HCA Healthcare is the single hospital operator that Bloomberg identifies as one of “50 Companies to Watch in 2024.”

“From Alphabet and BYD to Eli Lilly and Vivendi, keep an eye on these global stocks this year,” the outlet proposes for the 50 companies out of the 2,000 firms assessed. Bloomberg analysts highlighted the companies as those warranting a closer look, based on “contrarian views and upcoming catalysts for change such as new leadership, asset sales or acquisitions, and plans for new products and services.”

With 182 hospitals and more than 37,000 hospital beds, Bloomberg analyst Glen Losev said HCA “faces cost and revenue challenges that point to a reduction in its operating margin. Wages are increasing, especially for nurses, as are non-labor costs because of general inflation. And fewer physician visits indicate softening demand for care in areas such as elective surgeries.”

HCA is tied to an estimated 5% increase to its revenue in 2024 with a market cap of $72 billion.

The company posted $47.66 billion in revenue for the first nine months of 2023 compared to $44.73 billion in the same period of 2022. Its fourth quarter earnings are due later this month.

Other healthcare companies recognized by Bloomberg as worth watching are Novo Nordisk, BeiGene, Boston Scientific and Eli Lilly. Weight loss drug possibilities drive potential for Novo Nordisk and Eli Lilly, with estimated revenue increases of 22% and 16%, respectively.

The majority of hospitals are predicted to have negative margins in 2022, marking the worst year financially for hospitals since the beginning of the Covid-19 pandemic.

In Part 1 of Radio Advisory’s Hospital of the Future series, host Rachel (Rae) Woods invites Advisory Board experts Monica Westhead, Colin Gelbaugh, and Aaron Mauck to discuss why factors like workforce shortages, post-acute financial instability, and growing competition are contributing to this troubling financial landscape and how hospitals are tackling these problems.

As we emerge from the global pandemic, health care is restructuring. What decisions should you be making, and what do you need to know to make them? Explore the state of the health care industry and its outlook for next year by visiting advisory.com/HealthCare2023.

2022 has disproven the old trope that “healthcare is recession-proof”. With the average family deductible nearing $4,000, a significant portion of healthcare services are exposed to consumer concerns about affordability. Reflecting the impact of the recession, health systems nationwide have reported sluggish volumes, particularly for elective cases, in the second half of the year.

One COO recently shared, “We’re 15 percent off where we expected to be on elective cases…We didn’t see the usual pick-up in early fall, after summer vacation. I’m not sure if it’s related to the economy, or whether demand changed during COVID, but this decline has eroded any possibility of a positive margin for the quarter.” The recession hit just as providers mostly finished working through the backlog of cases delayed by COVID in 2020 and 2021.

To determine whether demand declines are related to the current economic environment, or signal real shifts in care patterns, health systems are looking closely to see if the usual end-of-year swell of demand for elective care materializes, as patients max out their deductibles. But even if the demand is there, some systems are worried about being able to accommodate it: “We’ve been so short-staffed for nurses and surgical techs, we’ve had to intermittently take some ORs and units offline…If we get a big December spike in elective care, I’m not sure we’ll have the staff to accommodate it.” Facing the triple threat of sky-high costs, sluggish demand, and a worsening payer environment, the ability to accommodate this demand will be critical to securing margins as providers move into 2023.

Banner Health will pause elective surgeries Jan. 1, the Phoenix-based system announced Dec. 30.

The health system is suspending nonurgent elective surgeries that can reasonably be postponed for 30 to 60 days without a negative impact on the patient’s health, according to TV station CBS 5.

Banner’s hospitals are facing a surge of COVID-19 patients. As of Dec. 29, the system was at 104 percent licensed bed capacity, Banner Chief Clinical Officer Marjorie Bessel, MD, said Dec. 30, according to TV station ABC 15. Some Banner hospitals have exceeded 120 percent licensed bed capacity.

Because of a backlog of patients, some Banner hospitals are diverting incoming ambulance transports.

“This diversion activity is an early indication that triage may soon be necessary if volumes continue to increase like they did this past week,” Dr. Bessel said, according to CBS 5. “What triage would look like, would be that we might, if we got to that point, be unable to care for everybody.”

Twenty-one Kaiser Permanente hospitals in Northern California are suspending elective, non-urgent procedures through Jan. 4 as they continue to face a surge in COVID-19 hospitalizations, according to The Mercury News.

The Oakland, Calif.-based system announced the suspension Dec. 26, days after Chairman and CEO Greg Adams said during a news conference, “We simply will not be able to keep up if the COVID surge continues to increase. We’re at or near capacity everywhere.”

California reported a record-high 20,059 current COVID-19 hospitalizations Dec. 27, a 13 percent increase from one week prior, according to The COVID Tracking Project.

Find a running list of other health systems that have adjusted their elective surgery timelines, organized by state, here.

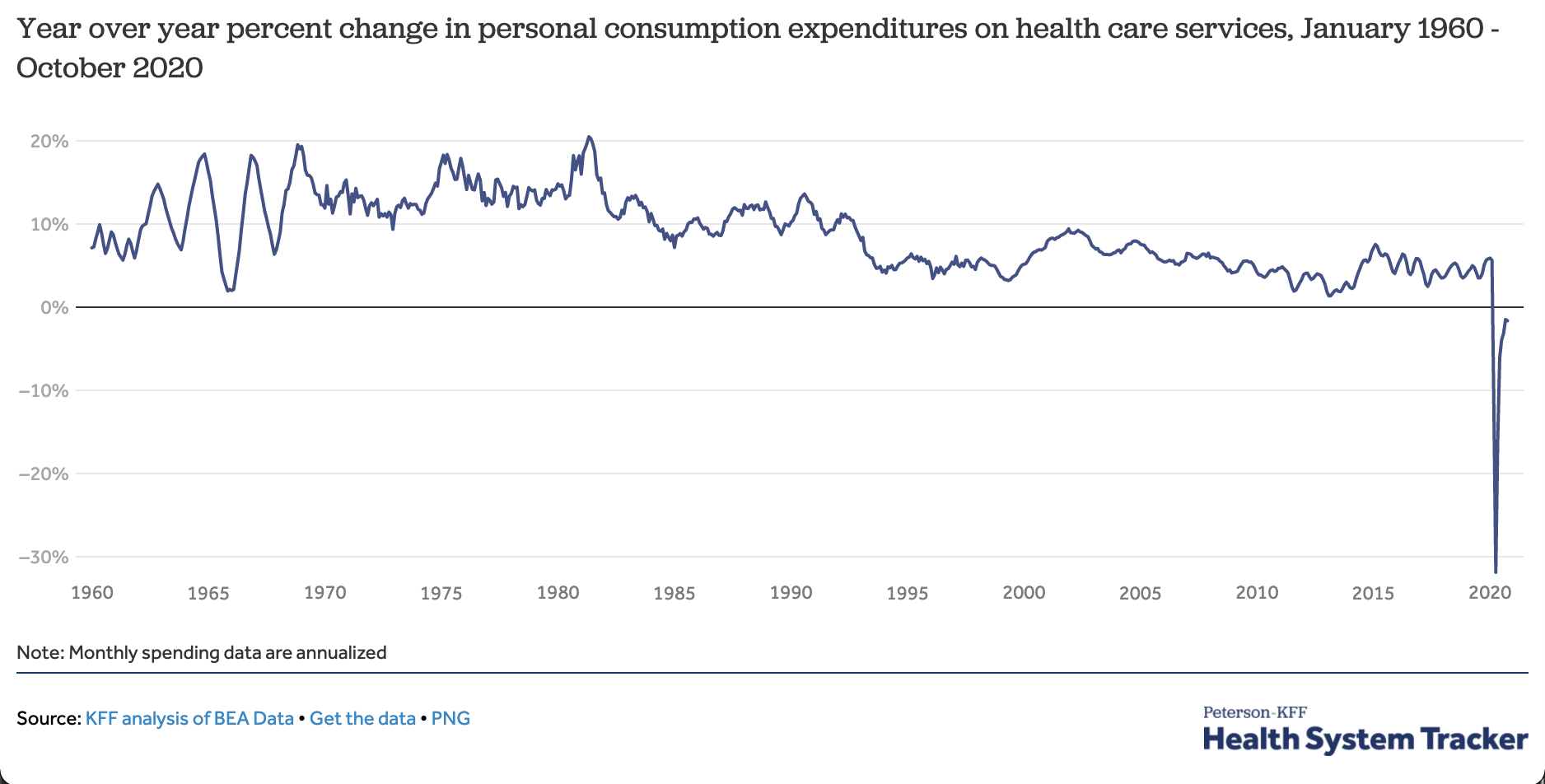

The coronavirus pandemic has caused national health care spending to go down this year — the first time that’s ever happened.

The big picture:Any big recession depresses the use of health services because people have less money to spend. But this pandemic has also directly attacked the health system, causing people to defer or skip care for fear of becoming infected.

By the numbers: Year-to-date spending on health services is down about 2% from last year. Health spending for the calendar year may end up lower than it was in 2019.

In April, when the pandemic forced many facilities to temporarily close, spending on health services had fallen an eye-popping 32% on an annualized basis.

The largest drop-offs were in outpatient care. Telehealth visits increased dramatically but did not make up all of the difference.

Context: This is the first time expenditures for patient care have fallen year-over-year since data became available in the 1960s.

What’s next: Spending and utilization have been recovering, but could fall again if the current spike in cases prompts either hospitals or patients to again hold off on elective care.

There has been a decline in cancer screenings and visits to manage chronic conditions, but it will take more research before we know precisely how this has affected outcomes.

Hospitals across the U.S. are beginning to suspend elective procedures to respond to an uptick in hospitalized COVID-19 patients.

Below is a breakdown of 66 hospitals postponing or canceling the procedures to free up space, ensure proper staffing or enough protective gear to care for COVID-19 patients:

1. Mercy Health Youngstown (Ohio) will indefinitely suspend elective procedures that require an inpatient admission starting Nov. 26, according to the Tribune Chronicle.

2. Prescot, Ariz.-based Yavapai Regional Medical Center, which recently joined Dignity Health, will limit elective procedures effective Nov. 26 to Dec. 4, according to The Daily Courier.

3. South Bend, Ind.-based Beacon Health System is suspending nonemergency surgeries to free up bed space and staff to care for a surge in COVID-19 cases, according to WSBT. The surgeries affected include those that require an inpatient stay.

4. Citing a spike in COVID-19 cases, Goshen (Ind.) Health is suspending nonurgent surgeries, according to WSBT.

5. Stormont Vail Health in Topeka, Kan., is rescheduling some elective surgeries that require overnight stays to free up bed space, according to local news station WIBW.

6. UW Medicine in Seattle will suspend nonemergency surgeries that require an inpatient hospital stay, effective Nov. 23 through Feb. 1.

7. Mercy Hospital South in St. Louis plans to delay some nonurgent procedures that require longer hospital stays amid a spike in COVID-19 hospitalizations, according to the St. Louis Post-Dispatch.

8. Metro Health-University of Michigan Health in Wyoming, Mich., has delayed some surgeries that require an inpatient stay, according to MiBiz.

9. Albuquerque, N.M.-based Presbyterian Healthcare Services is canceling nonurgent surgeries that require hospitalization, according to local news station KBOB. The health system said it will postpone those surgeries that can be delayed for six weeks or longer safely.

10. HSHS Sacred Heart Hospital in Eau Claire, Wis., is postponing electives on a case-by-case basis amid a surge in COVID-19 cases, according to The Leader-Telegram.

11. IU Health Methodist Hospital in Indianapolis has started to reduce the amount of elective procedures it will perform, while still trying to catch up on those that were postponed during the initial surge, according to MedPageToday.

12. Carson Tahoe Hospital in Carson City, Nev., has delayed non-time sensitive surgeries for a few weeks to free up space and staff to care for a surge in COVID-19 hospitalizations, according to local station News 4.

13. The 267-bed Mercy Health Muskegon (Mich.) has begun to delay elective surgeries as needed amid an influx of COVID-19 cases, according to MiBiz.

14. Buffalo, N.Y.-based Catholic Health will halt all inpatient elective surgeries that require an overnight stay for two weeks amid a COVID-19 hospitalization surge, according to Buffalo News. The healthcare system will start rescheduling procedures Nov. 21, and reevaluate if an extension is needed Dec. 5.

15. Chicago-based Northwestern Medicine will reduce the number of nonemergency surgeries it performs to help preserve bed capacity and staff to help care for a surge in COVID-19 cases, according to the Northwest Herald.

16. Morris (Ill.) Hospital and Healthcare Centers postponed some inpatient surgeries requiring overnight stays the week of Nov. 16 due to a bed shortage exacerbated by the rise in COVID-19 cases, according to NBC Chicago.

17. Memorial Community Hospital and Health System in Blair, Neb., is limiting elective surgeries requiring an overnight hospital stay for several weeks to preserve bed capacity and ensure proper staffing levels to care for the influx of COVID-19 cases, according to the Pilot-Tribune & Enterprise.

18. Spectrum Health in Grand Rapids, Mich., is deferring elective surgeries requiring an overnight hospital stay, according to Michigan Radio. The deferral rate is about 10 percent, according to the report.

19. Avera St. Mary’s Hospital in Pierre, S.D., is postponing nonemergency procedures so staff can care for the influx of COVID-19 cases and respond to emergent needs, according to DRGNews.

20. Salt Lake City-based Intermountain Healthcarewill postpone some surgeries that require an inpatient admission to free up beds, preserve supplies and free up providers amid a surge in COVID-19 hospitalizations. The hospital system will only delay those that can be safely postponed.

21. Froedtert Health in Wauwatosa, Wis., will delay non-urgent surgeries that require an inpatient admission post-surgery in an effort to free up staff and beds amid the coronavirus case surge in Wisconsin, according to local news stationTMJ4. The hospitals are located in Wauwatosa, Menomonee Falls and West Bend.

22. Memorial Hospital in Aurora, Neb., has suspended elective surgeries that take place at its Wortman Surgery Center to dedicate staff to inpatient and emergency care.

23. Minneapolis-based Allina Health is delaying some non-urgent procedures at three of its hospitals until at least Nov. 27, according to The Star Tribune. The delays will affect non-urgent procedures that require an overnight hospital stay.

24. Bloomington, Minn.-based HealthPartners has started postponing some total joint surgeries, including hip or knee replacements, at three Minnesota hospitals, according to The Twin Cities Business Journal. The affected hospitals are Methodist Hospital in St. Louis Park, Regions Hospital in St. Paul and Lakeview Hospital in Stillwater.

25. Southern Illinois Healthcare, a two-hospital system based in Carbondale, will reduce its elective surgery volume by about 50 percent as more people seek inpatient care for COVID-19, according to The Southern Illinoisan.The surgeries affected by the delay include those that require an overnight hospital stay.

26. University of Cincinnati Health activated surge operations Nov. 16, requiring a 50 percent reduction in elective inpatient surgeries and procedures across the health system, according to local news station WLWT.

27. Rochester, Minn.-based Mayo Clinic has started scaling back elective care to ensure it can care for patients with emergent needs and a high influx of COVID-19 patients, according to The Post Bulletin.

28. Citing a 1,500 percent increase in COVID-19 hospitalizations between Nov. 1 and Nov. 17, Lake Health in Concord Township, Ohio, is pausing elective surgeries that require an overnight stay, according to The News-Herald.The pause will continue through Nov. 20, but the system will reevaluate if the pause needs to be extended on a weekly basis.

29. Cook County Health, the public hospital system based in Chicago, is suspending elective surgeries requiring inpatient stays, according to WBEZ.The decision was made to ensure adequate staffing to care for an influx in COVID-19 cases.

30. Urbana, Ill.-based Carle Foundation Hospital has canceled some elective procedures that require an overnight hospital stay in an effort to free up beds and staff to care for COVID-19 patients, according to The News Gazette.

31. Elkhart (Ind.) General Hospital stopped all elective surgeries Nov. 17 after more than 200 patients were admitted to its 144-bed hospital, according to The New York Times. Of those patients 90 were being treated with COVID-19. The hospital also diverted ambulances during this time.

32. Advocate Aurora Health, with dual headquarters in Milwaukee and Downers Grove, Ill., has started reducing elective procedures by 50 percent at some of its facilities, according to a Nov. 16 media briefing. The health system said that more hospitals will look into the option to postpone elective procedures later the week of Nov. 16.

33. The University of Kansas Health System in Kansas City started postponing some elective surgeries to free up inpatient beds Nov. 12.

34. St. Luke’s Health System in Boise, Idaho, will stop scheduling certain elective surgeries and procedures through Dec. 25, according to a company news release. The temporary delay starts Nov. 16. St. Luke’s medical centers in Boise, Meridian, Magic Valley and Nampa will also cancel elective cases requiring an overnight stay scheduled for the week of Nov. 16, according to the news release.

35. Citing an increased demand for inpatient beds, Ascension Genesys Hospital in Grand Blanc, Mich., will not schedule any new inpatient elective surgeries until at least Nov. 30. The hospital said it has asked surgeons to “thoughtfully examine” already scheduled cases requiring extended recovery through Nov. 30.

36. SSM Health St. Mary’s Hospital in Madison began rescheduling nonemergent surgeries to free up intensive care unit bed space, according to local news station NBC 15.

37. Cedar Rapids, Iowa-based Mercy Medical Center will reduce elective surgery cases through Nov. 20. It also temporarily stopped scheduling new elective procedures.

38. Columbia Memorial Hospital in Astoria, Ore., will reduce some elective procedures due to an increase in COVID-19 cases, according to the Cannon Beach Gazette.

39. St. Louis-based BJC HealthCarewill postpone some elective surgery cases at all 15 of its hospitals and ambulatory care settings starting Nov. 16. The surgery postponement will last eight weeks. The announcement comes just one week after the health system started rescheduling nonemergency surgeries at four of its hospitals.

40. Citing a significant increase in COVID-19 hospitalizations, Cleveland Clinic said it will postpone some nonemergency surgeries. Cleveland Clinic said it will reschedule nonessential surgical cases that require an inpatient stay at its hospitals in Ohio through Nov. 20. It will reassess its scheduled surgical cases daily to determine if more cases need to be delayed.

41. Baxter County Regional Medical Center in Mountain Home, Ark., said Nov. 11 it will begin postponing nonemergency surgeries. The hospital will only defer procedures requiring an overnight hospital stay in order to free up beds for COVID-19 patients.

42. Portland, Ore.-based Legacy Healthwill reduce the number of elective procedures requiring an overnight hospital stay by 25 percent.

“We will monitor the situation and adjust as needed,” Trent Green, Legacy Health COO, wrote in an email to staff. “If the number of hospitalized patients continues to grow, we may cancel more surgeries. As hospital volumes lower, we will add back elective surgeries.”

43. Kaiser Permanente Northwest, which has hospitals in Oregon and southwest Washington state, is implementing a “scheduling pause” at some of its Oregon medical centers through Dec. 31.

44. Portland-based Oregon Health & Sciences Universityis implementing voluntary elective surgery deferrals. The hospital system will evaluate surgical cases daily to ensure it has the appropriate capacity to care for all patients.

45. Aurora, Colo.-based UCHealthbegan postponing some nonemergency surgeries due to a surge in COVID-19 hospitalizations. The health system will defer nonemergent surgeries that require inpatient admission. The health system began postponing some of those surgeries the week of Nov. 2.

46. As of Nov. 11, Grand Rapids, Mich.-based Spectrum Health has 14 hospitals nearing capacity amid a surge of COVID-19 cases. As a result it is starting to delay inpatient surgeries that require overnight stays.

47. Community Memorial Hospital in Cloquet, Minn., has halted some elective surgeries to free up beds amid a surge in hospitalizations.

48. Sarah Bush Lincoln, a 145-bed hospital in Mattoon, Ill., is postponing most inpatient elective surgeries due to bed capacity constraints. The hospital said it will make the decision on whether to postpone a surgery on a case-by-case basis.

49. Memorial Health System in Springfield, Ill., will begin delaying some nonurgent surgeries Nov. 16.

50. Evanston, Ill.-based NorthShore University HealthSystem, has started evaluating elective surgeries on a case-by-case basis and delaying those that can be postponed safely.

51. UnityPoint Health Meriter in Madison, Wis., is rescheduling nonemergent surgeries that require overnight stays to save beds for COVID-19 patients. The hospital has seen a “significant” uptick in COVID-19-related hospitalizations, with about one-third of UnityPoint Meriter’s beds occupied by patients with the virus.

52. St. Luke’s, a two-hospital system in Duluth, Minn., is postponing nonemergency surgeries amid a surge in COVID-19 patients. The health system said it will only delay surgeries that require an overnight stay and can be rescheduled safely.

53. Omaha, Neb.-based Methodist Health Systembegan postponing elective surgeries at its flagship hospital Oct. 29, president and CEO Steve Goeser told Becker’s. It is reviewing the surgery schedule to determine which ones can be postponed safely.

54. Omaha-based Nebraska Medicineis limiting nonurgent procedures due to a rise in COVID-19 hospitalizations. The health system said that it has enough beds, but high-level intensive care unit providers “aren’t an infinite resource.”

55. CHI Health in Omaha, Neb., said that some nonurgent procedures will be postponed amid the COVID-19 resurgence. By postponing some surgeries, CHI Health said it aims to free up beds and capacity for patients.

56. Sanford Health, a 46-hospital system based in Sioux Falls, S.D., will begin rescheduling some nonemergency inpatient surgeries that require an overnight hospital stay due to an influx of COVID-19 patients.

57. Bryan Health, based in Lincoln, Neb., will begin scaling back elective surgeries requiring an overnight hospitalization due to a rise in COVID-19 cases. The system said it will decrease elective surgeries requiring overnight stay by 10 percent for the week of Nov. 2 to ensure it is able to care for COVID-19 patients and perform essential surgeries.

58. Mayo Clinic Health Systembegan deferring elective procedures at its hospitals in Northwest Wisconsin Oct. 31 amid an escalation of COVID-19 cases. The health system did not say when elective procedures will restart. The Mayo Clinic Health System has clinics, hospitals and other facilities across Iowa, Minnesota and Wisconsin.

59. Madison, Wis.-based UW Health is postponing a small number of elective procedures to free up bed capacity to care for COVID-19 patients, according to WKOW. Jeff Pothof, MD, UW Health’s chief quality officer, said that patients may be asked to push back a non-emergency procedure by about a week.

60. Saint Vincent Hospital in Erie, Pa., will postpone a small number of elective procedures after some patients and caregivers tested positive for COVID-19. The hospital did not specify the number of patients and staff who tested positive.

61. Johnson City, Tenn.-based Ballad Healthwill begin deferring elective procedures at three of its Tennessee hospitals due to a spike in COVID-19 hospitalizations. On Oct. 26, Ballad began rescheduling up to 25 percent of elective services at Holston Valley Medical Center in Kingsport, Tenn. Procedures are also expected to begin being deferred at Bristol Regional Medical Center and Johnson City Medical Center.

62. Maury Regional Medical Center in Columbia, Tenn., will suspend elective procedures requiring an overnight stay for two weeks. Hospital leadership will re-evaluate the feasibility of elective surgeries by Nov. 9.

63. Cookeville (Tenn.) Regional Medical Center said Oct. 26 it suspended elective procedures requiring an overnight stay after it was caring for a record high of 71 COVID-19 patients, according to WKRN.

64. Salt Lake City-based University of Utah Hospitalcanceled elective procedures after its intensive care unit hit capacity on Oct. 16. The hospital said it needed to postpone the elective care to allocate staff to care for critically ill patients.

65. Sanford Health in Sioux Falls, S.D., will stop scheduling new elective surgery cases requiring an overnight stay, according to system CMO Mike Wilde, MD. New elective cases requiring an overnight stay were not scheduled for Oct. 19-23, but previously scheduled elective surgeries were performed.

66. Billings (Mont.) Clinic began evaluating each surgical case for urgency in late September. It is postponing those it says can wait, according to The Wall Street Journal.

In talking to our health system members from across the country in the past few weeks, we’ve heard that the COVID surge is happening everywhere. Nearly everyone we’ve talked to has told us that their inpatient census of COVID patients is as high or higher now than during the initial wave of the pandemic in March and April. And nearly everyone is expecting it to get much worse over the next few weeks, as hospitalizations increase in the wake of the explosion of cases we’re seeing now.

But there is something striking in our conversations in comparison to eight months ago: no one seems to be panicking. Crisis management processes that were developed and honed early in the pandemic are proving very helpful now. Normal patient care services are continuing despite the uptick in COVID volume, and protections are in place to keep the care environment segregated and COVID-free as possible.

While dozens of health systems, many in the hardest hit states in the Midwest and Great Plains, have announced plans to curtail elective care during this third wave, the decisions are based on individual hospital capacity and staffing, instead of being mandated by states. Having largely worked through the “COVID backlog” across the summer and early fall, system leaders want to avoid canceling surgeries again, and few are expecting state governments to force them to.

Many of our members have drawn up plans for selective cancellations depending on capacity, but we’re not likely to see sweeping shutdowns again—unless the workforce becomes so overstretched that it impacts operations.

That’s good news, and will likely lead to less interrupted patient care. And it’s good news for hospitals’ and doctors’ economic survival, as many would not be able to absorb the body blow of another widespread shutdown. Fingers crossed.

The financial challenges caused by the COVID-19 pandemic have forced hundreds of hospitals across the nation to furlough, lay off or reduce pay for workers, and others have had to scale back services or close.

Lower patient volumes, canceled elective procedures and higher expenses tied to the pandemic have created a cash crunch for hospitals. U.S. hospitals are estimated to lose more than $323 billion this year, according to a report from the American Hospital Association. The total includes $120.5 billion in financial losses the AHA predicts hospitals will see from July to December.

Hospitals are taking a number of steps to offset financial damage. Executives, clinicians and other staff are taking pay cuts, capital projects are being put on hold, and some employees are losing their jobs. More than 260 hospitals and health systems furloughed workers this year and dozens of others have implemented layoffs.

Below are 11 hospitals and health systems that announced layoffs since Sept. 1, most of which were attributed to financial strain caused by the pandemic.

1. NorthBay Healthcare, a nonprofit health system based in Fairfield, Calif., is laying off 31 of its 2,863 employees as part of its pandemic recovery plan, the system announced Nov. 2.

2. Minneapolis-based Children’s Minnesota is laying off 150 employees, or about 3 percent of its workforce. Children’s Minnesota cited several reasons for the layoffs, including the financial hit from the COVID-19 pandemic. Affected employees will end their employment either Dec. 31 or March 31.

3. Brattleboro Retreat, a psychiatric and addiction treatment hospital in Vermont, notified 85 employees in late October that they would be laid off within 60 days.

4. Citing a need to offset financial losses, Minneapolis-basedM Health Fairview said it plans to downsize its hospital and clinic operations. As a result of the changes, 900 employees, about 3 percent of its 34,000-person workforce, will be laid off.

5. Lake Charles (La.) Memorial Health Systemlaid off 205 workers, or about 8 percent of its workforce, as a result of damage sustained from Hurricane Laura. The health system laid off employees at Moss Memorial Health Clinic and the Archer Institute, two facilities in Lake Charles that sustained damage from the hurricane.

6. Burlington, Mass.-based Wellforce laid off 232 employees as a result of operating losses linked to the COVID-19 pandemic. The health system, comprising Tufts Medical Center, Lowell General Hospital and MelroseWakefield Healthcare,experienced a drastic drop in patient volume earlier this year due to the suspension of outpatient visits and elective surgeries. In the nine months ended June 30, the health system reported a $32.2 million operating loss.

7. Baptist Health Floyd in New Albany, Ind., part of Louisville, Ky.-based Baptist Health, eliminated 36 positions. The hospital said the cuts, which primarily affected administrative and nonclinical roles, are due to restructuring that is “necessary to meet financial challenges compounded by COVID-19.”

8. Cincinnati-based UC Health laid off about 100 employees. The job cuts affected both clinical and non-clinical staff. A spokesperson for the health system said no physicians were laid off.

9. Mercy Iowa City(Iowa) announced in September that it will lay off 29 employees to address financial strain tied to the COVID-19 pandemic.

10. Springfield, Ill.-based Memorial Health Systemlaid off 143 employees, or about 1.5 percent of the five-hospital system’s workforce. The health system cited financial pressures tied to the pandemic as the reason for the layoffs.

11. Watertown, N.Y.-based Samaritan Healthannounced Sept. 8 that it laid off 51 employees and will make other cost-cutting moves to offset financial stress tied to the COVID-19 pandemic.