Cartoon – Staffing Today

https://www.axios.com/2023/05/31/great-resignation-quitting-boom

A phenomenon that defined the pandemic-era labor market is over: the Great Resignation — workers furiously quitting for new, likely higher paying jobs — is a thing of the past.

Why it matters:

The historic surge of quitters was a symptom of an on-fire labor market, where demand for workers far outstripped supply of them.

By the numbers:

The quits rate fell to 2.4% in April, according to the Job Openings and Labor Turnover Survey, released this morning.

What they’re saying:

“We are pretty much back to a strong, robust labor market, but one that is no longer overheating,” says Julia Pollak, an economist at ZipRecruiter.

Flashback:

At the height of the Great Resignation, the overall quits rate most recently peaked at 3% in April 2022, when there were roughly 4.5 million quits in a single month.

The bottom line:

Americans who did job hop over the past few years have seen heftier pay gains. But that phenomenon, too, is fading — another sign of some heat coming off the labor market.

Contrary to widespread reports of staffing shortages, healthcare employment reached pre-pandemic levels with the addition of 44,200 jobs in February, according to a recent report from Altarum.

A recent survey of hospital CEOs found that healthcare staffing was their top concern. Nurses nationwide have reported unsafe staffing levels, leading health systems to restructure and lawmakers to consider safe-staffing laws.

Yet, healthcare currently has 1.3 percent more jobs than it did in February 2020, according to the monthly Health Sector Economic Indicators brief from Altarum. The nonprofit, healthcare-focused research and consulting organization analyzes available data on spending, prices, employment and utilization to craft the monthly report.

The data holds that this isn’t a new occurence. The sector has been adding — on average — 49,100 jobs per month for the past year, according to the brief. In February, hospitals led that growth, tapping 19,400 workers. Nursing and residential care facilities added 13,700 jobs, and ambulatory care settings added 11,100.

However, as healthcare employment rises, its wage growth continues to decline and now lags behind economywide growth. Healthcare wage growth has been declining since mid-2022; in January, pay grew 4.2 percent year over year, while total private sector wage growth grew 4.4 percent.

This statistic also defies industry narratives, as recent labor negotiations between unions and health systems have scored big raises for workers and clinicians.

https://mailchi.mp/d62b14db92fb/the-weekly-gist-february-10-2023?e=d1e747d2d8

Monday’s walkout of tens of thousands of nurses and ambulance staff was the largest in the NHS’s 75-year history.

Labor demonstrations have been ongoing across the past few months, as workers demand higher pay and better working conditions amid rampant national inflation and increased workloads.

Specific demands vary by union and nation within the United Kingdom. Welsh nurses called off their strike this week to review a proposal from Wales’ Labour Party-run government, while the Royal College of Nurses, the UK’s largest nursing union, has countered a nominal 5 percent pay increase proposal with demands for a five percent pay raise on top of inflation, which topped 10 percent in Britain in December.

The Gist: A glance at our neighbors across the pond shows that the US healthcare system is not the only one currently experiencing a labor crisis.

The UK’s nationalized system has also failed to shield its workers from the combined impact of COVID burnout and inflation. But the NHS, as the UK’s largest employer and perennial object of political maneuvering, is more susceptible to organized labor actions.

In contrast, American healthcare unions, which only covered 17 percent of the country’s nurses in 2021, must negotiate with local employers, whose responses to their demands vary.

While this may enhance the bargaining power of US health system leaders, it also heightens the risk that we will fail to adequately secure our nursing workforce, a key national resource already in short supply, for the longer term.

https://mailchi.mp/a44243cd0759/the-weekly-gist-february-3-2023?e=d1e747d2d8

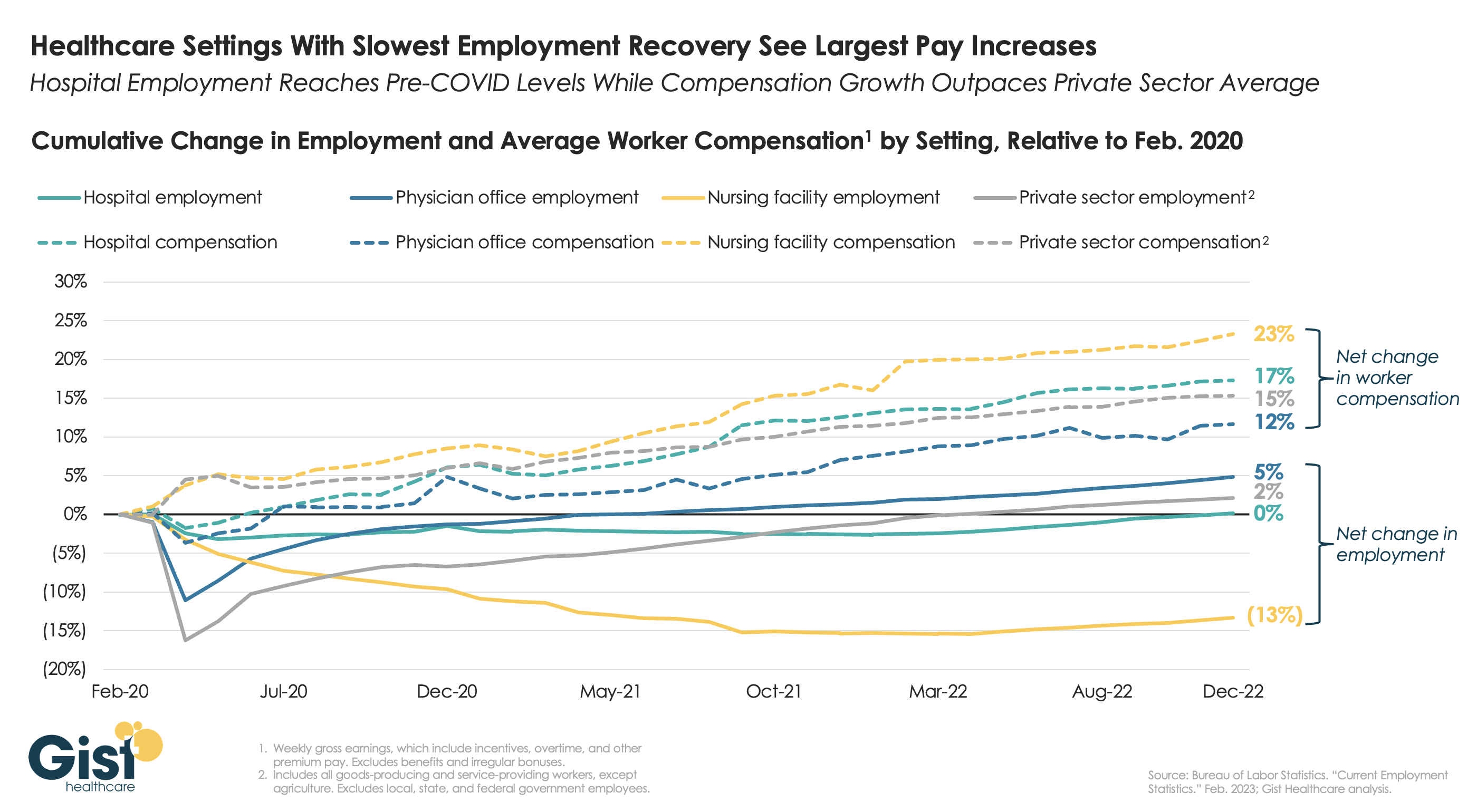

The healthcare sector has been navigating an intransigent staffing crisis since the widespread layoffs during the first few months of COVID. The graphic above uses Bureau of Labor Statistics data to illustrate the impact of this labor shock on both total employment and employee compensation.

Across key healthcare settings, workplaces with the slowest recovery of total workers have seen the largest increases in employee earnings. Hospital employment largely tracked with the rest of the private sector; however, hospitals raised employee compensation by two percent more than the private sector, while recovering two percent fewer jobs.

It is important to note that the relationship between employment levels and employee compensation is not causal, as evidenced by the ongoing labor shortages in nursing facilities, despite boosting average pay over 20 percent. Rather, the data suggest that, for as long as the tight labor market persists, pay raises alone are not sufficient to recruit and retain talent. Plus, while inflation may be abating, it has still outpaced earnings growth since December 2021.

Given that many healthcare workers saw pay bumps early in the pandemic, some are left still feeling underpaid, even if their compensation over the past three years has more than kept pace with inflation.

https://mailchi.mp/59374d8d7306/the-weekly-gist-january-13-2023?e=d1e747d2d8

Published this week in the New England Journal of Medicine, this concerning study found that seven percent of all inpatient hospital admissions feature at least one preventable adverse event, and that nearly a quarter of all adverse events are preventable, with drug administration errors the most frequent. While the complexities behind studying adverse events make it difficult to measure progress over time, the authors assert that these episodes are still far too common, and advocate for establishing standard approaches to measure the frequency of adverse events more reliably.

The Gist: Health systems had been making at least some progress in their decades-long effort to reduce adverse events before COVID turned the industry upside down, drawing clinical leaders’ focus to the crisis and upending industry benchmarks.

Today’s short-staffed, traveler-dependent labor force presents yet another challenge to hospitals aiming to achieve quality benchmarks. COVID has also accelerated the outpatient shift, heightening the importance of tracking quality metrics in non-hospital settings.

As more complex procedures are performed in ambulatory surgery centers, and more hospital care is administered at home, there’s also a concern that hospital-based quality measures are not telling the whole story on the state of patient safety.

A rethinking of quality metrics and processes to measure and prevent adverse events across the continuum is long overdue.

https://mailchi.mp/59374d8d7306/the-weekly-gist-january-13-2023?e=d1e747d2d8

In our decades of working in healthcare, we’ve never seen a time when payer-provider negotiations have been more tense. Emboldened insurers, having seen strong growth during the pandemic, are entering contract negotiations with an aggressive posture.

“They weren’t even willing to discuss a rate increase,” one CFO shared as he described his health system’s recent negotiations with a large national insurer. “The plan’s opening salvo was a fifteen percent rate cut!”

Health systems are feeling lucky to get even a two or three percent rate bump, well short of the historical average of seven percent—and far short of what would be needed to account for skyrocketing labor, supply, and drug costs. According to executives we work with, efforts to describe the current labor crisis and resulting cost impacts with payers are largely falling on deaf ears.

This scenario is playing out in markets across the country, with more insurers and health systems announcing that they are “terming” their contract, publicly stating they will cut ties should the stalemate in negotiations persist.

Speaking off the record, a system executive shared how this played out for them. With negotiations at an impasse, a large insurer began the process of notifying beneficiaries that the system would soon be out-of-network, and patients would be reassigned to new primary care providers. The health plan assumed that the other systems in the market would see this as a growth opportunity—and was shocked when they discovered that other providers were already operating at capacity, unable to accommodate additional patients from the “terminated” system.

Mounting concerns about access brought the plan back to the table. Even in the best of times, a major insurer cutting ties with a health system is extremely disruptive for consumers, who must shift their care to new providers or pay out-of-network rates. But given current capacity challenges in hospitals nationwide, major network disruptions can be even more dire for patients—and may force payers and providers to walk back from the brink of contract termination.

https://mailchi.mp/ad2d38fe8ab3/the-weekly-gist-january-6-2023?e=d1e747d2d8

At a recent health system retreat, the CFO shared data describing a trend we’ve observed at a number of systems: for the past few months, emergency department (ED) volumes have been up, but the percentage of patients admitted through the ED is precipitously down.

The CFO walked to through a run of data to diagnose possible causes of this “uncoupling” of ED visits and inpatient admissions. Overall, the severity of patients coming to the ED was higher compared to 2019, so it didn’t appear that the ED was being flooded with low-level cases that didn’t merit admission. Apart from the recent spike in respiratory illness brought on by the “tripledemic” of flu, COVID and RSV, there wasn’t a noteworthy change in case mix, or the types of patients and conditions being evaluated in the emergency room. (Fewer COVID patients were admitted compared to 2021, but that wasn’t enough to account for the decline.) The physicians staffing the ED hadn’t changed, so a shift in practice patterns was also unlikely.

A physician leader attending the retreat spoke up from the audience: “I can diagnose this for you. I work in the ED, and the problem is we can’t move them. Patients are sitting in the ED, in hallways, in observation, sometimes for days, because we can’t get a bed on the floor. The whole time we are treating them, and many of them get better, and we’re able to discharge them before a bed frees up.”

With nursing shortages and other staffing challenges, many hospitals have been unable to run at full capacity even if the demand for beds is there. So total admissions may be down, even if the hospital feels like it’s bursting at the seams.

The current staffing crisis not only presents a business challenge, but also adversely impacts patient experience, and makes it more difficult to deliver the highest quality care. A good reminder of the complexity of hospital operations, where strain in one part of the system will quickly impact the performance of other parts of the care delivery continuum.

The majority of hospitals are predicted to have negative margins in 2022, marking the worst year financially for hospitals since the beginning of the Covid-19 pandemic.

In Part 1 of Radio Advisory’s Hospital of the Future series, host Rachel (Rae) Woods invites Advisory Board experts Monica Westhead, Colin Gelbaugh, and Aaron Mauck to discuss why factors like workforce shortages, post-acute financial instability, and growing competition are contributing to this troubling financial landscape and how hospitals are tackling these problems.

Links:

As we emerge from the global pandemic, health care is restructuring. What decisions should you be making, and what do you need to know to make them? Explore the state of the health care industry and its outlook for next year by visiting advisory.com/HealthCare2023.

https://mailchi.mp/e44630c5c8c0/the-weekly-gist-december-16-2022?e=d1e747d2d8

It’s been a difficult year for the hospital workforce, both here and around the world, as the effects of the pandemic, the economy, and the legacy of lean staffing models have combined to drive up vacancy rates and threaten the sustainability of hospital operations.

Everywhere we’ve gone in the past six months, workforce issues have overshadowed every other topic: how can hospitals attract and retain staff given the environment, how can they stabilize finances in the face of 15-20 percent increases in labor costs, how can they safeguard patient care with intense turbulence in the clinical workforce?

This week we heard yet another wrinkle to this problem, one that had not occurred to us but in retrospect is obvious. A system CFO was lamenting the fact that even with big salary increases, the hospital workforce remains unstable. “It’s like we’re not even getting credit for raising base salary 15 percent across the board and giving big retention bonuses.”

As to why—it’s a timing issue. Her system, like many, delivered pay raises back in the late winter and early spring, when staff were still recovering from the Omicron surge and the urgency of reducing reliance on expensive agency labor became clear. But economy-wide inflation had only then begun to spike, and has since continued to be stuck at high levels.

Staff don’t view the earlier salary increases as a response to inflation, but as predating it—and they’re asking for still more, to offset rising prices for food, transportation and housing. “I wish we’d waited to give the pay bump,” the CFO told us. “Even though our wage increases have outpaced inflation this year, the timing of events didn’t help us at all.”

With the hospitals operating near capacity, and a severe flu season impacting both patient volumes and staff availability, her sense is that the system is back to square one on staffing—and more difficult financial decisions lie ahead.