Contrary to widespread reports of staffing shortages, healthcare employment reached pre-pandemic levels with the addition of 44,200 jobs in February, according to a recent report from Altarum.

A recent survey of hospital CEOs found that healthcare staffing was their top concern. Nurses nationwide have reported unsafe staffing levels, leading health systems to restructure and lawmakers to consider safe-staffing laws.

Yet, healthcare currently has 1.3 percent more jobs than it did in February 2020, according to the monthly Health Sector Economic Indicators brief from Altarum. The nonprofit, healthcare-focused research and consulting organization analyzes available data on spending, prices, employment and utilization to craft the monthly report.

The data holds that this isn’t a new occurence. The sector has been adding — on average — 49,100 jobs per month for the past year, according to the brief. In February, hospitals led that growth, tapping 19,400 workers. Nursing and residential care facilities added 13,700 jobs, and ambulatory care settings added 11,100.

However, as healthcare employment rises, its wage growth continues to decline and now lags behind economywide growth. Healthcare wage growth has been declining since mid-2022; in January, pay grew 4.2 percent year over year, while total private sector wage growth grew 4.4 percent.

This statistic also defies industry narratives, as recent labor negotiations between unions and health systems have scored big raises for workers and clinicians.

Monday’s walkout of tens of thousands of nurses and ambulance staff was the largest in the NHS’s 75-year history.

Labor demonstrations have been ongoing across the past few months, as workers demand higher pay and better working conditions amid rampant national inflation and increased workloads.

Specific demands vary by union and nation within the United Kingdom. Welsh nurses called off their strike this week to review a proposal from Wales’ Labour Party-run government, while the Royal College of Nurses, the UK’s largest nursing union, has countered a nominal 5 percent pay increase proposal with demands for a five percent pay raise on top of inflation, which topped 10 percent in Britain in December.

The Gist: A glance at our neighbors across the pond shows that the US healthcare system is not the only one currently experiencing a labor crisis.

The UK’s nationalized system has also failed to shield its workers from the combined impact of COVID burnout and inflation. But the NHS, as the UK’s largest employer and perennial object of political maneuvering, is more susceptible to organized labor actions.

In contrast, American healthcare unions, which only covered 17 percent of the country’s nurses in 2021, must negotiate with local employers, whose responses to their demands vary.

While this may enhance the bargaining power of US health system leaders, it also heightensthe risk that we will fail to adequately secure our nursing workforce, a key national resource already in short supply, for the longer term.

In our decades of working in healthcare, we’ve never seen a time when payer-provider negotiations have been more tense. Emboldened insurers, having seen strong growth during the pandemic, are entering contract negotiations with an aggressive posture.

“They weren’t even willing to discuss a rate increase,” one CFO shared as he described his health system’s recent negotiations with a large national insurer. “The plan’s opening salvo was a fifteen percent rate cut!”

Health systems are feeling lucky to get even a two or three percent rate bump, well short of the historical average of seven percent—and far short of what would be needed to account for skyrocketing labor, supply, and drug costs. According to executives we work with, efforts to describe the current labor crisis and resulting cost impacts with payers are largely falling on deaf ears.

This scenario is playing out in markets across the country, with more insurers and health systems announcing that they are “terming” their contract, publicly stating they will cut ties should the stalemate in negotiations persist.

Speaking off the record, a system executive shared how this played out for them. With negotiations at an impasse, a large insurer began the process of notifying beneficiaries that the system would soon be out-of-network, and patients would be reassigned to new primary care providers. The health plan assumed that the other systems in the market would see this as a growth opportunity—and was shocked when they discovered that other providers were already operating at capacity, unable to accommodate additional patients from the “terminated” system.

Mounting concerns about access brought the plan back to the table. Even in the best of times, a major insurer cutting ties with a health system is extremely disruptive for consumers, who must shift their care to new providers or pay out-of-network rates. But given current capacity challenges in hospitals nationwide, major network disruptions can be even more dire for patients—and may force payers and providers to walk back from the brink of contract termination.

At a recent health system retreat, the CFO shared data describing a trend we’ve observed at a number of systems: for the past few months, emergency department (ED) volumes have been up, but the percentage of patients admitted through the ED is precipitously down.

The CFO walked to through a run of data to diagnose possible causes of this “uncoupling” of ED visits and inpatient admissions. Overall, the severity of patients coming to the ED was higher compared to 2019, so it didn’t appear that the ED was being flooded with low-level cases that didn’t merit admission. Apart from the recent spike in respiratory illness brought on by the “tripledemic” of flu, COVID and RSV, there wasn’t a noteworthy change in case mix, or the types of patients and conditions being evaluated in the emergency room. (Fewer COVID patients were admitted compared to 2021, but that wasn’t enough to account for the decline.) The physicians staffing the ED hadn’t changed, so a shift in practice patterns was also unlikely.

A physician leader attending the retreat spoke up from the audience: “I can diagnose this for you. I work in the ED, and the problem is we can’t move them. Patients are sitting in the ED, in hallways, in observation, sometimes for days, because we can’t get a bed on the floor. The whole time we are treating them, and many of them get better, and we’re able to discharge them before a bed frees up.”

With nursing shortages and other staffing challenges, many hospitals have been unable to run at full capacity even if the demand for beds is there. So total admissions may be down, even if the hospital feels like it’s bursting at the seams.

The current staffing crisis not only presents a business challenge, but also adversely impacts patient experience, and makes it more difficult to deliver the highest quality care. A good reminder of the complexity of hospital operations, where strain in one part of the system will quickly impact the performance of other parts of the care delivery continuum.

The majority of hospitals are predicted to have negative margins in 2022, marking the worst year financially for hospitals since the beginning of the Covid-19 pandemic.

In Part 1 of Radio Advisory’s Hospital of the Future series, host Rachel (Rae) Woods invites Advisory Board experts Monica Westhead, Colin Gelbaugh, and Aaron Mauck to discuss why factors like workforce shortages, post-acute financial instability, and growing competition are contributing to this troubling financial landscape and how hospitals are tackling these problems.

As we emerge from the global pandemic, health care is restructuring. What decisions should you be making, and what do you need to know to make them? Explore the state of the health care industry and its outlook for next year by visiting advisory.com/HealthCare2023.

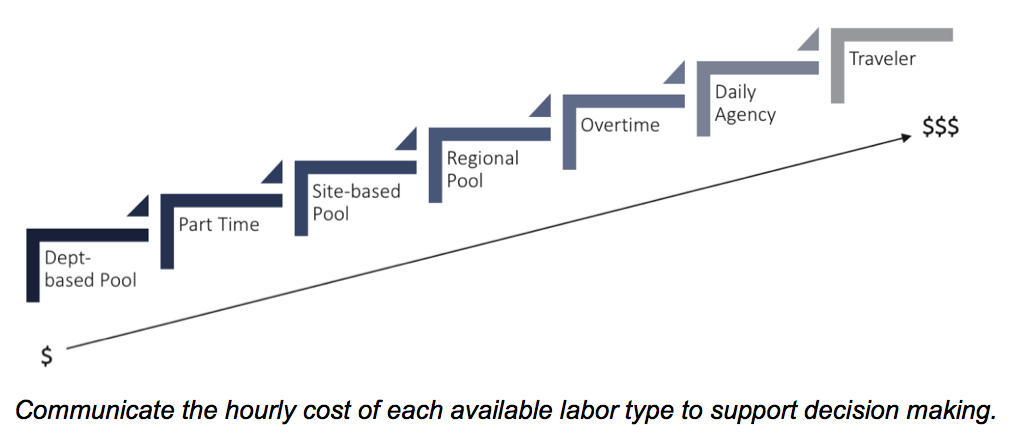

Many hospitals and health systems aim to recruit and retain permanent staff to replace contract labor positions, which have seen wages skyrocket because of staff shortages during the COVID-19 pandemic.

Hospitals across the country have relied on contract labor and temporary staffing agencies to support their clinical teams when many burned-out providers are exiting healthcare. An October survey conducted by Bain & Company found that 25 percent of physicians, advanced practice providers and nurses are considering changing careers. Eight-nine percent of the providers thinking about leaving the profession cited burnout as the driving force.

Staffing shortages are driving labor costs to an unsustainable level for hospitals operating on razor-thin margins and reducing temporary staffing costs is top of the agenda for many financial executives looking to reduce expenses in the coming quarters.

Here are 22 numbers that demonstrate the cost of contact labor for hospitals, according to reports from Kaufman Hall, Definitive Healthcare, Vaya Workforce and big hospital operators:

1. The demand for contract labor increased500 percent in fall 2021 compared with 2019, according to healthcare staffing services company Vaya Workforce. While demand has since decreased, it is still nearly triple pre-pandemic levels and is projected to remain as high as 20 percent above the 2019 baseline.

2. In 2020, the average amount hospitals spent on contract labor was $4.6 million, more than double the average expense of $2.2 million in 2011, according to a report from Definitive Healthcare, a data and analytics company.

3. Rochester, Minn.-based Mayo Clinic Hospital, Saint Mary’s Campus spent $286.8 million on contract labor in 2020, the most of any hospital in the country that year, according to Definitive Healthcare’s analysis of about 3,100 U.S. hospitals

4. From 2019 to 2022, the hourly wage rate for contract nurses increased106 percent, according to Kaufman Hall. Contract nurses are earning an average of $132an hour in 2022 versus $64an hour in 2019. At the height of the pandemic, some travel nurses earned up to $300 an hour, with rates as high as these placing immense pressure on hospital balance sheets.

5. The rise in contract labor from 2019 through March of 2022 led to a 37 percent increase in labor expenses per patient, equating to between $4,009 and $5,494 per adjusted discharge.

6. Hospitals with 25 beds or fewer spent about $460,000 on contract labor in 2020 compared to hospitals with more than 250 beds that spent almost $11 million on average, according to Definitive Healthcare.

7. Hospitals in the western U.S. have the highest contract labor expenses, with an average of $9.6 million reported in 2020. Large cities, high cost of living and high salary rates in the region contribute to this high average.

8. Labor costs were one of the core reasons Franklin, Tenn.-based Community Health Systems reported a net loss of $42 million in the third quarter, but CFO Kevin Hammons said he expects to see a 40 percent to 50 percent reduction in contract labor costs next year compared with 2022.

9. Nashville, Tenn.-based HCA Healthcare reported a 19 percent decrease in contract labor costs in the third quarter compared to the second quarter, allowing the system to absorb much of the market-based wage adjustment costs for its employee workforce, CFO Bill Rutherford said during an Oct. 21 earnings call.

10. According to Kaufman Hall’s “2022 State of Healthcare Performance Improvement” report, published Oct. 18, 46 percent of hospital and health system leaders identify labor costs as the greatest opportunity for cost reductions. This was significantly up from the 17 percent of respondents who noted labor costs as their greatest opportunity to cut costs last year.

11. There are some hopeful signs that the use of contract labor has stabilized and is steadily falling, according to Kaufman Hall: 44 percent of hospitals in its survey reported that their utilization of contract labor is declining while 29 percent said that it is holding steady.

Early into flu season, nationwide flu activity is ten times higher than at the same point last year. Meanwhile, cases of respiratory syncytial virus (RSV), a virus most severe in young children and the elderly, have tripled in the past two months, with some children’s hospitals reporting “unprecedented” admissions for the virus. And most experts expect at least some winter COVID surge, possibly involving several different variants. The combined threat of these viruses circulating together has been labeled a potential “tripledemic.”

The Gist: Across the past two winters, the widespread adoption of COVID prevention measures, including masking and social distancing, kept the spread of other viruses at bay. But with return to normal life for most Americans, other viruses have returned to circulation—and with a vengeance, as population immunity toward flu and RSV has weakened.

While it’s hard to predict when and where local surges will occur, hospitals struggling with staffing shortages may be forced to hire more contract labor to care for an influx of patients—making this a potentially challenging winter for already stretched facilities.

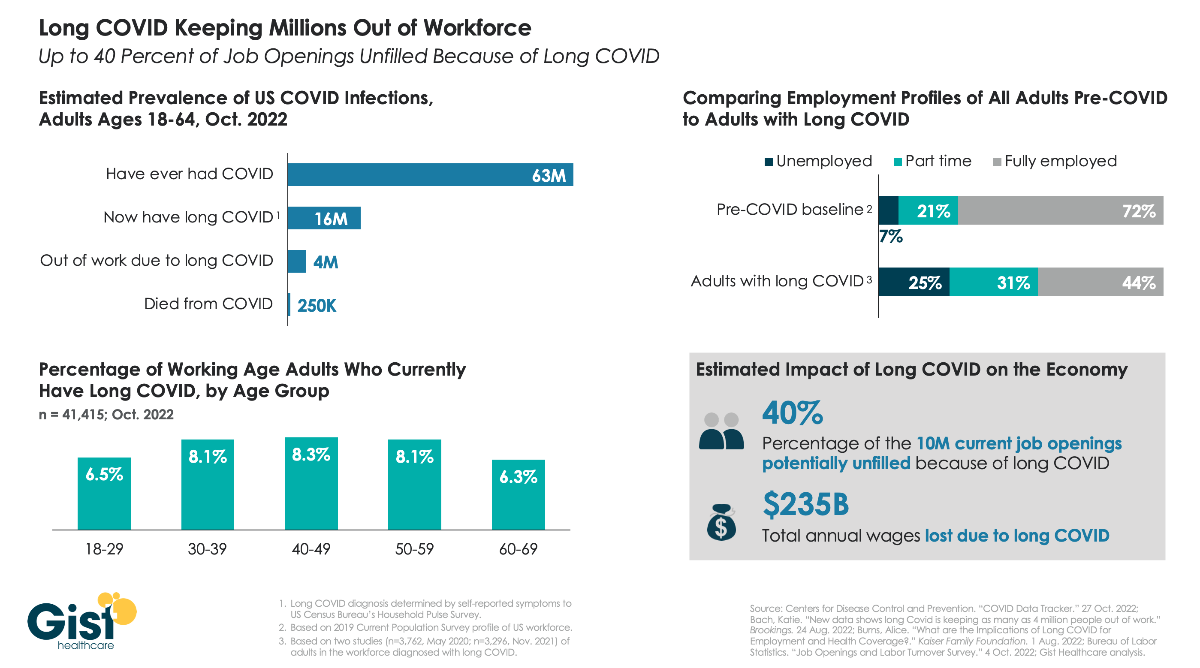

As the nation continues to grapple with the fallout from COVID, one of the greatest unknowns is “long COVID”, the broad range of health problems experienced by a significant number of individuals after contracting the virus. The Centers for Disease Control and Prevention defines long COVID as any post-COVID condition lasting three months or longer.

In the graphic above, we aim to quantify the prevalence of long COVID and its ongoing impact on the US workforce. While estimates for thesenumbers vary, data compiled by Brookings show that COVID infections in roughly one in four working age adults have resulted in long COVID, and up to one in four individuals with long COVID are unable to work due to their lingering health problems. Long COVID is also more prevalent in middle-aged adults, who are often at the peak of their working years. Dealing with symptoms like chronic fatigue and brain fog, long COVID patients are more likely to be unemployed or working reduced hours, compared to a pre-COVID baseline of the general adult population.

While it’s difficult to assess the precise impact on the nation’s current labor shortage, the estimate that 4M working age adults are no longer working because of long COVID equals about 40 percent of the 10M total job openings in August of this year, undoubtedly exacerbating ongoing economic challenges.

Employers face a brutal increase in health-insurance premiums for 2023, Axios’ Arielle Dreher writes from a Kaiser Family Foundation report out this morning.

Why it matters: Premiums stayed relatively flat this year, even as wages and inflation surged. That reprieve was because many 2022 premiums were finalized last fall, before inflation took off.

“Employers are already concerned about what they pay for health premiums,” KFF president and CEO Drew Altman said.

“[B]ut this could be the calm before the storm … Given the tight labor market and rising wages, it will be tough for employers to shift costs onto workers when costs spike.”

🧠 What’s happening: Nearly 159 million Americans get health coverage through work — and coverage costs and benefits have become a critical factor in a tight labor market.