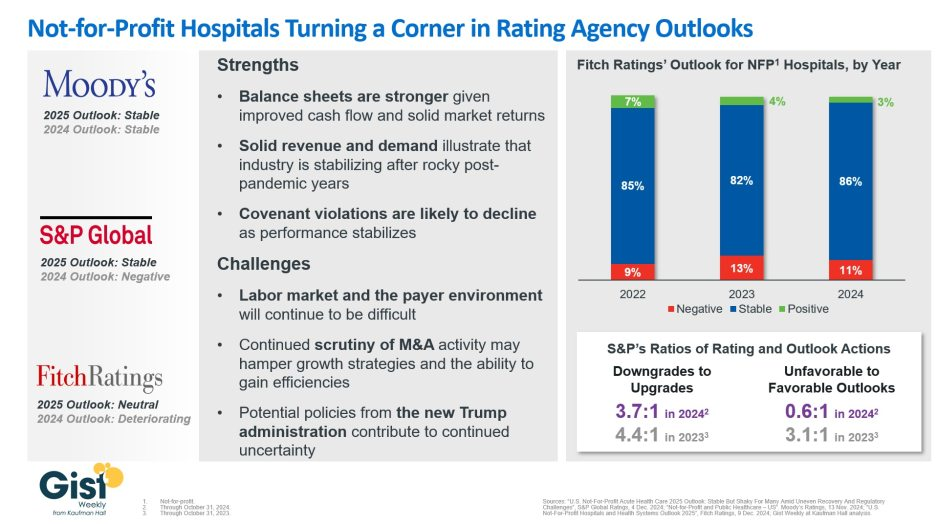

In late 2023, S&P Global and Fitch Ratings viewed the not-for-profit (NFP) hospital sector as negative or deteriorating, reflecting the difficult financial position many were in following the pandemic.

In recent weeks, S&P and Fitch upgraded their 2025 sector outlook for NFP hospitals to stable and neutral respectively, joining Moody’s Ratings, which held stable from last year.

This week’s graphic illustrates the rating agencies’ latest views on NFP hospitals, which point to a promising but uneven recovery for the industry.

Overall, the reports detail that stronger balance sheets, solid revenues, and improved demand have reduced the likelihood of covenant violations and strengthened NFP hospitals’ positions.

However, challenges persist that could impede further progress. The labor market, payer environment, antitrust enforcement, and a new administration all present complications for the continued recovery of NFP hospitals. Nonetheless, the reports indicate significant improvement for the industry since the post-pandemic ratings downturn.

Fitch’s report noted that the share of NFP hospitals with a stable outlook has reached a three-year high. Meanwhile, S&P reported that there are now almost twice as many NFP hospitals with favorable outlooks compared to unfavorable ones, a dramatic flip from 2023, which had a 3.1:1 ratio of unfavorable to favorable outlooks.

These ratings changes reflect the hard work put in by NFP hospitals across the country to improve their financial performance and find new ways to serve their communities sustainably.

However, the recovery remains “shaky” and incomplete, and hospitals still face a long road ahead as they reconfigure to a new normal.

Inflation, labor pressures, and general economic uncertainty have created significant financial strain for hospitals in the wake of the COVID pandemic. Compressed operating margins and weakened liquidity have left many hospitals in a precarious economic situation, with some entities deciding to delay or even cancel planned capital expenditures or capital raising. Given these tumultuous times, hospital entities could look to the realm of the higher education sector for a playbook on how to leverage non-core assets to unlock significant unrealized value and strengthen financial positions, in the form of public-private partnerships.

These structures, also known as P3s, involve collaborative agreements between public entities, like hospitals, and private sector partners who possess the expertise to unlock the value of non-core assets. A special purpose vehicle (SPV) is created, with the sole purpose of delivering the responsibilities outlined under the project agreement. The SPV is typically owned by equity members. The private sector would be responsible for raising debt to finance the project, which is secured by the obligations of the project agreement (and would be non-recourse to the hospital). Of note, the SPV undergoes the rating process, not the hospital entity. Even more importantly, the hospital retains ownership of the asset while benefiting from the expertise and resources of the private sector.

Hospitals can utilize P3s to capitalize on already-built assets, in what is known as a “brownfield” structure. A brownfield structure would typically result in an upfront payment to the hospital in exchange for the right of a private entity to operate the asset for an agreed-upon term. These upfront payments can range from tens of millions to hundreds of millions of dollars.

Alternatively, hospitals can engage in “greenfield” structures where the underlying asset is either not yet built or needs significant capital investment. Greenfield structures typically do not result in an upfront payment to the hospital entity. Instead, (in the example of a new build) private partners would typically design, build, finance, operate and maintain the asset. The hospital still retains ownership of the underlying asset at the completion of the agreed upon term.

P3 structures can be individually tailored to suit the unique needs of the hospital entity, and the resulting benefits are multifaceted. Financially, hospitals can increase liquidity, lower operating expenses, increase debt capacity, and create headroom for financial covenants. These partnerships provide a means to raise funds without directly accessing the capital markets or undergoing the rating process. Upfront payments represent unrestricted funds and can be used as the hospital entity sees fit to further its core mission. Operationally, infrastructure P3s offer hospitals the opportunity to address deferred maintenance needs, which may have accumulated over time. Immediate capital expenditure on infrastructure facilities can enhance reliability and efficiency and contribute to meeting carbon reduction or sustainability goals. Furthermore, these structures provide a means for the hospital to transfer a meaningful amount of risk to private partners via operation and maintenance agreements.

For years, various colleges and universities have adopted the P3 model, which is emerging as a viable solution for hospitals as well. Examples of recent structures in the higher education sector include:

Fresno State University, which partnered with Meridiam (an infrastructure private equity fund) and Noresco (a design builder) to deliver a new central utility plant. The 30-year agreement involved long-term routine and major maintenance obligations from the operator, with provisions for key performance indicators and performance deductions inserted to protect the university. Fresno State is not required to begin making availability payments until construction is completed.

The Ohio State University, which secured a $483 million upfront payment in exchange for the right of a private party to operate and maintain its parking infrastructure. The university used the influx of capital to hire key faculty members and to invest in their endowment.

The University of Toledo, which received an approximately $60 million upfront payment in exchange for a 35-year lease and concession agreement to a private operator. The private team will be responsible for operating and maintaining the university’s parking facilities throughout the term of the agreement.

Ultimately, healthcare entities can learn from the successful implementation of infrastructure P3 structures in the higher education sector. The experiences of Fresno State, The Ohio State University, and the University of Toledo (among others) serve as compelling examples of the transformative potential of P3s in the healthcare sector. By unlocking the true value of non-core assets through partnerships with the private sector, hospitals can reinforce their financial stability, meet sustainability goals, reduce risk, and shift valuable focus back to the core mission of providing high-quality healthcare services.

Author’s note: Implementing P3 structures requires careful consideration and expert guidance. Given the complex nature of these partnerships, hospitals can greatly benefit from the support of experienced advisors to navigate the intricacies of the process. KeyBank and Cain Brothers specialize in guiding entities through P3 initiatives, providing valuable expertise and insight. For additional information, please refer to a recording of our recent webinar and associated summary, which can be accessed here: https://www.key.com/businesses-institutions/business-expertise/articles/public-private-partnerships-can-unlock-hospitals-hiddenvalue.html

Not-for-profit hospitals and health systems rely on three interdependent functions to contribute to the financial resilience of the organization: namely, the ability to withstand adverse changes to these core functions and continue to provide services to the community (Figure above).

The Operating Function:

The Operating Function manages the portfolio of clinical services and strategic initiatives that define the charitable mission of the organization. Clinical services generate patient revenue, and if that revenue creates a positive margin (i.e., exceeds expenses), that excess is invested back into the health system. Operating margins are, on average, very low in not-for-profit healthcare. For example, for the not-for-profit hospitals and health systems rated by Moody’s Investors Service, median operating margins from 2017–2021 ranged between 2.1% and 2.9%. These rated organizations represent only a few hundred of the thousands of hospitals and health systems in the country and are among the most financially healthy. A 2018 study of a wider group of more than 2,800 hospitals found an average clinical operating margin of -2.7%.

The Finance Function:

Because the positive margins generated by the Operating Function are rarely enough to support the intensive capital needs of maintaining and improving acute-care facilities, care delivery models, and technology, not-for-profit health systems rely on the Finance Function for internal and external capital formation. The Finance Function builds cash reserves and secures external financing

(e.g., bond proceeds, bank lines of credit) to support the capital spending needs of the organization. The cash reserves maintained by the Finance Function also help the organization meet daily expenses at times when expenses exceed revenues.

The Investment Function:

Not-for-profit hospitals and health systems will also endeavor to invest some of their cash reserves to generate returns that, first, act as an additional hedge against potential risks that could disrupt operations or cash flow, and second, pursue independent returns. Any independent returns generated serve as an important supplement to revenues generated through the Operating Function.

The three functions described above are common to all not-for-profit organizations. The main differences are mostly within the Operating Function. In higher education, for example, tuition revenue takes the place of clinical revenue. While higher education also maintains enterprise risk, the Operating Function for colleges and universities is less vulnerable to volume swings as enrollment is typically steady and predictable. Likewise, higher education is less labor intensive than healthcare.

Financial reserves include all liquid cash resources and unrestricted investments held in the Finance and Investment Functions. These reserves are equivalent to the emergency funds individuals are encouraged to maintain to help them meet living expenses for six to twelve months in case of a job loss or other disruption to income.

Absolute reserve levels are important, as discussed above, but they must also be viewed relative to a hospital’s daily operating expenses. A common

metric used to describe these reserves is Days Cash on Hand. If an organization has 250 Days Cash on Hand, that means that it would be able to meet its operating expenses for 250 days if revenue was suddenly shut off. The size of Days Cash on Hand will be proportionate to the size of the hospital and health system. Some of the largest not-for-profit health systems have annual operating expenses approaching $30 billion annually: meeting those expenses for 250 days would require Days Cash on Hand of more than $20 billion.

The shutdown that occurred in the early days of the pandemic (March through May 2020) is an example of a time when cash flow nearly shut off for most hospitals (except for emergency care). Reserves, measured in absolute and relative terms such as Days Cash on Hand, allowed hospitals that were nearly empty to maintain staffing and operations throughout the period. Other hospitals that were inundated with patients during the initial surge were able to fund increased staffing and personal protective equipment costs through their reserves. Other examples of how reserves provide a buffer

against unexpected events include natural disasters such as hurricanes, tornadoes, deep freezes, and wildfires, which can require the temporary shutdown of operations; cyberattacks, which can halt a hospital’s ability to provide services; a defunct payer that is unable to reimburse hospitals for care already provided; or an escalation in labor costs as experienced by many during 2022.

Without the reserves to pay for contract labor or premium pay, many hospitals would have undoubtedly had to close or limit services to their community.

KEY TAKEAWAYS

Financial reserves are created through the interdependent relationship of operating, finance, and investment functions in not-for-profit health systems.

These reserves build financial resilience: the ability to withstand adverse changes to core functions and continue to provide services to the community.

Financial reserves play an important role in supplementing any shortfalls in revenue or capital formation in one or more of these three functions.

Financial reserves are equivalent to individual emergency funds—both are intended to cover expenses if income or revenue flows are significantly disrupted.

A common metric used to describe financial reserves is Days Cash on Hand: an organization’s combined liquid, unrestricted cash resources and investments, measured by how many days these reserves could cover operating expenses if cash flows were suddenly shut off.

Financial reserves, measured in absolute and relative terms such as Days Cash on Hand, allowed hospitals that were nearly empty during the early days of the pandemic to maintain staffing and operations throughout the period. Other hospitals that were inundated with patients during the initial surge were able to fund increased staffing and personal protective equipment costs through their reserves.

A Comparison: Financial Reserves and Higher Education Not-for-Profits

Not-for-profit hospitals and health systems are not alone in their reliance on financial reserves; most not-for-profit organizations carry reserves that enable them to maintain operations and make needed investments even in times of weaker operating performance. Higher education is probably most comparable to healthcare, with significant overlaps between the two sectors. Moody’s Investors Service, one of the three major rating agencies, notes that 16% of its rated higher education institutions have affiliated academic medical centers (AMCs), and revenue from patient care at these AMCs contributes to 28% of the overall revenues for the higher education sector.

The magnitude of Days Cash on Hand levels varies by industry; financial reserves maintained by private not-for-profit higher education

institutions, for example, are significantly greater than those maintained by not-for-profit hospitals and health systems. For comprehensive private universities across all rating categories, Moody’s reports median Days Cash on Hand in 2021 of 498 days for assets that could be liquidated within a year. This compares with a median 265 Days Cash on Hand in 2021 across all freestanding hospitals, single-state, and multi-state healthcare systems rated by Moody’s.

Financial reserves are a critical measure of financial health across both healthcare and higher education. They help ensure that not-for-profit colleges, universities, hospitals, and health systems can continue to fulfill their vital societal functions when operations are disrupted, or when they are experiencing a period of sustained financial distress.

Cash reserves, an important indicator of financial stability, are dropping for hospitals and health systems across the U.S.

Both large and small health systems are affected by rising labor and supply costs while reimbursement remains low. St. Louis-based Ascension reported days cash on hand dropped from 336 at the end of the 2021 fiscal year to 259 as of June 30, 2022, the end of the fiscal year. The system also reported accounts receivable increased three days from 47.3 in 2021 to 50.3 in 2022 because commercial payers were slow, especially in large dollar claims.

Trinity Health, based in Livonia, Mich., also reported days cash on hand dropped to 211 in fiscal year 2022, ending June 30, compared to 254 days at the end of 2021. Trinity attributed the 43-day decrease in cash on hand to “investment losses and the recoupment of the majority of the Medicare cash advances.”

Chicago-based CommonSpirit Health reported days cash on hand decreased by 69 days in the last year. The 140-hospital health system reported 245 days cash on hand at the 2021 fiscal year’s end June 30, and 176 days for 2022.

Lehigh Valley Health Network in Allentown, Pa., said unfavorable trends in the capital market led to investment losses and a drop in days cash on hand from 216 to 150 days in the 2022 fiscal year ending June 30. The health system also had a scheduled repayment of $191.1 million in advance Medicare dollars as well as $25 million in deferred payroll tax payments.

Philadelphia-based Thomas Jefferson Universityreported cash on hand for clinical operations dropped by 10.9 days in just the last quarter due to nonoperating investment losses and repaying government advances, which equaled about five days cash on hand. The health system reported 158.5 days cash on hand as of Sept. 30.

While the large health systems’ days cash on hand are dropping, they still have deep reserves. Smaller hospitals and health systems are in a more dire situation. Doylestown (Pa.) Hospital reported as of Sept. 30 the system had 81 days cash on hand, and Moody’s downgraded the hospital in June after the days cash on hand dropped below 100.

Kaweah Health in Visalia, Calif., saw reserves plummet since the pandemic began from 130 to 84 days cash on hand. Gary Herbst, CEO of Kaweah Health, blamed lost elective procedures, high labor costs, inflation and more for the system’s financial issues.

“The COVID-19 pandemic, and its aftermath, have brought District hospitals to the brink of financial collapse,” Mr. Herbst wrote in an open letter to Gov. Gavin Newsom published in the Visalia Times Delta. He asked Mr. Newsom to provide additional funding for public district hospitals. “Without your help, it will soon be virtually impossible for Medi-Cal patients to receive anything but emergency medical care in the State of California.”

The bill is coming due for federal loans given to hospitals early in the COVID-19 pandemic, adding to their financial woes, Oregon Public Broadcastingreported May 28.

The Medicare Accelerated and Advance Payment program offered hospitals short-term interest- free loans, according to the report. These loans are coming due as hospitals’ costs are rising quickly and revenue from patient stays and surgeries is growing more slowly.

The idea behind the program was that hospitals would be able to pay back the advance once the pandemic passed and operations returned to normal, according to the report. Hospitals are still dealing with the effects of the pandemic, but the federal government wants to recoup the money to keep Medicare funded.

In March 2021, HHS began recovering those cash advances by paying hospitals 25 percent less for Medicare reimbursement claims, according to the report. Earlier this year, HHS began paying hospitals 50 percent less for reimbursement claims.

Hospitals lobbied for the loans to be forgiven, but were unsuccessful, according to the report.

Kennett Square, Pa.-based Genesis Healthcare, one of the largest post-acute care providers in the U.S., warned that bankruptcy is possible if its financial losses continue.

“The virus continues to have a significant adverse impact on the company’s revenues and expenses, particularly in hard-hit Mid Atlantic and Northeastern markets,” Genesis CEO George V. Hager Jr., said in a Nov. 9 earnings release.

Mr. Hager said government stimulus funds the company received in the third quarter of this year fell nearly $60 million short of the company’s COVID-19 costs and lost revenue.

Genesis said it has taken several steps to help offset the financial damage linked to the pandemic, including delaying payment of a portion of payroll taxes incurred through December.

But the company warned that bankruptcy is possible if its financial losses continue.

“Even if the company receives additional funding support from government sources and/or is able to execute successfully all of its these plans and initiatives, given the unpredictable nature of, and the operating challenges presented by, the COVID-19 virus, the company’s operating plans and resulting cash flows, along with its cash and cash equivalents and other sources of liquidity. may not be sufficient to fund operations for the 12-month period following the date the financial statements are issued,” Genesis said. “Such events or circumstances could force the company to seek reorganization under the U.S. Bankruptcy Code.”

Genesis ended the third quarter of this year with a net loss of $62.8 million, compared to net income of $46.1 million in the same period a year earlier.

The financial challenges caused by the COVID-19 pandemic have forced hundreds of hospitals across the nation to furlough, lay off or reduce pay for workers, and others have had to scale back services or close.

Lower patient volumes, canceled elective procedures and higher expenses tied to the pandemic have created a cash crunch for hospitals. U.S. hospitals are estimated to lose more than $323 billion this year, according to a report from the American Hospital Association. The total includes $120.5 billion in financial losses the AHA predicts hospitals will see from July to December.

Hospitals are taking a number of steps to offset financial damage. Executives, clinicians and other staff are taking pay cuts, capital projects are being put on hold, and some employees are losing their jobs. More than 260 hospitals and health systems furloughed workers this year and dozens of others have implemented layoffs.

Below are 11 hospitals and health systems that announced layoffs since Sept. 1, most of which were attributed to financial strain caused by the pandemic.

1. NorthBay Healthcare, a nonprofit health system based in Fairfield, Calif., is laying off 31 of its 2,863 employees as part of its pandemic recovery plan, the system announced Nov. 2.

2. Minneapolis-based Children’s Minnesota is laying off 150 employees, or about 3 percent of its workforce. Children’s Minnesota cited several reasons for the layoffs, including the financial hit from the COVID-19 pandemic. Affected employees will end their employment either Dec. 31 or March 31.

3. Brattleboro Retreat, a psychiatric and addiction treatment hospital in Vermont, notified 85 employees in late October that they would be laid off within 60 days.

4. Citing a need to offset financial losses, Minneapolis-basedM Health Fairview said it plans to downsize its hospital and clinic operations. As a result of the changes, 900 employees, about 3 percent of its 34,000-person workforce, will be laid off.

5. Lake Charles (La.) Memorial Health Systemlaid off 205 workers, or about 8 percent of its workforce, as a result of damage sustained from Hurricane Laura. The health system laid off employees at Moss Memorial Health Clinic and the Archer Institute, two facilities in Lake Charles that sustained damage from the hurricane.

6. Burlington, Mass.-based Wellforce laid off 232 employees as a result of operating losses linked to the COVID-19 pandemic. The health system, comprising Tufts Medical Center, Lowell General Hospital and MelroseWakefield Healthcare,experienced a drastic drop in patient volume earlier this year due to the suspension of outpatient visits and elective surgeries. In the nine months ended June 30, the health system reported a $32.2 million operating loss.

7. Baptist Health Floyd in New Albany, Ind., part of Louisville, Ky.-based Baptist Health, eliminated 36 positions. The hospital said the cuts, which primarily affected administrative and nonclinical roles, are due to restructuring that is “necessary to meet financial challenges compounded by COVID-19.”

8. Cincinnati-based UC Health laid off about 100 employees. The job cuts affected both clinical and non-clinical staff. A spokesperson for the health system said no physicians were laid off.

9. Mercy Iowa City(Iowa) announced in September that it will lay off 29 employees to address financial strain tied to the COVID-19 pandemic.

10. Springfield, Ill.-based Memorial Health Systemlaid off 143 employees, or about 1.5 percent of the five-hospital system’s workforce. The health system cited financial pressures tied to the pandemic as the reason for the layoffs.

11. Watertown, N.Y.-based Samaritan Healthannounced Sept. 8 that it laid off 51 employees and will make other cost-cutting moves to offset financial stress tied to the COVID-19 pandemic.

Here are nine hospitals and health systems with strong operational metrics and solid financial positions, according to reports from Fitch Ratings, Moody’s Investors Service and S&P Global Ratings.

1. St. Louis-based Ascension has an “AA+” rating and stable outlook with Fitch. The system has a strong financial profile and a significant presence in several key markets, Fitch said. The credit rating agency expects Ascension will continue to produce healthy operating margins.

2. Phoenix-based Banner Health has an “AA-” rating and stable outlook with Fitch and S&P. Banner’s financial profile is strong, even taking into consideration the market volatility that occurred in the first quarter of this year, Fitch said. The credit rating agency expects the system to continue to improve operating margins and to generate cash flow sufficient to sustain strong key financial metrics.

3. Cincinnati-based Bon Secours Mercy Health has an “AA-” rating and stable outlook with Fitch. The health system has a good payer mix, a leading position in several of its markets and adequate margins to support its growth, Fitch said. The credit rating agency expects the system to maintain strong operating profitability.

4. Children’s Hospital of Philadelphia has an “Aa2” rating and stable outlook with Moody’s and an “AA” rating and stable outlook with S&P. The hospital has a strong market position and healthy liquidity, Moody’s said. The credit rating agency expects CHOP’s market position and brand equity will support its recovery from disruption caused by COVID-19.

5. Milwaukee-based Children’s Wisconsin has an “Aa3” rating and stable outlook with Moody’s and an “AA” rating and stable outlook with S&P. The health system has strong cash flow margins, Moody’s said. The credit rating agency expects the health system’s financial performance to remain solid, given its commanding market presence and demand for services.

6. Philadelphia-based Main Line Health has an “AA” rating and stable outlook with Fitch. The credit rating agency expects the system’s operations to recover after the COVID-19 pandemic and for it to resume its track record of strong operating cash flow margins.

7. Midland-based MidMichigan Health has an “AA-” rating and stable outlook with Fitch. The system has generated healthy operational levels through fiscal year 2020, and Fitch expects it to continue generating strong cash flow.

8. Columbus, Ohio-based Nationwide Children’s Hospital has an “Aa2” rating and stable outlook with Moody’s. The system has a strong market position in pediatric services in Columbus and the broad central Ohio region, and its advanced research capabilities will support volume recovery from disruption caused by COVID-19, Moody’s said. The credit rating agency expects Nationwide Children’s margins to remain strong and for cost management initiatives and volume recovery to drive improvements.

9. Chicago-based Northwestern Memorial HealthCare has an “Aa2” rating and stable outlook with Moody’s. The health system had strong pre-COVID margins and liquidity, Moody’s said. The credit rating agency expects the system to maintain strong operating cash flow margins.