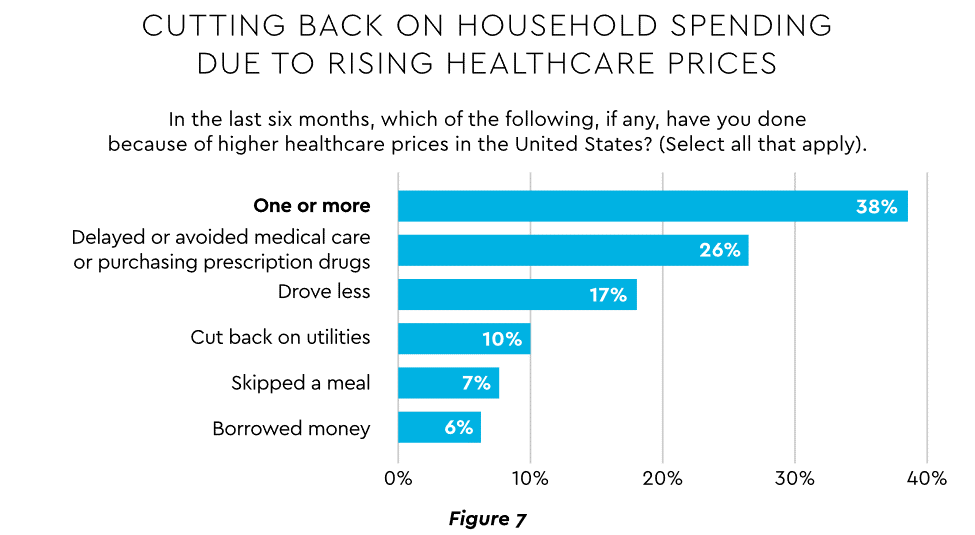

Commonwealth Fund found that 42% of individuals had problems paying medical bills or were paying off medical debt during the past year, while 49% were unable to pay an unexpected $1,000 medical bill.42 Health costs trigger reduction in a range of personal expenditures, led by deferring or avoiding care and drugs (Figure 7).

Twenty-eight percent of Americans now describe themselves as less prepared than last year to pay for routine or unanticipated care.

Patient obligation for care costs still rising

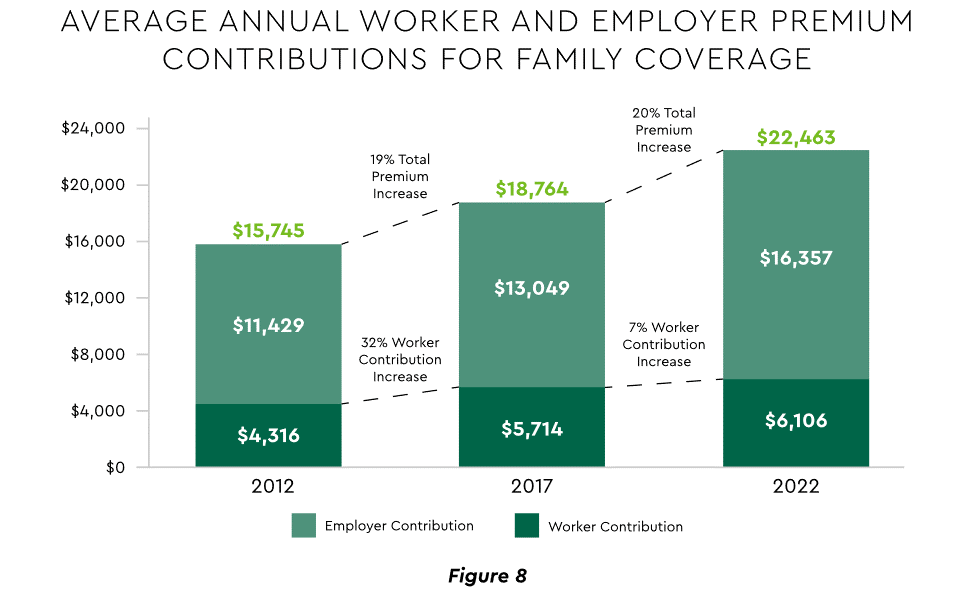

Patient obligation continues its upward march. Insurance premiums have climbed steadily for both the insured and their employers, and employees now pay over $6,000 annually on average for family coverage (Figure 8).45

High deductible health plans (HDHP) also place substantial burden on the patient. Through 2021, 28% of workers were enrolled in an HDHP with an average family deductible of $4,705. Employer satisfaction with these plans is high, auguring further expansion.

Providers feeling the financial effects

Patient payment difficulties are clearly impacting provider financials. A recent in-depth analysis uncovered substantial self-pay issues:

Self-pay accounts represented 60% of 2021 patient bad debt, up from 11% in 2018.

Nearly 18% of patient balances were over $7,500 and 17% over $14,000. Collections were noticeably lower at these balances.

Multiple chronic conditions add to the problem. A recent extensive analysis concluded: “Among individuals with medical debt in collections, the estimated amount increased with the number of chronic conditions ($784 for individuals with no conditions to $1,252 for individuals with 7–13).”

For their part, providers will be encouraged to broaden patient financing programs. Patients are certainly interested. When asked, 62% of consumers indicated they would use financing options or creative payment plans if available for large bill amounts. Many health systems, hospitals and practices will turn to outside help to satisfy the demand. A recent analysis recommended that health systems “consider keeping shorter-term payment plans in-house and extended term plans through external partnerships.”

Organizations will also need to step up their communications. A survey revealed that 64% of patients were unaware that their doctors and hospitals offered payment plans or financial help.

5. Building Trust Becoming a Critical Success Factor

Trust has emerged as a paramount issue today for most organizations as they encounter an “imperative to build trust and transparency among different stakeholder groups — employees, customers, suppliers, regulators and the communities in which they operate.” Healthcare is no exception, and the trust issue is growing in both complexity and urgency.

Healthcare’s trust gap

Trust in healthcare took a hit from the COVID-19 experience. A spring 2022 HFMA survey recorded 44% of finance leaders saying they perceived decreased patient trust. Between April 2020 and December 2021, the percentage of Americans who trusted information from doctors “a great deal” declined by 23%, from hospitals 21%, and from nurses 16%. The patient financial experience also faces “drivers of mistrust,” according to surveyed leaders who cited general payment confusion (58%), surprise billing (39%), high prices of commodity items (28%) and lack of price transparency (26%). Building trust reaps dividends. People who trust their providers are five times more likely to stay with them than those who are neutral or distrustful.

Strategies for building trust

Industry experts promote several approaches to galvanize trust among all constituencies:

Commitment. Embedding trust deeply in the organization requires full support from senior leadership.

Data transparency and governance. IDC predicts that “by end of 2023, 20% of expenses on care integration solutions will be centered around ‘trust’ to protect data, workflows and transactions.”

Reliance on fewer business partners. Many health systems, hospitals and practices are reducing their number of vendors in order to focus on a set of trusted long-term partners. For example, almost two-thirds of surveyed providers said they were seeking to streamline the number of software solutions over the next year.

The bank partner advantage

A provider’s banking relationship can yield valuable collaboration in the trust-building endeavor. Banks enjoy solid trust among consumers. As an example, 53.4% of consumers rated banks as most trusted to provide payment “super apps” and financial digital front doors ─ exceeding the next closest source by 10 points.

6. Cybersecurity in 2023: No Rest for the Weary

Cybersecurity is part of the trust calculus and has become an evergreen topic in healthcare. Compromised data and ransomware attacks are ongoing and leaders must continually refine their understanding in at least three areas: the overall security landscape, particular financially related considerations and contemporary security defenses.

The current landscape

The latest statistics quantify the cyber assault on healthcare:

Incidence. 89% of organizations suffered at least one attack in the past 12 months with the average number at 43.

Cost. A provider’s most serious attack costs an average of $4.4 million. IBM calculated healthcare’s average total cost of a breach at $10.1 million, up 42% since 2020.

Attack Characteristics. Healthcare data types most commonly compromised are personal (58%), medical (46%), and credentials (29%). Organizations have an exposure to an average of over 26,000 network-connected devices. A disturbing finding is that those healthcare institutions that paid ransom got back only 65% of their data in 2021.

Specific financial considerations

Finance leaders will also need awareness of the following:

Cyberattacks could affect credit ratings and are often a component of Environmental, Social and Governance assessments.

Financial outsourcing requires monitoring. A recent news story chronicled an accounts receivable firm’s breach that exposed individual information, account balances and payments.

Cyber insurance premiums are likely to increase substantially.

Responses/tools

Beyond a host of management and monitoring tools being deployed, a strategic philosophy is rapidly gaining ground. The “zero trust” model sounds counter to the trust-building mindset described earlier, but it has become essential. It “denies access to applications and data by default,” and 58% of hospitals and health systems have a zero trust initiative in place. Another 37% intend to implement one within 12–18 months.

Cybersecurity investment will challenge CFOs in 2023, especially in areas such as talent. Cybersecurity worker availability is estimated to satisfy only 68% of open positions. Banking partners will also be expected to play an important role. Over the years, major banks have become “leaders in enhancing cyber strategy and investing in cyber defenses, processes and talent.”

7. Digital Transformation of Finance In Focus

Digital transformation is fundamental to healthcare’s business and care delivery model changes. IBM’s website succinctly captures the goal, “Digital transformation means adopting digital-first customer, business partner, and employee experiences.” A leading forecaster believes 70% of healthcare organizations will rely on digital-first strategies by 2027.

Transformation efforts need to accelerate. One study showed that “digital, technology and analytics strategies exist for nearly all organizations, yet only 30% have begun to execute on those plans.”

One functional segment ramping up digital transformation is finance. According to a recent survey, 94% of CFOs and senior leaders stated that such efforts will be at the forefront of financial operations and strategy for 2023–2024, and 79% described it as an “absolute need” for “commercial stabilization and long-term survival of their healthcare organization.”

Advanced technology is gaining traction. Many see optimization in combining robotic process automation (RPA), artificial intelligence and machine learning to create “intelligent automation.” Together, these technologies create algorithms to automate decisions that guide “robotic” software to perform financial actions and thereby reduce manual labor.

Getting to digital-first in finance and across the enterprise has several critical success factors. These include sustained commitment, a platform-centric mindset and effective governance.

Commitment

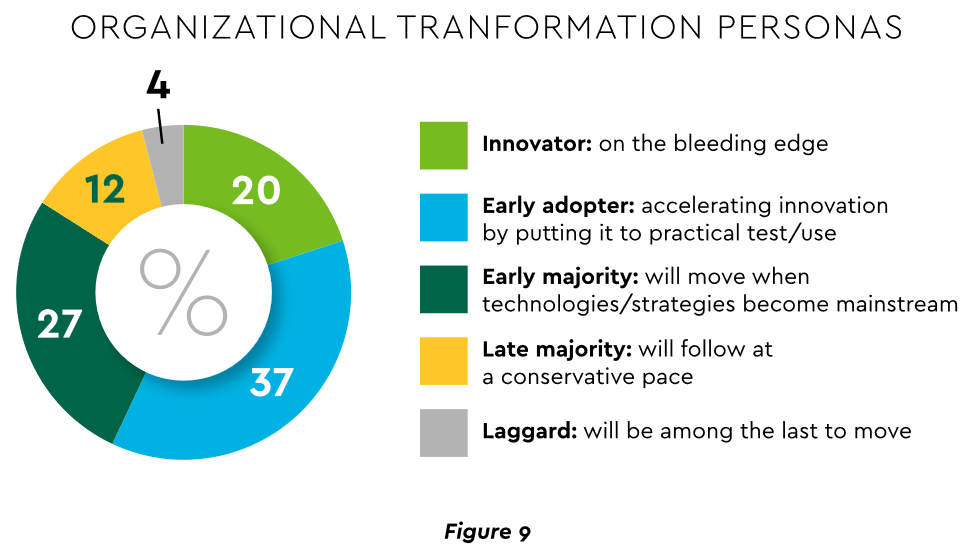

Some assert that few healthcare executives have “created digital strategies that look far enough into the future.” Speed of change is also important. Health systems, hospitals and practices exhibit varying risk appetites and change rates. When asked to self-identify “transformation personas,” a little over half regarded themselves as being on the innovative “early mover” end of the spectrum, while the remainder will adapt as technologies prove themselves (Figure 9). Slower organizations will likely need to increase the pace.

Implementing enterprise platforms rather than proliferating “point solutions” is obligatory. Organizations must be “prepared to compete in the platform economy as platform-based business models have changed the way we live, work and receive care.”

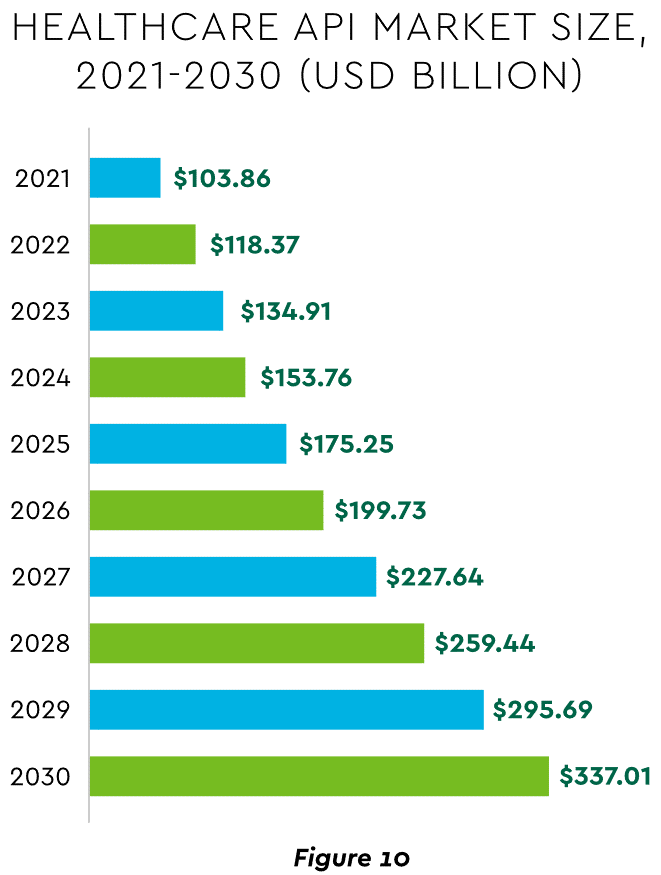

There are still too many tools and applications. A survey of top decision-makers at health systems found that 60% use over 50 software solutions just in operations (24% have over 150). System integration is one answer. Use of application programming interfaces (API) helps this effort substantially. API-first is fast becoming the norm among solution providers, with global API investment expected to nearly triple by 2030 (Figure 10)

Effective governance is vital to constructing a platform-based transformative model and to ensuring wide user adoption. Healthcare has seen the rise of new senior roles such as Chief Digital Officer and Chief Transformation Officer, positions focusing on initiatives like ownership of technology success at the department level and devising user incentives.

8. Digital Payments on the Horizon for Healthcare

A variety of emerging digital payment modes will further the transformation of finance. These payments are expected to grow almost 23% annually in healthcare. ACH payments have been on a strong upward trajectory in healthcare for several years, especially for business transactions. In 2021, ACH tallied a yearly increase of 18% in volume and 5% in dollars.

Notable technologies and payment rails to watch for expected crossover from consumer markets to healthcare include:

Mobile payments. The market for mobile payment technologies has been growing at a 16% compound annual clip and should reach $90 billion in 2023, powered by wide smartphone use, 5G networks and convenience. This category encompasses technologies such as e-wallets, forecasted to grow 23% annually worldwide through 2030.

Real-time payments (RTP). These digital transactions are settled nearly instantaneously through platforms such as The Clearing House. One forecast sees 30.4% compound RTP growth in the U.S. from 2022 to 2030.

Buy Now Pay Later (BNPL). This growing mode offers consumers short-term financing to stretch payments over several installments. A recent survey established that 23% of American adult respondents have used a BNPL service. BNPL is just entering healthcare and is currently regarded as an option for certain elective or cosmetic procedures or for specific individual credit scenarios.

Earned Wage Access (EWA). Using an RTP approach, employers are beginning to offer on-demand pay which enables “instant access to earned wages right after the work is performed, at the end of the shift, or upon completion of a project.” It is not a loan or advance pay. A 2021 poll conducted by Harris found that 83% of U.S. workers feel they should be able to access earned wages at the end of each day. Millennials were particularly interested: 80% would like daily automatic pay streaming to their bank accounts, and 78% said free EWA would boost loyalty to their employer. Given its pressing workforce concerns, healthcare is likely to find EWA a tool to promote retention.

Seeking the right use cases for these payment technologies offers many potential provider benefits.

Conclusion

The connected forces discussed and quantified here create major challenges to address in 2023. The strategic agenda calls for balancing tight cost control with investment in growth opportunities, significantly enhancing patient financial experience by meeting growing patient financial need, shoring up trusted relationships and cybersecurity, and accelerating the digital transformation of finance.

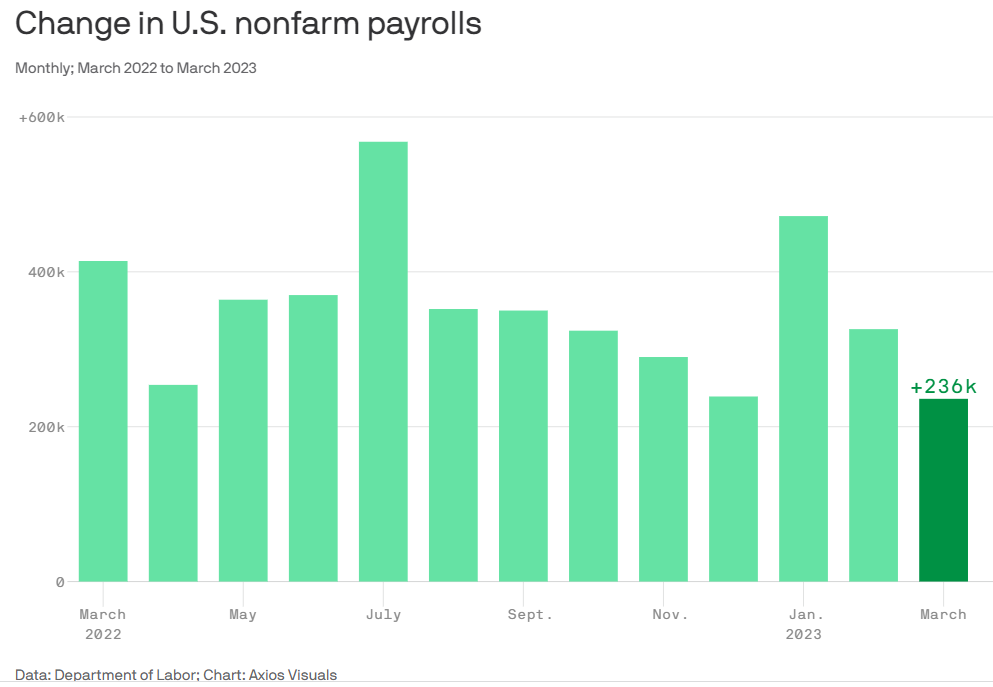

The labor market added 253,000 payrolls in April, while the unemployment rate dipped to 3.4% — a historically low level.

Why it matters:

Job growth continued to boom last month, the latest sign that economy has strong momentum despite recent bank failures.

Economists expected a gain of 185,000 jobs last month.

Details:

The April job figures are a pickup from the 165,000 jobs added the previous month, which were revised down by 71,000, the Labor Department said on Friday.

The Labor Department said that jobs growth in the previous two months was lower than first estimated: jobs growth was revised down by a combined 149,000 for February and March.

The big picture:

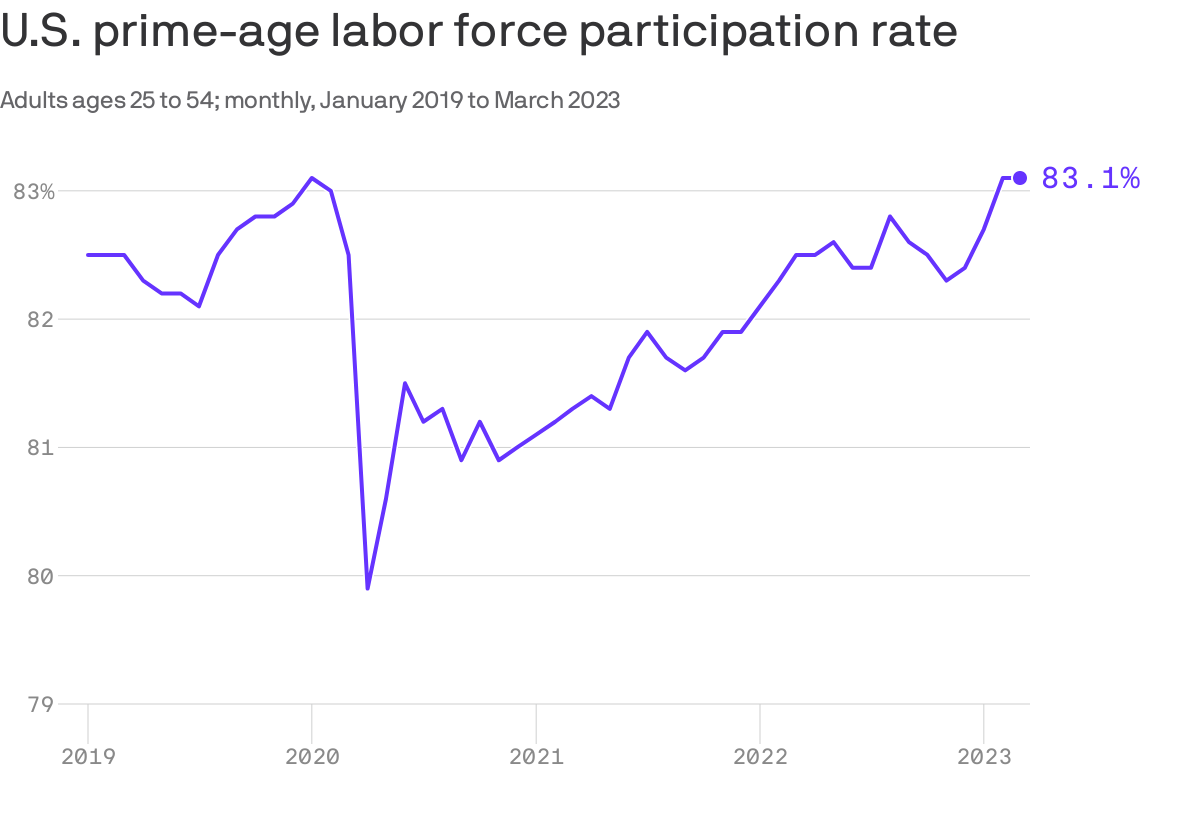

In recent months, more Americans have joined the workforce, helping to ease labor force shortages.

The labor force participation rate — or the share of workers employed or looking for work — held at 62.6% in April.

Average hourly earnings, a measure of wage growth, rose to 0.5% in March. Wages rose 4.4% from the same time last year.

But Fed Chair Jerome Powell said this week that there were signs that the workforce was “coming back into better balance,” though it remained “very tight.”

One of the most persistent economic narratives of 2021 and 2022 was that of missing workers. Many Americans seemed to have simply vanished from the labor force during the pandemic, leaving employers in a lurch.

That’s no longer the case, White House economists argue in a new post presenting evidence that labor supply has returned to its pre-pandemic trend.

Why it matters:

It would be way less painful if the U.S. labor market were to come into a better, non-inflationary balance because labor supply increased, rather than labor demand decreased.

And contrary to a widespread economic narrative of the last couple of years, that seems to be happening — as the Biden team seeks to emphasize.

State of play:

There has been ample speculation about why labor supply was depressed in the aftermath of the pandemic, the White House Council of Economic Advisers notes.

Maybe fear of COVID, or long COVID symptoms, kept people out of work. Maybe it was excess savings from the pandemic, or reassessment of life priorities, or a “collective loss of work ethic.”

Nah. It increasingly looks as if it just took some time for potential workers to match up with jobs and return to the labor force.

By the numbers:

The share of prime-age workers — those between 25 and 54 — who are part of the workforce is now a tick higher than it was before the pandemic: 83.1%, compared with 83.0% in February 2020.

The overall participation rate is down (62.6%, from 63.3% in February 2020), but that is due to the Baby Boom generation retiring. It’s on track with what forecasters at the Congressional Budget Office anticipated before the pandemic.

Moreover, immigration rates surged in 2022 after a pandemic collapse, also adding to the supply of labor.

What they’re saying:

“The swift but lagged response of labor supply to surging demand suggests that with time workers do respond to favorable economic conditions,” the White House economists write.

“There are many plausible reasons that explain why this response is lagged. Most obviously, the job search process itself is not frictionless; it may take workers some time to find a good job,” they wrote.

“Also, if households adapted to the pandemic in ways that can take a while to unwind (such as giving up formal child care), this would delay the labor supply response to growing demand.”

The bottom line:

“There’s still an inaccurate view that prime-age labor supply is depressed,

that immigration is way down, and that labor force participation rates aren’t back on trend following the pandemic shock to our economy,” Ernie Tedeschi, the chief economist at the CEA, tells Axios.

In fact, he said, tight labor markets “pull folks back into the workforce and, while we have more to do to break down barriers to entry, the ‘missing worker’ story doesn’t quite apply anymore.”

Workforce problems in U.S. hospitals are troublesome enough for the American College of Healthcare Executives to devote a new category to them in its annual survey on hospital CEOs’ concerns. In the latest survey, executives identified “workforce challenges” as the No. 1 concern for the second year in a row.

Financial challenges, which consistently held the top spot for 16 years in a row until 2021, were listed the second-most pressing concern in the American College of Healthcare Executives’ annual survey.

Although workforce challenges were not seen as the most pressing concern for 16 years, they rocketed to the top quickly and rather universally for healthcare organizations in the past two years. Most CEOs (90 percent) ranked shortages of registered nurses as the most pressing within the category of workforce challenges, followed by shortages of technicians (83 percent) and burnout among non-physician staff (80 percent).

Here are the most concerning issues hospital CEOs ranked in 2022, along with the score of how pressing CEOs find each issue.

1. Workforce challenges (includes personnel shortages and staff burnout, among other issues) — 1.8

2. Financial challenges — 2.8

3. Behavioral health and addiction issues — 5.2

4. Patient safety and quality — 5.9

5. Governmental mandates — 5.9

6. Access to care — 6.0

7. Patient satisfaction — 6.6

8. Physician-hospital relations — 7.6

9. Technology — 7.7

10. Population health management — 8.6

11. Reorganization (mergers and acquisitions, partnerships and restructuring) — 8.7

Within financial challenges, most CEOs (89 percent) ranked increasing costs for staff and supplies as the most pressing, followed by operating costs (66 percent) and Medicaid reimbursement (63 percent). CEOs are less concerned about price transparency and moving away from fee-for-service.

Seventy-eight percent of CEOs ranked lack of appropriate facilities/programs as most pressing within the category of behavioral health and addiction issues. That was followed by lack of funding for addressing behavioral health and addiction issues (77 percent).

The results are based on a survey administered to CEOs of community hospitals (non-federal, short-term, non-specialty hospitals). ACHE asked respondents to rank 11 issues affecting their hospitals in order of how pressing they are. Results are based on responses from 281 executives.

Healthcare added almost 45,000 jobs in November, but many hospitals and health systems will continue to struggle to meet staffing needs, retain top executives and providers, and foster long-term pipelines for talent, Ted Chien, president and CEO of independent consulting firm SullivanCotter, wrote in a Dec. 15 article for Nasdaq.

Hospitals and health systems are living “paycheck to paycheck” and unable to make long-term investments at the height of the current workforce crisis, Mr. Chien said.

The challenge boils down to a healthcare delivery problem, not a demand problem.

Baby Boomers are the greatest source of care demand on the healthcare system, but are unable to contribute to the provider workforce in the numbers needed to achieve balance, according to Mr. Chien. To compound that issue, burnout is a major factor why “too many” frontline workers have left or plan to exit healthcare, he said.

Last year, an estimated 333,942 healthcare providers dropped out of the workforce, including about 53,000 nurse practitioners, which has led hospitals to spend more on contract labor and feeling more pressure to consolidate, according to an October report published by Definitive Healthcare.

Long term, a continued lack of healthcare workers would force hospitals to operate in a heightened crisis mode, according to Mr. Chien, depriving non-critical patients of sufficient health prevention and demanding too much of providers who are already overly taxed.

Mr. Chien highlighted three key areas to tackle the workforce crisis: smarter technology, resilient teams and excellent leadership.

Technologies that alleviate providers’ administrative burdens will be critical to reduce burnout and keep caregivers focused on patient care, while smarter tech can also forge pipelines for future providers by streamlining clinical experience operations and aligning student placements with existing opportunities.

Building resilient teams begins with competitive pay and robust benefit packages, which fosters trust and demonstrates that a hospital values its staff, according to Mr. Chen. Supporting career growth, including upskilling and redeploying staff when appropriate, empowers employees.

Lastly, capable executive leadership teams, under intense scrutiny from industry stakeholders, must clearly outline their hospital or health system’s strategy and provide the change needed to support their staff. Lack of trust in leaders drives staff out of healthcare, so it is crucial to recruit and retain “modern, strategic thinkers with depth of experience who are prepared to lead,” Mr. Chien wrote.

The majority of hospitals are predicted to have negative margins in 2022, marking the worst year financially for hospitals since the beginning of the Covid-19 pandemic.

In Part 1 of Radio Advisory’s Hospital of the Future series, host Rachel (Rae) Woods invites Advisory Board experts Monica Westhead, Colin Gelbaugh, and Aaron Mauck to discuss why factors like workforce shortages, post-acute financial instability, and growing competition are contributing to this troubling financial landscape and how hospitals are tackling these problems.

As we emerge from the global pandemic, health care is restructuring. What decisions should you be making, and what do you need to know to make them? Explore the state of the health care industry and its outlook for next year by visiting advisory.com/HealthCare2023.

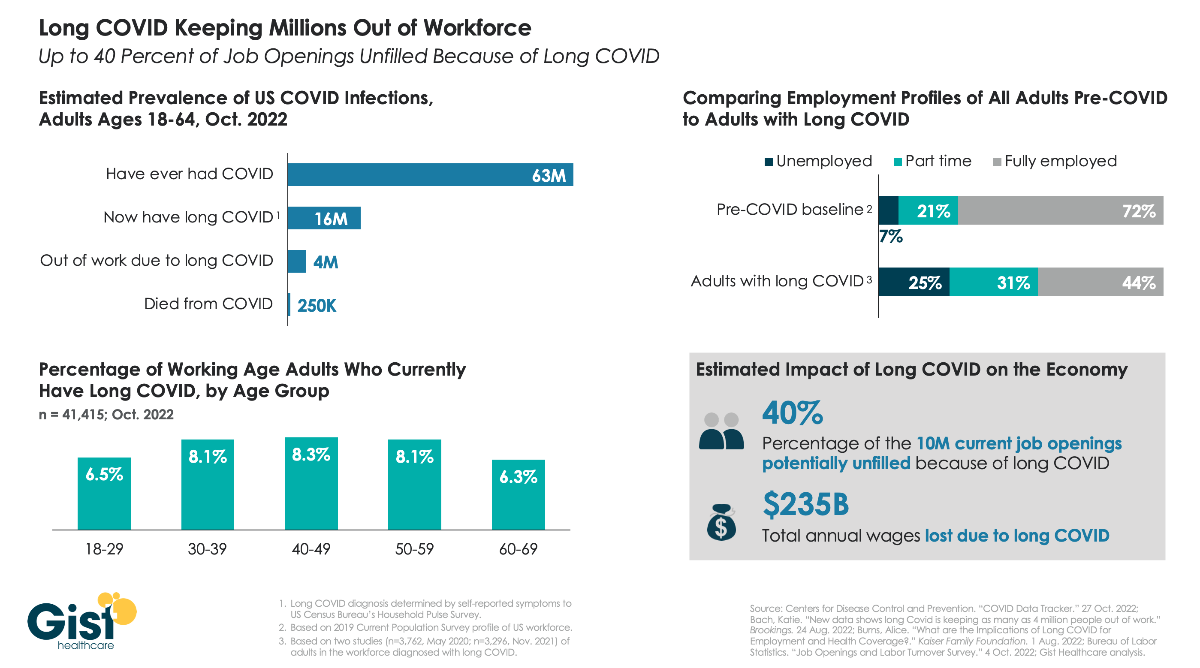

As the nation continues to grapple with the fallout from COVID, one of the greatest unknowns is “long COVID”, the broad range of health problems experienced by a significant number of individuals after contracting the virus. The Centers for Disease Control and Prevention defines long COVID as any post-COVID condition lasting three months or longer.

In the graphic above, we aim to quantify the prevalence of long COVID and its ongoing impact on the US workforce. While estimates for thesenumbers vary, data compiled by Brookings show that COVID infections in roughly one in four working age adults have resulted in long COVID, and up to one in four individuals with long COVID are unable to work due to their lingering health problems. Long COVID is also more prevalent in middle-aged adults, who are often at the peak of their working years. Dealing with symptoms like chronic fatigue and brain fog, long COVID patients are more likely to be unemployed or working reduced hours, compared to a pre-COVID baseline of the general adult population.

While it’s difficult to assess the precise impact on the nation’s current labor shortage, the estimate that 4M working age adults are no longer working because of long COVID equals about 40 percent of the 10M total job openings in August of this year, undoubtedly exacerbating ongoing economic challenges.

Citi, The American Hospital Association (AHA) and the Healthcare Financial Management Association (HFMA) recently hosted the 22nd annual Not-for-Profit Healthcare Investor Conference. The event was in person, after being virtual in 2021 and canceled in 2020 due to the pandemic. Leaders from over 25 diverse health systems, as well as private equity and fund managers, presented in panel discussions and traditional formats. The following summary attempts to synthesize key themes and particularly interesting work by leading health systems. The conference title was “Refining the Now, Reshaping What’s Next.”

Is Healthcare Headed for Best of Times or Worst of Times?

Clearly the pandemic showed how essential and adaptive the US healthcare industry is, and especially how incredible healthcare workers continue to be. It also exposed and accelerated many underlying dynamics, such as impact of disparities, clinical labor shortages and supply chain challenges. On balance, at this year’s conference presenters remained quite optimistic about the future, and felt that despite enormous pain, the pandemic has helped to accelerate positive transformation across healthcare.

At the same time, almost all presenters referenced future headwinds from labor and supply inflation, concerns about increasing payment pressures, and the continued need to address disparities and social justice. That being said, there was not much disclosure at the conference about just how bad things could get in the future given accelerated operational and financial risks.

As usual at such a conference, there was much passion, creativity, sharing and celebration. While each organization and market differ somewhat, the following are common themes discussed.

Key Themes

Enormous Workforce Challenges – Every speaker referenced workforce as being THE key issue they are facing, specifically retirement, recruitment, retention, well-being and cost. We have talked for years about a future caregiver shortage, but this reality was accelerated by the pandemic. The majority of health systems saw single-digit turnover rates grow to 20-30%, and the cost of temporary labor such as traveling nurses, decimate operating margins. The many strategies discussed at the conference went beyond simply paying more to attract and retain staff. A key question is whether organization-specific strategies will be enough, or whether we need a broader societal and industry-wide collaborative effort to dramatically increase training slots for nurses and other allied health professionals.

Pandemic Stressed Organizations and Accelerated Transformation – At the 2021 virtual Citi/AHA/HFMA conference, many posited that the country was past the worst of the pandemic. (In fact this author’s summary of last year’s conference was titled “Sunrise After the Storm”). That was before the Omicron wave hit hard in Q1 2022. First-quarter 2022 operating margins were negative for most but not all healthcare systems due to cumulative impact of Omicron, temporary labor and supply costs, especially since the governmental support that partially offset those costs in 2020 ended. Organizations and their teams remain resilient, but highly stressed. Risks and challenges associated with future waves continue, as well as high reliance on foreign drug and supply manufacturing. While highly distracting and painful, many organizations discussed how the pandemic actually accelerated the pace of transformation. Necessity drives required action, and at least temporarily overcomes political and cultural barriers to change.

Growing Pursuit of Scale, Including through M&A and Partnerships – All health systems continue to be highly complex with multiple competing “big-dot” priorities. Multiple systems described their current M&A and growth strategies, pursuit of scale, as well as how these strategies were impacted by the pandemic. While the provider community remains highly unconsolidated on a national basis, mergers are more frequent, including between non-contiguous markets. Systems said that larger size, coupled with disciplined management, can reduce cost structure and improve quality and patient experience. While some pursue scale through organic growth initiatives or M&A, others described success in creating scale by leveraging partnerships with “best-in-class” niche organizations and other outside expertise.

Health Equity, Diversity and ESG as Core to Mission – Consistent with last year, most speakers discussed their efforts to address health equity, social justice, diversity, and Social Determinants of Health. Many health systems have developed robust strategies quickly as the pandemic spotlighted the impact of existing disparities. There is increasing interest in Environment, Social and Governance (ESG) initiatives, including environmental stewardship to improve the health of their communities and the world by reducing their carbon footprint and medical waste.

Patient-Centric Care Transformation Continues as a Priority – The pandemic significantly accelerated the shift to telehealth and virtual care. Many health systems are increasing their efforts to design care around the patient instead of the traditional provider centric focus. While the need for inpatient care will always continue, more care is taking place in settings closer to or at home, with digital enablement. Expansion of personalized medicine, genetic testing and therapies, and drug discovery are transforming how healthcare is provided.

Affordability and Value-Based Care – US healthcare costs as a percentage of GDP increased from 18% in 2019 to almost 20% in 2020, mainly driven by the pandemic. There remains a dichotomy between reliance on fee-for-service payment and commitment to value-based care. Although only 11% of commercial payment is currently through two-sided risk arrangements, almost all presenting health systems discussed their strategies to continue moving to value-based care and to improve affordability. Some systems are leveraging their integrated health plans and/or expanding risk-based contracts. Many are trying to reduce unnecessary care through adoption of evidence-based models and to shift care to less costly settings.

Inflation and Accelerating Financial Pressures – Health systems are facing unprecedented increases in labor and supply costs, that are likely to continue into the foreseeable future. At the same time, commercial payment rate adjustments are “sticky low” as insurers and employers push back on rate increases. Governmental payment rate increases are less than cost inflation. In addition to current cuts like the re-implementation of sequestration, longer-term cuts to provider assessment programs, provider-based billing, disproportionate share and Medicaid expansion may severely impact many organizations over time. Benefits like 340b discounts are also experiencing pressure. Post-pandemic clinical-volume trends remain unclear, and additional governmental support associated with future pandemic waves is unlikely. Adding to these challenges, declines in stock and bond prices are negatively impacting currently strong balance sheets.

Conclusion: Best or Worst of Times in Healthcare?

Time will tell, in retrospect, if the next five years will be the best of times, worst of times, or both in healthcare. Optimists point to the resiliency of healthcare organizations; enormous opportunity to reduce unnecessary cost through adoption of evidence-based care and scale; pipeline of new cures and technology; and opportunities to address social and health equity. Pessimists point to likely unprecedented financial pressures and operational challenges due to endemic labor and supply shortages; high-cost inflation vs. constrained payment rates; and future uncertainty about the pandemic, the economy and investment markets.

The situation will undoubtedly vary by market and organization as reflected in conference presentations, but all systems will likely face substantial pressure. As one speaker noted “humans have a great ability to respond to pain,” so this may be the inflection point where more healthcare systems radically accelerate necessary change to improve health, make healthcare more equitable and affordable, with higher quality and better outcomes. Some health systems are clearly doing that, with pace, nimbleness and passion. Can the industry as a whole accomplish it successfully?