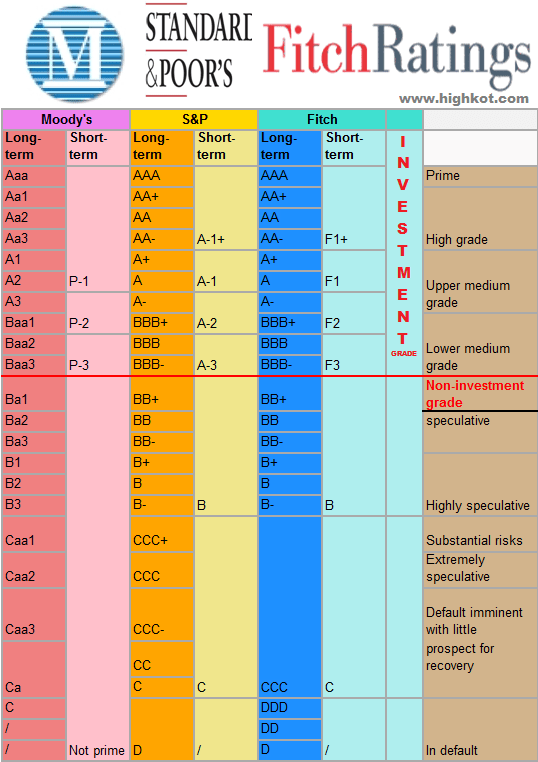

https://www.beckershospitalreview.com/finance/20-recent-hospital-health-system-outlook-and-credit-rating-actions.html?origin=cfoe&utm_source=cfoe

The following hospital and health system credit rating and outlook changes or affirmations occurred in the last two weeks, beginning with the most recent:

1. Fitch upgrades Cottage Health rating to ‘AA-‘

Fitch Ratings assigned an issuer default rating of “AA-” to Santa Barbara, Calif.-based Cottage Health and upgraded its revenue bond rating from “A+” to “AA-.”

2. Moody’s assigns ‘A1’ rating to Bexar County Hospital District

Moody’s Investors Service assigned an “A1” rating to Bexar County (Texas) Hospital District.

3. Moody’s confirms ‘Ba1’ ratings for Monroe County Health Authority

Moody’s Investors Service confirmed its “Ba1” issuer and general obligation limited tax ratings for Monroe County (Ala.) Health Care Authority.

4. Moody’s affirms ‘A3’ rating for The Christ Hospital

Moody’s Investors Service has affirmed its “A3” rating for Cincinnati-based The Christ Hospital, affecting $311 million of outstanding debt.

5. Moody’s assigns ‘Aa3’ rating to Partners Healthcare System

Moody’s Investors Service assigned an “A3” rating to Boston-based Partners Healthcare’s proposed revenue bonds.

6. Moody’s affirms ‘Aa2’ rating for Northwestern Memorial HealthCare

Moody’s Investors Service affirmed its “Aa2,” “Aa2/VMIG 1,” and “P-1” ratings for Chicago-based Northwestern Memorial HealthCare, affecting $1.1 billion of debt.

7. Moody’s affirms Yale New Haven Health’s ‘Aa3’ rating

Moody’s Investors Service affirmed the long-term underlying “Aa3” ratings of Yale New Haven (Conn.) Health, affecting $715 million of rated debt.

8. Moody’s assigns ‘A2’ rating to Kettering Health Network

Moody’s Investors Service assigned an “A2” rating to Dayton, Ohio-based Kettering Health Network.

9. S&P assigns ‘A+’ rating to Indiana’s Marion General Hospital

S&P Global Ratings assigned an “A+” long-term rating to Marion (Ind.) General Hospital.

10. Moody’s affirms ‘Ba3’ rating for Antelope Valley Healthcare District

Moody’s Investors Service affirmed its “Ba3” rating for Lancaster, Calif.-based Antelope Valley Health District, which includes Antelope Valley Hospital, affecting $122 million of revenue bonds.

11. Moody’s affirms ‘Ba2’ rating for Community Memorial Health System

Moody’s Investors Service affirmed Ventura, Calif.-based Community Memorial Health System’s “Ba2” rating, affecting $339 million of rated debt.

12. Moody’s affirms ‘A2’ rating for University of Maryland Medical System

Moody’s Investors Service affirmed its “A2” rating for the Baltimore-based University of Maryland Medical System, affecting $1.1 billion of outstanding debt.

13. Moody’s affirms ‘B1’ rating for Sauk Prairie Healthcare

Moody’s Investors Service affirmed its “B1” rating for Sauk Prairie Healthcare in Prairie du Sac, Wis., affecting $38 million of fixed rate bonds.

14. Moody’s affirms ‘A3’ rating for Excela Health

Moody’s Investors Service affirmed Greensburg, Pa.-based Excela Health’s “A3” rating, affecting $72 million of outstanding debt.

15. Moody’s affirms Northwest Community Hospital’s ‘A2’ rating

Moody’s Investors Service affirmed its “A2” rating for Arlington Heights, Ill.-based Northwest Community Hospital, affecting $194 million of rated debt.

16. Fitch assigns ‘AA-‘ long-term rating to Trinity Health

Fitch Ratings assigned an “AA-” long-term rating to Livonia, Mich.-based Trinity Health, affecting $175 million of bonds.

17. Fitch withdraws rating for Greenwich Hospital

Fitch Ratings has withdrawn its issuer default rating for Greenwich (Conn.) Hospital.

18. Fitch assigns ‘A’ rating to East Tennessee Children’s Hospital

Fitch Ratings has assigned an “A” rating and an “A” issuer default rating to Knoxville-based East Tennessee Children’s Hospital.

19. Moody’s affirms ‘A1’ rating for Lexington County Health Services District

Moody’s Investors Service affirmed its “A1” rating for Lexington County (S.C.) Health Services District, affecting $369 million of outstanding revenue bonds.

20. Moody’s assigns ‘A1’ rating to Munson Healthcare

Moody’s Investors Service assigned an “A1” long-term rating to the proposed revenue refunding bonds for Traverse City, Mich.-based Munson Healthcare while also maintaining an “A1” rating on the system’s existing debt.